AGA Kansas City Chapter Professional Development Seminar Kansas School Finance: Formula and Trends...

42

AGA Kansas City Chapter Professional Development Seminar Kansas School Finance: Formula and Trends Mark Tallman Associate Executive Director Kansas Association of School Boards November 16, 2015

-

Upload

amie-austin -

Category

Documents

-

view

256 -

download

0

Transcript of AGA Kansas City Chapter Professional Development Seminar Kansas School Finance: Formula and Trends...

AGA Kansas City ChapterProfessional Development Seminar

Kansas School Finance:Formula and Trends

Mark TallmanAssociate Executive Director

Kansas Association of School Boards

November 16, 2015

Why is school finance important?• 2015 Kansas Legislature abolished previous formula, replaced

with “block grant” system for two years.• Legislative Special Committee on K-12 Student Success

appointed; working on new system.• Kansas Supreme Court hearing state appeals of lower court

rulings current system is unconstitutional.• K-12 funding receives 50% of state general fund budget as

revenue projections continue to drop; $185 million deficit projected next year.

• K-12 total funding equal 4.5% of Kansas economy.• Linked to outcomes: education levels key to economic growth

and security.

Recent history of KS school finance

• 1966 – people adopt current education article.• Directs Legislature to establish a system of public schools to

promote intellectual, educational, vocational and scientific improvement.

• Elected state board of education for “general supervision” of public schools; appointed board of regents for higher ed.

• Local public schools to be “maintained, developed and operated by local elected boards.”

• Makes Legislature responsible for “suitable provision for finance” of the educational interests of the state.

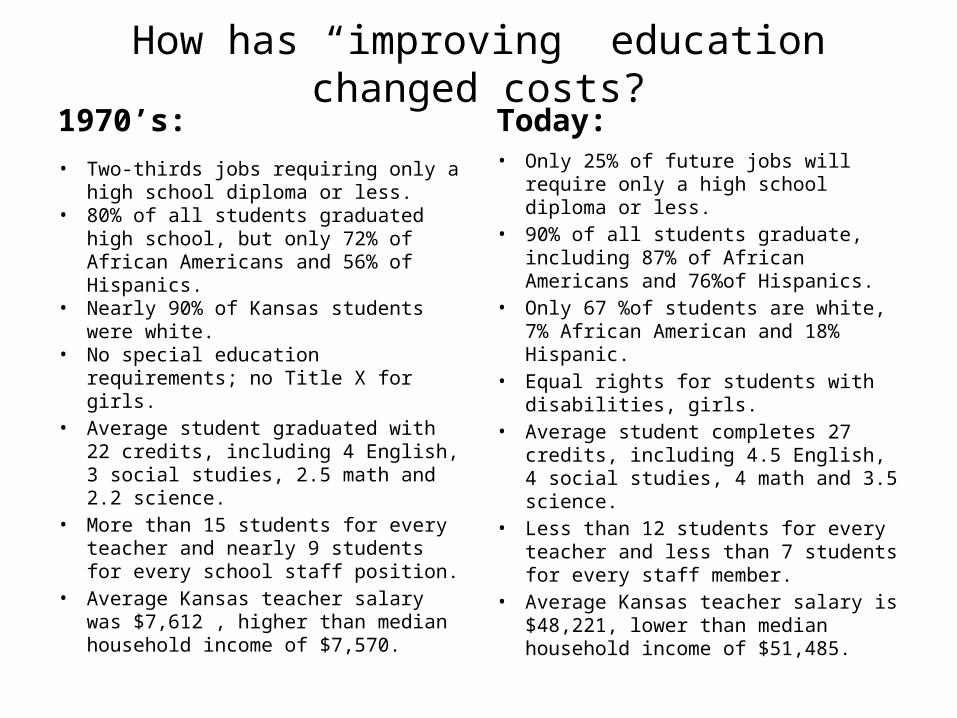

How has “improving” education changed costs?1970’s:• Two-thirds jobs requiring only a high

school diploma or less.• 80% of all students graduated high

school, but only 72% of African Americans and 56% of Hispanics.

• Nearly 90% of Kansas students were white.

• No special education requirements; no Title X for girls.

• Average student graduated with 22 credits, including 4 English, 3 social studies, 2.5 math and 2.2 science.

• More than 15 students for every teacher and nearly 9 students for every school staff position.

• Average Kansas teacher salary was $7,612 , higher than median household income of $7,570.

