Aggregation and the PPP Puzzle in a Sticky Price Model · Average frequency of price changes...

25

Aggregation and the PPP Puzzle in a Sticky Price Model Carlos Carvalho Federal Reserve Bank of New York Fernanda Nechio Princeton University May 2009 The views expressed in this presentation are those of the authors and do not necessarily reect the position of the Federal Reserve Bank of New York or the Federal Reserve System.

Transcript of Aggregation and the PPP Puzzle in a Sticky Price Model · Average frequency of price changes...

Aggregation and the PPP Puzzle in a StickyPrice Model�

Carlos CarvalhoFederal Reserve Bank of New York

Fernanda NechioPrinceton University

May 2009

�The views expressed in this presentation are those of the authors and do not necessarily re�ect theposition of the Federal Reserve Bank of New York or the Federal Reserve System.

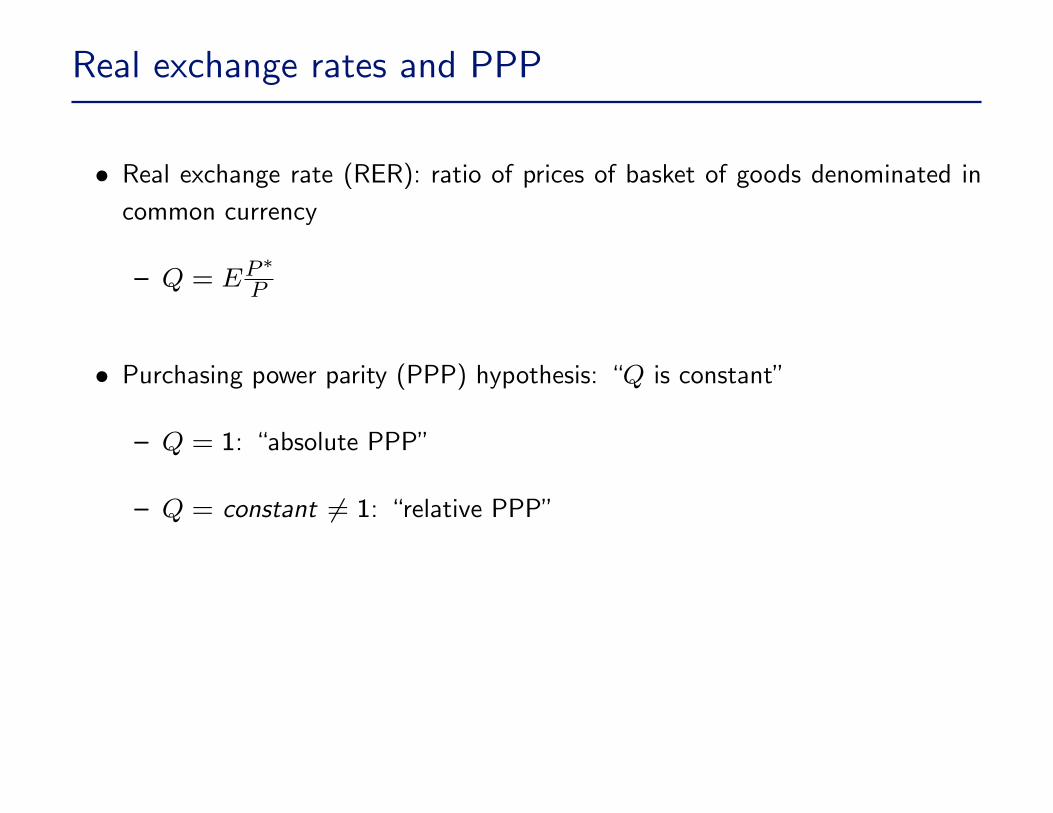

Real exchange rates and PPP

� Real exchange rate (RER): ratio of prices of basket of goods denominated incommon currency

� Q = EP�P

� Purchasing power parity (PPP) hypothesis: �Q is constant�

� Q = 1: �absolute PPP�

� Q = constant 6= 1: �relative PPP�

US Dollars / "French Franc-Euro"

