Ajit & Nagesh

114

A COMPREHENSIVE PROJECT REPORT ON “COMPARISON STUDY WITH VODAFONE & RELIANCE COMMUNICATION SPECIFICATION ON TELECOM INDUSTRY” Submitted to GROW MORE FACULTY OF MANAGEMENT HIMATNAGAR IN PARTIAL FULFILLMENT OF THE REQUIREMENT OF THE AWARD FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION In GUJARAT TECHNOLOGICAL UNIVERSITY Under The faculty Guidance Of Assi. Prof. Javed Jethara Submitted by Dabhi Ajit S. Enrollment No. : (107130592048) Patel Nagesh A. Enrollment No. : (107130592011) [Batch : 2010-12] MBA SEMESTER III/IV Grow More Faculty of Management 1

-

Upload

parth-patel -

Category

Documents

-

view

82 -

download

4

description

gfgggg

Transcript of Ajit & Nagesh

A

COMPREHENSIVE PROJECT REPORT

ON

“COMPARISON STUDY WITH VODAFONE & RELIANCE

COMMUNICATION SPECIFICATION ON TELECOM INDUSTRY”

Submitted to

GROW MORE FACULTY OF MANAGEMENT

HIMATNAGAR

IN PARTIAL FULFILLMENT OF THE

REQUIREMENT OF THE AWARD FOR THE DEGREE OF

MASTER OF BUSINESS ADMINISTRATION

In

GUJARAT TECHNOLOGICAL UNIVERSITY

Under The faculty Guidance Of

Assi. Prof. Javed Jethara

Submitted by

Dabhi Ajit S. Enrollment No. : (107130592048)

Patel Nagesh A. Enrollment No. : (107130592011)

[Batch : 2010-12]

MBA SEMESTER III/IV

Grow More Faculty of Management

Affiliated to Gujarat Technological University,

Ahmadabad.

1

PREFACE

According to the rules of G.T.U and part of our syllabus, we are the M.B.A

student have to take Comprehensive Project Report of any one industry in the

year 2010-2012 and we have to write about the technical knowledge and how

the Indian economy and also business running in present time.

In M.B.A. we get lots knowledge by our theoretical syllabus and management reference books. In this modern age practical knowledge is more important than theoretical knowledge. It does not mean that theoretical knowledge is not important but without practical knowledge students are incomplete. It proved that “PRACTICE MAKES THE MAN PERFACT.”

2

ACKNOWLEDGEMENT

It is almost inevitable to incur indebtedness to all who generously helped by

sharing their invaluable time and rich experience with me, without which this

project would have never been accomplished. No task can be achieved alone,

particularly while attempting to finish a project of such magnitude. It took many

very special people to facilitate it and support it. Hence, I would like to

acknowledge all of their valuable support and convey my humble gratitude to

them.

Success is a sweet fruit, which every one strives to taste. In the process one

takes help of encouraging and helping. “People one seed at a time and forest

grows and stone at a time and a place is built, a little effort at a time and project

is developed and ambition released.” This was solely the approach; I took

toward the development of the project.

We thankful to other administration staff for their co-operation and kindly take

on our project report.

We would like to express heartily thankful to our respected Prof. Javed Jethera.

who has given us valuable guidance and provide other required information for

the preparation of this report.

3

Students’ Declaration

We are Dabhi Ajit S. & Patel Nagesh A. hereby declare that the report for Comprehensive Project entitled “Comparison Study with Reliance Communication & Vodafone Specification on Telecom Industry ”is a result of our own work and our indebtedness to other work publications, references, if any, have been duly acknowledged.

Place : …… (Signature)

Date : (Name of Students)

Dabhi Ajit S. EN ROLL:(107130592048)

Patel Nagesh A. EN ROLL:(107130592011)

4

INDEX.

Sr. N Particular Page Number

I Preface

Ii Awknowledge

Chap-1. About the telecom industry

1.1 Growth & evolution telecom industry

2. World markets telecoms

3. Major players in industry

4. Services profile

5. Product profile

6. Demand determination of telecom industry

7. Key success factore of telecom industry

8. Pest analysis

9. Research methodology

9.1 Research objectives:-

9.3 Data collection

10 Michel porter’s five force model company

11 Company information

12 Swot analysis

14 Financial analysis

15 Research methodology ratio.

15.1 Liquidity ratio

15.1.1 Current ratio

15.1.2 Net working capital

15.1.3. Quick ratio

15.1.4. Cash ratio

5

15.2 Leverage

15.2.1 Debt equity ratio

15.2.2 Interest on coverage ratio

15.3. Profitability ratio (%)

15.3.1 Return on equity ratio

15.3.2 Net profit ratio

15.3.3 Return On Capital ivestmentRatio

15.3.4 Return On Capital Employed Ratio

15.4 Activity ratio

15.4.1 Net assets turn over ratio

15.4.2 Fixed assets turn over ratio

15.4.3 Total assets turn over ratio

15.5 Profitability ratio (%)

16 Conclusion

17 Annexure

18 Profit & Loss Account

19 Balance sheet

20 Bibliography

6

CHAPTER – 1

ABOUT THE INDUSTRY

7

TELECOM INDUSTRY IN INDIA

1 .1GROWTH & EVOLUTION TELECOM INDUSTRY:-

1.TELECOM NDUSTRY PROFILE:

The Indian Telecommunications network is the third largest in the world and the

second largest among the emerging economies of Asia. Today, it is the fastest

growing market in the world. The telecommunication sector continued to register

significant success during the year and has emerged as one of the key sectors

responsible for India’s resurgent India’s economic growth.

GROWTH:-

The Indian telecom industry has witnessed a significant upswing and is presently on

a high speed growth path, enjoying a growth rate of ~45 % p.a., among the highest

in the World. India currently has ~550 million telecom subscribers, translating to a

tele-density of ~46%. According to Business Monitor International, India is currently

adding 8-10 million mobile subscribers every month. Approximately 20% of the world

population has access to the Internet. The telecom industry is vast and offers a wide

range of career opportunities on both the hardware and software fronts. These

prospects include functional jobs in mobile telephony, internet protocol media

systems, wireless communications, GSM, GPRS and CDMA technology, VoIP, data

networks and optical networks amongst others.

The growth in number of broadband connections in India has accelerated since

2006. As of October 2011, total broadband Internet connections in India had reached

12.98 million constituting 1.0% of the population. India has one of the lowest

penetrations of broadband connectivity in the world. The industry is expected to

8

reach a size of 344,921 crore (US$65.53 billion) by 2011at a growth rate of over 26

percent, and generate employment opportunities for about 10 million people during

the same period. According to analysts, the sector would create direct employment

for 2.8 million people and for 7 million indirectly. The total revenue of the Indian

telecom sector grew by 7% to 283,207 crore (US$53.81 billion) for 2010-11 financial

year, while revenues from telecom equipment segment stood at 117,039 crore

(US$22.24 billion).The number of mobile phone subscribers in the country would

exceed 50 million by 2005 and cross 300 million by 2010, according to Cellular

Operators Association of India (COAI).