Today:• Only 25% of future jobs will require

only a high school diploma or less.• 90% of all students graduate,

including 87% of African Americans and 76%of Hispanics.

• Only 67 %of students are white, 7% African American and 18% Hispanic.

• Equal rights for students with disabilities, girls.

• Average student completes 27 credits, including 4.5 English, 4 social studies, 4 math and 3.5 science.

• Less than 12 students for every teacher and less than 7 students for every staff member.

• Average Kansas teacher salary is $48,221, lower than median household income of $51,485.

Recent history of KS school finance

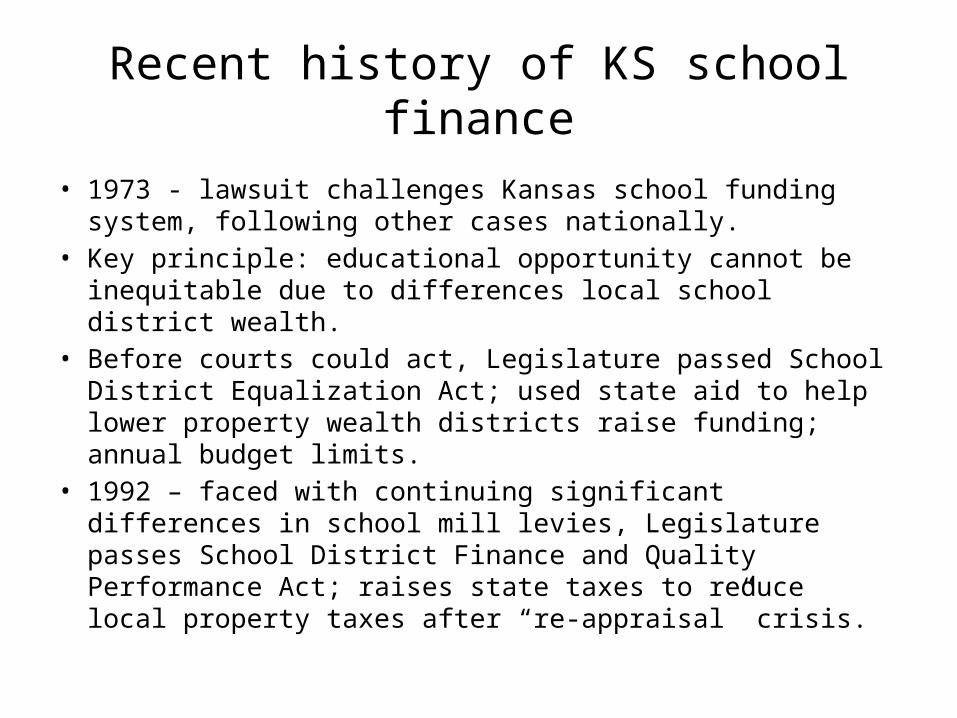

• 1973 - lawsuit challenges Kansas school funding system, following other cases nationally.

• Key principle: educational opportunity cannot be inequitable due to differences local school district wealth.

• Before courts could act, Legislature passed School District Equalization Act; used state aid to help lower property wealth districts raise funding; annual budget limits.

• 1992 – faced with continuing significant differences in school mill levies, Legislature passes School District Finance and Quality Performance Act; raises state taxes to reduce local property taxes after “re-appraisal” crisis.