0.4

0.6

0.8

1

1.2

1.4

1.6Ja

n-83

Jan-

84

Jan-

85

Jan-

86

Jan-

87

Jan-

88

Jan-

89

Jan-

90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

0.4

0.6

0.8

1

1.2

1.4

1.6

FX (left axis) RER (left axis) Price Ratio (right axis)

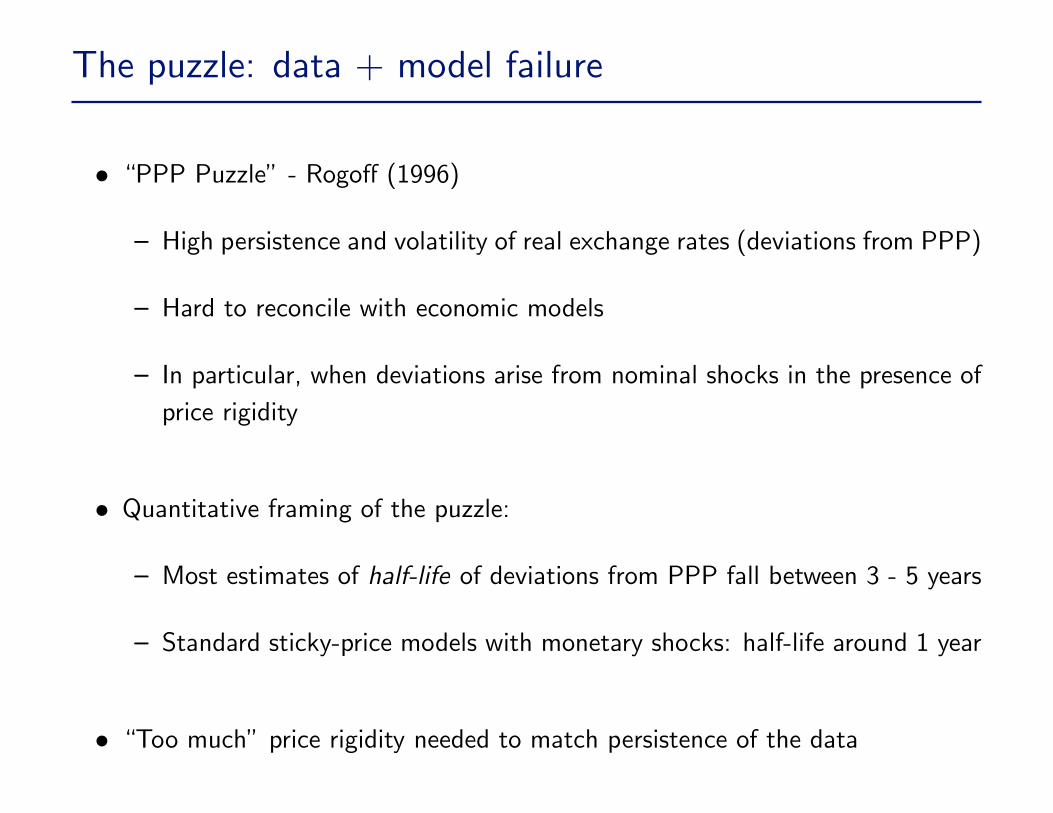

The puzzle: data + model failure

� �PPP Puzzle� - Rogo¤ (1996)

� High persistence and volatility of real exchange rates (deviations from PPP)

� Hard to reconcile with economic models

� In particular, when deviations arise from nominal shocks in the presence ofprice rigidity

� Quantitative framing of the puzzle:

� Most estimates of half-life of deviations from PPP fall between 3 - 5 years

� Standard sticky-price models with monetary shocks: half-life around 1 year

� �Too much�price rigidity needed to match persistence of the data

Our paper

� Build on ample evidence of heterogeneity in frequency of price adjustment (Bilsand Klenow 2004 and others)

� Average degree of price rigidity not the relevant statistic for aggregatedynamics (Carvalho 2006)

� Potential source of heterogeneity in dynamics of sectoral real exchange rates

� Multi-sector, two-country, sticky-price model:

