Alibaba Jeffrries

130

RMB Prev. 2014A Prev. 2015E Prev. 2016E Prev. 2017E Rev. (MM) -- 52,504.0 -- 76,812.0 -- 105,040.0 -- 132,115.0 Chg (% YoY) -- 52.1% -- 46.3% -- 36.7% -- 25.8% Operating Profit -- 29,392.0 -- 34,486.0 -- 46,382.0 -- 58,467.0 EBITDA (MM) -- 30,731.0 -- 36,242.0 -- 48,850.0 -- 61,855.0 Net Profit Non- GAAP -- 27,610.0 -- 31,489.0 -- 45,060.0 -- 58,541.0 BV/Share -- 17.50 -- 53.00 -- 70.25 -- 93.20 EPS Growth -- 103.9% -- 7.9% -- 41.6% -- 29.9% EPS FY Dec -- $1.90 -- $2.06 -- $2.92 -- $3.79 FY P/E 50.4x 46.5x 32.8x 25.3x Price Performance SEP-14 OCT-14 100 95 90 85 80 COMPANY NOTE Initiating Coverage CHN | Technology | Internet 27 October 2014 Alibaba (BABA) The Powerful E-Commerce Ecosystem Connecting Half of China; Initiate at Buy EQUITY RESEARCH CHINA BUY Price target $118.00 Price $95.76 Financial Summary Book Value (MM): Rmb40,818.0 Book Value/Share: Rmb17.50 Net Debt (MM): (Rmb2,557) Return on Avg. Equity: 106.5% Long-Term Debt (MM): Rmb30,711.0 Cash & ST Invest. (MM): Rmb43,632.0 Market Data 52 Week Range: $99.70 - $82.81 Total Entprs. Value (MM): $238,140.2 Market Cap. (MM): $238,557.3 Insider Ownership: 12.8% Institutional Ownership: 54.6% Shares Out. (MM): 2,491.2 Float (MM): NA Avg. Daily Vol.: NA Cynthia Meng * Equity Analyst +852 3743 8033 [email protected] Brian Pitz § Equity Analyst (212) 336-7413 [email protected] Brian Fitzgerald § Equity Analyst (212) 284-2491 [email protected] Karen Chan * Equity Associate +852 3743 8017 [email protected] Nick Wang * Equity Associate +852 3743 8059 [email protected] Qin Wang * Equity Associate +852 3743 8016 [email protected] * Jefferies Hong Kong Limited § Jefferies LLC Key Takeaway China's changing Internet user demographics and mobile development support our favorable view on e-Commerce for the next decade. Alibaba is the largest Chinese ecommerce player, with 80%+ GMV market share, but is only selling to less than 25% of the population now. We estimate well over half of Chinese population will be shopping on Alibaba’s platforms in 10 years. Initiate with Buy; PT USD118. Changing demographics & mobile support ecommerce in the next decade. As discussed in our sector note, "A Taste of Domestic Consumption: The Unleashing of China's E-Commerce Power" published on Sept 19, 2014, China’s e-Commerce growth for the next decade benefit from: 1) changing Internet user demographics towards 30+ year old age groups; 2) accelerating structural shift to online from traditional retail; 3) Chinese government’s massive support for urbanization and domestic consumption; 4) proliferation of affordable smart devices; 5) improving wireless and transport infrastructures in lower tier and rural markets, and 6) rising consumer demand for better quality, design & fashion, authenticity and timely delivery. Growth driven by mix shift towards Tmall, and improving mobile monetization. We expect Alibaba, as the largest e-Commerce player, to sell to well over half of the Chinese population in 10 years, up from less than 25% now. We estimate FY14-17E revenue CAGR of 36%, driven by continued commission revenues from Tmall. Alibaba’s mobile GMV accounted for 32.8% of total GMV in FY1Q15, +21pcpt YoY. We expect the mobile monetization rate to narrow the gap with that of PC. Cross-border e-Commerce provides upside for long-term growth. Addressing the growing appetite for foreign brands among Chinese consumers, Tmall Global lowers the cost, delivery time and language barriers in cross-border online shopping, which is expected to reach an RMB1trn market size by 2018. Our scenario analysis shows a 5-12% upside to our CY16 revenue estimate. Its recently launched ePass payment service allows U.S. retailers to reach Chinese online shoppers. Valuation/Risks Our PT of USD118 is derived from 10-year DCF based on a long-term EBIT margin of 43%, terminal growth rate of 5.5% and WACC of 10.2%, implying a CY16 P/E of 32.5x, 1.4% premium to global e-Commerce peer average of 32x, 20.4% premium to China e-Commerce peer group. Risks: limited ability to influence corporate matters by individual shareholders and potential conflict of interest arising from the company’s corporate structure. Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 126 to 130 of this report.

-

Upload

cartigayan -

Category

Documents

-

view

75 -

download

27

description

Inititating

Transcript of Alibaba Jeffrries

RMB Prev. 2014A Prev. 2015E Prev. 2016E Prev. 2017E

Rev. (MM) -- 52,504.0 -- 76,812.0 -- 105,040.0 -- 132,115.0

Chg (% YoY) -- 52.1% -- 46.3% -- 36.7% -- 25.8%

Operating Profit -- 29,392.0 -- 34,486.0 -- 46,382.0 -- 58,467.0

EBITDA (MM) -- 30,731.0 -- 36,242.0 -- 48,850.0 -- 61,855.0

Net Profit Non-GAAP

-- 27,610.0 -- 31,489.0 -- 45,060.0 -- 58,541.0

BV/Share -- 17.50 -- 53.00 -- 70.25 -- 93.20

EPS Growth -- 103.9% -- 7.9% -- 41.6% -- 29.9%

EPS

FY Dec -- $1.90 -- $2.06 -- $2.92 -- $3.79

FY P/E 50.4x 46.5x 32.8x 25.3x

Price Performance

SEP-14 OCT-14

100

95

90

85

80

COMPANY NOTE

Initiating Coverage

CHN | Technology | Internet 27 October 2014

Alibaba (BABA)The Powerful E-Commerce EcosystemConnecting Half of China; Initiate at Buy

EQU

ITY R

ESEARC

H C

HIN

A

BUYPrice target $118.00

Price $95.76

Financial SummaryBook Value (MM): Rmb40,818.0Book Value/Share: Rmb17.50Net Debt (MM): (Rmb2,557)Return on Avg. Equity: 106.5%Long-Term Debt (MM): Rmb30,711.0Cash & ST Invest. (MM): Rmb43,632.0

Market Data52 Week Range: $99.70 - $82.81Total Entprs. Value (MM): $238,140.2Market Cap. (MM): $238,557.3Insider Ownership: 12.8%Institutional Ownership: 54.6%Shares Out. (MM): 2,491.2Float (MM): NAAvg. Daily Vol.: NA

Cynthia Meng *Equity Analyst

+852 3743 8033 [email protected] Pitz §

Equity Analyst(212) 336-7413 [email protected]

Brian Fitzgerald §Equity Analyst

(212) 284-2491 [email protected] Chan *

Equity Associate+852 3743 8017 [email protected]

Nick Wang *Equity Associate

+852 3743 8059 [email protected] Wang *

Equity Associate+852 3743 8016 [email protected]

* Jefferies Hong Kong Limited § Jefferies LLC

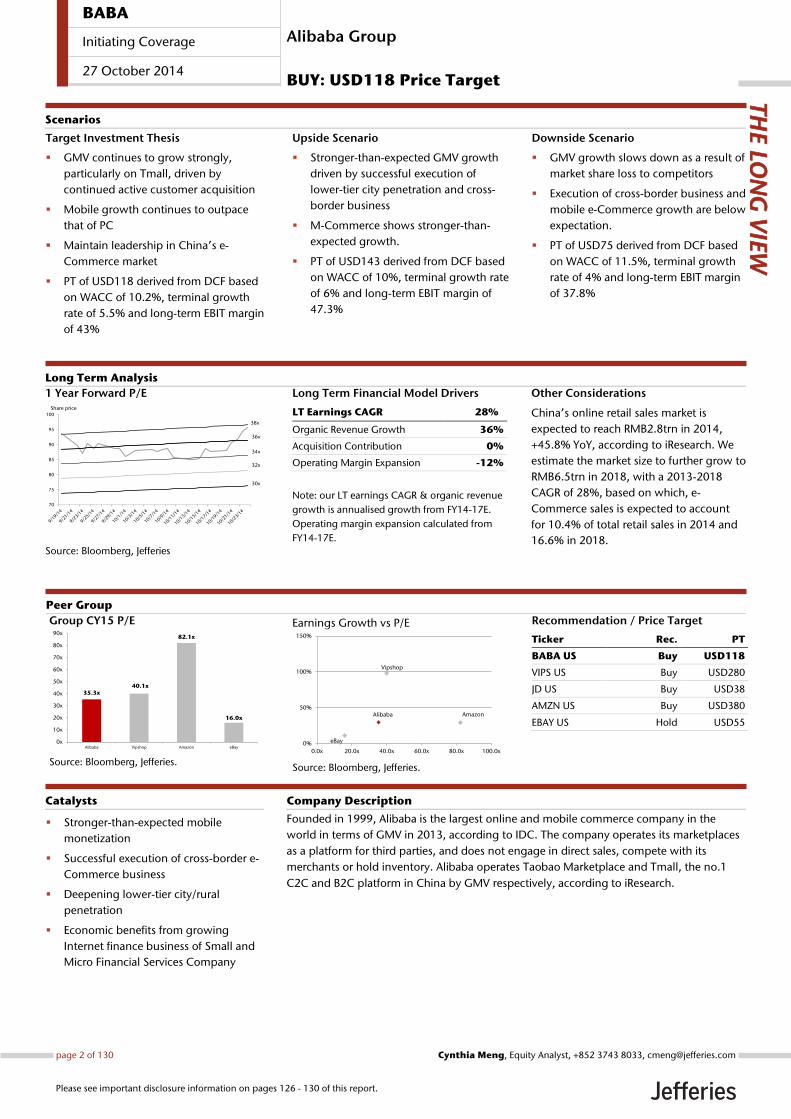

Key Takeaway

China's changing Internet user demographics and mobile developmentsupport our favorable view on e-Commerce for the next decade. Alibaba is thelargest Chinese ecommerce player, with 80%+ GMV market share, but is onlyselling to less than 25% of the population now. We estimate well over half ofChinese population will be shopping on Alibaba’s platforms in 10 years. Initiatewith Buy; PT USD118.

Changing demographics & mobile support ecommerce in the next decade. Asdiscussed in our sector note, "A Taste of Domestic Consumption: The Unleashing of China'sE-Commerce Power" published on Sept 19, 2014, China’s e-Commerce growth for thenext decade benefit from: 1) changing Internet user demographics towards 30+ year oldage groups; 2) accelerating structural shift to online from traditional retail; 3) Chinesegovernment’s massive support for urbanization and domestic consumption; 4) proliferationof affordable smart devices; 5) improving wireless and transport infrastructures in lowertier and rural markets, and 6) rising consumer demand for better quality, design & fashion,authenticity and timely delivery.

Growth driven by mix shift towards Tmall, and improving mobile monetization.We expect Alibaba, as the largest e-Commerce player, to sell to well over half of theChinese population in 10 years, up from less than 25% now. We estimate FY14-17E revenueCAGR of 36%, driven by continued commission revenues from Tmall. Alibaba’s mobileGMV accounted for 32.8% of total GMV in FY1Q15, +21pcpt YoY. We expect the mobilemonetization rate to narrow the gap with that of PC.

Cross-border e-Commerce provides upside for long-term growth. Addressing thegrowing appetite for foreign brands among Chinese consumers, Tmall Global lowers thecost, delivery time and language barriers in cross-border online shopping, which is expectedto reach an RMB1trn market size by 2018. Our scenario analysis shows a 5-12% upside toour CY16 revenue estimate. Its recently launched ePass payment service allows U.S. retailersto reach Chinese online shoppers.

Valuation/RisksOur PT of USD118 is derived from 10-year DCF based on a long-term EBIT margin of 43%,terminal growth rate of 5.5% and WACC of 10.2%, implying a CY16 P/E of 32.5x, 1.4%premium to global e-Commerce peer average of 32x, 20.4% premium to China e-Commercepeer group. Risks: limited ability to influence corporate matters by individual shareholdersand potential conflict of interest arising from the company’s corporate structure.

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have aconflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investmentdecision. Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 126 to130 of this report.

Long Term Financial Model Drivers

LT Earnings CAGR 28%

Organic Revenue Growth 36%

Acquisition Contribution 0%

Operating Margin Expansion -12%

Note: our LT earnings CAGR & organic revenue

growth is annualised growth from FY14-17E.

Operating margin expansion calculated from

FY14-17E.

Other Considerations

China’s online retail sales market is

expected to reach RMB2.8trn in 2014,

+45.8% YoY, according to iResearch. We

estimate the market size to further grow to

RMB6.5trn in 2018, with a 2013-2018

CAGR of 28%, based on which, e-

Commerce sales is expected to account

for 10.4% of total retail sales in 2014 and

16.6% in 2018.

1 Year Forward P/E

Source: Bloomberg, Jefferies

70

75

80

85

90

95

100

Share price

38x

36x

34x

32x

30x

Founded in 1999, Alibaba is the largest online and mobile commerce company in the

world in terms of GMV in 2013, according to IDC. The company operates its marketplaces

as a platform for third parties, and does not engage in direct sales, compete with its

merchants or hold inventory. Alibaba operates Taobao Marketplace and Tmall, the no.1

C2C and B2C platform in China by GMV respectively, according to iResearch.

Stronger-than-expected mobile

monetization

Successful execution of cross-border e-

Commerce business

Deepening lower-tier city/rural

penetration

Economic benefits from growing

Internet finance business of Small and

Micro Financial Services Company

Catalysts

Target Investment Thesis

GMV continues to grow strongly,

particularly on Tmall, driven by

continued active customer acquisition

Mobile growth continues to outpace

that of PC

Maintain leadership in China’s e-

Commerce market

PT of USD118 derived from DCF based

on WACC of 10.2%, terminal growth

rate of 5.5% and long-term EBIT margin

of 43%

Upside Scenario

Stronger-than-expected GMV growth

driven by successful execution of

lower-tier city penetration and cross-

border business

M-Commerce shows stronger-than-

expected growth.

PT of USD143 derived from DCF based

on WACC of 10%, terminal growth rate

of 6% and long-term EBIT margin of

47.3%

Downside Scenario

GMV growth slows down as a result of

market share loss to competitors

Execution of cross-border business and

mobile e-Commerce growth are below

expectation.

PT of USD75 derived from DCF based

on WACC of 11.5%, terminal growth

rate of 4% and long-term EBIT margin

of 37.8%

Long Term Analysis

Scenarios

Group CY15 P/E

Source: Bloomberg, Jefferies.

35.3x40.1x

82.1x

16.0x

0x

10x

20x

30x

40x

50x

60x

70x

80x

90x

Alibaba Vipshop Amazon eBay

Earnings Growth vs P/E

Source: Bloomberg, Jefferies.

Alibaba

Vipshop

eBay

Amazon

0%

50%

100%

150%

0.0x 20.0x 40.0x 60.0x 80.0x 100.0x

Recommendation / Price Target

Ticker Rec. PT

BABA US Buy USD118

VIPS US Buy USD280

JD US Buy USD38

AMZN US Buy USD380

EBAY US Hold USD55 N.A. N.A.