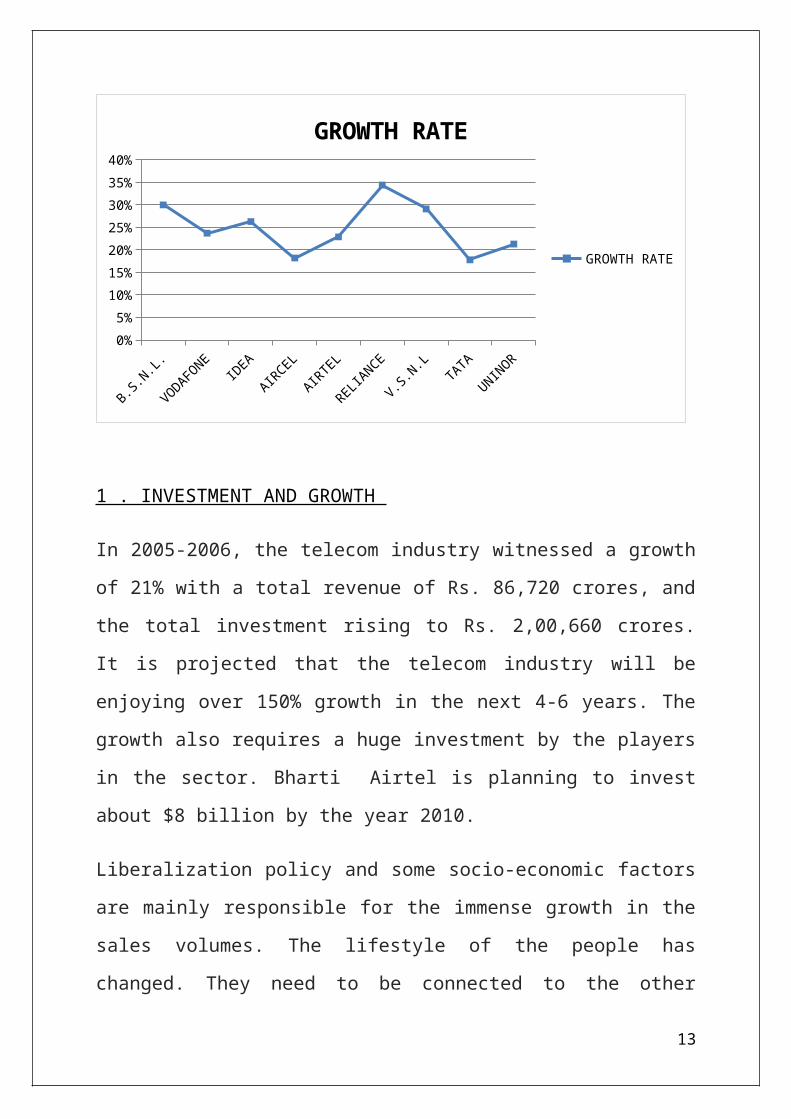

MAJOR PLAYERS IN TELECOM INDUSTRY OF GROWTH RATE OF

201 1 .

COMPANY GROWTH

RATE

B.S.N.L. 30%

VODAFONE 23.7%

IDEA 26.3%

AIRCEL 18.2%

AIRTEL 22.9%

RELIANCE 34.4%

V.S.N.L 29.1%

TATA 17.8%

UNINOR 21.3%

9

B.S.N.L.

VODAFONE

IDEAAIRCEL

AIRTEL

RELIANCE

V.S.N.L

TATA

UNINOR0%

5%

10%

15%

20%

25%

30%

35%

40%

GROWTH RATE

GROWTH RATE

1 . INVESTMENT AND GROWTH

In 2005-2006, the telecom industry witnessed a growth of 21% with a total

revenue of Rs. 86,720 crores, and the total investment rising to Rs. 2,00,660

crores. It is projected that the telecom industry will be enjoying over 150%

growth in the next 4-6 years. The growth also requires a huge investment by the

players in the sector. Bharti Airtel is planning to invest about $8 billion by the

year 2010.

Liberalization policy and some socio-economic factors are mainly responsible

for the immense growth in the sales volumes. The lifestyle of the people has

changed. They need to be connected to the other people all the time. With the

lowering down of the tariffs the affordability of the mobile phones has

increased. The finance sector has also come up with loans for handsets on 0%

interest. Mobile services providers are also expanding their coverage area by

installing more and more antennas and other equipments.

10

EVOLUTION:-

The number of smart devices already reached 940 million units by the end of

2010, suggesting a penetration rate of nearly 18%. Therefore, smart devices

have entered a period of rapid growth.

The telecom industry has entered a critical period for its transformation in

2011.Take mobile communications for example. Openness, competition, and

sharp decrease

of the operating expense (OPEX) have fueled the rapid growth of mobile

communications. There were already 5.6 billion mobile users worldwide in

March 2011 with a mobile communications penetration rate of more than 80%.

Mobile broadband services have become a highlight and drive of the entire

telecom industry, and the faster penetration of smart devices has been pushing

the rapid upgrading of the industry. Mature smart devices such as I Phone and I

Pad are contributing to the economies of scale of the industry, as their prices

keep falling to let them enter the low-end and mid-range markets..

Manufacture of Telecom Equipment:-

1 .

With a growth rate of 45 percent, the Indian telecom industry is booming.

Apart from providing mobile and broadband subscriptions, the telecom industry

is also involved in the manufacture of telecom equipment. Rising demand for a

wide range of telecom equipment, particularly in the area of mobile

telecommunication, has provided excellent opportunities to domestic and

foreign investors in the manufacturing sector. The last two years saw many

11

renowned telecom companies setting up their manufacturing base in India.

Ericsson has set up GSM Radio Base Station Manufacturing facility in Jaipur.

Elicited has set up handset manufacturing facilities in Bangalore. Nokia set up

its manufacturing plant in Chennai. LG Electronics set up plant of

manufacturing GSM mobile phones near Pune.

The Government has already set up Telecom Equipment and Services Export

Promotion Forum and Telecom Testing and Security Certification Centre

(TETC). A large number of companies like Alcatel, Cisco have also shown

interest in setting up their R&D centers in India. With above initiatives India is

expected to be a manufacturing hub for the telecom equipment.

2. WORLD MARKETS TELECOMS

World Markets Telecoms integrates our Same-Day Analysis with our Country

Intelligence and Company Analysis products. Our client website, My Insight,

enables you to link instantly from your daily desktop news to any related in-

depth reports on the countries or companies featured in the same-day analysis.

Subscribers to this service receive:

Same-Day Analysis of daily news, events, and trends in global telecom

markets, with the option to filter by product, company, or country.

Country Intelligence: uniform data, forecasts and analysis across 140

telecoms markets for valuable market insight.

Company Analysis: quarterly-updated statistics for tracking over 500

fixed, broadband and mobile operators in over 100 countries.

Benefits:

12

World Markets Telecoms enables you to:-

Evaluate market opportunities and risks in the fixed-line, mobile, and broadband

sectors. Assess investment opportunities.

Monitor your competitors and customers Stay up to date with recent industry

developments Conduct first-stage and ongoing market assessment of country

telecoms markets.

Assess market size allocate sales and marketing resources Identify convergence

and product substitution.

3. MAJOR PLAYERS IN TELECOM INDUSTRY

There are three types of players in telecom services:

• State owned companies (BSNL and MTNL)• Private Indian owned companies (Reliance Infocomm, Tata Teleservices,)• Foreign invested companies (Hutchison-Essar, Bharti Tele-Ventures, Escotel, IdeaCellular, BPL Mobile, Spice Communications)

13

Bharat Sanchar Nigam Limited (BSNL)

Name:- Bharat Sanchar Nigam Limited (BSNL).

Year of Establishment:- 2000

Company Profile:- Bharat Sanchar Nigam Ltd. is World's 7thlargest Tele

communications Company providing comprehensive range of telecom services

in India: Wire line, CDMA mobile ,GSM Mobile, Internet, Broadband, Carrier

service, MPLS-VPN, VSAT, VoIP services, INS services etc. Within a span of

five years it has become one of the largest public sector unit in India.

Global Presence/ Marketing:- It has a network of over 45 million lines

covering 5000.

14

Network:- towns with over 35 million telephone connections.

Future Prospect:- BSNL plans to expand its customer base from present

47millions lines to 125 million lines and infrastructure investment plan to the

tune of Rs. 733 crores(US$ 16.67 million) in the next three years.

Videsh Sanchar Nigam Limited (VSNL)

Name:- Videsh Sanchar Nigam Limited (VSNL)

Year of Establishment:- 1986.

Company Profile:- The Videsh Sanchar Nigam Limited (VSNL) – a wholly

Government owned corporation. The company operates a network of earth

stations, switches, submarine cable systems, and value added service nodes to

provide a range of basic and value added services and has dedicated work force

of about 2000 employees. VSNL' in gateway centers are located at Mumbai,

New Delhi, Kolkata and Chennai.

Global Presence/ Marketing Network:- The company has 52 subsidiaries in

21 countries as well as operations across four continents.

Acquisitions / Strategic Alliances:- VSNL acquired Nasdaq-listed Teleglobe

International Holdings Ltd for $239 million in2005 Videsh Sanchar Nigam Ltd

acquired Tyco Global Network, submarine cable system, for USD 130 million

in 2005.

15

Future Prospect:- The company plans to expand its wholesale voices services

across the EU, to effectively enable enterprise customers and retail voice

carriers to connect to India. VSNL is adding its capacity to meet the over whe-

lming demand for connectivity to India in the wholesale voice services domain.

The company is also offering flexible agreements and charging methods to meet

the growing demands of the whole sale voice

Reliance Communication

Name:- Reliance Communications.

Year of Establishment:- 1999.

Company Profile:- Reliance Telecom's cellular services are available in 340

towns within its eight-circle footprint. Reliance Infocomm also offered for the

first time in India, mobile data services though its R World mobile portal. This

portal leverages the data capability of the CDMA 1X network. Reliance

Infocomm offers a complete range of telecom services covering mobile and

fixed lintels phony including broadband, national and international long

distance services, data services and a wide range of value added services and

applications aimed at enhancing productivity of enterprises and individuals.

Global Presence/ Marketing Network:-Reliance Communications has IP-

enabled connectivity infrastructure comprising over150,000 kilometers of fiber-

optic cable systems in India, the US, Europe, Middle East, and the Asia Pacific

region.

