Alii Place, Suite 150 1099 Alakea Street, Honolulu,...

68

Daniel A. Grabauskas EXECUTIVE DIRECTOR AND CEO GOVERNMENT AFFAIRS/AUDIT/LEGAL MATTERS COMMITTEE MEMBERS Terrence M. Lee CHAIR Colleen Hanabusa VICE CHAIR Michael D. Formby Donald G. Horner Ivan Lui‐Kwan, Esq. Government Affairs/Audit/Legal Matters Committee Alii Place, Suite 150 1099 Alakea Street, Honolulu, Hawaii (entrance on Richards Street) Thursday, January 28, 2016, 8:30 am Agenda I. Call to Order by Chair II. Public Testimony on All Agenda Items III. Approval of Minutes of the December 17, 2015 Government Affairs/Audit/Legal Matters Committee Meeting IV. Report on the Independent Financial Audit V. Executive Session Pursuant to Hawaii Revised Statutes Section 92-4 and Section 92-5(a)(4), the Board may enter into Executive Session to consult with its attorneys on questions and issues on a matter pertaining to the Board’s powers, duties, privileges, immunities and liabilities with regard to the matters set forth in part VI. VI. Procurement of the Independent Financial Auditor Contract VII. Adjournment Note: Persons wishing to testify on items listed on the agenda are requested to register by completing a speaker registration form at the meeting or online on the HART section of the www.honolulutransit.org website. Each speaker is limited to a two-minute presentation. Persons who have not registered to speak in advance should raise their hands at the time designated for public testimony and they will be given an opportunity to speak following oral testimonies of the registered speakers. If you require special assistance, auxiliary aid and/or service to participate in this event (i.e. sign language interpreter; interpreter for language other than English, or wheelchair accessibility), please contact Cindy Matsushita at 768-6258 or email your request to [email protected] at least three business days prior to the event.

Transcript of Alii Place, Suite 150 1099 Alakea Street, Honolulu,...

Daniel A. GrabauskasEXECUTIVE DIRECTOR AND CEO

GOVERNMENT AFFAIRS/AUDIT/LEGAL MATTERS

COMMITTEE MEMBERS

Terrence M. Lee CHAIR

Colleen Hanabusa

VICE CHAIR

Michael D. Formby Donald G. Horner

Ivan Lui‐Kwan, Esq.

Government Affairs/Audit/Legal Matters Committee Alii Place, Suite 150

1099 Alakea Street, Honolulu, Hawaii (entrance on Richards Street)

Thursday, January 28, 2016, 8:30 am

Agenda

I. Call to Order by Chair

II. Public Testimony on All Agenda Items

III. Approval of Minutes of the December 17, 2015 Government Affairs/Audit/Legal Matters Committee Meeting

IV. Report on the Independent Financial Audit

V. Executive Session Pursuant to Hawaii Revised Statutes Section 92-4 and Section 92-5(a)(4), the Board may enter into Executive Session to consult with its attorneys on questions and issues on a matter pertaining to the Board’s powers, duties, privileges, immunities and liabilities with regard to the matters set forth in part VI.

VI. Procurement of the Independent Financial Auditor Contract

VII. Adjournment Note: Persons wishing to testify on items listed on the agenda are requested to register by completing a speaker registration form at the meeting or online on the HART section of the www.honolulutransit.org website. Each speaker is limited to a two-minute presentation. Persons who have not registered to speak in advance should raise their hands at the time designated for public testimony and they will be given an opportunity to speak following oral testimonies of the registered speakers. If you require special assistance, auxiliary aid and/or service to participate in this event (i.e. sign language interpreter; interpreter for language other than English, or wheelchair accessibility), please contact Cindy Matsushita at 768-6258 or email your request to [email protected] at least three business days prior to the event.

HONOLULU AUTHORITY FOR RAPIDTRANSPORTATION

HONOLULU RAIL TRANSIT PROJECT

INDEPENDENT FINANCIAL AUDITOR“II” CONTRACT

REQUEST FOR PROPOSALS

RFP-HRT-918006

OCTOBER 26, 2015

QUESTIONS RELATING TO THIS SOLICITATION, CONTACT:

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 1 of 13

INSTRUCTIONS TO OFFERORSTABLE OF CONTENTS

1.0 Overview ................................................................................................................................. 21.1 HRTP Description .................................................................................................................... 21.2 Independent Financial Auditor “II” Contract Description .......................................................... 21.3 Solicitation Timetable............................................................................................................... 3

2.0 Term of the Contract.............................................................................................................. 33.0 Communications ..................................................................................................................... 3

3.1 Inquiries and Requests for Clarification .................................................................................... 33.2 Rules of Contact ....................................................................................................................... 3

4.0 Procurement Process .............................................................................................................. 34.1 Addenda................................................................................................................................... 34.2 Modification or Withdrawal of Proposals................................................................................. 44.3 Receipt and Registration of Proposals ....................................................................................... 44.4 Proposal Confidential During Solicitation Process .................................................................... 44.5 Proposals Property of HART .................................................................................................... 44.6 Priority List .............................................................................................................................. 44.7 Discussions with Offerors......................................................................................................... 44.8 Best and Final Offers ................................................................................................................ 44.9 Rejection of Proposals; Waiver of Informalities and Minor Irregularities .................................. 44.10 Basis of Award ......................................................................................................................... 54.11 Verification of Responsibility of Offeror................................................................................... 54.12 Execution of Contract ............................................................................................................... 54.13 Cancellation of Solicitation....................................................................................................... 64.14 Public Inspection; Segregation of Confidential Information ...................................................... 64.15 Debriefing ................................................................................................................................ 64.16 Protests..................................................................................................................................... 64.17 Commencement of Work.......................................................................................................... 64.18 Suspension and Debarment ....................................................................................................... 74.19 Conflict of Interest and Non-Disclosure Requirements.............................................................. 7

5.0 PREPARATION OF PROPOSALS; SUBMITTAL REQUIREMENTS ............................. 75.1 Proposals Signed by Authorized Personnel ............................................................................... 75.2 Review of RFP ......................................................................................................................... 75.3 Proposal Due Date .................................................................................................................... 75.4 Submittal Location ................................................................................................................... 75.5 Format, and Quantities.............................................................................................................. 85.6 Organization of Proposal .......................................................................................................... 8

6.0 Proposal Requirements, Evaluation Criteria and Evaluation Points.................................... 86.1 Cover Letter ............................................................................................................................. 86.2 Organizational Eligibility (Section 1)........................................................................................ 86.3 Experience and Professional Qualification of the Offeror Relevant to the Contract (Section

2) (35 Points)............................................................................................................................ 96.4 Adequate Qualified Staffing to Complete the Assignment (Section 3) (25 Points) ................... 106.5 Ability to Complete the Work in a Timely Manner (Section 4) (20 Points) .............................. 116.6 Price Proposal (Section 5) (20 Points) ..................................................................................... 11

7.0 Insurance .............................................................................................................................. 128.0 Acceptance of Terms and Conditions................................................................................... 129.0 Disadvantaged Business Enterprise (DBE) Contract Goal ................................................. 1210.0 No Reimbursements.............................................................................................................. 12ITO EXHIBITS ................................................................................................................................... 13ATTACHMENTS................................................................................................................................ 13

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 2 of 13

INSTRUCTIONS TO OFFERORS

1.0 OVERVIEW

The Honolulu Authority for Rapid Transportation (“HART”) is a semi-autonomous agency ofthe City and County of Honolulu (“City”), created pursuant to an amendment to the RevisedCharter of the City and County of Honolulu 1973 (“RCH”) to develop, operate, and maintain theHonolulu Rail Transit Project (“HRTP”). Pursuant to Section 17-111 of the RCH, the accountsand financial status of HART shall be examined annually by a certified public accountant. Theresults of such examination shall be reported to the HART Board of Directors, the City Counciland the Mayor. Accordingly, HART is issuing this Request for Proposals (“RFP”) to seekcompetitive sealed proposals from offerors that are interested in providing independent auditingservices which comply with the requirements of the RCH.

