AGA Taxation Committee Meeting Accounting for … · AGA Taxation Committee Meeting Accounting for...

26

AGA Taxation Committee Meeting Accounting for Income Taxes: Recent Developments and Current Issues June 10, 2015 AGA Taxation Committee Meeting Accounting for Income Taxes: Recent Developments and Current Issues David J. Yankee Deloitte Tax LLP June 10, 2015 Copyright © 2015 Deloitte Development LLC. All rights reserved. 1 FASB developments • Balance sheet classification • Intra-entity transfer of assets • Investments in affordable housing credit projects • Employee share-based payment accounting improvements project FERC reporting • Tax receivables – overpayments and refunds • UTP reporting • Tax benefit related to interest expense • Accounting method changes Tangible property regulations • Accounting for effects of flow-through accounting Accounting for Income Taxes: Recent Developments and Current Issues

Transcript of AGA Taxation Committee Meeting Accounting for … · AGA Taxation Committee Meeting Accounting for...

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues

David J. YankeeDeloitte Tax LLP

June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 1

FASB developments• Balance sheet classification • Intra-entity transfer of assets • Investments in affordable housing credit projects• Employee share-based payment accounting improvements project

FERC reporting• Tax receivables – overpayments and refunds• UTP reporting• Tax benefit related to interest expense• Accounting method changes

Tangible property regulations• Accounting for effects of flow-through accounting

Accounting for Income Taxes: Recent Developments and Current Issues

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 2

February 2013 – Financial Accounting Foundation (FAF) announced a Post-Implementation Review (PIR) of FASB Statement No. 109, Accounting for Income Taxes

November 2013 – FAF completed its PIR of Statement 109 and concluded:• Statement 109 adequately achieved its intended purposes, although

slightly complex• Investors struggle to assess cash tax effects• Stakeholders find the following to be operationally challenging:

– Intraperiod tax allocation– Accounting for intercompany transfers of assets– Indefinitely reinvested foreign earnings

December 2013 – FASB Response Letter to FAF PIR Report• Will evaluate the PIR Report findings

FASB income tax projectTime line of key events

Copyright © 2015 Deloitte Development LLC. All rights reserved. 3

August 2014 – FASB added to its technical agenda a project to simplify the accounting for income taxes by eliminating:• Classification of deferred taxes between current and noncurrent• The exception to the income taxes accounting model that prohibits the

recognition of income tax consequences of intra-entity asset transfers

October 2014 – Board voted to issue an exposure draft

January 22, 2015 – Two Accounting Standards Updates (ASUs) proposed as part of the simplification initiative• Balance sheet classification • Intra-equity transfer of assets

May 29, 2015 – End of comment period for the proposed ASUs

FASB income tax projectTime line of key events (cont.)

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 4

Classify all deferred taxes as noncurrent• Jurisdictional netting still required

Transition guidance • Applies prospectively to all DTAs/DTLs (no restatement of prior periods)

Effective dates• Public business entities

– Annual periods, including interim periods within those annual periods, beginning after December 15, 2016

– Early adoption not permitted• All other entities

– One year later– Allowed to adopt early, but not before the effective date for public companies

and must adopt both issues if elect to early adopt

Balance sheet classification of deferred taxesFile Reference No. 2015-210

Copyright © 2015 Deloitte Development LLC. All rights reserved. 5

740-10-45-4 In a classified statement of financial position, an entity shall separate classify deferred tax liabilities and assets into a current amount and a as noncurrent amounts amount. Deferred tax liabilities and assets shall be classified as current or noncurrent based on the classification of the related asset or liability for financial reporting. 740-10-45-5 Paragraph superseded by Accounting Standards Update 2015-XX. The valuation allowance for a particular tax jurisdiction shall be allocated between current and noncurrent deferred tax assets for that tax jurisdiction on a pro rata basis. 740-10-45-6 For a particular tax-paying component of an entity and within a particular tax jurisdiction, all current deferred tax liabilities and assets shall be offset and presented as a single amount and all noncurrent deferred tax liabilities and assets, as well as any related valuation allowance, shall be offset and presented as a single noncurrent amount. However, an entity shall not offset deferred tax liabilities and assets attributable to different tax-paying components of the entity or to different tax jurisdictions.

