Agricultural Price Transmission Across Space and...

53

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT 1 Agricultural Price Transmission Across Space and Commodities The Case of the 2007-2008 Price Bubble Draft Version – 15th September 2010 Roberto Esposti Department of Economics – Università Politecnica delle Marche Piazzale Martelli 8 – 60121 Ancona (Italy) e-mail: r.esposti at univpm.it; phone: +39 071 2207119 Giulia Listorti : Federal Department of Economics Affairs - Federal Office for Agriculture (FOAG) Mattenhofstrasse 5 – CH-3003 Berne (Switzerland) e-mail: giulia.listorti at blw.admin.ch Abstract This paper analyses the horizontal transmission of cereal price shocks both across different market places and across different commodities. The analysis is carried out using Italian and international weekly spot (cash) price data and concentrating the attention on years 2006-2010, a period of generalized exceptional exuberance and consequent rapid drop of agricultural prices. The work aims at investigating, on the on hand, how price transmission may be affected during price bubbles and, at the same time, how the bubble is transmitted across markets. The properties of price time series are firstly explored in depth to assess which data generation process may have eventually produced the observed patterns. Secondly, the interdependence across prices is specified and estimated adopting appropriate cointegration techniques. Key-words: Price Transmission, Price Bubbles, Time Series Properties, Cointegration JEL Classification: Q110, C320 1. Introduction: objectives and data description The main motivation of this study is to understand the properties of agricultural price series over the 2007-2008 price rally (Ec, 2008; Irwin and Good, 2009) 1 to better analyse how the prices transmitted horizontally, i.e., across market places and commodities, during the bubble and how the bubble itself has been generated and transmitted. This analysis of the horizontal price transmission during price exuberance concerns agricultural weekly spot prices and is limited to the abovementioned four years. We opt for this restriction of the time coverage for three major reasons. First of all, this period fully contains the bubble as the last observed weekly price levels (last week of April 2010) are almost equal to the first observed week (last week of April 2006). Over this period, therefore, the bubble firstly inflated and then completely deflated (Figure 1). Secondly, we can assume an almost-constant policy regime in the EU over this period. In 2006, the 2003 CAP Reform was entirely in force, included its : The views expressed in this article are the sole responsibility of the authors and do not reflect, in any way, the position of the FOAG. Authorship may be attributed as follows: sections 3.2, 3.3, 3.4, 4 and 5 to Listorti; sections 1, 2 and 3.1 to Esposti. 1 Henceforth, the “agricultural price bubble”. Heuristically, and generically, the bubble clearly appear in Figure 1. From a more rigorous point of view, however, we will formally define and test the presence of a bubble in price series in section 2.5.

Transcript of Agricultural Price Transmission Across Space and...

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

1

Agricultural Price Transmission Across Space and Commodities

The Case of the 2007-2008 Price Bubble Draft Version – 15th September 2010

Roberto Esposti

Department of Economics – Università Politecnica delle Marche Piazzale Martelli 8 – 60121 Ancona (Italy)

e-mail: r.esposti at univpm.it; phone: +39 071 2207119

Giulia Listorti♣ Federal Department of Economics Affairs - Federal Office for Agriculture (FOAG)

Mattenhofstrasse 5 – CH-3003 Berne (Switzerland) e-mail: giulia.listorti at blw.admin.ch

Abstract

This paper analyses the horizontal transmission of cereal price shocks both across different market places and across different commodities. The analysis is carried out using Italian and international weekly spot (cash) price data and concentrating the attention on years 2006-2010, a period of generalized exceptional exuberance and consequent rapid drop of agricultural prices. The work aims at investigating, on the on hand, how price transmission may be affected during price bubbles and, at the same time, how the bubble is transmitted across markets. The properties of price time series are firstly explored in depth to assess which data generation process may have eventually produced the observed patterns. Secondly, the interdependence across prices is specified and estimated adopting appropriate cointegration techniques.

Key-words: Price Transmission, Price Bubbles, Time Series Properties, Cointegration JEL Classification: Q110, C320

1. Introduction: objectives and data description

The main motivation of this study is to understand the properties of agricultural price series over the

2007-2008 price rally (Ec, 2008; Irwin and Good, 2009)1 to better analyse how the prices transmitted

horizontally, i.e., across market places and commodities, during the bubble and how the bubble itself

has been generated and transmitted. This analysis of the horizontal price transmission during price

exuberance concerns agricultural weekly spot prices and is limited to the abovementioned four years.

We opt for this restriction of the time coverage for three major reasons. First of all, this period fully

contains the bubble as the last observed weekly price levels (last week of April 2010) are almost equal

to the first observed week (last week of April 2006). Over this period, therefore, the bubble firstly

inflated and then completely deflated (Figure 1). Secondly, we can assume an almost-constant policy

regime in the EU over this period. In 2006, the 2003 CAP Reform was entirely in force, included its

♣ The views expressed in this article are the sole responsibility of the authors and do not reflect, in any way, the position of the FOAG. Authorship may be attributed as follows: sections 3.2, 3.3, 3.4, 4 and 5 to Listorti; sections 1, 2 and 3.1 to Esposti. 1 Henceforth, the “agricultural price bubble”. Heuristically, and generically, the bubble clearly appear in Figure 1. From a more rigorous point of view, however, we will formally define and test the presence of a bubble in price series in section 2.5.

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

2

limited implications in terms of price policy and market intervention; the regime then remained

constant over the whole 2006-2010 period. The only relevant policy regime change over the period

under consideration has been the temporary suspension of EU import duties on cereals from January

2008 to October 2008. This change, in fact, was justified by price movements themselves (the bubble).

Therefore, in investigating price transmission during the bubble it is also possible to assess the role

played by this single policy measure whose application is confined into a limited number of months.

Finally, concentrating on this period facilitates international price comparison as the cumulative

inflation rate has been quite limited and relatively similar in Italy and in North-America (the two areas

under study here). Therefore, comparison of agricultural prices across different countries does not

require the deflation of nominal prices into a common real base.

The dataset here adopted is made of cereal weekly spot price series observed in different Italian

locations (from North to South) (source: ISMEA) and in international (North-American) markets

(source: International Grain Council, IGC). Commodities under consideration are soft wheat, durum

wheat, barley and corn (with soft and durum wheat possibly distinguished in different quality grades).

Therefore the dataset dimensions are: T = 210 weeks (from last week of April 2006 to last week of

April 2010); K commodities; N market places, that is North-Italy (Milan), Centre-North Italy

(Bologna), Centre-South Italy (Rome), South-Italy (Catania, Foggia, Naples), US and Canada (or

Rotterdam; see below). In practice, the dataset has a Tx(NxK) size. Table A1 (Appendix) details the

NxK = 28 price series under investigation and their respective acronyms.

To facilitate comparisons and analysis of transmission, international and national prices have to be

expressed in a common currency. Therefore, US and Canadian prices have been converted from US

dollars to Euros by taking the weekly official $/€ exchange rate provided by Eurostat-ECB.2 These

North-American prices actually are FOB prices. For agricultural commodities, the ratio of freight rates

on FOB prices is quite high and it also considerably oscillated during the commodity price bubble

(especially due to volatility in energy, namely oil, prices). According to this, freight rates (source:

IGC) were added to US and Canadian prices in order to obtain the respective CIF prices. The freight

rates used in this study are those from US Gulf (or Canada, where applicable) to ARAH (i.e,

Amsterdam/Rotterdam/Antwerp/Hamburg destinations). In practice, in our analysis the North-

American prices actually serve as international price taken at Rotterdam, thus as EU-reference prices.

Henceforth, we will refer to international prices as Rotterdam prices (see Table A.1).

Figure 1 reports the 28 price series over the period under investigation here. Simple inspection clearly

reveals the price bubble and that the price exuberance concerned almost all markets but with a

remarkable different intensity. A proper empirical analysis of price transmission over this period,

therefore, requires two steps. First of all, the time-series properties of these agricultural prices have to

be carefully investigated to understand which process can have eventually generated the explosive

2 It implies that adjustments to the exchange rate are considered instantaneous.

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

3

pattern and the consequent drop, and for which prices we can look for a common behaviour and,

therefore, for interdependence (section 2). Then, such interdependence across markets (commodities

and places) is specified (section 3) and estimated (section 4) within a proper cointegration framework.

Section 5 concludes.

2. Some basic evidence on agricultural price behaviour

High frequency (daily or weekly) agricultural price series combine the properties of lower-frequency

(monthly or annual) agricultural price series with the typical properties of financial series (Wei and

Leuthold, 1998). In short, agricultural price series often maintain characteristics that are naturally

attributed to agricultural products and markets (Wright, 2001), namely, seasonality and long memory

(i.e, high persistence of shocks over time, but no evident short-run cycles) and, sometimes, even

chaotic behaviour in the longer run (Wei and Leuthold, 1998). At the same time, other features,

usually attributed to the specific nature of financial markets, may be detected as well: changing

volatility (i.e., changing price variance), non-stationarity (i.e., prices following random walk

behaviour) and temporary (and even periodic) exuberance or explosive behaviour (the bubbles).

