All content in this document is copyright 2001, Gómez, Inc. Paradoxes and Progress American Bankers...

14

All content in this document is copyright 2001, Gómez, Inc. Paradoxes and Progress American Bankers Association Webcast Online Banking Best Practices Christopher Musto Vice President, Research Gomez, Inc. January 31, 2002

-

Upload

justus-bridgers -

Category

Documents

-

view

213 -

download

0

Transcript of All content in this document is copyright 2001, Gómez, Inc. Paradoxes and Progress American Bankers...

All content in this document is copyright 2001, Gómez, Inc.

Paradoxes and Progress

American Bankers Association Webcast

Online Banking Best Practices

Christopher MustoVice President, Research

Gomez, Inc.

January 31, 2002

Paradoxes and Progress

Agenda

Research methods

How resolving four paradoxes leads us to rethink the Internet

Paradoxes and Progress

Research Methods

Trends in consumer behavior and attitudes

Business and product strategies

The utility, usability and reliability of the Internet offering

The integration of the Internet into the overall value proposition

Paradoxes and Progress

Four paradoxes that lead us to rethink the Internet

Drawing from the consumer marketplace:

Financial planning Aggregation Advisors Credit cards

Paradoxes and Progress

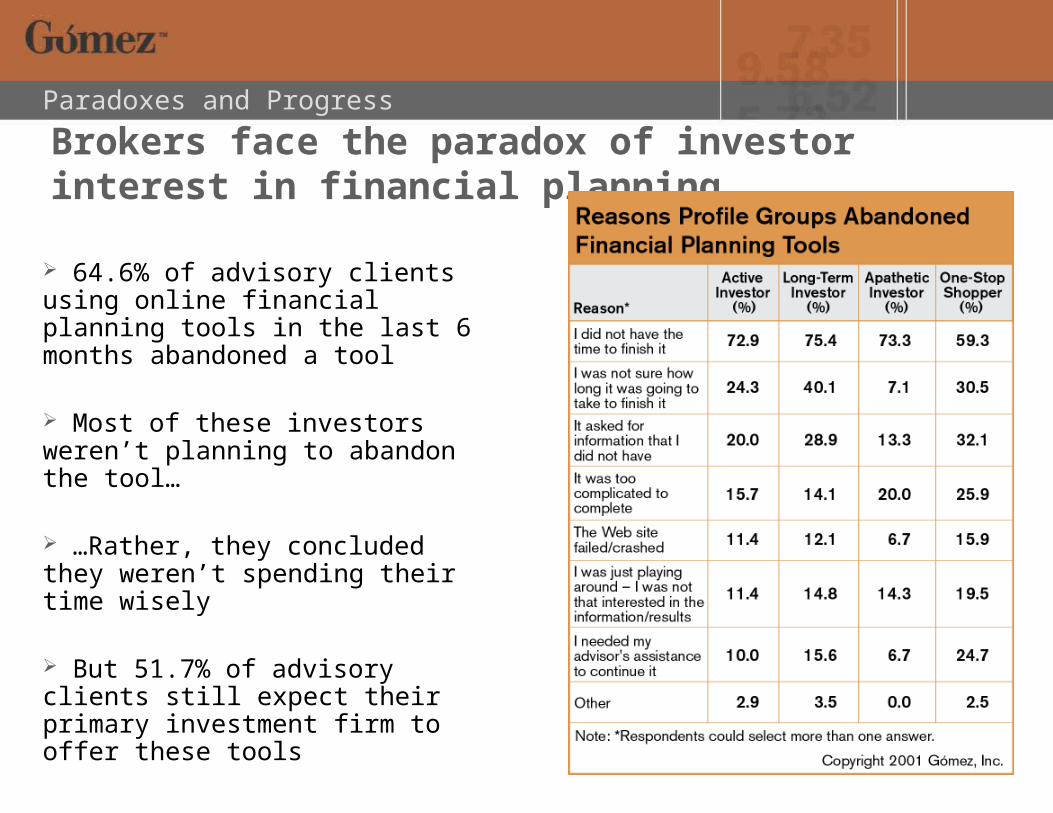

Brokers face the paradox of investor interest in financial planning

64.6% of advisory clients using online financial planning tools in the last 6 months abandoned a tool