Income Taxes – Overall – Other Presentation Matters –Deferred Tax Accounts

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 6

Company has a net DTA of $750 as of the end of 20X1, as reflected below

Company expects the following reversals of the its DTAs/(DTLs) in 20X2• Accounts receivable – bad debt reserve $40 deductible• Fixed assets $100 taxable• Net operating loss (state) $50 deductible

Balance sheet classification of the DTAs/(DTLs) at the end of 20X1:

Balance sheet classification of deferred taxesCurrent and proposed accounting – example

Current guidance Proposed guidanceBalance sheet as of 12/31/20X1 DTA/(DTL) Current Non-current Current Non-

currentAccounts receivable –bad debt reserve 50 50 50

Fixed assets (1,000) (1,000) (1,000)Net operating loss (state) 200 50 150 200Total DTA/(DTL) ($750) $100 ($850) $0 ($750)

Copyright © 2015 Deloitte Development LLC. All rights reserved. 7

Company has a gross DTA of $250, a gross DTL of $1,000 and a valuation allowance related to the state NOL carryforward of $100 as of the end of 20X1.• None of the state NOL carryforward is expected to reverse in 20X2.

Under the current guidance, the valuation allowance is allocated between the current DTA and the non-current DTA on a pro rata basis. No allocation is necessary under the proposed guidance because the entire DTA would be classified as non-current.

Balance sheet classification of DTA valuation allowancesCurrent and proposed accounting – example

Current guidance Proposed guidanceBalance sheet as of 12/31/20X1 DTA/(DTL) Current Non-current Current Non-

currentAccounts receivable –bad debt reserve 50 50 50

Fixed assets (1,000) (1,000) (1,000)Net operating loss (state) 200 200 200Valuation allowance (100)) (20) (80) (100)Net DTA/(DTL) ($850) $30 ($880) $0 ($850)

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 8

Question

SFAS 109 requires entities that prepare classified statements of financial position to separate deferred tax liabilities and assets into current and noncurrent amounts. Should entities reclassify the current portion of deferred tax liabilities or assets to current accounts, such as Account 174, Miscellaneous Current and Accrued Assets, or Account 242, Miscellaneous Current and Accrued Liabilities, for FERC accounting and financial reporting purposes?

ResponseNo. All deferred tax liabilities and assets shall be recorded in Accounts 190, 281, 282, or 283, as appropriate, and the current portion of those amounts shall not be reclassified to other accounts for FERC reporting purposes.

FERC guidanceAI93-5-000 — Accounting for Income Taxes16. CLASSIFICATION OF CURRENT PORTION OF DEFERRED INCOME TAXES

Copyright © 2015 Deloitte Development LLC. All rights reserved. 9

FERC guidance• All DTAs/DTLs are classified as non-current• DTAs and DTLs are not netted

ASC 740• A DTA or DTL related to a temporary difference with respect to an asset

or liability is classified as current or noncurrent based on the classification of the related asset or liability– If not related to an asset or liability, classify based on the expected reversal

date of the temporary difference• By taxing jurisdiction, report net current DTA or DTL and net non-current

DTA or DTL

FERC-GAAP difference• Reclassification of current portion of DTAs/DTLs and present net

DTAs/DTLs on a gross basis

Balance sheet classification of deferred taxesFERC-GAAP difference — current rules

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 10

FASB simplification initiative• Would classify all deferred taxes as non-current in a classified balance

sheet• Would eliminate the requirement to allocate a valuation allowance on a

pro rata basis between gross current and noncurrent DTAs

Would be consistent with the balance sheet presentation of deferred taxes under IFRS and FERC

Comment letters posted

Balance sheet classification of deferred taxesSummary

Copyright © 2015 Deloitte Development LLC. All rights reserved. 11

Eliminate prohibition on recognition of income taxes paid for intra-entity transactions and the related deferred tax asset on differences between the tax basis of the assets in a buyer’s tax jurisdiction and their cost as reported in the consolidated financial statements

The proposed Update would align the recognition of income tax consequences of intra-entity asset transfers with IFRS. • IAS 12, Income Taxes, requires recognition of current and deferred

income taxes resulting from an intra-entity asset transfer when the transfer occurs.

Intra-entity transfer of assets File Reference No. 2015-200

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 12

Transition guidance • Entities would be required to apply the proposed amendments on a

modified retrospective basis, with a cumulative-effect adjustment directly to retained earnings as of the beginning of the period of adoption for the recognition of the income tax consequences of intra-entity asset transfers occurring before the effective date.

Effective dates• Public business entities

– Annual periods, including interim periods within those annual periods, beginning after December 15, 2016

– Early adoption not permitted• All other entities

– One year later– Allowed to adopt early, but not before the effective date for public companies

and must adopt both issues if elect to early adopt

Intra-entity transfer of assets File Reference No. 2015-200 (cont.)