1.1 HRTP Description

The HRTP will provide high-capacity rapid transit service in the travel corridor between EastKapolei and Ala Moana Center. This corridor includes the majority of housing and employmenton O’ahu. The north-south width of the corridor is a maximum of four (4) miles, with thecorridor constrained by the Ko’olau and Wai’anae Mountain Ranges to the north and the PacificOcean to the south.

The HRTP is identified in the Final Environmental Impact Statement (“FEIS”) as the design,construction and operation of a twenty (20) mile grade-separated fixed guideway transit systembetween East Kapolei and Ala Moana Center. All parts of the guideway will be elevated, exceptnear Leeward Community College where it will be at-grade. The system will incorporate steelwheel on steel rail technology. The HRTP includes twenty-one (21) stations, one (1)Maintenance and Storage Facility (MSF), and eighty (80) light metro vehicles and associatedcore systems.

The FEIS was released in June 2010 and a Final Supplemental EIS and Amended Record ofDecision (ROD) were released in September 2013. The FEIS and additional information on theHRTP can be found at: http://honolulutransit.org.

1.2 Independent Financial Auditor “II” Contract Description

The work performed under the contract will be under the direction of HART Board’sGovernment Affairs/Audit/Legal Matters Committee Chair or his/her designee. The selectedcontractor may be required to perform a variety of financial auditing services, includingconducting financial audits of HART’s transactions accounts and books for fiscal years endingJune 30, 2016, June 30, 2017, June 30, 2018, and June 30, 2019, and conducting an examinationof the systems and procedures for accounting, reporting, and operational and internal controls ofHART.

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 3 of 13

1.3 Solicitation Timetable

The following solicitation timetable will be used for this RFP:

ACTIVITY DATEIssue RFP October 26, 2015Deadline for Clarification Requests November 9, 2015Issue Final Addendum November 17, 2015Proposal Due Date December 1, 2015 at 2:00 p.m. HSTAward of Contract (Tentative) January 20, 2015Notice to Proceed (Tentative) February 19, 2015

Any changes to the dates in the above timetable will be made by HART by written addendum.

2.0 TERM OF THE CONTRACT

The term of this Contract shall be for four (4) years commencing from the issuance of the Noticeto Proceed (“NTP”).

3.0 COMMUNICATIONS

3.1 Inquiries and Requests for Clarification

All inquiries and requests for clarification regarding this RFP shall be submitted to the TransitMailbox at the following email address: [email protected] by no later than thedeadline set forth above. All correspondence shall refer to the appropriate RFP number, pagenumber, and section number. See Exhibit 1. Oral interpretations or clarifications will be withoutlegal effect. Only answers to questions issued by a formal written addendum shall be binding onHART. Offerors may not contact HART officials, employees, Board members, orrepresentatives concerning this RFP while the solicitation process is in progress.

3.2 Rules of Contact

Offerors may not contact HART officials, Board members, employees or representativesconcerning this RFP while the solicitation process is in progress. The solicitation process beginswhen the RFP is issued and will be completed with the Award of the Contract. Any contactdetermined to be improper, at the sole discretion of HART, may result in disqualification.

4.0 PROCUREMENT PROCESS

4.1 Addenda

As it deems necessary, HART will issue responses to inquiries or corrections/amendments byway of written addenda issued prior to the Proposal Due Date. Additional background materialor modifications to RFP requirements, where necessary, will be communicated to all offerors bywritten addenda issued by HART.

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 4 of 13

4.2 Modification or Withdrawal of Proposals

Proposals submitted pursuant to this RFP may be modified or withdrawn prior to the ProposalDue Date in accordance with HAR §3-122-16.07.

4.3 Receipt and Registration of Proposals

In accordance with HAR § 3-122-51, proposals and any modifications thereto will be time-stamped upon receipt and held in a secure place by HART until the Proposal Due Date.Proposals and modifications will not be opened publicly, but will be opened in the presence oftwo or more HART officials. Prior to Contract award, proposals will be shown only to membersof the evaluation committee and HART personnel or their designees having legitimate interest inthem.

4.4 Proposal Confidential During Solicitation Process

HART will maintain a confidential process for the duration of this solicitation. All recordsrelated to this procurement, including, but not limited to, proposals, evaluations, priority listprocedures, price proposals, evaluation and selection procedures, and records during theevaluation and selection process, will remain confidential until the Contract award has beenposted by HART in accordance with HAR §3-122-9.01.

4.5 Proposals Property of HART

Proposals will become the property of HART. Copies of each proposal will be retained byHART after the proposal evaluation process.

4.6 Priority List

In accordance with HRS § 103D-303 and HAR § 3-122-53, a priority list will be establishedconsisting of up to three offerors. If more than three acceptable or potentially acceptableproposals have been submitted, the priority list will be limited through evaluation and ranking tothe offerors who submitted the highest-ranked proposals.

4.7 Discussions with Offerors

If discussions with offerors are required to make a selection, they will be conducted inaccordance with HAR § 3-122-53.

4.8 Best and Final Offers

If required, best and final offers will be accepted in accordance with HAR § 3-122-54.

4.9 Rejection of Proposals; Waiver of Informalities and Minor Irregularities

Proposals may be rejected in accordance with HAR § 3-122-97. Furthermore, HART may:a) Reject any or all proposals if such action is in the public interest; and

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 5 of 13

b) Waive informalities and minor irregularities in proposals received.

4.10 Basis of Award

The basis of award of the contract will be the “best value” in accordance with the evaluationcriteria set forth herein.

4.11 Verification of Responsibility of Offeror

The successful offeror shall, within three (3) business days of notification of contract awardfurnish proof of compliance with the requirements of HRS §103D-310(c):

HRS Chapter 237, tax clearance; HRS Chapter 383, unemployment insurance; HRS Chapter 386, workers’ compensation; HRS Chapter 392, temporary disability insurance; HRS Chapter 393, prepaid health care; and One of the following:

(a) Registered and incorporated or organized under the laws of the State ofHawaii, hereafter referred to as a “Hawaii business”; or

(b) Registered to do business in the State of Hawaii, hereinafter referred to as a“compliant non-Hawaii business.”

Vendors may choose to use the Hawaii Compliance Express (HCE), which allows businesses toregister online at http://vendors.ehawaii.gov to acquire a single, printable electronic “Certificateof Vendor Compliance.” The HCE provides current compliance status as of the issuance date.The “Certificate of Vendor Compliance,” indicating that the offeror’s status is compliant with therequirements of HRS section 103D-301(c), will be accepted for both contracting purposes andfinal payment. Vendors that elect to use the new HCE services will be required to pay an annualfee of twelve dollars ($12.00) to the Hawaii Information Consortium, LLC (HIC). Offerorschoosing not to participate in the HCE program will be required to provide the paper certificatesas specified above.

4.12 Execution of Contract

(a) Subsequent to contract award, HART will present the contract to the successfulofferor for execution. The successful offeror shall return the signed contract withinten (10) days from the date upon which the contracted was presented for signature byHART, or within such time as HART may otherwise allow.

(b) The successful offeror shall provide evidence of the required insurance coverageswhen it returns the signed contract to HART.

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 6 of 13

4.13 Cancellation of Solicitation

This solicitation may be cancelled at any time pursuant to the Chief Procurement Officer’sdetermination that cancellation is in the public interest or reasons based on, but not limited to,those set forth in HAR § 3-122-96.

4.14 Public Inspection; Segregation of Confidential Information

Public inspection will be in accordance with HAR §3-122-58. The existing contract file, exceptthose portions the offeror designates in writing to be confidential as trade secrets or otherproprietary data, subject to HAR § 3-122-58(b), will be available for public inspection uponposting of the Award pursuant to HRS § 103D-701.

If a person requests to inspect the portions of an offeror's proposal designated as confidentialpursuant to HAR § 3-122-46(9), the inspection will be subject to written determination byCorporation Counsel for confidentiality in accordance with HRS Chapter 92F. If CorporationCounsel determines in writing that the material designated as confidential is subject todisclosure, the material will be open to public inspection unless the offeror appeals pursuant toHRS § 92F-42(1).

