Aitor Erce's discussion of "The Seniority Structure of Sovereign Debt"

16

“The Seniority of Sovereign Debt” (M. Schlegl, C. Trebesch & M.Wright) A discussion by Aitor Erce (European Stability Mechanism) Debt Sustainability and Lending Institutions Cambridge University 2 nd -3 rd September 2016

-

Upload

ademuproject -

Category

Economy & Finance

-

view

92 -

download

0

Transcript of Aitor Erce's discussion of "The Seniority Structure of Sovereign Debt"

“The Seniority of Sovereign Debt”

(M. Schlegl, C. Trebesch & M.Wright)

A discussion by Aitor Erce (European Stability Mechanism)

Debt Sustainability and Lending Institutions

Cambridge University

2nd-3rd September 2016

Introduce a detailed dataset on the existence of payment arrears by

sovereign on various types of external creditors: multilateral, bilateral,

foreign banks, foreign-law bonds & trade credits.

Compute measures of relative importance of arrears per creditor group

and study their determinants: fundamentals vs. “pure discrimination”.

Introduce a dataset on restructurings with private and official creditors.

Methodology to calculate haircuts on official debt

Stylised facts and determinants of haircut sizes

Main fact: Clear pecking order (Multilateral, bonds, bilateral, banks,

suppliers.

Main policy message: The official sector should reconsider its approach

to debt restructuring

1

- Concerns regarding public debt overhang in both AEs and EMEs.

If the overhang is not dissolved, someone will end up losing money…who ?!!

- Sovereign risk literature recognizes the role of the sovereign’s creditor structure

One very important aspect, when studying (modelling) default, regards to the

extent to which different creditors may face burdens in resolving a default.

These burden sharing differences reflect the extent to which some types of

creditors are senior vis-à-vis other creditors.

The theoretical literature models seniority with very little empirical guidance.

This paper informs these efforts by presenting two amazingly rich datasets,

computing seniority metrics and characterizing the creditors’ pecking order.

In my view this is a major step forward and, as with his previous efforts,

empiricists and theorists we will all learn from it and, if ever released, use the

data extensively.

2

3

*

Arrears represent the extent to which interest and principal fails to be paid when due. As such, they measure how creditors are treated while a country undergoes a sovereign default.

But…A larger accumulation of arrears need not imply that, after default is cured, losses are going to be higher on an NPV sense.

For understanding that, why not mingling the arrears data with the haircuts after restructuring?

4

*

About half of the debt restructurings on the sample occurred without accumulation of arrears.

Anecdotal evidence seems to indicate that trade credits are not “haircuted”

How do we know that, in those cases, discrimination did not operate on the opposite direction?

Note that this does not invalidate the ranking that emerges from the categories present on the haircuts database

5

*

The credit instruments provided by the various groups of creditors have different characteristics.

One such characteristic that can be important to understand the results is the maturity of the underlying instruments.

In the absence of acceleration clauses (or if they are not triggered), the longer the maturity of the instruments, the longer it takes for principal to become unpaid.

Could this partly explain the remarkably junior status of trade creditors/suppliers?

Do bonds and bank loans have different acceleration features (acceleration might be simpler for bank loans)?

6

*

When comparing seniority via haircuts, authors use a price metric.

What about the quantity metric? The amount of private claims involved is systematically larger than that of the official sector.

If one computes the product of the debt involved and the average haircut per unit of debt involved, does the discrimination ranking change?

7

*

Various (missing) elements can explain the direction of discrimination:

Origin of the liquidity pressures - debt servicing perspective

Legal framework - Ease to modify terms varies across instruments

Private sector dependence on foreign funds (IIPL composition) – limit spill-overs

Sovereign engagement with the International Monetary Fund – Lending into Arrears Policy

