Alpesh Final

69

Management Thesis 2010 BHAVNAGAR Prepared By: Faculty Guide: Alpesh Lathia Mrs. Gutam Majumdar

-

Upload

jimmy-sachde -

Category

Documents

-

view

222 -

download

0

Transcript of Alpesh Final

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 1/69

Management Thesis 2010

BHAVNAGAR

Prepared By: Faculty Guide:

Alpesh Lathia Mrs. GutamMajumdar

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 2/69

M ar .2

27

Final Thesis

8NBBG010

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 3/69

M ar .2

27

Final Thesis

A

THESIS

ON

“ A competitive of study on consumer investor

behaviors with reference to TATA Mutual Fund

and HDFC Mutual Fund ”

Prepared By:

ALPESH LATHIA

8NBBG010

A report submitted in partial fulfillment of the requirements of

THE MBA PROGRAM

(The Class of 2008-10)

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 4/69

M ar .2

27

Final Thesis

Preface

Management thesis provides an opportunity to the MBA students to

apply their theoritical and practical concepts, which they have been studying in the

business school to the practicle world. As we all know that practicle world is far

different than the theoritical, every MBA student is required to acquire both

theoritical as well as practicle knowledge in order to survive the increasing

competition in the field of management. The period of management thesis is very

important for a student, as he has to work in the market for the thesis and he has to

do some survey for finding actual production position in the market.

As my area of interst from beginning is Finance and retail, I was

interested, to undergo my Management Topic-II in some prestigious financial

institution.

At present mutual fund is doing very well in India. It has given a safe

option to the investors when the bank and other institutions are loosing faith

amongst the people. Many companies having realised mutual fund sector provides

the market potential and opportunity for growth this has given more employment

opportunity in this sector, which is deadly required by Indian Economy.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 5/69

M ar .2

27

Final Thesis

Table Of Content

1. Acknowledgement 05

2. Review of Literature 06

3. Objective of the Study 07

4. Research Methodology 08

5. Limitation of the Study 10

6. Introduction 11

7. Industry Profile 13

8. History & Background 18

9. Drawbacks of Investing in Mutual Funds 25

10. A big Mutual Fund Industry today 29

11. Process of Mutual Fund 35

12. Investment Avenues Preferred 37

13. Facts for the growth of Mutual Funds 38

14. TATA Mutual Fund 40

15. HDFC Mutual Fund 43

16. Empirical Analysis 46

17. Findings & Suggestions 55

18. Conclusion 59

19. Appendix 64

20. References 66

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 6/69

M ar .2

27

Final Thesis

Acknowledgement

I have the opportunity to express my sincere gratitude towrds all

the people who have helped me in the successful completion of my half

management thesis.

I feel glad to put this Management Thesis Report as a part of

submission of subject “Management Thesis-II” of MBA with present era of

Mutual Fund.

I am greatly thankful to our respected Campus Head Mr.

Gautam Majumdar who has given me an opportunity to express my views

for this topic. I appreciate the efforts, guidance and inspiration of my Faculty

Supervisor Mr. Gutam Majumdar who leads me to the proper rules and

regulations regarding the thesis. She helped me to search and refine title on

this topic successfully.

Only because of the above efforts, advise and co-operations of

our respected faculty members, I can reach to the last mark.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 7/69

M ar .2

27

Final Thesis

Review Of Literature

♦ Global Mutual Fund Author: Prof. John Bang

♦ Mutual fund Author: Dr. Admon mrSatin

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 8/69

M ar .2

27

Final Thesis

Objectives Of The Study

In order to examine the issues rose above, this survey has the following

objectives before it:

1) To understand the savings avenue preference among MF investors

2) To identify the features the investors look for in Mutual Fund products.

3) To identify the schemes preference of investors.

4) To identify the factors that influencing the investor’s fund/schemeselection.

5) To identify the information sources influencing the scheme selectiondecision.

6) To identify the preferred communication mode.

IMPORTANCE AND BENEFITS :

Though many MF are giving nearly 100% returns in a year, only 2% of total

population has invested in MF. The research would help to understand the

reasons why people invest less in MF. This research would help AMCs to

understand what steps can be taken to increase the investment in MF.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 9/69

M ar .2

27

Final Thesis

Resarch Methodology

HYPOTHESIS:

Investors still prefer investment in safety instrument then mutual

fund and shares. And because of this mutual fund investment in market is

only 4%.

RESEARCH OBJECTIVE

To study

• Investment pattern of investors.

• Key factors to be considered before investing.

• Mutual funds scope and acceptance of mutual funds of HDFC or

TATA..

TYPE OF SURVEY

The questionnaire based survey is selected for conducting the

research. The questionnaire based survey is selected because it is the most

effective and efficient way to conduct research of investors investing in

mutual fund since they just have to give their opinion for the question asked

by the researcher and also they can just select from the alternatives given in

the questionnaire.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 10/69

M ar .2

27

Final Thesis

SAMPLING

Simple Random Sampling

For the study the sampling technique used is that of Simple

random Sampling in this every people has equal chance of selection.

SAMPLE SIZE

The population defined for the study is any investor and into any

kind of investment. The population defined would give inferences. So the

population is divided here in different classes. All the professionals, service,

businessmen and would include any person who make any kind of

investment became my population. The sample size is approximately size is

kept 100 randomly.

TYPE OF QUESTIONNAIRE

The questionnaire designed contained

Dichotomous questions

Multiple-choice questions

Thus it was easy for the investors to select from the alternatives, the

alternative which suits them the best. The data or the data the information

collected from the respondents were the respondents were then compiled,

tabulated and classified for analysis and interpretation with the use of

Microsoft Excel, Microsoft Word etc.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 11/69

M ar .2

27

Final Thesis

Limitation Of The Study

1. Sample size is limited to 150 educated investors in Bhavnagar only.The sample size may not adequately represent the National market.

2. This study has not been conducted over an extended period of the time

having both market ups and downs. The market state has significance

influence on the buying patterns and preferences of investors. For

example, the July 2001 fall has sent violent shock waves across the

MF investor community and is bound to influence the scheme

preference/ selection of the investors. The study has not captured such

situations.

3. We have to depend on a small sample size of investors to find out the

results of the study which may become biased and this sample might

be small to gather an in depth knowledge of MF.

4. Investor’s behavior is affected by various factors and in a short span of

time it is not possible to study all this factors.

5. It may not be possible to take proportional sample size from each area.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 12/69

M ar .2

27

Final Thesis

Introduction

BACKGROUND &NEED FOR THE STUDY

It is widely believed that MF is a retail product designed to target

small investors, salaried people and others who are intimidated by the stock

market but nevertheless, like to reap the benefits of stock market investing.

At the retail level, investors are unique and are a highly heterogeneous

group. Hence, designing a general product and expecting a good response

will be futile, through UTI could do this nearly for three decades (1964-

1987) due to its monopoly in the industry. In the second phase of

oligopolistic competition (1987-1992), the public sector banks and financial

institutions entered the field, but with the then existing boom condition, it

was a smooth sailing for the industry. Further, the globalization and

liberalization measures announced by the government led to a paradigm shift

in the mindset of investors and the capital market environment become more

unfriendly to retail investors. They had no other choice but to turn to MFs to

reap the benefits of stock market investing. Hence, the need to be innovative

in designing the product was not felt and investors had to choose from the

limited schemes offered. During the third phase (1992 hence) the industry

was thrown open to the private sector and the stage got set for competition.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 13/69

M ar .2

27

Final Thesis

Currently there are more than 477 schemes with varied

objectives and 33 AMCs compete against one another by launching new

products or repositioning old ones. Now Mutual Fund industry is facing

competition not only from within the industry but also from other financial

products that may provide many of the same economic functions, as MFs but

are not strictly MFs. For example, in US, one saving institution has patented

a product that promises to deliver consumers a pay off indexed to college

tuition costs, thus attempting to meet a common consumer requirement. This

product is structured as a certificate of deposit, but it could have been set up

as a Mutual Fund. Such products will shortly appear in the Indian market

also. Other examples could be ULIP plans which are giving a good

competition to MFs. All this, in aggregate, heightens the consumer confusion

in his selection of the product.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 14/69

M ar .2

27

Final Thesis

Industry Profile

WHAT EXACTLY MUTUAL FUND IS?

A Mutual Fund is a trust that pools the savings of a number of

investors who share a common financial goal. The money thus collected is

then invested in capital market instruments such as shares, debentures and

other securities. The income earned through these investments and the

capital appreciations realized are shared by its unit holders in proportion to

the number of units owned by them. Thus a Mutual Fund is the most suitable

investment for the common man as it offers an opportunity to invest in a

diversified, professionally managed basket of securities at a relatively low

cost. The flow chart below describes broadly the working of a mutual fund.

The Situation could vary as per age groups, mindsets and risk

taking ability, but the solution, in each case wants money to grow. Most of

the investors don’t have sufficient knowledge about different investment

options, financial instrument’s nature, market information, analytical skills

and therefore their funds are lacking proper management and diversification

to get market-linked return with flexibility as well as liquidity. These kinds

of investors should prefer mutual funds to channelize their funds properly.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 15/69

M ar .2

27

Final Thesis

A security that gives small investors access to a well-diversified

portfolio of equities, bonds and other securities. Each shareholder

participates in the gain or loss of the fund. Shares are issued and can be

redeemed as needed.

Mutual Funds are the unique instrument that offers an

individual professional management, diversification, flexibility, liquidity

and a chance to get market linked returns. Mutual funds are indeed the best

tool for wealth creation. Whatever other instruments can do, mutual funds

can do too – and more efficiently.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 16/69

M ar .2

27

Final Thesis

Mutual Fund Industry

Alone UTI with just one scheme in 1964 now competes with as

many as 400 odd products and 34 players in the market. In spite of the stiff

competition and losing market share, UTI still remains a formidable force to

reckon with.

Last six years have been the most turbulent as well as exiting

ones for the industry. New players have come in, while others have decidedto close shop by either selling off or merging with others. Product innovation

is now passé with the game shifting to performance delivery in fund

management as well as service. Those directly associated with the fund

management industry like distributors, registrars and transfer agents, and

even the regulators have become more mature and responsible.

