Alexander JanLondon School of Economics – MSc Urban & Regional Planning 28 January 2013 Road...

80

Alexander Jan London School of Economics – MSc Urban & Regional Planning 28 January 2013 Road pricing in England: has its time finally come?

-

Upload

moriah-bury -

Category

Documents

-

view

214 -

download

0

Transcript of Alexander JanLondon School of Economics – MSc Urban & Regional Planning 28 January 2013 Road...

Alexander Jan London School of Economics – MSc Urban & Regional Planning

28 January 2013

Road pricing in England: has its time finally come?

2

Agenda

Historical context

The problem as was

The problem looking forward

Experience from London

Government proposals

Concluding thoughts

3

Historical context

“It is impossible to spend any time on the study of the future of traffic in towns without at once being appalled by the magnitude of the emergency that is coming upon us. We are nourishing at immense cost a monster of great potential destructiveness, and yet we love him dearly. To refuse to accept the challenge it presents would be an act of defeatism”

HMSO, Penguin Books, Traffic in Towns The Specially shortened edition of the Buchanan Report, Penguin Books, London, 1964

4

Historical context “We think the public can justifiably demand

to be fully informed about the possibilities of adapting towns to motor traffic before there is any question of applying restrictive measures.”

HMSO, Penguin Books, Traffic in Towns The Specially shortened edition of the Buchanan Report, Penguin Books, London, 1964

5

That was then….

Traffic in towns

DfT, Transport Statistics Great Britain, London, 2012

6

A seven fold increase in vehicles since the 1950s…

DfT, Transport Statistics Great Britain, London, 2012

Traffic in towns

7

Brixton Town Centre – post redevelopment, seen from the motorwaywww.cbrd.co.uk

Brixton in the snow. “We’re still loving snowy SW9!”© urban7, 2nd/3rd Feb, 2009

Brixton….

8

Finchley Road, Belsize Park….

www.cbrd.co.uk

9

The problem…

Congestion

Pollution

Economic impacts

Accidents

Quality of life

(Competiveness, growth, employment?)

10

The problem

“Despite the government’s efforts, the deterioration in the network is noticeable. Congestion already costs the UK economy up to £8bn each year and without measures to tackle this, the figure could riseto £22bn a year by 2025.”

Source: CBI, Bold thinking A model to fund our future roads, London, 2012

11

Well, may be not worse, just more complicated…

12

UK context: long term traffic forecasts

80

100

120

140

160

180

200

220

240

260

Inde

x (1

980

= 10

0) Historical traffic

Forecast traffic

Source: Department for Transport

13

UK context: long term congestion forecasts

0

100

200

300

400

500

600

700

800

900

Commuters Employer's Business

Education and Personal Business

Home based Recreation

and Holiday

Non home based

Recreation and Holiday

LGVs HGVs

Tot

al L

ost T

ime

(mill

ion

hour

s)

2003 2015 2025 2035

Source: Department for Transport

14

Some things have got better…

DfT, Transport Statistics Great Britain, London, 2012

15

…in environmental terms…

In: Johnson et al, Fuel for Thought , RAC Foundation, Institute for Fiscal Studies, London, 2012

16

But with unintended consequences….?

In: Johnson et al, Fuel for Thought , RAC Foundation, Institute for Fiscal Studies, London, 2012

17

The government has done well out of the motorist...

DfT, Transport Statistics Great Britain, London, 2012

18

But the motorist has learned….

Johnson et al, Fuel for Thought , RAC Foundation, Institute for Fiscal Studies, London, 2012

19

…to fight back….

Johnson et al, Fuel for Thought , RAC Foundation, Institute for Fiscal Studies, London, 2012

“Overall, one cannot help but think that the current levels of motoring taxationhave little to do with either sound revenue-raising principles or external costarguments. Rather, they are an accident of history by which the governmentraises as much as it can get away with.”

20

Looking forward, problem is changing…

Fuel duty and Vehicle Excise Duty (VED) contribute c. £38 billion a year, some 7% of all the Exchequer’s income.