The combination of these properties may generate very peculiar patterns and, in particular, nonlinear

dynamics. In practice, they can be often hardly distinguishable and separated especially whenever they

partially overlap. As these features may characterize most agricultural commodities and markets, they

also make the identification of market interdependence (i.e., how they affect each other) particularly

difficult as a given price movement can be attributed to either own price dynamics or to response to

other markets’ variations. This is even more true over period of price bubbles, that is, of strongly

nonlinear dynamics with rapid (and apparently unexpected) price increase soon followed by a period

of as much intense price drop. More specifically, during such periods of exuberance, the identification

issues becomes whether the typical abovementioned behaviour of high-frequency agricultural price

series experiences a structural change or, on the contrary, bubbles are nothing but “normal” outcomes

of the interactions among these typical characters.

Therefore, before entering the analysis of how market prices interact, thus reciprocally transmitting

price shocks, it seems rational to firstly assess the time series properties of the prices under study. This

analysis not only allows identifying those prices showing common features but it is also needed to

achieve a proper specification of price transmission/interdependence relations.

Let consider agricultural prices observed over these three different dimensions: space, commodity and

time. The generic price is, therefore, tkip ,, where i=1,…,j,…,N is the (local) market (spatial

dimension); k=1,…,h,…,K is the commodity; t=1,…,s,…,T is the period of observation (time

dimension). By more conventionally distinguishing between a cross-sectional dimension, given by the

combination of the dimensions ik, and a time dimension t, we can identify any generic price

observation as tikp , (scalar) and any generic price series (vector) as ikp . Through a sequence of

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

4

testing procedures, this section aims at detecting the abovementioned properties of time series ikp .

Both price levels ( ikp ) and logarithmic transformations (iklp ) are considered and in both cases, if

needed, tests are repeated on the respective first-order differences ( ikp∆1 and iklp∆1 ) to observe

whether the abovementioned features remain or vanish after differentiation.

The analysis of price patterns, and of their nonlinear dynamics, is performed by testing, in sequence,

their distributional properties (normality), seasonality, volatility (ARCH effects), stationarity,

persistence (long memory or fractional integration) and explosiveness. All these features may be

responsible for nonlinear dynamics and, therefore, may be invoked as possible causes of the observed

exuberance. At the same time, they also imply different stochastic processes and price

interdependence.

2.1. Normality, seasonality and structure of autocorrelation

Some of the typical properties of high-frequency agricultural price series may imply nonlinear

dynamics that, in turn, induces non normal unconditional distributions usually showing strong

skewness and fat tails (Wei and Leuthold, 1998). Therefore, testing for unconditional normality of

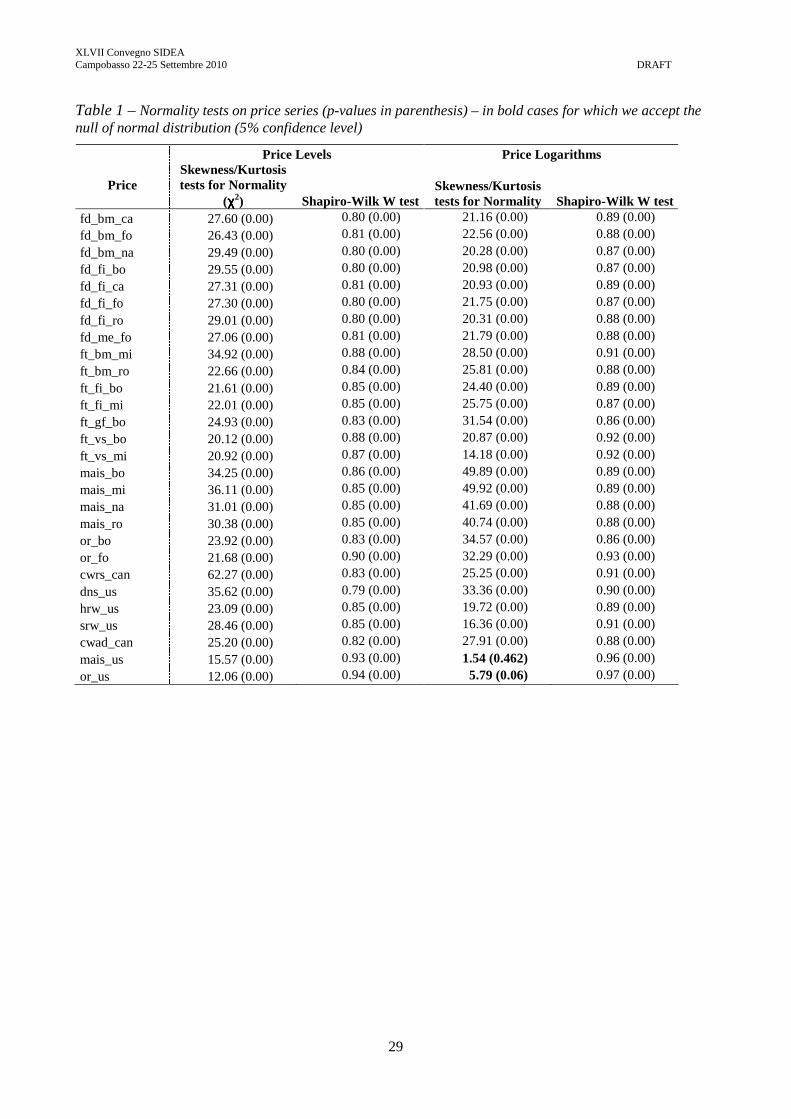

price series is a basic and simple way to detect the presence of such nonlinearities. Table 1 reports

normality tests on price series (in both levels and logarithms) suggesting that in all cases we can reject

the hypothesis of underlying normal unconditional distribution. Test also confirm the presence of

skewness and fat tails as could be easily expected over a period of price exuberance and rapid drop

(the bubble).

A period of relatively long exuberance not only affect the distributional properties of agricultural price

series, but also influences another of their typical characters, namely, the presence of short-run (within

year) cycles or recurrence. Previous studies on similar markets and data frequency (weekly or even

monthly prices) (Verga and Zuppiroli, 2003, and Listorti, 2007, 2009, respectively) show that cereal

markets are often characterised by a significant seasonality. The presence of these seasonal (or other

short-run) cycles is not surprising considering that, especially in national markets, production is

concentrated in a specific part (just few weeks) of the year while prevalent uses are homogeneously

distributed over the year. This inevitably generates, even for highly storable commodities like cereals,

a cyclical seasonal behaviour of prices. Seasonality in series ikp would imply that an observation at a

given time t, tikp , , shows a significant partial autocorrelation not only with closer observations

( 1, −tikp , 2, −tikp , etc.) but also with observations far-away in time, stikp −, , with s usually taking values

close to 45-50 expressing the seasonal recurrence.

Table 2 reports selected results emerging from the estimation of the Partial AutoCorrelogram (PAC) of

prices under study. Series behaviour is pretty similar across all prices. In all cases, partial

autocorrelation coefficients are significant within few lags (2 or 3 in most cases) and particularly high

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

5

(close to 1) for lag t-1, but no clear short-run (within year) cycles comes out, though in few cases we

can observe significant partial correlation coefficients for lags between 45 and 50 weeks. Therefore,

seasonal recurrence does neither clearly nor homogeneously emerge and, when and if present (mostly

in international prices), only weakly influences the price pattern over the period. This conclusion is

also easily detectable by taking, for any week, the average price over observed years. Figure 2 displays

these 52 average prices for the whole period and for the two sub-periods (April 2006- April 2008;

April 2008-2010), that is, for the ascending and the descending parts of the price bubble. Price

averages does not significantly change over the year. No sharp drop or rise is observed in

correspondence to seasonal recurrences.

This evidence is at odds with previous results on weekly data of national and international cereal

markets (Verga and Zuppiroli, 2003) but should not surprise for two basic reasons. First of all, the

period under consideration covers just four years, thus four possible seasonal recurrences. Even from a

strictly statistical point of view, seasonal patterns can be hardly detected with such limited number of

events. A secondly, and more important, reason is that the bubble itself, and the nonlinearities

associated to this, may hide a slight seasonality. This is illustrated in the lower part of Figure 2. In the

two sub-periods, average prices actually change over the year and, in particular, regularly increases in

the first two years and then regularly declines in the second sub-period. No clear discontinuity is

observed. This is perfectly consistent with the formation of the bubble and has almost nothing to do

with real seasonal patterns.

Therefore, considering the limited number of years under investigation and that, even when present, it

only marginally affects the observed price patterns, seasonality will be ignored henceforth.3

2.2. Stationarity

Regardless the presence of seasonal or other short-term cycles, what really matters in understanding

the behaviour of price series especially in a period of such dramatic exuberance and drop, is the

presence of unit and/or explosive roots. Stationary (i.e. I(0)) series can be hardly reconciled with the

formation of the bubble. Even stationarity around a drift (a constant term) and/or a deterministic trend

is not evidently helpful in this respect. Figure 1 shows, in particular, how the presence of a

deterministic trend can be easily excluded by a simple visual inspection of the series themselves. As

will be clarified below, testing for the presence of a temporary explosive pattern can not be simply

achieved through conventional unit-root tests. Nonetheless, albeit not sufficient, these latter tests still

3 The exception are unit-root tests (Table 3) in which we still include seasonal dummies as their exclusion, in those cases where they are significant, may affect test validity. In general terms, though not presented here (they are available upon requests), all tests and estimates reported in the present paper have been also obtained by introducing seasonal dummies. This additional evidence suggests that all results are robust with respect to seasonality: the coefficients associated to dummies are always hardly significant and, in any case, results do not change significantly.

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

6

allow assessing a necessary outcome of nonlinearities within price series: series turn out to be I(1) and

not I(0) (Diba and Grossman, 1988; Evans, 1991; Phillips and Magdalinos, 2009; Philips et al., 2009;

Phillips and Yu, 2009; Gutierrez, 2010).