16

Acquisitions / Strategic Alliances:- International wholesale

telecommunications service provider, FLAG Telecom amalgamates with

Reliance Gateway, a wholly owned subsidiary of Reliance Infocomm in 2004.

Vodafone

Name:- Vodafone

Year of Establishment:- Acquired majority stake in Hutch Essar in India ,by

buying out complete stake of Hutch in 2007, Essar is still minority stakeholder

in company.

Company Profile:- Vodafone Essar in India is a subsidiary of Vodafone Group

Plc and commenced operations in 1994 when its predecessor Hutchison

Telecom acquired the cellular license for Mumbai. Vodafone Essar now has

operations in 16 circles covering 86% of India's mobile customer base, with

over 45.78 million customers. Vodafone Essar, under the Hutch brand, has been

named the 'Most Respected Telecom Company', the 'Best Mobile Service in the

country' and the 'Most Creative and Most Effective Advertiser of the Year'.

Global Presence/ Marketing:- It has operations in 25 countries across

5continents and 40.

Network:- partner networks with over 200 million customers worldwide.

17

Acquisitions / Strategic Alliances Future Prospect:- Vodafone Essar is

expecting to touch over 35million customers across 400,000 shops and thousand

of hutch’s own employees along with employees of its business associates.

Idea

Name:- Idea.

Year of Establishment :-1995.

Company Profile:- Idea Cellular is part of the Aditya Birla Group, which is

India's first truly multinational corporation. Aditya Birla Nuvo Ltd. holds

35.7per cent, Birla TMT Holdings Ltd. 44.9 percent, Grasim 7.5 per cent, and

Hindalco 10.1per cent in Idea.

Global Presence/ Marketing Network:- Has a customer base of over 17

million, IDEA Cellular has operations in Delhi, Maharashtra, Goa, Gujarat,

Andhra Pradesh, Madhya Pradesh, Chattisgarh, Uttaranchal, Haryana, UP West,

Himachal Pradesh and Kerala.

Acquisitions / Strategic Alliances:- Merged with Tata Cellular Limited in

2001,thereby acquiring original license for the Andhra Pradesh Circle Acquired

RPG Cellular Limited and consequently the license for the Madhya Pradesh

(including Chattisgarh) Circle in 2001 In2004 acquired Escotel, incumbent

cellular service provider in Haryana, UP(W) & Kerala and new licensee in HP

Acquired Escorts Telecommunications Limited (subsequent lyre named as Idea

Telecommunications Limited)in 2006 Merger of seven subsidiaries with Idea

Cellular Limited in 2007.

18

Future Prospect:- Idea also plans to enter rural and neglected circles as a

strategy to gain subscribers. Other advancements in the telecom industry will

help it cut costs - use of e-mail to send bills to customers; sharing cell sites;

smaller base transmission stations that will mean lesser infrastructure

requirements and expenses and independent tower operators. Along with its

plan to go for a national long distance license, it will also look at international

long distance in the near future.

Bharti airtel

Year of Establishment :-1985.

Global Presence/ Marketing:- Bharti airtel has IP-enabled connectivity

infrastructure comprising over 148900 kilometers of fiber-optic cable systems

in India, the US, Europe, Middle East, and the Asia Pacific region.

Network:- We provide internet connection - Airtel Broadband, Reliance

Netconnect, MTS MBlaze,7.2 Mbps 3g Huawei 3g Unlocked Data cards, Tata

Photon plus.

Market share:- 20.09%26

Tata Teleservices

Name:- Tata Teleservices

Year of Establishment:- 1996.

19

Company Profile:- Tata Teleservices is a part of the $12 billion Tata Group,

which has 93 companies, over200,000 employees and more than 2.3 million

shareholders. Tata Teleservices’ bouquet of telephony services includes Mobile

services, Wireless Desktop Phones, Public Booth Telephony and Wire line

services. Other services include value added services like voice portal, roaming,

post-paid Internet services, 3-wayconferencing, group calling, Wi-Fi Internet,

USB Modem, data cards, calling card service and enterprise services.

Global Presence/ Marketing:- Tata Teleservices has presence in across

19circles that includes Andhra Pradesh, Chennai, Gujarat, Karnataka, Delhi,

Maharashtra, Mumbai, Tamil Nadu, Orissa, Bihar, Rajasthan, Punjab, Haryana,

Himachal Pradesh, Uttar Pradesh (E), Uttar Pradesh (W), Kerala, Kolkata,

Madhya Pradesh and West Bengal.

Acquisitions / Strategic Alliances:- Tata Teleservices has acquired

HughesTele.com (India) Limited [now renamed Tata Teleservices

(Maharashtra) Limited] in 2002.

Future Prospect:- The company is also expanding its footprint, and has paid

Rs. 4.17 billion ($90 million) to Do T for 11 new licenses under the

IUC(interconnect usage charges) regime.

Uninor

Year of Establishment :-. Founded 2009 Headquarters Gurgaon, India.

Services are Mobile telephony Wireless internet. Owner(s) Telenor Group

(67.25%) Unitech Group (32.75%) Employees 2,000.Uninor is an Indian mobile

20

network operator based in Gurgaon, India. The company holds Unified Access

Service(UAS) licenses to offer mobile telephony services in each of India’s 22

telecom circles, and has received spectrum to roll out services in 21 of these

(excluding Delhi). The company is a joint venture between Telenor Group, a

telecommunications company headquartered in Oslo, Norway, and Unitech

Group, an Indian real estate company. Telenor owns a controlling majority

stake in the company (67.25%), which has been branded Uninor in the Indian

market.

Uninor offers mobile voice and data services based on the GSM technology,

currently on a 4.4 MHz spectrum. Uninor services are commercially available in

13 circles across India. With a ‘value for money’ proposition in the market,

Uninor targets youth and other communities within the Indian mass market.

As of Q2, 2011, Uninor had 26 million customers, 2,200 employees and a sales

force of 7,000 people. Uninor products and services are available from a more

than 330,000 retail outlets serviced by 1,600 distributors all over the country.

4.SERVICES PROFILE:-

21

INTERNET SERVICES:-

Internet services were launched in India on August 15, 1995. In November

1998 the government top ended up the sector to private operators. A liberal

licensing regime was put in place to increase Internet penetration across the

country. The growth of IP telephony or grey market is also a serious concern.

Government loses revenue, while unlicensed operation by certain operators

violates the law and depletes licensed operators market share. New services like

IP-TV and IP-Telephony are becoming popular with the demand likely to

increase in coming years. The scope of services under existing ISP license

conditions.

3G TECHNOLOGY SERVICES :-

3G: There was always a question mark over profitability after more than 67,000

crores were paid by telecom service firms in the 3G spectrum auction. So, who

was to be blamed, the telecom firms who overpaid or the auction process that

was touted as the most efficient price discovery mechanism? May be the

government did not put many blocks on offer thus creating artificial scarcity and

so the prices went up. But it’s not easy to pin down a scientific price to

spectrum. As Marten Peters, MD of Vodafone Essar recounts his experience

when in the beginning of the last decade, 3G spectrum and other spectrum

auctions in Europe fetched very high prices. But a big spectrum auction in

Germany in 2010 saw them getting four times as much spectrum at half the

price. The other problem is the readiness e.g. only 3% of the 141mn Vodafone

subscribers have a 3G enabled handset (Please don’t mistake them as 3G users

yet). So the existing scenario entails that the companies are still some distance

away from breaking even.

22

2G TECHNOLOGY SERVICES:-

2G:2G scam comes to your mind straightaway. Undoubtedly it’s a blot on the

Indian face. And its findings will certainly leave many embarrassed. But let’s

not waste our time over this. Let’s concentrate on the other major issues. The

one that comes to the mind is “too much competition or should I This has

resulted in players with large subscriber base having too little spectrum while

many with little or no subscriber base are sitting on precious resources. The

industry despite taking care of network effect doesn’t seem to be achieving the

economies of scale (remember it’s a capital intensive industry) thus forcing lots

of customers in very little spectrum. As a result India is struggling to improve

the quality of coverage despite achieving decent breadth of coverage at 800mn

subscribers. This could lead to future tariff hikes by major players as low tariffs

become unsustainable say too many players”. While basis used to allocate

spectrum helped keep the cost down hence low tariffs but it allowed too many

players to enter the fray.

CDMA SERVICES:-

CDMA technology was introduced in India as a limited mobility solution. The

introduction of CDMA services has created competition, lowered tariffs and

offered many citizens access to communication services for the first time.

WIRELINE SERVICES:-

With increasing penetration of the wireless services, the wire line services in the

country is becoming stagnant. On the other hand, Broadband demand has

picked up and promises to stabilize fixed linegrowth.

