AGRICULTURAL SERVICES - sgs.com · 4 HIGHLIGHTS & OUTLOOK 1st semester 2012 results • Total...

32

1

Transcript of AGRICULTURAL SERVICES - sgs.com · 4 HIGHLIGHTS & OUTLOOK 1st semester 2012 results • Total...

1

2

V

3

4

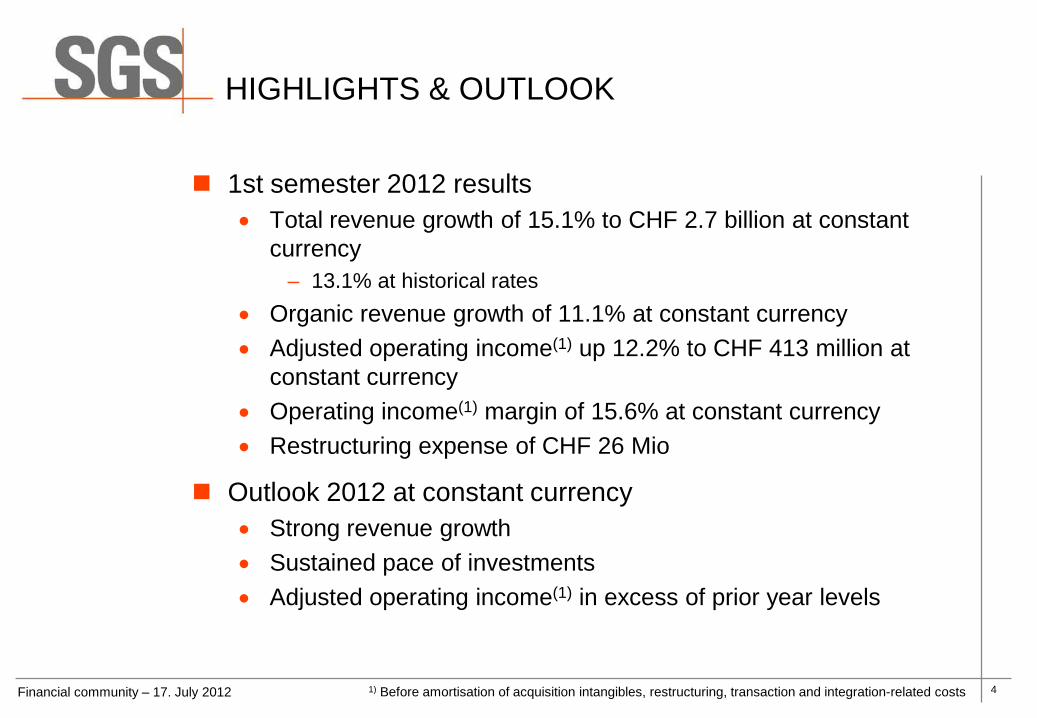

HIGHLIGHTS & OUTLOOK

1st semester 2012 results • Total revenue growth of 15.1% to CHF 2.7 billion at constant

currency – 13.1% at historical rates

• Organic revenue growth of 11.1% at constant currency • Adjusted operating income(1) up 12.2% to CHF 413 million at

constant currency • Operating income(1) margin of 15.6% at constant currency • Restructuring expense of CHF 26 Mio

Outlook 2012 at constant currency • Strong revenue growth • Sustained pace of investments • Adjusted operating income(1) in excess of prior year levels

Financial community – 17. July 2012 1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

5

FINANCIAL HIGHLIGHTS

1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs 2) Constant currency basis

Financial community – 17. July 2012

CHF million 2012June

2011June

2011June

Pro-forma(2) Published

Revenue 2,651 2,303 2,345 Change in % 15.1 % 13.1 %

Adjusted Operating Income(1) 413 368 374 Change in % 12.2 % 10.4 %

Adjusted Operating Income Margin (1) 15.6 % 16.0 % 16.0 %

Operating Income (EBIT) 373 357 363 Change in % 4.5 % 2.8 %

Net income 245 241 246 Change in % 1.7 % (0.4)%

Adjusted Basic EPS (CHF) 36.26 33.08 33.71 Basic EPS (CHF) 32.16 31.72 32.30 Period end no. of employees 76,993 67,144