The industry is also having a profound impact on financial

markets. While UTI has always been a dominant player on the bourses as

well as the debt markets, the new generations of private funds which have

gained substantial mass are now seen flexing their muscles. Fund managers,

by their selection criteria for stocks have forced corporate governance on the

industry. By rewarding honest and transparent management with higher

valuations, a system of risk-reward has been created where the corporate

sector is more transparent then before.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 17/69

M ar .2

27

Final Thesis

Funds have shifted their focus to the recession free sectors like

pharmaceuticals, FMCG and technology sector. Funds performances are

improving. Funds collection, which averaged at less than Rs100bn per

annum over five-year period spanning 1993-98 doubled to Rs210bn in 1998-

99. In the current year mobilization till now have exceeded Rs300bn. Total

collection for the current financial year ending March 2000 is expected to

reach Rs450bn.

What is particularly noteworthy is that bulk of the mobilization

has been by the private sector mutual funds rather than public sector mutual

funds. Indeed private MFs saw a net inflow of Rs. 7819.34 crore during the

first nine months of the year as against a net inflow of Rs.604.40 crore in the

case of public sector funds.

Mutual funds are now also competing with commercial banks in

the race for retail investor’s savings and corporate float money. The power

shift towards mutual funds has become obvious. The coming few years will

show that the traditional saving avenues are losing out in the current

scenario. Many investors are realizing that investments in savings accounts

are as good as locking up their deposits in a closet. The fund mobilization

trend by mutual funds in the current year indicates that money is going to

mutual funds in a big way. The collection in the first half of the financial

year 1999-2000 matches the whole of 1998-99.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 18/69

M ar .2

27

Final Thesis

India is at the first stage of a revolution that has already peaked

in the U.S. The U.S. boasts of an Asset base that is much higher than its bank

deposits. In India, mutual fund assets are not even 10% of the bank deposits,

but this trend is beginning to change. Recent figures indicate that in the first

quarter of the current fiscal year mutual fund assets went up by 115%

whereas bank deposits rose by only 17%. (Source: Think-tank, the Financial

Express September 99) This is forcing a large number of banks to adopt the

concept of narrow banking wherein the deposits are kept in Gilts and some

other assets, which improves liquidity and reduces risk. The basic fact lies

that banks cannot be ignored and they will not close down completely. Their

role as intermediaries cannot be ignored. It is just that Mutual Funds are

going to change the way banks do business in the future.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 19/69

M ar .2

27

Final Thesis

History & Background

Four Phases of Mutual Fund in India

The mutual fund industry can be broadly put into four phases according to the

development of the sector. Each phase is briefly described as under.

►First Phase - 1964-87

An Act of Parliament established Unit Trust of India (UTI) on 1963. It was set up

by the Reserve Bank of India and functioned under the Regulatory and

administrative control of the Reserve Bank of India. In 1978 UTI was de-linked

from the RBI and the Industrial Development Bank of India (IDBI) took over the

regulatory and administrative control in place of RBI. The first scheme launched

by UTI was Unit Scheme 1964. At the end of 1988 UTI had Rs.6, 700 crores of

assets under management.

►Second Phase - 1987-1993 (Entry of Public Sector Funds)

Entry of non-UTI mutual funds. SBI Mutual Fund was the first followed byCanbank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89),

Indian Bank Mutual Fund (Nov 89), Bank of India (Jun 90), Bank of Baroda

Mutual Fund (Oct 92). LIC in 1989 and GIC in 1990. The end of 1993 marked

Rs.47, 004 as assets under management.

►Third Phase - 1993-2003 (Entry of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian

mutual fund industry, giving the Indian investors a wider choice of fund families.

Also, 1993 was the year in which the first Mutual Fund Regulations came into

being, under which all mutual funds, except UTI were to be registered and

governed. The erstwhile Kothari Pioneer (now merged with Franklin Templeton)

was the first private sector mutual fund registered in July 1993.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 20/69

M ar .2

27

Final Thesis

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more

comprehensive and revised Mutual Fund Regulations in 1996. The industry now

functions under the SEBI (Mutual Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual

funds setting up funds in India and also the industry has witnessed several mergers

and acquisitions. As at the end of January 2003, there were 33 mutual funds with

total assets of Rs. 1, 21,805 crores. The Unit Trust of India with Rs.44, 541 crores

of assets under management was way ahead of other mutual funds.

►Fourth Phase - since February 2003

This phase had bitter experience for UTI. It was bifurcated into two separate

entities. One is the Specified Undertaking of the Unit Trust of India with AUM of Rs.29, 835 crores (as on January 2003). The Specified Undertaking of Unit Trust

of India, functioning under an administrator and under the rules framed by

Government of India and does not come under the purview of the Mutual Fund

Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC.

It is registered with SEBI and functions under the Mutual Fund Regulations. With

the bifurcation of the erstwhile UTI which had in March 2000 more than Rs.76,

000 crores of AUM and with the setting up of a UTI Mutual Fund, conforming to

the SEBI Mutual Fund Regulations, and with recent mergers taking place among

different private sector funds, the mutual fund industry has entered its current

phase of consolidation and growth. As at the end of September, 2004, there were

29 funds, which manage assets of Rs.153108 crores under 421 schemes.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 21/69

M ar .2

27

Final Thesis

Growth in assets under management

MUTUAL FUND – A GLOBALLY PROVEN INVESTMENT

Worldwide, the Mutual Fund, or Unit Trust as it is called in some parts of the

world, has long and successful history. The popularity of the Mutual Fund has

increased manifold. In developed financial markets, like the United States, Mutual

Funds have almost overtaken bank deposits and total assets of insurance funds.

1. As at the end of December 1999, in the US alone there were 7,791 MutualFunds with total assets of over US $ 6.8 Trillion (296 Lac Crores).

2. Out of the top 10 mutual funds worldwide, eight are bank sponsored. OnlyFidelity and Capital are non-bank mutual funds in the group

3. In US about 9.7 million households are managing their assets on-line, sucha facility is not yet available in India.

4. On-line trading is a great idea to reduce management expenses from thecurrent 2% of total assets to about 0.75% of the total assets.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 22/69

M ar .2

27

Final Thesis

Internationally, on-line investing continues its meteoric rise. Many have debated

about the success of e-commerce and its breakthroughs, but it is true that this

aspect of technology could and will change the way financial sectors function.

However, mutual funds cannot be left far behind. In fact advanced countries like

US, mutual funds buy-sell transactions have already begun on the net, while inIndia the net is used as a source of information. Such changes could facilitate easy

access, lower intermediation costs and better services for all. A research agency

that specializes in Internet technology estimates that over the next four to five

years mutual fund assets trading will grow by ten folds, where equity trading will

increase during the period by seven to eight folds. This will increase the share of

mutual funds from 34% to 40% during the period.

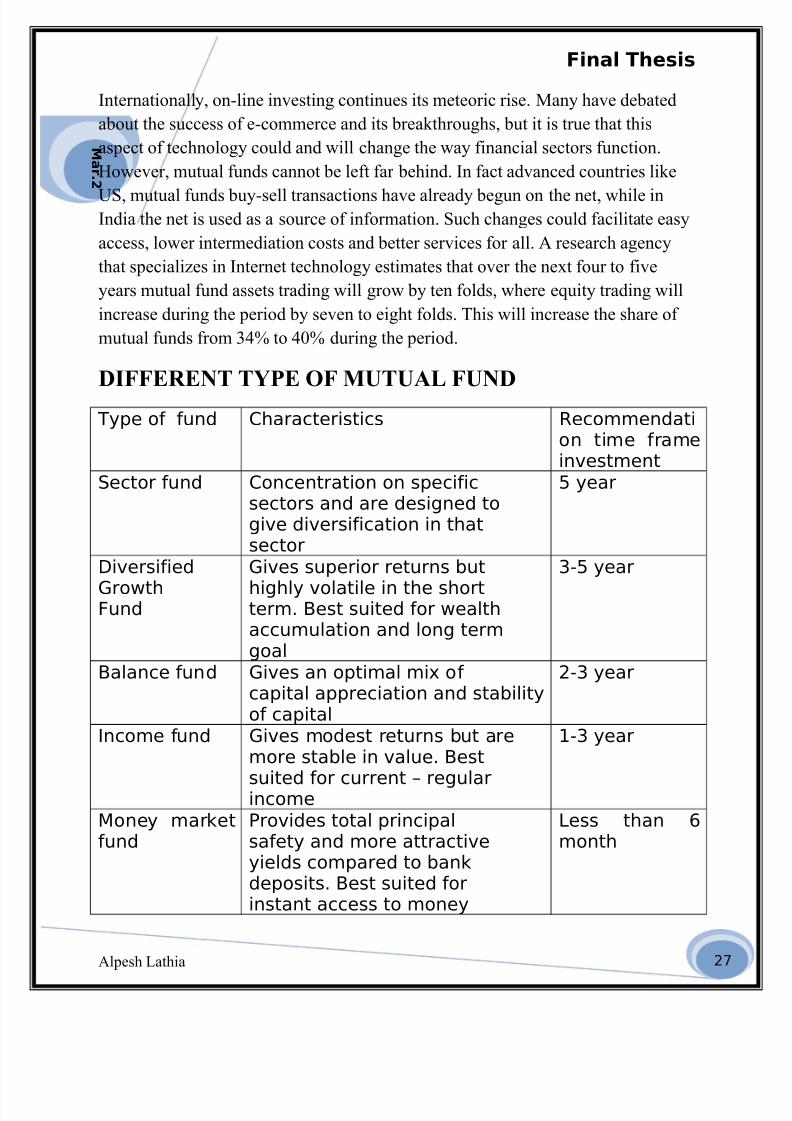

DIFFERENT TYPE OF MUTUAL FUND

Type of fund Characteristics Recommendation time frameinvestment

Sector fund Concentration on specificsectors and are designed togive diversification in thatsector

5 year

Diversified

GrowthFund

Gives superior returns but

highly volatile in the shortterm. Best suited for wealthaccumulation and long termgoal

3-5 year

Balance fund Gives an optimal mix of capital appreciation and stabilityof capital

2-3 year

Income fund Gives modest returns but aremore stable in value. Best

suited for current – regularincome

1-3 year

Money marketfund

Provides total principalsafety and more attractiveyields compared to bankdeposits. Best suited forinstant access to money

Less than 6month

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 23/69

M ar .2

27

Final Thesis

MUTUAL FUNDS FOR WHOM AND WHY?