4.15 Debriefing

The purpose of a debriefing is to inform the non-selected offerors of the basis for the sourceselection decision and contract award. A written request for a debriefing shall be made withinthree (3) working days after the posting of the award of the contract. To the extent practicable,debriefing shall be held by HART within seven (7) working days of the request for thedebriefing, provided the Chief Procurement Officer may determine whether to conductindividual or combined debriefings.

4.16 Protests

Protests shall be made in accordance with HRS § 103D-701 and HAR § 3-122-60. Any protestby a non-selected offeror pursuant to section HRS §103D-701 following a debriefing shall befiled in writing within five (5) working days after the date upon which the debriefing wasconducted.

Offerors are hereby notified of their right to appeal to the FTA pursuant to FTA C 4220.1FChapter VII, Section 1.b.

4.17 Commencement of Work

Work shall not commence until: (a) the contract has been executed; (b) the Chief ProcurementOfficer has certified the availability of funds; and (c) and written Notice to Proceed has beenissued.

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 7 of 13

4.18 Suspension and Debarment

In accordance with 2 CFR §1200 the Offeror is required to verify that none of the offeror’sprincipals, as defined in 2 CFR §180.995, or affiliates, as defined at 2 CFR §180.905, areexcluded or disqualified as defined at 2 CFR §§180-945 and 180.935. The offeror is required tocomply with 2 CFR §1200, Subpart C, and must include the requirements to comply with 2 CFR§1200, Subpart C, in any lower tier covered transaction it enters into. By signing and submittingits proposal, the offeror certifies to these requirements.

4.19 Conflict of Interest and Non-Disclosure Requirements

A contractor who was or is being paid for developing or preparing work specifications shall beprecluded from submitting an offer or receiving a contract for that particular solicitation inaccordance with HRS § 103D-405(d) and HAR § 3-122-13(e).

5.0 PREPARATION OF PROPOSALS; SUBMITTAL REQUIREMENTS

5.1 Proposals Signed by Authorized Personnel

Each proposal shall be signed in ink by the person legally authorized to do so on behalf of theentity submitting the and pursuant to proof of the authorized person’s authority to bind the entity.

5.2 Review of RFP

It is the responsibility of all offerors to examine the entire RFP and to seek clarification of anyrequirement that may not be clear and to check all responses for accuracy before submitting apProposal. Negligence in preparing a proposal confers no right of withdrawal after the ProposalDue Date.

5.3 Proposal Due Date

As specified above, proposals must be submitted to HART by no later than 2:00 p.m. HST onDecember 1, 2015. The proposals shall be enclosed in sealed containers, marked clearly withthe RFP number. Late submittals will not be accepted. It is the responsibility of the offeror toensure that its proposal is delivered at the location indicated below by the Proposal Due Date.

5.4 Submittal Location

Proposals shall be delivered to the following address:

HART Chief Procurement OfficerAttn: Procurement DivisionRFP-HRT-918006Honolulu Authority for Rapid Transportation1099 Alakea Street, Suite 1700Honolulu, Hawaii 96813

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 8 of 13

Submittals by facsimiles are not acceptable and shall not be considered.

5.5 Format, and Quantities

See ITO Exhibit 2 for Proposal format. Offerors shall provide one (1) original and four (4)copies of the proposal and appendices thereto. The signed original copy is to be identified as the“Original” on the cover and marked as “Copy 1 of 5.” All copies shall be provided in loose-leaf,3-ring binders, with the three appendices placed in a separate 3-ring binder. Each copy should beidentified on the cover(s) as “Copy # of 5.” Proposals are to be written in English, minimum 12-point font, and printed on 8-1/2” x 11” paper; any larger sheets should be folded to that size.Pages are to be consecutively numbered.

5.6 Organization of Proposal

Offerors are to follow the outline format provided in Exhibit 2 when preparing and organizingtheir proposals. All exhibits identified in ITO Exhibit 2 shall be submitted with the proposal.Specific content requirements for each section of the proposal and the corresponding evaluationpoints are described below.

6.0 PROPOSAL REQUIREMENTS, EVALUATION CRITERIA AND EVALUATIONPOINTS

6.1 Cover Letter

Offerors shall provide a 1-2 page letter indicating their desire to be considered for the RFP andstating the official names and roles of all Principal Participants, and known subcontractors.Offerors shall identify a single point of contact and the address, telephone and fax numbers, andemail address to which questions should be directed. Authorized representatives of the offeror'sorganization shall sign the letter. ITO Exhibits 3 and 4 shall be attached to the proposal coverletter.

6.2 Organizational Eligibility (Section 1)

Requirements and information to be provided in Section 1 of the Proposal are:

(a) Organizational Information, as identified on ITO Exhibit 5;

(b) If a partnership or corporation, submit ITO Exhibit 6;

(c) Principal Participant certification on ITO Exhibit 7 for each Principal Participantcovering the last five years;

(d) If a Joint Venture, Limited Liability Company, or Partnership:(1) Identity of the lead Principal Participant of the entity, if any;(2) Indicate the equity share percentage held by each member;(3) Include an express statement from each of the equity members of the entity to

confirm their joint and several liability; and

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 9 of 13

(4) Identify full details of the organizational structure.

(e) Certificate Regarding Lobbying on ITO Exhibit 11;

(f) Bidder Registration Form on ITO Exhibit 14; and

(g) Requirements and information to be provided in Appendix A to the Proposal:(1) Notarized Power(s) of Attorney for each Principal Participant indicating the

authority of the Principal Participant’s representative to sign for that PrincipalParticipant;

(2) Notarized Power(s) of Attorney for each Principal Participant indicating theauthority of the offeror’s designated point of contact to sign documents for and onbehalf of the offeror’s organization; and

(3) Alternatively, in lieu of the Powers of Attorney, the offeror may submit certifiedoriginal corporate resolutions for each Principal Participant and the offeror (asappropriate) indicating the authority of the Principal Participant’s and/or offeror’sdesignated point of contact to sign documents for and on behalf of the PrincipalParticipant and/or offeror’s organization. Such resolutions must be signed by theSecretary of the corporation and contain a corporate seal or notarization.

6.3 Experience and Professional Qualification of the Offeror Relevant to the Contract(Section 2) (35 Points)

(a) Experience and professional qualifications in performing similar financial audits ofgovernmental units:(1) Background and experience of the offeror. Provide description and background

information of the offeror, demonstrating that the offeror is qualified to performthe financial services requested. Information should include:(A) Name of the offeror, the address of the principal place of business in

Hawaii, and the length of time the offeror has been doing business inHawaii.

(B) The average number of Hawaii employees in the governmental audit sectionover the past three (3) years.

(C) Describe pertinent and unique resources of the offeror that the project teammay utilize for the proposed work (i.e., members with specialized expertise,national/international offices, expert panels and resources, databases, etc).

(D) Briefly describe the quality control system of the offeror.(E) Provide a copy of the latest external quality review of the offeror and

statement whether that review included a review of specific governmentalengagements.

(F) Disclose whether any Federal or state desk or field reviews have beenperformed on any of the offeror’s government audits during the past three(3) years.

(G) Provide any information on any disciplinary action taken or pending againstthe offeror during the past three (3) years with state regulatory bodies orprofessional organizations.

(H) Provide a copy of the latest audit reports of a governmental entity.

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 10 of 13

(2) Financial stability of the offeror:(A) The offeror must provide a credit reference(s).(B) The offeror shall provide its capability to meet the requirements of the

Contract specifically with respect to cash and working capital.(C) A copy of the Offeror’s most current balance sheet certified by the Offeror

to be a “Certified True Copy” shall be enclosed in Section II. If the Offerorwishes for such data to remain confidential, such pages containing thefinancial data shall be clearly marked “CONFIDENTIAL” on every pagethat contains confidential data.

(3) Identification of any Potential Conflicts of Interest:(A) The offeror shall disclose and provide what may be or may be perceived as a

potential conflict of interest, the nature of the potential conflict, andwhether it can be minimized or mitigated to safeguard the independence ofthe audits.

(B) The offeror shall provide an affirmative statement if there are no potentialconflicts of interest.