6

SERVICE PORTFOLIO

Financial community – 17. July 2012

AGRI6.0%

MIN18.8%

OGC14.8%

LIFE1.8%CTS

23.9%

SSC7.6%

IND9.8%

ENVI2.9%

AUTO7.6%

GIS6.8%

ADJUSTED OPERATING INCOME(1)AGRI

6.5%

MIN15.9%

OGC18.8%

LIFE3.6%CTS

16.5%

SSC7.0%

IND15.9%

ENVI5.7%

AUTO5.5%

GIS4.6%

REVENUE

EUROPE / AFRICA /

MIDDLE EAST48.2%

AMERICAS23.6%

ASIA PACIFIC28.2%

REVENUE REGION

1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

7

8

REVENUE GROWTH COMPOSITION

Financial community – 17. July 2012

RevenuesJune 11 Organic Acquisitions Disposals

Currencyimpact

RevenuesJune 12

2,345

256 92

(42)

2,651

11.1% 4.0% 0.0% (2.0)% 13.1%

Constant currency growth: 15.1%

9

YEAR-OVER-YEAR H1 REVENUE GROWTH

Financial community – 17. July 2012

11.5% 15.1%

4.1%

1.0%

9.7% 11.1%

0.3%

1.9% 1.9% 0.7%

3.1% 4.0%

1.4%

(7.0)%

(4.7)%

(0.7)%

(13.1)%

(2.0)%

2007 2008 2009 2010 2011 2012

Organic Acquisitions/Disposals Currency Impact

13.2% 10.0% 1.3% 1.0% (0.3)% 13.1 %

15.1%

10

LOCAL CURRENCY GROWTH BY BUSINESS

Financial community – 17. July 2012

11.1%

20.5%

5.3%

5.5%

9.0%

6.0%

11.5%

(2.5)%

11.2%

20.6%

13.3%

4.0%

3.1%

6.1%

9.4%

1.5%

0.9%

0.6%

10.9%

0.7%

TOTAL

GIS

AUTO

ENVI

IND

SSC

CTS

LIFE

OGC

MIN

AGRI

Organic Acquisition Disposal

14.0%

31.5%

11.8%

(1.6)%

13.0%

6.0%

18.4%

11.6%

8.4%

20.5%

15.1%

11

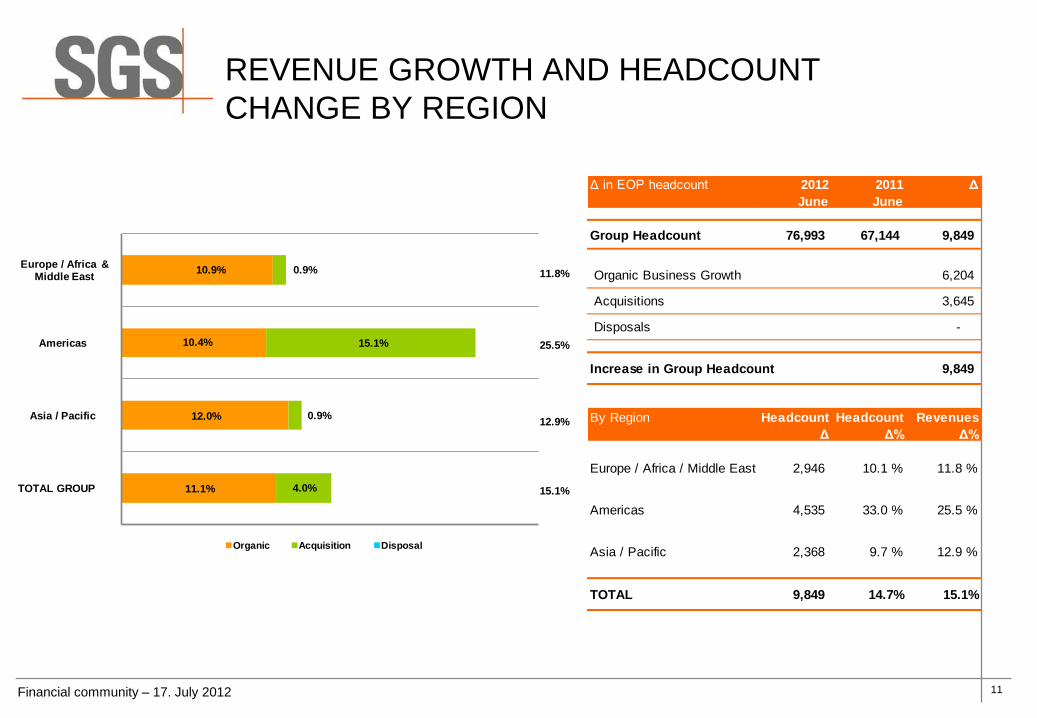

REVENUE GROWTH AND HEADCOUNT CHANGE BY REGION

Financial community – 17. July 2012

11.1%

12.0%

10.4%

10.9%

4.0%

0.9%

15.1%

0.9%

TOTAL GROUP

Asia / Pacific

Americas

Europe / Africa & Middle East

Organic Acquisition Disposal

11.8%

25.5%

12.9%

15.1%

Δ in EOP headcount 2012June

2011June

Δ

Group Headcount 76,993 67,144 9,849

Organic Business Growth 6,204

Acquisitions 3,645

Disposals -

Increase in Group Headcount 9,849

By Region Headcount Δ

Headcount Δ%

Revenues Δ%

Europe / Africa / Middle East 2,946 10.1 % 11.8 %