Copyright © 2015 Deloitte Development LLC. All rights reserved. 13

Historical guidance • ARB 51 and SFAS No. 109, paragraph 9(e)Current guidance• ASC 810-10-45-8 and ASC 740-10-25-3(e)Pending guidance• Proposed deletion of current ASC 740-10-25-3(e)

A prohibition on recognition of a deferred tax asset for the intra-entity difference between the tax basis of the assets in the buyer’s tax jurisdiction and their cost as reported in the consolidated financial statements. Income taxes paid on intra-entity profits on assets remaining within the group are accounted for under the requirements of Subtopic 810-10.

• Proposed additional example of a temporary difference in ASC 740-10-25-20

The difference between the tax basis of the asset in the buyer’s tax jurisdiction and the cost of the asset reported in the consolidated financial statements as a result of an intra-entity asset transfer from one taxpaying entity to another taxpaying entity of the same consolidated group.

Intra-entity transfer of assets Historical, current and pending guidance

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 14

Intra-entity transfer of assets Sale of inventory example – current rules

Parent

Sub A Sub BTax rate = 30% Tax rate = 40%

No DTA recorded pursuantto ASC 740-10-25-3(e)

Consolidated Financial StatementsPrepaid taxes $ 15DTA $ 0 Taxes payable ($ 15)Tax expense $ 0

Selling price $ 150Cost 100Margin $ 50Tax rate 30%Tax paid $ 15

Tax basis $ 150Book basis 100Difference – no DTA $ 50

Tax expense deferred(e.g., recorded as a prepaid)pursuant to ASC 810-10-45-8

Inventory

Copyright © 2015 Deloitte Development LLC. All rights reserved. 15

Intra-entity transfer of assets Sale of inventory example – pending guidance

Parent

Sub A Sub BTax rate = 30% Tax rate = 40%

DTA and deferred tax benefit recognized

Consolidated Financial StatementsDTA $ 20 Taxes payable ($ 15)Tax benefit ($ 5)

Selling Price $ 150Cost 100Margin $ 50Tax rate 30%Tax paid $ 15

Tax basis $ 150Book basis 100Difference $ 50DTA $ 20

Current tax expense recognized

Inventory

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 16

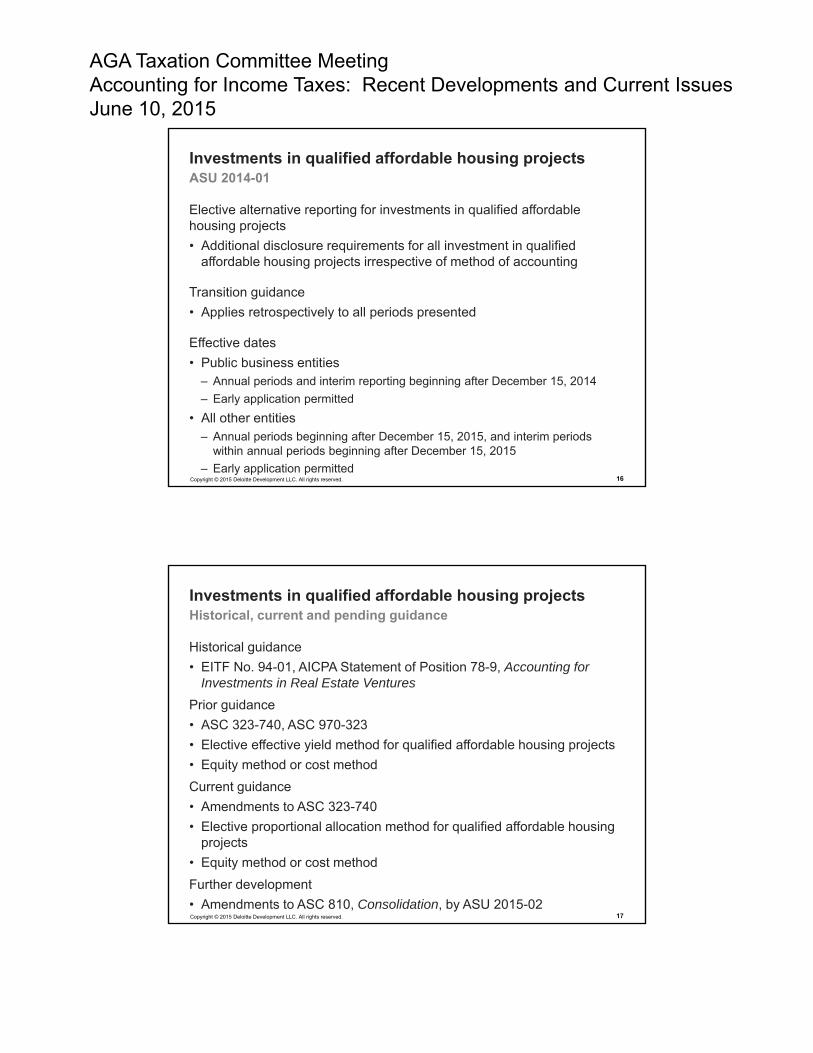

Elective alternative reporting for investments in qualified affordable housing projects• Additional disclosure requirements for all investment in qualified

affordable housing projects irrespective of method of accounting

Transition guidance • Applies retrospectively to all periods presented

Effective dates• Public business entities

– Annual periods and interim reporting beginning after December 15, 2014– Early application permitted