(b) Exhibits:(1) Submit Experience on ITO Exhibit 8.(2) Submit Past Performance on ITO Exhibit 10.

6.4 Adequate Qualified Staffing to Complete the Assignment (Section 3) (25 Points)

(a) Proposed Auditing Team. The offeror will be evaluated for the proposed auditingteam’s qualifications to perform the audit work. Please provide the following:(1) State the total number of professionals on the offeror’s proposed audit team and

each person’s name. Identify each person’s current standing as a certified publicaccountant in Hawaii and the credential to perform government financial audits.

(2) Specify the proposed scope of work and number of work hours for HART’sannual financial audit and total number of hours to be worked on the annualfinancial audit by all team members.

(3) Identify the person who shall serve as the Project Manager in charge ofcoordinating the engagement and list qualifications to serve in that capacity.

(4) Identify the person who shall serve as designated alternate to the Project Managerand list qualifications to serve in that capacity.

(5) Identify a person who shall serve as the primary contact person with HART. Theperson may be the Project Manager or designated alternate, but if another personis selected, that person’s qualifications to serve in this capacity shall be listed.

(6) The proposed Project Manager and alternate must be employed by the offeror asfull-time certified public accountants, who have been licensed to practice publicaccountancy in the State of Hawaii, and possess a current permit for the same.The proposal shall state the length of time the Project Manager and alternate havebeen licensed to practice public accountancy in the State of Hawaii and shallaffirm that the permit to practice public accountancy in the State of Hawaii will beheld for the term of the contract and that the Project Manager and alternate will beassigned to the offeror’s Oahu office for the contract.

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 11 of 13

(7) The offeror’s description of the qualifications of the proposed Project Manager’sand alternate’s experience shall include a listing of the following personallycompleted or directly supervised audit engagement:i) Limited general audits of governmental propriety and/or enterprise funds in

conformance with generally accepted government auditing standards,examining the financial statements, internal control structure, and compliancewith laws and regulations pertaining to the use of funds.

ii) Single audits of federal financial assistance programs of a government agencyin conformance with the Federal Single Audit Act of 1984 and pertinent U.S.Office of Management and Budget (OMB) Circulars.

iii) Limited general audits of governmental entities in conformance with generallyaccepted government auditing standards that required a total of at least onethousand (1,000) work hours which may be the same or similar to (i) and (ii)above.

iv) For each of the qualifying audit engagements noted in (i), (ii) and (iii),reference contract information, report date, the number of professionals in theaudit work team, and whether the report was personally completed by thesubject person, or completed under the direct supervision of the subjectperson.

v) For evaluation purposes only, copies of qualifying reports for (i), (ii) and (iii)shall be provided for review with the submitted proposal.

(8) For each person who shall serve as an audit team member, list the role assignedand qualifications to service in the capacity.

(b) Submit Key Personnel Information on ITO Exhibit 12.

6.5 Ability to Complete the Work in a Timely Manner (Section 4) (20 Points)

Offerors shall provide a preliminary work plan addressing the offeror’s proposed approach forthe following:

(a) The extent to which the proposal addresses and satisfies the scope of the work.

(b) All work elements are addressed and resources necessary to complete the scope ofwork.

(c) Access the offeror’s ability to complete the work in a timely manner.

6.6 Price Proposal (Section 5) (20 Points)

(a) Provide pricing in all the required fields in ITO Exhibit 9.

(b) Proposals shall include any and all applicable taxes.

(c) The Grand Total price of the proposal shall be considered the cost factor forevaluation purposes under HAR § 3-122-52(d).

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 12 of 13

(d) Submit Certificate of Current Cost or Pricing Data on ITO Exhibit 13.

7.0 INSURANCE

Offerors shall obtain and maintain insurance in the amounts and kinds specified in the GeneralTerms and Conditions of Professional Services, as may be amended by the Special Provisions.

8.0 ACCEPTANCE OF TERMS AND CONDITIONS

By submitting a proposal, an offeror expressly agrees to all of the terms, conditions, provisions,and requirements set forth in this RFP and the General Terms and Conditions of ProfessionalServices.

9.0 DISADVANTAGED BUSINESS ENTERPRISE (DBE) CONTRACT GOAL

HART has established an overall DBE goal of 13.00% for the duration of this contract and aseparate contract goal has not been established for this procurement.

Reports to HART. The successful offeror shall report its DBE participation obtained throughrace-neutral means throughout the period of performance. The successful offeror shall submitthe “DBE PARTICIPATION REPORT” reflecting payments made by the Contractor to DBEsubcontractors in accordance with Attachment A, Section 1.6(p)-(r) of the General Conditions.Payments to the Contractor will not be processed if the DBE PARTICIPATION REPORT is notproperly completed and attached. The DBE PARTICIPATION REPORT shall be prepared inthe format set forth in Attachment 1.6(a).

10.0 NO REIMBURSEMENTS

HART will not provide any reimbursement for the cost of developing or submitting a proposal inresponse to this RFP.

RFP-HRT-918006 Instructions to OfferorsIndependent Financial Auditor “II” Contract Page 13 of 13

ITO EXHIBITSThe following exhibits are attached hereto and incorporated herein by reference:

Exhibit 1 - Offeror's Clarification RequestExhibit 2 - Proposal FormatExhibit 3 - Acknowledgment of Receipt Request for Proposals, Addenda and Responses

to Offeror's Clarification RequestsExhibit 4 - Proposal FormExhibit 5 - Offeror's Organization InformationExhibit 6 - Information Requested of Partnerships and CorporationsExhibit 7 - Principal Participant CertificationExhibit 8 - ExperienceExhibit 9 - Price Proposal FormExhibit 10 - Past PerformancesExhibit 11 - Certification Regarding LobbyingExhibit 12 - Key Personnel InformationExhibit 13 - Certificate of Current Cost or Pricing DataExhibit 14 - Bidder Registration Form

ATTACHMENTS Sample Agreement

Special Provisions

HART General Terms and Conditions for Professional Services (v8/2015)

Financial Statements and Independent Auditor’s Report

Honolulu Authority for Rapid Transportation

(a component unit of the City and County of Honolulu) June 30, 2015 and 2014

A Hawaii Limited Liability Partnership

1 1003 Bishop Street Suite 2400 Honolulu, HI 96813 Telephone: 808-526-2255 Fax: 808-536-5817 www.kmhllp.com

January 21, 2016 To the Board of Directors Honolulu Authority for Rapid Transportation City and County of Honolulu Ladies and Gentlemen: We have completed our financial audit of the Honolulu Authority for Rapid Transportation, a component unit of the City and County of Honolulu, (HART) as of and for the fiscal year ended June 30, 2015. The audit was performed in accordance with our agreement dated June 22, 2015. Objective of the audit The primary purpose of our audit was to form an opinion on the fairness of the presentation of HART’s financial statements as of and for the fiscal year ended June 30, 2015

Scope of the audit Our audit was performed in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. The scope of our audit included an examination of the transactions and accounting records of HART for the fiscal year ended June 30, 2015. Organization of the report This report is organized into five parts:

PART I. FINANCIAL STATEMENTS

PART II. REQUIRED SUPPLEMENTARY INFORMATION

PART III. REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON

COMPLIANCE AND OTHER MATTERS

PART IV. SCHEDULE OF FINDINGS

PART V. RESPONSE OF THE AFFECTED AGENCY

At this time, we wish to thank HART’s personnel for their cooperation and assistance extended to us during our audit. We will be happy to respond to any questions that you may have on this report.