� Heterogeneity in frequency of price changes

� Price discrimination and local currency pricing

) Heterogeneous sectoral real exchange rates

Summary of the model - K sectors

Consumers Consumers*

Home Foreign

FinalGoods

FinalGoods*

IntermediateGoods

IntermediateGoods*

Sector 1 ... Sector KSector k ...YH,k,j

Y*H,k,j

Sector 1 ... Sector KSector k ...YF,k,j

Y*F,k,j

C

L

C*

L*

Y Y*

YH,k,j Y*H,k,j YF,k,j Y*

F,k,j

Summary of the model - 1 sector

Consumers Consumers*

Home Foreign

FinalGoods

FinalGoods*

IntermediateGoods

IntermediateGoods*

C

L

C*

L*

Y Y*

YH,j Y*H,j YF,j Y*

F,j

Summary of core quantitative results

� Quantitative model

� Discipline our argument: distribution of price stickiness chosen to matchmicro data

� Average frequency of price changes implies average spells of 4.4 months

� Half-life of deviations from PPP in heterogeneous economy: 3.8 years

� Half-life of deviations from PPP in homogeneous economy: 1.2 years

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

Core results: intuition I

� Sectors with more stickiness are disproportionally important for aggregate dy-namics

� Extreme case: 1 �exible- and 1 sticky-price sector, no pricing complementarities

� Aggregate RER dynamics driven only by sticky-price sector

� Mathematically: measures of persistence (and volatility) are convex in thefrequency of price changes

CVIANAC

Highlight

CVIANAC

Highlight

Core results: intuition II

� E¤ects even stronger in the presence of pricing complementarities!

� Not-so-extreme version of �responders vs non-responders�of Haltiwanger andWaldman (1991)

� Bottom line in terms of persistence:

� heterogeneous economy � homogeneous economy with more price sticki-ness than what�s implied by average frequency of price changes

CVIANAC

Highlight

CVIANAC

Highlight

The model

� Two countries, Home and Foreign, with identical, in�nitely lived consumers

� Commodities are labor, a consumption good and a continuum of intermediategoods

� Consumer supplies labor, invests in complete set of state-contingent assets, andconsumes non-traded �nal good

� Competitive �nal good producers bundle intermediate goods; �exible prices

� Monopolistically competitive intermediate goods producers:

� Price discriminate, setting prices in local currency

� Sticky prices; adjustment frequency varies across sectors

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

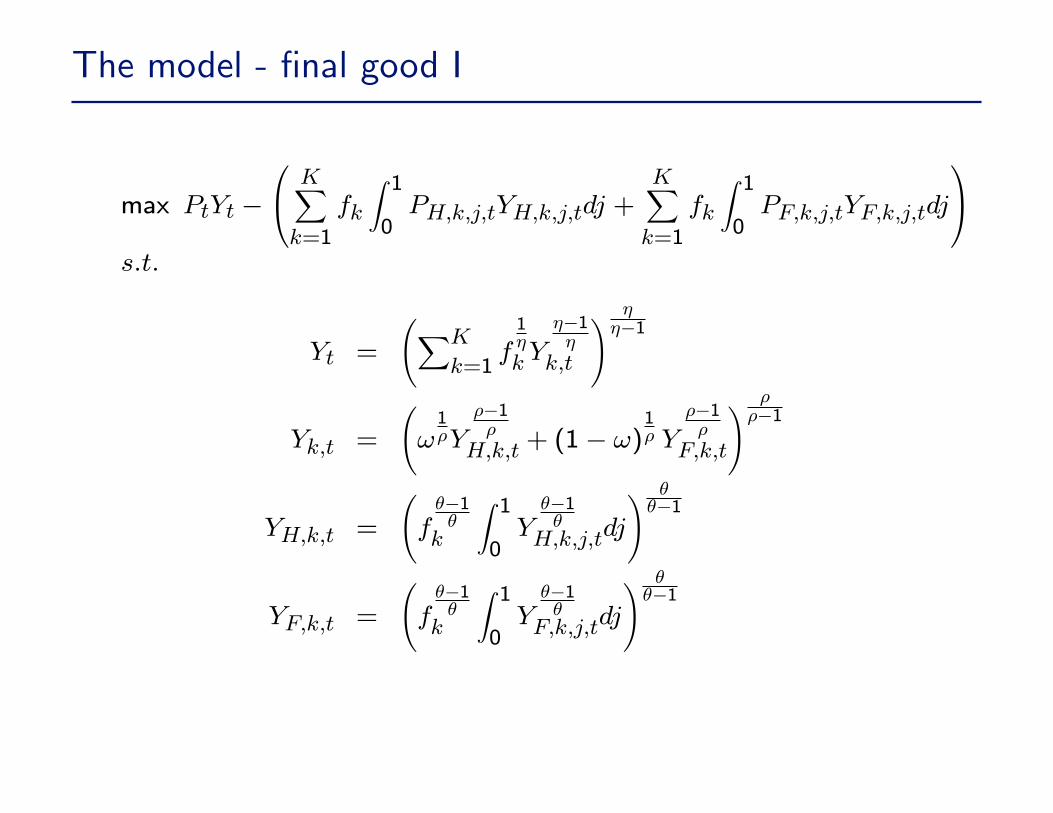

The model - �nal good I

max PtYt �

0@ KXk=1

fk

Z 10PH;k;j;tYH;k;j;tdj +

KXk=1

fk

Z 10PF;k;j;tYF;k;j;tdj

1As:t:

Yt =

XK

k=1f1�k Y

��1�

k;t

! ���1

Yk;t =

!1�Y

��1�

H;k;t + (1� !)1� Y

��1�

F;k;t

! ���1

YH;k;t =

f��1�

k

Z 10Y��1�

H;k;j;tdj

! ���1

YF;k;t =

f��1�

k

Z 10Y��1�

F;k;j;tdj

! ���1

The model - �nal good II

� Demands

YH;k;j;t = !

PH;k;j;t

PH;k;t

!�� PH;k;tPk;t

!�� Pk;tPt

!��Yt

YF;k;j;t = (1� !) PF;k;j;t

PF;k;t

!�� PF;k;tPk;t

!�� Pk;tPt

!��Yt

� Price Indices:

Pt =�XK

k=1fkP

1��k;t

� 11��

Pk;t =�!P

1��H;k;t + (1� !)P

1��F;k;t

� 11��

PH;k;t =

Z 10P 1��H;k;j;tdj

! 11��

PF;k;t =

Z 10P 1��F;k;j;tdj

! 11��

The model - intermediate �rms I

� Intermediate �rms:

� divided into sectors that di¤er in the frequency of price changes

� Calvo (1983) pricing: �k = frequency of price changes in sector k

� indexed by country, sector (k 2 K), and by j 2 [0; 1]