Table 3 thus reports unit root tests on ikp , iklp , ikp∆1 and iklp∆1 . Two different tests are run, the

ADF and the PP tests (Enders, 1995), as the latter is expected to be more robust under

heteroskedasticity which may, in fact, occur (see below the test on ARCH effects). In general terms, it

looks like that, once the proper specification has been selected (in terms of admitted lags and of

presence of drift and deterministic trend), all ikp and iklp

series show a unit root. On the contrary, all

ikp∆1 and iklp∆1

series are stationary. The conclusion would be that all price series can be

considered I(1) but not I(2).

I(1) series (random walks possibly with a drift and/or a deterministic trend), however, are apparently

at odds with the evidence of a price bubble, as they can hardly generate temporary explosive

behaviour. More generally, it remains to explain how such I(1) ikp series may have eventually

generated the observed price pattern in all markets (Figure 1). Three possible explanations can be

considered in this respect. The first is that I(1) series generate the observed pattern due to a sudden and

temporary increase in volatility, namely, of price variance. The second explanation is that ikp∆1 and

iklp∆1 are, in fact, neither I(0) nor I(1) series (therefore ikp is neither I(1) nor I(2)). They could rather

show fractional integration (or long-memory), that would make sudden exogenous price shocks

persistent over long time (i.e, many weeks). A final explanation is that, as conventional unit-root tests

can not really assess (or exclude) the presence of temporary explosive roots (the bubble), more

appropriate ad hoc tests should be adopted.

2.3. Increasing volatility

One possible reconciliation of I(1) series with nonlinearities implied by bubbles can be found in the

presence of ARCH effects (Hamilton, 1994; Enders, 1995). The observed behaviour of price series

could be attributed to I(1) series showing a dramatic increase in volatility during the bubble. ARCH

theory admits the nonormality of the unconditional distribution of the data emerging in Table 1 (Wei

and Leuthold, 1998, p. 15) and the presence of ARCH effects does not prevent the use of ADF test to

assess nonstationarity. Therefore, series could be correctly assumed I(1) still in the presence of ARCH

effects. One way to assess the hypothesis that series ikp ( iklp ) originate from a combination of

random walk and autoregressive conditional heteroskedasticity consists in testing the presence of such

ARCH effects in ADF regressions (Table 3).

For the generic price tikp , , the ADF regression, possibly with drift ikµ and deterministic trend t, is

specified as usual:

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

7

(1) tikik

S

sstikistikikiktik etppp ,

21,1,, ++∆++=∆ ∑

=+−− βπρµ

where 0=ikρ under the null of unit-root process, while it is expected to be <0 for stationary process

and >0 under explosive roots. If an ARCH is admitted, however, the distribution of usual error term

tike , instead of being assumed i.i.d N(0,σ2), behaves according to an ARCH(m) process:

(2) tike , ∼ N(0, hik) where ∑=

−+=m

sstiksik eh

1

2,0 θθ with mss ,...,10,00 =∀≥> θθ

Testing for the presence of an ARCH effect thus means to perform an LM test on this heteroskedastic

structure of the error term. Table 4 reports these ARCH tests on ADF regressions for both ikp and

iklp . Results are mixed but, particularly in the logarithmic transformation, there is a clear prevalence

of series for which the ARCH effect can be rejected. In practice, only for corn and for international

prices we observe a generalised evidence of an ARCH effect. For all other series, changing volatility

in I(1) series does not provide, in any case, an explanation of the observed behaviour of prices over the

period. On the contrary, in principle, in those series for which ARCH effects are present, the

combination of I(1) series with varying volatility may remains a plausible justification. Nonetheless,

though to a different extent, the price exuberance and fall during years 2007-2008 is generalised across

almost all cereal markets under investigations here. It clearly emerge also for prices for which an

ARCH effect is excluded (durum wheat, for instance, shows the largest bubble among all cereals). We

could admit that exuberance was originally generated in markets with the ARCH effects and then

transmitted to other markets. It is not clear, however, why such transmission did not imply even the

change in volatility.

Analysing this latter aspect goes beyond the scopes of the present analysis. Benavides (2004) provides

an example of a Multiple GARCH approach to agricultural commodity markets to analyse price

interdependence even in terms of changing volatility. It must be noted, however, that such kind of

analysis, is much more frequent and suitable for higher-frequency price series whose patterns (and

underlying mechanisms) are very close to purely financial markets. This is clearly the case of future

prices of agricultural commodities (see Wei and Leuthold, 1998; future prices rather spot prices are, in

fact, investigated by Benavides, 2004) while it seems less suited for monthly or weekly agricultural

spot prices under study here.

2.4. Long memory (fractional integration)

As emphasized by Wei and Leuthold (1998), agricultural prices (and, in particular, future prices) are

often characterised by long memory that may also generate non-linear patterns quite close to chaotic

processes. In such cases, strictly speaking, price series are neither I(0) nor I(1) as they are rather I(d)

processes, with 0<d<1 (fractional integration). Conventional unit-root tests may fail in assessing

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

8

whether price series are I(0) or I(1) while, in fact, they are I(d) The presence of fractional integration

thus may be not excluded in allegedly I(0) series with long persistence of shocks. Originally proposed

by Granger and Joyeux (1980), the idea of fractional integration implies that, though not behaving as

random walk (where shocks never vanish over time), price series keep the memory of a given shock

for a long period. Roughly speaking, the importance of market information (price shocks) does not

decay (or very slowly decay) over time.

This kind of stochastic process assumes specific interest here as it may be consistent with evident

nonlinearities and time-varying variances within price series. In particular, I(1) price series with or

without ARCH effects can generate the nonlinearities observed during the bubble when fractional

integration occurs in the first differences. In such case, though an unit root in first-differenced series

can not be detected, a long-memory process would still imply strong persistence of momentary shocks.

The presence of such long memory within the price series can be tested following the approach

originally proposed by Geweke and Porter-Hudak (1983) and then modified by Phillips (1999a,b).

Such test is based on a particular representation of the stochastic process generating the generic price

series ikp or its first differences ikp1∆ . This representation is called ARFIMA(p,d,q) (Autoregressive

Fractionally Integrated Moving Average) model. In the case of ikp1∆ the AFIMA(p,d,q) model is

specified as follows:

(3) ( ) tik

q

s

sstik

dp

s

ss LpLL ,

1,

1

111 εθα

−=∆−

− ∑∑

==

where L is the usual lag operator. αs are the parameters of the autoregressive part of the model, θs the

parameters of the moving average part. tik ,ε is a conventional normally distributed spherical

disturbance. If a series exhibits long memory, it is neither a I(0) nor a I(1) process; it is an I(d) process.

By testing for the value of parameter d, the test proposed by Phillips (1999a,b), and here adopted, can

distinguish among stationary, unit-root and fractionally integrated processes. The procedure produces

two test statistics, one for the null d=0 and one for d=1. If d=0 is accepted the series is stationary; if

d=1 is accepted the series has an unit root. If both are rejected (namely, if 0<d<1), then fractional

integration (long memory) is accepted.

Results of these tests are reported in Table 5. Test results confirm that, when applied to original series,

unit root is evidently observed. When applied to first differences (either in the levels or in the

logarithmic transformations), the presence of unit root is always rejected but in few cases (and in all

international prices) the presence of fractional integration cannot be excluded. This would suggest

that, although no evidence emerge in favour of ikp (or iklp ) as I(2) series, at least some prices are

“something more” than I(1) series as their first differences show long memory, therefore long

persistence of shocks. Long-memory (fractionally integrated) processes are expected to show

relatively low but constant and long-lasting autocorrelations (Wei and Leuthold, 1998, p. 14). If

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

9

observed in the first difference ( ikp∆1 ), this property may generate the temporarily non-linear pattern

observed in the recent years in cereal markets. Once more, however, as the support to such behaviour

is not generalized (that is, is only observed in few prices), it remains hard to explain why, on the

contrary, the exuberance is, in fact, generalized across the markets. Even assuming that shocks are

transmitted across markets, the long memory character should itself be transmitted to all markets.4

2.5. Testing explosiveness: recursive unit root tests

The analysis carried out so far attempted to identify those possible common stochastic processes that

may have generated the price patterns observed in the recent years. Although, given test results, we

may be confident on the fact that ikp (or iklp ) behave as I(1) processes. It is also clear that there must

be “something more” beyond unit roots in price series to explain the exuberance and rapid drop (thus

temporary nonlinear dynamics) recorded during the so-called price bubble. Possible explanations

(ARCH effects in price levels of long memory in price first differences) may provide a possible

explanation only in some cases while, in fact, the temporary nonlinear dynamics we are trying to

explain is generalized across all observed cereal markets.

A final and, in fact, more intuitive explanation could simply be that the observed dynamics is

generated by unit root processes in which an explosive root temporarily overlaps. A more formal and

rigorous definition of a temporary (or periodically collapsing) bubble in price or financial series

consists in the presence of temporary explosive roots. Such temporary explosive patterns present a

problem to standard time series analysis. In time-series econometrics, non-stationary variables are

usually assumed to be either first-order integrated, I(1), or second-order integrated, I(2), or perhaps

fractionally integrated processes (Engsted, 2006). Nonlinear patterns, in fact, could more naturally

emerge from I(2) processes. Nonetheless, a price series showing a period of explosive behaviour (a

temporary bubble) is not necessarily an I(2) series. On the contrary, a I(2) process would imply a

permanent exuberance of prices while, in fact, the observed bubble inflates and deflates within a

relatively limited period of time.