Very truly yours,

KMH LLP Honolulu Hawaii January 21, 2016

2

Contents Page PART I FINANCIAL STATEMENTS

Independent Auditor’s Report 4 Management's Discussion and Analysis 6 Basic Financial Statements

Statements of Net Position 12 Statements of Revenues, Expenses and Changes in Net Position 13 Statements of Cash Flows 14

Notes to Financial Statements 16 PART II REQUIRED SUPPLEMENTARY INFORMATION

Schedule of the HART’s Proportionate Share of the Net Pension Liability 42 Schedule of the HART’s Contributions 43 Schedule of Funding Progress for the Hawaii Employer-Union

Health Benefits Trust Fund 44 PART III REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

AND ON COMPLIANCE AND OTHER MATTERS

Independent Auditor’s Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 46

PART IV SCHEDULE OF FINDINGS 48 PART V RESPONSE OF THE AFFECTED AGENCY 50

3

PART I FINANCIAL STATEMENTS

A Hawaii Limited Liability Partnership

4 1003 Bishop Street Suite 2400 Honolulu, HI 96813 Telephone: 808-526-2255 Fax: 808-536-5817 www.kmhllp.com

Independent Auditor’s Report To the Board of Directors Honolulu Authority for Rapid Transportation City and County of Honolulu Report on the Financial Statements

We have audited the accompanying financial statements of the Honolulu Authority for Rapid Transportation (HART), a component unit of the City and County of Honolulu, as of and for the years ended June 30, 2015 and 2014, and the related notes to the financial statements, which collectively comprise the HART’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Honolulu Authority for Rapid Transportation, as of June 30, 2015 and 2014, and the changes in its financial position and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

5

Emphasis of a Matter

As discussed in Note A to the basic financial statements, in 2015 the HART adopted Governmental Accounting Standards Board (GASB) Statements no. 68 (GASB 68), Accounting and Reporting for Pensions (an amendment of GASB Statement No. 27) and GASB Statement No. 71 (GASB 71), Pension Transition for Contributions Made subsequent to the Measurement Date, an Amendment of GASB Statement No. 68. As a result of adopting these standards and management’s determination that the restatement of the basic financial statements as of and for the year ended June 30, 2014 is not practical, the HART has elected to restate beginning net position for fiscal year ended June 30, 2015. Our opinion is not modified with respect to this matter. Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis on pages 6 through 11 and the schedule of the HART’s proportionate share of the net pension liability, schedule of HART’s contributions and schedule of funding progress for the Hawaii Employer-Union Health Benefits Trust Fund on pages 42, 43, and 44, respectively be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated January 21, 2016 on our consideration of the HART's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering HART’s internal control over financial reporting and compliance.

KMH LLP Honolulu, HI January 21, 2016

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

MANAGEMENT’S DISCUSSION AND ANALYSIS

June 30, 2015 and 2014

6

The Honolulu Authority for Rapid Transportation (HART) is a semi-autonomous government unit of the City and County of Honolulu (City), which came into being on July 1, 2011 pursuant to a 2010 amendment to the Revised Charter of the City and County of Honolulu (RCH). HART consists of a board of directors (Board), executive director, and staff. HART is authorized under the RCH to “develop, operate, maintain and expand the city fixed guideway system.” The Honolulu Rail Transit Project (the Project) consists of design and construction of a 20-mile, grade-separated fixed rail system from East Kapolei to the Ala Moana Center in Honolulu, Hawaii. The Project begins in East Kapolei, proceeds to the University of Hawaii at West Oahu, then turns east to Pearl Harbor and the Honolulu International Airport, and ends at Kona Street adjacent to the Ala Moana Center. The Project will operate in an exclusive right-of-way and will be elevated except for a 0.6-mile, at-grade section near Leeward Community College. The Project includes 21 transit stations; a maintenance and storage facility; 80 light metro fully automated (driverless) rail vehicles and associated core systems; and four park-and-ride facilities at several locations. This section presents the management’s discussion and analysis of HART’s financial condition and activities for the fiscal years ended June 30, 2015 and 2014. This summary is designed to provide an introduction to the financial statements and the financial condition of HART. This information should be read in conjunction with the financial statements. Prior to July 1, 2011, the financial position and results of operations of the Project were reported as a governmental fund in the City’s Comprehensive Annual Financial Reports. Overview of the Financial Statements The financial statements are presented using the economic resources measurement focus and the accrual basis of accounting, whereby revenues and expenses are recognized in the period earned or incurred. The basic financial statements include statements of net position, statements of revenues, expenses and changes in net position, statements of cash flows, and notes to the financial statements. The statements of net position present the resources and obligations of HART at June 30, 2015 and 2014 respectively. The statement of revenues, expenses and changes in net position present information showing how HART’s net position changed during the past two fiscal years. The statements of cash flows present changes in cash and cash equivalents resulting from operating, investing, capital and related financing activities, and non-capital financing activities. The notes to the financial statements provide required disclosures and other information necessary for the fair presentation of the financial statements. The notes detail information about HART’s significant accounting policies, account balances, related party transactions, employee benefit plans, commitments, contingencies, and other significant events. Supplementary information on pension and post-employment benefits is also included.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

MANAGEMENT’S DISCUSSION AND ANALYSIS

June 30, 2015 and 2014

7

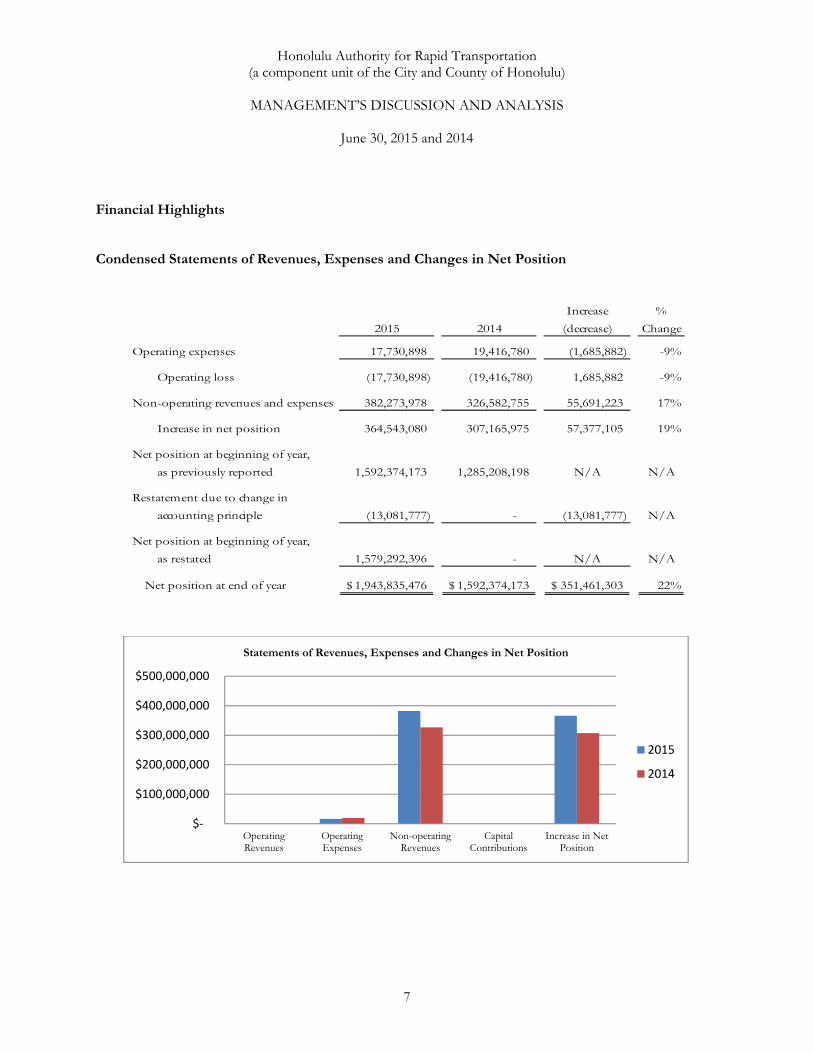

Financial Highlights Condensed Statements of Revenues, Expenses and Changes in Net Position