� sectoral weights fk

� produce di¤erentiated varieties using labor

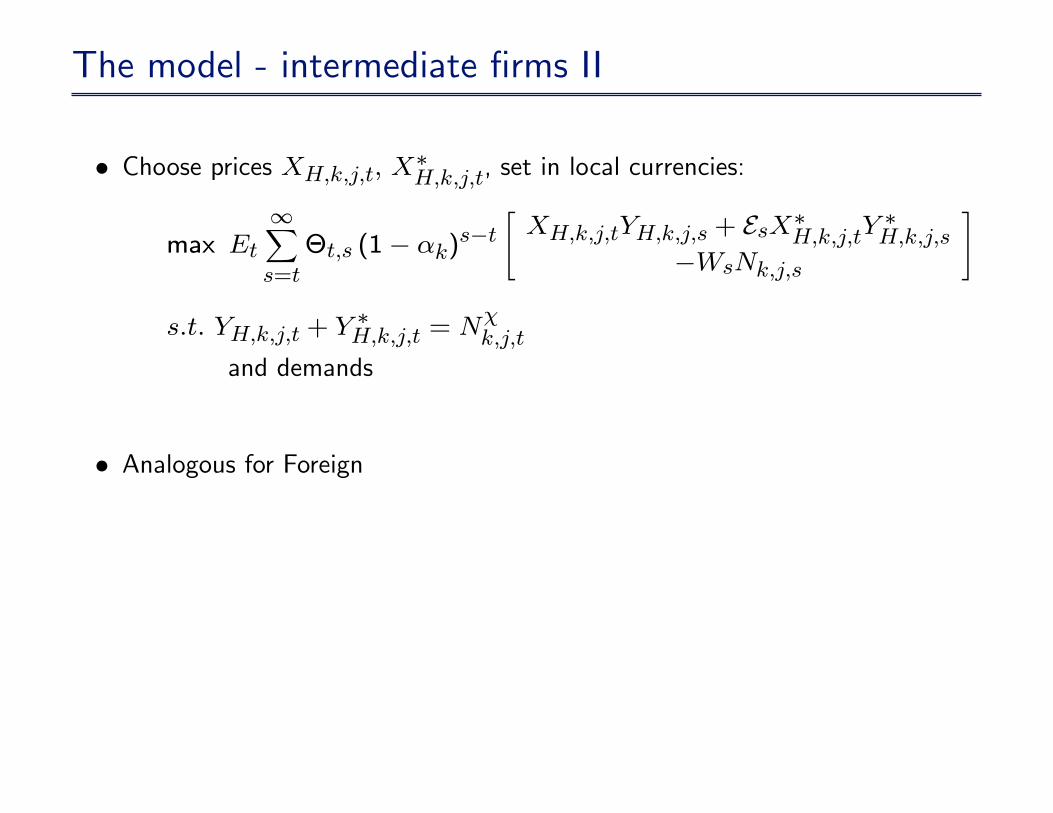

The model - intermediate �rms II

� Choose prices XH;k;j;t; X�H;k;j;t, set in local currencies:

max Et

1Xs=t

�t;s (1� �k)s�t"XH;k;j;tYH;k;j;s + EsX�H;k;j;tY

�H;k;j;s

�WsNk;j;s

#

s:t: YH;k;j;t + Y�H;k;j;t = N

�k;j;t

and demands

� Analogous for Foreign

The model - aggregate and sectoral RERs

� Aggregate:

Qt �EtP �tPt

� Sectoral:

Qk;t �EtP �k;tPk;t

Closing the model

� Speci�cations for monetary policy that ensure existence and uniqueness of REequilibrium

� Equilibrium: optimality and market clearing conditions

� Solution: loglinearization around zero in�ation steady-state

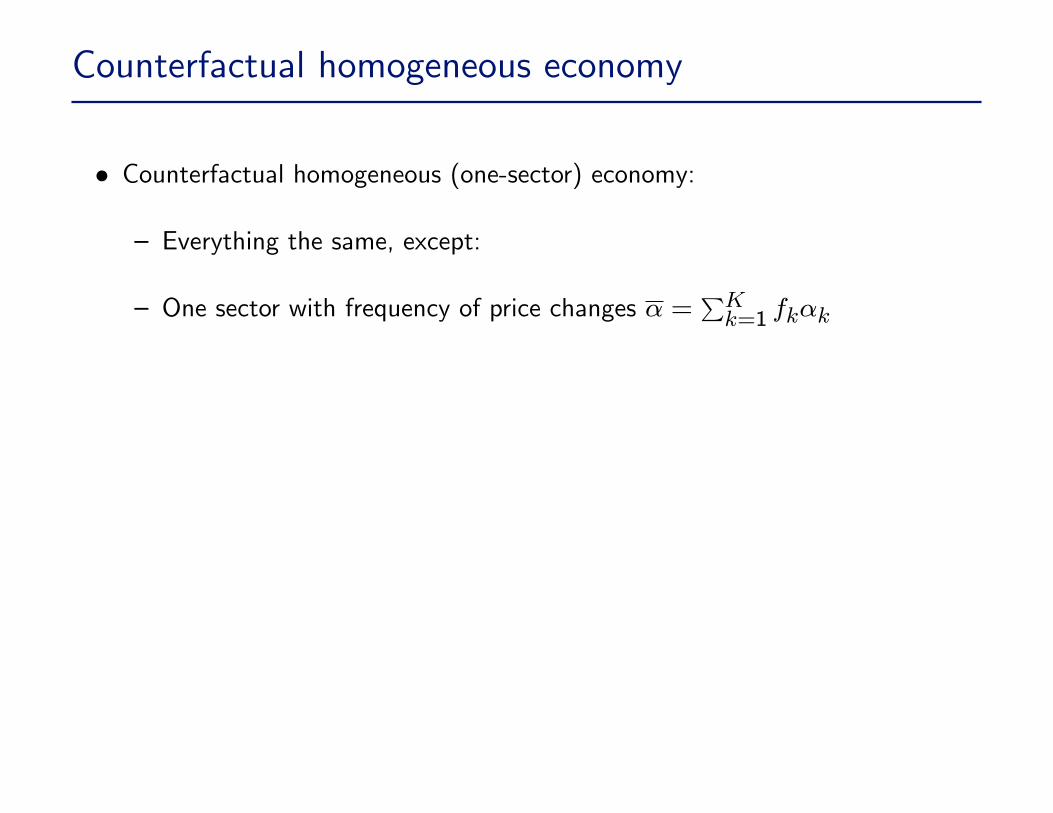

Counterfactual homogeneous economy

� Counterfactual homogeneous (one-sector) economy:

� Everything the same, except:

� One sector with frequency of price changes � =PKk=1 fk�k

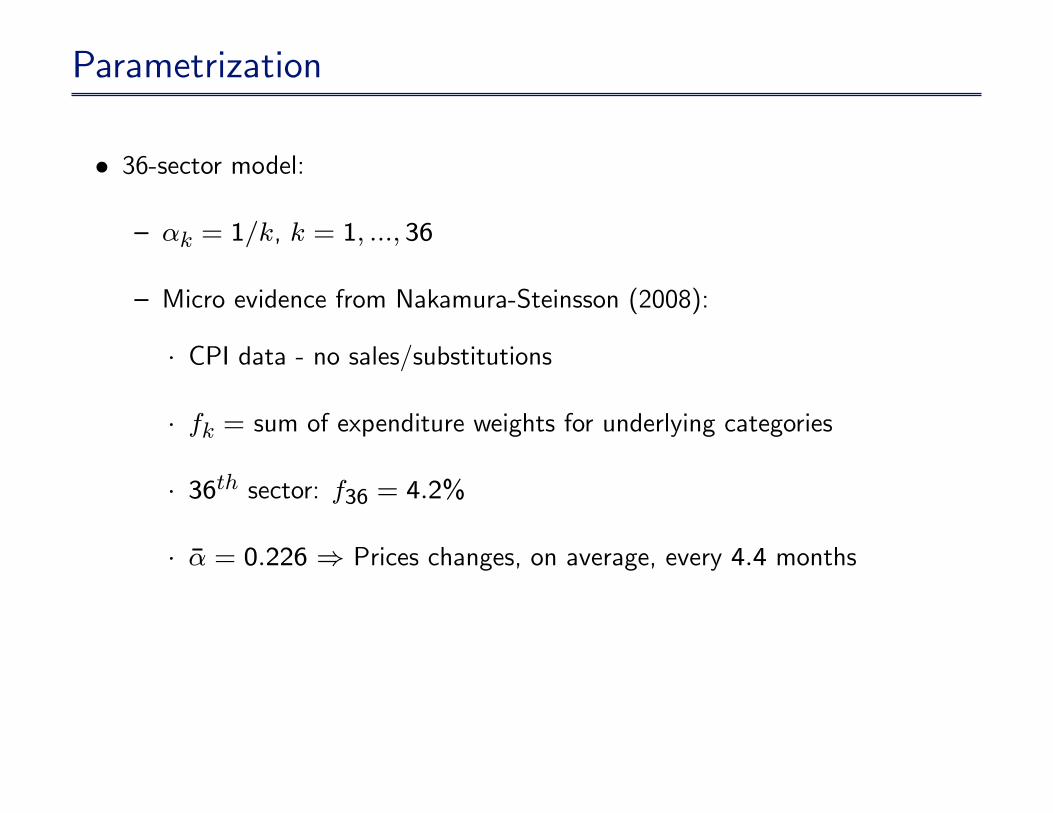

Parametrization

� 36-sector model:

� �k = 1=k, k = 1; :::; 36

� Micro evidence from Nakamura-Steinsson (2008):