44 % more traffic by 2035…. but revenue from motoring taxation is set to drop by £13 billion a year by 2029 to £25 billion

Key driver has been fuel efficiency of vehicles (Govt climate change policy)

Congestion set to get worse

Less than one third of this money is spent on national and local roads

Major population growth and ageing assets means more expenditure to “standstill”

21

Experience from London Introduced by Ken Livingstone, February 2003, if driving

within central London between 7 a.m. and 6.30 p.m. on a weekday

July 2005 rose to £8, increased to current level £10

Within a year, day-time average speed increased to 16.7 km/h from 14.3 km/h (c17% improvement)

Car traffic decreased 34%, trucks 7% and vans 5%

Charge was not really on congestion: “greener” vehicle discounts allowed motorists to drive for free

Public opposition turned to public support!

Tenth anniversary this year….

22

Success, but a one-off?

Congestion charge introduced February 2003

DfT, Transport Statistics Great Britain, London, 2012

23

But overall scheme has produced mixed results? Costly… c. 50% of revenues spend on running the system (2006/07

~ £252m vs costs of £130m); 40%+ of revenues came from enforcement charges

Downing Street on-line petition (2007)

Western extension removed by Boris Johnson (December 2010)

Big “no” vote in Greater Manchester (78.8%) (April 2010)

Whilst traffic volumes are lower, congestion has crept back up… (2007 levels close to 2002)

Cities have not rushed to replicate the scheme

London mayor(s) wary about introducing London wide user charging…

24

Further change any time soon?

“And yet no government has really solved the problem of how to finance the infrastructure we need within the public spending constraints we have.”

Finally, on top of the failures of vision and of financing, there's been a simple failure of nerve.”

No government has acted with the necessary determination to blast through the vested interests and bureaucratic hurdles in order to provide what the long-term national interest demands.”

To put it crudely, we've become good in Britain at sweating old assets.”

Prime minister, David Cameron, March 2012

25

“Road tolling is one option - but we are only considering this for new, not existing, capacity.”

Why is it that other infrastructure - for example water - is funded by private sector…but roads in Britain call on the public finances for funding?”

That's why I have asked the Department for Transport and the Treasury to carry out a feasibility study of new ownership and financing models for the national roads system and to report progress to me in the Autumn.”

Let me be clear: this is not about mass tolling - and as I've said, we're not tolling existing roads...it's about getting more out of the money that motorists already pay.”

Prime minister, David Cameron, March 2012

26

UK: Investment backlog

96 unfunded projects identified, including for local authorities.

Cost estimates available for 77 of them, totalling £10.7bn billion.

Weighted average BCR of 3.6 where known, but some as high as 10.

Some clusters of projects around regions or corridors.

Source: Arup

27

UK context: international comparison

Country reviewedWorld Economic Forum

highways ranking

France 1

Portugal 5

Spain 11

Canada 14

USA 20

Australia 34

UK 26Source: World Economic Forum

28

International experience: investment trends

Source: OECD

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

€m

illio

ns

p.a

. (20

09 v

alu

es)