• All other entities– Annual periods beginning after December 15, 2015, and interim periods

within annual periods beginning after December 15, 2015– Early application permitted

Investments in qualified affordable housing projectsASU 2014-01

Copyright © 2015 Deloitte Development LLC. All rights reserved. 17

Historical guidance • EITF No. 94-01, AICPA Statement of Position 78-9, Accounting for

Investments in Real Estate VenturesPrior guidance• ASC 323-740, ASC 970-323• Elective effective yield method for qualified affordable housing projects• Equity method or cost methodCurrent guidance• Amendments to ASC 323-740• Elective proportional allocation method for qualified affordable housing

projects• Equity method or cost methodFurther development• Amendments to ASC 810, Consolidation, by ASU 2015-02

Investments in qualified affordable housing projectsHistorical, current and pending guidance

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 18

ASU 2014-01 amends ASC 323-740 to expand the scope of theexception originally provided by EITF 94-1 to report the pretax lossfrom investments in certain affordable housing projects as part of thetax provision and to modify the allocation of the cost of the investment

Report pretax loss fromqualified investments as part of the income tax provision

Prior GuidanceEffective yield method

Amortize initial cost of investment to provide a constant effective yield over the period that the tax credits are allocated to the investor

Current GuidanceProportional amortization method

General – amortize initial cost of investment to in proportion to the tax credits and other benefits allocated to the investorPractical expedient – amortize initial cost of investment in proportion to the tax credits allocated to the investor

Elective reporting for qualified investments

Income (loss) before taxes (Loss)

Income taxes (Tax benefit)

Income (loss) Income

Investments in qualified affordable housing projects — summaryASU 2014-01

Copyright © 2015 Deloitte Development LLC. All rights reserved. 19

Prior requirements –for effective yield method

New requirements –for proportional amortization method

The availability (but not necessarily the realization) of the tax credits to the investor is guaranteed by creditworthy entity through a letter of credit, a tax indemnity agreement, or another similar arrangement

It is probable (higher threshold thanMLTN) that the tax credits allocable to theinvestor will be available

Not applicable The investor does not have the ability toexercise significant influence over theoperating and financial policies of the limited liability entity

Not applicable Substantially all of the projected benefitsare from tax credits and other tax benefits(e.g., tax benefits from operating losses of the investment)

The investor’s projected yield based solely on cash flows from guaranteed tax credits is positive

The investor's projected yield basedsolely on the cash flows from the taxcredits and other tax benefits is positive(no guarantee required)

The investor is a limited partner in the affordable housing project for both legal and tax purposes and the investor’s liability is limited to its capital investment

The investor is a limited liability investorin the limited liability entity for bothlegal and tax purposes, and the investor’s liability is limited to its capitalinvestment (same as prior requirement)

Criteria for elective alternative “net” income tax accountingInvestments in qualified affordable housing projects

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 20

EITF 94-1 – The SEC Observer commented that the SEC staff believesthat it would be inappropriate to extend the effective yield method ofaccounting to analogous situations

ASU 2014-01 – The Task Force also discussed whether the scope of the amendments in this Update should be extended to tax credit investments other than investments in qualified affordable housing projects. . . . The Task Force reached a consensus to limit the scope of the amendments in this Update to only investments in qualified affordable housing projects because it will more quickly address the concerns in practice about the income statement presentation of those investments.

What about “similar investments”?Proportional amortization method

Copyright © 2015 Deloitte Development LLC. All rights reserved. 21

A reporting entity that invests in a qualified affordable housing project shall disclose information that enables users of its financial statements to understand the following:• The nature of its investments in qualified affordable housing projects• The effect of the measurement of its investments in qualified affordable

housing projects and the related tax credits on its financial position and results of operations

Investments in qualified affordable housing projectsDisclosure requirements – ASC 323-740-50-1

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 22

To meet the objectives in the preceding paragraph, a reporting entity may consider disclosing the following:• The amount of affordable housing tax credits and other tax benefits

recognized during the year• The balance of the investment recognized in the statement of financial

position• Proportional amortization method – the amount recognized as a

component of income tax expense (benefit)• Equity method – the amount of investment income or loss included in

pretax income• Any commitments or contingent commitments including the amount of

equity contributions that are contingent commitments and the year or years in which contingent commitments are expected to be paid