Bubbles induce a temporary explosive root in price series in addition to a unit root. The problem, once

more, is that price series containing a temporary exuberance do behave neither as I(1) processes nor as

I(2) processes and, therefore, if this additional root is not appropriately considered, conventional

testing may fail in detecting the real underlying stochastic process (Evans, 1991).

Recent works by Phillips and Magdalinos (2009), Philips et al. (2009) and Phillips and Yu, 2009 (see

also Gutierrez, 2010) have provided an appropriate framework for assessing the presence of an

explosive root (a bubble) within processes that would be otherwise ruled as I(1). They propose a test

4 As for the ARCH effect, even the presence of long memory in agricultural price series is more often mentioned in the case of future prices rather than spot prices (Wei and Leuthold, 1998).

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

10

for the presence of bubbles where forward recursive ADF tests are run on the price series. These

sequential tests allow assessing period-by-period the possible nonstationarity of the price series against

an explosive alternative. The forward recursive test is based on a conventional ADF regression like (1)

where in the first recursion only To = [ ro T] observations are used, and ro is a fraction of the total

sample T.5 In subsequent regressions the originating data set is supplemented by successive

observations any time giving a sample of size Tr = [nr] for ro ≤ r ≤ 1.

For any recursive sub-sample Tr , the respective ADF test is computed. Of these forward recursive

ADF tests (ADFr), the test of explosiveness consider the maximum observed value:

[ ]r

rr

ADFsupSADF1,0∈

= . Under the null hypothesis of unit root (H0: ikρ =1) and against the right-tailed

alternative hypothesis of presence of explosive root (H1: ikρ >1), if the estimated test SADF is higher

than the respective critical values, we accept that the series contains an explosive root. Critical values

are reported in Phillips et al. (2009). Here, ro has been alternatively fixed at 0.10 (21 observations) at

0.20 (42 observations) (see Phillips et al, 2009, and Phillips and Yu, 2009) and then incremented by

each single following observation. The SADF tests have been repeated on price series, including the

constant term and with 12 lags and then compared with the critical values provided, for different

sample sizes, in Phillips et al. (2009) and Phillips and Yu (2009). Tests are only performed on iklp .

While in all previous tests ikp and iklp

provided a similar information, in this case the presence of

explosiveness ma have a different implication if ikp rather than iklp

is considered. While we can

exclude an explosive root in iklp if rejected in ikp , it might be the case that non-explosive iklp still

admits explosiveness in ikp (Waters, 2008, p. 280). Therefore, as iklp will be considered in the

following analysis, the presence of explosiveness (therefore of bubble) will be henceforth refereed to

iklp .

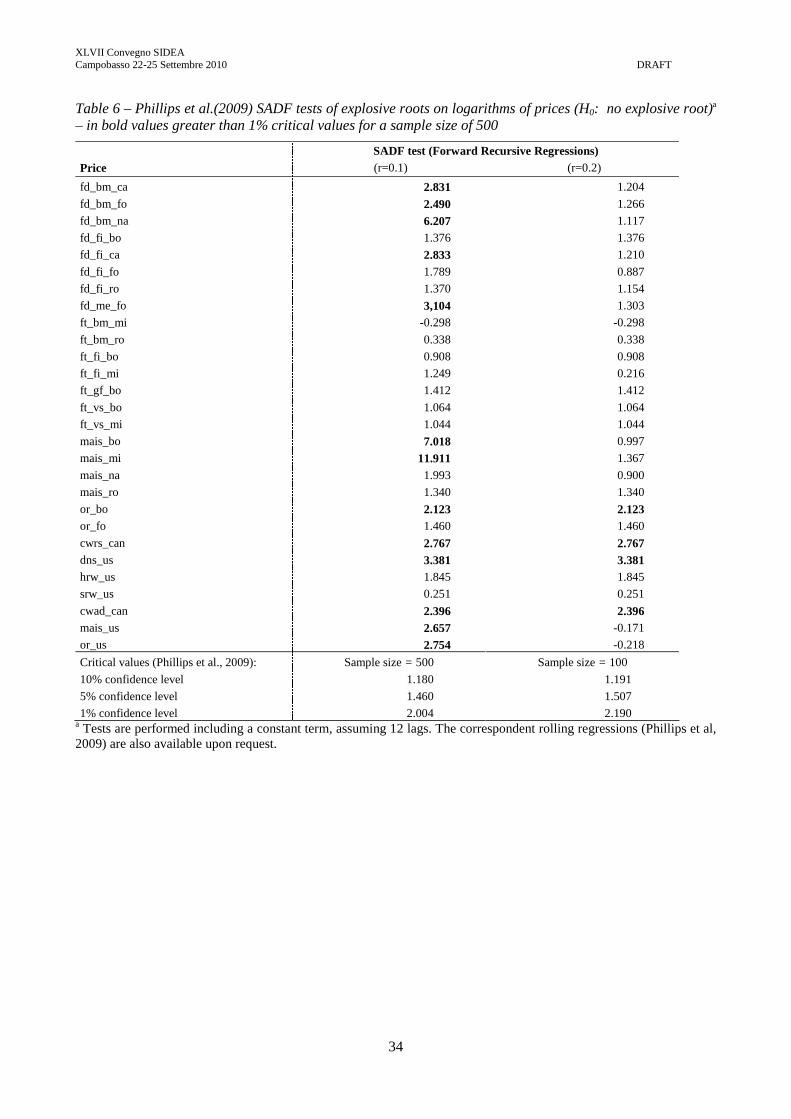

Table 6 reports results of these SADF tests. Results are reported for both r=0.10 and r=0.20. The latter

case, however, provides more robust evidence because it uses larger sub-samples thus reducing the

risk of poor test performance in the first runs of the recursive process. Moreover, a restrictive 1%

critical value is used to test the presence of explosive roots. On this basis, we can definitely conclude

that a temporary explosive behaviour is actually found in durum and soft wheat international

(Rotterdam) prices. Among national prices the bubble is found only in the barley price of the Bologna

market. The presence of a an explosive root is doubtful in few cases, while it can be excluded in most

of the other price series.

Although this kind of test may be not conclusive with respect to the presence of explosive roots, the

underlying approach is particularly helpful in understanding the timing of price exuberance and,

5 The square brackets in [ro T] indicates that the integer part of the argument is taken.

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

11

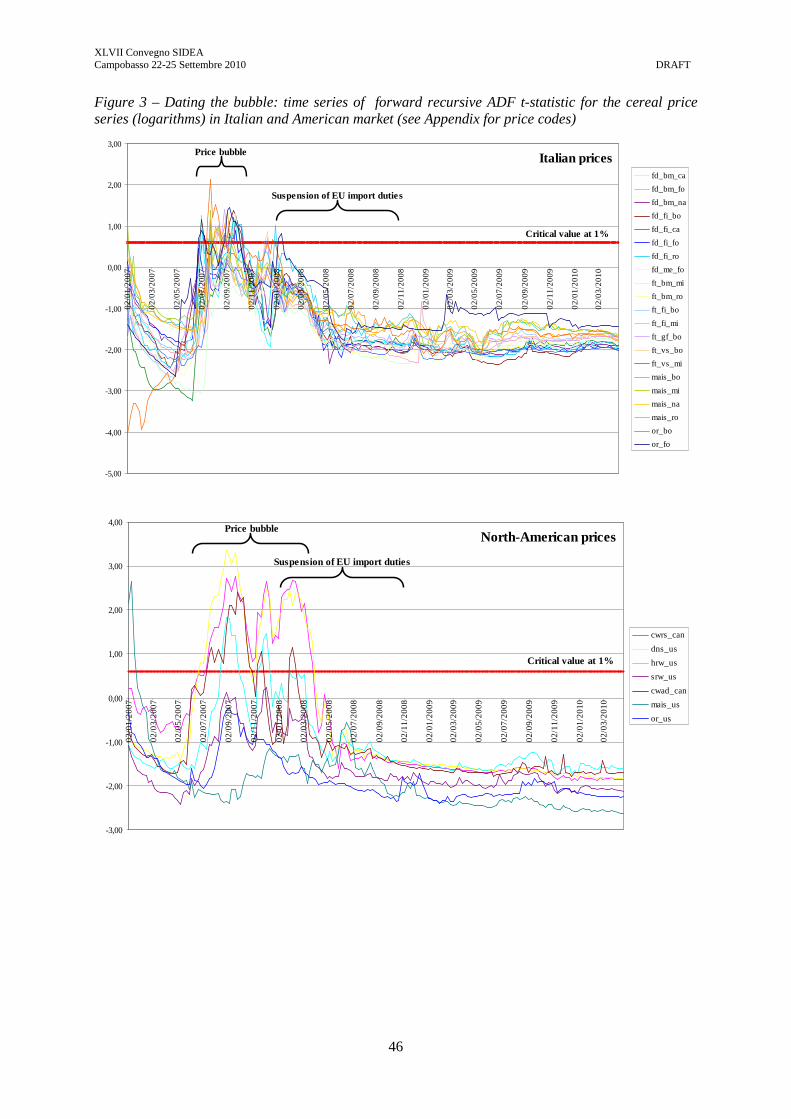

therefore, to eventually date the beginning and the end of the price bubble. To locate the origin and the

conclusion of the exuberance, one can display the series of the abovementioned forward recursive

ADFr test and check if, when and how long ADFr exceeds the right-tailed critical values of the

asymptotic distribution of the standard Dickey–Fuller t-statistic (Phillips et al. 2009). Still adopting a

restrictive 1% critical value, Figure 3 reports this evidence and clearly shows that the price bubble in

national markets is limited to very few cases and lasts for a very short period not overlapping with the

period of suspension of the EU import duties on cereals. In international markets, the price bubble

involves more commodities and its duration is much longer clearly overlapping with the period of

suspension of the EU import duties on cereals.