Historical highways investment in countries reviewed

Australia

Canada

France

Portugal

Spain

UK

29

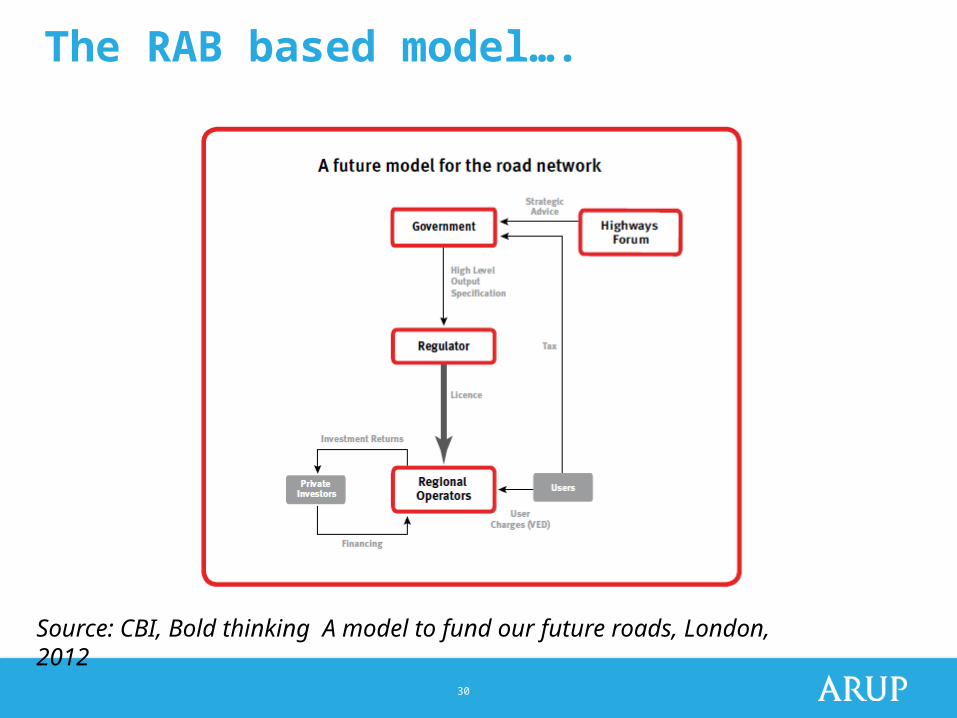

Government way forward?

Giving the sector a revenue stream - a proportion of Vehicle Excise Duty?

A change to the HA’s corporate status or break up into regions….

So called “RAB” model to attract investment

Independent regulation of the sector, with customer service obligations (water)

30

The RAB based model….

Source: CBI, Bold thinking A model to fund our future roads, London, 2012

31

Conclusions

Problem of congestion is persistent and likely to get worse (return of economic growth, population increase)

Other policy factors now in play (declining source of general taxation for government)

Some indication that Government is considering reform (including a user charge) for motorways but nervousness over public acceptability (Downing Street petition)

Strong investor appetite – could raise significant revenues for HMT…

Brings into focus the question of what are our roads for?

32

“End of the free green run... now hybrid cars will have to pay congestion charge too”

London Evening Standard, 28 January 2013

Discussion and questions

34

Recommendations: projects

Potential for user charging on major schemes (e.g. Dartford and A14).

Innovation within PPPs (e.g. a more constructive public-private interface, and allocation of traffic risk).

Local innovation to allow authorities and other bodies more flexibility in funding priority schemes.

35

Recommendations: policy

Acknowledge the funding challenge.

Longer term strategy to address growing demand.

Stable, long term funding to support investment.

Regionalisation / localism.

36

UK context: policy and budgets

IUK providing focus at heart of government on long term infrastructure challenges.

Investment in economic infrastructure prioritised at CSR 2010.

But cuts to investment budgets for HA and local transport major projects.

Is investment in our highways sector being overlooked?

37

UK context: highways investment

HA pioneered use of PPPs for highways, since copied and modified by the rest of the world.

M6 toll and river crossings are isolated examples of tolling.

Strategic road network highly dependent on central government for funding.

Contrasts with other parts of the infrastructure sector.

38

UK context: sector investment backlog

96 unfunded projects identified, including for local authorities.

Cost estimates available for 77 of them, totalling £10.7bn billion.

Weighted average BCR of 3.6 where known, but some as high as 10.

Some clusters of projects around regions or corridors.

Source: Arup

39

UK context: sector investment backlog

Source: Arup; DfT data

0 2 4 6 8 10 120

200

400

600

800

1,000

1,200

Costs and BCRs for unfunded projects

BCRs

£ m

illio

ns,

201

0 va

lues

£32,000

40

UK context: investment backlog...contd

Source: Department for Transport data, Arup analysis

1,749

3,947

917

1,129

1,175

Breakdown of project types, by value (£ millions, 2010 values) Widenings

New connections

Junction improvements

Managed Motorways

Other

41

UK context: some questions

How important is investment in our strategic road network, compared with other priorities?