Americas 4,535 33.0 % 25.5 %

Asia / Pacific 2,368 9.7 % 12.9 %

TOTAL 9,849 14.7% 15.1%

12

13

ADJUSTED OPERATING INCOME(1) GROWTH

Financial community – 17. July 2012

Op. IncomeJune 11 Organic Acquisitions Disposals

Currencyimpact

Op. IncomeJune 12

374

35 10

(6)

413

9.5% 2.7% 0.0% (1.8)% 10.4%

Constant currency growth: 12.2%

1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

14

ADJUSTED OPERATING MARGIN(1) BY BUSINESS

Financial community – 17. July 2012

13.7

%

18.4

%

13.0

%

10.4

%

23.6

%

17.4

%

10.8

%

8.6%

21.1

%

20.7

%

14.4

% 18

.4%

12.2

%

7.9%

22.5

%

16.9

%

9.5%

8.0%

21.8

%

22.8

%

5.0%

10.0%

15.0%

20.0%

25.0%

AGRI

MIN

OG

C

LIFE

CTS

SSC

IND

ENV

AUTO GIS

June 11 June 12

1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

15

RESTRUCTURING COSTS

Financial community – 17. July 2012

AGRI2.7%

MIN19.4%

OGC11.8%

LIFE1.9%

CTS12.9%SSC

6.1%

IND19.0%

ENVI19.8%

AUTO6.4%

RESTRUCTURING BY BUSINESS

Activity closures

21.5%

Location closures

13.9%Cost optimisation

64.6%

RESTRUCTURING BY TYPE

16

CASH FLOW

Financial community – 17. July 2012

CHF million Jun 12 Jun 11

PROFIT FOR THE PERIOD 259 259 Non-cash items 251 208

Depreciation, amortisation and impairment 130 113 Share based payments 9 9 Tax 96 93 Other 16 (7)

(Increase)/decrease in net working capital (155) (130) Taxes paid (111) (109)

OPERATING CASH FLOW 244 228 Net (purchase)/sale of fixed assets (176) (134) Acquisition and divestments of businesses (103) (27) Other from investing activities 4 (5)

CASH FLOW FROM INVESTING ACTIVITIES (275) (166) Dividend paid to equity holders of SGS SA (497) (494) Dividend paid to non-controlling interests (5) (4) Net cash received/(paid) on treasury shares 76 (30) Proceeds of corporate bonds - 714 Interest paid (26) (14) Net flows on interest rate swaps 7 - (Decrease)/increase in borrowings (15) 8