• The amount and nature of impairment losses during the year resulting from the forfeiture or ineligibility of tax credits or other circumstances

Investments in qualified affordable housing projectsDisclosure considerations – ASC 323-740-50-2

Copyright © 2015 Deloitte Development LLC. All rights reserved. 23

August 2014 – the FAF issued its PIR Report on Statement 123(R), Share-Based Payment

October 2014 – the FASB added a project to improve the accounting for share-based payment to employees in the following areas:• Withholding requirements• Presentation in the statement of cash flows• Accounting for forfeitures• Accounting for income taxes

Exposure draft expected in the second quarter of 2015

FASB employee share-based payment accounting improvements project

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 24

Accounting for income taxes upon vesting or settlement of awards• The Board proposed excess tax benefits and deficiencies be recognized

in the income statement. – Prospective transition method

• The Board also decided to remove the requirement to delay recognition of an excess tax benefit until the tax benefit is realized.– Modified retrospective transition method with a cumulative-effect adjustment

recognized in equity

Presentation of excess tax benefits on the statement of cash flows• The Board decided to remove the requirement that employers present

excess tax benefits as a cash inflow from financing activities and a cash outflow from operating activities.– Retrospective transition method

FASB employee share-based payment project Accounting for income tax aspects – tentative decisions

Copyright © 2015 Deloitte Development LLC. All rights reserved. 25

Common differences between the methods used for financial reporting of income taxes and for regulatory accounting of income taxes• Balance sheet presentation of DTAs and DTLs

– Current vs. non-current– Gross vs. netting

• Uncertain tax positions– Classification of tax-related interest– Classification of liabilities related to temporary differences

• Separate company financial statements• Income tax allowances ‒ rate-regulated partnerships

FERC-GAAP reporting differencesSummary of income tax reporting issues

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 26

Issues – in what account(s) should the following tax receivables be recorded?• IRS settlement results in a refund to be received• Overpayment of estimated taxes to be applied to next year’s taxes• Overpayment of estimated taxes to be settled through tax-sharing

agreement

Considerations• Is the account included in rate base?

– Formula rate templates

FERC audits – finding and recommendations

FERC reportingTax receivables – overpayments and refunds

Copyright © 2015 Deloitte Development LLC. All rights reserved. 27

Relevant accounts• 143 Other accounts receivable• 165 Prepayments• 236 Taxes accrued

FERC 2014 Report on Enforcement (Docket No. AD07-13-008)• Division of Audits and Accounting (DAA) continues to examine

accounting that populates formula rate recovery mechanisms used in determining billings to wholesale customers. In recent formula rate audits, DAA observed certain patterns of noncompliance in the following areas:– Tax Prepayments – incorrectly recording tax overpayments not applied to a

future tax year’s obligation as a prepayment leading to excess recovery through working capital

FERC reportingTax receivables – overpayments and refunds

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 28

AI07-2-000, Accounting and Financial Reporting for Uncertainty in Income Taxes• Classification of interest and penalties• Classification as current vs. non-current• Temporary items ‒ impact of gross vs. net presentation

Uncertain tax positionsOverview of FERC guidance

Copyright © 2015 Deloitte Development LLC. All rights reserved. 29

ASC 740-10-45-25 provides that classification of interest (and penalties) is an accounting policy• Disclosure of accounting policy per ASC 740-10-50-19• Disclosure of amounts per ASC 740-10-50-15c

Balance sheet classification should be consistent with income statement classification

Tax-related interest is accounted for under ASC 740 regardless of the classification of interest