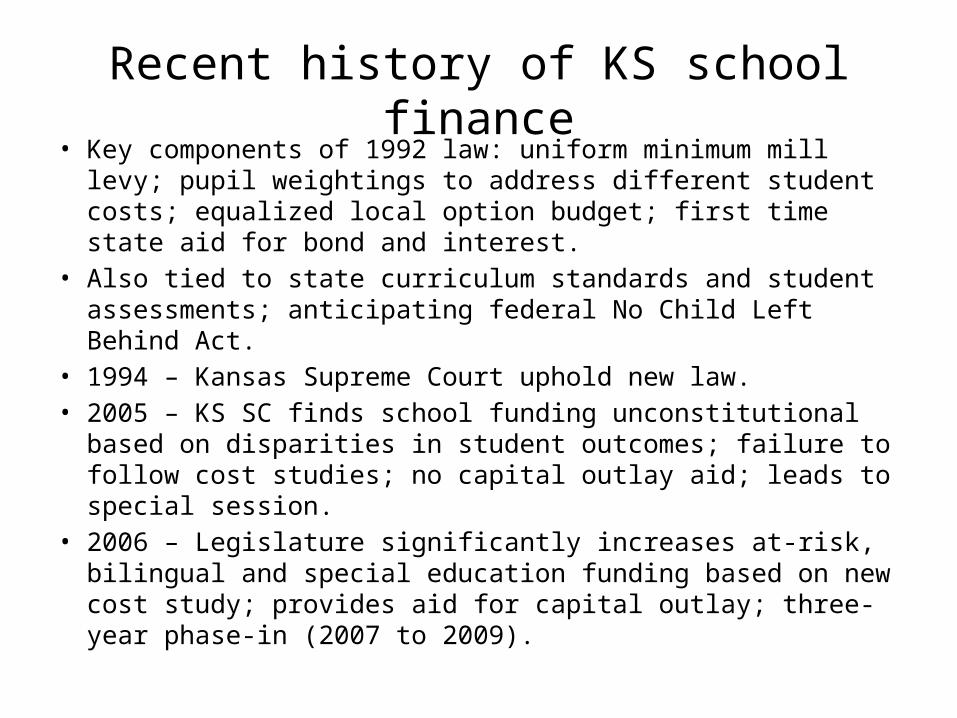

Recent history of KS school finance• Key components of 1992 law: uniform minimum mill levy;

pupil weightings to address different student costs; equalized local option budget; first time state aid for bond and interest.

• Also tied to state curriculum standards and student assessments; anticipating federal No Child Left Behind Act.

• 1994 – Kansas Supreme Court uphold new law.• 2005 – KS SC finds school funding unconstitutional based on

disparities in student outcomes; failure to follow cost studies; no capital outlay aid; leads to special session.

• 2006 – Legislature significantly increases at-risk, bilingual and special education funding based on new cost study; provides aid for capital outlay; three-year phase-in (2007 to 2009).

Recent history of KS school finance• 2009 – Great recession reduces state revenues, leads to cuts

in school aid far below Montoy “settlement;” school districts file Gannon lawsuit.

• 2014 – KS SC agrees with panel that KS funding in inequitable; orders reconsideration of “adequacy” based on new standard.

• Legislature approves $130 million to fully fund local option budget and capital outlay aid; courts approve.

• 2015 – Legislature learns it will require additional $50 million to fund formulas (and USD budgets) ; instead, changes formulas to reduce cost and creates two-year block grants system to essentially “freeze” budgets for 2016 and 2017.

• Panel orders Legislature to pay the additional funding and reverse block grants; Supreme Court hearing was Nov. 6.

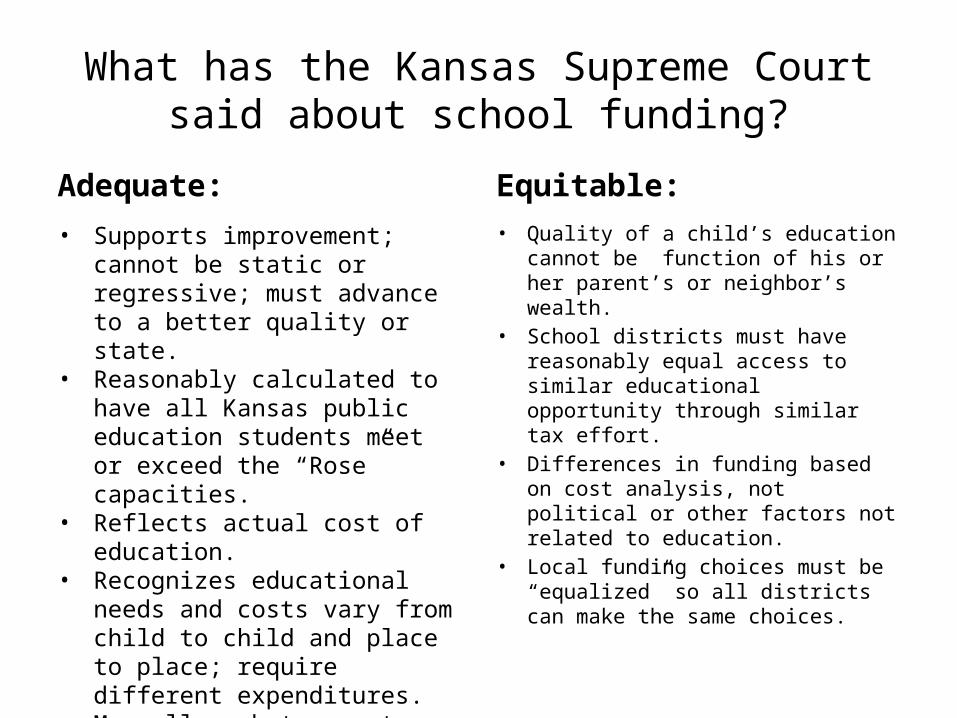

What has the Kansas Supreme Court said about school funding?