CASH FLOW FROM FINANCING ACTIVITIES (460) 180 Currency translations 7 (10)

INCREASE/(DECREASE) IN CASH AND CASH EQUIVALENTS (484) 232

17

CAPITAL EXPENDITURE

Financial community – 17. July 2012

AGRI6.6%

MIN22.1%

OGC17.1%

LIFE5.0%

CTS21.0%

SSC1.7%

IND8.8%

ENVI5.5%

AUTO2.8%

GIS9.4%

CAPEX BUSINESS

EUROPE / AFRICA /

MIDDLE EAST43.6%

AMERICAS20.5%

ASIA PACIFIC35.9%

CAPEX REGION

150

250

350

450

550

Capital Expenditure Depreciation & amortisation

2007 2008 2009 2010 2011 2012

ANNUAL CAPEXCHF million

18

FOREIGN CURRENCY REVENUES H1 2012

Financial community – 17. July 2012

EUR29.2%

USD14.6%

CNY9.5%

AUD5.8%

CAD4.6%

GBP3.0%

CLP2.9%

TWD2.8%

HKD2.3%

Other25.3%

2012 2011 ChangeEUR 1.2052 1.2713 (5.2)% USD 0.9287 0.9072 2.4 % CNY 0.1469 0.1387 6.0 % AUD 0.9584 0.9366 2.3 % CAD 0.9234 0.9287 (0.6)% GBP 1.4643 1.4650 (0.0)% CLP 0.0019 0.0019 (1.2)% TWD 0.0313 0.0312 0.4 % HKD 0.1197 0.1166 2.7 % INR 0.0178 0.0202 (11.6)%

AVERAGE RATES

19

FOREIGN CURRENCY SENSITIVITY ANALYSIS

Financial community – 17. July 2012

EURO 1.17 1.21 1.24

Revenues (23) 0 22Income (2) 0 2

USD 0.91 0.93 0.95

Revenues (8) 0 9Income (1) 0 1

CNY 0.143 0.147 0.153

Revenues (8) 0 10Income (2) 0 3

21

AGRICULTURAL SERVICES (AGRI)

Overview H1 2012 • Seed and Crop Services continued their positive

trend with +40% revenue growth including 3 acquisitions from 2011. Investments continue to expand the business into new geographies and widen the service offering.

• Trade Services benefited from good export volumes from the Black Sea; overall improved volumes and increased market share especially in cereals.

• Market Research; Information Services; Process plant monitoring and Supply Chain Services reported excellent growth.

Outlook 2012 • Black Sea exports expected to reduce slightly, partly

offset by solid global demand for all agricultural commodities.

• Demand for Seed and Crop Services drives development in Asia-Pacific & Sub-Saharan Africa.

• Continued investments in US, Canada, South Africa, and India enhance our presence in Food Safety.

• Outlook for agricultural sustainability and precision farming services remains positive.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 173.1 151.8 155.8 Change in % 14.0 11.1

Adj. Operating Inc.(1) 24.9 20.8 21.4 Change in % 19.7 16.4

Margin %1 14.4 13.7 13.7

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

22

MINERALS SERVICES (MIN)

Overview H1 2012 • Total revenue growth of 31.5%, of which 20.6%

organic and margin improvement (CIMM acquisition dilutive to margin).

• Sustained growth across all regions and service portfolio, the key drivers being exploration and metallurgical projects.

• Expansion of the commercial laboratory network including coal labs in Australia and geochemical labs in Liberia and Turkey.

• Key project wins include AGA & Independence Tropicana Gold Mine in Australia and the BHP exploration coal programme in South Africa.

Outlook 2012 • Pipeline in all major laboratories and metallurgical

testing facilities robust for H2. • Financing for junior mining companies difficult due to

the general financial situation. • The major mining companies, whilst reviewing their

investment plans, continue to announce investments in key expansion projects.