Classification of tax-related interestGAAP

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 30

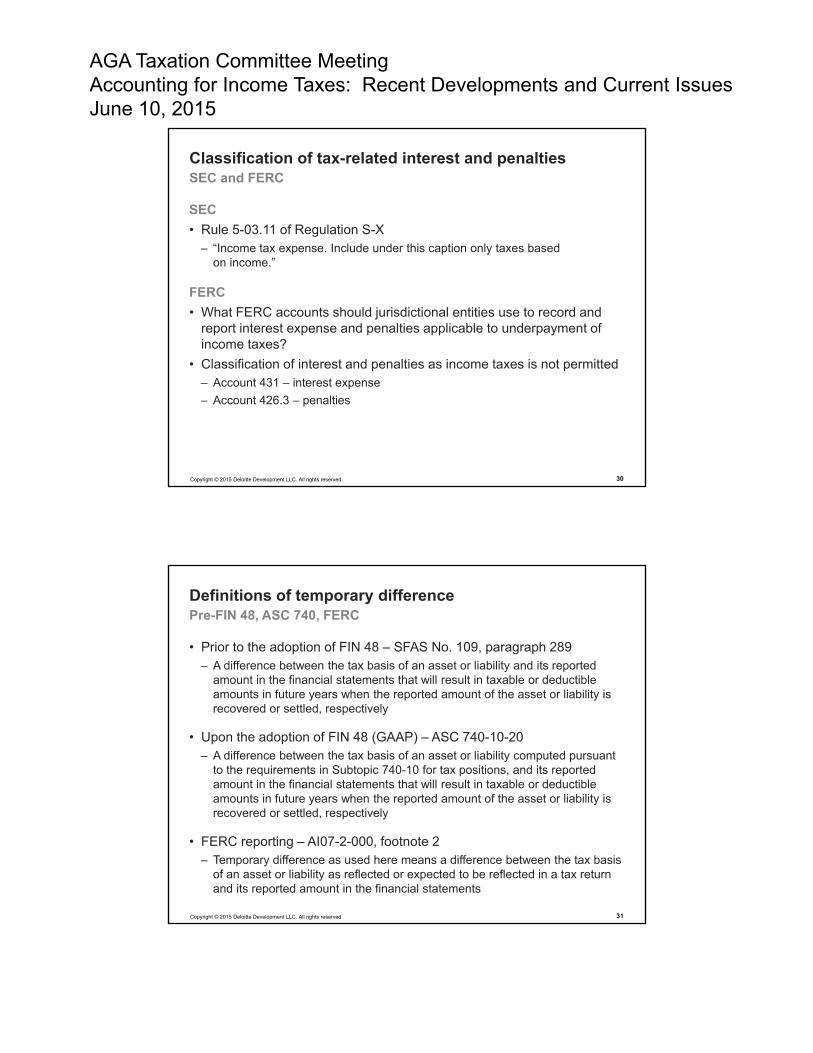

SEC• Rule 5-03.11 of Regulation S-X

– “Income tax expense. Include under this caption only taxes based on income.”

FERC• What FERC accounts should jurisdictional entities use to record and

report interest expense and penalties applicable to underpayment of income taxes?

• Classification of interest and penalties as income taxes is not permitted– Account 431 ‒ interest expense– Account 426.3 ‒ penalties

Classification of tax-related interest and penaltiesSEC and FERC

Copyright © 2015 Deloitte Development LLC. All rights reserved. 31

• Prior to the adoption of FIN 48 ‒ SFAS No. 109, paragraph 289– A difference between the tax basis of an asset or liability and its reported

amount in the financial statements that will result in taxable or deductible amounts in future years when the reported amount of the asset or liability is recovered or settled, respectively

• Upon the adoption of FIN 48 (GAAP) ‒ ASC 740-10-20– A difference between the tax basis of an asset or liability computed pursuant

to the requirements in Subtopic 740-10 for tax positions, and its reported amount in the financial statements that will result in taxable or deductible amounts in future years when the reported amount of the asset or liability is recovered or settled, respectively

• FERC reporting ‒ AI07-2-000, footnote 2– Temporary difference as used here means a difference between the tax basis

of an asset or liability as reflected or expected to be reflected in a tax return and its reported amount in the financial statements

Definitions of temporary differencePre-FIN 48, ASC 740, FERC

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 32

ASC 740• Liabilities associated with UTBs should be classified as current liabilities

to the extent that payment (or receipt) of cash is anticipated within one year

• Consider the reversal of temporary differences in accordance with the original filing position in the subsequent tax year

• UTB liabilities should not be combined with deferred tax liabilities and must be netted against deferred tax assets in certain specified circumstances

FERC guidance• Continue to treat temporary differences as non-current deferred taxes,

even those that are payable within 12 months

Unrecognized tax benefitsClassification

Copyright © 2015 Deloitte Development LLC. All rights reserved. 33

Temporary items ‒ impact of gross vs. net presentation• Certain aspects of FIN 48, if not implemented in accordance with the

guidance contained herein, could reduce the usefulness of income tax data for ratemaking purposes and or otherwise be inconsistent with existing Commission accounting requirements

• Therefore, Commission jurisdictional entities should implement FIN 48 for Commission accounting and reporting purposes, but in doing so should comply with the guidance set forth below

Unrecognized tax benefitsClassification – FERC guidance

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 34

How should jurisdictional entities account for unrecognized tax benefits related to temporary differences for Commission and reporting purposes?• Recognition of a separate liability for any uncertainty related to

temporary differences is therefore not necessary because the entity has already recorded a deferred tax liability for the item or would be entitled to record a deferred tax asset for the item if a separate liability for the uncertainty was recognized

• This practice results in the accumulated deferred income tax accounts reflecting an accurate measurement of the cash available to the entity as a result of temporary differences– This is an important measurement objective of the Commission’s Uniform