Company Description

THE LO

NG

VIE

W

Peer Group

Alibaba Group

BUY: USD118 Price Target

BABA

Initiating Coverage

27 October 2014

page 2 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Table of Contents

Investment Summary p.5

Valuation and Risks p.6

Changing Demographics and Mobile Support E-Commerce in the Next Decade p.11

Alibaba - The Powerful E-Commerce Ecosystem Connecting Half of China p.25

Business Model and Segment Revenue p.27

A Strong Self-reinforcing Network Effect p.33

Extending Mobile Leadership p.53

Building the Largest Ecosystem p.63

Expanding Cross-Border E-Commerce p.83

Company Background p.91

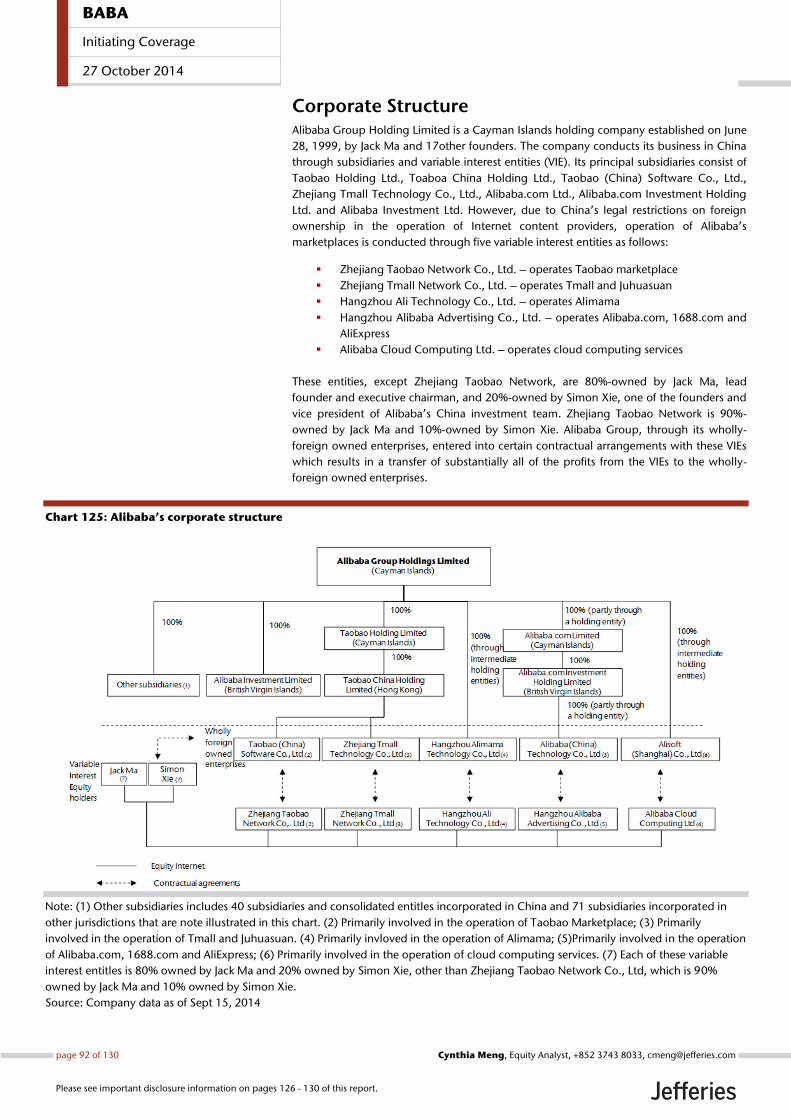

Corporate & Shareholding Structure p.92

Partnership System p.94

Small and Micro Financial Services Company p.98

Management Team p.100

Financial Statements p.102

Appendix p.116

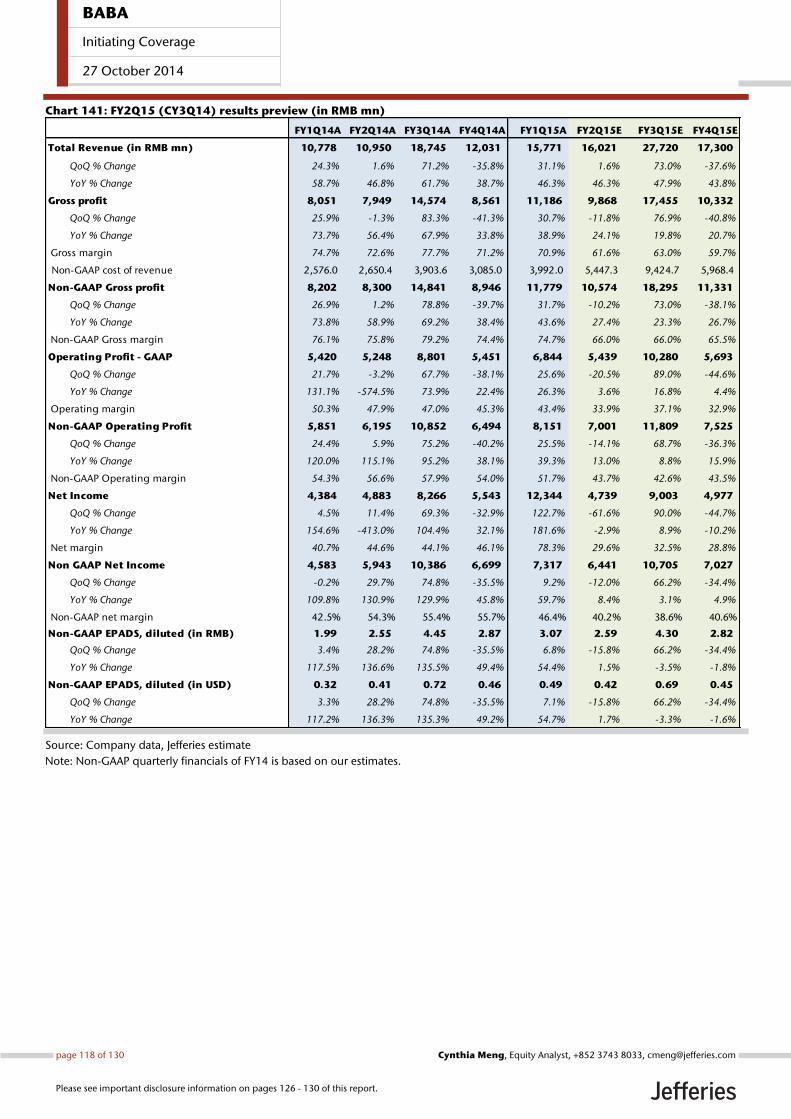

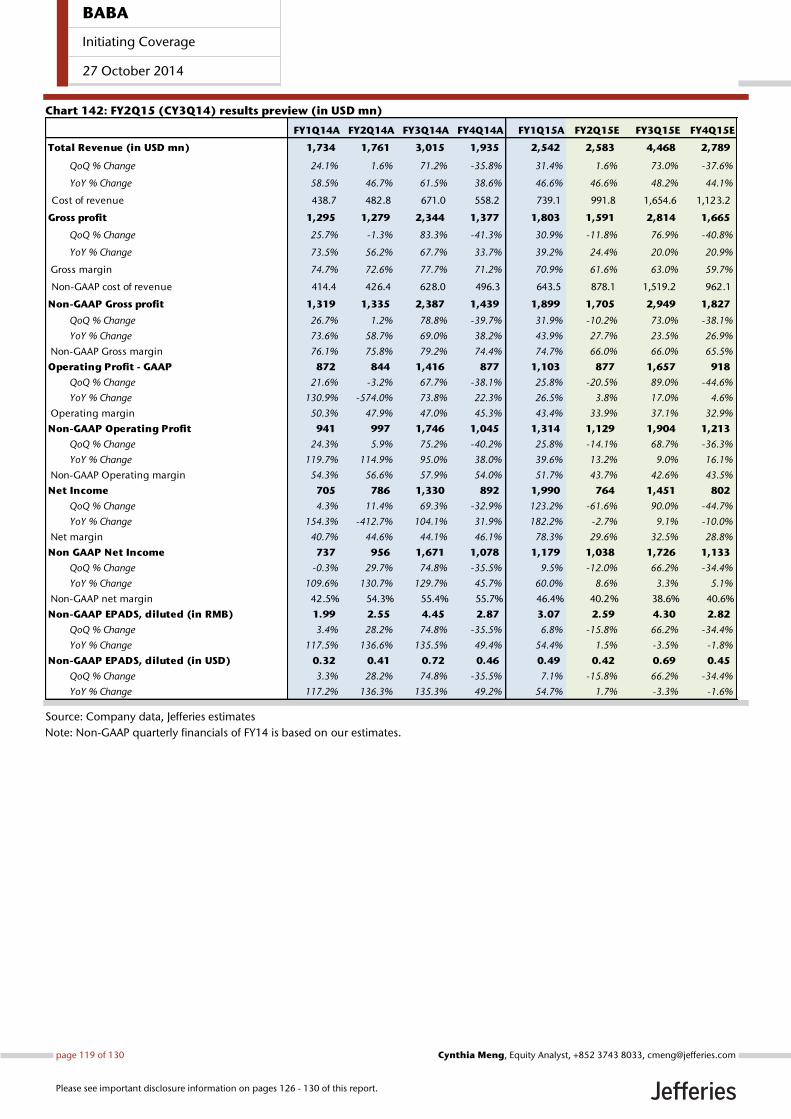

FY2Q15 Results Preview p.117

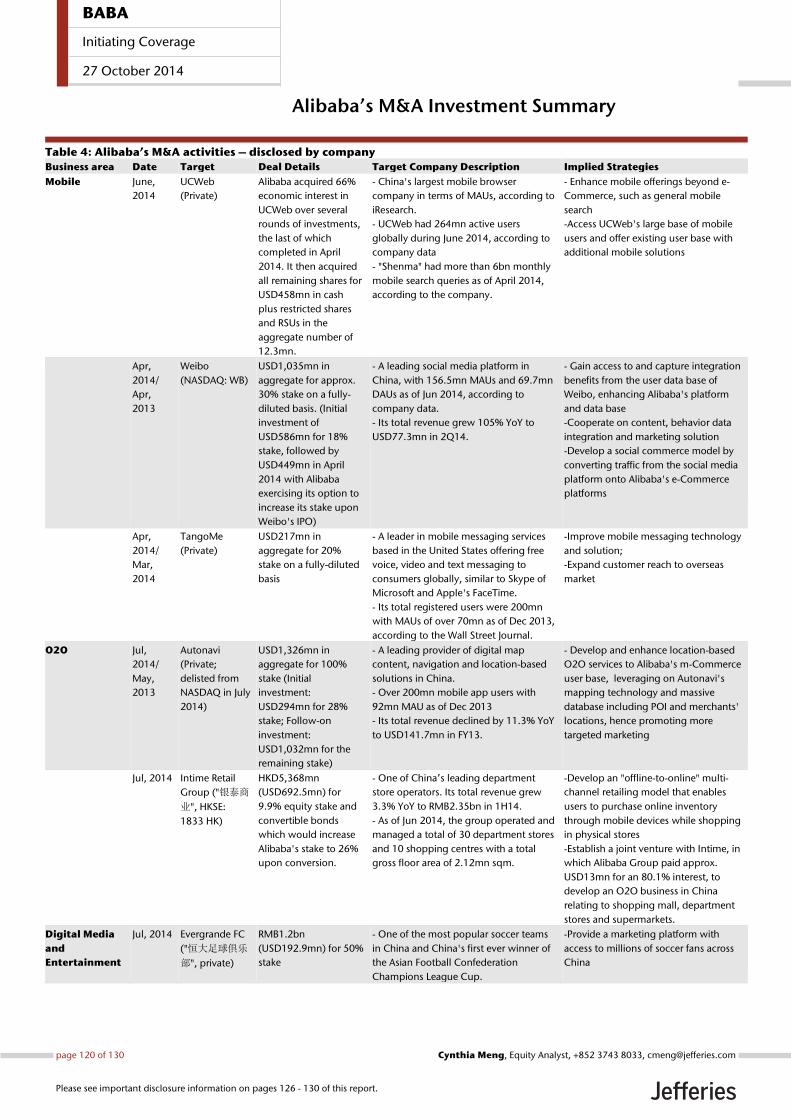

M&A Investment Summary p.120

BABA

Initiating Coverage

27 October 2014

page 3 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

This page is intentionally kept blank

BABA

Initiating Coverage

27 October 2014

page 4 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Alibaba Group Investment Summary We are initiating coverage of Alibaba at Buy, with a price target of USD118.

China’s changing Internet user demographics and mobile development

support our favorable view on e-Commerce for the next decade. Alibaba is the

largest Chinese ecommerce player with 80%+ GMV market share, but is only

selling to less than 25% of the population now. We estimate well over half of

the Chinese population will be shopping on Alibaba’s platforms in 10 years.

Alibaba is the largest online and mobile commerce company in the world by GMV in 2013,

according to IDC. Its no.1 C2C and B2C platforms in China, Taobao and Tmall, in

aggregate generated a GMV of RMB1,833bn (USD296bn) in the twelve months ended

June 30, 2014.

Key Points to Highlight

Changing demographics & mobile support ecommerce in the next decade

As discussed in our sector note, "A Taste of Domestic Consumption: The Unleashing of

China's E-Commerce Power," published on Sept 19, 2014, China’s e-Commerce growth

for the next decade should benefit from: 1) changing Internet user demographics towards

30+ year old age groups; 2) accelerating structural shift to online from traditional retail; 3)

the Chinese government’s massive support for urbanization and domestic consumption;

4) proliferation of affordable smart devices; 5) improving wireless and transport

infrastructures in lower tier and rural markets, and 6) rising consumer demand for better

quality, design & fashion, authenticity and timely delivery.

A powerful ecosystem with strong self-reinforcing network effect

We expect Alibaba, as the largest e-Commerce player with 80%+ GMV market share as of

1H14, to sell to well over half of Chinese population in ten years, up from less than 25%

now. We expect increasing GMV contribution from Tmall given its higher listing priority

and rising consumer demand for quality goods. We estimate FY14-17E revenue CAGR of

36%, driven by continued commission revenues from Tmall.

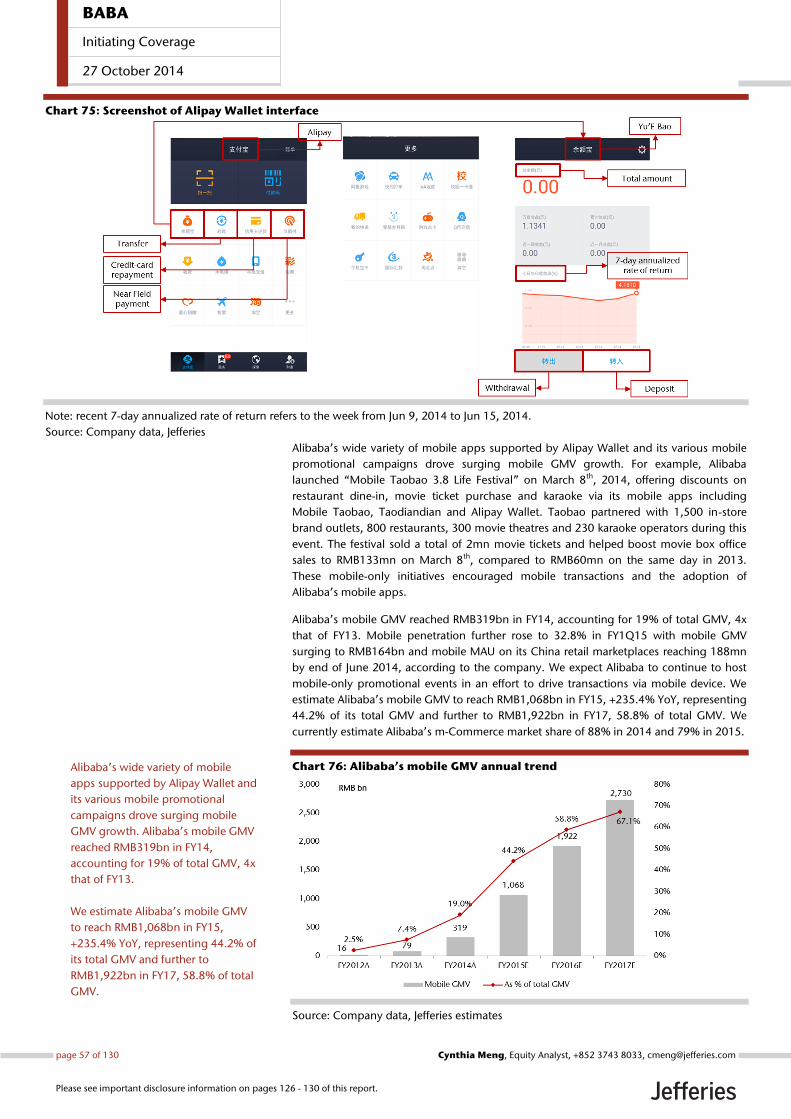

Improving monetization with extended mobile leadership

Driven by its diversified portfolio of mobile apps, including Alipay Wallet, and mobile-

targeted promotional efforts, Alibaba’s mobile GMV accounted for 32.8% of total GMV in

FY1Q15, +21pcpt YoY. We expect mobile monetization rate to narrow the gap with that of

PC as Alibaba enhances its mobile ads products and increases both paid clicks and CTR,

eventually closing the CPC gap across mobile and PC platforms.

Closing the loop with logistics support, Internet finance and banking

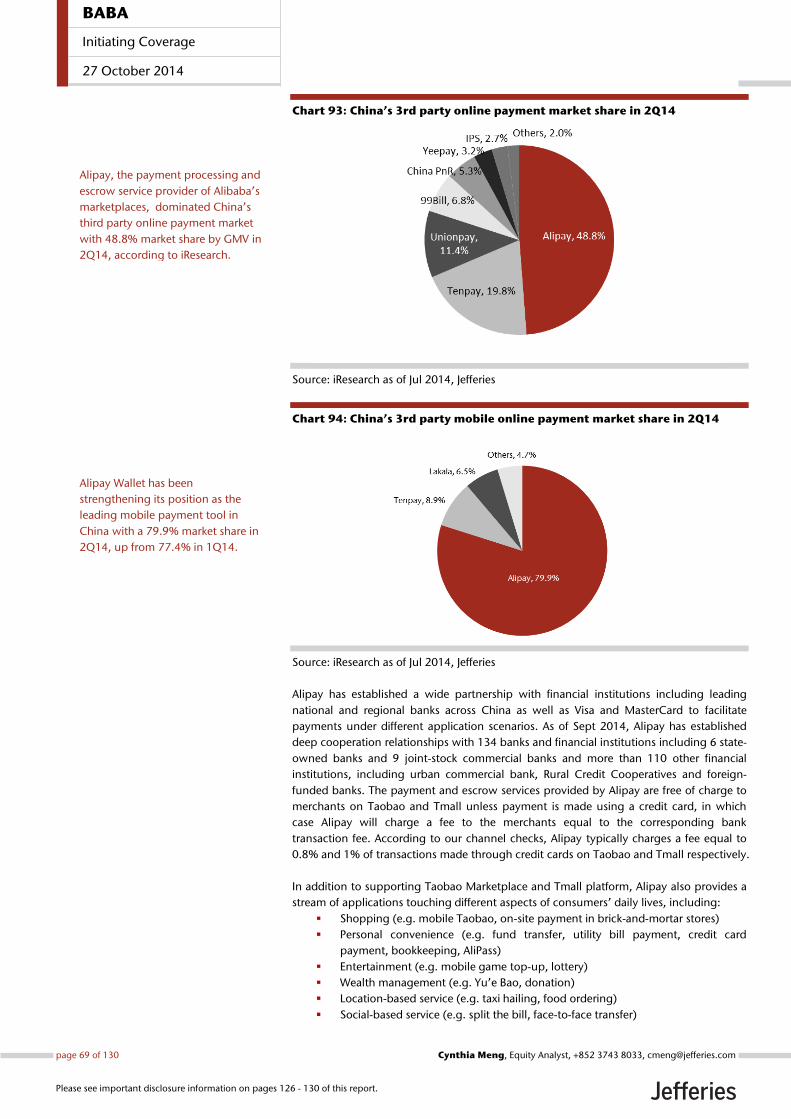

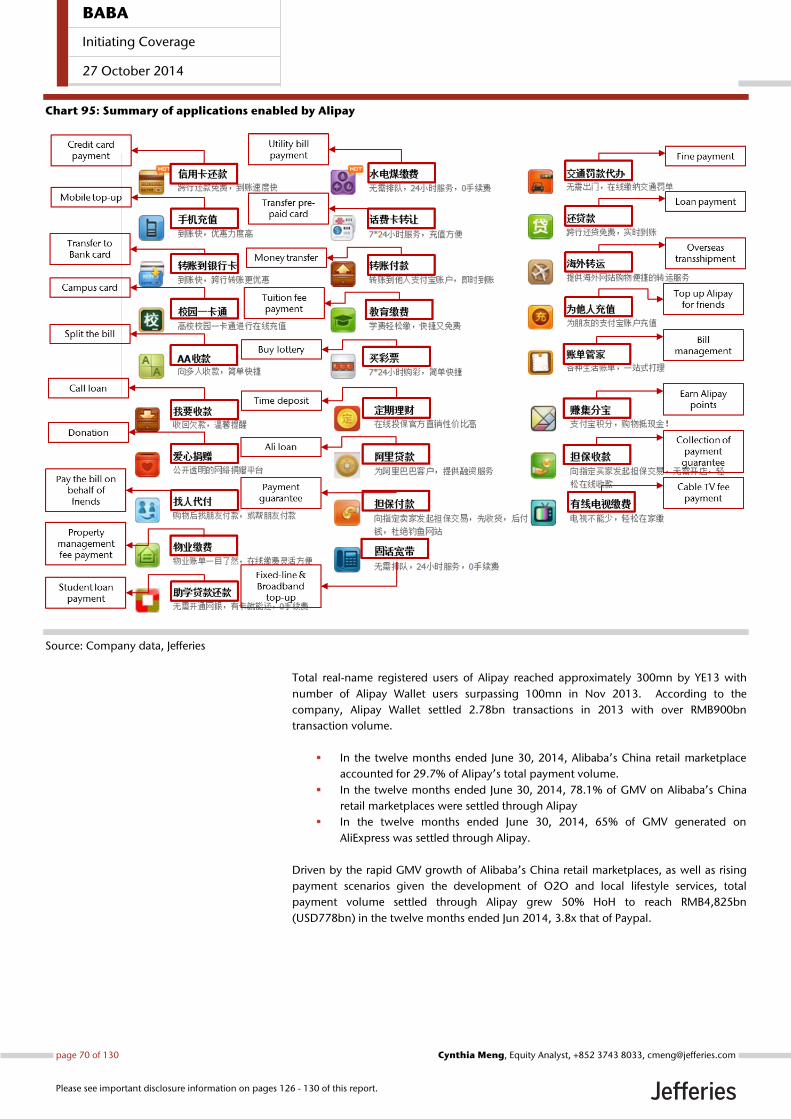

Alibaba’s large and growing ecosystem is supported by its expanding logistics platform

and Alipay which accounted for 48.8% of China’s third-party online payment market

share in 2Q14, according to iResearch. Leveraging on the data accumulated from its

online platforms, Alibaba entered into Internet finance including wealth management,

SME loan and Internet banking to further enhance user engagement within its ecosystem.

Cross-border e-Commerce may drive upside for long-term growth

Addressing the growing appetite for foreign brands among Chinese consumers, Tmall

Global lowers the cost, delivery time and language barriers in cross-border online

shopping which is expected to reach an RMB1trn market size by 2018. Our scenario

analysis shows a 5-12% upside to our CY16 revenue estimate. Its recently launched ePass

payment service allows U.S. retailers to reach to Chinese online shoppers.