• Continued investments planned to handle high sample volumes and meet client demand.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 421.7 320.7 323.2 Change in % 31.5 30.5

Adj. Operating Inc.(1) 77.6 58.8 59.4 Change in % 32.0 30.6

Margin %1 18.4 18.3 18.4

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

23

OIL, GAS & CHEMICALS SERVICES (OGC)

Overview H1 2012 • Strong growth in Upstream Services with contract

wins in Australia, Middle East and sub-surface consultancy in Europe.

• Oil Condition Monitoring expansion in South America and Asia.

• Cargo Treatment Services grew strongly, particularly in the USA and South East Asia.

• Growth in PTO continues, driven by the USA and Europe and the underlying outsourcing trend.

• Margin impacted by changes in business pattern (refinery closures in Europe and the Caribbean) and ramp-up costs in Upstream Services.

Outlook 2012 • Existing business segments with continued growth

(Trade Related, PTO, Oil Condition Monitoring, Upstream, Cargo Treatment Services).

• Major growth from new innovative services wrapped around new proprietary technologies.

• Sustained growth in Upstream Services: • Metering projects in Mid East, Americas, Asia. • Unconventional gas projects. • Expansion of well testing and onsite analysis.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 498.9 446.2 451.0 Change in % 11.8 10.6

Adj. Operating Inc.(1) 60.9 57.7 58.8 Change in % 5.5 3.6

Margin %1 12.2 12.9 13.0

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

24

LIFE SCIENCE SERVICES (LIFE)

Overview H1 2012 • Double-digit organic revenue growth in laboratory

segment offset, as expected, by Clinical Research. • Laboratory growth driven by expansion in Asia and

leveraging state-of-the-art laboratories in Europe and North America.

• Biologics: M-Scan acquisition contributing above expectations and services enriched by the Vitrology acquisition in the UK.

• Very difficult semester for Clinical Research with market volume decline affecting revenue and operating income margins.

Outlook 2012 • Laboratory growth and margins to increase,

supported by global key accounts managers. • Biologics service expansion will continue fully

leveraging new acquisitions and recent investment in centers of excellence (biosimilar, cell-based assay, serology, protein characterisation).

• Clinical Research activity will remain under pressure. Efficiency improvements on-going.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 94.8 96.3 99.5 Change in % (1.6) (4.7)

Adj. Operating Inc.(1) 7.5 10.0 10.3 Change in % (25.0) (27.2)

Margin %1 7.9 10.4 10.4

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

25

CONSUMER TESTING SERVICES (CTS)

Overview H1 2012 • Good revenue growth driven by Western Europe,

South America and all Asia both in traditional and new services.

• Capital investments and personnel development progressing as planned to support 2014 targets.

• All business sectors, and particularly softlines, food and E&E, benefited from improved global economic conditions in H2 last year and during the semester.

• Margin below prior year reflecting a transition period in product mix, investments in new activities and acquisitions not yet fully performing.

Outlook 2012 • Unstable markets but strong order pipeline makes

us optimistic about full year 2012 results. • Strong growth in Europe, despite the crisis; South

America to continue on its solid path; Asia expected to continue on track but with some cost pressure.

• Further investments (E&E, Auto) to meet new technological and regulatory requirements (functional safety, wireless).

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 437.8 387.4 387.5 Change in % 13.0 13.0

Adj. Operating Inc.(1) 98.7 92.7 91.4 Change in % 6.5 8.0

Margin %1 22.5 23.9 23.6

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

26

SYSTEMS & SERVICES CERTIFICATION (SSC)

Overview H1 2012 • Excellent market share gains and double digit

growth in Asia, Eastern Europe, South America and Africa.

• Strong recovery in Japan after last year’s natural disaster.

• Difficult market conditions in Spain and Italy impact both growth in Europe and margin.

• Growing demand for sustainability related audit schemes.

• New mandates ensure compliance of supply chains with environmental, health, safety and social norms.

Outlook 2012 • Expect solid growth across major markets

particularly in Asia, Eastern Europe and the Americas.