According to these results, and following restrictive criteria as explosiveness may be easily confused

with different processes generating similar patterns (as in the case of possible fraction integration of

iklp∆1 for international prices), we will henceforth consider that only prices l_or_bo, l_cwad_can,

l_cwrs_can and l_dns_us (see Table A1; l_ indicates that they are logarithms) clearly contain an

explosive root. Of these, however, l_cwrs_can and l_dns_us will be not used in the following analysis

(see Table A.2). The period of the bubble is assumed to start in the first week of July 2007 and finish

in the last week of March 2008. In all other price series, the observed nonlinear dynamics should be

attributed to the other kinds of stochastic processes that have been tested in this section (or to a

combination of them).

[Table 6 here]

[Figure 3 here]

3. Modelling price interdependence as price transmission mechanisms

In the previous section, a large number of different cereal price series have been investigated at the

research of a stochastic process that may have generated their relatively homogenous behaviour over

the last years. Some evidence emerged in favour of the presence of “something more” than a simple

I(1) process, but this evidence is not concordant across all prices. The paradox, therefore, is that

although cereal prices clearly moved together, despite differences, over time (see Figure 1), the price-

by-price analysis performed so far did not find any clear common feature for ikp (or iklp ) except the

fact that they all seems to be I(1) series.

One possible way to deal with this apparent paradox, however, is to directly look for linkage

(interdependence) across prices rather than examining their individual properties then looking for

some common properties. After all, beyond visual inspection, there is very clear evidence of a strong

interdependence across markets of both different commodities (same place) and difference places

(same commodity). Table 7 reports the (NKxNK) correlation matrix across prices (ikp ). Price

correlation is evidently high not only within the same commodity but also across different

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

12

commodities in the same market place. This is not in any conclusive as this strong correlation among

I(1) series can be, in fact, spurious. Nonetheless, a generalized correlation across prices is confirmed

by the fact that the error terms of the ADF regressions (1) themselves show a very strong cross-

sectional correlation. Performing the Pesaran (2004) test for cross-sectional correlation (CD test; H0:

no cross-sectional correlation) on error terms of the ADF equations of Table 3, we obtain the

following results: 45,98 and 47,56 (with the constant term), 46,07 and 47,99 (without the constant

term) for ikp and iklp , respectively. All these test values are largely statistical significant at the 1%

confidence level.

More generally, there is a diffuse evidence of a strong linkage across price series. Asking whether this

linkage is just a spurious evidence or can be interpreted as a real interdependence across cereal

markets in both the space and commodity dimensions, inevitably leads to specify which form this

interdependence is expected to take and, then, to test and estimate it.

3.1. A general model of price transmission

Let us consider the generic agricultural price tkip ,, . The behaviour of tkip ,, over its three dimensions

might be evidently represented within appropriate structural models as the combination of market

fundamentals such as supply, demand and stock formation. But such models are inherently very

complex and hardly tractable in the empirical analysis, whereas the analysis of price evolution and

linkage is more frequently afforded within reduced-form model. For example, Fackler and Goodwin

(2001) provide a common template embracing all dynamic regression models, based on linear excess

demand functions, from which an estimable reduced-form model (in their case, a VAR in prices) can

be eventually derived within this framework. Reduced-form models are actually and by far more

feasible and of immediate use to generate price predictions on the basis of the available observations

and when the three dimensions are explicitly considered, i.e., to estimate

( )stkisthistkjtki ppppE −−− ,,,,,,,, ,, .

A generic reduced-form model of price formation and transmission over the three dimensions can be

represented as follows:

(4a) tki

TSs

ssthjkh

skh

TSs

sstkjij

sij

TSs

sstkiskitki pppp ,,

0,,

0,,

1,,,,, εϖωρα ++++= ∑∑∑∑∑

<=

=−≠

<=

=−≠

<=

=−

where tki ,,ε ∼ ( )2,,,0 tkiN σ . Equation (4a) can be rewritten, as mentioned, in a more conventional form

by distinguishing a cross-sectional dimension (given by the combination of the dimensions ik) and a

time dimension, t. Therefore, we are interested in a reduced-form model predicting the expected value

of the generic price ( )stikstjhtik pppE −− ,,, , and (4a) becomes:

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

13

(4b) tik

TSs

sstjhikjh

sjhik

TSs

sstiksiktik ppp ,

0,,

1,, εωρα +++= ∑∑∑

<=

=−≠

<=

=−

where tik ,ε ∼ ( )2,,0 tikN σ . Equation (4b) can be written in a more compact matrix form:

(4c) t

TSs

sss εWPαP ++= ∑

<=

=0

where P , sP and tε are (Tx(NxK)) matrices, s expresses the time lag, α is a (Tx(NxK)) matrix of

time invariant parameters, that is, sjiααα ikstiktik ,,,,, ∀== − (any column of α contains T elements

with constant value ikα ) and tε ∼ ( )tN Ω0, . sW is a ((NxK)x(NxK)) matrix of unknown parameters

incorporating the correlation across prices within both the time and space-commodity dimensions. The

diagonal elements, sikik ,ω , actually represent the auto-correlation over time, with the exclusion of the

matrix 0W , where diagonal elements are evidently ikikik ∀= ,00,ω . The off-diagonal elements, s jhik ,ω ,

represent the cross-sectional dependence of prices; in other words, they express the degree of common

movement shown by different prices and, therefore, the degree and the direction at which price shocks

are transmitted.6

In particular:

- if h=k but i≠j, we are considering the spatial price transmission for the same commodity across

different market places. In this case, under perfect spatial arbitrage, the Law of One Price (LOP)

holds and we may expect jkik ,ω =1 ;

- if i=j but h≠k, we are considering the price transmission between different commodities in the

same market. In this case, elements ihik ,ω indicate the degree of substitutability between the

different goods (Dawson et al., 2006). ihik ,ω will be close to 1 under perfect substitutability

between h and k, while it will be close to 0 under low substitutability.

If model (4a-c) is specified in tlP (the matrix of price logarithms), elements of sW indicate the price

transmission elasticities that is, how much of a percentage variation in stikp −, is transmitted to tjhp , .

Within logarithmic form, the implicit assumption is that all factors possibly contributing to price

differentials but not explicitly taken into account in the model (for example, transportation and

transaction costs) are a constant proportion of prices. Elements of α indicate these constant

multiplicative terms (that can be naturally intended as percentages) applied to price stikp −, to obtain

tjhp , .

6 See Fackler and Goodwin (2001), for a comprehensive description. Indeed, the study of price transmission mechanisms implies referring to a number of economic concepts for which no common definitions exist in literature.

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

14

If matrix of unknown parameters, sW , contains all information about price linkages over the three

dimensions, we can expect that (4a-c) gets rid of autocorrelation and heteroskedasticity across both the

time and cross-sectional dimensions, that is, it restores spherical error terms: tε ∼ ( )I0 σ,N and

( ) 0, =−sttE εε . The proper specification of (4a-c), therefore, should aim at restoring such conditions.

3.2. Model specification

The first specification issue concerning model (4a-c) has to do with its size. With 28 price series, the

size of sW becomes particularly large especially whenever several lags (due to weekly data) had to be

admitted. To reduce the size of the problem (and the number of parameters to be estimated),

assumption can be made about the relevant interactions to be considered. Therefore, also to facilitate

the economic interpretation of the results, the analysis of the price interdependence have to be

“confined” and “segmented”. In particular, we may firstly assume that price transmission only occurs

within the same commodity (that is, ikp and jkp are interdependent) and within the same market

place (that is, ikp and ihp are interdependent). The consequent assumption is that ikp and jhp have

no direct linkage. This implies fixing at 0 some of the elements of the 0W matrix. Secondly, the

relation across prices can be separately studied by group of commodities segmenting the analysis

within the fixed-commodity/cross-space(market) dimension ( ikp , jkp ) from the analysis within the

fixed-space(market)/cross-commodity dimension (ikp , ihp ). Table A.2 in the Appendix details the

groups of prices whose interdependence has been considered.7

The conclusion achieved in the testing section, that all series iklp can be considered I(1) processes

with some of them also showing a temporary bubble, must be appropriately taken into account when

developing, specifying and estimating model (4a-c). Actually, agricultural commodity price series are

often found to be I(1); for this reason, since the seminal work of Ardeni (1989), cointegration

techniques have been extensively used for the study of price transmission mechanisms. Cointegration

models presuppose that variables exhibiting nonstationary behaviour will nonetheless be linked by a

long run relation, whose residuals are stationary. When fixed-commodity and cross-market price

relations are considered, under perfect spatial arbitrage, this relation is the LOP, which is expected to

hold in the long-run (LR) despite in short-run (SR) prices are allowed to deviate from it.