23

GSM Sector

In terms of the Global System for Mobile Communication (GSM) subscriber

base thisnow places India third after China and Russia. China had 401.7 million

GSM Subscribers.

5. PRODUCT PROFILE :-

2. Broad brand

3. Hand set

4. Cell phone

5. Ear- phone

6. I-pod

7. Wi Max

8. Wireless

6.DEMAND DETERMINATION Of TELECOM INDUSTRY

Demanding that the telecom industry in India should:

• Make clear investment plans for the co-development of renewable energy

based generating capacity sources along with development of new telecom

infrastructure. Enable a low-carbon economy by playing a significant role in

advocating strong climate and energy policy changes in favor of renewable

energy sources and technologies at national and international levels. Commit to

24

shifting the sourcing of their energy requirements significantly towards

renewable sources.

Demand-related Factors

Demand for telecom services evolves from a core demand for a homogenous

output –basic telephony – for which pure transmission is the common ingredient

in a wide range of services, where transmission often is combined with other

service functions. Increasingly these services are offered by service providers

other than the provider of the basic transmission services, Other producers may

be foreign telecom operators, computer companies or companies from another

industry. Cost structures differ for different services, and market structure

depends a great deal on the type of service demanded.

KEY SUCCESS FACTORE OF TELECOM INDUSTRY

PEST ANALYSIS

7.KEY SUCCESS FACTORE OF TELECOM INDUSTRY.

MARKET POSITION:-

25

The company presence& dominant in the market can be reflected by the

company business size as well as market share in each business segment

through number of subscribers, numbers of tariffs’ or connection time, plus

production and etc. the capability enlarge the customer base in line with

capability to enhance the network coverage. Which often require of sizable

investment cost. Therefore market position of cellular company usually depend

on the financial capacity to support the capital expenditure.

OPERATING MANAGEMENT:-

The company quality also play key role through it’s businesses strategy to

anticipate the rapid growth of technology global trend and change in regulation

as well as ability to generate efficiency businesses activity. Which can be

indicated by growth of probability of margin of from each business segment,

average revenue per users, revenue per employee, tariff setting for each

services. The company also advantage to capture more market opportunity

relatively stronger price position, which can generate sustain margin to cover

the cost of investment research &development.

DIVERSIFICATION:-

The company ability to event diversify revenue generation base the on the type

of basis or services provide market segment and areas include revenue from

overseas market can insure it’s revenue stream. The capability to product

differentiation as well as disperse revenue from various segment market

geographical areas not will ensure the stability of the companies but also

provide particular business downturn.

QUALITY Of SERVICES & INFRASTRUCTURE:-

The company ability to provide satisfactory services to customer it’s on the key

success factor ,which can be reflected by it’s network coverage areas line

exchange capacity technology, users for the services which will determined the

connection quality ,numbers and accessibility of it’s customers services

26

supports as well as other operational indicators such as level of churn rates

successful connection ratios, track records of any major disruption and etc.

8.PEST ANALYSIS:-

POLITICAL :-

The telecom business has always experienced government regulation and

political involvement. Recently, for example, the Federal

Communications Commission (FCC) issued its guidelines related to net

neutrality: FCC 1, Business 0. That trend continues today with companies

involved in the wireless business. More specifically, the government is

heavily involved in the proposed merger of AT&T and T-Mobile as well

as the approval of Light Square’s nationwide Long-Term Evolution

(LTE) network.

27

The benefits of the merger seem to be that AT&T will have far greater

coverage of GSM/WDCMA/HSPA/LTE by acquiring all the T-Mobile

sites. That is a good thing for subscribers since greater coverage usually

leads to broader, more reliable, and faster service. Furthermore, with

more area covered, the implementation of the government’s National

Broadband Plan becomes more realistic.

The downside, of course, is the threat of price hikes given the less

competitive nature of the market. Of course, the inevitable consolidation

of resources will lead to big layoffs—not such a good thing in our jobless

economy.

ECONOMICAL FACTORS

An important point in relation to the need for regulation is that the

demand profiles of these groups are quite different. A few decades ago

all customers were demanding the same service – namely telephony.

Business customers were generating more traffic but the service

demand was basically the same. Today many business customers are

demanding a wide range of communication services, which only a few

residential customers consider to be relevant for them. On the other

hand cable TV is only of limited use for business customers and other

infotainment services primarily directed toward residential customers

are being developed.

As the load of traffic per connection is relatively low, the needs110for

capacity have been more stable in residential markets than business

markets. Most residential customers have needed only an ordinary

telephone line to meet their demands. Therefore, the need for

investments to upgrade the network have been most apparel in

business districts.

28

Residential Market Business Customers. Homogenous market

Heterogeneous market Many small customers Both small and large

customers1-2 lines per customer Limited load of traffic per line Some

customers with many lines More traffic per line Telephony and Cable-

TV dominant services Demand for a wide range of services Limited

use of advanced services Many customers with special needs.

SOCIAL FACTOR:-

The Indian tea industry directly employs over one million workers, the largest

in any industry of which 60 per cent are women. It takes care of the basic social

needs such as housing, education, Medicare, family welfare, recreation, etc of

four million dependents of these employees. Located in remote rural areas

where infrastructure is significantly lacking and employment opportunity is low

key the tea industry covers all core priorities of our national economy.

TECHNOLOGICAL :-

Technical innovations have contributed to a reduction of barriers to

competition in several ways: Changing structures of network costs:

Reductions in transmission costs limit investments needed for delivery

of the same services. particular the unit costs of the interexchange

network capacity are being reduced continuously.

Development of broadband services is closely related to reductions in

costs of transmission. However, substantial demand for broadband

services will multiply he demand for transmission capacity, and the

costs of both the access and interexchange network will increase as a

result of this major network upgrade.Lifetime of equipment is reduced:

29

With rapid technological innovations old equipment becomes obsolete

more quickly. This increases capital costs (a faster rate of depreciation

is needed), shortens the planning horizon and increases the risk.

Digitization increases economies of scope for provision of facilities,

but reduces economies of scope for service provision. If effective

interconnection rules are established, digitalization improves the

conditions for service providers without their own physical

infrastructure.Satellite and cellular services can provide alternatives

for some local exchange network services. The cost structure of air-

borne services involve few economies of density than wired services.

Therefore a degree of infrastructure competition can be introduced at

lower costs. Although satellite and cellular services cannot be

complete substitutes for wired based services they do reduce the

monopoly power of local exchange operators somewhat, and provide

an alternative for some business and residential services and customers

although far less than a majority.

9. RESEARCH METHODOLOGY

30

Objective of financial analysis:-

Every person has the objectives of respected work therefore I have also the

objectives to make this project report are as under.

To study about financial position of the company.

To know the liquidity position of the company.

To collect the data and find the growth in finance in these three years.

To know how to manage current assets and current liabilities of the

company.

To compare the net profit of the Vodafone & Reliance to previous year.

11.DATA COLLECTION:-

The data collection in this project was through secondary sources. The

secondary sources include Textbooks, journals, internet websites and other

magazines provided the secondary data for the project

31

SCOPE of the study:-

The scope of study in confined to the company “Vodafone & Reliance” is

alarge scale unit. Its scope is very widely. It includes financial analysis of last

three year data. I get the balance sheet and profit & loss account of last three

years.These data are collected from the secondary data method to observe last

three years data and find to the various method of ratio analysis. Last three

years data are very useful to the scope of study to the “Vodafone & Reliance”.

About topic:-

Financial analysis is the process of identifying the financial strengths and

weaknesses of the firm by properly establishing relationship between the items

of the balance sheet and profit and loss account. Management of the firm can

undertake financial analysis, or by parties outside the firm viz. owners,

creditors, investors, and others. The nature of analysis will differ depending on

the purpose of the analyst. The focus of financial analysis is on key figures in

the financial statements and the significant relationship that exist between them.

The analysis of financial statement is a process of evaluating the relationship

between component parts of financial statements to obtain a better

understanding of the firm’s position and performance. The first task of financial

analyst is to select the information relevant to the decision under consideration

from the total information contained in the financial statements. The second step

is to arrange the information in a way to highlight significant relationship. The

final step is to interpretation and drawing of inferences and conclusion.

In brief, analysis is the process of selection, relation and evaluationl

Ratio analysis.

12. Porter's 5 Forces Analysis of Telecom Industry.

32

The five competitive forces model, here is a brief background on who

developed it, and why it is useful. The model originated from Michael E.