� CPI data - no sales/substitutions

� fk = sum of expenditure weights for underlying categories

� 36th sector: f36 = 4:2%

� �� = 0:226 ) Prices changes, on average, every 4:4 months

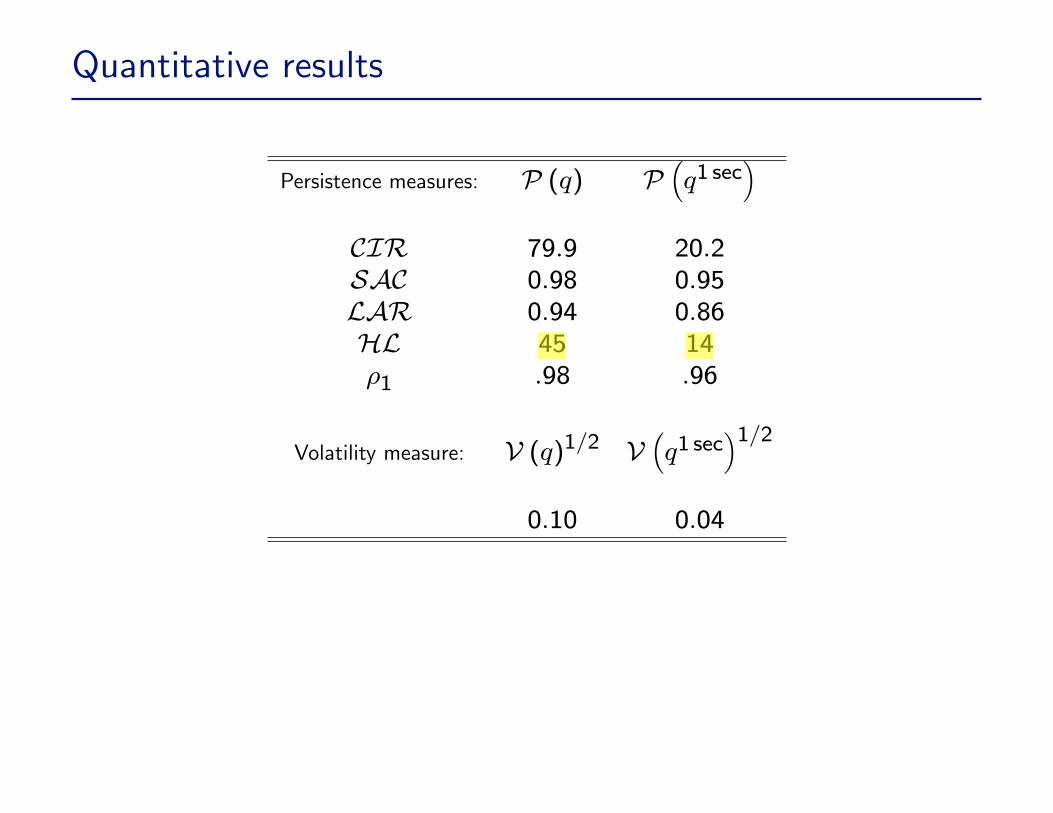

Quantitative results

Persistence measures: P (q) P�q1 sec

�CIR 79:9 20:2SAC 0:98 0:95LAR 0:94 0:86HL 45 14�1 :98 :96

Volatility measure: V (q)1=2 V�q1 sec

�1=20:10 0:04

CVIANAC

Highlight

CVIANAC

Highlight

Using our structural model - extras

� We provide structural interpretation to the (reduced-form) empirical literatureon heterogeneity, aggregation and PPP

� �PPP Strikes Back/Aggregation Bias�debate between Imbs et al. (2005),and Chen and Engel (2005) / Crucini and Shintani (2008)

� Study persistence in the cross-section of sectoral exchange rates ; touch basewith Kehoe and Midrigan (2008) (this is work in progress)