BABA

Initiating Coverage

27 October 2014

page 5 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Valuation Our price target of USD118 is derived from a 10-year DCF analysis based on long-term

non-GAAP EBIT margin estimate of 43%, a terminal growth rate of 5.5% and a WACC of

10.2%. This is equivalent to a market cap of USD292.9bn, implying a FY17 P/E multiple of

31x or CY16 P/E of 32.5x, 1.4% premium to global e-Commerce peer average of 32x,

20.4% premium to China e-Commerce peer average of 27x, and 62.2% premium to China

Internet peer group average of 20x. We do not see a direct comparable to Alibaba among

China’s e-Commerce players given that JD.com operates an online direct sales model

while Vipshop focuses on a niche flash sales market. Among China’s Internet subsectors,

we see e-Commerce as the most favorable sector (followed by mobile games, and online

travel) benefitting from the shift in Internet user demographics towards the more mature

30+ year old users who have higher consumption power and will shop online. Companies

in other subsectors such as portal and PC games generally trade at a lower multiple. Based

on Bloomberg consensus, U.S. e-Commerce players, including Amazon, Ebay and Zulily,

on average trade at a 73% and 10% premium to Internet average in FY15 and FY16 P/E

respectively.

At the current price of USD95.8, Alibaba is trading at 25.3x FY17 P/E or 26.5x CY16 P/E.

Our PT of USD118 represents 23% upside to last closing price. Near-term potential

catalysts of the stock include the upcoming Nov 11th Singles Day sales and FY2Q15

earnings results to be released on Nov 4th.

Year-to-date share price performance compared to peers

As of Oct 24, 2014, Alibaba has traded up 40.8% since IPO. China’s e-Commerce names

have fared well with JD.com up 26.4% since its IPO in May and Vipshop up 155.2% YTD.

On the other hand, U.S. e-Commerce players such as Amazon and Ebay have traded down

28% and 6.8%, respectively, YTD. The average share price of China’s brick-and-mortar

department store names, including Parkson, Intime Retail, Golden Eagle Retail, Lifestyle

International and Springland International, declined 7.5% YTD on a weighted average

basis.

BABA

Initiating Coverage

27 October 2014

page 6 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

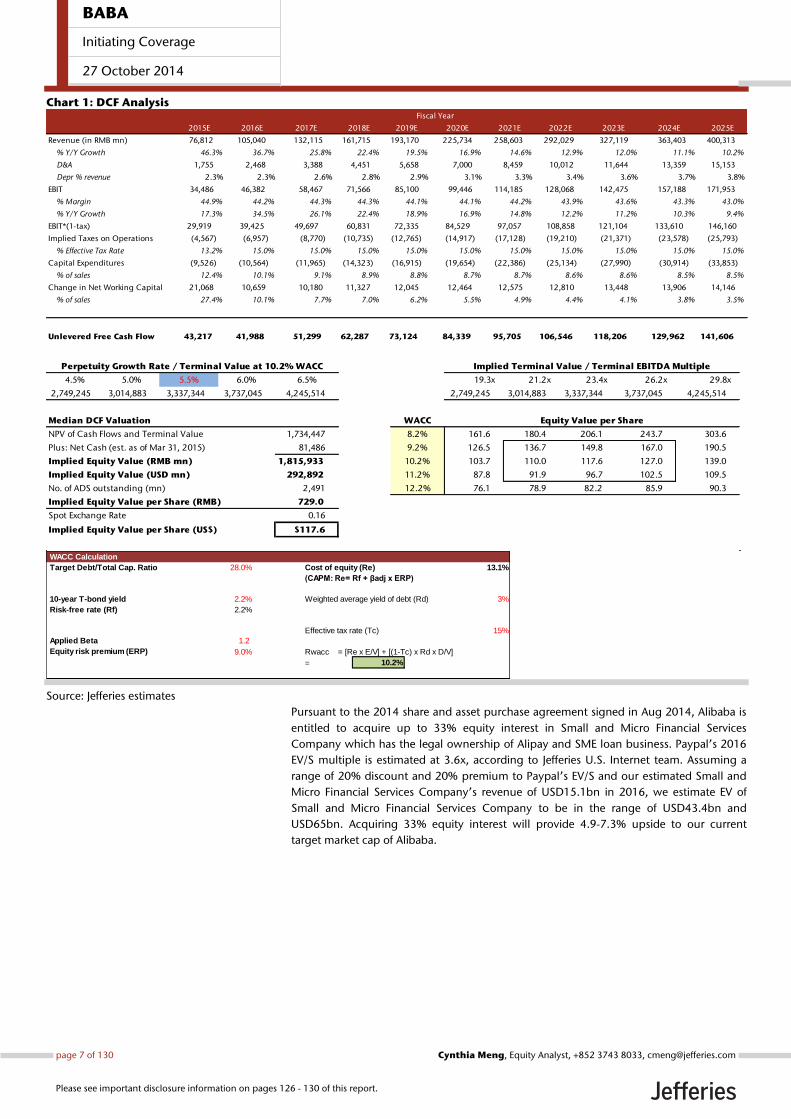

Chart 1: DCF Analysis

Source: Jefferies estimates

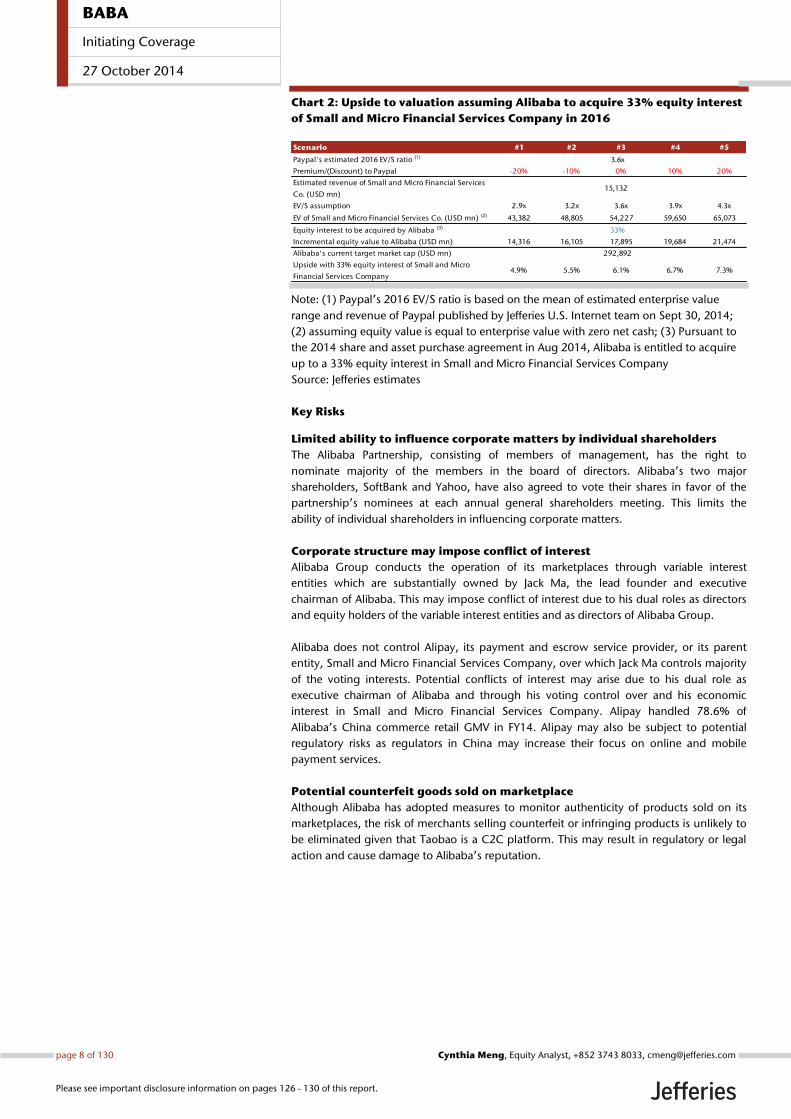

Pursuant to the 2014 share and asset purchase agreement signed in Aug 2014, Alibaba is

entitled to acquire up to 33% equity interest in Small and Micro Financial Services

Company which has the legal ownership of Alipay and SME loan business. Paypal’s 2016

EV/S multiple is estimated at 3.6x, according to Jefferies U.S. Internet team. Assuming a

range of 20% discount and 20% premium to Paypal’s EV/S and our estimated Small and

Micro Financial Services Company’s revenue of USD15.1bn in 2016, we estimate EV of

Small and Micro Financial Services Company to be in the range of USD43.4bn and

USD65bn. Acquiring 33% equity interest will provide 4.9-7.3% upside to our current

target market cap of Alibaba.

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Revenue (in RMB mn) 76,812 105,040 132,115 161,715 193,170 225,734 258,603 292,029 327,119 363,403 400,313

% Y/Y Growth 46.3% 36.7% 25.8% 22.4% 19.5% 16.9% 14.6% 12.9% 12.0% 11.1% 10.2%

D&A 1,755 2,468 3,388 4,451 5,658 7,000 8,459 10,012 11,644 13,359 15,153

Depr % revenue 2.3% 2.3% 2.6% 2.8% 2.9% 3.1% 3.3% 3.4% 3.6% 3.7% 3.8%

EBIT 34,486 46,382 58,467 71,566 85,100 99,446 114,185 128,068 142,475 157,188 171,953

% Margin 44.9% 44.2% 44.3% 44.3% 44.1% 44.1% 44.2% 43.9% 43.6% 43.3% 43.0%

% Y/Y Growth 17.3% 34.5% 26.1% 22.4% 18.9% 16.9% 14.8% 12.2% 11.2% 10.3% 9.4%

EBIT*(1-tax) 29,919 39,425 49,697 60,831 72,335 84,529 97,057 108,858 121,104 133,610 146,160

Implied Taxes on Operations (4,567) (6,957) (8,770) (10,735) (12,765) (14,917) (17,128) (19,210) (21,371) (23,578) (25,793)

% Effective Tax Rate 13.2% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0%

Capital Expenditures (9,526) (10,564) (11,965) (14,323) (16,915) (19,654) (22,386) (25,134) (27,990) (30,914) (33,853)

% of sales 12.4% 10.1% 9.1% 8.9% 8.8% 8.7% 8.7% 8.6% 8.6% 8.5% 8.5%

Change in Net Working Capital 21,068 10,659 10,180 11,327 12,045 12,464 12,575 12,810 13,448 13,906 14,146

% of sales 27.4% 10.1% 7.7% 7.0% 6.2% 5.5% 4.9% 4.4% 4.1% 3.8% 3.5%

Unlevered Free Cash Flow 43,217 41,988 51,299 62,287 73,124 84,339 95,705 106,546 118,206 129,962 141,606

Fiscal Year

Perpetuity Growth Rate / Terminal Value at 10.2% WACC Implied Terminal Value / Terminal EBITDA Multiple

4.5% 5.0% 5.5% 6.0% 6.5% 19.3x 21.2x 23.4x 26.2x 29.8x

2,749,245 3,014,883 3,337,344 3,737,045 4,245,514 2,749,245 3,014,883 3,337,344 3,737,045 4,245,514

Median DCF Valuation WACC Equity Value per Share

NPV of Cash Flows and Terminal Value 1,734,447 8.2% 161.6 180.4 206.1 243.7 303.6

Plus: Net Cash (est. as of Mar 31, 2015) 81,486 9.2% 126.5 136.7 149.8 167.0 190.5

Implied Equity Value (RMB mn) 1,815,933 10.2% 103.7 110.0 117.6 127.0 139.0

Implied Equity Value (USD mn) 292,892 11.2% 87.8 91.9 96.7 102.5 109.5

No. of ADS outstanding (mn) 2,491 12.2% 76.1 78.9 82.2 85.9 90.3

Implied Equity Value per Share (RMB) 729.0

Spot Exchange Rate 0.16

Implied Equity Value per Share (US$) $117.6

WACC Calculation

Target Debt/Total Cap. Ratio 28.0% Cost of equity (Re) 13.1%

(CAPM: Re= Rf + βadj x ERP)

10-year T-bond yield 2.2% Weighted average yield of debt (Rd) 3%

Risk-free rate (Rf) 2.2%

Effective tax rate (Tc) 15%

Applied Beta 1.2

Equity risk premium (ERP) 9.0% Rwacc = [Re x E/V] + [(1-Tc) x Rd x D/V]

= 10.2%

BABA

Initiating Coverage

27 October 2014

page 7 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Chart 2: Upside to valuation assuming Alibaba to acquire 33% equity interest

of Small and Micro Financial Services Company in 2016

Note: (1) Paypal’s 2016 EV/S ratio is based on the mean of estimated enterprise value

range and revenue of Paypal published by Jefferies U.S. Internet team on Sept 30, 2014;

(2) assuming equity value is equal to enterprise value with zero net cash; (3) Pursuant to

the 2014 share and asset purchase agreement in Aug 2014, Alibaba is entitled to acquire

up to a 33% equity interest in Small and Micro Financial Services Company

Source: Jefferies estimates

Key Risks

Limited ability to influence corporate matters by individual shareholders

The Alibaba Partnership, consisting of members of management, has the right to

nominate majority of the members in the board of directors. Alibaba’s two major

shareholders, SoftBank and Yahoo, have also agreed to vote their shares in favor of the

partnership’s nominees at each annual general shareholders meeting. This limits the

ability of individual shareholders in influencing corporate matters.

Corporate structure may impose conflict of interest

Alibaba Group conducts the operation of its marketplaces through variable interest

entities which are substantially owned by Jack Ma, the lead founder and executive

chairman of Alibaba. This may impose conflict of interest due to his dual roles as directors

and equity holders of the variable interest entities and as directors of Alibaba Group.

Alibaba does not control Alipay, its payment and escrow service provider, or its parent

entity, Small and Micro Financial Services Company, over which Jack Ma controls majority

of the voting interests. Potential conflicts of interest may arise due to his dual role as

executive chairman of Alibaba and through his voting control over and his economic

interest in Small and Micro Financial Services Company. Alipay handled 78.6% of

Alibaba’s China commerce retail GMV in FY14. Alipay may also be subject to potential

regulatory risks as regulators in China may increase their focus on online and mobile

payment services.

Potential counterfeit goods sold on marketplace

Although Alibaba has adopted measures to monitor authenticity of products sold on its

marketplaces, the risk of merchants selling counterfeit or infringing products is unlikely to

be eliminated given that Taobao is a C2C platform. This may result in regulatory or legal

action and cause damage to Alibaba’s reputation.

Scenario #1 #2 #3 #4 #5

Paypal's estimated 2016 EV/S ratio (1)

Premium/(Discount) to Paypal -20% -10% 0% 10% 20%

Estimated revenue of Small and Micro Financial Services

Co. (USD mn)

EV/S assumption 2.9x 3.2x 3.6x 3.9x 4.3x

EV of Small and Micro Financial Services Co. (USD mn) (2) 43,382 48,805 54,227 59,650 65,073

Equity interest to be acquired by Alibaba (3)

Incremental equity value to Alibaba (USD mn) 14,316 16,105 17,895 19,684 21,474

Alibaba's current target market cap (USD mn)

Upside with 33% equity interest of Small and Micro

Financial Services Company4.9% 5.5% 6.1% 6.7% 7.3%

3.6x

33%

292,892

15,132

BABA

Initiating Coverage

27 October 2014

page 8 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

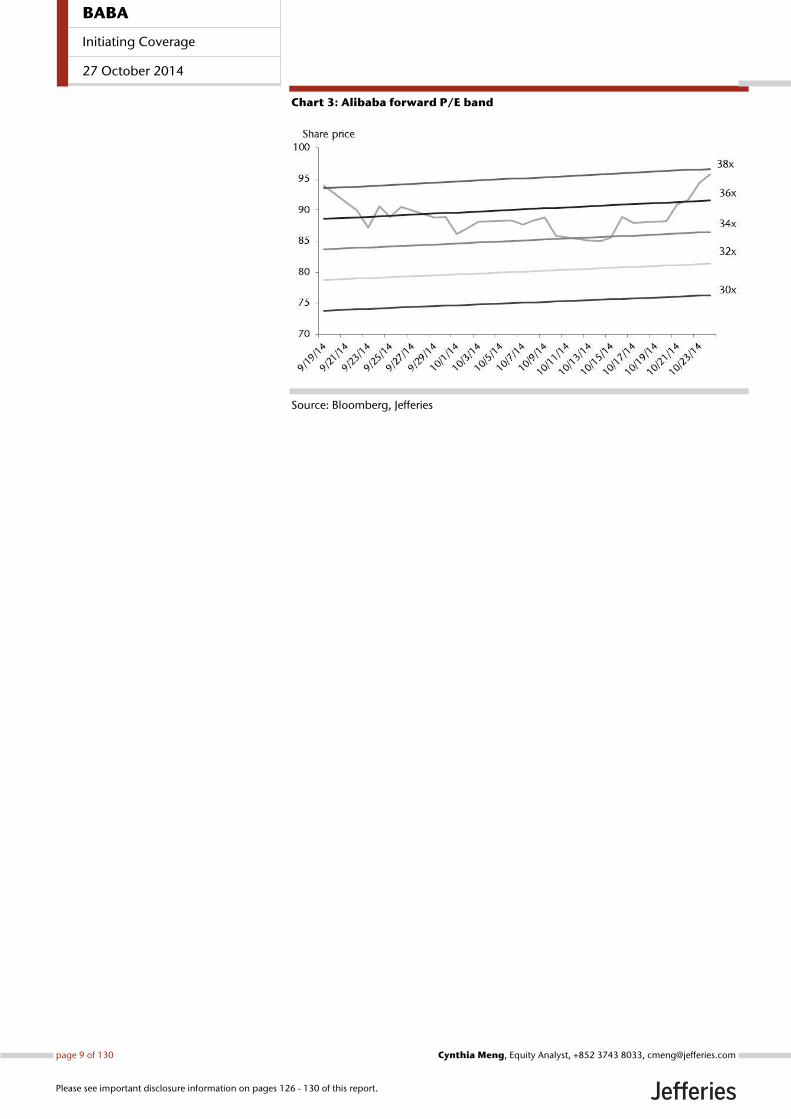

Chart 3: Alibaba forward P/E band

Source: Bloomberg, Jefferies

BABA

Initiating Coverage

27 October 2014

page 9 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

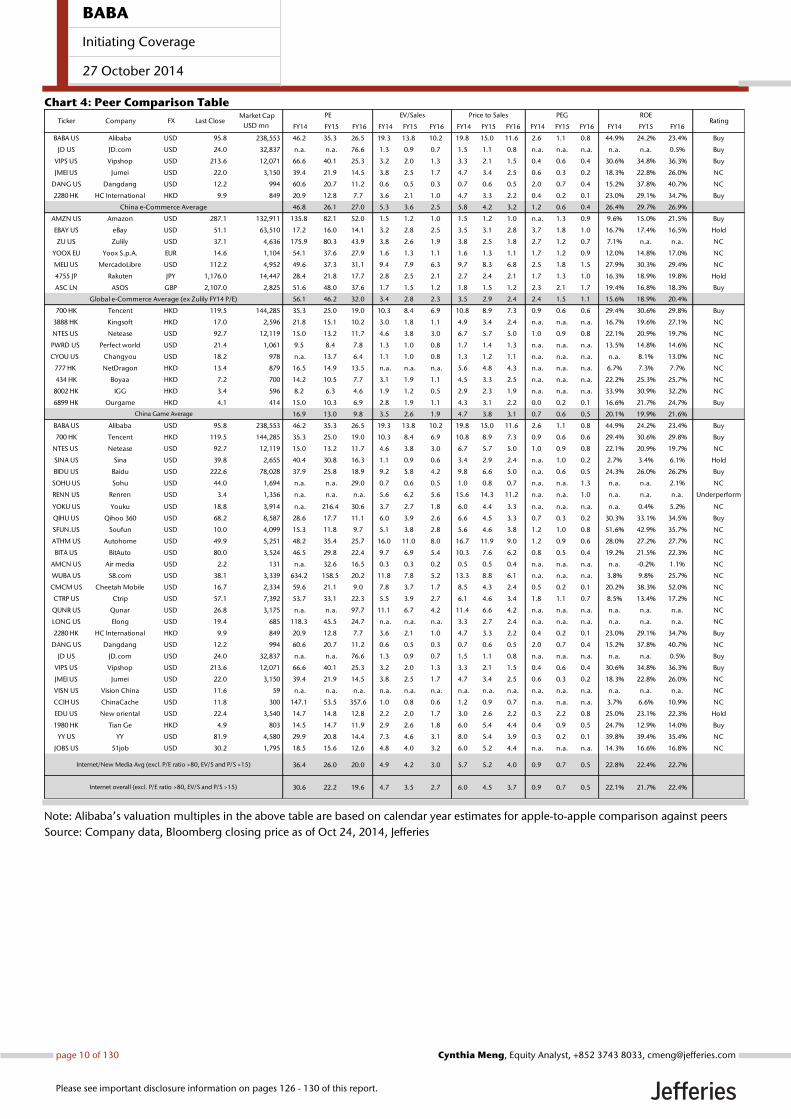

Chart 4: Peer Comparison Table

Note: Alibaba’s valuation multiples in the above table are based on calendar year estimates for apple-to-apple comparison against peers