Porter's 1980 book "Competitive Strategy. Techniques for Analyzing Industries

and Competitors." Since then, it has become a frequently used tool for

analyzing a company's industry structure and its corporate strategy. In his book,

Porter identified five competitive forces that shape every single industry and

market. These forces help us to analyze everything from the intensity of

competition to the profitability and attractiveness of an industry. Figure 1 shows

the relationship between the different competitive forces.

Porter's five competitive forces.

1. Threat of New Entrants:-

33

The easier it is for new companies to enter the industry, the more cutthroat

competition there will be. Factors that can limit the threat of new entrants are

known as barriers to entry.

Some examples include:

Low Declining Average Revenue Per User. Infrastructure tenancy

costs. Brand pull exists to some extent for brands like Airtel /

Idea/ Vodafone. Extremely high infrastructure setup costs

Spectrum License cost- Lotteries, auctions. Incumbent

Advantages: Established brand image, Reliability of network.

Existing loyalty to major brands. Incentives for using a particular

buyer (such as frequent shopper programs)

High fixed costs

Scarcity of resources

High costs of switching companies

Government restrictions or legislation

2.Power of Suppliers:-

This is how much pressure suppliers can place on a business. If one supplier has

a large enough impact to affect a company's margins and volumes, then it holds

substantial power. Here are a few reasons that suppliers might have power:

Low Large number of suppliers. Shared tower infrastructure.

Limited pool of skilled managers and engineers especially those

well versed in the latest technologies. Medium cost of switching

since changing their hardware would lead to additional cost in

34

modifying the architecture. Overall influence on the industry–

medium.

There are very few suppliers of a particular product .There are no

substitutes Switching to another (competitive) product is very

costly The product is extremely important to buyers - can't do

without it The supplying industry has a higher profitability than

the buying industry

Some examples include:-

Broadband Access: The penetration rate of broadband access in the

United States, the lifeblood of pay VoIP services, is around 55 to 60

percent. This effectively caps the number of customers that have access to

VoIP services and places more power in the hands of the broadband

access providers.

3.Power of Buyers :-

This is how much pressure customers can place on a business. If one customer

has a large enough impact to affect a company's margins and volumes, then the

customer hold substantial power. Here are a few reasons that customers might

have power:

9 .

High Lack of differentiation among the service provider Cut throat competition

Customer is price sensitive.

Increased choice – high bargaining power

Small number of buyers

Purchases large volumes

35

Talented managers & engineers

Switching costs – individual & large business customers.

The product is not extremely important to buyers; they can do without the

product for a period of time.

Customers are price sensitive

Some examples include:-

Pricing: Wireless / cellular and traditional phone service providers have seen

demands from consumer’s drive their price per minute via lower tiered minute

and flat rate plans. Pay VoIP providers are entering not at the top, but closer to

the bottom of these pricing levels.

A few reasons that customers might have power are: there are small number of

buyers, buyers purchase large volumes, customers are price sensitive etc.

4.Availability of Substitutes:-

What is the likelihood that someone will switch to a competitive product or

service? If the cost of switching is low, then this poses a serious threat. Here are

a few factors that can affect the threat of substitutes:

The main issue is the similarity of substitutes.

Some examples include:-

If the price of coffee rises substantially, a coffee drinker may switch over to a

beverage like tea.

If substitutes are similar, it can be viewed in the same light as a new entrant.

36

Wireless Local-Area Networks: The Internet and broadband-based VoIP

market could soon face competitors from the wireless / cellular service

providers (Substitutes) via wireless local area networks.

Low Some Substitutes: VoIP (Skype, Messenger etc.)Online Chat

Email Satellite phones None of the above a major threat in current

scenario, but a potential threat for near future.

5.Competitive Rivalry:-

This describes the intensity of competition between existing firms in an

industry. Highly competitive industries generally earn low returns because the

cost of competition is high. A highly competitive market might result from:

Many players of about the same size;

There is no dominant firm Little differentiation between competitors products

and services.

A mature industry with very little growth; companies can only grow by stealing

customers away from competitors.

Usage of phone,

competition is high

• Price

• Value added services

• Profitability low

37

Some examples include:-

Major players of Indian telecom industry The Top five companies, on the basis

of ‘Market Share’

:1. Bharti Airtel Ltd.2. Reliance Communications Ltd.3. Vodafone Essar Ltd.4.

BSNL5. Idea Cellular + Spice Bottom five companies,

Consolidation: As we have seen in the wireless / cellular service provider

market, this can mean threats from existing companies who consolidate their

position and acquire additional market share by purchasing their competition.

High High Exit Barriers High Fixed Cost6-7 players in each region3 out of 4

BIG, present in each region Very less time to gain advantage by an innovation

(Eg. Caller tunes, life time card)Price wars.

12.1. Company information:-

Vodafone Essar, previously Hutchison Essar is a cellular operator in India that

covers 23 telecom circles in India. Despite the official name being Vodafone

Essar, its products are simply branded Vodafone. It offers both prepaid and

postpaid GSM cellular phone coverage throughout India with good presence in

then metros. Vodafone Essar provides 2.75G services based on 900 MHz and

1800 MHz digital GSM technology, offering voice and data services in 23 of

the country's 23 license areas. It is among the top three GSM mobile operators

38

ofIndia.

Vodafone Essar is owned by Vodafone 52%, Essar Group 33%, and other

Indian nationals, 15%. On February 11, 2007, Vodafone agreed to acquire the

controlling interest of 67% held by Li Ka Shing Holdings in Hutch-Essar for

US$11.1 billion, piping Reliance Communications, Hinduja Group, and Essar

Group, which is the owner of the remaining 33%. The whole company was

valued at USD 18.8 billion. [2] . The transaction closed on May 8, 2007.

Vodafone Year of Establishment Acquired majority stake in Hutch Essar in

India ,by buying out complete stake of Hutch in 2007, Essar is still minority

stakeholder in company.

Company Profile is Vodafone Essar in India is a subsidiary of Vodafone Group

Plc and commenced operations in 1994 when its predecessor Hutchison

Telecom acquired the cellular license for Mumbai. Vodafone Essar now has

operations in 16 circles covering 86% of India's mobile customer base, with

over 45.78 million customers. Vodafone Essar, under the Hutch brand, has been

named the 'Most Respected Telecom Company', the 'Best Mobile Service in the

country' and the 'Most Creative and Most Effective Advertiser of the Year'.

It has operations in 25 countries across 5continents and 40. partner networks

with over 200 million customers worldwide.

39

Reliance Telecom and Flag Telecom, is part of Reliance Communications

Ventures (RCoVL). It is an Indian telecommunications company. According to

National Stock Exchange data, Anil Dhirubhai Ambani controls 66.77 per cent

of the company, which accounts for more than 1.36 billion shares.[3] It is the

flagship company of the Reliance-Anil Dhirubhai Ambani Group, comprising of

power (Reliance Energy), financial services (Reliance Capital) and telecom

initiatives of the Reliance ADAG. It uses CDMA2000 1x technology for its

existing CDMA mobile services, and GSM-900/GSM-1800 technology for its

existing/newly launched GSM services.

Reliance Communications is Year of Establishment:-1999.Company Profile is

Reliance Telecom's cellular services are available in 340 towns within its eight-

circle footprint. Reliance Info comm also offered for the first time in India,

mobile data services though its RWorld mobile portal. This portal leverages the

data capability of the CDMA 1X network. Reliance Info comm offers a

complete range of telecom services covering mobile and fixed lintels phony

including broadband, national and international long distance services, data

services and a wide range of value added services and applications aimed at

enhancing productivity of enterprises and individuals RelCom is also into

Wireline Business throughout India and has the largest optical fiber

communication (OFC) backbone architecture [roughly 110,000 km] in the

country.

Reliance Communications has interests in Direct To Home (DTH) TV also,

known as "Big TV". It plans to launch its DTH business by July 2008. Once

launched, RelCom will have presence across all B2C communications channel

in one of the fastest growing markets in the world. On July 2007, the company

announced it is buying US-based managed ether net and application delivery

services company Yipes Enterprise Services for a cash amount of Rs. 1200

crore rupees (equivalent of USD 300 million). The deal was announced

40

complete in a press release in December 2007.In its first overseas acquisition,

the Reliance group has amalgamated the United States-based Flag Telecom for

Undertook financial restructuring of Reliance communications•To spend Rs 16,000 crore to expand and strengthen network coverage

12. SWOT ANALYSIS

41

SWOT analysis is a basic, straightforward model that provides

direction and serves as a basis for the development of marketing

plans. It accomplishes this by assessing an organizations strengths

(what an organization can do) and weaknesses (what an organization

cannot do) in addition to opportunities (potential favorable conditions

for an organization) and threats (potential unfavorable conditions for

an organization)

42

Strength

attributes of the organization those are helpful to achieving the objective.

Weaknesses:

attributes of the organization those are harmful to achieving the objective.