►For whom

Mutual Funds target the small investors. Most schemes keep their minimum

investment at Rs. 1000-5000. For an affordable amount such as this, investors get

lots more through a mutual fund than what would ever manage on own. e.g. on 22

April 2004, for instance, one share of Infosys alone cost Rs. 5400, one share of

Wipro Rs. 1600. If an investor wanted to invest Rs. 5400 he would get only one

stock of Infosys while investing the same amount in mutual fund he would get

more numbers of diversified stocks. These funds can survive and thrive only if

they can live up to the hopes and trusts of their individual members. These hopes

and trusts echo the peculiarities, which support the emergence and growth of such

in rescue of such investors who come to the rescue of such investors who face

following constraints while making direct investments:

1. Limited resources in the hands of investors quite often take them awayfrom stock market transactions.

2. Lack of funds forbids investors to have a balanced and diversified portfolio.3. Lack of professional knowledge associated with investment business unable

investors to operate gainfully in the market. Small investors can hardlyafford to have expensive investment consultations.

4. To buy shares, investors have to engage share brokers who are the membersof stock exchange and have to pay their brokerage.

5. They hardly have access to price sensitive information in time.6. It is difficult for them to know the development taking place in share market

and corporate sector.7. Firm allotments are not possible for small investors on when there is a trend

of over subscription to public issues.

► WHY?

Mutual Funds are becoming a very popular form of investment characterized by

many advantages that they share with other forms of investment characterized by

many advantages that they share with other forms of investments and what they

possess uniquely themselves. The primary objectives of an investment proposal

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 24/69

M ar .2

27

Final Thesis

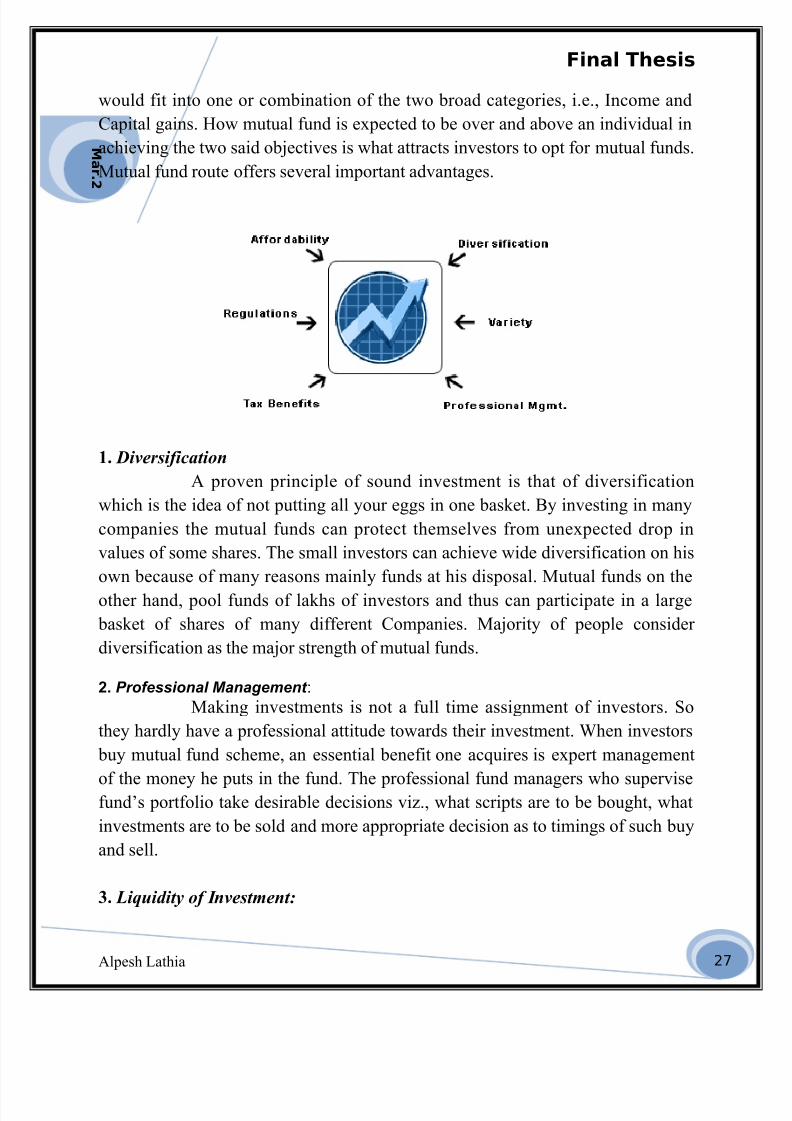

would fit into one or combination of the two broad categories, i.e., Income and

Capital gains. How mutual fund is expected to be over and above an individual in

achieving the two said objectives is what attracts investors to opt for mutual funds.

Mutual fund route offers several important advantages.

1. Diversification

A proven principle of sound investment is that of diversification

which is the idea of not putting all your eggs in one basket. By investing in many

companies the mutual funds can protect themselves from unexpected drop in

values of some shares. The small investors can achieve wide diversification on his

own because of many reasons mainly funds at his disposal. Mutual funds on the

other hand, pool funds of lakhs of investors and thus can participate in a large

basket of shares of many different Companies. Majority of people consider

diversification as the major strength of mutual funds.

2. Professional Management :

Making investments is not a full time assignment of investors. So

they hardly have a professional attitude towards their investment. When investors

buy mutual fund scheme, an essential benefit one acquires is expert management

of the money he puts in the fund. The professional fund managers who supervisefund’s portfolio take desirable decisions viz., what scripts are to be bought, what

investments are to be sold and more appropriate decision as to timings of such buy

and sell.

3. Liquidity of Investment:

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 25/69

M ar .2

27

Final Thesis

A distinct advantage of a mutual fund over other investments is that

there is always a market for its unit/ shares. Moreover, Securities and Exchange

Board of India (SEBI)requires the mutual funds in India have to ensure liquidity.

Mutual funds units can either be sold in the share market as SEBI has made it

obligatory for closed-ended schemes to list themselves on stock exchanges. For open-ended schemes investors can always approach the fund for repurchase at net

asset value (NAV) of the scheme. Such repurchase price and NAV is advertised in

newspaper for the convenience of investor.

4. Convenient Administration:

Investing in a Mutual Fund reduces paperwork and helps you avoid

many problems such as bad deliveries, delayed payments and unnecessary follow

up with brokers and companies. Mutual Funds save time and make investing easyand convenient.

5. Transparency:

Regular information on the value of investment in addition to

disclosure on the specific investments made by investors, the proportion invested

in each class of assets and the fund manager’s investment strategy and outlook is

provided on regular basis by different fund houses.

6. Flexibility:

Through features such as regular investment plans, regular

withdrawal plans and dividend reinvestment plans, investors can systematically

invest or withdraw funds according to investors’ needs and conveniences.

7. Reduced risks:

Risk in investment is as to recovery of the principal amount and as to

return on it. Mutual fund investments on both fronts provide a comfortable

situation for investors. The expert supervision, diversification and liquidity of

units ensured in mutual funds minimize the risks. Investors are no longer expected

to come to grief by falling prey to misleading and motivating ‘headline’ leads and

tips, if they invest in mutual funds.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 26/69

M ar .2

27

Final Thesis

8. Safety of Investment:

Besides depending on the expert supervision of fund managers, the

legislation in a country (like SEBI in India) also provides for the safety of

investments. Mutual funds have to broadly follow the laid down provisions for

their regulations, SEBI acts as a watchdog and attempts whole-heartedly tosafeguard investor’s interests.

9. Tax Shelter:

Depending on the scheme of mutual funds, tax shelter is also

available. As per the union budget-99, income earned through dividends from

mutual funds is 100% tax free to investors.

10. Well Regulated:All Mutual Funds are registered with SEBI and they function within

the provisions of strict relations designed to protect the interests of investors. The

operations of Mutual Funds are regularly monitored by SEBI.

11. Minimize Operating Costs:

Mutual funds having large investible funds at their disposal avail

economies of scale. The brokerage fee or trading commission may be reduced

substantially. The reduced operating cost obviously increases the income available

for investors. Investing in securities through mutual funds has many advantages

like – option to reinvest dividends, strong possibility of capital appreciation,

regular returns, etc.

DRAWBACKS OF INVESTING IN MUTUAL FUNDS

Potential loss

Unlike a bank deposit, the investment in a mutual fund could fall in

value, as the fund is nothing but a portfolio of different securities. Apart from a

few assured returns schemes, the fund does not guarantee any minimum

percentage of return.

The Diversification Penalty

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 27/69

M ar .2

27

Final Thesis

While diversification reduces the risk of loss from holding a single

security, it also limits the larger gains if a single security increases dramatically in

value. Also, diversification does not protect the unit holders totally from an overall

decline in the market. No tailor made portfolio Mutual fund portfolios are created

and marked by AMCs, in to which investors invest. They cannot made tailor made portfolio

CLASSIFICATION OF MUTUAL FUND SCHEMES

Any mutual fund has an objective of earning income for investors and/ or

getting increased value of their investments. To achieve these objectives mutual

funds adopt different strategies and accordingly offer different schemes of

investments. On this basis the simplest way to categories schemes would be to

group these into two broad,

►Operational classification:

Highlights the two main types of schemes, i.e., open-ended and close-ended which

are offered by the mutual funds.

►Portfolio classification:

Projects the combination of investment instruments and Investment avenues

available to mutual funds to manage their funds. Any portfolio scheme can be

either open ended or close ended.