Systems of Account because accumulated deferred income tax balances, which are significant in amount for most Commission jurisdictional entities, reduce the base on which cost-based, rate-regulated entities are permitted to earn a return

Uncertain tax positions — temporary differencesFERC guidance

Copyright © 2015 Deloitte Development LLC. All rights reserved. 35

UTB (or portion of a UTB) is presented as a reduction to the DTA for a net operating loss carryforward, a similar tax loss, or tax credit carryforward unless tax law prohibits settlement with NOL/tax credit (or tax law does not require use of the carryforward and entity does not intend to offset)• ASC 740-10-45-10A, 10B

Effective date and transition• Prospective application to any UTBs that exist as of effective date

– Public companies – interim and annual periods beginning after December 15, 2013

– Non-public companies – interim and annual periods beginning after December 15, 2014

• Retrospective application permitted; early adoption permitted

Presentation of UTB when attribute DTAs existASU 2013-11 issued July 18, 2013

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 36

Tax rates• 35% federal rate, 5% state rate, 38.25% composite statutory rate• Federal benefit of deduction of state income taxes = 1.75%

Uncertain income tax positions• Eligibility for a federal credit – no impact on deductions or basis• Timing of deduction of repair expenditures

Gross vs. net presentation of UTBs – GAAP v. FERCExample – facts

Tax positionGross

amount

Federal tax

benefit reported (gross)

State tax benefit

reported (gross)

Federal benefit of deduction

of state income

tax

Net benefit per tax return

Federal credit 100 100 100Repairs 2,614 915 131 (46) 1,000

Copyright © 2015 Deloitte Development LLC. All rights reserved. 37

Assumes no NOL or credit carryforward

Gross vs. net presentation of UTBs – GAAP v. FERCExample – reporting of liabilities

GAAP reporting FERC reporting

Tax position

Liability for UTB(federal

and state –gross)

DTL (federal

and state –gross)

Federal DTA for

state UTB

liability or DTL

Liability for UTB

DTL (federal

and state –gross)

Federal DTA for

state UTB

liability or DTL

Federal credit (100) (100)Repairs (1,046) 46 (1,046) 46Total (1,146) 46 (100) (1,046) 46

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 38

Assumes $13,072 NOL carryforward for federal and state purposes• $5,000 net DTA

– $4,575 federal DTA, $654 state DTA, $229 federal DTL (on state DTA)

Gross vs. net presentation of UTB liabilities with NOLsExample – reporting of liabilities before and after ASU 2013-11

Acceptable beforeASU 2013-11

Acceptable before and after ASU 2013-11

Tax position

Liability for UTB(federal

and state –gross)

DTA or (DTL)

(federal and

state –gross)

Federal DTA or (DTL)

for state

liability or asset

Liability for UTB(federal

and state –gross)

DTA or (DTL)

(federal and

state –gross)

Federal DTA or (DTL)

for state

liability or asset

Federal credit (100) NettedRepairs (1,046) 46 Netted 46NOL carryforward 5,229 (229) 4,083 (229)Total (1,146) 5,229 (183) 4,083 (183)

Copyright © 2015 Deloitte Development LLC. All rights reserved. 39

Assumes $13,072 NOL carryforward for federal and state purposes• $5,000 net DTA

– $4,575 federal DTA, $654 state DTA, $229 federal DTL (on state DTA)

Gross vs. net presentation of UTB liabilities with NOLsExample – reporting of liabilities – after ASU 2013-11 – GAAP v. FERC

GAAP FERC

Tax positionLiability for UTB

DTA or (DTL)

(federal and

state –gross)

Federal DTA or (DTL)

for state

liability or asset

Taxes accrued (liability

for UTB)

DTA or (DTL)

(federal and

state –gross)

Federal DTA or (DTL)

for state

liability or asset

Federal credit Netted (100)Repairs Netted 46 (1,046) 46NOL carryforward 4,083 (229) 5,229 (229)Total 4,083 (183) (100) 4,183 (183)

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 40

Disclosures — tabular rollforwardExample

TotalState,perm,

credits

Temp items

Unrecognized tax benefits, opening balance $XX $AA $BB

Gross increases ‒ tax positions in prior periods XX AA BB

Gross decreases ‒ tax positions in prior periods (XX) (AA) (BB)

Gross increases ‒ current period tax positions XX AA BB

Settlements (XX) (AA) (BB)

Lapse of statute of limitations (XX) (AA) (BB)

Unrecognized tax benefits, ending balance $XX $AA $BB

Use in Form10-K

Use in FERC Form No. 1

Note: This annual disclosure is not required during interim periods, but quarterly MD&A disclosure of (de)recognition of material amounts may be required

Copyright © 2015 Deloitte Development LLC. All rights reserved. 41

Special Instructions – Accounts 409.1, 409.2 and 409.3

B. The accruals for income taxes shall be apportioned among utility departments and to Other Income and Deductions so that, as nearly as practicable, each tax shall be included in the expenses of the utility department or Other Income and Deductions, the income from which gave rise to the tax. The tax effects relating to Interest Charges shall be allocated between utility and nonutility operations. The basis for this allocation shall be the ratio of net investment in utility plant to net investment in nonutility plant.