Opportunities:

external conditions those are helpful to achieving the objective.

Threats:

external conditions that is harmful to achieving the objective.

STRENGTH

Low Entry Cost

Commission Structure

Fast Activation Process

Network

Connectivity

Data GPRS

WEAKNESS

Branding Image

Distribution problem

Limited product portfolio-Only Mobile

Lack of Competitive Strength

Limited Budget

OPPORTUNITY

Preference of GSM over CDMA

New Specialist Application

Rural Telephony

43

New Market, Vertical, Horizontal

Competitors` Vulnerabilities

THREAT

Political destabilization.

New Entrants

44

FINANCIAL ANALYSIS

2.3 MEANING OF RATIO.

“Ratio is well known and most kindly used tolls of financial analysis.

A ratio gives the mathematical relationship between on variable & another. The

usefulness of ratio is ultimately dependent on their intelligent skillful

interpretation.

‘”Financial analysis is process of identifying the financial strength

and weakness of the firm by properly established relationship between the item

of the balance sheet and profit & loss account.”

“ Ratio is used by different people for various purpose. It mainly

helps in valuing the firm in quantitative terms, two groups of people are

interested in valuation of firms and they are creditors & shareholders.”

According to traditional classification ratios are classified into three

categories. They are as under.

(1) Revenue statement Ratios.

(2) Balance Sheet Ratios.

45

2.4 IMPORTANCE OF RATIO ANALYSIS.

Ratio analysis is the important tools of financial analysis of firm. It present facts

on a comparative basis and performance of a firm. Ratio analysis is relevant in

assessing the performance of a firm in respect of the following aspects.

Liquidity Position:-

The ratio analysis helps in assessing liquidity position of a firm. The liquidity

ratios are particularly used in credit analysis by bank and other suppliers of a

short loan.

Long -term solvency:-

The long-term solvency is measured by the leverage and profitability ratios

which focus on earning power and operating efficiency. Ratio analysis reveals

the strength and weakness of a firm.

Operating Efficiency:-

Ratio analysis is also used to measure efficiency of in the management and

utilization of the assets.

Overall Profitability:-

The most important use of ratio analysis is the ascertaining the profitability of a

business on the basis of sales, total assets, and capital employed as well share

holders’ funds in a business.

Inter-firm comparison:-

Ratio analysis is also used for comparison of business’ performance with

competitors as well as industry’s performance. It is indicator of position of a

firm in an industry.

46

15. RESEARCH METHODOLOGY RATIO.

15.1 LIQUIDITY RATIO.

This ratio measures the firm’s ability to meet current obligation. A firm ensures

that it does not surer from lack of liquidity and also does not have excess

liquidity. The failure of a company to meet its obligation due to lack of

sufficient liquidity will result in a poor credit worthiness loss of creditor’s

confidence or even in legal tangle resulting in the closure of the company.

CURRENT RATIO.

The current ratio is calculated by dividing the current assets by the current

liability. The current ratio of the firm measures its short term solvency that is its

ability to meet short-term obligation. The higher the current ratio, the larger is

the amount of rupees available per rupee of current liability, the more is the firm

ability to meet current obligation and greater is the safety of short term creditor.

Current Assets

Current ratio=--------------------------------

Current Liabilit

Vodafone

Years 2009-10 2010-11 2011-12

47

Current Assets 21897646 54471212 63032860

Current Liability 7030237 8305435 13510078

Ratio 3.12 6.56 4.67

Reliance

Years 2009-10 2010-11 2011-12

Current Assets 25862456 28349335 35173485

Current Liability 3471551 3959637 4541512

Ratio 7.44 7.41 7.74

2009-10 2010-11 2011-12

Vodafone 3.12 6.56 4.67

Reliance 7.44 7.41 7.74

0.51.52.53.54.55.56.57.5

Current ratio

Ratio

Interpretation:

This current ratio measures the firms ability to meet it current obligation.

current ratio is more than 4:1. The current ratio represent margin of safety for

creditors, the firms ability to meet their obligation

48

2 NET WORKING CAPITAL RATIO:

Net Working Capital means the different between current assets & current

liability excluding short term bank borrowing is called net working capital.

Net Working Capital

Net Working Capital Ratio = -----------------------------

Net Assets

Net Working Capital;-

Current Assets – Current Liabilities.

Net Assets;-

Fixed Assets Current Assets – Current Liabilities.

Vodafone

Years 2009-10 2010—11 2011-12

Current Assets 21897646 54471212 63032860

- Current Liability 7030237 8305435 13510078

Net assets 65130079 109118824 114387435

Ratio 0.23 0.42 0.43

Reliance

Years 2009-10 2010-11 2011-12

Current Assets 21897646 54471212 63032860

- Current Liability 7030237 8305435 13510078

49

Net assets 32524611 35723959 41048529

Ratio 0.68 0.71 0.74

2009-10 2010-11 2011-12

Vodafone 0.23 0.42 0.43

Reliance 0.68 0.710000000000001

0.740000000000001

0.050.150.250.350.450.550.650.75

Net working capital ratio

ર્�ATi

O

INTERPRETATION:-

The Net working capital ratio indicate the firms potential reservoir of funds. If

the ratio is high than the more proportion of working capital in total assets. If

the ratio is for the higher than the working capital remain idle and the ratio is

lower than the it is bed for the company.

3. QUICK RATIO

Quick ratio is considered to be better measure of the liquidity of a company as

compared to the current ratio. This is because the current ratio includes

50

inventories which cannot be converted into cash. The ideal quick ratio is

assumed to be 1:1 for any company. It is computed by dividing the value of

quick assets by liquid liability.

Current Assets - Inventories

Quick ratio = ---------------------------------------------------

Current Liability

Vodafone

Reliance

Interpretation:-

The quick ratio is also more than 2:1 which indicate more penetrating test of

liquidity than the current ratio. This ratio represents the company ability to meet

51

Years 2009-10 2010-11 2011-12

Current Assets 21897646 54471212 63032860

- Inventories 4279295 13526986 17583190

Current Liability 7030237 8305435 13510076

Ratio 2.51 4.93 3.36

Years 2009-10 2010-11 2011-12

Current Assets 21897646 54471212 63032860

- Inventories 13463272 14840585 14859056

Current Liability 35996162 396883596 45890041

Ratio 3.57 3.66 4.19

its immediate obligation . here the ratio is whole year the ratio excludes the

inventory and bank over staff. From the above chart we can conclude that the

main reason in decline the ratio is the reduction of investment done by the

company in the inventories. This is shows that the company seems to plan its

production well in advance. Also even as a result of reduction still the quick

ratio for the company is greater than the ideal ratio of 2.5.

. 4. CASH RATIO.

The cash position ratio is calculated by dividing the cash plus marketable

securities with the current liability of the firm. Where the marketable

securities is share capital. The higher the cash position of the strong the

position of the company in the market.

Cash

Cash ratio = ----------------------------

Current Liability

Vodafone

YEAR 2009-10 2010-11 2011-12

Cash 1234434 1630314 2541662

Current Liability 7030237 8305435 13510078

Ratio 0.17 0.19 0.18

52

Reliance

YEAR 2009-10 2010-11 2011-12

Cash 2106002 2677103 3044191

Current Liability 3471551 3959637 4541512

Ratio 0.60 0.67 0.62

2009-10 2010-11 2011-12

Vodafone 0.17 0.19 0.18

Reliance 0.600000000000001

0.670000000000002

0.620000000000002

0.050.150.250.350.450.550.65

Cash Ratio

Ratio

INTERPRETATION:-

Cash ratio shows the total cash available against the current liability. Here this

ratio is the decrease year by year so, it is not good for the company. The ratio of

the company is decrease from the year 2009-10the ratio is 0.17 and the ratio in

the year 2010-11 is 0.18. It has cash ratio indicates that in this year the cash

ratio is satisfying in compare to last year.

53

15.2 LEVERAGE RATIO.

To judge the long term financial position of the firm financial of leverage of

capital structure ratio are calculated. The process of magnify the share holder

return through the use of debt is called “financial leverage” or “financial

gearing” or “ trading on equity.”

Leverage ratio are calculated to measure the financial risk and the ability of

using debt.

.

1 . DEBT EQUITY RATIO.

This ratio indicates to how many times do the creditors contributes for each

time of the owner’s contribution. It is calculated as follow.

54

Total Debt

Debt Equity Ratio = ----------------------------

Net Worth

Total Debt;- Secured loans + Unsecured loans + Sundry Creditors.