Why is our approach to funding highways so different from other infrastructure sectors?

What happened to the UK Government’s enthusiasm for highways PPPs?

Why does the M6 toll remain a one-off?

International experience

43

International experience: key differences

Investment trends and investment planning

Roles of central and regional / state governments

Attitudes towards private finance

User charging

44

International experience: investment planning

Longer term investment planning for highways in comparator countries:

- Australian Nation Building Economic Stimulus Plan

- Building Canada Fund

- Investment planning cycles built into privatised French networks

- Spain’s 15 year Infrastructure Plan

45

International experience: roles of central and regional / state government

Central governments typically provide funding support (e.g. Australia, Canada, USA).

State / regional governments lead most procurements (most notably Spain).

Picture in France more complex, but significant devolution through privatisation of sub-regional networks.

46

International experience: attitudes towards private finance

Strong support for PPP in comparators.

Commercial models similar to those used in the UK, but note significance of different accounting rules.

Relationships between public and private sector appear more constructive (e.g. Spain and France).

Government bodies actively promote PPPs (e.g. European PPP Expertise Centre, PPP Canada, FHWA Office of Innovative Programme Delivery).

47

International experience: user charging

Longer and more extensive history of tolling strategic networks in European comparators.

Use of tolling growing in the US and Canada.

Some high profile financial failures (e.g. In Australia).

Revenue stream allows sector to fund its own development.

48

International experience: investor appetite

Separate markets for brownfield and greenfield projects.

Lenders reluctant to take full volume risk, particularly for greenfield projects. Some notable failures...

Governments acting to reduce private sector risk exposure.

New projects less likely to be delivered as direct tolls.

2010

Technical and commercial adviser to CVC Capital

Partners in the acquisition of 23% of the shareholdings of Abertis, operator of 10,000 km of highways in Spain, France and South America

2010

Technical adviser to DIF Infrastructure in the

acquisition of shareholdings in two tolled bridge projects

owned by NTR in Ireland.

€1.72bn

Technical and commercial adviser to Eiser Infrastructure in

the acquisition of 49% stakes from Sacyr in two shadow toll

roads and two transport interchanges in, Spain

€47M 2010Price confidential

Lessons learned and recommendations

50

Lessons learned: recap and summary of differences

Congestion is forecast to increase significantly, and there is a large investment backlog.

Businesses rank our roads network as poorer than most developed countries.

Governance of the strategic network is relatively centralised.

The sector does not generate and retain significant revenues.

The private sector has a limited role, and government is relatively pessimistic about the potential of PPPs.

51

Recommendations: projects

Potential for user charging on major schemes (e.g. Dartford and A14).

Innovation within PPPs (e.g. a more constructive public-private interface, and allocation of traffic risk).

Local innovation to allow authorities and other bodies more flexibility in funding priority schemes.

52

Recommendations: strategic reform

Giving the sector a revenue stream (e.g. user charges or hypothecation of VED).

A change to the HA’s corporate status.

Independent regulation of the sector, with customer service obligations.

A move away from central planning.

http://www.cbi.org.uk/media-centre/press-releases/2012/10/gear-change-can-accelerate-the-uk-towards-a-21st-century-road-network/

Spare slides

54

Discussion and questions: some suggested themes...

Should the funding gap provide an impetus to new thinking?

What role do we see for the private sector in highways investment?

Is the UK regulated utility model the right one for roads?

Who should draw up a strategy for roads?

55

Further information

http://www.racfoundation.org/assets/rac_foundation/content/downloadables/providing_and_funding_strategic_roads-arup-071111.pdf

www.arup.com

56

Vehicle Excise Duty revenues have almost doubled between 1987 and 2011 whereas the

increase in the revenue from fuel duty has more than tripled.

As well as the £26.9 billion collected in fuel duty in 2011, there was an additional £5.4 billion

collected in VAT on fuel duty. Over the same period the RPI has more than

doubled.