Adequate:• Supports improvement; cannot be

static or regressive; must advance to a better quality or state.

• Reasonably calculated to have all Kansas public education students meet or exceed the “Rose” capacities.

• Reflects actual cost of education.• Recognizes educational needs and

costs vary from child to child and place to place; require different expenditures.

• May allow, but cannot reply on, local funding choices.

Equitable:• Quality of a child’s education cannot

be function of his or her parent’s or neighbor’s wealth.

• School districts must have reasonably equal access to similar educational opportunity through similar tax effort.

• Differences in funding based on cost analysis, not political or other factors not related to education.

• Local funding choices must be “equalized” so all districts can make the same choices.

What are the “Rose” capacities?• Oral and written communication skills to enable students to function in a

complex and rapidly changing civilization;• Knowledge of economic, social, and political systems to enable the

student to make informed choices;• Understanding of governmental processes to enable the student to

understand the issues that affect his or her community, state, and nation;

• Self knowledge and knowledge of his or her ‐ mental and physical wellness;

• Grounding in the arts to enable each student to appreciate his or her cultural and historical heritage;

• Training or preparation for advanced training in either academic or vocational fields so as to enable each child to choose and pursue life work intelligently; and

• Academic or vocational skills to enable public school students to compete favorably with their counterparts in surrounding states, in academics or in the job market.