Vodafone

YEAR 2009-10 2010-11 2011-12

Total Debt 55922358 83335745 82303553

Net Worth 15816636 32199848 43507195

Ratio 3.54 2.59 1.89

Reliance

YEAR2009-10 2010-11 2011-12

Total Debt 25315385 26334822 57190655

Net Worth 55077171 56813862 58550554

Ratio 0.46 0.65 0.91

55

2009-10 2010-11 2011-12

Vodafone 3.54 2.59 1.89

Reliance 0.46 0.650000000000002

0.91

0.250.751.251.752.252.753.253.75

Debt Equity RatioRa

tio

Interpretation:-

Here Debt-Equity ratio indicate, numerator is an equity part while denominator

is a debt part. So we can easily say that equity part is more than debt part.

.2 INTEREST ON COVERAGE RATIO.

56

This ratio is also known as “Time interest earned ratio”. It measures the debt

servicing the capacity of firm in so far as fixed interest on long term is

concerned.

E.B.I.T

Interest On Coverage Ratio = -----------------------------------

Interest

Vodafone

Years 2009-10 2010-11 2011-12

E.B.I.T 4316143 7488303 9224754

Interest 3426813 5876380 6939261

Ratio 1.25% 1.27% 1.32%

Years 2009-10 2010-11 2011-12

E.B.I.T 3298138 4030289 5396556

Interest 2845009 2524072 3498874

Ratio 1.15 1.59 1.53

57

2009-10 2010-11 2011-12

Vodafone 1.25 1.27 1.32

Reliance 1.15 1.59 1.53

0.10.30.50.70.91.11.31.5

Interest on coverage atioRa

tio

INTERPRETATION:-

The ratio is continuously year by year it is good from the company’s point of

view. In the year 2010-11 it is 1.27% and then increases by 0.05% point it is

good for the company.

15.3 PROFITABILITY RATIO. (%)

58

PROFITABILITY RATIO OF TWO YTPES;-

1. Profitability in relation to sales.

2. Profitability in relation to investment.

1. RETURN ON EQUITY.

This ratio indicates how many times the earnings are obtain as

related to the return provided to the shareholders. It is calculated as follow.

Net Profit After Tax

Return On Equity Ratio = ----------------------- × 100

Net Worth

Net Worth;-

Share capital + reserve & surplus

Years 2009-10 2010-11 2011-12

Net Profit After Tax 863783 1532171 1492690

Net Worth 15816636 32199848 43507195

Ratio 5.46% 4.76% 3.43%

Years 2009-10 2010-11 2011-12

Net Profit After Tax 3298138 4030289 5396556

59

Net Worth 55077171 56813862 58550554

Ratio 3.11 % 3.26% 3.28%

2009-10 2010-11 2011-12

Vodafone 0.0546 0.0476 0.0343

Reliance 0.0311 0.0326000000000001

0.0328000000000001

0.50%

1.50%

2.50%

3.50%

4.50%

5.50%

Return on equity ratio

Ratio

INTERPRETATION:-

From the above calculations we can observe that there is a continuous rise in the

returns provided by the company to the shareholder. This is a good for the

company. For an Rs 1 investment by Shareholder Company gives 3.43 Paisa in

the present year.

2. NET PROFIT RATIO.

60

As the name suggest the net profit ratio is calculated by dividing the net profit

with the sales and multiplying by hundred.A high net profit ratio obtain cost of

production is rising and demand for the product is falling. A firm with a low

profit margin can earn a high rate of return on investment.

Net profit After Tax

Net profit ratio = --------------------------- × 100

Net sales

Years 2009-10 2010-11 2011-12

Net profit 863783 1532171 1492690

Net Sales 77397386 176395209 263421217

Ratio 1.12% 0.87% 0.54%

Years 2009-10 2010-11 2011-12

Net profit 1717764 1852760 1919496

Net Sales 57374086 63974385 75317434

Ratio 2.99% 2.89% 2.55%

61

2009-10 2010-11 2011-12

Vodafone 0.0112 0.00870000000000001

0.00540000000000001

Reliance 0.0299 0.0289 0.0255

0.25%

0.75%

1.25%

1.75%

2.25%

2.75%

Net profit ratioRa

tio

Interpretation:-

Net profit ratio shows relationship between net profit & sales and indicates

management efficiency in manufacturing administrating and selling of products.

As we can see from calculation& graph that the net profit ratio is fluctuating

which not good for the company.Net profit ratio must be continuous and this

good for the company.Net profit ratio which indicates that management

efficiency in mfg., administering, and selling the product. Net profit 0.54%%

which slightly less than previous year.

3 RETURN ON INVESTNENT RATIO.

62

This ratio indicates that the earning obtained for the company are hoe much as

comparable to the capital employed by the company. It is calculated as follow:

E.B.I.T.

Return On Investment Ratio= -------------------------- ×100

Capital Employed

Years 2009-10 2010-11 2011-12

E.B.I.T 4316143 7488303 9224754

Capital Employed 15816636 32199848 43507195

Ratio 22% 23% 21%

Years 2009-10 2010-11 2011-12

E.B.I.T 3298138 4030289 5396556

Capital Employed 55077171 56813862 58550554

Ratio 5% 7% 9%

63

2009-10 2010-11 2011-12

Vodafone 0.22 0.23 0.21

Reliance 0.05 0.07 0.09

3%

8%

13%

18%

23%

Return on investment ratioRa

tio

INTERPRETATION:-

From the above calculations we can observe that is a continuous rise in this

ratio which indicates that the earning of the company is growing consistently.

On a Rs. 1 investment in the year 2009-10 provided a return of 0.22% paisa

while in the year2010-11 financial year the investment of Rs.1 provided a

return of0.23% paisa. in the year2011-12 financial year the investment of Rs.1

provided a return of 0.21%paisa

64

.4 RETURN ON CAPITAL EMPLOYED.

This ratio indicates how many times the earnings are obtain as related to the

return provided to the shareholders. It is calculated as follow.

Net Profit Before Tax

Return On Capital Employed Ratio = -------------------------- × 100

Capital Employed

Capital Employed;-

Share capital + reserve & surplus + Debenture.

Years 2009-10 2010-11 2011-12

Net Profit Before Tax 4316143 7488303 9224754

Capital Employed 15166368 32199848 43507195

Ratio 27.28% 23.25% 21.20

Years 2009-10 2010-11 2011-12

Net Profit Before Tax 1717764 1852760 1919496

Capital Employed 55077171 56813862 58550554

Ratio 5.98 7.09 9.16

65

2009-10 2010-11 2011-12

Vodafone 27.28 23.25 21.2

Reliance 5.98 7.09 9.16

2.5

7.5

12.5

17.5

22.5

27.5

Retrun on capital employed ratioRa

tio

Interpretation:-

From the above calculations we can observe that is a continuous rise in this ratio

which indicates that the earning of the company is growing consistently.

66

1 5. 4 . ACTIVITY RATIO.

The activity ratio are employed to evaluated the efficiency with which the firm

manager utility it’s assets there ratio also called” Turn over ratio “it’s show the

relationship between shares & assets.

.1. NET ASSETS TURN OVER RATIO.

This ratio indicates to how many times the sales of the

company are as compared to the investment of the company in the total assets.

A net asset is obtained as the sum total of the fixed and net current assets of the

company.

Sales

Net assets turn over ratio = ----------------------------

Net Assets

Net Assets;-

Fixed Assets + Current Assets – Current Liabilities.

Years 2009-10 2010-11 2011-12

Sales 77397386 176395209 263421217

Net Assets 6513079 109118824 114387435

Ratio 1.19 1.62 2.30

67

Years 2009-10 2010-11 2011-12

Sales 57374086 63974385 75317434

Net Assets 32524611 35723959 41048529

Ratio 1.76 1.79 1.83

2009-10 2010-11 2011-12

Vodafone 1.19 1.62 2.3

Reliance 1.76 1.79 1.83

0.25

0.75

1.25

1.75

2.25

Net assets turnover ratio

Ratio

INTERPRETATION:-

From the above calculations we can observe that there is an increase in this

ratio over the various financial years. This indicative of the fact that the sales of

the company are increasing for each the we carefully analyze that the last

financial ratio it indicates that the sales of the company were of Rs. 1.19 per

each investment of Rs. 1 in the assets of the company as compared to the first

financial year which indicates that the sales of the company were of Rs. 1.62 for

the investment of each Rs. 1 in the company assets.

68

.2. FIXED ASSETS TURN OVER RATIO.

To ascertain the efficiency and profitability of business, the

total fixed assets are compared to sales. The more the sales in relation to the

amount invested in fixed assets, the more the efficient is the use of fixed assets.

It’s indicating higher efficiency. If the sales are less as compared to investment

in fixed assets, it means that fixed assets are not adequately utilized in the

business.