Increase %

2015 2014 (decrease) Change

Operating expenses 17,730,898 19,416,780 (1,685,882) -9%

Operating loss (17,730,898) (19,416,780) 1,685,882 -9%

Non-operating revenues and expenses 382,273,978 326,582,755 55,691,223 17%

Increase in net position 364,543,080 307,165,975 57,377,105 19%

Net position at beginning of year,

as previously reported 1,592,374,173 1,285,208,198 N/A N/A

Restatement due to change in

accounting principle (13,081,777) - (13,081,777) N/A

Net position at beginning of year,

as restated 1,579,292,396 - N/A N/A

Net position at end of year 1,943,835,476$ 1,592,374,173$ 351,461,303$ 22%

$‐

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

OperatingRevenues

OperatingExpenses

Non-operatingRevenues

CapitalContributions

Increase in NetPosition

Statements of Revenues, Expenses and Changes in Net Position

2015

2014

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

MANAGEMENT’S DISCUSSION AND ANALYSIS

June 30, 2015 and 2014

8

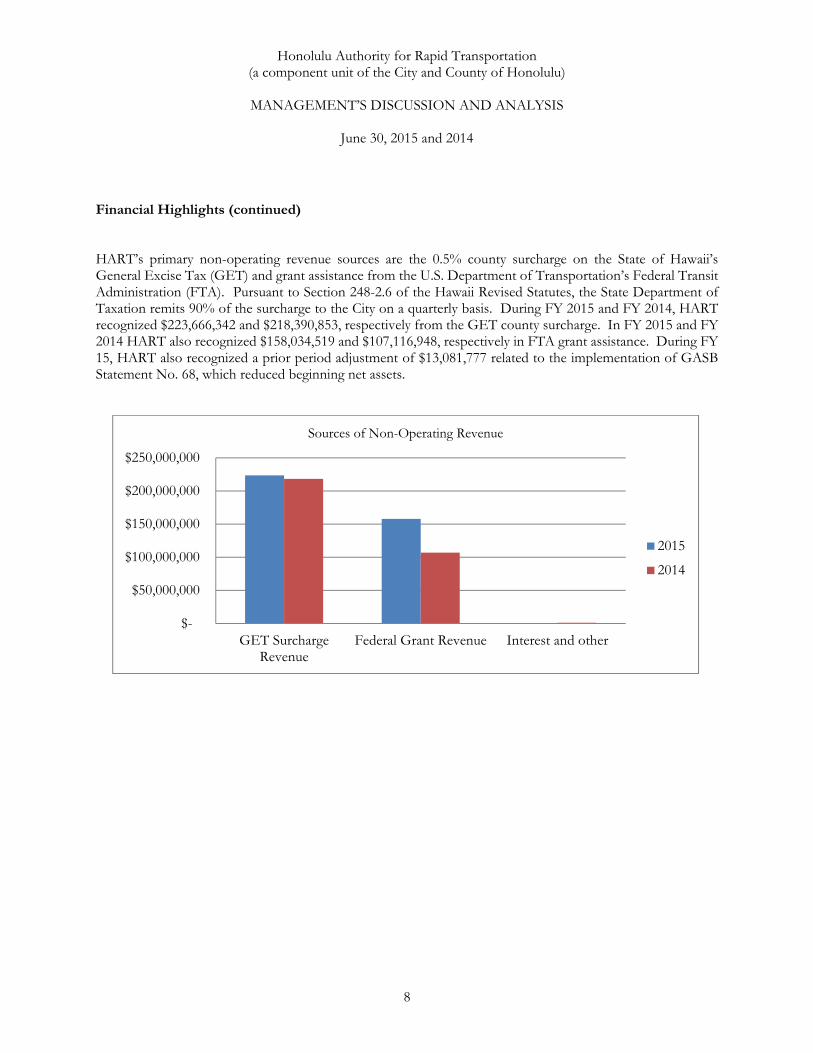

Financial Highlights (continued) HART’s primary non-operating revenue sources are the 0.5% county surcharge on the State of Hawaii’s General Excise Tax (GET) and grant assistance from the U.S. Department of Transportation’s Federal Transit Administration (FTA). Pursuant to Section 248-2.6 of the Hawaii Revised Statutes, the State Department of Taxation remits 90% of the surcharge to the City on a quarterly basis. During FY 2015 and FY 2014, HART recognized $223,666,342 and $218,390,853, respectively from the GET county surcharge. In FY 2015 and FY 2014 HART also recognized $158,034,519 and $107,116,948, respectively in FTA grant assistance. During FY 15, HART also recognized a prior period adjustment of $13,081,777 related to the implementation of GASB Statement No. 68, which reduced beginning net assets.

$-

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

GET SurchargeRevenue

Federal Grant Revenue Interest and other

Sources of Non-Operating Revenue

2015

2014

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

MANAGEMENT’S DISCUSSION AND ANALYSIS

June 30, 2015 and 2014

9

Financial Highlights (continued) Condensed Statements of Net Position

Increase %

2015 2014 (decrease) Change

Assets

Current assetsCash and cash equivalents 293,010,823$ 441,011,319$ (148,000,496)$ -34%Receivables 133,672,108 129,991,834 3,680,274 3%Prepaid expenses 27,800,740 1,217,390 26,583,350 2184%Capital assets, net 1,708,618,647 1,184,636,596 523,982,051 44%

DEFERRED OUTFLOWS OF RESOURCES 2,913,149 - 2,913,149 N/A

Total assets 2,166,015,467$ 1,756,857,139$ 409,158,328 23%

LiabilitiesCurrent liabilities 171,750,169 151,431,453$ 20,318,716$ 13%Other long-term liabilities - noncurrent 48,757,933 13,051,513 35,706,420 274%DEFERRED INFLOWS OF RESOURCES 1,671,889 - 1,671,889 N/A

Total liabilities 222,179,991 164,482,966 57,697,025 35%

Net position 1,943,835,476 1,592,374,173 351,461,303 22%

Total liabilities and net position 2,166,015,467$ 1,756,857,139$ 409,158,328 23%

$-

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

$1,400,000,000

$1,600,000,000

$1,800,000,000

Current Assets Capital Assets, net Current Liabilities Other Long TermLiabilities

Statements of Net Position

2015

2014

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

MANAGEMENT’S DISCUSSION AND ANALYSIS

June 30, 2015 and 2014

10

Financial Highlights (continued) Total assets and deferred outflows at year-end FY 2015 and FY 2014 were $2,166,015,467 and $1,756,857,139, respectively. Total liabilities and deferred inflows at year-end FY 2015 and FY 2014 were $222,179,991 and $164,482,966, respectively. Net position increased by $364,543,080 primarily due to intergovernmental revenues and federal grants. The Project has executed $2,486,920,607 in contracts since October 2009 to date for the planning, design, and construction of the Project. This amounts to 56.7% of the anticipated total project cost. The Project will affect an estimated 224 parcels of real property. As of June 30, 2015, HART has acquired title to or use of 120 parcels of real property. As of June 30, 2015, 9.3% of the utilities have been relocated. Utility relocations are performed by the respective companies owning the equipment. Overall design progress is 85.7% based on the weighted average progress of the individual final design contracts and the design levels of effort of the Design-Build (DB) and Design-Build-Operate-Maintain (DBOM) construction contracts. The construction of the west guideway aerial structure from East Kapolei Station to Leeward Community College (LCC) is well underway as part of the West Oahu/Farrington Highway (WOFH) Guideway design-build project. Additionally, the Kamehameha Highway (KHG) Guideway design-build project continues with wet and dry utility relocations as well as roadway widening work in preparation for the production drilled shaft and segmented guideway construction from LCC to Aloha Stadium. Over three miles of the elevated guideway between east Kapolei and Waipahu has been completed with more than 180 columns built and nearly 1,600 guideway segments erected. The balanced cantilever construction work over the westbound side of the H-1 Freeway for the West Oahu Farrington Highway segment and the elevated rail guideway over the Fort Weaver Road overpass have been completed. The design-build construction of the HART Maintenance and Storage Facility (MSF) is progressing as planned with substantial completion expected in April 2016.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

MANAGEMENT’S DISCUSSION AND ANALYSIS

June 30, 2015 and 2014

11

Financial Highlights (continued) Capital Assets and Long-Term Debt As of the end of FY 2015, HART had $1,708 million invested in capital assets. This amount represents an increase (including additions and deductions) of approximately $524 million, or 44%, over last year.