In the cointegration context, it is possible to take care of both issues raised by the presence of the

bubble. On the one hand, separating the LR and SR price interdependence allows identifying what

links prices outside and beyond the bubble from the temporary linkages caused by the bubble. On the

7 Some of the 28 price series here available (see Table A.1) are not used in the empirical analysis as they are highly redundant (in particular prices of different qualities of soft and durum wheat are almost coincident)

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

15

other hand, we may ask to what extent the bubble itself affected the structural (LR) linkages across

prices. This can be achieved by firstly testing for the presence of cointegration and, then, estimating

appropriate Vector Error Correction Models (VECM). The standard VECM equation can be written as

(5) t

k

iiti1tt εlp∆lpαβlp∆

' +Γ+= ∑−

=−−

1

111

where lpt now is the (Vx1) vector containing the logarithms of the V prices at time over the selected

dimension (space ij , commodity kh).8 β is the cointegration matrix which contains the long-run

coefficients (the degree of price transmission). α is the loading matrix which contains the adjustments

parameters (a measure of the speed of price transmission,). Γi are matrixes containing coefficients that

account for short-run relations, and εt are white-noise error terms. The rank of αβ′ gives information

about the presence of cointegration amongst the variables. The fundamental assumptions underlying

(5) is that, the model expressed in logarithms, price spreads (and also, all components which account

for price spreads) are a stationary proportion of prices9.

As already mentioned, we cannot exclude the presence of explosive behavior in some of the price

series. However, Engsted (2006) and Nielsen (2010) have shown that the use of the Johansen (1995)

approach to test and estimate cointegration relationships is still admitted. The cointegrated VAR

model developed by Johansen turns out to be an “ideal framework” for analyzing the linkage between

variables that have a common stochastic trend (they are cointegrated), but in which one of the series

also has an explosive root: the Johansen method makes it possible to estimate the cointegrating

relationship even though the relationship contains this explosive component. Under these

circumstances, it is possible to rewrite equation (5) in a form that admits two structural relations. The

first contains the usual cointegrating parameters (their linear combination that is not I(1)); the second

the co-explosive ones (their linear combination that is not explosive) (Engested, 2006, p. 2006):

(6) t

k

iiti1t1tt εlp∆∆lp∆βαlp∆βαlp∆∆

'' +Γ++= ∑−

=−−−

2

111111 ρρρρρ

where ( )Lρρ −= 1∆ and ρ is the explosive (ρ>1) root. The conventional cointegration vector is 1β as

it can be demonstrated that ββ =1 (Nilelsen, 2010), while ρβ contains the co-explosive parameters.

All other parameter matrices can be interpreted accordingly. The interesting thing, here, is that if our

interest prevalently is in the usual cointegrating relationship between prices (and/or we have not a

reliable estimate of ρ), the standard Johansen estimation procedure holds its validity and we may

simply proceed estimating (5).

8 As evident in Table A.2, V always ranges between 3 and 4. 9 For a general review of the implications of the use of cointegration techniques in price transmission analyses see Listorti, (2009).

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

16

This approach seems appropriate in the present case. We are looking for horizontal price transmission,

therefore for what links together prices across different markets, but we also need to take into account

that, over the investigation period, some prices showed an explosive root. If we were also interested in

investigating the price relationships within the (co)explosive period, however, we should firstly find

out the value of ρ>1 and, then, estimate (6) to obtain an estimate of ρβ . In considering the bubble in

our analysis of price linkages, however, we can even go further by admitting that the period of

exuberance (or the shock that generated it) influenced the cointegration relationship, ββ =1 , itself. In

particular, we may be interested in taking into account the presence of structural breaks within the

cointegration relationship. In this respect, Johansen et al. (2000) generalized the standard Johansen

cointegration test by admitting up to two predetermined breaks in the cointegration space, and

proposed a model where breaks in the deterministic terms are allowed at known points in time.10 The

sample is divided in q periods, separated by the occurrence of the structural breaks, where j denotes

each period. The general VECM becomes:

(7) t

d

mtm,m

k

iiktj,

q

jji,

k

iitit

1t

1tt t

εwΘDklp∆ΓγEE

lp'

µ

βαlp∆ +++++

= ∑∑∑∑

==−+

=

−

=−

−

−

11 2

1

111

where k is the lag length of the underlying VAR. Et is a vector of q dummy variables that take the

value 1, i.e. 1=jtE , if the observation belongs to the j th period (j = 1, …, q), and 0 otherwise; that is,

[ ] '

21 ... qtttt EEE=E .11 Dt is an impulse dummy (with its lagged values) that equals unity if

the observation t is the ith of the jth period, and is included to allow the conditional likelihood function

to be derived given the initial values in each period (for example, if k = 3, impulse dummies will

thereby have the value 1 at t+2, t+1, t, where t is the first observation of each period). wt are the

intervention dummies (up to d) included to obtain well-behaving residuals. The short run parameters

are included in matrices γ (2 x q), Γ (2 x 2), k (2 x 1) for each j and i, and Θ (2 x 2). εt are assumed to

be i.i.d. with zero mean and symmetric and positive definite variance, Ω. [ ] '

21 ... qttt µµµ=µ

is the vector containing the long run drift parameters and β contains the usual the long run coefficients

in the cointegrating vector.

The cointegration hypothesis is formulated by testing the rank of '

=

µ

βαπ ; its asymptotic

distribution can not be generalized as it depends on the number of non-stationary relations, on the

10 See Dawson et al. (2006) and Dawson and Sanjuan (2006) for an application to agricultural future and export prices. 11 For example, if q = 3, i.e. there are two structural breaks, we have [ ] [ ]001,3,2,1 == ttt EEEt

'E if the

observations of time t belong to the first period, [ ]010=t'E if they belong to the second one,

and [ ]100=t'E otherwise.

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

17

location of breakpoints and on the trend specification. The Johansen et al. (2000) procedure directly

stems from the Johansen framework. For this reason, and given the non appropriateness of the

conventional Engle and Granger (1987) cointegration test when evidence of explosive behaviour is

found (Engsted, 2006), we ignore here possible alternative procedures admitting breaks in the long-run

relationship (Carraro and Stefani, 2010).

3.3. Structural breaks: the bubble and the policy regime switching

Two structural breaks are taken into account in the present study as both might have influenced the LR

price transmission relations. For this reason, a “bubble” and a “policy” dummy has been included in

the cointegration space as exogenous variables following (7). Based on the results obtained from tests

on presence and timing of the explosive behaviour (Figure 3), the former dummy has been given the

value 1 for all weekly observations situated between the first week of July 2007 and the last week of

March 2008, and zero otherwise. The second dummy mimics the suspension of the EU import duties

on cereals (Figure 3).

It is well known that agricultural markets are often subject to considerable policy intervention (Listorti

2007, 2009). Especially when international markets are considered, the evaluation of price

transmission mechanisms must take into account the policy regimes that is in place. In our case, this

means considering that the relation between US (or Canadian) and EU prices may be affected by

domestic and border policies of the EU. The European Common Agricultural Policy (CAP) evolved

considerably during the past 20 years, moving from market regulation policies to the use of less

distortive instruments. With the MacSharry Reform in 1992 substantial cuts in cereal intervention

prices were implemented (-30%), the influence of the intervention price on EU markets being

henceforth considerably reduced. The intervention prices for cereals were further reduced with the

Agenda 2000 reform (-15%), and, in particular, they didn’t change over the few years here considered.

For this reason, we do not include them in the estimated models as there is no argument to argue that

they may influence cereal price linkages.

On the contrary, the trade policy regime may have had a role because border policy for cereals

changed during the years of observation. It must be recalled that the EU protection mechanism for

cereals, even after the URAA converted all border measures into import duties, for a long period

resulted in a wide gap between entry (border) and intervention (domestic) prices and, consequently,

high duties. During the 2007-2008 price bubble, however, as a reaction to the exceptionally tight

situation on the world cereals markets, the European Union suspended import duties for cereals

though, in fact, they were already set at very low levels due to the high world prices. The suspension

began in January 2008, it was originally meant to last until the end of the campaign and then

prolonged until June 2009; finally, the reintroduction of duties was anticipated at the end of October

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

18

2008.12 This temporary measure might have altered the price transmission mechanisms between

international (Rotterdam) and national (Italian) prices.13 To take into account this aspect within the

adopted model, the policy dummy takes the value 1 for all weekly observations between January 2008

and October 2008, and 0 otherwise.

3.4. Econometric procedure

For every group of fixed-market/cross-commodity or fixed-commodity/cross-market prices (see Table

A.2), price linkages are assessed according to the following estimation strategy. Following from the

considerations presented in the previous paragraph, an appropriate econometric procedure has been

put in place. This methodology has been repeated, or fixed commodity- cross market prices (in this

case, both with and without the international prices). First of all, cointegration among prices within the

group is assessed using the conventional Johansen (trace) test. If cointegration is found, then the

respective VECM of the prices is estimated.14 If cointegration is not found, and no explosive root is

present within the price group, a first-difference VAR is estimated. Finally, if an explosive root is

present, without cointegration, no model specification can be adopted as first order differentiation

itself can not ensure the removal of the explosive pattern.15

In all the cointegration tests and VECM estimates, the “restricted constant case” of the Johansen

procedure has been considered. The series don’t show any linear trend in levels, but both theory and

visual inspection of the data imply the presence of a constant in the long-run relationship, accounting

for all elements contributing to price differentials not explicitly modelled in the price transmission

equation. This means that, even if there are no linear deterministic trends in the level of the data, the

cointegrating relation has a constant mean.16

Each model is estimated with and without the bubble and policy structural breaks. In VECM models,

following Johansen et al. (2000), these dummies are assumed to have an impact on the constant term

only inside the cointegrating space. Therefore, in equation (7), t has been fixed =1 and γ=0, a constant

term included with the corresponding elimination of one of the q dummy variables. This means that

the coefficients of the structural break dummies have to be interpreted as relative to the constant valid

over the overall period.