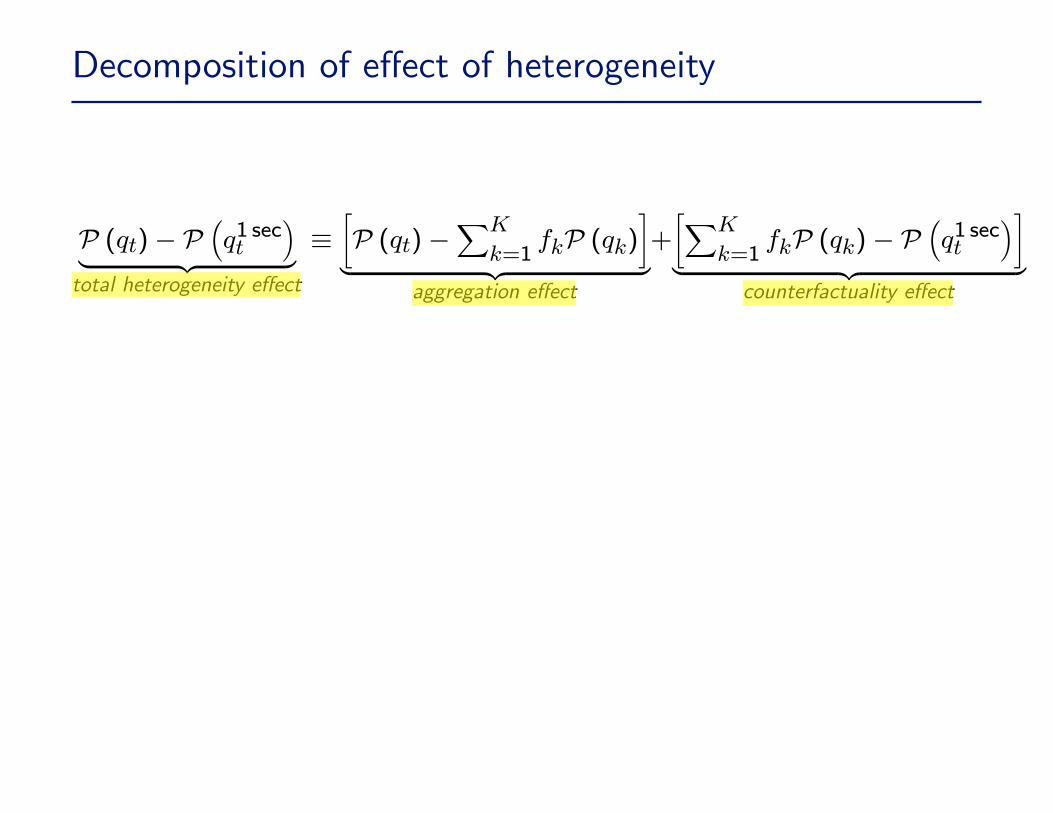

Decomposition of e¤ect of heterogeneity

P (qt)� P�q1 sect

�| {z }total heterogeneity e¤ect

��P (qt)�

XK

k=1fkP (qk)

�| {z }

aggregation e¤ect

+�XK

k=1fkP (qk)� P

�q1 sect

��| {z }

counterfactuality e¤ect

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

Applying decomposition

"Eurostatdata

#Data Panel, agg. Panel, sect. Panel, sect.

Estim. method Fixed E¤ects OLS MGP (q) 1

K

PP (qk) P�q1 sec

�Persist. meas.:

CIR 64:39 59:48 33:19SAC 0:98 0:97 0:97LAR 0:97 0:94 0:95HL 46 43:16 26

"Simulateddata

#Economy Heterog. Heterog. One-sectorData Single, agg. Panel, sect Single, agg.

Estim. method OLS OLS OLSP (q) 1

K

PP (qk) P�q1 sec

�Persist. meas.:

CIR 73:4 60:8 36:9SAC 0:98 0:97 0:97LAR 0:96 0:89 0:87HL 43:1 31:6 21:8

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

CVIANAC

Highlight

Conclusion - I

� Multi-sector, two-country, sticky-price model can produce RER that is as per-sistent as in the data

� One-sector version of same economy with average frequency of price changesfails to do so

� We use our model to explain the apparently con�icting �ndings in reduced-formempirical literature

� Di¤erent papers measured di¤erent objects

� As Chen and Engel (2005) and Crucini and Shintani (2008), we �nd aggre-gation e¤ect to be small (in the parametrized model and in the data)

� As Imbs et al. (2005), we �nd total heterogeneity e¤ect to be large (in theparametrized model and in the data). This is due to the counterfactualitye¤ect

Conclusion - II

� What matters for understanding the gap between data and standard one-sectormodels is total heterogeneity e¤ect

� Heterogeneity in price stickiness goes a long way towards solving the PPPpuzzle

� Such type of heterogeneity known to matter for policy:

� In �closed economies�: Aoki (2001), Benigno (2004), Eusepi, Hobjn andTambalotti (2008), Berriel and Sinigaglia (2008)

� In open economies: ?