Most of these investors weren’t planning to abandon the tool…

…Rather, they concluded they weren’t spending their time wisely

But 51.7% of advisory clients still expect their primary investment firm to offer these tools

Paradoxes and Progress

Resolving the financial planning paradox

Empower advisors to collaborateAdvisors want to see same information client is viewing

and collaborate online

Make use of email and other outreach21.6% of advisory clients accessing investment accounts

somewhere online would prefer to communicate with their advisors by email

Recognize that most consumers aren’t going to engage in involved financial planning on their own

Paradoxes and Progress

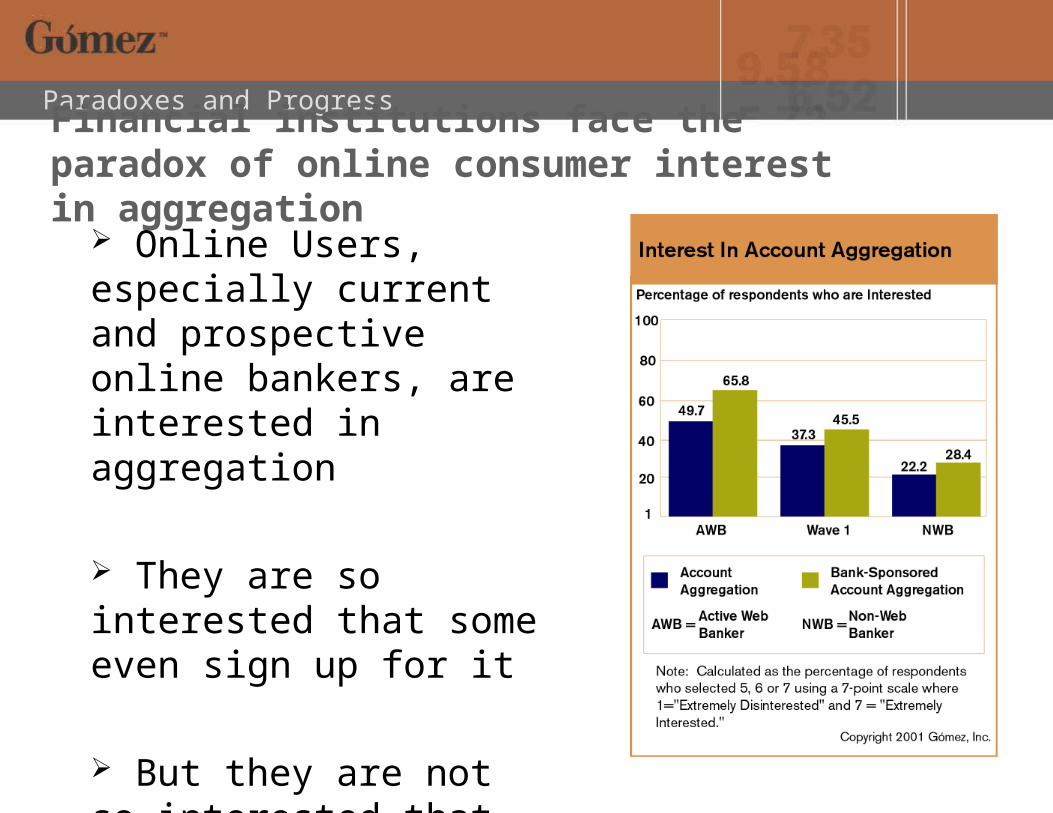

Financial institutions face the paradox of online consumer interest in aggregation

Online Users, especially current and prospective online bankers, are interested in aggregation

They are so interested that some even sign up for it

But they are not so interested that they use it

Paradoxes and Progress

Resolving the aggregation paradox

Integrate aggregation into existing account management interfaces

Consumers express the more interest in aggregation when it is offered by their bank and integrated into existing account management