Source: Company data, Bloomberg closing price as of Oct 24, 2014, Jefferies

FY14 FY15 FY16 FY14 FY15 FY16 FY14 FY15 FY16 FY14 FY15 FY16 FY14 FY15 FY16

BABA US Alibaba USD 95.8 238,553 46.2 35.3 26.5 19.3 13.8 10.2 19.8 15.0 11.6 2.6 1.1 0.8 44.9% 24.2% 23.4% Buy

JD US JD.com USD 24.0 32,837 n.a. n.a. 76.6 1.3 0.9 0.7 1.5 1.1 0.8 n.a. n.a. n.a. n.a. n.a. 0.5% Buy

VIPS US Vipshop USD 213.6 12,071 66.6 40.1 25.3 3.2 2.0 1.3 3.3 2.1 1.5 0.4 0.6 0.4 30.6% 34.8% 36.3% Buy

JMEI US Jumei USD 22.0 3,150 39.4 21.9 14.5 3.8 2.5 1.7 4.7 3.4 2.5 0.6 0.3 0.2 18.3% 22.8% 26.0% NC

DANG US Dangdang USD 12.2 994 60.6 20.7 11.2 0.6 0.5 0.3 0.7 0.6 0.5 2.0 0.7 0.4 15.2% 37.8% 40.7% NC

2280 HK HC International HKD 9.9 849 20.9 12.8 7.7 3.6 2.1 1.0 4.7 3.3 2.2 0.4 0.2 0.1 23.0% 29.1% 34.7% Buy

46.8 26.1 27.0 5.3 3.6 2.5 5.8 4.2 3.2 1.2 0.6 0.4 26.4% 29.7% 26.9%

AMZN US Amazon USD 287.1 132,911 135.8 82.1 52.0 1.5 1.2 1.0 1.5 1.2 1.0 n.a. 1.3 0.9 9.6% 15.0% 21.5% Buy

EBAY US eBay USD 51.1 63,510 17.2 16.0 14.1 3.2 2.8 2.5 3.5 3.1 2.8 3.7 1.8 1.0 16.7% 17.4% 16.5% Hold

ZU US Zulily USD 37.1 4,636 175.9 80.3 43.9 3.8 2.6 1.9 3.8 2.5 1.8 2.7 1.2 0.7 7.1% n.a. n.a. NC

YOOX EU Yoox S.p.A. EUR 14.6 1,104 54.1 37.6 27.9 1.6 1.3 1.1 1.6 1.3 1.1 1.7 1.2 0.9 12.0% 14.8% 17.0% NC

MELI US MercadoLibre USD 112.2 4,952 49.6 37.3 31.1 9.4 7.9 6.3 9.7 8.3 6.8 2.5 1.8 1.5 27.9% 30.3% 29.4% NC

4755 JP Rakuten JPY 1,176.0 14,447 28.4 21.8 17.7 2.8 2.5 2.1 2.7 2.4 2.1 1.7 1.3 1.0 16.3% 18.9% 19.8% Hold

ASC LN ASOS GBP 2,107.0 2,825 51.6 48.0 37.6 1.7 1.5 1.2 1.8 1.5 1.2 2.3 2.1 1.7 19.4% 16.8% 18.3% Buy

56.1 46.2 32.0 3.4 2.8 2.3 3.5 2.9 2.4 2.4 1.5 1.1 15.6% 18.9% 20.4%

700 HK Tencent HKD 119.5 144,285 35.3 25.0 19.0 10.3 8.4 6.9 10.8 8.9 7.3 0.9 0.6 0.6 29.4% 30.6% 29.8% Buy

3888 HK Kingsoft HKD 17.0 2,596 21.8 15.1 10.2 3.0 1.8 1.1 4.9 3.4 2.4 n.a. n.a. n.a. 16.7% 19.6% 27.1% NC

NTES US Netease USD 92.7 12,119 15.0 13.2 11.7 4.6 3.8 3.0 6.7 5.7 5.0 1.0 0.9 0.8 22.1% 20.9% 19.7% NC

PWRD US Perfect world USD 21.4 1,061 9.5 8.4 7.8 1.3 1.0 0.8 1.7 1.4 1.3 n.a. n.a. n.a. 13.5% 14.8% 14.6% NC

CYOU US Changyou USD 18.2 978 n.a. 13.7 6.4 1.1 1.0 0.8 1.3 1.2 1.1 n.a. n.a. n.a. n.a. 8.1% 13.0% NC

777 HK NetDragon HKD 13.4 879 16.5 14.9 13.5 n.a. n.a. n.a. 5.6 4.8 4.3 n.a. n.a. n.a. 6.7% 7.3% 7.7% NC

434 HK Boyaa HKD 7.2 700 14.2 10.5 7.7 3.1 1.9 1.1 4.5 3.3 2.5 n.a. n.a. n.a. 22.2% 25.3% 25.7% NC

8002 HK IGG HKD 3.4 596 8.2 6.3 4.6 1.9 1.2 0.5 2.9 2.3 1.9 n.a. n.a. n.a. 33.9% 30.9% 32.2% NC

6899 HK Ourgame HKD 4.1 414 15.0 10.3 6.9 2.8 1.9 1.1 4.3 3.1 2.2 0.0 0.2 0.1 16.6% 21.7% 24.7% Buy

16.9 13.0 9.8 3.5 2.6 1.9 4.7 3.8 3.1 0.7 0.6 0.5 20.1% 19.9% 21.6%

BABA US Alibaba USD 95.8 238,553 46.2 35.3 26.5 19.3 13.8 10.2 19.8 15.0 11.6 2.6 1.1 0.8 44.9% 24.2% 23.4% Buy

700 HK Tencent HKD 119.5 144,285 35.3 25.0 19.0 10.3 8.4 6.9 10.8 8.9 7.3 0.9 0.6 0.6 29.4% 30.6% 29.8% Buy

NTES US Netease USD 92.7 12,119 15.0 13.2 11.7 4.6 3.8 3.0 6.7 5.7 5.0 1.0 0.9 0.8 22.1% 20.9% 19.7% NC

SINA US Sina USD 39.8 2,655 40.4 30.8 16.3 1.1 0.9 0.6 3.4 2.9 2.4 n.a. 1.0 0.2 2.7% 3.4% 6.1% Hold

BIDU US Baidu USD 222.6 78,028 37.9 25.8 18.9 9.2 5.8 4.2 9.8 6.6 5.0 n.a. 0.6 0.5 24.3% 26.0% 26.2% Buy

SOHU US Sohu USD 44.0 1,694 n.a. n.a. 29.0 0.7 0.6 0.5 1.0 0.8 0.7 n.a. n.a. 1.3 n.a. n.a. 2.1% NC

RENN US Renren USD 3.4 1,356 n.a. n.a. n.a. 5.6 6.2 5.6 15.6 14.3 11.2 n.a. n.a. 1.0 n.a. n.a. n.a. Underperform

YOKU US Youku USD 18.8 3,914 n.a. 216.4 30.6 3.7 2.7 1.8 6.0 4.4 3.3 n.a. n.a. n.a. n.a. 0.4% 5.2% NC

QIHU US Qihoo 360 USD 68.2 8,587 28.6 17.7 11.1 6.0 3.9 2.6 6.6 4.5 3.3 0.7 0.3 0.2 30.3% 33.1% 34.5% Buy

SFUN.US Soufun USD 10.0 4,099 15.3 11.8 9.7 5.1 3.8 2.8 5.6 4.6 3.8 1.2 1.0 0.8 51.6% 42.9% 35.7% NC

ATHM US Autohome USD 49.9 5,251 48.2 35.4 25.7 16.0 11.0 8.0 16.7 11.9 9.0 1.2 0.9 0.6 28.0% 27.2% 27.7% NC

BITA US BitAuto USD 80.0 3,524 46.5 29.8 22.4 9.7 6.9 5.4 10.3 7.6 6.2 0.8 0.5 0.4 19.2% 21.5% 22.3% NC

AMCN US Air media USD 2.2 131 n.a. 32.6 16.5 0.3 0.3 0.2 0.5 0.5 0.4 n.a. n.a. n.a. n.a. -0.2% 1.1% NC

WUBA US 58.com USD 38.1 3,339 634.2 158.5 20.2 11.8 7.8 5.2 13.3 8.8 6.1 n.a. n.a. n.a. 3.8% 9.8% 25.7% NC

CMCM US Cheetah Mobile USD 16.7 2,334 59.6 21.1 9.0 7.8 3.7 1.7 8.5 4.3 2.4 0.5 0.2 0.1 20.2% 38.3% 52.0% NC

CTRP US Ctrip USD 57.1 7,392 53.7 33.1 22.3 5.5 3.9 2.7 6.1 4.6 3.4 1.8 1.1 0.7 8.5% 13.4% 17.2% NC

QUNR US Qunar USD 26.8 3,175 n.a. n.a. 97.7 11.1 6.7 4.2 11.4 6.6 4.2 n.a. n.a. n.a. n.a. n.a. n.a. NC

LONG US Elong USD 19.4 685 118.3 45.5 24.7 n.a. n.a. n.a. 3.3 2.7 2.4 n.a. n.a. n.a. n.a. n.a. n.a. NC

2280 HK HC International HKD 9.9 849 20.9 12.8 7.7 3.6 2.1 1.0 4.7 3.3 2.2 0.4 0.2 0.1 23.0% 29.1% 34.7% Buy

DANG US Dangdang USD 12.2 994 60.6 20.7 11.2 0.6 0.5 0.3 0.7 0.6 0.5 2.0 0.7 0.4 15.2% 37.8% 40.7% NC

JD US JD.com USD 24.0 32,837 n.a. n.a. 76.6 1.3 0.9 0.7 1.5 1.1 0.8 n.a. n.a. n.a. n.a. n.a. 0.5% Buy

VIPS US Vipshop USD 213.6 12,071 66.6 40.1 25.3 3.2 2.0 1.3 3.3 2.1 1.5 0.4 0.6 0.4 30.6% 34.8% 36.3% Buy

JMEI US Jumei USD 22.0 3,150 39.4 21.9 14.5 3.8 2.5 1.7 4.7 3.4 2.5 0.6 0.3 0.2 18.3% 22.8% 26.0% NC

VISN US Vision China USD 11.6 59 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. NC

CCIH US ChinaCache USD 11.8 300 147.1 53.5 357.6 1.0 0.8 0.6 1.2 0.9 0.7 n.a. n.a. n.a. 3.7% 6.6% 10.9% NC

EDU US New oriental USD 22.4 3,540 14.7 14.8 12.8 2.2 2.0 1.7 3.0 2.6 2.2 0.3 2.2 0.8 25.0% 23.1% 22.3% Hold

1980 HK Tian Ge HKD 4.9 803 14.5 14.7 11.9 2.9 2.6 1.8 6.0 5.4 4.4 0.4 0.9 0.5 24.7% 12.9% 14.0% Buy

YY US YY USD 81.9 4,580 29.9 20.8 14.4 7.3 4.6 3.1 8.0 5.4 3.9 0.3 0.2 0.1 39.8% 39.4% 35.4% NC

JOBS US 51job USD 30.2 1,795 18.5 15.6 12.6 4.8 4.0 3.2 6.0 5.2 4.4 n.a. n.a. n.a. 14.3% 16.6% 16.8% NC

36.4 26.0 20.0 4.9 4.2 3.0 5.7 5.2 4.0 0.9 0.7 0.5 22.8% 22.4% 22.7%

30.6 22.2 19.6 4.7 3.5 2.7 6.0 4.5 3.7 0.9 0.7 0.5 22.1% 21.7% 22.4%

Rating PE EV/Sales Price to Sales PEG ROE

Ticker Company FX Last Close Market Cap

USD mn

China e-Commerce Average

Global e-Commerce Average (ex Zulily FY14 P/E)

China Game Average

Internet/New Media Avg (excl. P/E ratio >80, EV/S and P/S >15)

Internet overall (excl. P/E ratio >80, EV/S and P/S >15)

BABA

Initiating Coverage

27 October 2014

page 10 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Changing Demographics and Mobile Support E-Commerce in the Next Decade

China’s e-Commerce market is forecast to grow at a 2013-2018 CAGR of 28%, accounting

for 10.4% of total retail sales in 2014. As discussed in our sector note, “A Taste of

Domestic Consumption: The Unleashing of China’s E-Commerce Power” published on

Sept 19, 2014, China’s e-Commerce growth is driven by secular trends including

urbanization and increasing household income, rising smartphone and Internet

penetration, the mix shift towards more mature Internet user demographics, as well as

improving communications and transportation infrastructure.

In this section, we discuss the following:

1. Favorable government policy and increasing urbanization drives domestic

consumption as household income rises.

2. Our analysis shows that China's Internet users aged 30+ years will account for

54% of total Internet users by 2018, up from 33% in 2008, and 81% of the

240mn new incremental Internet users will be 30+ years old. Internet

demographics mix shift to more 30+ year old age groups indicates huge

opportunities in e-Commerce as these users adopt online shopping.

3. China’s relatively low penetration of consumption, Internet, e-Commerce and

online shoppers compared to developed countries suggests ample room for

growth.

4. Given the proliferation of affordable smart devices, improving wireless 3G and

4G coverage and user experience, expected further data pricing declines due to

LTE promotions by the telcos, we believe that m-Commerce is still at very early

stage of monetization.

5. Accelerating structural shift to online from traditional retail. According to

linkshop.cn’s 1H14 survey, the revenues of 73 surveyed offline retailers showed

only moderate YoY growth. In the department store category, 34 out of the 54

surveyed stores posted revenue decline with average sales down by 2% YoY in

1H14.

BABA

Initiating Coverage

27 October 2014

page 11 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Changing Demographics and Mobile Support E-Commerce in the Next Decade

China’s online retail sales market is expected to reach RMB2.8trn in 2014, +45.8% YoY,

accounting for 10.4% of total retail sales. We estimate the market size to further grow to

RMB6.5trn in 2018, with a 2013-2018 CAGR of 28%. In our view, China’s e-Commerce

growth is driven by secular trends including urbanization and increasing household

income, the mix shift towards more mature Internet user demographics, rising

smartphone and Internet penetration as well as improving communications and

transportation infrastructure. This leads to accelerating structural shift to online from

traditional retail.

Chart 5: China online retail sales (2007A-2018E)

Source: iResearch (2007A-2017E) as of Jul 2014, Jefferies estimates (2018E)

Chart 6: China online retail sales structure (2008A-2018E)

Source: iResearch (2008A-2017E) as of Jul 2014, Jefferies estimates (2018E)

China’s online retail sales market is

expected to reach RMB2.8trn in

2014, +45.8% YoY, accounting for

10.4% of total retail sales.

We estimate the market size to

further grow to RMB6.5trn in 2018,

with a 2013-2018 CAGR of 28%.

B2C market is estimated to account

for 48% of total online retail sales in

2014 and 62% in 2018.

BABA

Initiating Coverage

27 October 2014

page 12 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

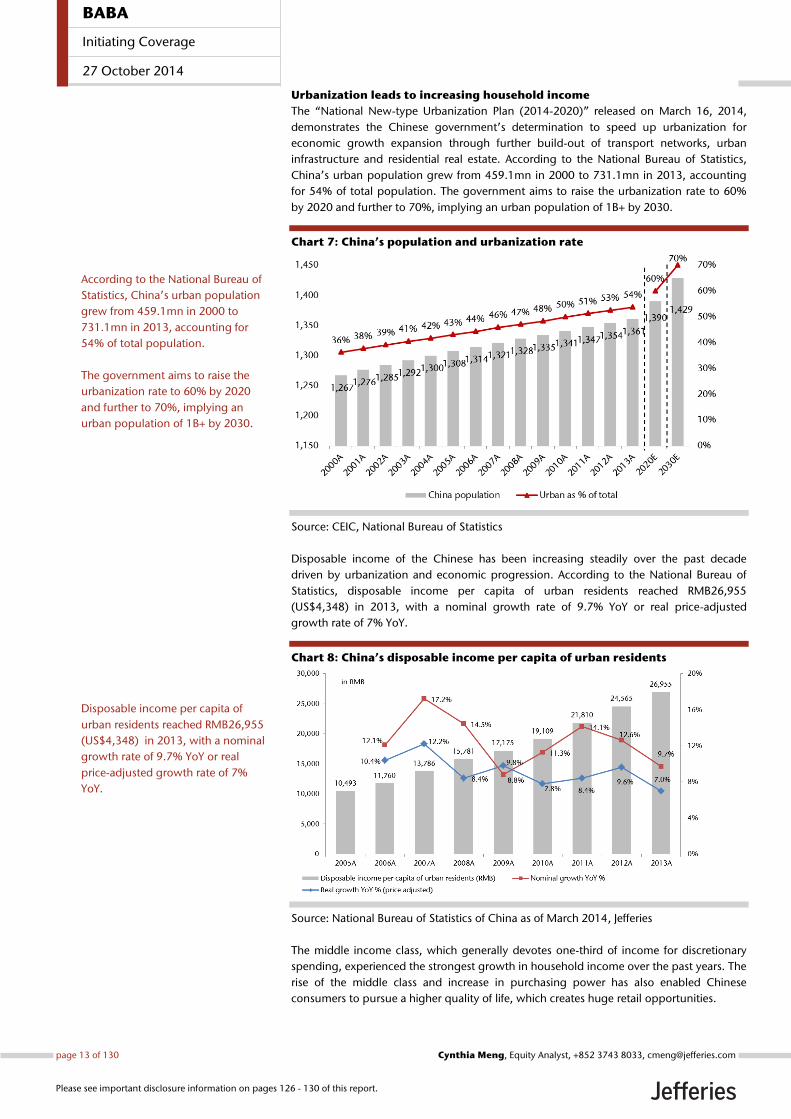

Urbanization leads to increasing household income

The “National New-type Urbanization Plan (2014-2020)” released on March 16, 2014,

demonstrates the Chinese government’s determination to speed up urbanization for

economic growth expansion through further build-out of transport networks, urban

infrastructure and residential real estate. According to the National Bureau of Statistics,

China’s urban population grew from 459.1mn in 2000 to 731.1mn in 2013, accounting

for 54% of total population. The government aims to raise the urbanization rate to 60%

by 2020 and further to 70%, implying an urban population of 1B+ by 2030.