2015 2014

Equipment and machinery 68,778$ 86,500$ Land 91,102,437 64,768,559 Construction in progress 1,617,447,432 1,119,781,537

Total 1,708,618,647$ 1,184,636,596$

HART has not issued any long-term bonds. Additional information on HART’s capital assets and long-term liabilities can be found in note D to the financial statements. Risks On June 29, 2012, HART submitted the City’s request to the FTA for a Full Funding Grant Agreement (FFGA) which was awarded on December 19, 2012. The maximum Federal New Starts financial contribution under the FFGA is $1.55 billion for the Project; however the annual appropriation amounts may be reduced and appropriated over a longer period than planned. The project faces the normal risks associated with a multi-year, major construction project that includes unanticipated construction delays, cost inflation over the period of construction, and economic downturns that impact revenues. See Notes J and L for a discussion on pending litigation and the liquidity risk to the project. Request for Information This financial report is designed to provide a general overview of HART’s finances. Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to the Honolulu Authority for Rapid Transportation, 1099 Alakea Street, Suite 1700, Honolulu, Hawaii 96813.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

STATEMENTS OF NET POSITION

June 30, 2015 and 2014

12

2015 2014

ASSETSCurrent assets:

Cash & cash equivalents 293,010,823$ 441,011,319$ Receivables 133,672,108 129,991,834 Prepaid expenses 27,800,740 1,217,390

Total current assets 454,483,671 572,220,543

Capital assets:Equipment and machinery 171,540 171,540 Accumulated depreciation (102,762) (85,040)

68,778 86,500 Land 91,102,437 64,768,559 Construction work in progress 1,617,447,432 1,119,781,537

Capital assets, net 1,708,618,647 1,184,636,596

Total assets 2,163,102,318 1,756,857,139

DEFERRED OUTFLOWS OF RESOURCES 2,913,149 -

Total assets and deferred outflows of resources 2,166,015,467$ 1,756,857,139$

LIABILITIESCurrent liabilities:

Accounts payable 137,921,888$ 115,552,902$ Accrued liabilities 373,203 392,537 Other long-term liabilities 33,455,078 35,486,014

Total current liabilities 171,750,169 151,431,453

Other long-term liabilities - noncurrent 48,757,933 13,051,513 Total liabilities 220,508,102 164,482,966

DEFERRED INFLOWS OF RESOURCES 1,671,889 -

Total liabilities and deferred inflows of resources 222,179,991 164,482,966

NET POSITIONNet investment in capital assets 1,506,183,913 1,069,158,564 Unrestricted 437,651,563 523,215,609

Total net position 1,943,835,476 1,592,374,173

Total liabilities, deferred inflows of resources, and net position 2,166,015,467$ 1,756,857,139$

The accompanying notes are an integral part of these financial statements.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

STATEMENTS OF REVENUES, EXPENSES AND CHANGES IN NET POSITIION

Years ended June 30, 2015 and 2014

13

2015 2014OPERATING EXPENSES

Administration and general 11,721,853$ 12,015,351$ Fringe benefits 4,383,253 3,835,579 Insurance 1,092,851 1,909,200 Contractual services 357,133 1,145,619 Utilities 83,590 221,445 Materials and supplies 69,422 245,541 Depreciation 17,722 36,622 Maintenance 5,074 7,423

Total operating expenses 17,730,898 19,416,780

Operating loss (17,730,898) (19,416,780)

NON-OPERATING REVENUES AND EXPENSESIntergovernmental revenues:

County surcharge 223,666,342 218,390,853 Federal grants 158,034,519 107,116,948

Interest income 208,245 298,748 Other revenue 364,872 776,206

Total nonoperating revenues 382,273,978 326,582,755

Change in net position 364,543,080 307,165,975

Net position at beginning of year, as previously reported 1,592,374,173 1,285,208,198

Restatement due to change in accounting principle (13,081,777) -

Net position at beginning of year, as restated 1,579,292,396 -

Net position at end of year 1,943,835,476$ 1,592,374,173$

The accompanying notes are an integral part of these financial statements.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

STATEMENTS OF CASH FLOWS

Years ended June 30, 2015 and 2014

14

2015 2014

Cash flows from operating activitiesCash payments to suppliers for goods and services (11,028,378)$ (10,594,843)$ Cash payments to employees (12,301,128) (11,566,726)

Net cash used in operating activities (23,329,506) (22,161,569)

Cash flows from noncapital financing activitiesIntergovernmental revenues 376,704,770 332,188,472

Net cash provided by noncapital financing activities 376,704,770 332,188,472

Cash flows from capital and related financing activitiesAcquisition and construction of capital assets (501,584,005) (263,024,043)

Net cash used in capital and related financing activities (501,584,005) (263,024,043)

Cash flows from investing activitiesInterest on cash and cash equivalents 208,245 298,748

Net cash provided by investing activities 208,245 298,748

NET (DECREASE) INCREASEIN CASH AND CASH EQUIVALENTS (148,000,496) 47,301,608

Cash and cash equivalents at beginning of year 441,011,319 393,709,711

Cash and cash equivalents at end of year 293,010,823$ 441,011,319$

The accompanying notes are an integral part of these financial statements.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

STATEMENTS OF CASH FLOWS (continued)

Years ended June 30, 2015 and 2014

15

2015 2014

Reconciliation of operating loss to net cash used in operating activitiesOperating loss (17,730,898)$ (19,416,780)$ Adjustments to reconcile operating loss to

net cash used in operating activitiesDepreciation 17,722 36,622 Changes in assets and liabilities

Increase in deferred outflows of resources (1,311,007) - Increase in deferred inflows of resources 1,671,889 - Decrease (increase) in receivables 1,680,689 (1,627,203) (Increase) decrease in prepaid expenses (26,583,350) 1,848,984 (Decrease) in accounts payable (46,782) (262,808) (Decrease) increase in accrued liabilities (19,334) 31,119 Increase (decrease) in other liabilities 18,991,565 (2,771,503)

Total adjustments (5,598,608) (2,744,789)

Net cash used in operating activities (23,329,506)$ (22,161,569)$

Non-cash capital financing activities: During the year ended June 30, 2015 and 2014, HART accrued additional costs as construction in progress of $22,415,768 and $63,684,666, respectively. The accompanying notes are an integral part of these financial statements.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

NOTES TO FINANCIAL STATEMENTS

June 30, 2015 and 2014

16

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

1. Operations The Revised Charter of the City and County of Honolulu authorizes the Honolulu Authority for Rapid Transportation (HART) to develop, operate, maintain and expand the city fixed guideway system. HART is a semi-autonomous government unit of the City and County of Honolulu (City). It is a component unit of the City. HART is in the process of developing the rail transit system and has not begun revenue operations.

2. Financial Statement Presentation

The accounting policies of HART conform to accounting principles generally accepted in the United States of America as applicable to enterprise activities of governmental units, as promulgated by the Government Accounting Standards Board (GASB). Recently Adopted Accounting Pronouncements Effective July 1, 2014 the HART implemented Governmental Accounting Standards Board (GASB) Statement No. 68 (GASB 68), Accounting and Reporting for Pensions (an amendment of GASB Statement No. 27) and GASB Statement No. 71 (GASB 71), Pension Transition for Contributions Made Subsequent to the Measurement Date, an Amendment of GASB Statement No. 68. GASB 68 establishes standards of accounting and financial reporting for defined benefit pensions and defined contribution pensions provided to the employees of state and local government employers through pension plans that are administered through trusts or equivalent arrangements in which:

Contributions from employers and nonemployer contributing entities to the pension plan and

earnings on those contributions are irrevocable. Pension plan assets are dedicated to providing pensions to plan members in accordance with

the benefit terms. Pension plan assets are legally protected from the creditors of employer, nonemployee

contributing entities, and the pension plan administrator. If the plan is a defined benefit pension plan, plan assets also are legally protected from creditors of the plan members.