8

*

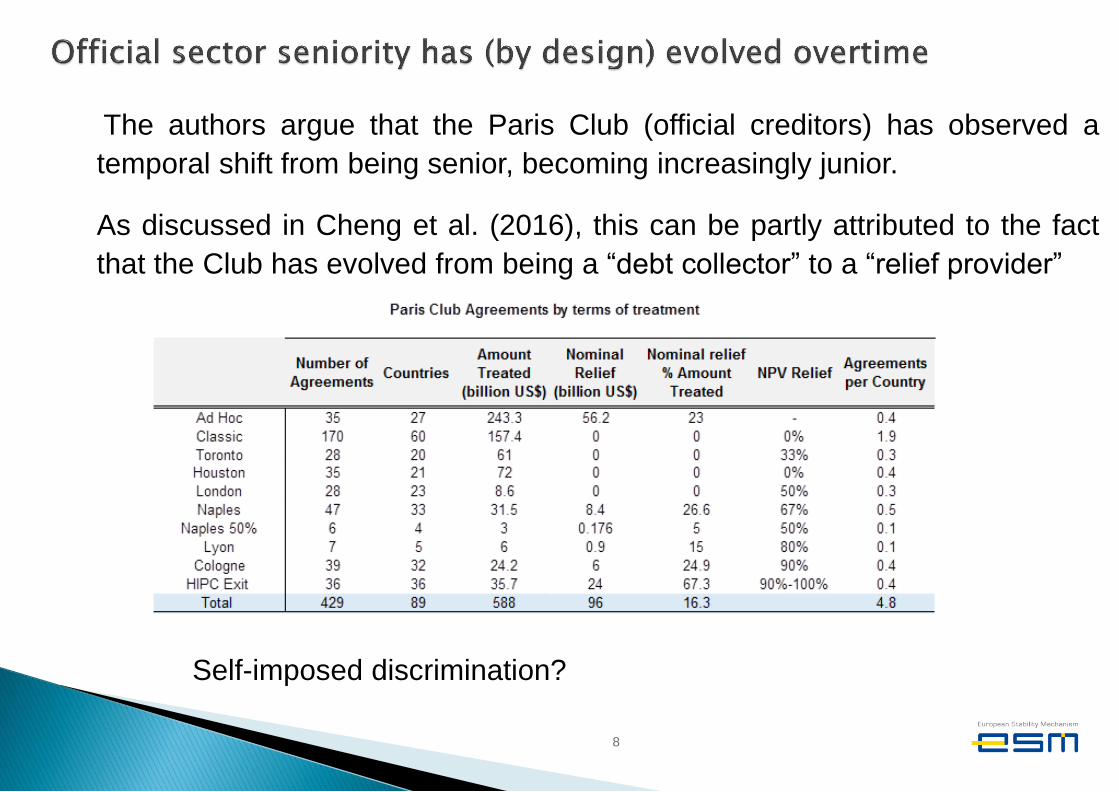

The authors argue that the Paris Club (official creditors) has observed a

temporal shift from being senior, becoming increasingly junior.

As discussed in Cheng et al. (2016), this can be partly attributed to the fact

that the Club has evolved from being a “debt collector” to a “relief provider”

Self-imposed discrimination?

The paper presents a new method to compute haircuts on official debt:

- In computing haircuts, the paper uses average terms of borrowing (ATB) from

the WB, which is an annual average. Would it make sense to use current year

ATB for defaults on the second half of year and past year ATB for those

occurring on the first half of the year? Does it make a difference?

- How have they evolved overtime? According to Cheng et al. calculations,

haircuts started to increase since the early 90s. Do you obtain similar results?

The paper studies discrimination by adding creditor dummies into the

econometric specifications:

- If trends for PS and OS haircuts are present, Are these a concern when running

the econometric analysis?

- Why the arrears regressions separate banks and bonds but the haircut

regressions do not?

9

10

*

One stylised fact arising from the haircuts database is that serial restructuring is present both for private and official claims.

As regards OSI, the authors may want to clarify that some of those sequences correspond a pre-determined plan.

As detailed in Cheng et al. (2016), the HIPC Initiative and the Evian approach (both PC restructuring tools) imply sequences of 2-3 sequential restructurings.

11

*

The absence of detailed information has forced Chris & co. to stay short from broadening the creditor group to include domestic/resident creditors.

Such extension, if feasible, would be incredibly informative for the theoretical literature, where the foreign/domestic divide is increasingly important and seems to lack guidance.