Chart 7: China’s population and urbanization rate

Source: CEIC, National Bureau of Statistics

Disposable income of the Chinese has been increasing steadily over the past decade

driven by urbanization and economic progression. According to the National Bureau of

Statistics, disposable income per capita of urban residents reached RMB26,955

(US$4,348) in 2013, with a nominal growth rate of 9.7% YoY or real price-adjusted

growth rate of 7% YoY.

Chart 8: China’s disposable income per capita of urban residents

Source: National Bureau of Statistics of China as of March 2014, Jefferies

The middle income class, which generally devotes one-third of income for discretionary

spending, experienced the strongest growth in household income over the past years. The

rise of the middle class and increase in purchasing power has also enabled Chinese

consumers to pursue a higher quality of life, which creates huge retail opportunities.

Disposable income per capita of

urban residents reached RMB26,955

(US$4,348) in 2013, with a nominal

growth rate of 9.7% YoY or real

price-adjusted growth rate of 7%

YoY.

According to the National Bureau of

Statistics, China’s urban population

grew from 459.1mn in 2000 to

731.1mn in 2013, accounting for

54% of total population.

The government aims to raise the

urbanization rate to 60% by 2020

and further to 70%, implying an

urban population of 1B+ by 2030.

BABA

Initiating Coverage

27 October 2014

page 13 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

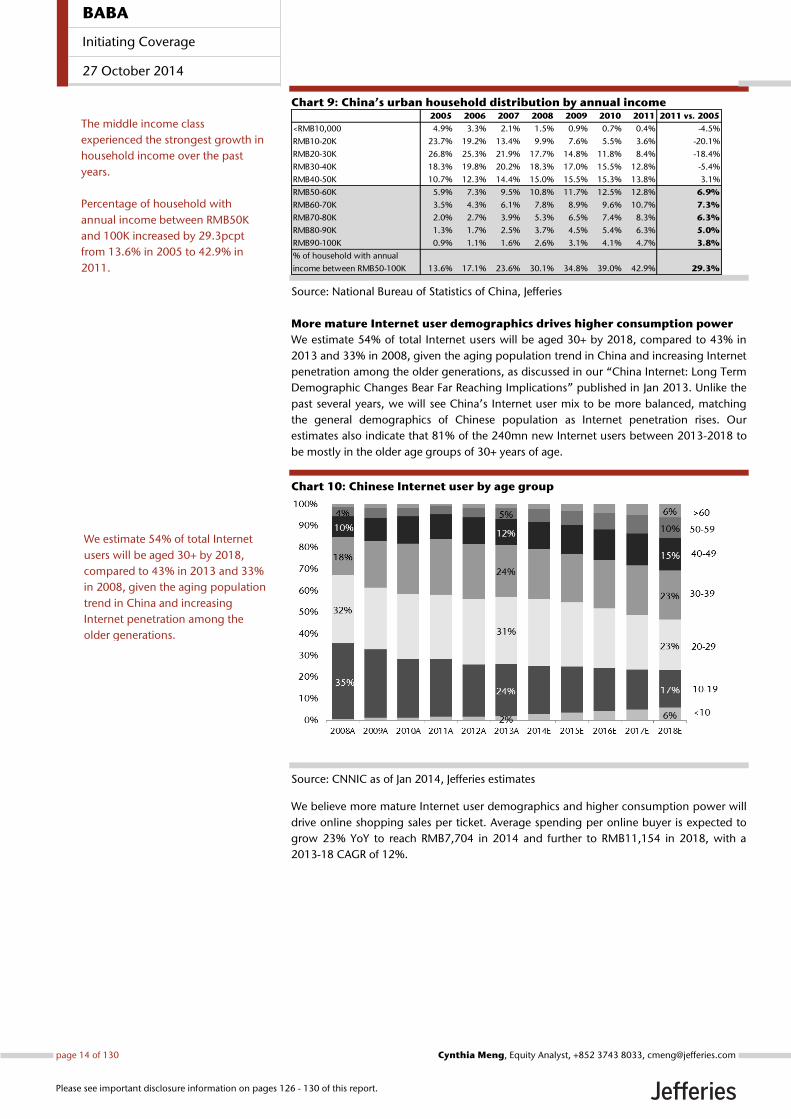

Chart 9: China’s urban household distribution by annual income

Source: National Bureau of Statistics of China, Jefferies

More mature Internet user demographics drives higher consumption power

We estimate 54% of total Internet users will be aged 30+ by 2018, compared to 43% in

2013 and 33% in 2008, given the aging population trend in China and increasing Internet

penetration among the older generations, as discussed in our “China Internet: Long Term

Demographic Changes Bear Far Reaching Implications” published in Jan 2013. Unlike the

past several years, we will see China’s Internet user mix to be more balanced, matching

the general demographics of Chinese population as Internet penetration rises. Our

estimates also indicate that 81% of the 240mn new Internet users between 2013-2018 to

be mostly in the older age groups of 30+ years of age.

Chart 10: Chinese Internet user by age group

Source: CNNIC as of Jan 2014, Jefferies estimates

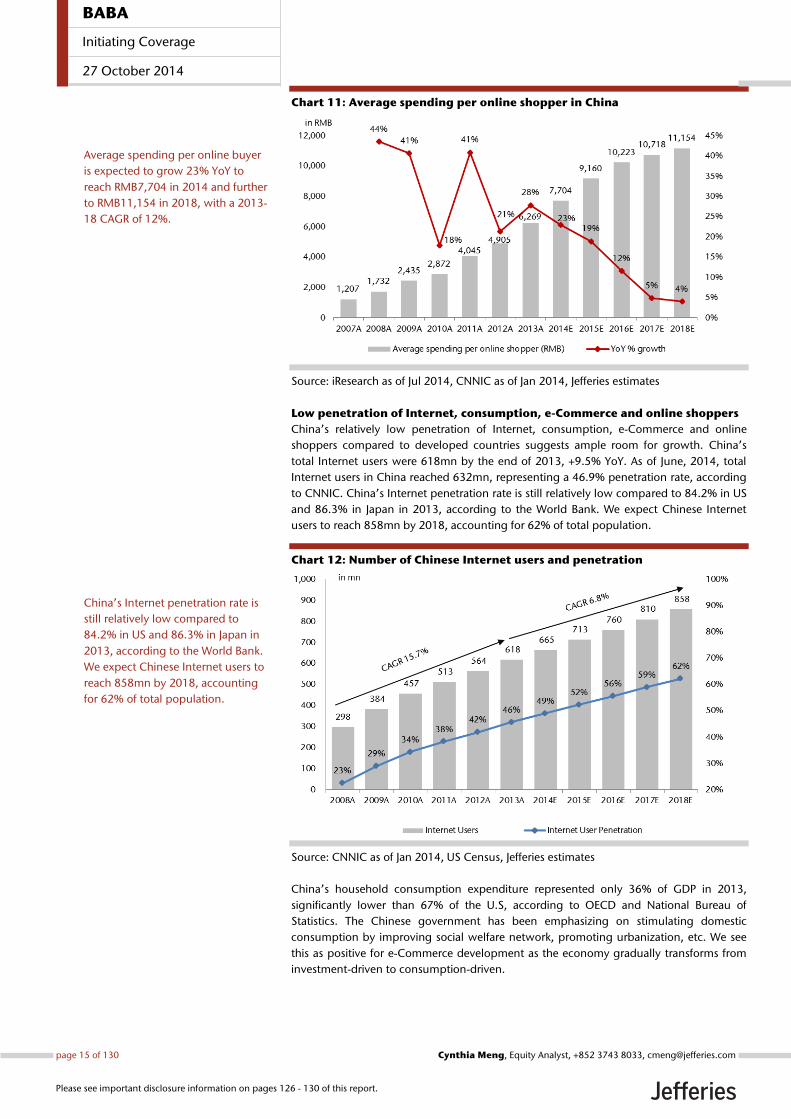

We believe more mature Internet user demographics and higher consumption power will

drive online shopping sales per ticket. Average spending per online buyer is expected to

grow 23% YoY to reach RMB7,704 in 2014 and further to RMB11,154 in 2018, with a

2013-18 CAGR of 12%.

2005 2006 2007 2008 2009 2010 2011 2011 vs. 2005

<RMB10,000 4.9% 3.3% 2.1% 1.5% 0.9% 0.7% 0.4% -4.5%

RMB10-20K 23.7% 19.2% 13.4% 9.9% 7.6% 5.5% 3.6% -20.1%

RMB20-30K 26.8% 25.3% 21.9% 17.7% 14.8% 11.8% 8.4% -18.4%

RMB30-40K 18.3% 19.8% 20.2% 18.3% 17.0% 15.5% 12.8% -5.4%

RMB40-50K 10.7% 12.3% 14.4% 15.0% 15.5% 15.3% 13.8% 3.1%

RMB50-60K 5.9% 7.3% 9.5% 10.8% 11.7% 12.5% 12.8% 6.9%

RMB60-70K 3.5% 4.3% 6.1% 7.8% 8.9% 9.6% 10.7% 7.3%

RMB70-80K 2.0% 2.7% 3.9% 5.3% 6.5% 7.4% 8.3% 6.3%

RMB80-90K 1.3% 1.7% 2.5% 3.7% 4.5% 5.4% 6.3% 5.0%

RMB90-100K 0.9% 1.1% 1.6% 2.6% 3.1% 4.1% 4.7% 3.8%

% of household with annual

income between RMB50-100K 13.6% 17.1% 23.6% 30.1% 34.8% 39.0% 42.9% 29.3%

The middle income class

experienced the strongest growth in

household income over the past

years.

Percentage of household with

annual income between RMB50K

and 100K increased by 29.3pcpt

from 13.6% in 2005 to 42.9% in

2011.

We estimate 54% of total Internet

users will be aged 30+ by 2018,

compared to 43% in 2013 and 33%

in 2008, given the aging population

trend in China and increasing

Internet penetration among the

older generations.

BABA

Initiating Coverage

27 October 2014

page 14 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Chart 11: Average spending per online shopper in China

Source: iResearch as of Jul 2014, CNNIC as of Jan 2014, Jefferies estimates

Low penetration of Internet, consumption, e-Commerce and online shoppers

China’s relatively low penetration of Internet, consumption, e-Commerce and online

shoppers compared to developed countries suggests ample room for growth. China’s

total Internet users were 618mn by the end of 2013, +9.5% YoY. As of June, 2014, total

Internet users in China reached 632mn, representing a 46.9% penetration rate, according

to CNNIC. China’s Internet penetration rate is still relatively low compared to 84.2% in US

and 86.3% in Japan in 2013, according to the World Bank. We expect Chinese Internet

users to reach 858mn by 2018, accounting for 62% of total population.

Chart 12: Number of Chinese Internet users and penetration

Source: CNNIC as of Jan 2014, US Census, Jefferies estimates

China’s household consumption expenditure represented only 36% of GDP in 2013,

significantly lower than 67% of the U.S, according to OECD and National Bureau of

Statistics. The Chinese government has been emphasizing on stimulating domestic

consumption by improving social welfare network, promoting urbanization, etc. We see

this as positive for e-Commerce development as the economy gradually transforms from

investment-driven to consumption-driven.

Average spending per online buyer

is expected to grow 23% YoY to

reach RMB7,704 in 2014 and further

to RMB11,154 in 2018, with a 2013-

18 CAGR of 12%.

China’s Internet penetration rate is

still relatively low compared to

84.2% in US and 86.3% in Japan in

2013, according to the World Bank.

We expect Chinese Internet users to

reach 858mn by 2018, accounting

for 62% of total population.

BABA

Initiating Coverage

27 October 2014

page 15 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Chart 13: China’s household consumption expenditure

growth (2003-2013)

Source: National Bureau of Statistics, Jefferies

Note: The household consumption refers to the market value of

goods and services purchased by households including both real

and imputed consumption expenses, according to China’s National

Bureau of Statistics.

Chart 14: Comparison of household consumption

expenditure in China Vs. US (2003-2013)

Source: National Bureau of Statistics, OECD, Jefferies

Note: US data refers to OECD. The household consumption data

refers to market value of all goods and services purchased by

households, including durable products, imputed rent for owner-

occupied dwellings and payments and fees to governments to

obtain permits and licenses.

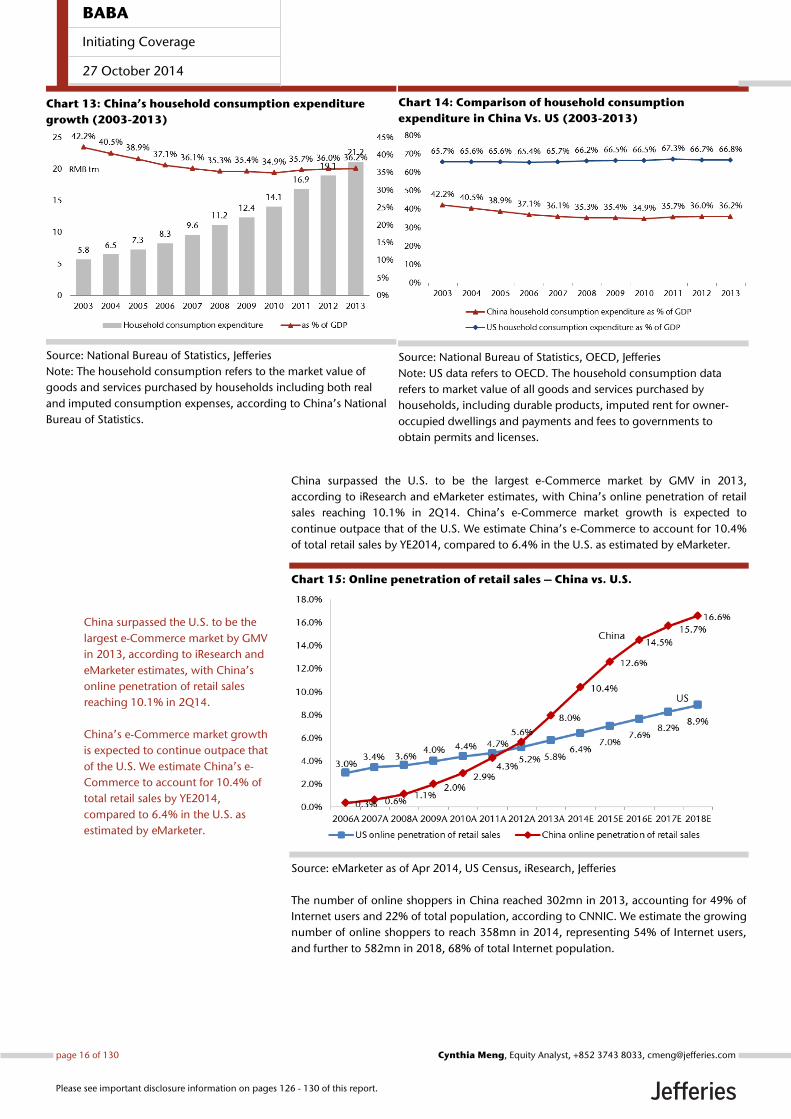

China surpassed the U.S. to be the largest e-Commerce market by GMV in 2013,

according to iResearch and eMarketer estimates, with China’s online penetration of retail

sales reaching 10.1% in 2Q14. China’s e-Commerce market growth is expected to

continue outpace that of the U.S. We estimate China’s e-Commerce to account for 10.4%

of total retail sales by YE2014, compared to 6.4% in the U.S. as estimated by eMarketer.

Chart 15: Online penetration of retail sales – China vs. U.S.

Source: eMarketer as of Apr 2014, US Census, iResearch, Jefferies

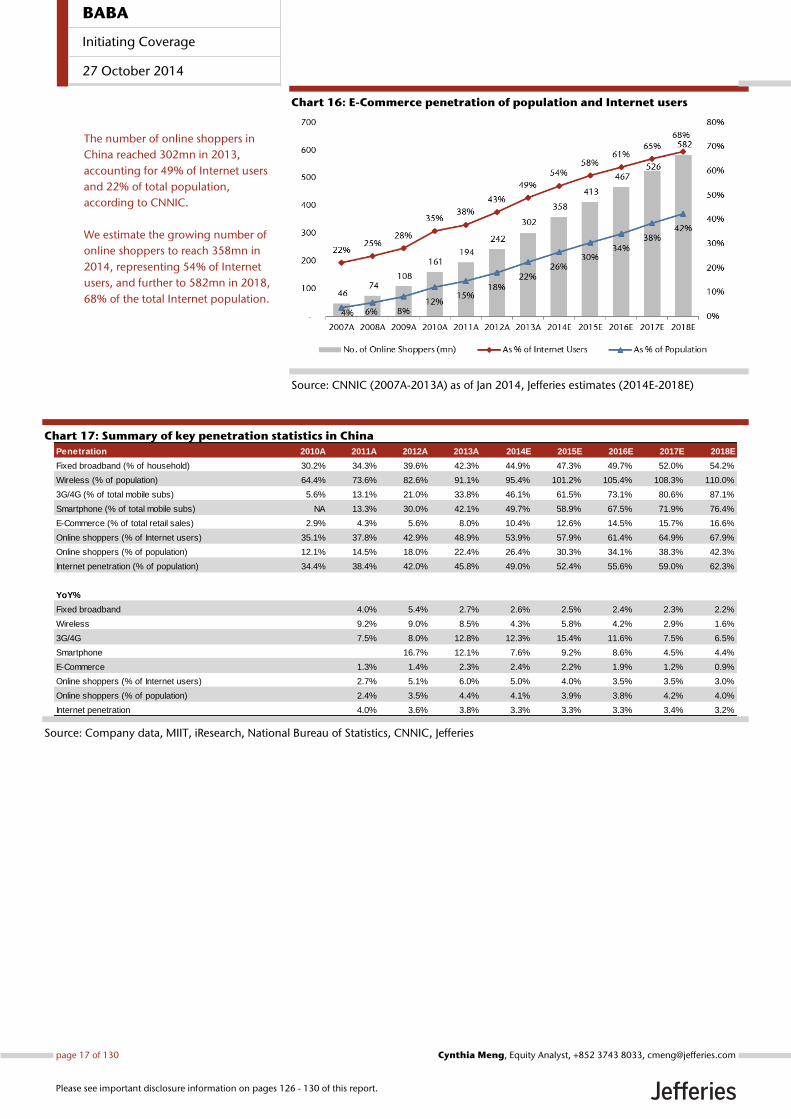

The number of online shoppers in China reached 302mn in 2013, accounting for 49% of

Internet users and 22% of total population, according to CNNIC. We estimate the growing

number of online shoppers to reach 358mn in 2014, representing 54% of Internet users,

and further to 582mn in 2018, 68% of total Internet population.

China surpassed the U.S. to be the

largest e-Commerce market by GMV

in 2013, according to iResearch and

eMarketer estimates, with China’s

online penetration of retail sales

reaching 10.1% in 2Q14.

China’s e-Commerce market growth

is expected to continue outpace that

of the U.S. We estimate China’s e-

Commerce to account for 10.4% of

total retail sales by YE2014,

compared to 6.4% in the U.S. as

estimated by eMarketer.