A. OPERATIONAL CLASSIFICATION

(a) Open Ended Schemes:

As the name implies the size of the scheme (Fund) is open – i.e.,not specified or predetermined. Entry to the fund is always open

to the investor who can subscribe at any time. Such fund stands

ready to buy or sell its securities at any time. It implies that the

capitalization of the fund is constantly changing as investors sell

or buy their shares. Further, the shares or units are normally not

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 28/69

M ar .2

27

Final Thesis

traded on the stock exchange but are €comparatively Better

liquidity despite the fact that these are not listed. The reason is

that investor can Any time approach mutual fund for sale of

such units. No intermediaries are required Moreover, the

realizable amount is certain since repurchase is at a price basedon declared net asset value (NAV). No minute to minute

fluctuations in rates haunt the Investors. The portfolio mix of

such schemes has to be investments, which are actively traded

in the market. Otherwise, it will not be possible to calculate

NAV. This is the reason that generally open-ended schemes are

equity based. Moreover, desiring frequently traded securities,

open-ended schemes hardly have in their portfolio shares of

comparatively new and smaller companies since these are notgenerally traded. In such funds, option to reinvest its dividend is

also available. Since there is always a possibility of

withdrawals, the management of such funds becomes more

tedious as managers have to work from crisis to crisis. Crisis

may be on two fronts, one is, that unexpected withdrawals

require funds to maintain a high level of cash available every

time implying thereby idle cash. Fund managers have to face

questions like ‘ what to sell’. He could very well have to sell his

most liquid assets. Second, by virtue of this situation such funds

may fail to grab favorable opportunities. Further, to match quick

cash payments, funds cannot have matching realization from

their portfolio due to intricacies of the stock market. Thus,

success of the open-ended schemes to a great extent depends on

the efficiency of the capital

(b) Close Ended Schemes:

Such schemes have a definite period after which their shares/units are redeemed. Unlike open-ended funds, these funds have

fixed capitalisation, i.e., their corpus normally does not change

throughout its life period. Close ended fund units trade among

the investors in the secondary market since these are to be

quoted on the stock exchanges. Their price is determined on the

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 29/69

M ar .2

27

Final Thesis

basis of demand and supply in the market. Their liquidity

depends on the efficiency and understanding of the engaged

broker. Their price is free to deviate from NAV, i.e., there is

every possibility that the market price may be above or below

its NAV. If one takes into account the issue expenses,conceptually close ended fund units cannot be traded at a

premium or over NAV because the price of a package of

investments, i.e., cannot exceed the sum of the prices of the

investments constituting the package. Whatever premium exists

that may exist only on account of speculative activities. In India

as per SEBI (MF) Regulations every mutual fund is free to

launch any or both types of schemes.

B. PORTFOLIO CLASSIFICATION OF FUNDS:

Following are the portfolio classification of funds, which may

be offered. This classification may be on the basis of (a) Return,

(b) Investment Pattern, (c) Specialized sector of investment, (d)

Leverage and (e) Others.

Alpesh Lathia

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 30/69

66

(a) Return Based Classification:

To meet the diversified needs of the investors, the mutual fund schemes are

made to enjoy a good return. Returns expected are in form of regular dividends

or capital

appreciation or a combination of these two.

# Income Funds:

For investors who are more curious for returns, Income funds are floated. Their

objective is to maximize current income. Such funds distribute periodically the

income earned by them. These funds can further be splitters up into categories

those that stress constant income at relatively low risk and those that attempt to

achieve maximum income possible, even with the use of leverage. Obviously,

the higher the expected returns, the higher the potential risk of the investment.

# Growth Funds:

Such funds aim to achieve increase in the value of the underlying investments

through capital appreciation. Such funds invest in growth oriented securities

which can appreciate through the expansion production facilities in long

run?.An investor who selects such funds should be able to assume a higher than

normal degree of risk.

# Conservative Funds:

The fund with a philosophy of “ all things to all” issue offer document

announcing

objectives as: (i) To provide a reasonable rate of return, (ii) To protect the value

of investment and, (iii) To achieve capital appreciation consistent with the

fulfillment of the first two objectives. Such funds which offer a blend of

immediate average return and reasonable capital appreciation are known as

“Conservative fund”.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 31/69

66

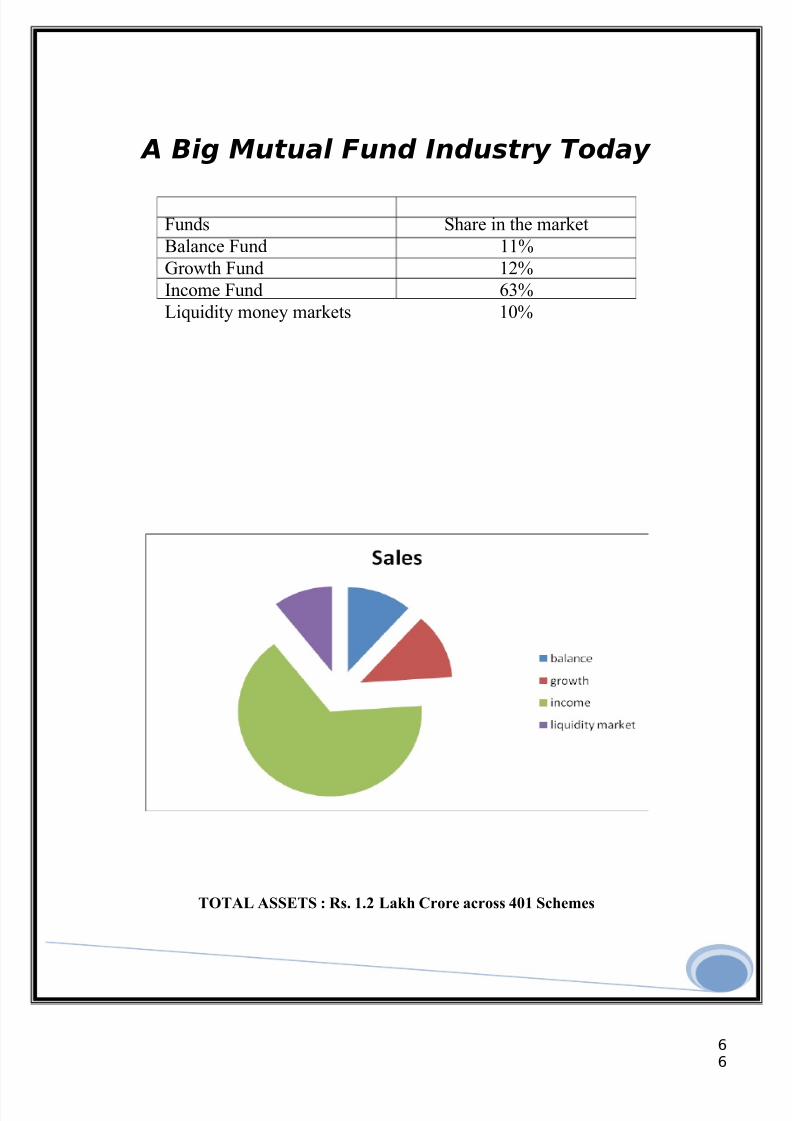

A Big Mutual Fund Industry Today

TOTAL ASSETS : Rs. 1.2 Lakh Crore across 401 Schemes

Funds Share in the market

Balance Fund 11%

Growth Fund 12%

Income Fund 63%

Liquidity money markets 10%

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 32/69

66

(b) Investment Based Classification:

Mutual funds may also be classified on the basis of securities in which they

invest. Basically, it is renaming the subcategories of return based classification.

# Equity Fund:

Such funds as the name implies, invest most of their investible shares in equity

shares of companies and undertake the risk associated with the investment in

equity shares. Such funds are clearly expected to outdo other funds in rising

market, because these have almost all their capital in equity. Equity funds again

can be of different categories varying from those that invest exclusively in high

quality ‘blue chip’ companies to those that invest solely in the new, un

established companies. The strength of these funds is the expected capital

appreciation. Naturally, they have a higher degree of risk.

# Debt Funds:

Such funds have their portfolio consisted of bonds, debentures, etc. this type of

fund is expected to be very secure with a steady income and little or no chance

of capital appreciation. Obviously risk is low in such funds. In this category we

may come across the funds called ‘Liquid Funds’ which specialize in investing

short term money market instruments. The emphasis is on liquidity and is

associated with lower risks and low returns.

# Balanced Fund:

The funds, which have in their portfolio a reasonable mix of equity and debt,

are known as balanced funds. Such funds will put more emphasis on equity

share investments when the outlook is bright and will tend to switch to

debentures when

the future is expected to be poor for shares.

(c) Sector Based Funds:

There are number of funds that invest in a specified sector of economy. While

such

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 33/69

66

funds do have the disadvantage of low diversification by putting all their all

eggs in one basket, the policy of specializing has the advantage of developing

in the fund managers an intensive knowledge of the specific sector in which

they are investing. Sector based funds are aggressive growth funds which make

investments on the basis of assessed bright future for a particular sector. These

funds are characterized by high viability, hence more risky.

OTHER INVESTMENT PLANS AND SERVICES IN MUTUAL FUNDS

1) SYSTEMATIC INVESTMENT PLAN

Systematic Investment Plan (SIP) is a simple, time-honored strategy

designed to help investors to accumulate wealth in a discipline manner over

the long-term and to plan a better future for them. SIP is more suitable for a

salaried employee with investible savings every month and who wishes to

generate better returns than other instruments at a low risk of price volatility.

# How do SIPs work? Instead of a lumpsum amount, you invest a pre-

specified amounting a scheme at pre-specified intervals. The number of units

that accrue to you on each periodic investment is a function of the then

prevailing net asset value (NAV) of the scheme you have opted for. Thus

irrespective of market conditions, your cost of investment will be mostly

lower than the average cost of market prices. This disciplined approach for

investing will provide the investors with the following benefits:

1) Reduces average cost2) Can be done regularly even for savings of Rs 1000

3) Encourages disciplined investing,

4) Eliminates the need to decide when to invest

5) Avoids the temptation to time the market.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 34/69

66

How Do Sips Better Market Average?

Rising market Falling market Volatile market

Month Amount

invetsted

Nav Unit

allotted

Nav Unit

allotted

Nav Unit allotted

1 1000 10 100 10 100 10 100

2 1000 12 83.33 8 125 12 83.33

3 1000 14 71.43 6 166.67 8 125

4 1000 16 62.5 4 250 10 100

Total 4000 52 317.26 28 641.67 40 408.33

AverageCost

per Units

12.61(Average Cost 13)

6.23(Average Cost 7)

9.8(Average Cost 10)

As one can see, the average cost per unit under an SIP programme

results in an average cost which is lower than most of the prices at

which one bought units.

2. Convenience – Save yourself the trouble of doing the same thing

Investor does not have to take time out from his busy schedule for managing

his investments. Enroll for the SIP by starting an account and providing the

fund with post-dated cheques of periodic investment (monthly, quarterly) based

on his convenience. Investor can relax once he has enrolled the form along with

postdated

cheques. Fund then bank his cheques on the requested date and credit the units

to his account. Besides the fund will send quarterly reports giving complete

transparency about his investments.

3. A boon for small investors (Low income group)

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 35/69

66

SIP has proved to be a boon for small investors, who has got a small saving

every month, but cannot find a suitable scheme to invest. Mutual funds SIP

plan provides a higher return than other small saving scheme.