Most models assume:

- Absence of discrimination (equal treatment)

- Seniority of residents (who either enter in the Government’s U function or can vote the Government out)

12

*

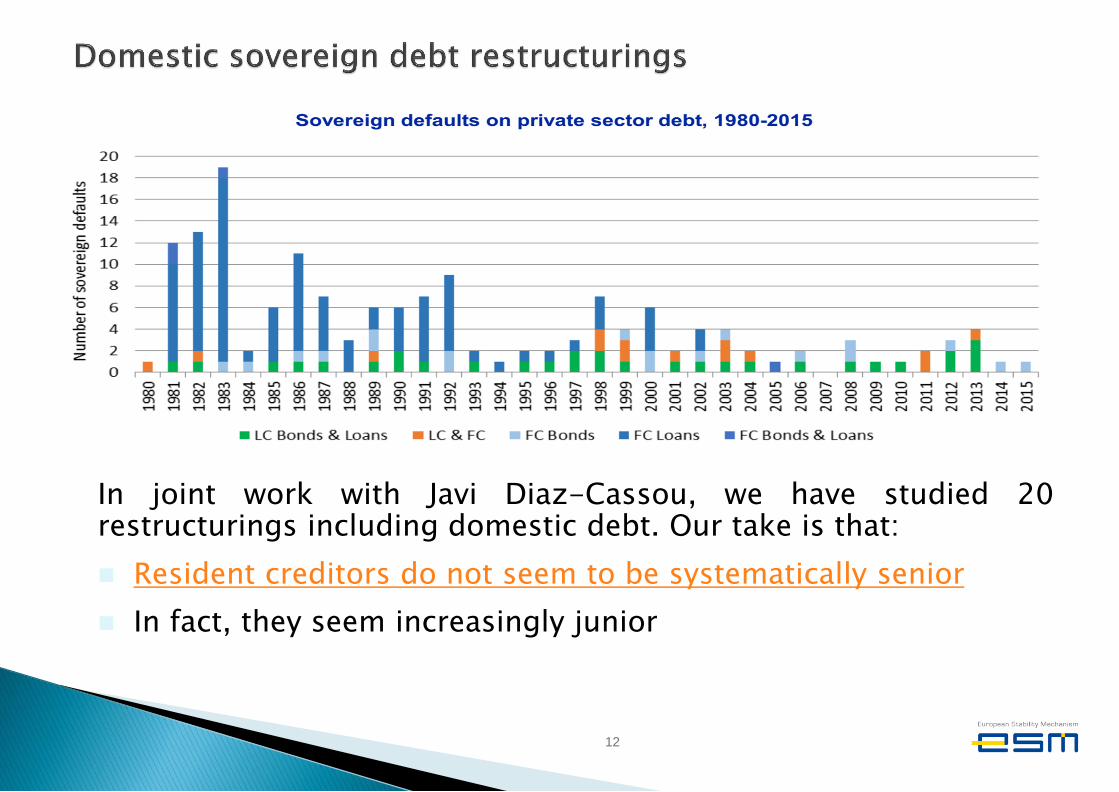

In joint work with Javi Diaz-Cassou, we have studied 20 restructurings including domestic debt. Our take is that:

Resident creditors do not seem to be systematically senior

In fact, they seem increasingly junior

Moreover, there is also a pecking order of domestic creditors.

Using information of IMF program reviews, in Erce (2015) I present information regarding the treatment of domestic non-bank/non debt-holding creditors.

Arrears to local suppliers are large and are the first to accumulate

13

Country Year Volume of Arrears (% GDP)

Russia 1998 3%

Ukraine 1999 5%

Dominican Republic 2005 5.00%

Jamaica 2009 2%

Hungary 2008 1.50%

Greece 2010 6%

Ireland 2011 0%

Portugal 2011 2.50%

Spain 2011 4.50%

This is a really important, nicely crafted, paper.

As always, I have learned a lot from reading Chris’s work and can

only recommend you all to go though this piece

Many layers of analysis…a paper or a research agenda?

14

15