BABA

Initiating Coverage

27 October 2014

page 16 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Chart 16: E-Commerce penetration of population and Internet users

Source: CNNIC (2007A-2013A) as of Jan 2014, Jefferies estimates (2014E-2018E)

Chart 17: Summary of key penetration statistics in China

Source: Company data, MIIT, iResearch, National Bureau of Statistics, CNNIC, Jefferies

Penetration 2010A 2011A 2012A 2013A 2014E 2015E 2016E 2017E 2018E

Fixed broadband (% of household) 30.2% 34.3% 39.6% 42.3% 44.9% 47.3% 49.7% 52.0% 54.2%

Wireless (% of population) 64.4% 73.6% 82.6% 91.1% 95.4% 101.2% 105.4% 108.3% 110.0%

3G/4G (% of total mobile subs) 5.6% 13.1% 21.0% 33.8% 46.1% 61.5% 73.1% 80.6% 87.1%

Smartphone (% of total mobile subs) NA 13.3% 30.0% 42.1% 49.7% 58.9% 67.5% 71.9% 76.4%

E-Commerce (% of total retail sales) 2.9% 4.3% 5.6% 8.0% 10.4% 12.6% 14.5% 15.7% 16.6%

Online shoppers (% of Internet users) 35.1% 37.8% 42.9% 48.9% 53.9% 57.9% 61.4% 64.9% 67.9%

Online shoppers (% of population) 12.1% 14.5% 18.0% 22.4% 26.4% 30.3% 34.1% 38.3% 42.3%

Internet penetration (% of population) 34.4% 38.4% 42.0% 45.8% 49.0% 52.4% 55.6% 59.0% 62.3%

YoY%

Fixed broadband 4.0% 5.4% 2.7% 2.6% 2.5% 2.4% 2.3% 2.2%

Wireless 9.2% 9.0% 8.5% 4.3% 5.8% 4.2% 2.9% 1.6%

3G/4G 7.5% 8.0% 12.8% 12.3% 15.4% 11.6% 7.5% 6.5%

Smartphone 16.7% 12.1% 7.6% 9.2% 8.6% 4.5% 4.4%

E-Commerce 1.3% 1.4% 2.3% 2.4% 2.2% 1.9% 1.2% 0.9%

Online shoppers (% of Internet users) 2.7% 5.1% 6.0% 5.0% 4.0% 3.5% 3.5% 3.0%

Online shoppers (% of population) 2.4% 3.5% 4.4% 4.1% 3.9% 3.8% 4.2% 4.0%

Internet penetration 4.0% 3.6% 3.8% 3.3% 3.3% 3.3% 3.4% 3.2%

The number of online shoppers in

China reached 302mn in 2013,

accounting for 49% of Internet users

and 22% of total population,

according to CNNIC.

We estimate the growing number of

online shoppers to reach 358mn in

2014, representing 54% of Internet

users, and further to 582mn in 2018,

68% of the total Internet population.

BABA

Initiating Coverage

27 October 2014

page 17 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

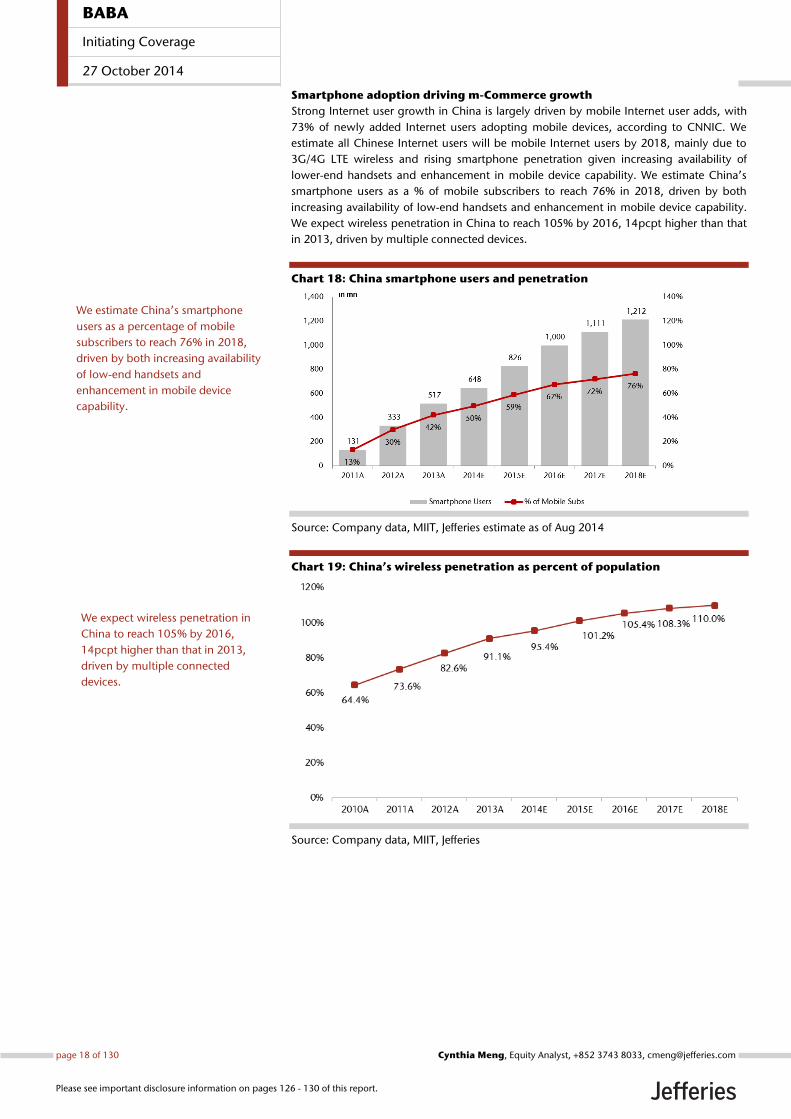

Smartphone adoption driving m-Commerce growth

Strong Internet user growth in China is largely driven by mobile Internet user adds, with

73% of newly added Internet users adopting mobile devices, according to CNNIC. We

estimate all Chinese Internet users will be mobile Internet users by 2018, mainly due to

3G/4G LTE wireless and rising smartphone penetration given increasing availability of

lower-end handsets and enhancement in mobile device capability. We estimate China’s

smartphone users as a % of mobile subscribers to reach 76% in 2018, driven by both

increasing availability of low-end handsets and enhancement in mobile device capability.

We expect wireless penetration in China to reach 105% by 2016, 14pcpt higher than that

in 2013, driven by multiple connected devices.

Chart 18: China smartphone users and penetration

Source: Company data, MIIT, Jefferies estimate as of Aug 2014

Chart 19: China’s wireless penetration as percent of population

Source: Company data, MIIT, Jefferies

We estimate China’s smartphone

users as a percentage of mobile

subscribers to reach 76% in 2018,

driven by both increasing availability

of low-end handsets and

enhancement in mobile device

capability.

We expect wireless penetration in

China to reach 105% by 2016,

14pcpt higher than that in 2013,

driven by multiple connected

devices.

BABA

Initiating Coverage

27 October 2014

page 18 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

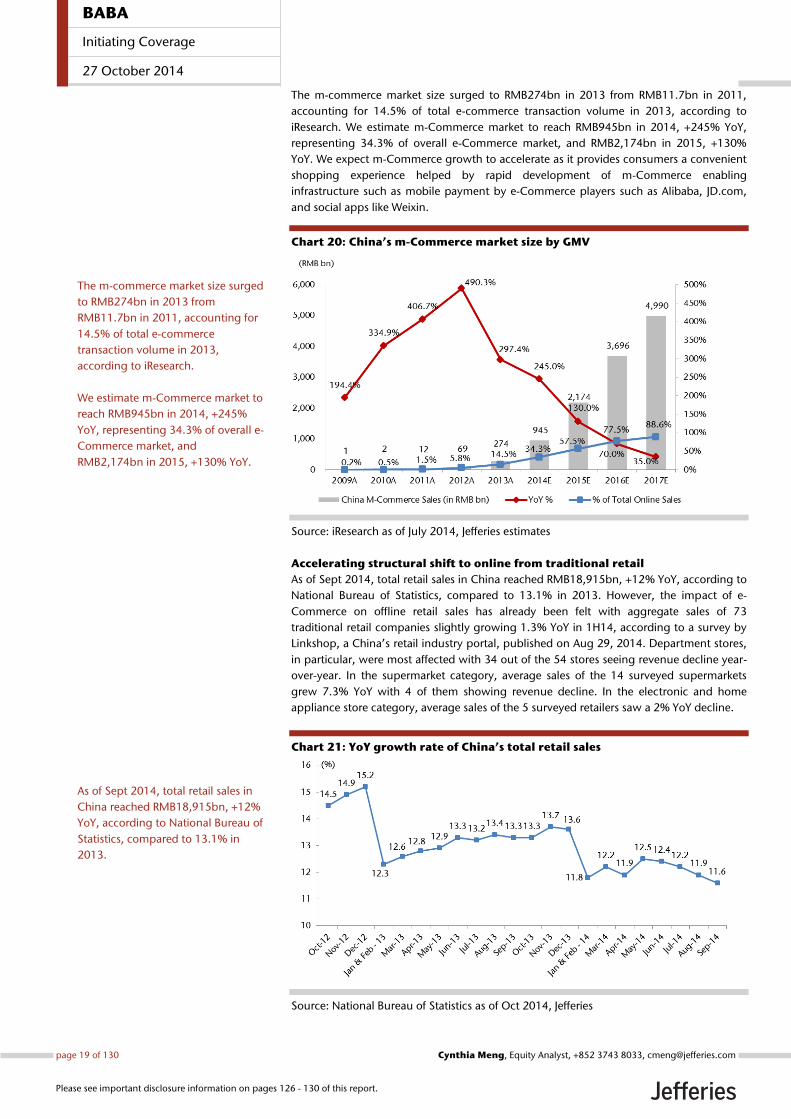

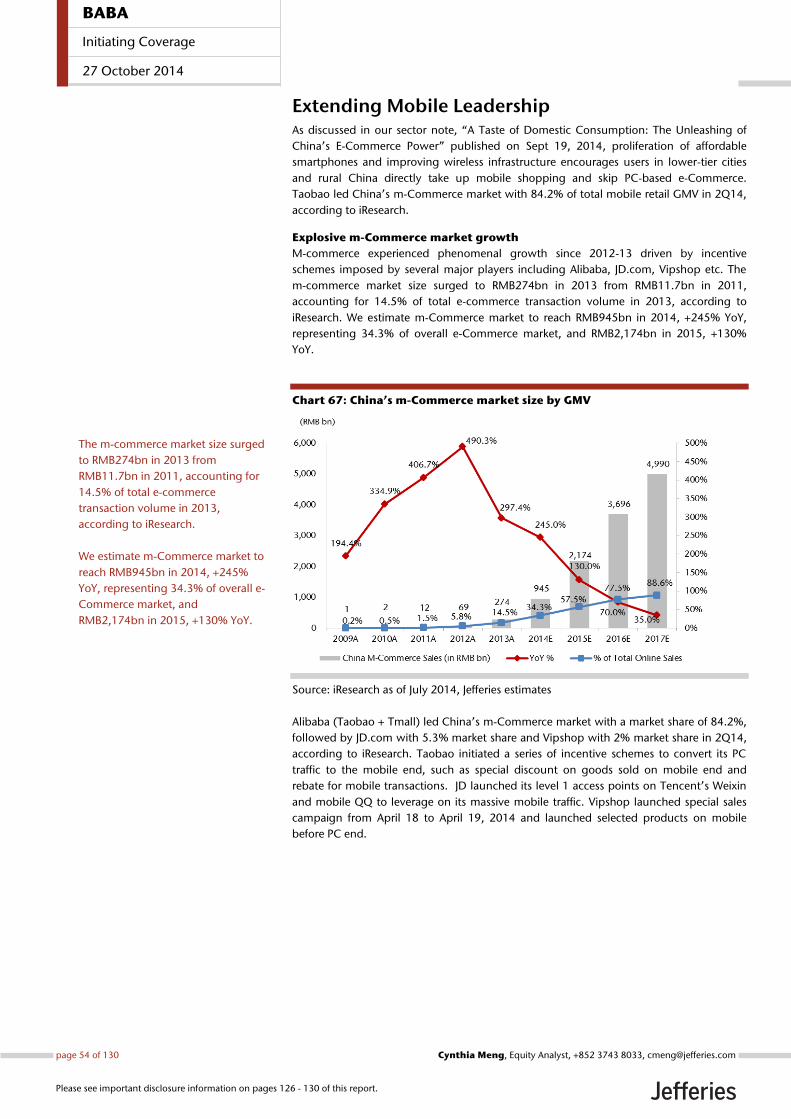

The m-commerce market size surged to RMB274bn in 2013 from RMB11.7bn in 2011,

accounting for 14.5% of total e-commerce transaction volume in 2013, according to

iResearch. We estimate m-Commerce market to reach RMB945bn in 2014, +245% YoY,

representing 34.3% of overall e-Commerce market, and RMB2,174bn in 2015, +130%

YoY. We expect m-Commerce growth to accelerate as it provides consumers a convenient

shopping experience helped by rapid development of m-Commerce enabling

infrastructure such as mobile payment by e-Commerce players such as Alibaba, JD.com,

and social apps like Weixin.

Chart 20: China’s m-Commerce market size by GMV

Source: iResearch as of July 2014, Jefferies estimates

Accelerating structural shift to online from traditional retail

As of Sept 2014, total retail sales in China reached RMB18,915bn, +12% YoY, according to

National Bureau of Statistics, compared to 13.1% in 2013. However, the impact of e-

Commerce on offline retail sales has already been felt with aggregate sales of 73

traditional retail companies slightly growing 1.3% YoY in 1H14, according to a survey by

Linkshop, a China’s retail industry portal, published on Aug 29, 2014. Department stores,

in particular, were most affected with 34 out of the 54 stores seeing revenue decline year-

over-year. In the supermarket category, average sales of the 14 surveyed supermarkets

grew 7.3% YoY with 4 of them showing revenue decline. In the electronic and home

appliance store category, average sales of the 5 surveyed retailers saw a 2% YoY decline.

Chart 21: YoY growth rate of China’s total retail sales

Source: National Bureau of Statistics as of Oct 2014, Jefferies

The m-commerce market size surged

to RMB274bn in 2013 from

RMB11.7bn in 2011, accounting for

14.5% of total e-commerce

transaction volume in 2013,

according to iResearch.

We estimate m-Commerce market to

reach RMB945bn in 2014, +245%

YoY, representing 34.3% of overall e-

Commerce market, and

RMB2,174bn in 2015, +130% YoY.

As of Sept 2014, total retail sales in

China reached RMB18,915bn, +12%

YoY, according to National Bureau of

Statistics, compared to 13.1% in

2013.

BABA

Initiating Coverage

27 October 2014

page 19 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

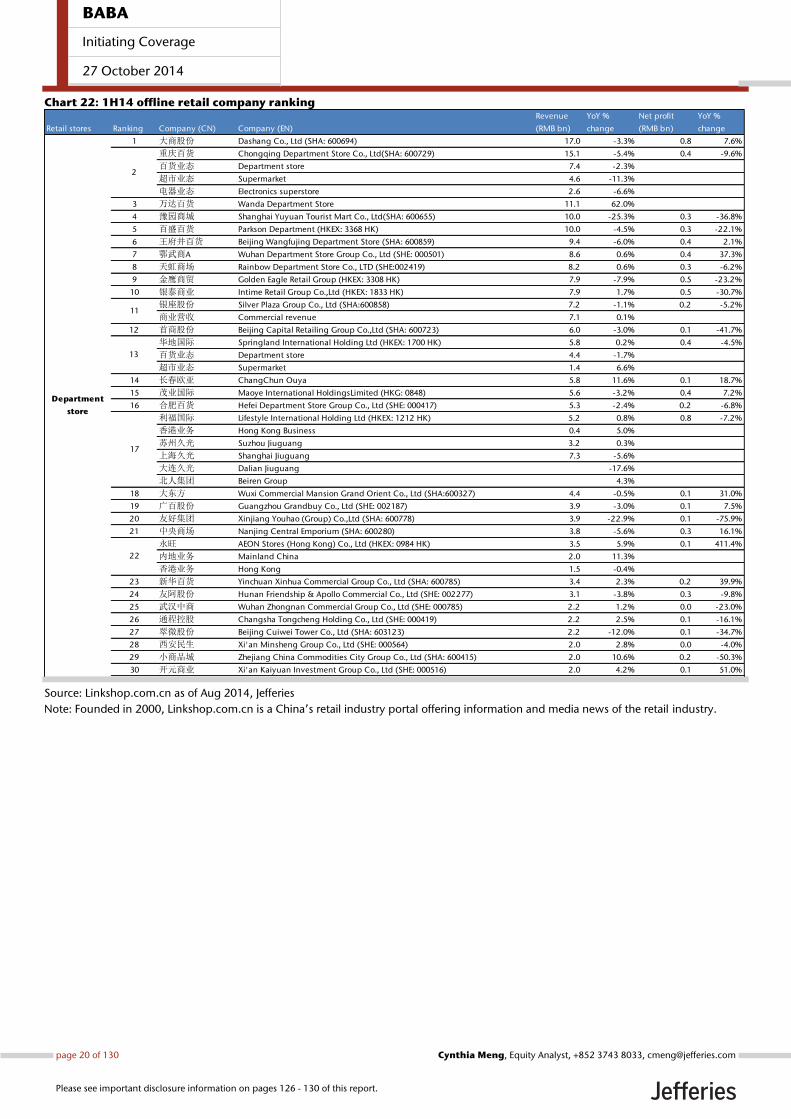

Chart 22: 1H14 offline retail company ranking

Source: Linkshop.com.cn as of Aug 2014, Jefferies

Note: Founded in 2000, Linkshop.com.cn is a China’s retail industry portal offering information and media news of the retail industry.