MUTUAL FUND CONSTITUENTS

All mutual funds comprise four constituents – Sponsors, Trustees, Asset

Management Company (AMC) and Custodians.

a) Sponsors:

The sponsors initiate the idea to set up a mutual fund. It could be a registered

company, scheduled bank or financial institution. A sponsor has to satisfycertain conditions, such as capital, record (at least five years’ operation in

financial services), de-fault free dealings and general reputation of fairness.

The sponsors appoint the Trustee, AMC and Custodian. Once the AMC is

formed, the sponsor is just a stakeholder.

b) Trust/ Board of Trustees:

Trustees are like internal regulators in a mutual fund, and their job is to protect

the

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 36/69

66

interest of unit holders. Sponsors appoint trustees. Trustees float and market

schemes, and secure necessary approvals. They check if the AMC’s

investments are within well defined limits, whether the fund’s assets are

protected, and also ensure that unit holders get their due returns. They also

review any due diligence by the AMC. For major decisions concerning the

fund, they have to take the unit holders ‘consent.

c) Fund Managers/ AMC:

An AMC-Asset Management Company is the legal entity formed by the

sponsor to

run a mutual fund. They are the ones who manage money of the investors.

There is

the head of the fund house, generally referred to as the chief executive officer

(CEO). Under him comes the chief investment officer (CIO), who shapes the

fund’

investment philosophy, and the fund managers, who manage its schemes. They

are

assisted by a team of analysts, who track markets, sectors and companies. An

AMC takes decisions, compensates investors through dividends, maintains

proper accounting and information for pricing of units, calculates the NAV, and

provides information on listed schemes. It also exercises due diligence on

investments, and submits quarterly reports to the trustees. A fund’s AMC can

neither act for any other fund nor undertake any business other than asset

management. Its net worth should not fall below Rs. 10 Crore. And, its fee

should not exceed 1.25 percent if collections are below Rs. 100 Crore and 1

percent if collections are above Rs. 100 Crore. SEBI can pull up an AMC if it

deviates from its prescribed role.

d) Custodian:

Often an independent organization, it takes custody of securities and other

assets of

Mutual fund. Its responsibilities include receipt and delivery of securities,

collecting income-distributing dividends, safekeeping of the units and

segregating assets and settlements between schemes. Their charges range

between 0.15-0.2 percent of the net value of the holding. Custodians can

service more than one fund.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 37/69

66

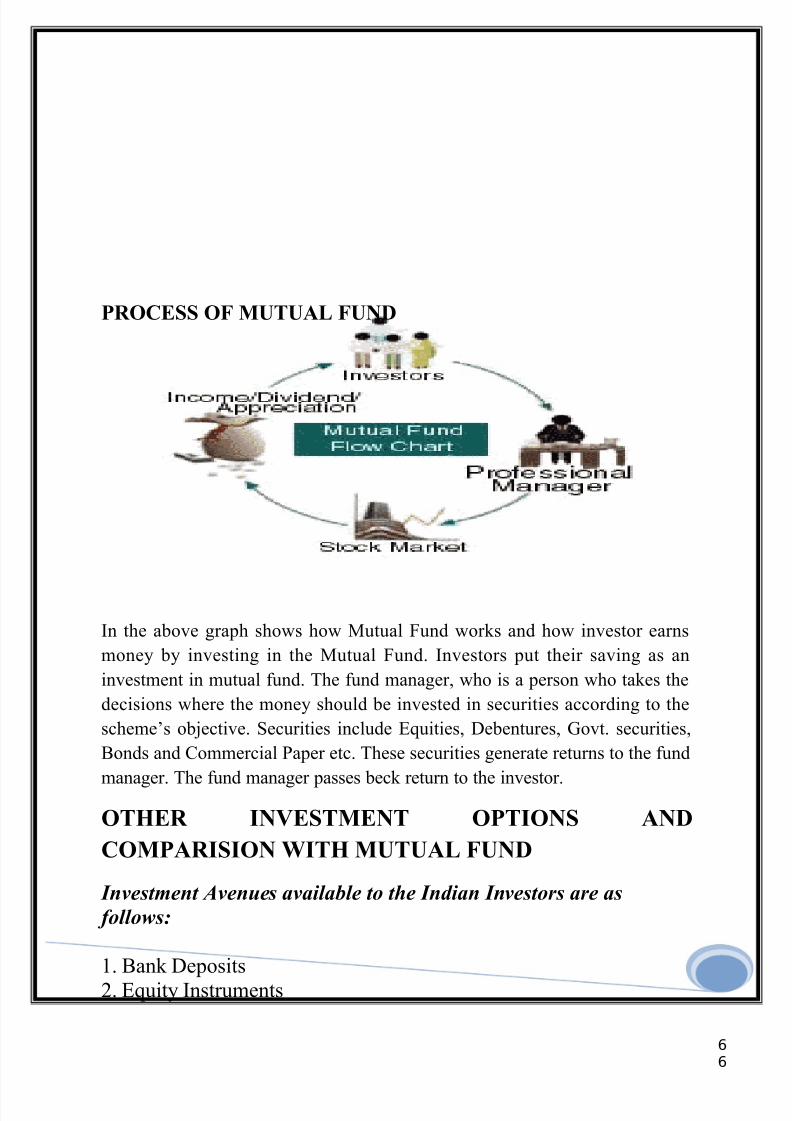

PROCESS OF MUTUAL FUND

In the above graph shows how Mutual Fund works and how investor earns

money by investing in the Mutual Fund. Investors put their saving as an

investment in mutual fund. The fund manager, who is a person who takes the

decisions where the money should be invested in securities according to the

scheme’s objective. Securities include Equities, Debentures, Govt. securities,

Bonds and Commercial Paper etc. These securities generate returns to the fund

manager. The fund manager passes beck return to the investor.

OTHER INVESTMENT OPTIONS AND

COMPARISION WITH MUTUAL FUND

Investment Avenues available to the Indian Investors are as

follows:

1. Bank Deposits

2. Equity Instruments

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 38/69

66

3. Debentures4. Fixed Deposits by Companies5. Bonds6. RBI Relief Bonds7. Public Provident Fund8. National Saving Certificates / National Saving Schemes9. Monthly Income Schemes10. Life Insurance11. Mutual Funds

INVESTMENT AVENUES

95

79

67

58

6

75

50

8

19

0

1 0

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 0 0

1

R E S P O N

D E N

T S

Insurance Bank FD/Company FD

Post Office Savings Government Securities

Gold/Silver Stocks

Mutual Fund IPO

Others

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 39/69

66

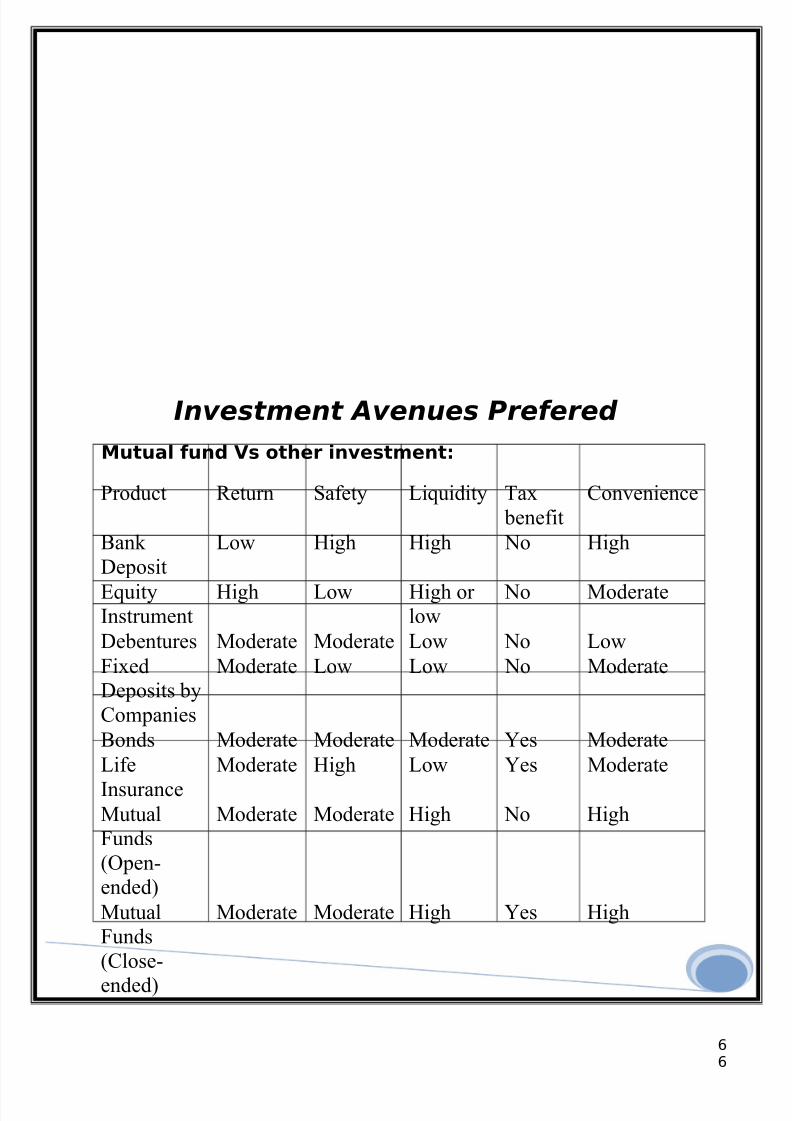

Investment Avenues Prefered

Mutual fund Vs other investment:

Product Return Safety Liquidity Tax benefit

Convenience

Bank Deposit

Low High High No High

EquityInstrument

High Low High or low

No Moderate

Debentures Moderate Moderate Low No Low

FixedDeposits byCompanies

Moderate Low Low No Moderate

Bonds Moderate Moderate Moderate Yes Moderate

Life

Insurance

Moderate High Low Yes Moderate

MutualFunds(Open-ended)

Moderate Moderate High No High

MutualFunds(Close-

ended)