Use advisors to transform data into financial adviceYodlee’s “Quicken on Steroids” comparison inadvertently

gets to the point: PFM users don’t use PFM financial planning tools

Paradoxes and Progress

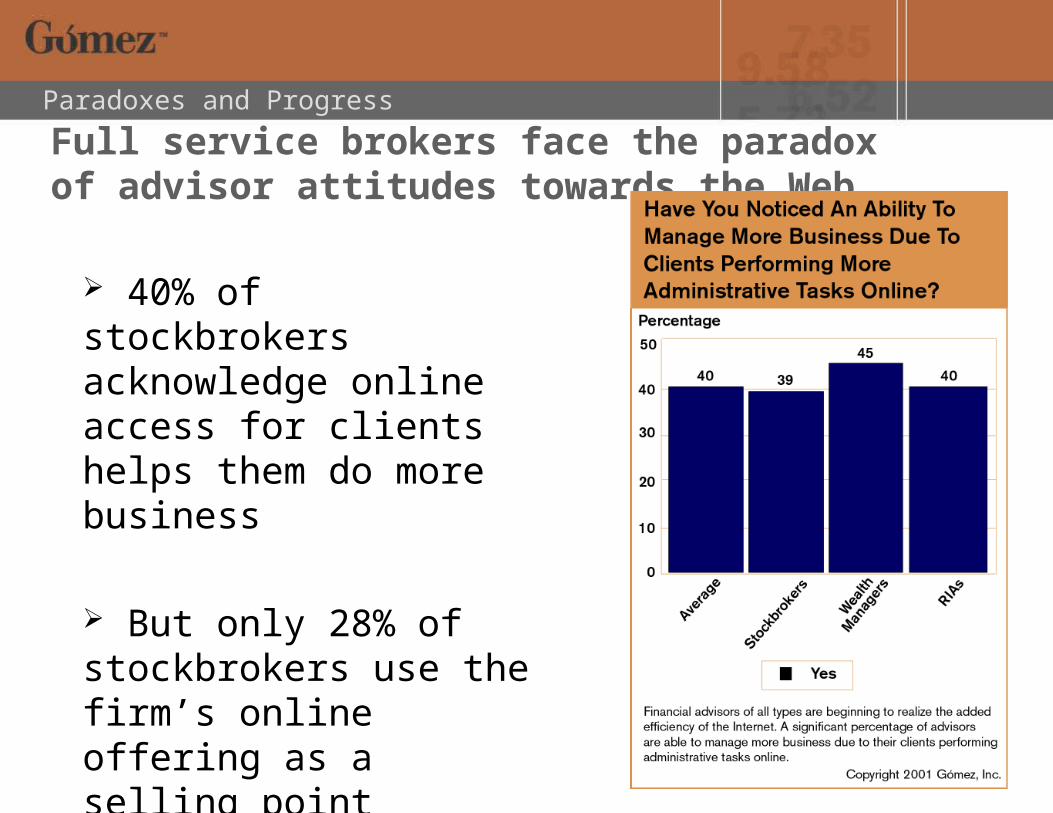

Full service brokers face the paradox of advisor attitudes towards the Web

40% of stockbrokers acknowledge online access for clients helps them do more business

But only 28% of stockbrokers use the firm’s online offering as a selling point

Paradoxes and Progress

Resolving the advisor paradox

Market relationships, not products, to wealthier customers

“Half the time clients ask about content and products you know are inappropriate and you need to spend the time explaining to them why it’s inappropriate” (stockbroker)