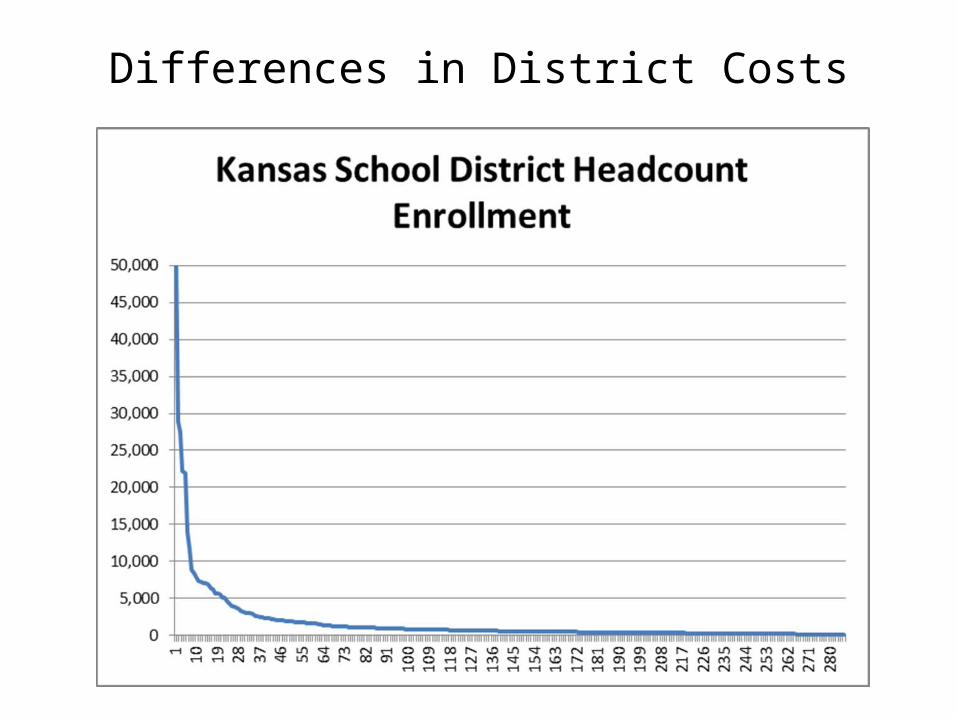

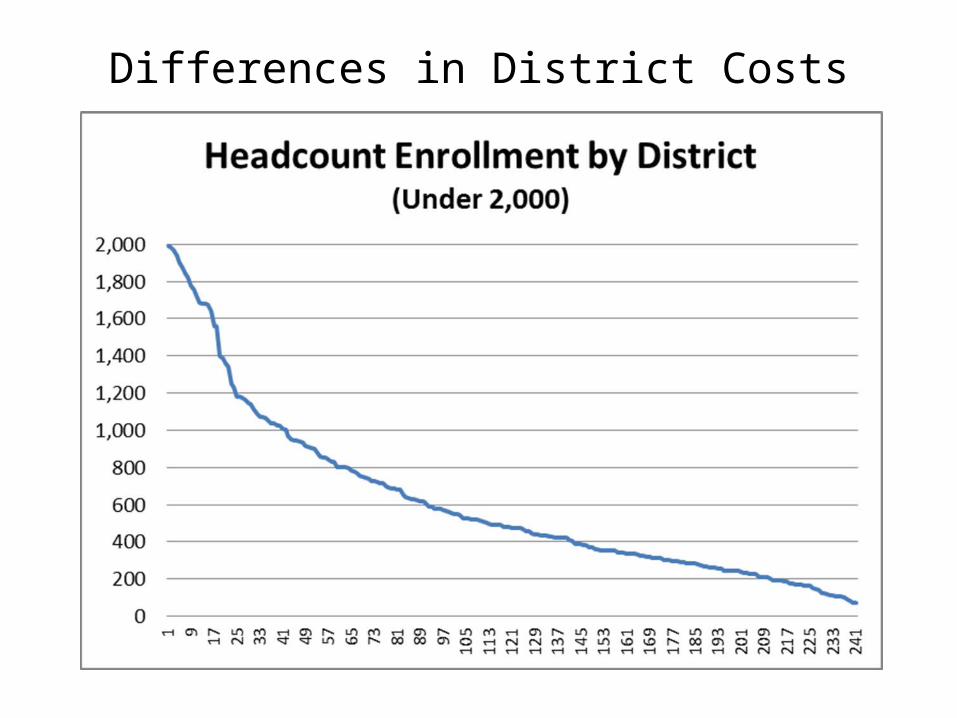

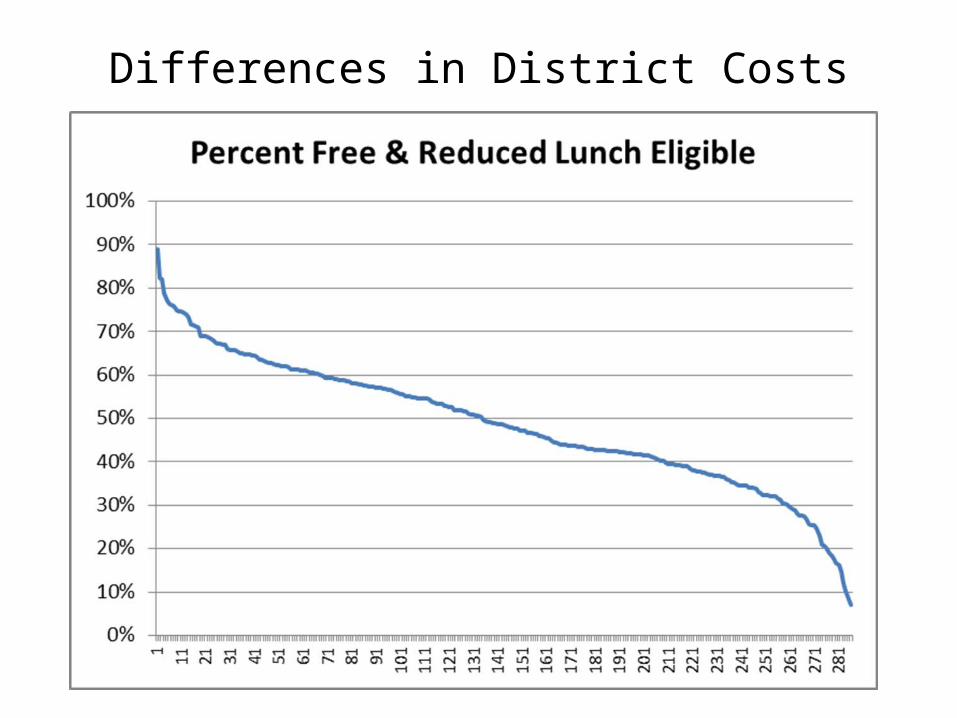

Differences in District Costs

Differences in District Costs