Retail stores Ranking Company (CN) Company (EN)

Revenue

(RMB bn)

YoY %

change

Net profit

(RMB bn)

YoY %

change

1 大商股份 Dashang Co., Ltd (SHA: 600694) 17.0 -3.3% 0.8 7.6%

重庆百货 Chongqing Department Store Co., Ltd(SHA: 600729) 15.1 -5.4% 0.4 -9.6%

百货业态 Department store 7.4 -2.3%

超市业态 Supermarket 4.6 -11.3%

电器业态 Electronics superstore 2.6 -6.6%

3 万达百货 Wanda Department Store 11.1 62.0%

4 豫园商城 Shanghai Yuyuan Tourist Mart Co., Ltd(SHA: 600655) 10.0 -25.3% 0.3 -36.8%

5 百盛百货 Parkson Department (HKEX: 3368 HK) 10.0 -4.5% 0.3 -22.1%

6 王府井百货 Beijing Wangfujing Department Store (SHA: 600859) 9.4 -6.0% 0.4 2.1%

7 鄂武商A Wuhan Department Store Group Co., Ltd (SHE: 000501) 8.6 0.6% 0.4 37.3%

8 天虹商场 Rainbow Department Store Co., LTD (SHE:002419) 8.2 0.6% 0.3 -6.2%

9 金鹰商贸 Golden Eagle Retail Group (HKEX: 3308 HK) 7.9 -7.9% 0.5 -23.2%

10 银泰商业 Intime Retail Group Co.,Ltd (HKEX: 1833 HK) 7.9 1.7% 0.5 -30.7%

银座股份 Silver Plaza Group Co., Ltd (SHA:600858) 7.2 -1.1% 0.2 -5.2%

商业营收 Commercial revenue 7.1 0.1%

12 首商股份 Beijing Capital Retailing Group Co.,Ltd (SHA: 600723) 6.0 -3.0% 0.1 -41.7%

华地国际 Springland International Holding Ltd (HKEX: 1700 HK) 5.8 0.2% 0.4 -4.5%

百货业态 Department store 4.4 -1.7%

超市业态 Supermarket 1.4 6.6%

14 长春欧亚 ChangChun Ouya 5.8 11.6% 0.1 18.7%

15 茂业国际 Maoye International HoldingsLimited (HKG: 0848) 5.6 -3.2% 0.4 7.2%

16 合肥百货 Hefei Department Store Group Co., Ltd (SHE: 000417) 5.3 -2.4% 0.2 -6.8%

利福国际 Lifestyle International Holding Ltd (HKEX: 1212 HK) 5.2 0.8% 0.8 -7.2%

香港业务 Hong Kong Business 0.4 5.0%

苏州久光 Suzhou Jiuguang 3.2 0.3%

上海久光 Shanghai Jiuguang 7.3 -5.6%

大连久光 Dalian Jiuguang -17.6%

北人集团 Beiren Group 4.3%

18 大东方 Wuxi Commercial Mansion Grand Orient Co., Ltd (SHA:600327) 4.4 -0.5% 0.1 31.0%

19 广百股份 Guangzhou Grandbuy Co., Ltd (SHE: 002187) 3.9 -3.0% 0.1 7.5%

20 友好集团 Xinjiang Youhao (Group) Co.,Ltd (SHA: 600778) 3.9 -22.9% 0.1 -75.9%

21 中央商场 Nanjing Central Emporium (SHA: 600280) 3.8 -5.6% 0.3 16.1%

永旺 AEON Stores (Hong Kong) Co., Ltd (HKEX: 0984 HK) 3.5 5.9% 0.1 411.4%

内地业务 Mainland China 2.0 11.3%

香港业务 Hong Kong 1.5 -0.4%

23 新华百货 Yinchuan Xinhua Commercial Group Co., Ltd (SHA: 600785) 3.4 2.3% 0.2 39.9%

24 友阿股份 Hunan Friendship & Apollo Commercial Co., Ltd (SHE: 002277) 3.1 -3.8% 0.3 -9.8%

25 武汉中商 Wuhan Zhongnan Commercial Group Co., Ltd (SHE: 000785) 2.2 1.2% 0.0 -23.0%

26 通程控股 Changsha Tongcheng Holding Co., Ltd (SHE: 000419) 2.2 2.5% 0.1 -16.1%

27 翠微股份 Beijing Cuiwei Tower Co., Ltd (SHA: 603123) 2.2 -12.0% 0.1 -34.7%

28 西安民生 Xi'an Minsheng Group Co., Ltd (SHE: 000564) 2.0 2.8% 0.0 -4.0%

29 小商品城 Zhejiang China Commodities City Group Co., Ltd (SHA: 600415) 2.0 10.6% 0.2 -50.3%

30 开元商业 Xi'an Kaiyuan Investment Group Co., Ltd (SHE: 000516) 2.0 4.2% 0.1 51.0%

2

13

17

22

11

Department

store

BABA

Initiating Coverage

27 October 2014

page 20 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

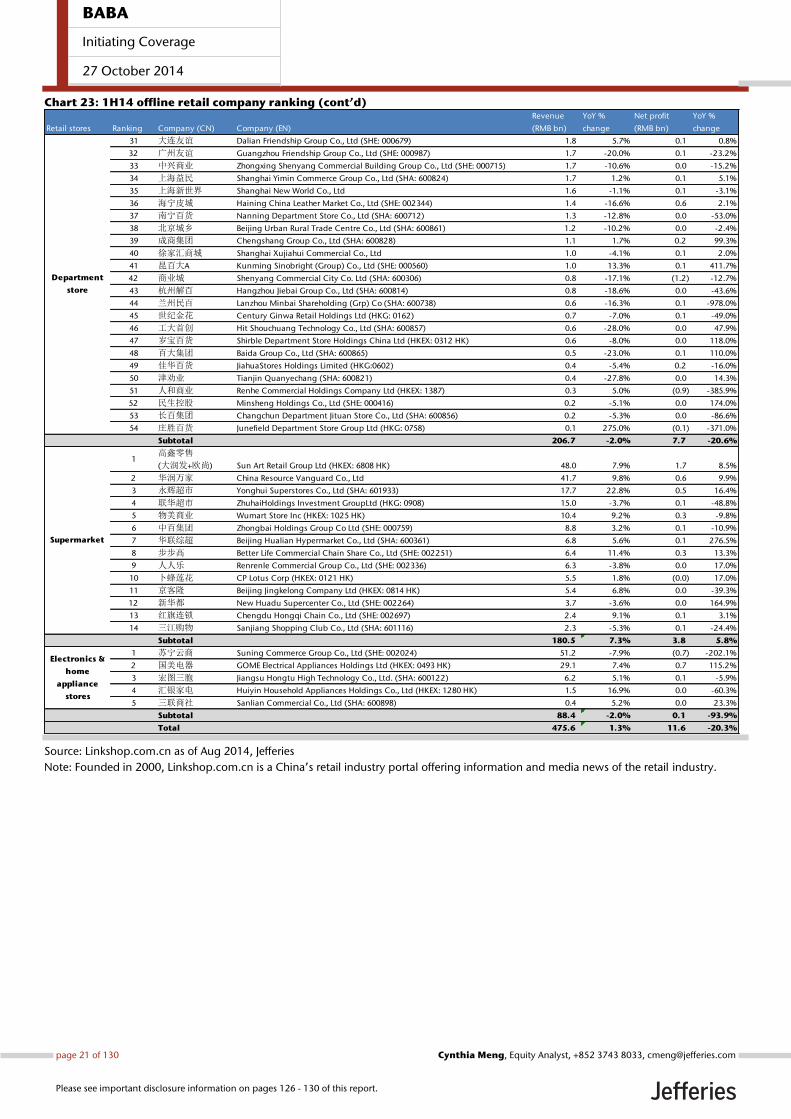

Chart 23: 1H14 offline retail company ranking (cont’d)

Source: Linkshop.com.cn as of Aug 2014, Jefferies

Note: Founded in 2000, Linkshop.com.cn is a China’s retail industry portal offering information and media news of the retail industry.

Retail stores Ranking Company (CN) Company (EN)

Revenue

(RMB bn)

YoY %

change

Net profit

(RMB bn)

YoY %

change

31 大连友谊 Dalian Friendship Group Co., Ltd (SHE: 000679) 1.8 5.7% 0.1 0.8%

32 广州友谊 Guangzhou Friendship Group Co., Ltd (SHE: 000987) 1.7 -20.0% 0.1 -23.2%

33 中兴商业 Zhongxing Shenyang Commercial Building Group Co., Ltd (SHE: 000715) 1.7 -10.6% 0.0 -15.2%

34 上海益民 Shanghai Yimin Commerce Group Co., Ltd (SHA: 600824) 1.7 1.2% 0.1 5.1%

35 上海新世界 Shanghai New World Co., Ltd 1.6 -1.1% 0.1 -3.1%

36 海宁皮城 Haining China Leather Market Co., Ltd (SHE: 002344) 1.4 -16.6% 0.6 2.1%

37 南宁百货 Nanning Department Store Co., Ltd (SHA: 600712) 1.3 -12.8% 0.0 -53.0%

38 北京城乡 Beijing Urban Rural Trade Centre Co., Ltd (SHA: 600861) 1.2 -10.2% 0.0 -2.4%

39 成商集团 Chengshang Group Co., Ltd (SHA: 600828) 1.1 1.7% 0.2 99.3%

40 徐家汇商城 Shanghai Xujiahui Commercial Co., Ltd 1.0 -4.1% 0.1 2.0%

41 昆百大A Kunming Sinobright (Group) Co., Ltd (SHE: 000560) 1.0 13.3% 0.1 411.7%

42 商业城 Shenyang Commercial City Co. Ltd (SHA: 600306) 0.8 -17.1% (1.2) -12.7%

43 杭州解百 Hangzhou Jiebai Group Co., Ltd (SHA: 600814) 0.8 -18.6% 0.0 -43.6%

44 兰州民百 Lanzhou Minbai Shareholding (Grp) Co (SHA: 600738) 0.6 -16.3% 0.1 -978.0%

45 世纪金花 Century Ginwa Retail Holdings Ltd (HKG: 0162) 0.7 -7.0% 0.1 -49.0%

46 工大首创 Hit Shouchuang Technology Co., Ltd (SHA: 600857) 0.6 -28.0% 0.0 47.9%

47 岁宝百货 Shirble Department Store Holdings China Ltd (HKEX: 0312 HK) 0.6 -8.0% 0.0 118.0%

48 百大集团 Baida Group Co., Ltd (SHA: 600865) 0.5 -23.0% 0.1 110.0%

49 佳华百货 JiahuaStores Holdings Limited (HKG:0602) 0.4 -5.4% 0.2 -16.0%

50 津劝业 Tianjin Quanyechang (SHA: 600821) 0.4 -27.8% 0.0 14.3%

51 人和商业 Renhe Commercial Holdings Company Ltd (HKEX: 1387) 0.3 5.0% (0.9) -385.9%

52 民生控股 Minsheng Holdings Co., Ltd (SHE: 000416) 0.2 -5.1% 0.0 174.0%

53 长百集团 Changchun Department Jituan Store Co., Ltd (SHA: 600856) 0.2 -5.3% 0.0 -86.6%

54 庄胜百货 Junefield Department Store Group Ltd (HKG: 0758) 0.1 275.0% (0.1) -371.0%

Subtotal 206.7 -2.0% 7.7 -20.6%

1高鑫零售

(大润发+欧尚) Sun Art Retail Group Ltd (HKEX: 6808 HK) 48.0 7.9% 1.7 8.5%

2 华润万家 China Resource Vanguard Co., Ltd 41.7 9.8% 0.6 9.9%

3 永辉超市 Yonghui Superstores Co., Ltd (SHA: 601933) 17.7 22.8% 0.5 16.4%

4 联华超市 ZhuhaiHoldings Investment GroupLtd (HKG: 0908) 15.0 -3.7% 0.1 -48.8%

5 物美商业 Wumart Store Inc (HKEX: 1025 HK) 10.4 9.2% 0.3 -9.8%

6 中百集团 Zhongbai Holdings Group Co Ltd (SHE: 000759) 8.8 3.2% 0.1 -10.9%

7 华联综超 Beijing Hualian Hypermarket Co., Ltd (SHA: 600361) 6.8 5.6% 0.1 276.5%

8 步步高 Better Life Commercial Chain Share Co., Ltd (SHE: 002251) 6.4 11.4% 0.3 13.3%

9 人人乐 Renrenle Commercial Group Co., Ltd (SHE: 002336) 6.3 -3.8% 0.0 17.0%

10 卜蜂莲花 CP Lotus Corp (HKEX: 0121 HK) 5.5 1.8% (0.0) 17.0%

11 京客隆 Beijing Jingkelong Company Ltd (HKEX: 0814 HK) 5.4 6.8% 0.0 -39.3%

12 新华都 New Huadu Supercenter Co., Ltd (SHE: 002264) 3.7 -3.6% 0.0 164.9%

13 红旗连锁 Chengdu Hongqi Chain Co., Ltd (SHE: 002697) 2.4 9.1% 0.1 3.1%

14 三江购物 Sanjiang Shopping Club Co., Ltd (SHA: 601116) 2.3 -5.3% 0.1 -24.4%

Subtotal 180.5 7.3% 3.8 5.8%

1 苏宁云商 Suning Commerce Group Co., Ltd (SHE: 002024) 51.2 -7.9% (0.7) -202.1%

2 国美电器 GOME Electrical Appliances Holdings Ltd (HKEX: 0493 HK) 29.1 7.4% 0.7 115.2%

3 宏图三胞 Jiangsu Hongtu High Technology Co., Ltd. (SHA: 600122) 6.2 5.1% 0.1 -5.9%

4 汇银家电 Huiyin Household Appliances Holdings Co., Ltd (HKEX: 1280 HK) 1.5 16.9% 0.0 -60.3%

5 三联商社 Sanlian Commercial Co., Ltd (SHA: 600898) 0.4 5.2% 0.0 23.3%

Subtotal 88.4 -2.0% 0.1 -93.9%

Total 475.6 1.3% 11.6 -20.3%

Electronics &

home

appliance

stores

Supermarket

Department

store

BABA

Initiating Coverage

27 October 2014

page 21 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

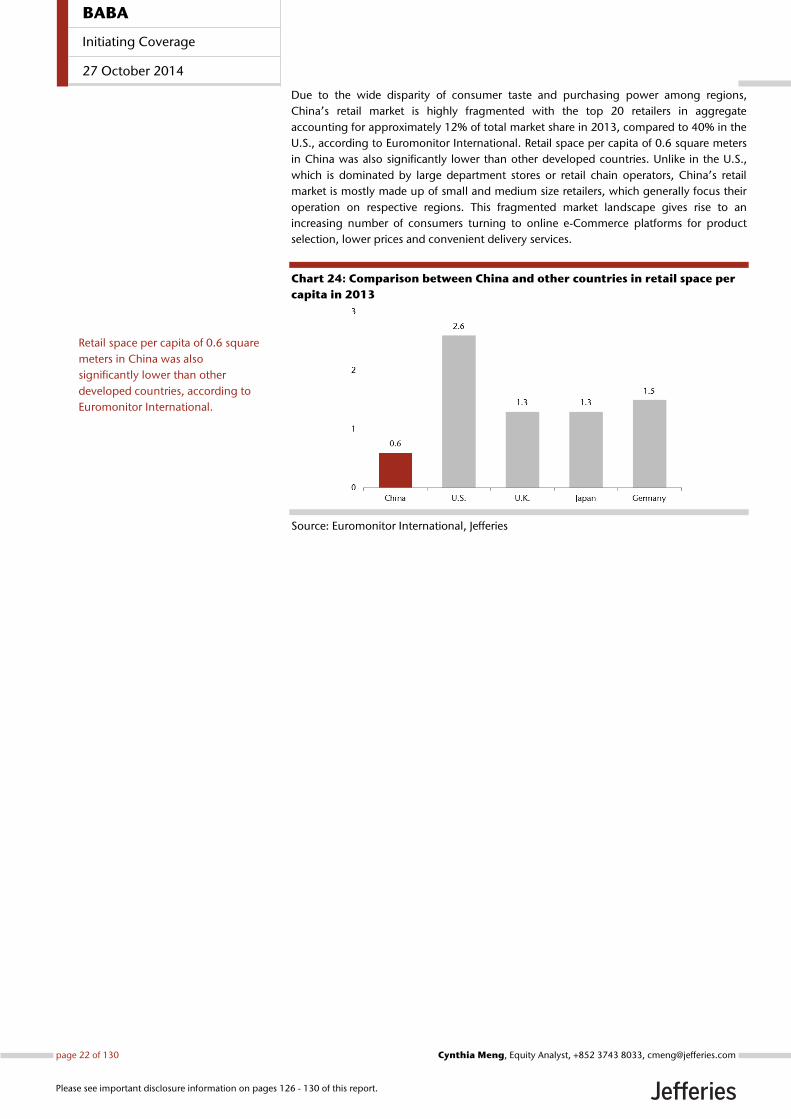

Due to the wide disparity of consumer taste and purchasing power among regions,

China’s retail market is highly fragmented with the top 20 retailers in aggregate

accounting for approximately 12% of total market share in 2013, compared to 40% in the

U.S., according to Euromonitor International. Retail space per capita of 0.6 square meters

in China was also significantly lower than other developed countries. Unlike in the U.S.,

which is dominated by large department stores or retail chain operators, China’s retail

market is mostly made up of small and medium size retailers, which generally focus their

operation on respective regions. This fragmented market landscape gives rise to an

increasing number of consumers turning to online e-Commerce platforms for product

selection, lower prices and convenient delivery services.

Chart 24: Comparison between China and other countries in retail space per

capita in 2013

Source: Euromonitor International, Jefferies

Retail space per capita of 0.6 square

meters in China was also

significantly lower than other

developed countries, according to

Euromonitor International.

BABA

Initiating Coverage

27 October 2014

page 22 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

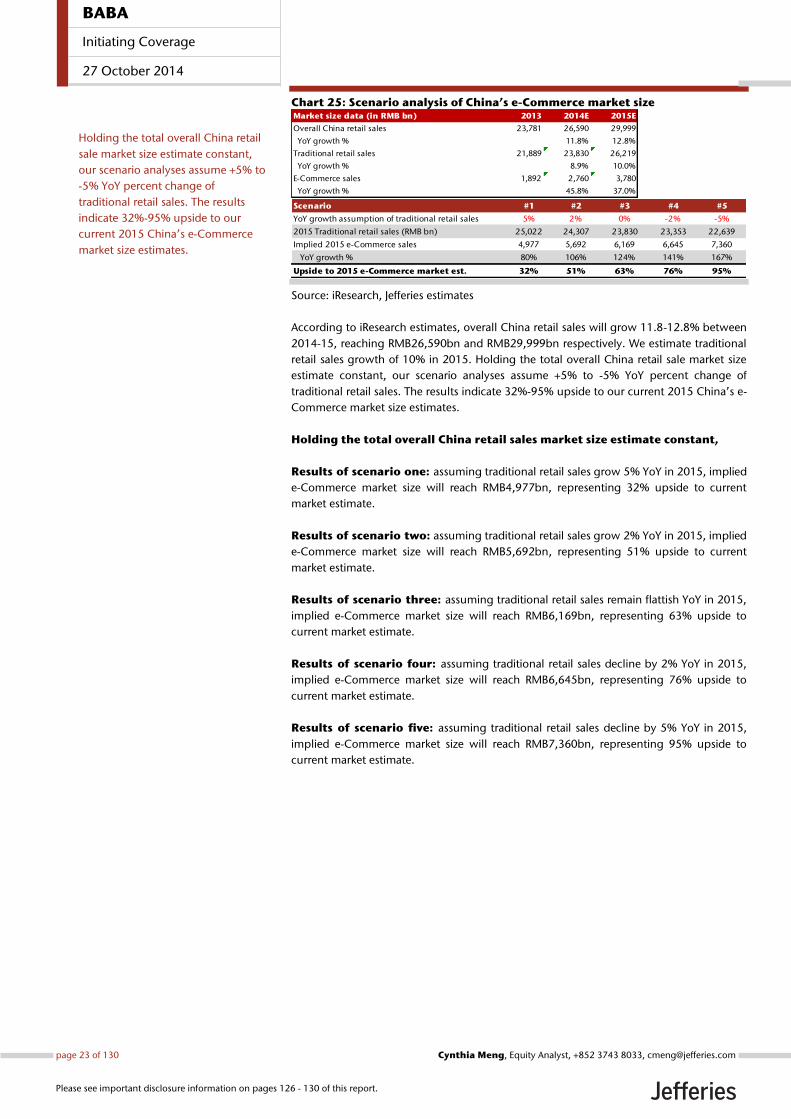

Chart 25: Scenario analysis of China’s e-Commerce market size

Source: iResearch, Jefferies estimates

According to iResearch estimates, overall China retail sales will grow 11.8-12.8% between

2014-15, reaching RMB26,590bn and RMB29,999bn respectively. We estimate traditional

retail sales growth of 10% in 2015. Holding the total overall China retail sale market size

estimate constant, our scenario analyses assume +5% to -5% YoY percent change of

traditional retail sales. The results indicate 32%-95% upside to our current 2015 China’s e-

Commerce market size estimates.

Holding the total overall China retail sales market size estimate constant,

Results of scenario one: assuming traditional retail sales grow 5% YoY in 2015, implied

e-Commerce market size will reach RMB4,977bn, representing 32% upside to current

market estimate.