Moderate Moderate High Yes High

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 40/69

66

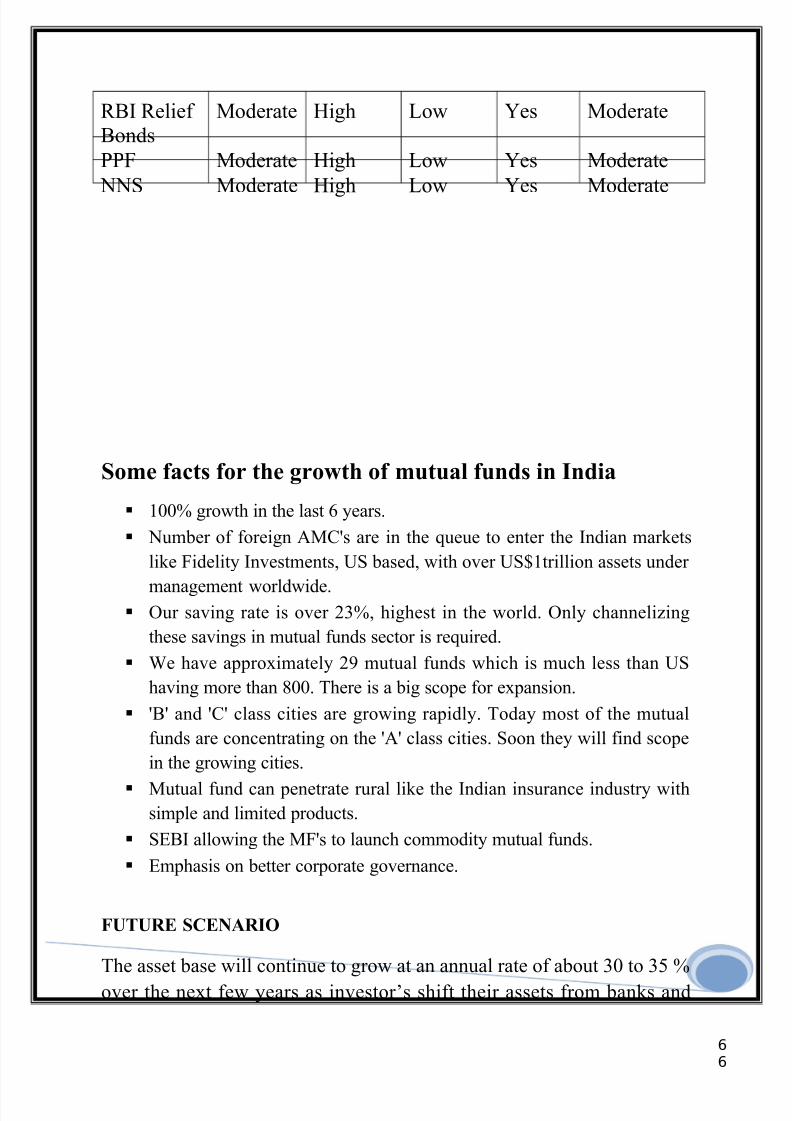

RBI Relief Bonds

Moderate High Low Yes Moderate

PPF Moderate High Low Yes Moderate

NNS Moderate High Low Yes Moderate

Some facts for the growth of mutual funds in India

100% growth in the last 6 years.

Number of foreign AMC's are in the queue to enter the Indian markets

like Fidelity Investments, US based, with over US$1trillion assets under

management worldwide. Our saving rate is over 23%, highest in the world. Only channelizing

these savings in mutual funds sector is required.

We have approximately 29 mutual funds which is much less than US

having more than 800. There is a big scope for expansion.

'B' and 'C' class cities are growing rapidly. Today most of the mutual

funds are concentrating on the 'A' class cities. Soon they will find scope

in the growing cities.

Mutual fund can penetrate rural like the Indian insurance industry withsimple and limited products.

SEBI allowing the MF's to launch commodity mutual funds.

Emphasis on better corporate governance.

FUTURE SCENARIO

The asset base will continue to grow at an annual rate of about 30 to 35 %

over the next few years as investor’s shift their assets from banks and

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 41/69

66

other traditional avenues. Some of the older public and private sector

players will either close shop or be taken over.

Out of ten public sector players five will sell out, close down or merge

with stronger players in three to four years. In the private sector this trend

has already started with two mergers and one takeover. Here too some of

them will down their shutters in the near future to come.

But this does not mean there is no room for other players. The market will

witness a flurry of new players entering the arena. There will be a large

number of offers from various asset management companies in the time to

come. Some big names like Fidelity, Principal, Old Mutual etc. arelooking at Indian market seriously. One important reason for it is that

most major players already have presence here and hence these big names

would hardly like to get left behind.

In the U.S. most mutual funds concentrate only on financial funds like

equity and debt. Some like real estate funds and commodity funds also

take an exposure to physical assets. The latter type of funds are preferred

by corporate who want to hedge their exposure to the commodities theydeal with.

For instance, a cable manufacturer who needs 100 tons of Copper in the

month of January could buy an equivalent amount of copper by investing

in a copper fund. For Example, Permanent Portfolio Fund, a conservative

U.S. based fund invests a fixed percentage of it’s corpus in Gold, Silver,

Swiss francs, specific stocks on various bourses around the world, short –

term and long-term U.S. treasuries etc.

In U.S.A. apart from bullion funds there are copper funds, precious metal

funds and real estate funds (investing in real estate and other related assets

as well.).In

India, the Canada based Dundee mutual fund is planning to launch a gold

and a real estate fund before the year-end.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 42/69

66

In developed countries like the U.S.A there are funds to satisfy

everybody’s requirement, but in India only the tip of the iceberg has been

explored. In the near future India too will concentrate on financial as well

as physical funds.

The mutual fund industry is awaiting the introduction of DERIVATIVES

in the country as this would enable it to hedge its risk and this in turn

would be reflected in it’s Net Asset Value (NAV).

SEBI is working out the norms for enabling the existing mutual fund

schemes to trade in Derivatives. Importantly, many market players have

called on the Regulator to initiate the process immediately, so that themutual funds can implement the changes that are required to trade in

Derivatives.

Tata Mutual Fund

Backed by one of the most trusted and valued brands in India, TataMutual Fund has earned the trust of lakhs of investors with its consistent

performance and world-class service.

Tata Mutual Fund manages around Rs. 21,197.00 crores (average AUM

for the month) as on August 31, 2008 worth of assets across its varied

offerings. Tata Mutual Fund offers an investment option for everyone,

whether you are a businessman or salaried professional, a retired person

or housewife, an aggressive investor or a conservative capital builder.

The Tata Asset Management philosophy is centered on seeking consistent,

long-term results. Tata Asset Management aims at overall excellence,

within the framework of transparent and rigorous risk controls.

We constantly benchmark our efforts against these tenets of performance:

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 43/69

66

Consistency: We strive to deliver consistent results through our value-

based investing methodology, keeping alive the credo of the late doyen of

the Tata Group, Mr. J.R.D. Tata, that money received from the people

should go back to them several times over.

Flexibility: Tata Mutual Fund offers investors a broad range of managed

investment products in various asset classes and risk parameters, with

operational flexibility to suit their varied investment needs.

Stability: Our commitment to the highest quality of service and integrity

is the foundation upon which we build trust with our clients.

Service: We offer a wide range of services to assist investors have a

fulfilling and rewarding financial planning experience with us.

A Proud Pedigree

Tata Asset Management Ltd is a part of the Tata

group, one of India's largest and most respected

industrial groups, renowned for its adherence to

business ethics.

The Group has always believed in returning wealth to the society that it

serves. Thus, nearly two-thirds of the equity of Tata Sons, the Group's

promoter company, is held by philanthropic trusts, which have created ahost of national institutions in the natural sciences, medical care, energy

and the arts. The trusts also give substantial annual grants and

endowments to deserving individuals and institutions in the areas of

education, healthcare and social uplift.

By combining ethical values with business acumen, globalization with

national interests and core businesses with emerging ones, the Tata Group

aims to be the largest and most respected global brand from India. This

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 44/69

66

way, it fulfills its long-standing commitment to improving the quality of

life of its stakeholders.

Leadership with Trust

Our purpose at the Tata Group is to improve the

quality of life of the communities we serve. We do this

by attaining leadership positions in sectors of national

economic significance, to which the Group brings a unique set of

capabilities. This requires us to grow aggressively in focused areas of

business.

Our heritage of returning to society what we earn evokes trust among

consumers, employees, shareholders and the community. It is an ongoing

process, continuously enriched by the formalization of the high standards

of behavior that we expect from employees and companies.

Overview

At Tata Asset Management Company, we believe that your investment

needs depend on personal and financial goals. Identifying your financial

goals is the key to achieving the big things in your life, be it your child's

education or a carefree and comfortable retired life.

After identifying and defining your financial goals, you now need to plan

for each of them in an organized and a professional way. Investment

experts around the world advise instruments like equity funds and stocks

for long-term (more than 5 years), income funds for medium-term and

liquid funds for short-term needs.

The investment matrix here depicts the entire available variety of

investment options. Those at the top provide for a greater opportunity for

long-term capital growth while those at the bottom take care of current

income and reasonable return & liquidity. Tata Mutual Fund offers a wide

range of funds for different investment instruments designed to cater to

your individual profile and life-stage.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 45/69

66

Product of Tata Mutual Fund:

♦ Tata Dynamic Bond Fund♦ Tata Fixed Income Portfolio Fund♦ Tata Income Plus Fund♦ Tata Short Term Bond Fund♦ Tata Treasury Manager Fund♦ Tata Monthly Income Fund♦ Tata M I P Plus Fund♦ Tata bonus fund

Promotion of Mutual Fund:

Tata Mutual Fund Company promotes his mutual fund through TVadvertising. Outdoor media and agents.

HDFC Mutual Fund

HDFC Asset Management Company Limited (AMC)

VisionTo be a dominant player in the Indian mutual fund space recognized for its high

levels of ethical and professional conduct and a commitment towards

enhancing investor interests.

Sponsors

Housing Development Financial Corporation Limited (HDFC)

HDFC was incorporated in 1977 as the first specialized housing financeinstitution in India. HDFC provides financial assistance to individuals,

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 46/69

66

corporate and developers for the purchase or construction of residential

housing. It also provide property related services (e.g. property identification,

sales services and valuation), training and consultancy. Of course activities,

housing finance remains the dominant activity. HDFC currently has a client

base of over 800000 borrowers, 1200000 depositors, 92000 shareholders and

50000 deposit agents. HDFC raises funds from international agencies such as

the World Bank, IFC (Washington), USAID, CDC, ADB and KFW, domestic

term loans from banks and insurance companies, bonds and deposits. HDFC

has received the highest rating for its bonds and deposits program for the 9 th

year in succession. HDFC Standard Life Insurance Company Limited.