57

Carbon

DfT, Transport Statistics Great Britain, London, 2012

58

King’s Cross as it could have been….

www.cbrd.co.uk

59

RACF/IFS 61/120

60

RACF/IFS 56/71

61

62

63

But overall scheme has produced mixed results? Typically 50% of revenues spend on running the system (2006/07 - £252m vs costs of £130m)

TfL's annual report for 2006–7 shows that revenues from the congestion charge were £252.4m over the financial year, representing 8.5% of TfL's annual revenues.

More than half of this was spent on the cost of running the toll system, at £130.1 million. Once other charges were deducted, the congestion charge brought in an

annual operating net income of £89.1m for TfL.[145] This income compares with TfL's total revenue from bus and tube fares of £2,269.4m, or 76.6% of revenue

before costs, or grants from central government of £2,390.3 million.

The initial operating revenues from the congestion charge did not reach the levels that were originally expected. Within six months of the start of the scheme, the

reduction in traffic had been such that TfL were predicting a £65 million revenue shortfall.[146]

By law, all surpluses raised must be reinvested into London's transport infrastructure; at the start of the scheme it was anticipated that this would be around

£200 million.[147][148] According to a report issued in February 2007, the initial costs of setting up the scheme were £161.7 million,[148] with an annual operating cost

of about £115m anticipated.[149] Total revenues over the first three and a half years had been £677.4 million, with TfL reporting a surplus over operating costs of

£189.7 million.[148] The Bow Group, compiled from TfL data estimated that by 2007 the project had only returned a modest £10 million profit.[52]

Although Parliament has limited the amount that authorities can borrow, for some time it had been speculated that the regular income obtained from the

congestion charge and other revenues could be used to securitise a bond issue that finances other transport projects across London.[150] TfL issued their first bond

for £200 million in 2005, to be repaid at 5% interest over 30 years. TfL plans to borrow £3.1 billion more to fund a 5-year transport programme across London,

including works on London Underground and road safety schemes.[151]

Revenues (£m) provisional 2004/5[14] 2005/6[90] 2006/7[15] Standard daily vehicle charges (currently £10) 98 121 125 Enforcement income 72 65 55 Fleet vehicle daily

charges (currently £7) 17 19 27 Resident vehicles (currently £4 per week) 2 2 6 Other income 2 Total revenues 190 210 213 Total operation and administration costs

(92) (88) (90) Net revenues 97 122 123 Expenditure (% of operating revenue) 2004/5[14] 2006/7[15] Bus network improvements (incl. vehicles, garages & shelters)

80% 82% Road and bridge maintenance & upgrades 11% Road safety (incl. research & campaigns) 11% 4% Walking & cycling programmes & publicity 6%

2.5% Distribution and freight (incl. review of a London lorry ban) 1% "Safer routes to schools" initiative

64

Revenues (£m) provisional 2004/5[14] 2005/6[90] 2006/7[15]

Standard daily vehicle charges (currently £10) 98 121 125

Enforcement income 72 65 55

Fleet vehicle daily charges (currently £7) 17 19 27

Resident vehicles (currently £4 per week) 2 2 6

Other income 2

Total revenues 190 210 213

Total operation and administration costs (92) (88) (90)

Net revenues 97 122 123

London, including works on London Underground and road safety schemes.151

65

66

67

Page 38 (53) in January 2011 (though charging hours now end at 6 p.m.). Exemptions from

the scheme exist for a number of vehicles including taxis, motorcycles, bicycles,

buses, disabled badge holders, emergency vehicles and some vehicles that

run on alternative fuel. Additionally, residents living in the zone receive a 90%

discount. The charge raised £158.1 million in 2010, net of operating costs (TfL,�

2011a). These revenues are hypothecated towards the improvement of public

transport in London, as is required by the Greater London Authority Act 1999.

The original zone comprised an area bounded by the Inner Ring Road,

covering approximately eight square miles. In February 2007, this was

extended to include additional parts of Westminster, Kensington and Chelsea.