12 See Reg. CE 1/2008, Reg. CE 608/ 2008 and Reg. CE 1039/2008. 13 The conversion of the North-American prices into Rotterdam prices with the addition of the freight rates (see section 1) does not consider the import duty. Therefore, while the Rotterdam price may be not directly affected by this policy measure its relation with the Italian actually is. 14 The lag length is selected according to the conventional information criteria (HQIN, SBIC, AIC). In all models, autocorrelation has been tested with a LM test up to the fourth lag. 15 As evident in Table A.2, however, this circumstance never occurs in the present study. 16 It is worth reminding that a constant (additive) term in tlp corresponds to a multiplicative term in price level

( tp ).

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

19

For these VECM estimates, the underlying assumption is that the rank of the cointegration matrix

remains the same with or without the two structural breaks. As a matter of fact, the Johansen, et al.

(2000) procedure doesn’t allow testing for the cointegration rank with the number of breaks here

considered. For this reason, unit root tests are run on the residuals of the cointegration relation to

check if the rank selected without the breaks can be confirmed ex post after their introduction.17

The introduction of the bubble and policy dummies is straightforward when prices are not

cointegrated. Within the standard first-difference VAR to be estimated in this case, structural breaks

simply enter as exogenous dummy variables in the VAR, thus allowing for a shift in the constant term

of the VAR equations. In such case, however, the response to a price shock can not be interpreted as a

reversion to some LR relationship because no evidence support the existence of such LR pattern.

Weak exogeneity tests (i.e., convention t-tests on coefficients of vector αααα) for the estimated VECM

and Granger causality tests for the VAR, are eventually performed to assess how price horizontally

transmits from ikp to jkp or ikp to ihp . Through these tests, for any group of prices we can identify

which causal relationships emerge, that is, which are the “central” (leader in price formation) and

“satellite” (follower) markets (Verga and Zuppiroli, 2003). Finally, the size and the direction of these

significant causal relationships are analysed by estimating the respective Impulse Response Functions

(IRF).18

4. Results

4.1. Cross-market transmission

The results for the models estimated in the fixed-commodity/cross-market case are reported in Tables

8A-N. According to the groupings reported in Table A.2, six commodities have been analysed: durum

wheat; high quality soft wheat; medium quality soft wheat; low quality soft wheat; corn; barley. Any

model has been estimated both with and without the Rotterdam price in order to separately analyse the

relationship occurring among national prices and between them and the international one.

For durum wheat the cointegration rank turns out to be 1. In the cointegration vector the coefficient of

the Foggia price is higher and more significant than Rome (-0.811 vs -0.235)19 and is the only price for

which we can reject weak exogeneity (the adjustment coefficient is 0.2). Including the bubble and

policy dummies doesn’t alter these results significantly. The coefficients of the two dummies are very

similar and not significant but have the same sign of the constant term (0.025, 0.026 and 0.507 for the

bubble, policy dummy and the constant term, respectively), which means that there is an increase of

17According the discussion above, however, due the presence of an explosive ρ>1 we can not exclude that the

linear combination 1t' lpβ − contains an explosive component.

18 IRF computes the response of price ikp (or jhp ) to a one-time unit shock on price jkp . 19 Statistical significance of the coefficients of the cointegrating vector is obtained by testing the respective exclusion restrictions.

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

20

the distance among the prices during the structural breaks. When the international price is included,

the rank of the cointegration matrix remains equal to one. Though the Rotterdam price presents strong

evidence of explosive behaviour (Table 6), the residuals from the cointegration relation remain

stationary. All coefficients within the cointegration space are now significant (-0.472 for the Rome

price, -0.648 for the Foggia price, and 0.069 for the Rotterdam price), although in the case of the

Rotterdam price is much lower than the others and has not the expected sign. Both the Rome and the

Foggia price adjustment coefficients are significant (they are, respectively, 0.134 and 0.256), whereas

the Bologna and Rotterdam prices are weakly exogenous. Even in this case, the bubble and the policy

dummies do not substantially affect the findings. Their coefficients are once again positive in sign

(0.014 for the bubble dummy and 0.007 for the policy dummy, with a constant of 0.407), but not

significant.

The estimated IRFs of the endogenous prices in the model with the international price and the policy

dummies, that is the Rome and Foggia prices, are reported in Figure 4. We can notice that all response

are positive and do not die out (as implied by the existence of a cointegrating vector between the

prices), the only exception being the response of Foggia on a shock in the Rome price, the two

evidently behaving as “satellite” markets. In general, the responses to shocks in the international prices

are lower than the ones to shocks on the domestic ones. In this respect, Bologna seems to behave as

the leading market.

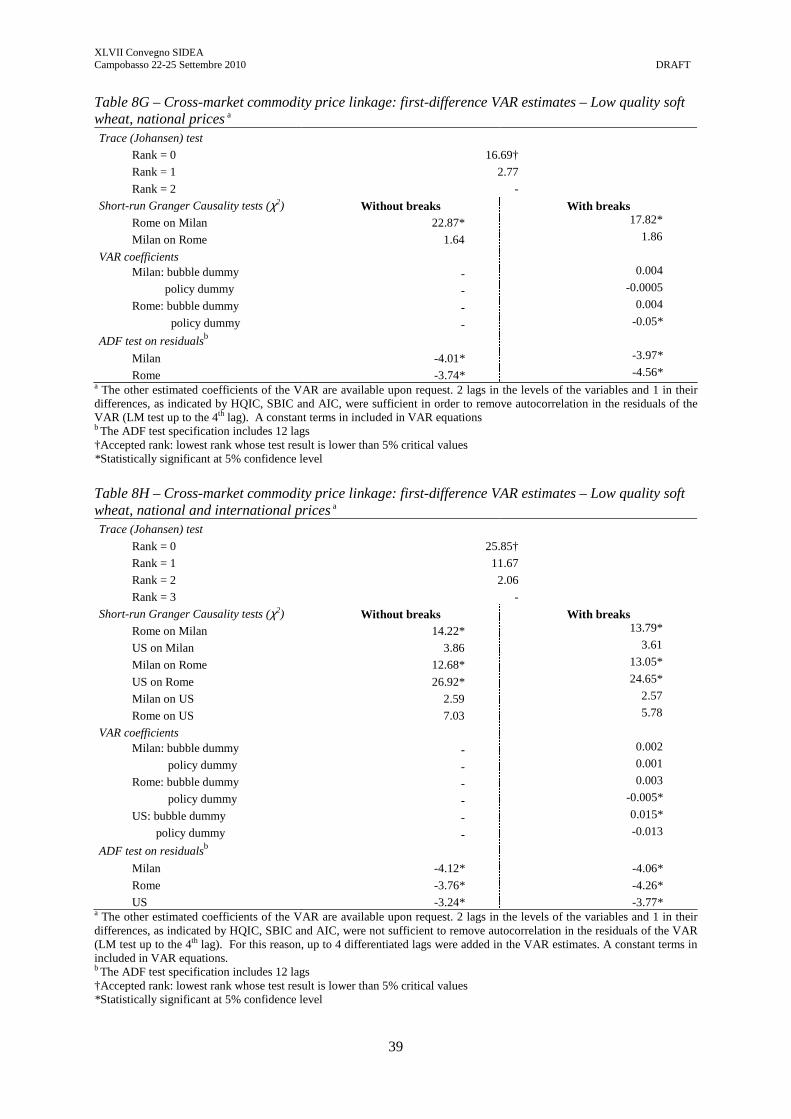

For all soft wheat qualities (high, medium and low quality), prices are never cointegrated (regardless

the inclusion of the international price).20 The respective VAR models in the first differences have

been thus estimated. For high and medium-quality soft wheat, when only national prices are

considered, we may notice that the Bologna price Granger causes (GC) the Milan one. For low-quality

soft wheat, the Rome price GC the Milan one. In general, when only national prices are considered,

the structural breaks tend to have low impact and statistical significance. For all qualities the bubble

dummy has a positive sign, whereas the policy dummy has a negative sign (with the only exception of

the Milan price equation in the case of medium-quality soft wheat).

When also the Rotterdam price is included in the VAR system, estimates show that, for high-quality

soft wheat the Rotterdam price GC the Bologna and Milan prices (and Bologna GC Milan), while for

medium-quality soft wheat it GC the Bologna price only (and Bologna GC Milan and US), and for

low-quality only the Rome price (and Rome GC Milan, and Milan GC Rome). A rather clear pattern

of causality would thus emerge: with the exception of high-quality soft wheat, for which the

Rotterdam price affect both the Milan and the Bologna prices, Rotterdam price shocks are first

transmitted to a “central” Italian market (Bologna or Rome, according to quality), and then to the

20 In all cases, the Rotterdam price correspondent to US HRW has been used as international reference. This price, therefore, is not among those clearly showing an explosive behaviour (Tables 6 and A.2)

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

21

“satellite” ones. For high and medium-quality soft wheat, the centrality of the Bologna market with

respect to the Milan is confirmed. This pivotal role could be interpreted arguing that Bologna is a

closer market to the largest production area of soft wheat in Italy (see also Verga and Zuppiroli, 2003).