GASB 68 replaces the requirements of GASB Statement No. 27 (GASB 27), Accounting for Pensions by State and Local Governmental Employers, as well as the requirements of GASB Statement No. 50 (GASB 50), Pension Disclosures, as they related to pensions that are provided through pension plans administered as trusts or equivalent arrangements that meet certain criteria. The requirements of GASB 27 and 50 remain applicable for pensions that are not covered by the scope of GASB 68.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

NOTES TO FINANCIAL STATEMENTS (continued)

June 30, 2015 and 2014

17

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

2. Financial Statement Presentation (continued) GASB 71 is required to be implemented simultaneously with GASB 68 and amends the requirement related to certain pension contributions made to defined benefit pension plans prior to implementation of GASB 68 by employers and nonemployer contributing entities.

As permitted in GASB 68, management determined that the restatement of fiscal year 2014 is not practical; the cumulative effect of adopting GASB 68 related to prior fiscal years has been recorded as a restatement adjustment to beginning net position for the fiscal year ended June 30, 2015. The adoption of GASB 68 and 71 has resulted in the restatement of the HART’s fiscal year 2015 beginning net position by $(14,683,919) and $1,602,142 related to changes in net pension liability and deferred outflows, respectively, from prior fiscal years. See Note G for further information. Recently Issued Accounting Pronouncements In February 2015, GASB issued Statement No. 72, Fair Value Measurement and Application. This Statement enhances the comparability of financial statements among governments by requiring measurement of certain assets and liabilities at fair value using a consistent and more detailed definition of fair value and accepted valuation techniques. The provisions of this Statement are effective for periods beginning after June 15, 2015. The HART has not yet determined the effect this Statement will have on its financial statements. In June 2015, GASB issued Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions, replacing Statement No. 45 Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions, as amended, and Statement No. 57 OPEB Measurements by Agent Employers and Agent Multiple-Employer Plans, for OPEB. This statement establishes new accounting and financial reporting requirements for OPEB plans. This Statement requires governments providing defined benefit OPEB plans to recognize their long-term obligation for OPEB as a liability for the first time, and to more comprehensively and comparably measure the annual cost of OPEB benefits. The provisions of this Statement are effective for periods beginning after June 15, 2017. The HART has not yet determined the effect this Statement will have on its financial statements.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

NOTES TO FINANCIAL STATEMENTS (continued)

June 30, 2015 and 2014

18

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

2. Financial Statement Presentation (continued) In August 2015, GASB issued Statement No. 76, The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments. This statement supersedes Statement No. 55, The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments. The objective of this Statement is to identify the hierarchy of generally accepted principles used to prepare financial statements of state and local governments. As a result, governments will apply financial reporting guidance with less variation, which will improve the usefulness of financial statements. The provisions of this Statement are effective for periods beginning after June 15, 2015. The HART has not yet determined the effect this Statement will have on its financial statements.

3. Basis of Accounting

The accompanying financial statements are presented using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded at the time liabilities are incurred. The operating revenues of HART are the result of providing services in connection with the delivery of transportation services of the rail system, which is not yet operational. The operating expenses of HART include the cost of services, administrative expenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reported as non-operating revenues and expenses.

4. Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent liabilities at the date of the financial statements and the reported amount of revenues and expenses during the reporting period. Specifically, management has made estimates based on assumptions for intergovernmental receivables, construction delay claims, environmental remediation liabilities and net pension liability. Actual results could differ from those estimates.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

NOTES TO FINANCIAL STATEMENTS (continued)

June 30, 2015 and 2014

19

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

5. Deferred Outflows and Inflows of Resources

Deferred outflows of resources represent consumptions of net position that apply to future periods and will not be recognized as an outflow of resources (expenditures) until then. Deferred inflows represent acquisitions of net position that apply to future periods and will not be recognized as an inflow of resources (revenues). According to paragraph 33 of GASB No. 68, differences between expected and actual experience and changes in assumptions are recognized in pension expense using a systematic and rational method over a closed period equal to the average of the expected remaining service lives of all employees that are provided with pensions through the pension plan (active and inactive employees) determined as of the beginning of the measurement period. The average of expected remaining service lives for the purposes of recognizing the applicable deferred outflows and inflows of resources established in the 2014 fiscal year is 5.7661 years. Additionally, differences between projected and actual earnings on pension plan investments are recognized in pension expense using a systematic and rational method over a closed five-year period. Contributions to the pension plan from the employer subsequent to the measurement date of the net pension liability and before the end of the reporting period are reported as deferred outflows.

6. Revenue Recognition

Revenue sources that are considered susceptible to accrual when earned include a county surcharge on the State of Hawaii’s General Excise Tax (GET) and grant assistance from the U.S. Department of Transportation’s Federal Transit Administration (FTA). GET revenue is recognized when earned. Revenues on cost reimbursement contracts are recognized when allowable and reimbursable expenses are incurred, and upon meeting the legal and contractual requirements of the funding source. No allowance for doubtful accounts was recorded as of June 30, 2015 and 2014.

7. Cash and Cash Equivalents

HART considers all cash on hand, demand deposits, and short-term investments with original maturities of three months or less from the date of acquisition to be cash and cash equivalents.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

NOTES TO FINANCIAL STATEMENTS (continued)

June 30, 2015 and 2014

20

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) 8. Capital Assets

Capital assets are generally those assets with an individual price in excess of $5,000 for equipment and machinery and $100,000 for infrastructure, buildings, and structures with a useful life of more than one year. Capital assets are stated at cost and include contributions by governmental agencies at cost or estimated value. Additions, improvements, and other capital outlays that significantly extend the useful life of an asset are capitalized. Other costs related to repairs and maintenance is expensed as incurred. Assets are depreciated over the individual asset’s estimated useful life using the straight-line method. Depreciation on both purchased and contributed assets is charged against operations Depreciation on all assets is provided for on the straight-line basis over the following estimated useful lives:

Years

Infrastructure 50-75 Buildings and improvements 30-50 Equipment and machinery 5-25 Rail vehicles 25-35

9. Compensated Absences HART accrues accumulated vacation when earned by the employee. Vacation benefits accrue at a rate of one and three-quarters working days per month. Each employee is allowed to accumulate a maximum of 90 days of accrued vacation as of the end of the calendar year (see Note F). Sick leave accumulates at the rate of one and three-quarters working days for each month. Sick leave is taken only in the event of illness and is not convertible to pay; accordingly, sick leave is not accrued in the accompanying financial statements. Employees who retire or leave government service in good standing with 60 or more unused sick leave days are entitled to an additional service credit in the retirement system. At June 30, 2015 and 2014, accumulated sick leave amounted to approximately $2,063,000 and $1,771,000, respectively.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)

NOTES TO FINANCIAL STATEMENTS (continued)

June 30, 2015 and 2014

21

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

10. Deferred Compensation Plan

All full-time employees of HART are eligible to participate in the City and County of Honolulu’s Public Employees’ Deferred Compensation Program (Plan), adopted pursuant to Internal Revenue Code Section 457. The Plan permits eligible employees to defer a portion of their salary until future years by contributing to a fund managed by a plan administrator. The deferred compensation amounts are not available to employees until termination, retirement, death, or unforeseeable emergency. A trust fund was established to protect Plan assets from claims of general creditors and from diversion to any uses other than paying benefits to participants and beneficiaries. Plan assets of approximately $3,497,000 and $3,280,000 are not reported in the accompanying financial statements at June 30, 2015 and 2014, respectively.

11. Net Position

Net position comprises the various net earnings (losses) from operating and non-operating revenues, expenses and contributed capital. Net position is classified in the following two components: net investment in capital assets or unrestricted net position. Net investment in capital assets consists of capital assets, net of accumulated depreciation and reduced by outstanding debt that is attributable to the acquisition, construction, or improvement of those assets. Unrestricted net position consists of all other net position not included in net investment in capital assets.

12. Risk Management

HART is exposed to various risks for losses related to torts; theft of or damage to, or destruction of assets; errors or omissions; natural disasters; and injuries to employees. A liability for a claim for a risk of loss is established if the information indicates that it is probable that a liability has been incurred at the date of the financial statements and the amount of the loss is reasonably estimable.

13. Reclassifications Certain reclassifications were made to prior year’s financial statements to conform to the 2015 presentation. Such reclassifications had no impact on the previously reported change in net position.

Honolulu Authority for Rapid Transportation (a component unit of the City and County of Honolulu)