Sales

Fixed assets turn over ratio= ---------------------------

Fixed Assets

Years 2009-10 2010-11 2011-12

Sales 77397386 176395209 263421217

Fixed Assets 50262670 62953047 64864651

Ratio 1.54 2.80 4.06

Years 2009-10 2010-11 2011-12

Sales 57374086 63974385 75317434

Fixed Assets 101333706 10334261 10716556

Ratio 5.66 6.19 7.02

69

2009-10 2010-11 2011-12

Vodafone 1.54 2.8 4.06

Reliance 5.66 6.19 7.02

0.51.52.53.54.55.56.57.5

Fixed assets turnover ratio

Ratio

INTERPRETATION:-

Higher net fixed assets ratio shows good result and it shows efficient use of

fixed assets. If the ratio is low then the utilization of the fixed assets is not

efficient. Here the ratio is, 1.54, 2.80 and 4.06 in the year, Here the company’s

fixed assets turnover ratio is higher. It shows better position of the company.

70

.3. TOTAL ASSETS TURN OVER RATIO.

The total amount invested in all assets jointly and sales are

offered through them to earn profits. So in order to find out the relation between

total assets turn over ratio.

Sales

Total assets turn over ratio = -----------------------------

Total Assets

Total Assets;-

Fixed Assets + Current Assets.

71

Years 2009-10 2010-11 2011-12

Sales 77397386 176395209 263421217

Total Assets 72160316 117424259 127897511

Ratio 1.07 1.50 2.06

Years 2009-10 2010-11 2011-12

Sales 57374086 63974385 75317434

Total Assets 35996162 396883596 45890041

Ratio 1.59 1.61 1.64

2009-10 2010-11 2011-12

Vodafone 1.07 1.5 2.06

Reliance 1.59 1.61 1.64

0.25

0.75

1.25

1.75

2.25

Total assets turnover ratio

Ratio

INTERPRETATION:-

If the ratio is higher it shows that with less amount of investment in total assets,

the business has a capacity to sell more and as such its profitability is also more.

The ratio of the company in2010-11is 2.06 shows the favorable position of the

business. The ratio is increase year by year for the company.

72

15.5 . PROPRIETERY RATIO.

The proprietary ratio is calculate by dividing the proprietors fund by the total

assets of the firm with multiplying by hundred. Where as the proprietors fund is

the sum of share capital and reserve and surplus and the total assets is the sum

of net assets, investment and net current assets of the firm.

The ratio shows the proportion of proprietors funds to the total assets employed

in the business. The higher the ratio the stronger the financial position of the

enterprise.

Proprietor’s capital

Proprietary ratio =--------------------------------------- × 100

Total Assets

Proprietor’s capital;-

Share capital + reserve & surplus.

Total Assets;-

Fixed assets + Current assets.

Years 2009-10 2010-11 2011-12

Proprietor’s

capital

55077171 56813862 58550554

Total Assets 72160316 117424259 127897511

73

Ratio 21.9% 27.42% 34.01%

Years 2009-10 2010-11 2011-12

Proprietor’s

capital

55077171 56813862 58550554

Total Assets 35996162 396883596 45890041

Ratio

1.53 1.43 1.43

2009-10 2010-11 2011-12

Vodafone 21.9 27.4 34

Reliance 1.53 1.43 1.43

2.5

7.5

12.5

17.5

22.5

27.5

32.5

Proprietary ratio

Ratio

Interpretation:-

The ratio shows the proportion of proprietors funds to the total assets

employed in the business. In above the graph the proprietary ratio is satisfactory

74

position. In the years, 2009-10, 2010-11 and 2011-12 the ratio is, 21.9, 27.42

and 34.01% respectively.

1 6 . CONCLUSION.

75

We have good experience to know about “Vodafone & Reliance” its efficient

financial management. The company is now very good position. It has the

approval of many good standards. This is also improving the in the mind of the

investors and parties related to the company.

The sale of the Vodafone & Reliance is very good, but the company should try

to reduce the cost of production and administration by efficient use of resources.

This way Vodafone & Reliance can improve its profitability ratio.

After observation over all position of the Vodafone & Reliance. we can say that

overall position of company is very sound and company would progress very

fast in the future Reliance compare to Vodafone ..

This current ratio measures Reliance better compare to Vodafone ability to

meet it current obligation. Quick ratio represents the company ability to meet

its immediate obligation .

The return on equity means the rate of return on equity share by the holder of

the share. Return on equity shows the earning of equity shareholders, this shows

that how much rate of return shareholder is good “Vodafone & Reliance”.

18 . ANNEXURE.

76

19. PROFIT 1 1 & LOSS A/C. of V odafone

PARTICULAR 2009-10 2010-11 2011-12

(A). INCOME

Sales a/c 77397386 176395209 263421217

Other income 1630659 5389185 4631825

TOTAL (A) 79028045 181784394 268053042

(B). EXPENDITURE

Raw-material consumed

3519420 14825000 15478826

Manufacturing expenses

14392303 16885063 18009224 Purchase 49218432 138662236 194658333

Other expenses 2682434 3557390 5836720

Interest 3426813 5876380 6939261

Depreciation14,72,500 17,90,022 2384750

Total Expenditure 74711902 174296091 258828288

Profit Before Tax 4316143 7488303 9224754

Provision for Taxation

-Current Tax 698172.00 3273500 5527530

-Deferred Tax 2695271 2473835 1957120

-For Fringe Benefit Tax 58917 208797 247414

Profit after Taxation 863783 1532171 1492690

Surplus at the Beginning 0.50 .32 0.74

BALANCE AVAILABLE FOR APPROPRIATION

863783.50 1532171.32 1492690.74

19. Balance Sheet of . V odafone

PARTICULAR 2009-10 2010-11 2011-12

77

SOURCES OF FUND;-

share holder’s capital 15000000 30000000 40000000

Reserve & surplus 166368 2199848 3507195

LOAN FUNDS:-

Unsecured loans 30079470 11241355 6287820

Secured loans 20420342 66605470 654557889

Sundry Creditors 5422546 5488920 10557844

TOTAL 71738994 115535593 125810746

APPLICATION OF FUNDS;-

FIXED ASSETS 50262670 62953047 64864651

INVESTMENT 75,000 75,000 75,000

CURRENT ASSETS;-

Inventories 4279295 13526986 17583190

Sundry Debtors 4422546 5488920 10557844

Cash & bank balance 1234434 1630314 2541662

Other current assets 16799454 48214311 51609782

loans & advances 600646 692981 790234

Current Assets 21897646 54471212 63032860

Total Current Assets 72160316 117424259 127897511

Less :-Current Liability & Provision 7030237 8305435 13510078

NET CURRENT ASSETS 65130079 109118824 114387435

Miscellaneous Expenditure 1186369 927849 865467

TOTAL 71738994 115535593 125810746

20.1 PROFIT & LOSS A/C. of Reliance

PARTICULAR 2009-10 2010-11 2011-12

(A). INCOME

Sales a/c 57374086 63974385 75317434

78

Other income 208973 228900 225000

TOTAL (A) 57583059 64203285 75542434

(B). EXPENDITURE

Raw-material

consumed

24089306 26824913 32471500

Manufacturing

expenses 8347150 10467085 1106325

Other expenses 7992004 8715933 9246130

Interest 2845009 2524072 3498874

Depreciation 1501728 11640993 13845045

Total

Expenditure

54284921 60172996 70167856

Profit Before Tax 3298138 4030289 5396556

Provision for Taxation 1580374 2177529 3397060

Profit after Taxation 1717764 1852760 1919496

20.1 Balance Sheet 0f Reliance

PARTICULAR 2009-10 2010-11 2011-12

SOURCES OF FUND;-

share holder’s capital 52000000 52000000 52000000

Reserve & surplus 30771716 4813862 6550554

79

LOAN FUNDS:-

Unsecured loans 19791333 19543940 19028260

Secured loans 5524052 6690882 38162395

Sundry Creditors 5422546 5488920 10557844

TOTAL 80392556 83148684 115741209

APPLICATION OF

FUNDS;-

FIXED ASSETS 101333706 10334261 10716556

INVESTMENT 1550001 1550001 1550001

CURRENT ASSETS;-

Inventories 13463272 14840585 14859056

Sundry Debtors 24013570 234001 183690

Cash & bank balance 2106002 2677103 3044191

Other current assets 136420 425270 325000

loans & advances 812346 120690 872500

Current Assets 25862456 28349335 35173485

Total Current Assets 35996162 396883596 45890041

Less :-Current Liability &

Provision

3471551 3959637 4541512

NET CURRENT ASSETS 32524611 35723959 41048529

Miscellaneous Expenditure 47667945 47424725 74692680

TOTAL 80392556 83148684 115741209

80

21. BIBLIOGRAPHY:-