Build offerings that stand up to scrutinyFully 50% of advisors report that site performance alone

has caused client complaints about the Internet offering

Don’t try to ape discount brokerage model

Full service is a different market and not trade-driven

Paradoxes and Progress

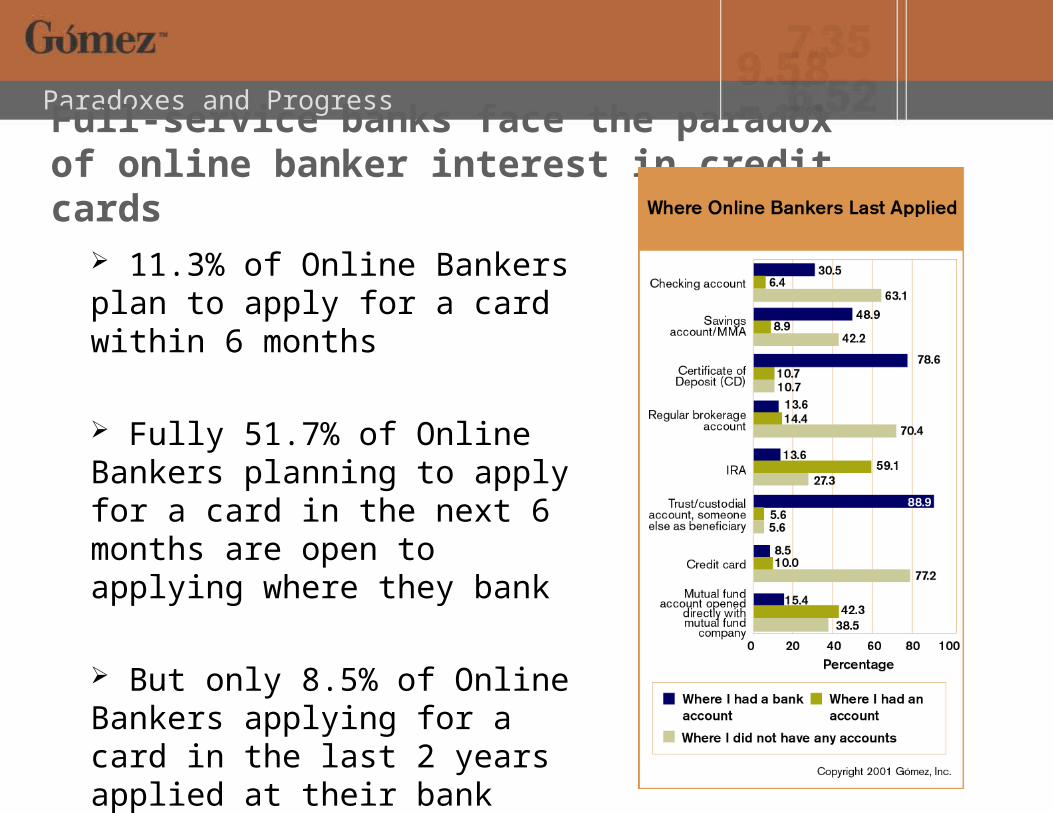

Full-service banks face the paradox of online banker interest in credit cards

11.3% of Online Bankers plan to apply for a card within 6 months

Fully 51.7% of Online Bankers planning to apply for a card in the next 6 months are open to applying where they bank

But only 8.5% of Online Bankers applying for a card in the last 2 years applied at their bank

Paradoxes and Progress

Resolving the credit card paradox

Promote credit card pre-approvals within account management interface or by email

28.7% of online bankers about to apply for another account say a targeted email from their bank would be highly effective

Stress online applicationsFully 69.7% of Online Bankers planning to apply for a card

in the next 6 months plan to apply for the card online

Pre-populate credit card applicationsOnly 40% of Scorecard banks pre-fill customer data for any

online account applications

Paradoxes and Progress

Resolving paradoxes takes next-generation thinking throughout your markets

Static functionality has become too broad and too complex to be useful or used

Your customers are creatures of habit

First generation worries about channel conflict don’t address the real challenge

Being more means being proactive

All content in this document is copyright 2001, Gómez, Inc.

Paradoxes and Progress

American Bankers Association Webcast

Online Banking Best Practices

Christopher MustoVice President, Research

Gomez, Inc.

January 31, 2002