• Training activity becomes an important source of growth.

• Further cost optimisation in key affiliates in response to increasingly competitive environment.

• Continued investments to diversify the portfolio of services with new industry bespoke services.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 186.0 175.5 177.4 Change in % 6.0 4.8

Adj. Operating Inc.(1) 31.4 30.6 30.8 Change in % 2.6 1.9

Margin %1 16.9 17.4 17.4

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

27

INDUSTRIAL SERVICES (IND)

Overview H1 2012 • Strong organic growth, especially in Asia, Australasia

and Middle East. • Margin under pressure in Europe, Africa and North

America as investment projects are delayed and public spending reduces.

• Continued restructuring to align organisational structures to the new market conditions in Europe.

• Acquisition of ETSA in Colombia for engineering project supervision and Metlab in South Africa for metallurgical testing; Margins dilutive in H1 due to strong seasonality.

Outlook 2012 • Expect continued growth in revenue and operating

income supported by 5 recent acquisitions. • First revenues in H2 from large inspection service

contracts with oil majors signed last year. • Investing in new testing capabilities in North America. • Increasing exploration activity in Asia & Australasia to

benefit our upstream services. • First revenues in H2 from investments made last year

in organic growth initiatives. Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 422.1 356.4 368.7 Change in % 18.4 14.5

Adj. Operating Inc.(1) 40.3 38.1 39.8 Change in % 5.8 1.3

Margin %1 9.5 10.7 10.8

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

28

ENVIRONMENTAL SERVICES (ENVI)

Overview H1 2012 • Accelerated growth in Africa, Asia and South

America with focus on mining and oil sectors. • European and Canadian operations maintained high

levels of activity thanks to their diversified portfolio of services (lab and non lab).

• Operating income impacted by ongoing investments in new service offerings.

– New laboratories in Congo and Guinea and new environmental studies offices in Paris, Shanghai, Durban, Doha, Kuwait, Dubai, Conakry and Krakow.

• Acquisitions in Brazil (Environ) and USA (Analytical Perspective).

Outlook 2012 • Continued investments in emerging markets to meet

rapidly growing environmental demands. • Diversification of service portfolio to directly serve

end-customers and enhance margins. • Implement a plan to enter new African countries and

serve mining customers with on-site services. • Significant demand for SGS E-data (data

management) services in Australia and Europe.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 151.4 135.7 140.2 Change in % 11.6 8.0

Adj. Operating Inc.(1) 12.1 11.6 12.0 Change in % 4.3 0.8

Margin %1 8.0 8.5 8.6

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

29

AUTOMOTIVE SERVICES (AUTO)

Overview H1 2012 • Statutory business showed solid results in Europe,

the Americas and Africa, with additional stations in Spain, Morocco, South Africa and Ivory Coast.

• Non-statutory activities in the USA still negatively impacted by significantly lower volumes.

• Strong engine testing results in the USA from the ETC acquisition, however vehicle testing remains slightly below expectations.

• Tender secured with the Road Safety Authority in Ireland to develop an IT platform for the control, monitoring and enforcement of commercial vehicles inspections.

Outlook 2012 • Statutory business expected to continue delivering

solid results. • Low commercial inspection volumes likely to remain

throughout 2012 in the USA. • Several opportunities being pursued in the statutory

field in Asia, South America and Africa. • Expand statutory business into Road Safety

Services.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 143.1 132.0 136.6 Change in % 8.4 4.8