The Bologna market transfers the Rotterdam price shocks to the Milan one. As far as the structural

breaks are concerned, their behaviour is in line with what observed in the case of the national-market

specification. Their coefficients are rather low (between -0.013 and 0.015) and hardly significant

(with the exception of the equation of the Milan price for low-quality soft wheat)

The significant (according to Granger causality) IRF are reported in Figures 5-7. The pattern of the

response over time generally indicates a rapid decay of the response in few years. In the case of the

VAR model here estimated this can be considered as an evidence of the fact that a shock in iklp∆1

(that is, in growth rate of prices) only temporarily affects the growth rates of the other prices that

eventually came back to the initial growth rates. It is worth noticing that the lack of a cointegration

relationship prevents from interpreting this response in terms of reversion to a LR relationship among

prices. In general terms, the IRF suggest that the response to a shock in a national price is higher than

to a shock in Rotterdam price. For high-quality soft wheat, the response of Milan on Bologna is rather

high, and tends to die out after the 4th lag, whereas the response of Milan and Bologna on Rotterdam

are lower and decay after 2 lags. Although the Bologna price GC the Milan one, both prices respond to

a shock in the Rotterdam prices, and this response is higher in Milan, that evidently behaves as a final

(or destination) market (Verga and Zuppiroli, 2003). For medium-quality soft wheat, the response of

Milan to a shock in the Bologna price is rather high, and tends to die out after the 4th lag, whereas the

response of Bologna on Rotterdam is much lower, reaches a peak after 2 lags, and then decays. The

Rotterdam response on a Bologna shock reaches a peak after 1 lag, and then decays. For low-quality

soft wheat, the response of Milan to a shock in the Rome price is rather high, and has an oscillating

behaviour. The response of Rome to a shock in the Rotterdam price is higher than the one to a shock

in the Milan price. Both die out after the 4th lag.

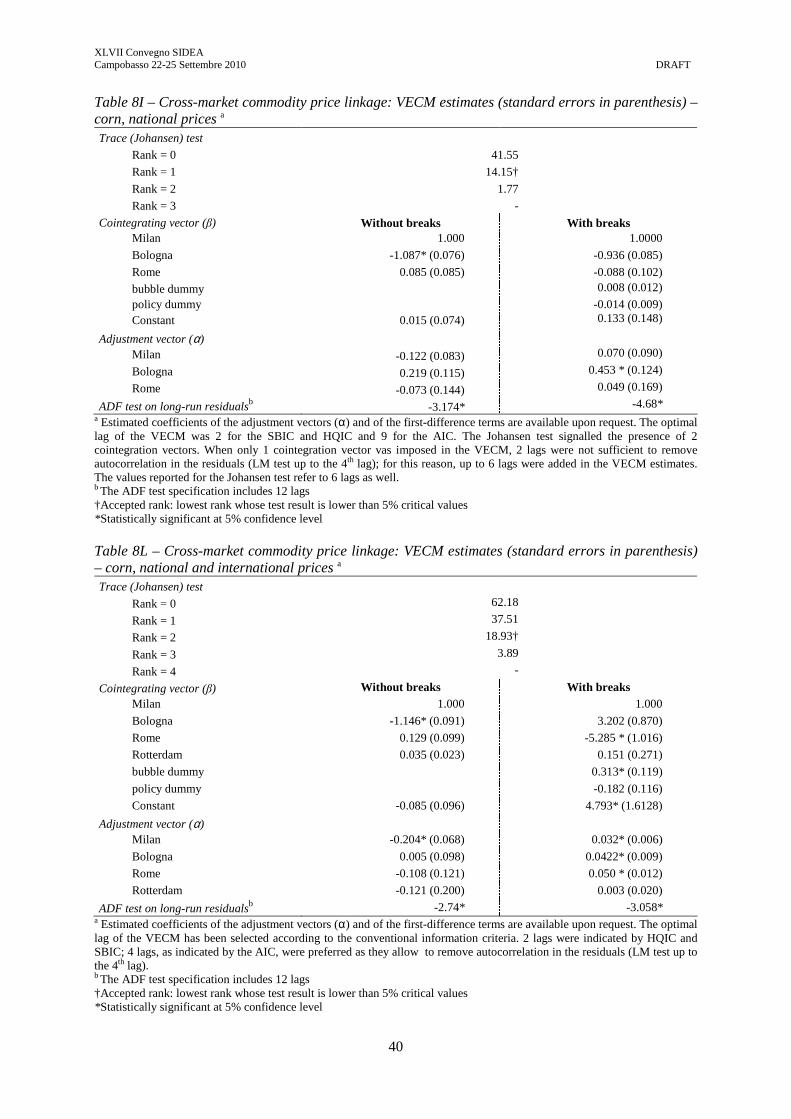

In the case of corn, the cointegration rank among national prices is one. No conclusive evidence of

explosive behaviour among these prices emerges (Tables 6 and A.2). As expected, therefore, the

residuals from the cointegration relation are stationary. The elasticity of price transmission in the

cointegration vector between the Milan and the Bologna price is very close to one (-1.087) and

significant, whereas the coefficient of the Rome price is not statistically significant and has not the

correct sign (0.085). None of the adjustment coefficients, however, is significant at the 5% level.

When the structural break dummies are included in the cointegration space, the coefficient of the

Bologna price remains very close to one (-0.936), and the coefficient of the Rome price becomes

negative (-0.088), although none of them is significant. The coefficient of the bubble dummy is

positive in sign (0.008), whereas the policy dummy has a negative coefficient (-0.014) but both are not

statistically significant. Considering the sign of the constant term, this would mean that during the

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

22

bubble the distance between the prices widened, while it diminished during the suspension of the EU

import duties. Only the Bologna price can be considered endogenous as it significantly responds to the

disequilibria with respect to the LR relation. When the Rotterdam price is included, two cointegration

vectors emerge. In estimating the VECM, however, we imposed only one cointegration vector.

Although the Rotterdam price is suspected to have an explosive behaviour, the residuals form the

cointegrating relations still are stationary. In the VECM without the bubble and policy dummies, the

estimates are very similar to the model with only national prices: the coefficient of the Bologna price

is very close to one, and significant (-1.146). The coefficient of the Rome and Rotterdam prices are

positive and not significant (0.129 and 0.035, respectively). When the structural breaks are included,

the estimates remarkably change: all national price series adjustment coefficients become positive and

significant (namely, they are endogenous), and the coefficients of the long run relation become very

high.

The IRF for corn (Figure 8) show that the response of Milan to a shock in Bologna is higher than to a

shock in Rotterdam, whereas the response of Milan to a shock in Rome is negative. Even in this case,

even if the Rotterdam price behaves as an international leading price, at the national level the

prevailing leading role is of the Bologna market, while both Milano and Rome behave as destination

markets.

Finally, in the case of barley, no cointegration emerges both with and without the international price.

For this commodity, the Bologna price presents evidence of explosive behaviour albeit even for the

Rotterdam price there may be support in this direction. The respective VAR estimates suggest that

Bologna price GC the Foggia one. Once again, the bubble dummy has a positive sign (0.004 and

0.002, respectively, in the Bologna and Foggia equations), whereas the policy dummy has a negative

sign (-0.011 and -0.002, respectively). After the inclusion of the Rotterdam price in the VAR system,

all GC relations become not statistically significant. The structural breaks behave very similarly,

though in the Rotterdam price equation, the bubble and the policy dummies are both negative (and

equal to -0.003 and -0.007, respectively). Only the policy dummy in the Bologna price, however, is

statistically significant.

The IRF (Figure 9) for barley are reported only under the case with the bubble and policy dummies but

without the international prices (as no significant Granger causality emerge in this latter case). We can

notice that the response of Foggia to a shock in the Bologna price is much higher than the other way

round. It has an oscillating behaviour and dies out only after the 10th lag. Even in this case, Bologna

seems to emerge as the leading market even Foggia can be considered closer to vast productions areas.

Summing up, as far as structural breaks are concerned, we can notice that in all estimated VAR

models (all qualities of soft wheat and barley), both with and without the international prices, the sign

of the bubble dummy is positive, whereas the sign of the policy dummy tends to be negative. This

would confirm that, whereas, as obvious, prices did increase their upward response to shocks during

the inflation of the price bubble (as expressed by an upward shift of constant term of all VAR

XLVII Convegno SIDEA Campobasso 22-25 Settembre 2010 DRAFT

23

equations), the suspension of the EU import duties on cereals is associated to a reduction of this

upward push. The same holds also in the VECM for corn: the bubble dummy shows the same sign of

the constant term in the cointegration space, which means that there is an increase in the gap between

prices. This gap is then partially compensated in correspondence of the suspension of the EU import

duties. On the contrary, for durum wheat VECM both the bubble and the policy dummies show the

same sign of the constant term in the cointegration space, thus contributing to increase the gap

between prices within the system. In most cases the policy dummy is more significant than the bubble

one and, interestingly, their coefficients tend to be rather close in magnitude. In other words, when

they show opposite signs (as in all commodities, durum wheat excluded), it would mean that the

policy intervention (that came after the bubble inflation) partially neutralized the impact of the bubble

on price gaps.

As far as the IRF are concerned, the responses to price shocks in the domestic markets are generally

higher than those to price shocks in the international ones. While, as obvious, the response never goes

to zero in the VECM cases, the impact on price growth rates tends to die out after the 4th lag, for