FERC reportingTax benefit related to interest expense

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 42

Instructions to Statement of Income for the Year• 13. Enter on page 122 a concise explanation of only those changes in

accounting methods made during the year which had an effect on net income, including the basis of allocations and apportionments from those used in the preceding year. Also, give the appropriate dollar effect of such changes.

• Pages 122-123 = Notes to Financial Statements

FERC audit report – findings and recommendations

FERC reportingChanges in tax methods of accounting

Copyright © 2015 Deloitte Development LLC. All rights reserved. 43

In general, the book/tax differences arising from implementation of the tangible property regulations regarding capitalization are unprotected basis differences• Not subject to the Section 168 deferred tax normalization requirements

Accounting method changes to implement the tangible property regulations regarding dispositions are subject to the deferred tax normalization requirements• Public utility commission notification requirements in Rev. Proc. 2015-

14 for 16 method changes related to depreciation or dispositions

Significance of historical deferred tax accounting and ratemaking policies

Proposals to normalize Section 481(a) adjustments (cumulative catch-up adjustments) associated with implementing the regulations or safe harbor guidance but flowing through ongoing tax benefits

Tangible property regulationsNormalization v. flowthrough of deferred tax expense

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 44

(2) Adjustments to reserve

(i) The taxpayer must credit the amount of deferred Federal income tax determined under subparagraph (l)(i) of this paragraph for any taxable year to a reserve for deferred taxes, a depreciation reserve, or other reserve account. The taxpayer need not establish a separate reserve account for such amount but the amount of deferred tax determined under subparagraph (l)(i) of this paragraph must be accounted for in such a manner so as to be readily identifiable. With respect to any account, the aggregate amount allocable to deferred tax under section 167(l) shall not be reduced except to reflect the amount for any taxable year by which Federal income taxes are greater by reason of the prior use of different methods of depreciation under subparagraph (l)(i) of this paragraph. An additional exception is that the aggregate amount allocable to deferred tax under section 167(l) may be properly adjusted to reflect asset retirements or the expiration of the period for depreciation used in determining the allowance for depreciation under section 167(a).

Normalization method of accounting Adjustments to reserve – Reg. Sec. 1.167(l)-1(h)(2)

Copyright © 2015 Deloitte Development LLC. All rights reserved. 45

As of the beginning of the year of change, the taxpayer will adjust its deferred tax reserve account or similar account in the taxpayer’s regulatory books of account by the amount of the deferral of federal income tax liability associated with the Section 481(a) adjustment applicable to the public utility property subject to the application

Within 30 calendar days of filing the federal income tax return for the year of change, the taxpayer will provide a copy of the completed application to any regulatory body having jurisdiction over the public utility property subject to the application.• Public utility commission notification requirement for 16 of the listed

automatic accounting method changes

Adjustments to DTLs for Section 481(a) adjustmentsRev. Proc. 2015-14

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 46

Books Tax Temp. Diff. DTL (40%)

Original cost 1,000 1,000

<Acc. Dep.> <200> <500>

Adjusted basis 800 500 300 120 normalized

481(a) adjustment - <500> 500 200 Eligible for FT

Adjusted basis 800 0 800 320

What’s the journal entry to record the additional DTL?Regulatory Asset 333 Complies with

the normalization requirements

533Deferred Tax Liability (account 282) 200 200Deferred Tax Liability (account 283) 133 May not comply

with the normalization

requirements

213Deferred Tax Benefit 120

Tangible property regulationsFlowthrough accounting example

Copyright © 2015 Deloitte Development LLC. All rights reserved. 47

Use of ASC 740-270 forecasted annual tax rates• Fiscal year test periods• Interim period regulatory reporting

Allocation of total interim period tax provision between current and deferred components

Estimating changes in deferred tax assets/liabilities

Interim period tax provisionsDiscussion topics

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

Copyright © 2015 Deloitte Development LLC. All rights reserved. 48

Copyright © 2015 Deloitte Development LLC. All rights reserved. 49

This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

AGA Taxation Committee MeetingAccounting for Income Taxes: Recent Developments and Current Issues June 10, 2015

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2015 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu Limited