Promoted by HDFC was the 1st life insurance company in the private sector to

be granted a Certificate of Registration(on October 23, 2000) by the Insurance

Regulatory and Development Authority to transact life insurance business in

India.

Standard Life Investment Limited

The Standard Life Assurance Company was established in 1825 and has

considerable experience in global financial markets. In 1998, Standard Life

Investment Limited became the dedicated investment management company of

The Standard Life Group and is owned 100% by the Standard Life AssuranceCompany. With the global assets under management of approximately

US$186.45 billion as at March 31, 2005, Standard Life Investment Limited is

one of the world’s major investment companies and is responsible for investing

money on behalf of five million retail and institutional clients worldwide. With

its headquarters in Edinburgh, Standard Life Investment Limited has an

extensive and developing global presence with operations in the United

Kingdom, Ireland, Canada, USA, China, Korea and Hong Kong. In order to

meet the different needs and risk profiles of its clients, Standard LifeInvestment Limited manages a diverse portfolio covering all the major markets

world-wide, which includes a range of private and public equities, government

and company bonds, property investments and various derivative instruments.

HDFC Trustee Company Ltd.

A company incorporated under the Companies Act, 1956 is the Trustee to the

Mutual Fund vide the Trust deed dated June 8, 2000, as amended from time to

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 47/69

66

time. HDFC Trustee Company Limited is a wholly owned subsidiary of HDFC

Limited.

HDFC asset Management Company (AMC)

HDFC AMC was incorporated under the Companies Act, 1956, on December

10, 1999, and was approved to act as an Asset Management Company for the

Mutual Fund by SEBI on July 3, 2000. The registered office of the AMC is

situated at Ramon House, 3rd Floor, H.T. Parekh Marg, 169, Back bay

Reclamation, Church gate, Mumbai - 400 020.

In terms of the Investment Management Agreement, the Trustee has appointed

HDFC Asset Management Company Limited to manage the Mutual Fund. The

paid up capital of the AMC is Rs. 75.161 crore.

Zurich Insurance Company (ZIC), the Sponsor of Zurich India Mutual Fund,

following a review of its overall strategy, had decided to divest its Asset

Management business in India. The AMC had entered into an agreement with

ZIC to acquire the said business, subject to necessary regulatory approvals.

On obtaining the regulatory approvals, the Schemes of Zurich India Mutual

Fund has now migrated to HDFC Mutual Fund on June 19, 2003.AMC is

managing 18 open-ended schemes of the Mutual Fund

♦HDFC Growth Fund (HGF)

♦HDFC Balanced Fund (HBF)

♦HDFC Income Fund (HIF)

♦HDFC Liquid Fund (HLF)

♦HDFC Tax Plan 2000 (HTP)

♦HDFC Children's Gift Fund (HDFC CGF)

♦HDFC Gilt Fund (HGILT)

♦HDFC Short Term Plan (HSTP)

♦HDFC Index Fund, HDFC Floating Rate Income Fund (HFRIF)

♦HDFC Equity Fund (HEF)

♦HDFC Top 200 Fund,(HT200)

♦HDFC Capital Builder Fund (HCBF)

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 48/69

66

♦HDFC TaxSaver (HTS)

♦HDFC Prudence Fund (HPF)

♦HDFC High Interest Fund (HHIF)

♦HDFC Sovereign Gilt Fund (HSGF)

♦HDFC Cash Management Fund (HCMF)

The AMC is also managing the respective Plans of HDFC Fixed Investment

Plan, a closed ended Income Scheme. The AMC has obtained registration from

SEBI vide Registration No. - PM / INP000000506 dated December 22, 2000 to

act as a Portfolio Manager under the SEBI (Portfolio Managers) Regulations,

1993. The Certificate of Registration is valid from January 1, 2001 to

December 31, 2003. The AMC is also providing portfolio management /

advisory services and such activities are not in conflict with the activities of the

Mutual Fund.

Promotion of Mutual Fund:

Tata Mutual Fund Company promotes his mutual fund through

TV advertising. Outdoor media and agents.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 49/69

66

Empirical Analysis

Investment instrument

People invest their money in different investment instrument for different

purpose; above I have draw graphs of people invest their money in

different instrument. In above graphs I have done survey of 100 people,

out of 100 people 27% of people invest in bank Deposits, 24% of people

invest in Direct equity, 14% of people invest in mutual fund and 9% of

people invest in Postal Scheme. So from above data we can say that mostof people prefer investment in Bank Deposits then other instrument.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 50/69

66

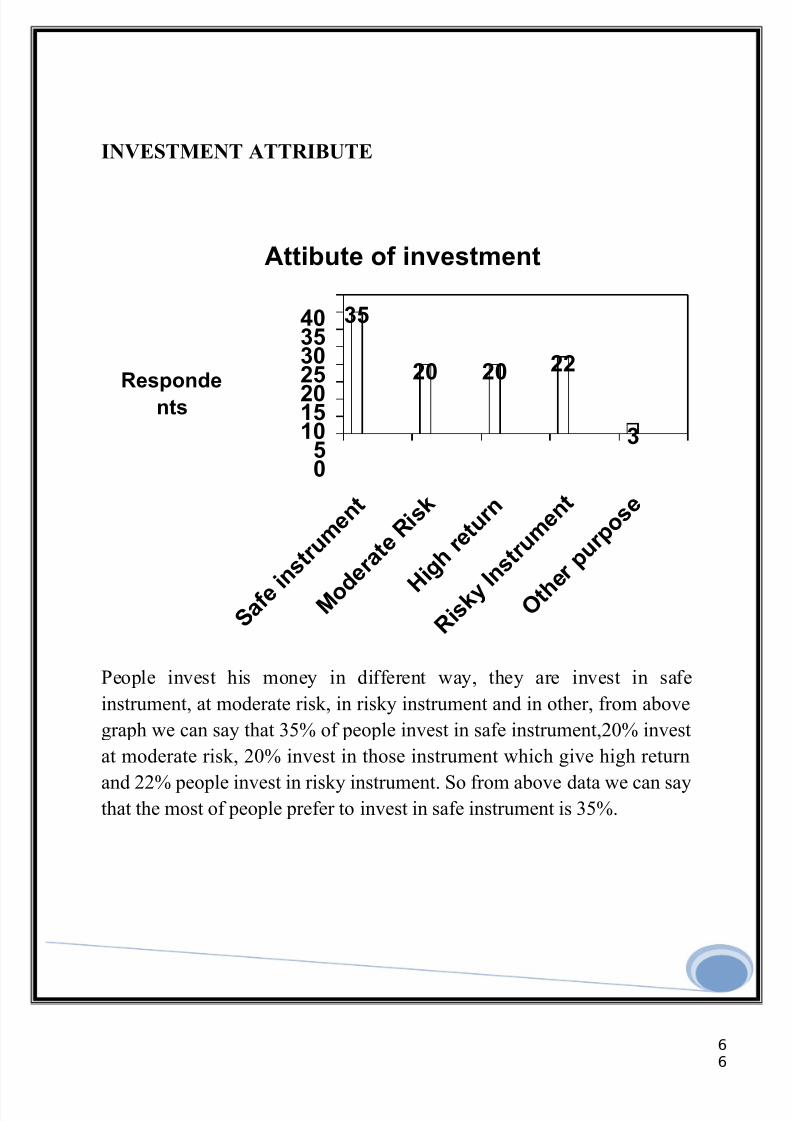

INVESTMENT ATTRIBUTE

Attibute of investment

35

20 20 22

3

05

101520

25303540

S a f e i

n s t r u

m e n

t

M o d e r a t e R i

s k

H i g h

r e t u r n

R i s k y I

n s t r u

m e n

t

O t h e

r p u r p o

s e

Responde

nts

People invest his money in different way, they are invest in safe

instrument, at moderate risk, in risky instrument and in other, from above

graph we can say that 35% of people invest in safe instrument,20% invest

at moderate risk, 20% invest in those instrument which give high return

and 22% people invest in risky instrument. So from above data we can saythat the most of people prefer to invest in safe instrument is 35%.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 51/69

66

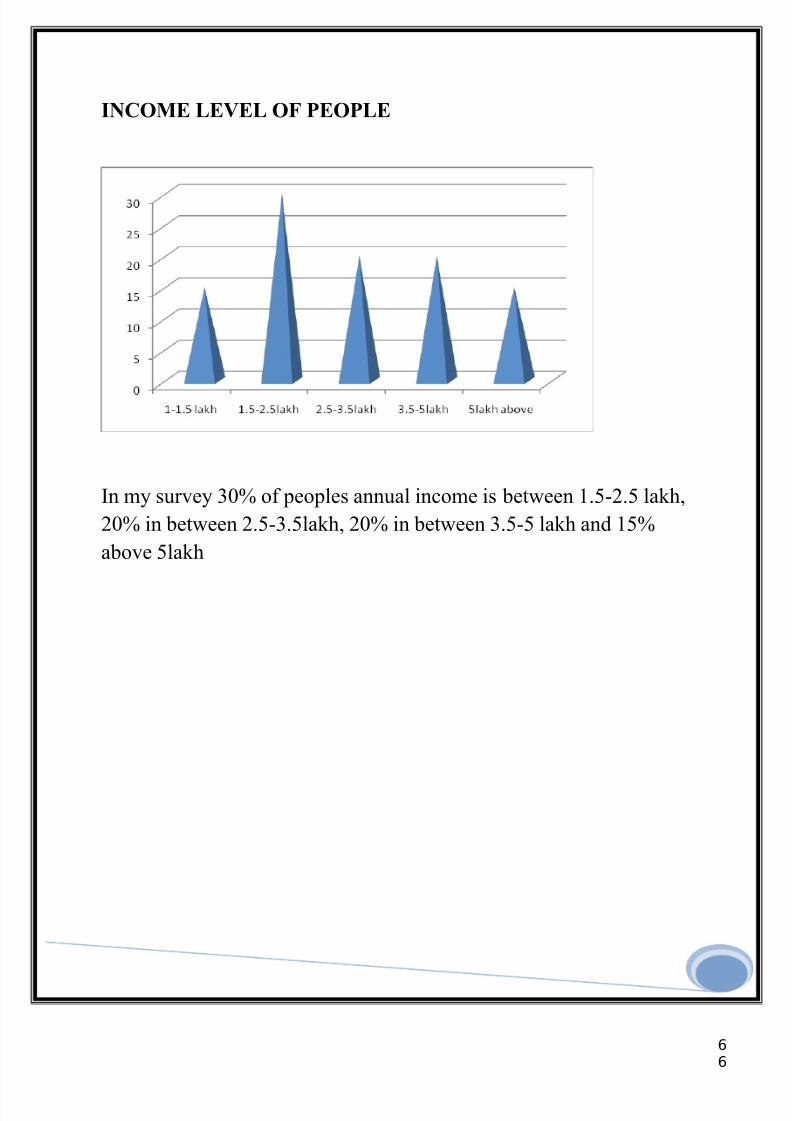

INCOME LEVEL OF PEOPLE

In my survey 30% of peoples annual income is between 1.5-2.5 lakh,

20% in between 2.5-3.5lakh, 20% in between 3.5-5 lakh and 15%

above 5lakh

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 52/69

66

Attribute that people look before investment

In present situation people are more knowledgeable than before,

people know everything about investment instrument available in the

market. They also know which are more profitable and which are not profitable for him. People invest money for different purpose like

some people invest money which instrument has high liquidity, The

main purpose of investing in liquidity instrument is to get money

back whenever require. Some invest in those instruments which has

high safety of money like FD and Postal Scheme. Some people invest

in those instruments which give high return like Shares and mutual

Fund

From above pie chart we can say that the 40% of people invest in

safety instrument and 30% of people invest in those instruments

which have high liquidity and 25% invest which give high return.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 53/69