Results of scenario two: assuming traditional retail sales grow 2% YoY in 2015, implied

e-Commerce market size will reach RMB5,692bn, representing 51% upside to current

market estimate.

Results of scenario three: assuming traditional retail sales remain flattish YoY in 2015,

implied e-Commerce market size will reach RMB6,169bn, representing 63% upside to

current market estimate.

Results of scenario four: assuming traditional retail sales decline by 2% YoY in 2015,

implied e-Commerce market size will reach RMB6,645bn, representing 76% upside to

current market estimate.

Results of scenario five: assuming traditional retail sales decline by 5% YoY in 2015,

implied e-Commerce market size will reach RMB7,360bn, representing 95% upside to

current market estimate.

Market size data (in RMB bn) 2013 2014E 2015E

Overall China retail sales 23,781 26,590 29,999

YoY growth % 11.8% 12.8%

Traditional retail sales 21,889 23,830 26,219

YoY growth % 8.9% 10.0%

E-Commerce sales 1,892 2,760 3,780

YoY growth % 45.8% 37.0%

Scenario #1 #2 #3 #4 #5

YoY growth assumption of traditional retail sales 5% 2% 0% -2% -5%

2015 Traditional retail sales (RMB bn) 25,022 24,307 23,830 23,353 22,639

Implied 2015 e-Commerce sales 4,977 5,692 6,169 6,645 7,360

YoY growth % 80% 106% 124% 141% 167%

Upside to 2015 e-Commerce market est. 32% 51% 63% 76% 95%

Holding the total overall China retail

sale market size estimate constant,

our scenario analyses assume +5% to

-5% YoY percent change of

traditional retail sales. The results

indicate 32%-95% upside to our

current 2015 China’s e-Commerce

market size estimates.

BABA

Initiating Coverage

27 October 2014

page 23 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

This page is intentionally kept blank

BABA

Initiating Coverage

27 October 2014

page 24 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Alibaba - The Powerful E-Commerce Ecosystem Connecting Half of China

BABA

Initiating Coverage

27 October 2014

page 25 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

This page is intentionally kept blank

BABA

Initiating Coverage

27 October 2014

page 26 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

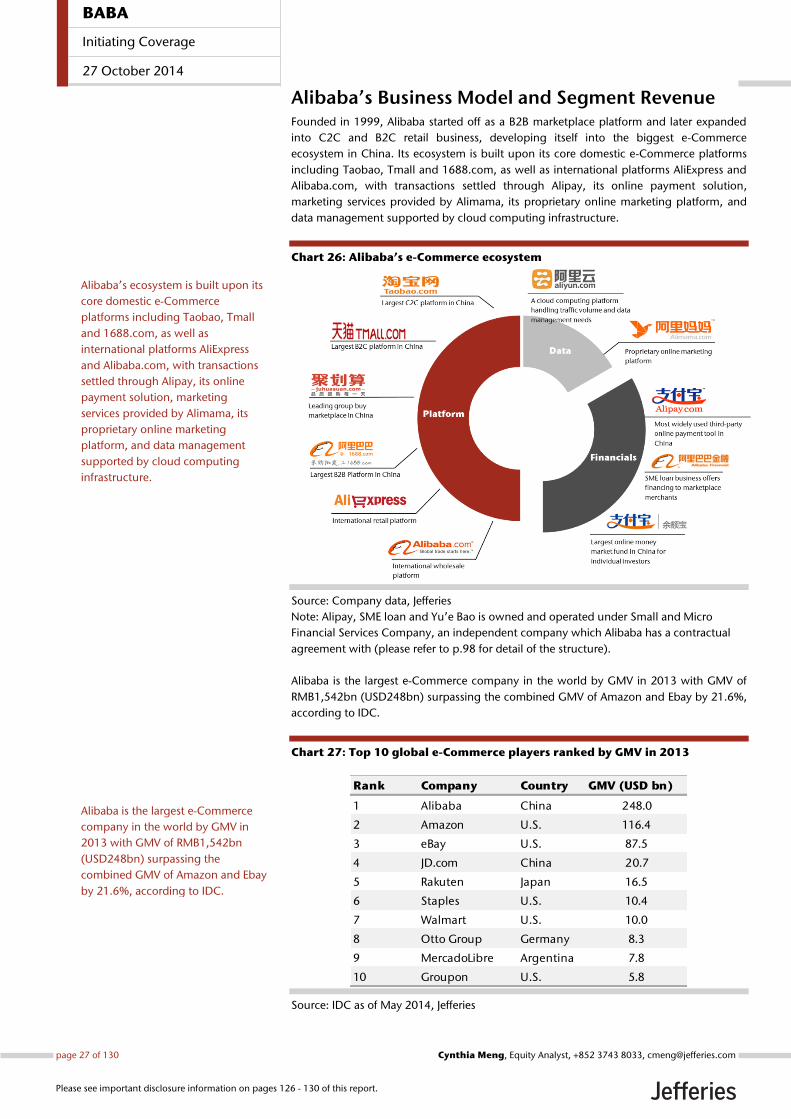

Alibaba’s Business Model and Segment Revenue Founded in 1999, Alibaba started off as a B2B marketplace platform and later expanded

into C2C and B2C retail business, developing itself into the biggest e-Commerce

ecosystem in China. Its ecosystem is built upon its core domestic e-Commerce platforms

including Taobao, Tmall and 1688.com, as well as international platforms AliExpress and

Alibaba.com, with transactions settled through Alipay, its online payment solution,

marketing services provided by Alimama, its proprietary online marketing platform, and

data management supported by cloud computing infrastructure.

Chart 26: Alibaba’s e-Commerce ecosystem

Source: Company data, Jefferies

Note: Alipay, SME loan and Yu’e Bao is owned and operated under Small and Micro

Financial Services Company, an independent company which Alibaba has a contractual

agreement with (please refer to p.98 for detail of the structure).

Alibaba is the largest e-Commerce company in the world by GMV in 2013 with GMV of

RMB1,542bn (USD248bn) surpassing the combined GMV of Amazon and Ebay by 21.6%,

according to IDC.

Chart 27: Top 10 global e-Commerce players ranked by GMV in 2013

Source: IDC as of May 2014, Jefferies

Rank Company Country GMV (USD bn)

1 Alibaba China 248.0

2 Amazon U.S. 116.4

3 eBay U.S. 87.5

4 JD.com China 20.7

5 Rakuten Japan 16.5

6 Staples U.S. 10.4

7 Walmart U.S. 10.0

8 Otto Group Germany 8.3

9 MercadoLibre Argentina 7.8

10 Groupon U.S. 5.8

Alibaba’s ecosystem is built upon its

core domestic e-Commerce

platforms including Taobao, Tmall

and 1688.com, as well as

international platforms AliExpress

and Alibaba.com, with transactions

settled through Alipay, its online

payment solution, marketing

services provided by Alimama, its

proprietary online marketing

platform, and data management

supported by cloud computing

infrastructure.

Alibaba is the largest e-Commerce

company in the world by GMV in

2013 with GMV of RMB1,542bn

(USD248bn) surpassing the

combined GMV of Amazon and Ebay

by 21.6%, according to IDC.

BABA

Initiating Coverage

27 October 2014

page 27 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

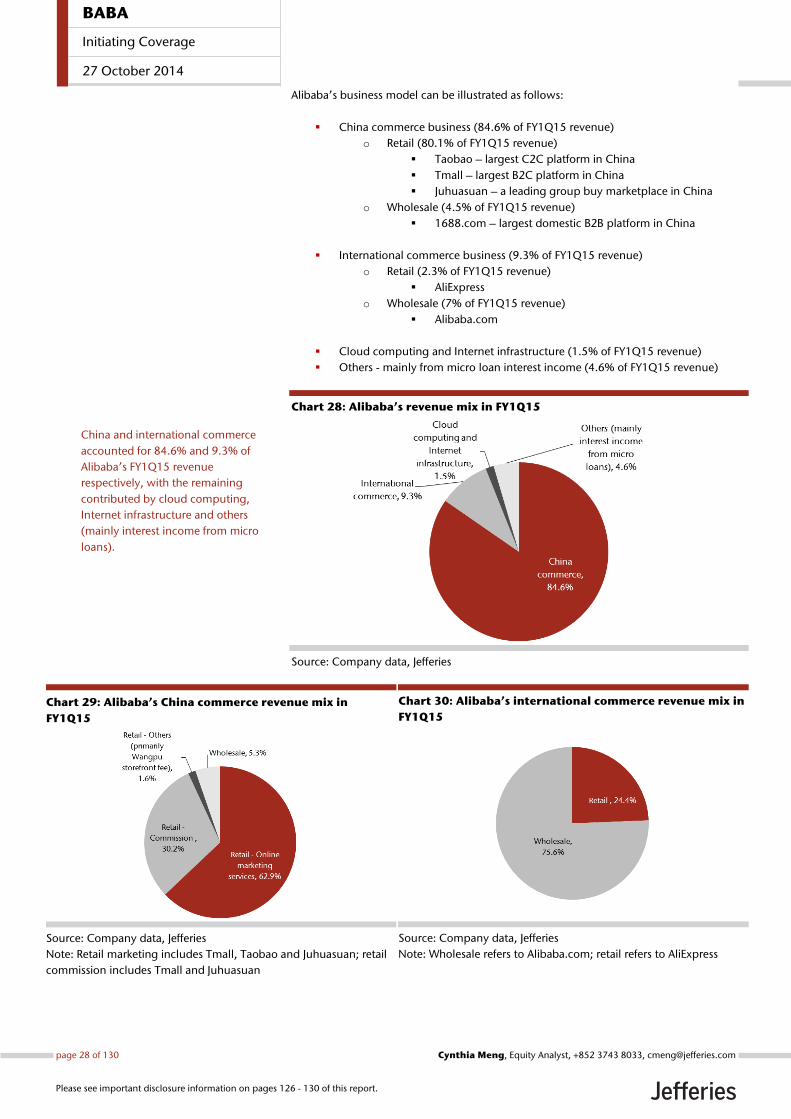

Alibaba’s business model can be illustrated as follows:

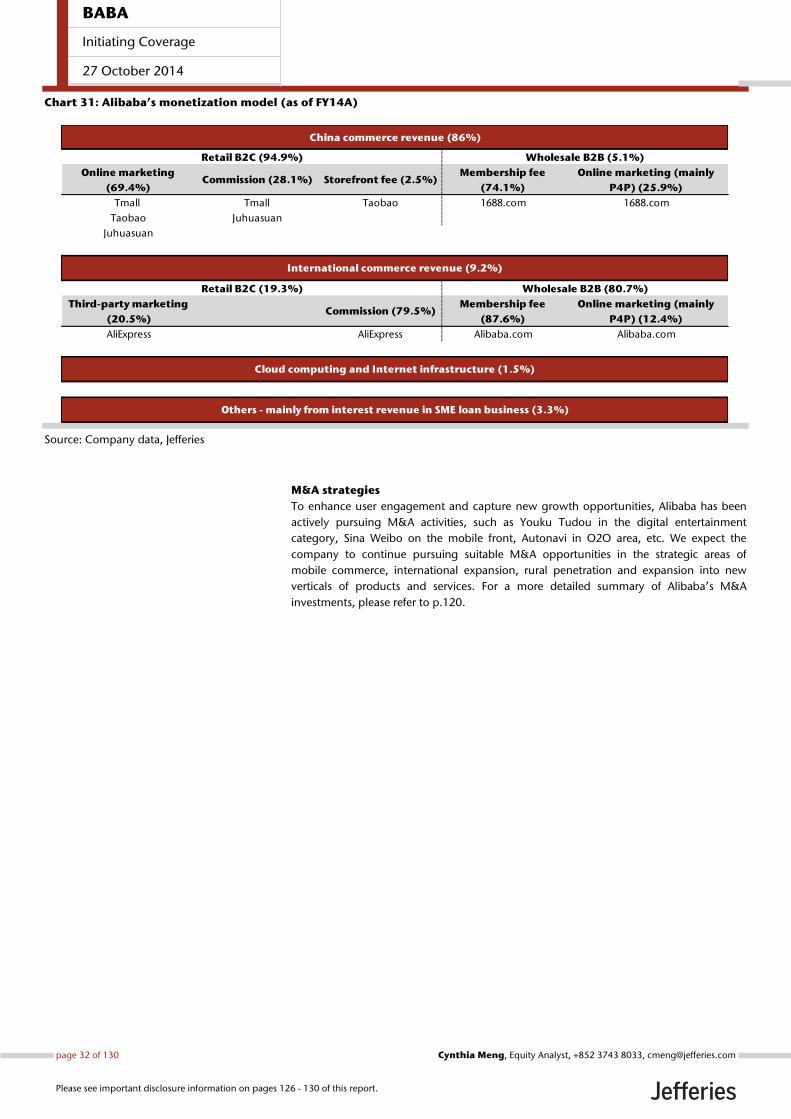

China commerce business (84.6% of FY1Q15 revenue)

o Retail (80.1% of FY1Q15 revenue)

Taobao – largest C2C platform in China

Tmall – largest B2C platform in China

Juhuasuan – a leading group buy marketplace in China

o Wholesale (4.5% of FY1Q15 revenue)

1688.com – largest domestic B2B platform in China

International commerce business (9.3% of FY1Q15 revenue)

o Retail (2.3% of FY1Q15 revenue)

AliExpress

o Wholesale (7% of FY1Q15 revenue)

Alibaba.com

Cloud computing and Internet infrastructure (1.5% of FY1Q15 revenue)

Others - mainly from micro loan interest income (4.6% of FY1Q15 revenue)

Chart 28: Alibaba’s revenue mix in FY1Q15

Source: Company data, Jefferies

Chart 29: Alibaba’s China commerce revenue mix in

FY1Q15

Source: Company data, Jefferies

Note: Retail marketing includes Tmall, Taobao and Juhuasuan; retail

commission includes Tmall and Juhuasuan

Chart 30: Alibaba’s international commerce revenue mix in

FY1Q15

Source: Company data, Jefferies

Note: Wholesale refers to Alibaba.com; retail refers to AliExpress

China and international commerce

accounted for 84.6% and 9.3% of

Alibaba’s FY1Q15 revenue

respectively, with the remaining

contributed by cloud computing,

Internet infrastructure and others

(mainly interest income from micro

loans).

BABA

Initiating Coverage

27 October 2014

page 28 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

China commerce retail (94.7% of FY1Q15 China commerce revenue) –

Taobao, Tmall, Juhuasuan

Alibaba’s China commerce retail business, comprising Taobao Marketplace, Tmall and

Juhuasuan, in aggregate contributed 81.6% of Alibaba’s total revenue in FY14, and 80.1%

in FY1Q15. This includes online marketing revenue, transaction-based commission and

storefront fees. The three marketplaces generated a combined GMV of RMB1,833bn

(USD296bn) from 279mn active buyers and 8.5mn active sellers in the twelve months

ended June 30, 2014.

We estimate China commerce retail revenue to reach RMB64.8bn in FY15, +51.3% YoY,

accounting for 84.4% of total revenue, largely driven by strong growth in commission

revenue. We expect revenue to further grow 42% YoY to reach RMB92bn in FY16.

Online marketing service revenue (66.5% of FY1Q15 China commerce

retail revenue): We estimate online marketing service revenue to reach

RMB39.4bn in FY15, +32.7% YoY, accounting for 51.3% of total revenue, and

RMB50.1bn in FY16, +27.1% YoY, 47.7% of total revenue. Our estimates are

based on continued strong GMV growth partially offset by declining merchants’

advertising budget-to-GMV ratio, due to the increasing GMV contribution from

mobile on which merchants typically allocate a smaller proportion of their

budget to advertising due to limited ad slots from screen size constraints.

Commission revenue (31.9% of FY1Q15 China commerce retail

revenue): We estimate commission revenue of RMB24.5bn in FY15, +104%

YoY, representing 31.9% of total revenue, and RMB41.2bn in FY16, +68% YoY,

39.2% of total revenue. This is based on strong GMV growth of 81.5% YoY and

62.2% YoY on Tmall in the respective years, and assuming average commission

rate to grow slightly to 3.4% and 3.6% respectively.

Other revenue (1.7% of FY1Q15 China commerce retail revenue): We

estimate other revenue, mainly comprised of Wangpu storefront fees, continue

to account for a declining revenue contribution of 1.1% in FY15 and 0.6% in

FY16.

Taobao

Taobao is the largest C2C platform in China with GMV reaching RMB1.2trn in FY14,

+42.4% YoY, representing 69.9% of total China commerce retail GMV, and RMB342bn in

FY1Q15, +33.1% YoY, accounting for 68.3% of total GMV. Major product categories on

Taobao Marketplace include apparel and accessories, electronics and appliances, home

furnishings, maternity and baby products.

Basic storefront and listings on Taobao are available for free to sellers. Instead, revenue is

mainly generated through:

Pay-for-performance (P4P) and display marketing services: merchants

bid for keywords or place display ads to direct traffic to storefronts.

Taobaoke program (categorized as online marketing revenue):

merchants pay Alibaba a GMV-based commission fee for transactions settled

through Alipay from users sourced from third-party marketing affiliates.

Storefront fee: merchants who pay a RMB50 monthly subscription fee for

premium storefront software, Wangpu (“旺铺”), can get access to a suite of

store management and decoration tools, including store logo, customized

storefront, product recommendation column.

BABA

Initiating Coverage

27 October 2014

page 29 of 130 , Equity Analyst, +852 3743 8033, [email protected] Meng

Please see important disclosure information on pages 126 - 130 of this report.

Tmall

Tmall was launched in 2008 to address growing consumer demand for branded products.

GMV generated from Tmall platform reached RMB505bn in FY14, +99.6% YoY,

accounting for 30.1% of total GMV, and RMB159bn in FY1Q15, +80.7% YoY, representing

31.7% of total GMV. Major product categories on Tmall include apparel and accessories,

electronics and appliances, home furnishings, home appliances and maternity and baby

products.

Tmall’s revenue is mainly generated through:

Pay-for-performance (P4P) and display marketing services: merchants

bid for keywords or place display ads to direct traffic to storefronts.

Taobaoke program (categorized as online marketing revenue):

merchants pay Alibaba a GMV-based commission fee for transactions settled

through Alipay from users sourced from third-party marketing affiliates.

Commission revenue: sellers on Tmall are required to pay a commission

typically ranging from 0.3% to 5% of GMV for transactions settled through

Alipay depending on the product category.

Successful execution of cross-border business development will provide upside to Tmall’s

revenue in the long term.

Juhuasuan

Launched in 2010, Juhuasuan is China’s most popular group buying marketplace by

MAUs in 2013, according to iResearch. GMV generated from traffic through Juhuasuan

reached RMB58.2bn (USD9.4bn) in FY14. Operated on a flash sales model, Juhuasuan

allows sellers, majority of which are Tmall merchants, to sell products at a discounted

price for a limited period of time. Major product categories on Juhuasuan include apparel

and accessories, electronics and appliance, home appliance products, beauty and health

product and home furnishings.

Juhuasuan’s revenue is mainly generated through:

Placement revenue: merchants pay placement fees to purchase promotional

slots on Juhuasuan marketplace for a specified period;

Commission revenue: sellers on Juhuasuan are required to pay a commission

typically ranging from 0.3% to 5% of GMV for transactions settled through

Alipay depending on the product category.

China commerce wholesale (5.3% of FY1Q15 China commerce revenue)

1688.com

1688.com is a leading online wholesale marketplace in China connecting Chinese

wholesalers, suppliers or distributors with buyers, majority of which are merchants on

Taobao and Tmall marketplaces.