ALC FORUM 2016 Tony Hatch - austlogistics.com.au€¦ · ALC FORUM 2016 Tony Hatch Railroad Capital...

8

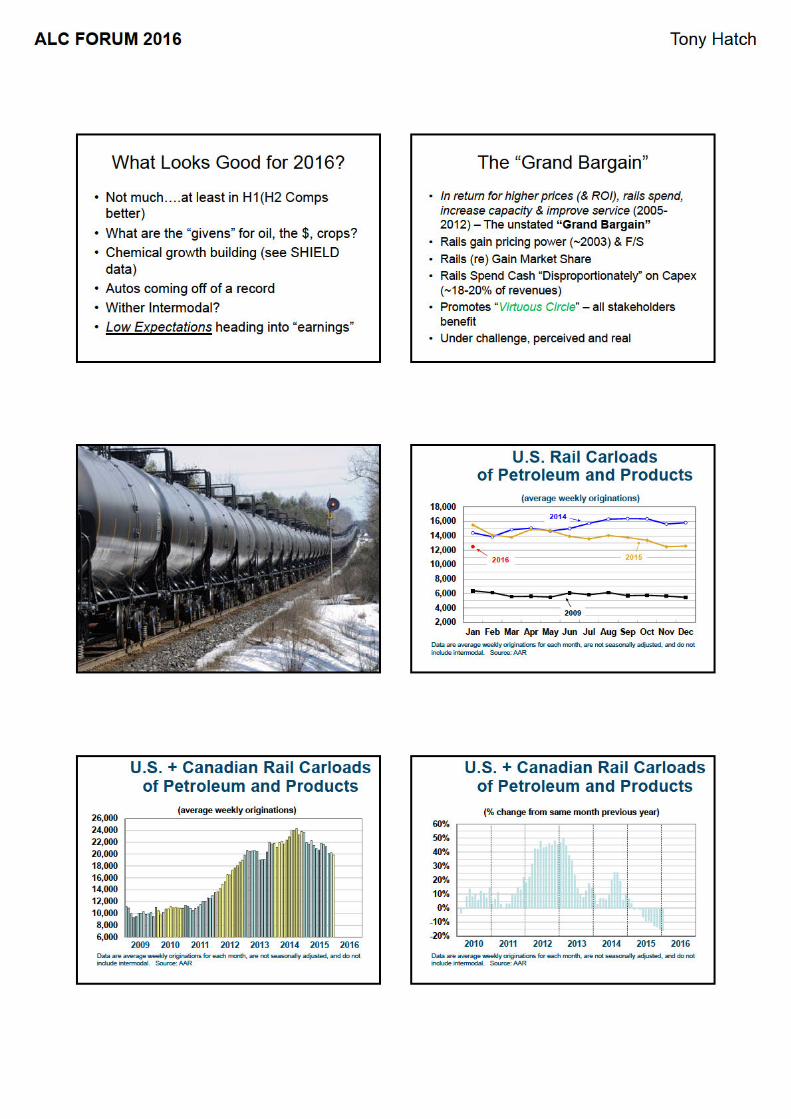

ALC FORUM 2016 Tony Hatch Is the NA Railroads’ “Renaissance” simply a thing of the past? ALC 2016 Forum Sydney abh consulting/NYC March 2, 2016 North American Freight Railroading Today • Two Historic Canadian “transcon” carriers • “Big Four” US - 2 in the East (CSX & NS), 2 in the West (UP & BNSF) • KCS running North South from the midwest to Mexico • ~550 short lines • Canadian Model* - 2015 Operating Ratio of 59.6% is over 800bps better than Major US Rail average • Canadian Benefits: FX, Management, Health Care Costs, Length of Haul, etc. • 2 Mexican Carriers – KCSM and Ferromex • Mexico – labor costs, peso vs. “rule of law issues” 2 North American Freight Railroads 3 4 RR Deregulation - & Vertical Integration – Works! The “Grand Bargain” • In return for higher prices (& ROI), rails spend, increase capacity & improve service (2005- 2012) – The unstated “Grand Bargain” • Rails gain pricing power (~2003) & F/S • Rails (re) Gain Market Share • Rails Spend Cash “Disproportionately” on Capex (~18-20% of revenues) • Promotes “Virtuous Circle” – all stakeholders benefit • Under challenge, perceived and real Overview of North American Rail Environment & Key Issues • Rail Renaissance the key theme (1980-) 2001-2013 • Challenges Emerge – Energy Decline (Coal/Oil) • End of the “Commodity Super Cycle” • Service & Safety Issues; Rereg threats re-emerge • Rails are still re-gaining market share from the highway • (therefore) Intermodal is Even More Important • (and .) Service & Productivity are Even More Important • Managements, New & Challenged: Visibility Capex & Cash • Is M&A the Solution? (What’s the problem?) 6

Transcript of ALC FORUM 2016 Tony Hatch - austlogistics.com.au€¦ · ALC FORUM 2016 Tony Hatch Railroad Capital...

ALC FORUM 2016 Tony Hatch

Is the NA Railroads’ “Renaissance” simply a thing of the past?