66

0

10

20

30

40

50

60

70

80

90

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

East

West

North

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 54/69

66

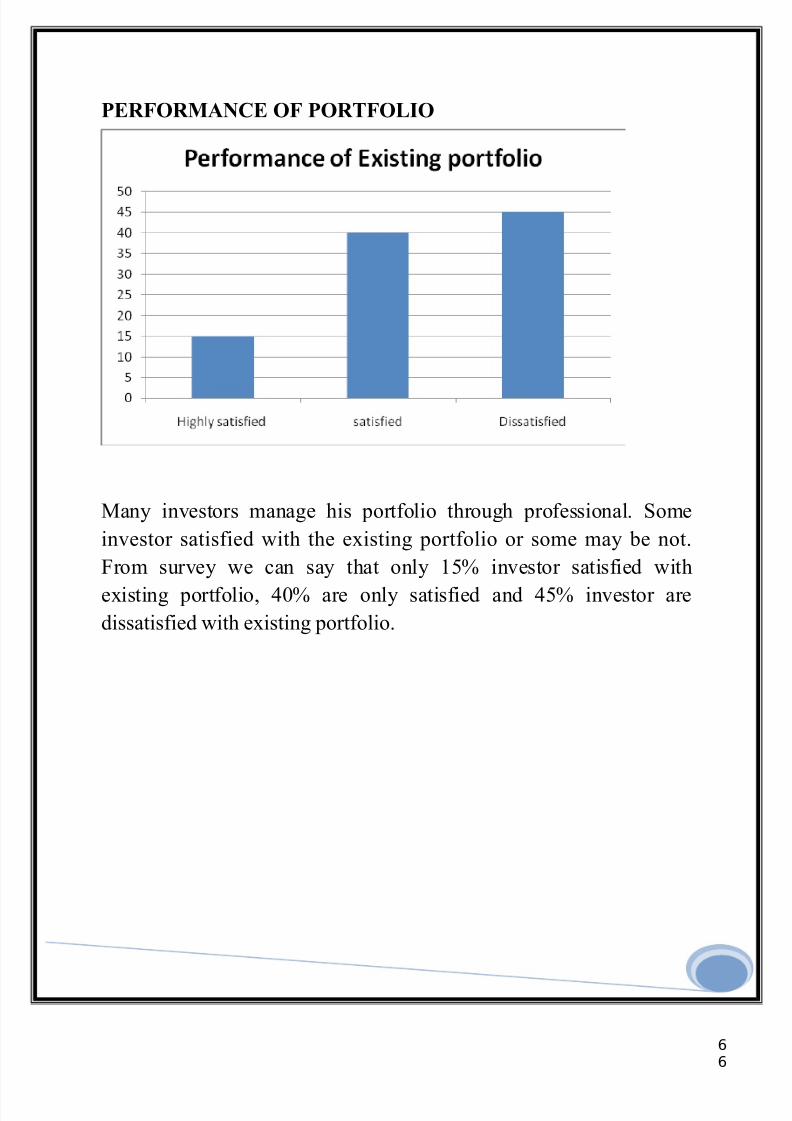

PERFORMANCE OF PORTFOLIO

Many investors manage his portfolio through professional. Some

investor satisfied with the existing portfolio or some may be not.

From survey we can say that only 15% investor satisfied with

existing portfolio, 40% are only satisfied and 45% investor are

dissatisfied with existing portfolio.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 55/69

66

PROFESSIONAL SERVICE FOR MANAGING PORTFOLIO

In survey I find that the 68% of people want some professional service

from expert for managing their portfolio, these type of people have large

portfolio of investment in different instrument. 35% of people does not

want any portfolio management service from expert

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 56/69

66

FREQUENCY

Today rich people have no time to see where their money was investedand it is difficult to manage all this thing so they hire expert to manage his

portfolio or outsource it to agency. From above graphs we can say that

25% of people want his statement monthly, 20% people want daily

statement and 18% of people quarterly.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 57/69

66

PEOPLE PREFERENCE

Today people are more aware about market and performance of

investment instrument in market, they prefer that instrument which is

more profitable. Second image of investment instrument in the mind of

people,Third because word of mouth publicity. Fourth loyalty People

prefer different company mutual fund because of above reasons like Ex,

in case of two wheeler we prefer Hero Honda. In Mutual fund 30% of

people prefer Reliance Mutual Fund, 23% of people prefer SBI Mutual

Fund, 20% of people prefer TATA Mutual Fund and 15% prefer HDFC

mutual Fund.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 58/69

66

Finding And Suggestion

The findings from the study are as under:

The people are basically of conservative nature and hence are very

precautious about their hard earned money. Hence they would like

to play it safe when it comes to spending of their money.

Security and returns are the two main reasons that are taken into

consideration before making an investment.

Bank fixed deposits and post office savings seem to be most

preferred one among the investors because it is considered to be the

most secured one.

Shares and mutual funds were considered to be very risky and hence

that seemed to be the last choice of the general mass

Amongst mutual fund and shares people preferred shares because

the possessed complete knowledge about the shares but had very

little knowledge about the mutual fund industry.

The people who do not invest in mutual fund basically fear that they

are less secured as compared with other investments.

The others were aware about the concept of mutual fund but were

not full aware of its intricacy hence were not interested in investing

in it.

Most of the investors who invest in Mutual Fund substitute the same

against the Bank Deposits, insurance and other saving schemes. The

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 59/69

66

investors are not willing to invest in mutual fund industry unless

they are guaranteed about minimum returns.

Most of investor invests in safe instrument which has high security

of capital.

The increase in Mutual fund and various schemes have increased

competition. Hence it has been remarked by many investors “ they

prefer Reliance mutual fund than other because it give higher return

than other

Many investor want professional service to manage his portfolio.

Many Investors prefer his statement monthly.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 60/69

66

SUGGESTION

The Indian Investment Industry’s development and success would depend

on various issues such as:

Educate the people: There are lots of alternatives available in the

present time. But because of lack of knowledge people are not ready

to try them. Even because of the fear to try new ones the investment

industry has limited itself. The same can be done through arranging

events that promote such innovations.

Preconceptions rule: The preconceptions that a person carries tries

rule his investment decisions. The past record of shares and mutual

fund restrict the people in investing in the same. Though the rules

and regulations have changed a lot but there are still people who are

not ready to accept such facts.

Let them know where there amount in reinvested: The investors

should know that the amount that is invested in the company how

the funds are used and for what purpose .They have the right to

know where are their funds reinvested i.e. the companies should be

transparent.

Do not cut others line for showing yourself bigger: The

promoters to promote their funds degrading the other modes of

investment and hence this limits their investment scopes itself

because this act degrades the company in the eyes of the customers

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 61/69

66

Lead through Innovation: Although there is enough room in the

market, unfortunately in Indian market, all mutual funds have been

chasing the same set of investors with the same set of products and

inducements. Product differentiation is the first step towards

escaping competition and attracting more investors.

Rebuild investor’s confidence: For a long term growth of the

industry, it is a must to win the confidence of the investors and there

is no way to do this other than bringing in more transparency in the

operations, proper communications between the market players and

their customers.

Manage risks through derivatives: India has a wide range of

derivatives products in the market. Mutual Fund should also come

forward with more of such products. In the Business World dated

24th November 2003 there was news that Benchmark fund is coming

out with an Equity Arbitrage Fund called “Dynamic Arbitrage

Fund”. Otherwise SEBI has not allowed any AMC to float a hedge

fund in India.

Educate investor’s about the principles: There is no doubt that

investor’s education is one area, which has to be concentrated upon

in the mutual fund industry. The Mutual funds must come forward

to make funds understandable to them. The must be made aware

about various asset allocation principles.

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 62/69

66

Conclusion

The Ground rules of Investing

Moses gave to his followers 10 commandments that were to be followed

till eternity. The world of investments too has several ground rules meant

for investors who are novices in their own right and wish to enter the

myriad world of investments. These come in handy for there is every

possibility of losing what one has if due care is not taken.

1. Assess yourself: Self-assessment of one’s needs; expectations and

risk profile is of prime importance failing which; one will make

more mistakes in putting money in right places than otherwise. One

should identify the degree of risk bearing capacity one has and also

clearly state the expectations from the investments. irritational

expectation will only bring pain

2. Try to understand where the money is going: It is important to

identify the nature of investment and to know if one is compatible

with the investment. One can lose substantially if one picks the

wrong kind of fund. In order to avoid any confusion it is better to go

through the literature such as offer document and fact sheets that

company provide their own fund.

3. Don't rush in picking funds, think first: One first has to decide

what he wants the money for and it is this investment goal that

should be the guiding light for all investments done. It is thus

important to know the risks associated with the fund and align it

with the quantum of risk one is willing to take. One should take a

7/28/2019 Alpesh Final

http://slidepdf.com/reader/full/alpesh-final 63/69

66

look at the portfolio of the funds for the purpose. Excessive

exposure to any specific sector should be avoided, as it will only

add to the risk of the entire portfolio. Identifying the proposed