This ‘Western extension’ was abolished in December 2010, returning the zone

to its original area.

The effect of the scheme on traffic levels and congestion is quite difficult to

determine. The most recent estimates come from Transport for London (TfL,

2008) suggesting that traffic in 2007 was around 18% lower in the central

congestion zone relative to pre-charging levels (and 36% lower for car traffic).

However, congestion levels in 2007 appeared to be no lower than they were

in 2002 (though they were cut during 2003 to 2006) – though of course to fully

assess the impact of the charge requires us to estimate the counterfactual level

of congestion in its absence. TfL (2008) suggests that congestion was lower

in 2007 than it would have been without the charge, after taking into account

factors such as an increased level of road maintenance work and changes

to traffic signal timings. Unfortunately, the 2008 report was the last available

– they are no longer published annually by TfL. Instead, information on

congestion is included as part of a wider annual report on transport in London.

The most recent (TfL, 2011b) suggests that removing the Western extension

increased traffic entering that area by about 8%, and congestion by about 3%.

68

RACF IFS (61/76)

70

Government proposalsAnd yet no government has really solved the problem of how to finance the infrastructure we need within the public spending constraints we have.Finally, on top of the failures of vision and of financing, there's been a simple failure of nerve.No government has acted with the necessary determination to blast through the vested interests and bureaucratic hurdles in order to provide what the long-term national interest demands.To put it crudely, we've become good in Britain at sweating old assets.But if you do that for too long, there's a price to pay.It's not enough just to keep the existing infrastructure going.We need to build - as other countries are building - the completely new infrastructure we need for the future.And on top of all this we haven't focused - as other countries focus - on ensuring that investment in infrastructure helps business at home.That's not about picking winners.It's about helping British companies to be winners.We haven't done anything like enough to help grow British expertise and jobs in building not only the infrastructure we need here, but in booming markets overseas.Now, after all these years of failure, compromise and lack of ambition, the reckoning is upon us.

71

Government proposalsAnd yet no government has really solved the problem of how to finance the infrastructure we need within the public spending constraints we have.Finally, on top of the failures of vision and of financing, there's been a simple failure of nerve.No government has acted with the necessary determination to blast through the vested interests and bureaucratic hurdles in order to provide what the long-term national interest demands.To put it crudely, we've become good in Britain at sweating old assets.But if you do that for too long, there's a price to pay.It's not enough just to keep the existing infrastructure going.We need to build - as other countries are building - the completely new infrastructure we need for the future.And on top of all this we haven't focused - as other countries focus - on ensuring that investment in infrastructure helps business at home.That's not about picking winners.It's about helping British companies to be winners.We haven't done anything like enough to help grow British expertise and jobs in building not only the infrastructure we need here, but in booming markets overseas.Now, after all these years of failure, compromise and lack of ambition, the reckoning is upon us.

72

Has it changed? - a perfect storm for policymakers

The report discusses in detail the second line of argument as to how motoring

taxes might be structured: rather than simply raising revenue, taxes should

reflect the various economic and social impacts that the use of vehicles has

on other road users and the community at large. These impacts include traffic

congestion, accidents, visual intrusion, noise and air pollution, and greenhouse

gas emissions.2

‘Revenue raising’ and ‘paying the external costs’ are quite distinct principles.

The amount of tax gathered under a revenue-raising regime might bear no

particular relation to the yield that reflects external economic, environmental

and social impacts.

73

Has it changed? - a perfect storm for policymakers

On top of the 14p for carbon you can reasonably add to fuel duty elements

corresponding to external costs such as air pollution. But then you have

a problem: by far the most costly damage inflicted by road users is traffic

congestion. This is not directly related to the amount of fuel used, and hence it

is hard to justify factoring it into fuel duty. Traffic congestion varies enormously

by time and place. Thus no single, universal rate of fuel duty can be regarded

as appropriate for all. The IFS estimates that at the current rate of duty, about

half of all vehicle miles are taxed too highly – many of them on uncongested

rural roads; one quarter are taxed about right; and the remainder are charged

too little – in some congested urban locations, far too little.