ALC 2016 Forum

Sydney

abh consulting/NYC

March 2, 2016

North American Freight Railroading Today

• Two Historic Canadian “transcon” carriers

• “Big Four” US - 2 in the East (CSX & NS), 2 in the West (UP & BNSF)

• KCS running North South from the midwest to Mexico

• ~550 short lines

• Canadian Model* - 2015 Operating Ratio of 59.6% is over 800bps better than Major US Rail average

• Canadian Benefits: FX, Management, Health Care Costs, Length of Haul, etc.

• 2 Mexican Carriers – KCSM and Ferromex

• Mexico – labor costs, peso vs. “rule of law issues”

2

North American Freight Railroads

3 4

RR Deregulation - & Vertical Integration – Works!

The “Grand Bargain”

• In return for higher prices (& ROI), rails spend, increase capacity & improve service (2005-2012) – The unstated “Grand Bargain”

• Rails gain pricing power (~2003) & F/S

• Rails (re) Gain Market Share

• Rails Spend Cash “Disproportionately” on Capex (~18-20% of revenues)

• Promotes “Virtuous Circle” – all stakeholders benefit

• Under challenge, perceived and real

Overview of North American Rail Environment & Key Issues

• Rail Renaissance the key theme (1980-) 2001-2013

• Challenges Emerge – Energy Decline (Coal/Oil)

• End of the “Commodity Super Cycle”

• Service & Safety Issues; Rereg threats re-emerge

• Rails are still re-gaining market share from the highway

• (therefore) Intermodal is Even More Important

• (and .) Service & Productivity are Even More Important

• Managements, New & Challenged: Visibility Capex & Cash

• Is M&A the Solution? (What’s the problem?)

6

ALC FORUM 2016 Tony Hatch

Railroad Capital ExpendituresClass I Railroads

$0

$5

$10

$15

$20

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16

Billions

Source: RRFacts & Analysis of Class I RRs, AAR; abh estimates

19

Q3: Do you expect RR service in 2016 to?

Shipper Poll (continued): Based on the "value proposition" for rail vs other modes, for 2016 do you expect to:

Winter 2015-16 – Inflection Point?

• Low expectations for rail (transport) quarterly earnings – CSX starts us off with a “win”

• Coal stabilizing? Sigh….

• Productivity/service turnaround?

• Management confidence/guidance?

• Waiting further “Big Decisions” on Capex, “stranded assets”

• The “Renaissance” thesis faces first real challenges this century

RR Q4/15- How Full is the Glass?

RR VOL% REV% EPS% W/L/T OR% BPS PRICE ‘16CapExYOY

CSX -6 -13 -2 W 71.60% -20 4.1 -4NSC -6 -12 -27 L 72.50% 350 NA! -13UNP -9 -16 -19 L 63.20% 180 3.5 -13

BNSF TBD -25CNI -8 -1 15 W 57.20% -350 3 +7%!CP -6 -4 1 L 59.80% 3 -26KSU -2 -7 -3 W 63.40% -330 4 -15

GWRR TBD

AVG* -6 -9NMF 3/3/0* 65.10% -25NA (~3+) -13

Renaissance Discussion Points!

• Can Rails Survive (or even thrive) the N/N?

• Or, can rails replace coal (ROI if not OR) with (domestic) intermodal (etc)?

• What is the future of industrial/merchandise railroading? (A: “Plastics”….)

• Rails will exit transitional period (faith)

• CBR to continue longer term – as volatile as Ag?

• Service Recovery – Politics, Productivity & Price

• What is the new standard for Capex?

• Is M&A the answer?

ALC FORUM 2016 Tony Hatch

Railroad Philosophy

• Critical to the “RR Renaissance” has been Capex

• Private vs public capital (failing US infrastructure)

• Capex sparked by growth and ROI prospects –examples: IM, CBR

• “Open Access” antithetical to this….right?

• Is a RR its Network (Class One belief) OR is it its Operators (Hunter)??

• Cult of the OR vs ROIC; short-termism

Top 10 Thoughts on Possible CP-NS merger

1. Risk/Reward Ratio Unfavorable

2. Diplomacy (“Politesse”) Required

3. Shipper Support Required

4. NS Approval Important (and….); Valentine’s Day Filing?

5. STB/CTA (etc) Pro-cess Will Be Long & Drawn-Oot

Top Ten NS/CP Continued

6. NS’ “Problems” Mostly Not of its Own Making (COAL!) – yet value is in “fixing” NS!

7. NS is Advanced in Preparing for “Post-Coal” World

8.New RR World to be Very-High-Service Focus

9. CP-NS Could Stand alone -but would it? NO….

10. YET: Never Underestimate EHH

Q6: Are you in favor of RR consolidation (merger)?

(30)

Future Growth Potential (Revised)

Specific

targeted sectors

Secular stories (in order) .

1. Intermodal – international and now domestic

2. Chemicals/re‐industrialization? Near‐sourcing/Mexico

3. Cyclical recovery – housing, autos

4. Grain & Food – the world s breadbasket, (un)predictable?

5. Shale/oil/sand – problem and solution?

6. Other rail opportunities exist but in smaller scale: for ex: The manifest/carload “problem”

‐ Unitization

‐ Industrial Products/MSW

‐ Perishables