Adj. Operating Inc.(1) 31.2 27.3 28.8 Change in % 14.3 8.3

Margin %1 21.8 20.7 21.1

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

30

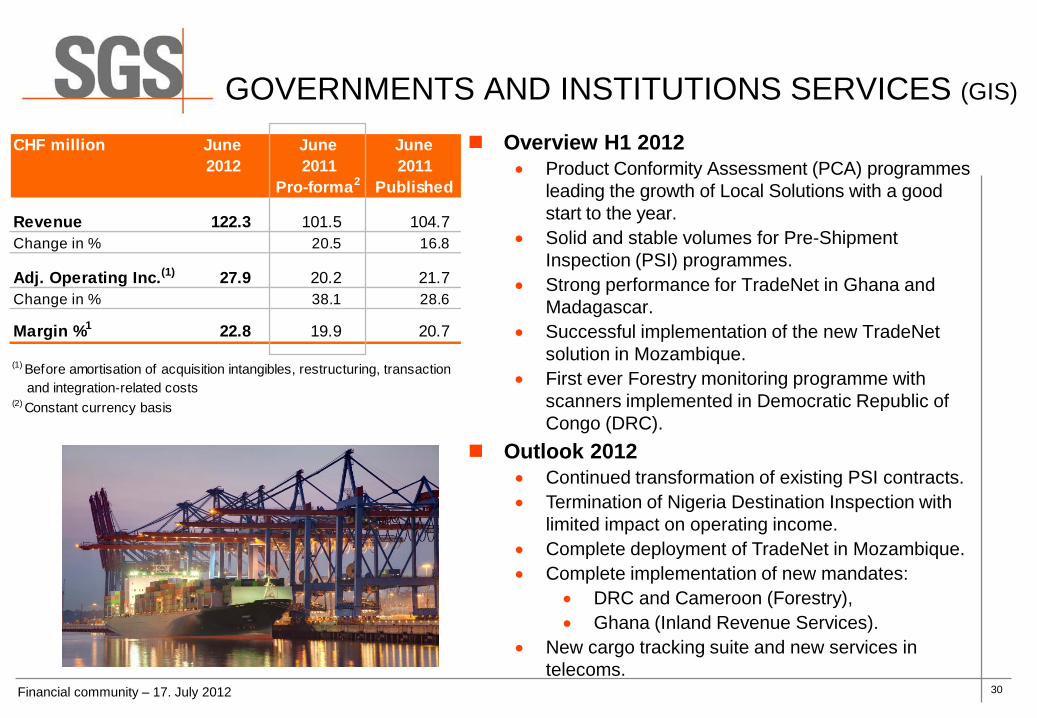

GOVERNMENTS AND INSTITUTIONS SERVICES (GIS)

Overview H1 2012 • Product Conformity Assessment (PCA) programmes

leading the growth of Local Solutions with a good start to the year.

• Solid and stable volumes for Pre-Shipment Inspection (PSI) programmes.

• Strong performance for TradeNet in Ghana and Madagascar.

• Successful implementation of the new TradeNet solution in Mozambique.

• First ever Forestry monitoring programme with scanners implemented in Democratic Republic of Congo (DRC).

Outlook 2012 • Continued transformation of existing PSI contracts. • Termination of Nigeria Destination Inspection with

limited impact on operating income. • Complete deployment of TradeNet in Mozambique. • Complete implementation of new mandates:

• DRC and Cameroon (Forestry), • Ghana (Inland Revenue Services).

• New cargo tracking suite and new services in telecoms.

Financial community – 17. July 2012

CHF million June2012

June2011

June2011

Pro-forma2 Published

Revenue 122.3 101.5 104.7 Change in % 20.5 16.8

Adj. Operating Inc.(1) 27.9 20.2 21.7 Change in % 38.1 28.6

Margin %1 22.8 19.9 20.7

(2) Constant currency basis

(1) Before amortisation of acquisition intangibles, restructuring, transaction and integration-related costs

32

WWW.SGS.COM

© SG

S SA

2012

. ALL

RIG

HTS

RESE

RVED

.

![15.1(1) SWIMMINGPOOLSANDSPAS 15.1(2) · IAC6/3/09 PublicHealth[641] Ch15,p.1 CHAPTER15 SWIMMINGPOOLSANDSPAS 641—15.1(135I)Applicability. 15.1(1) Theserulesapplytoswimmingpools,spas,wadingpools,waterslides](https://static.fdocuments.net/doc/165x107/5f08ea2d7e708231d42456b9/1511-swimmingpoolsandspas-1512-iac6309-publichealth641-ch15p1-chapter15.jpg)