74

Has it changed? - a perfect storm for policymakers

The IFS is driven to the conclusion that if the ‘paying the external costs’

justification is to be sustained then a significant portion of current fuel duty

must be replaced by some form of ‘pay-as-you-go’ charge based on distance

driven in congested conditions. Such a charge moderates demand, and

therefore reduces congestion. There is a net overall gain, and the economic

value of the road is increased. The amount of revenue is determined by the

characteristics of the road and the level of demand for use of it. But this begs

the question: who gets the benefit of the use of the revenue?

75

Future trends….

Major shift in funding towards China, Asia, South America

Constraints on affordability, especially from state funding sources next 10+ years? Some

increasing role for the private sector. Some continued resistance to real tolls (Europe, US)

Elsewhere in the world, “long march” of highways likely to continue – less reluctance to toll

(key to demand management…) so globally more “user pays” projects

Sustained interest from longer term investors (pensions etc) - attractive asset class (matching

of liabilities…)

Impact of technology on payment mechanisms and traffic demand - more sophisticated, user

friendly, intelligent. Better use of existing assets…

Environmental issues: a continuing challenge as car ownership increases. Rate of growth

likely to outstrip technological improvements in energy efficiency, emissions etc?

Extent of change will vary dramatically by global region.

Today, in London, we travel at around 6 miles per hour – the standard set by the horse and cart

over a hundred years ago... plus ça change….

76

It should be noted that the congestion charge does not explicitly target

congestion. Motorists who pay it have unlimited use of roads within the

zone

during that day. Therefore, the charge does not take into account the

distance

driven, the location, or the time (within the specified hours) of the

journey.

Motorists who cause a greater congestion externality through driving

greater

distances at busier times are charged the same amount as other drivers

causing smaller external costs.

77

But good railways are only part of the answer on transport.

We need good roads, too.

Again, the problem's clear: we don't have enough capacity in places of key demand.

There's nothing green about a traffic jam - and gridlock holds the economy back.

So here's what we should do.

Yes, move passengers and heavy goods onto rail.

But also widen pinch points, add lanes to motorways by using the hard shoulder to increase

capacity and dual overcrowded A-roads.

The massive programme announced during last year's Growth Review made a good start.

But how do we do more, when , frankly, there isn't enough money?

We need to look at innovative approaches to the funding of our national roads - to increase

investment to reduce congestion.

78

Road tolling is one option - but we are only considering this for new, not existing, capacity.

For example, we're looking at how improvements to the A14 could be part funded through tolling.

But we now need to be more ambitious.

Why is it that other infrastructure - for example water - is funded by private sector capital through privately owned,

independently regulated, utilities but roads in Britain call on the public finances for funding?

We need to look urgently at the options for getting large-scale private investment into the national roads network - from

sovereign wealth funds, pension funds, and other investors.

That's why I have asked the Department for Transport and the Treasury to carry out a feasibility study of new ownership

and financing models for the national roads system and to report progress to me in the Autumn.

Let me be clear: this is not about mass tolling - and as I've said, we're not tolling existing roads...

...it's about getting more out of the money that motorists already pay.

79

Recommendations: policy

Acknowledge the funding challenge.

Longer term strategy to address growing demand.

Stable, long term funding to support investment.

Regionalisation / localism.

UK context

![Prima Pagina · 2017. 3. 16. · 11 12 14 16 19 21 24 29 MSC MSC Ji[han MSC MSC Jilhan MSC Jilhan AS Venus MSC Jilhan Tongan MSC MSC ]ilhan AS Venus MSC MSC Jilhan AS Venus AS Venus](https://static.fdocuments.net/doc/165x107/60ea7428e144a50de815ab4a/prima-pagina-2017-3-16-11-12-14-16-19-21-24-29-msc-msc-jihan-msc-msc-jilhan.jpg)