Differences in District Costs

Differences in District Costs

Differences in District Costs

Differences in District Costs

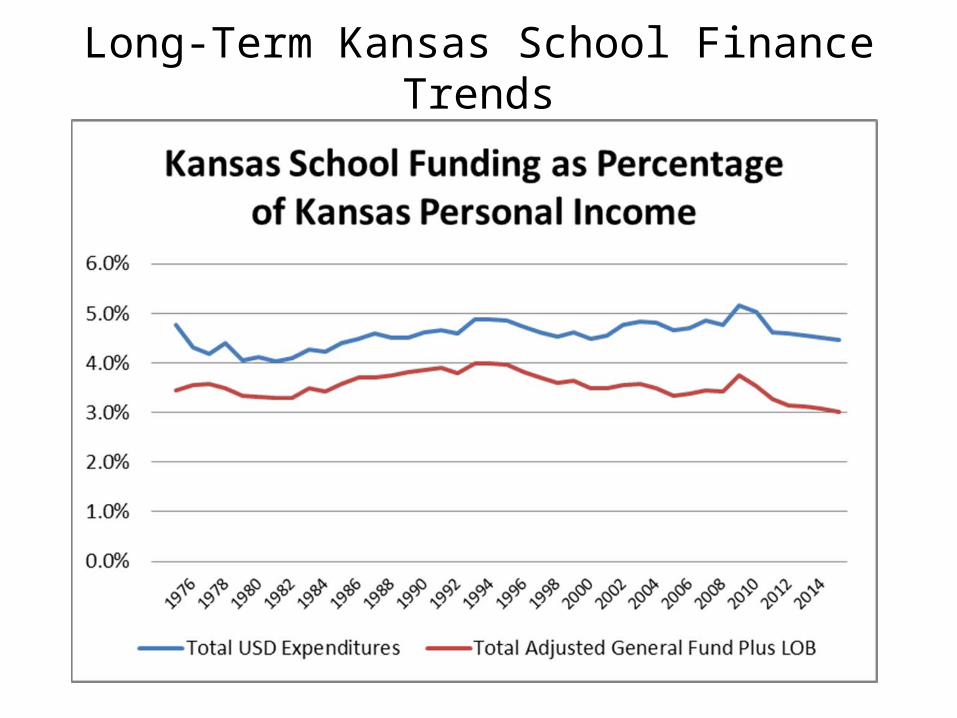

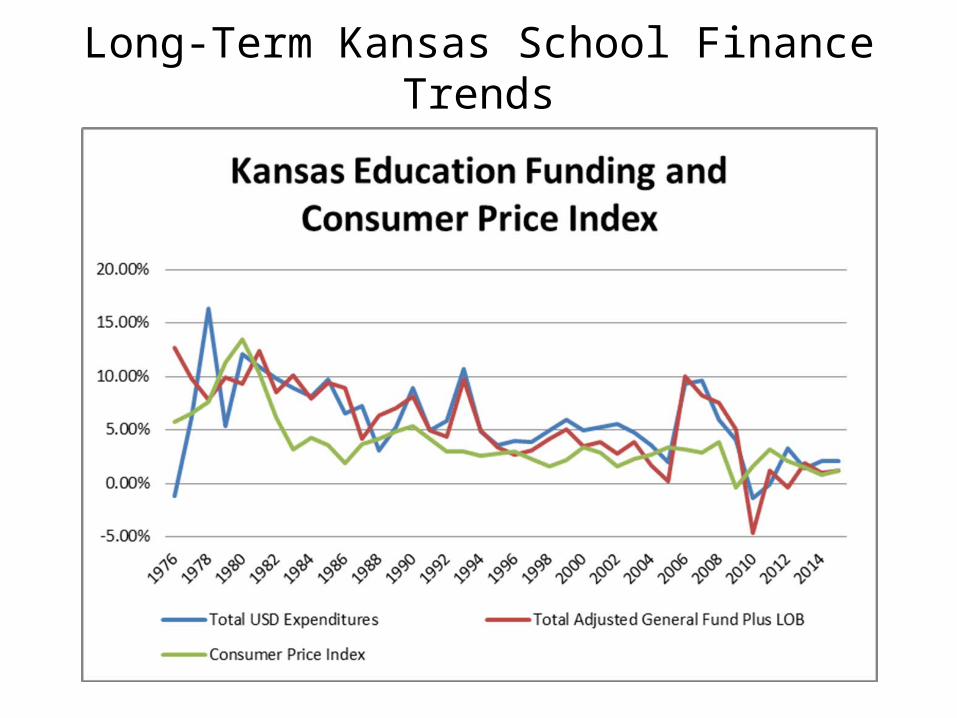

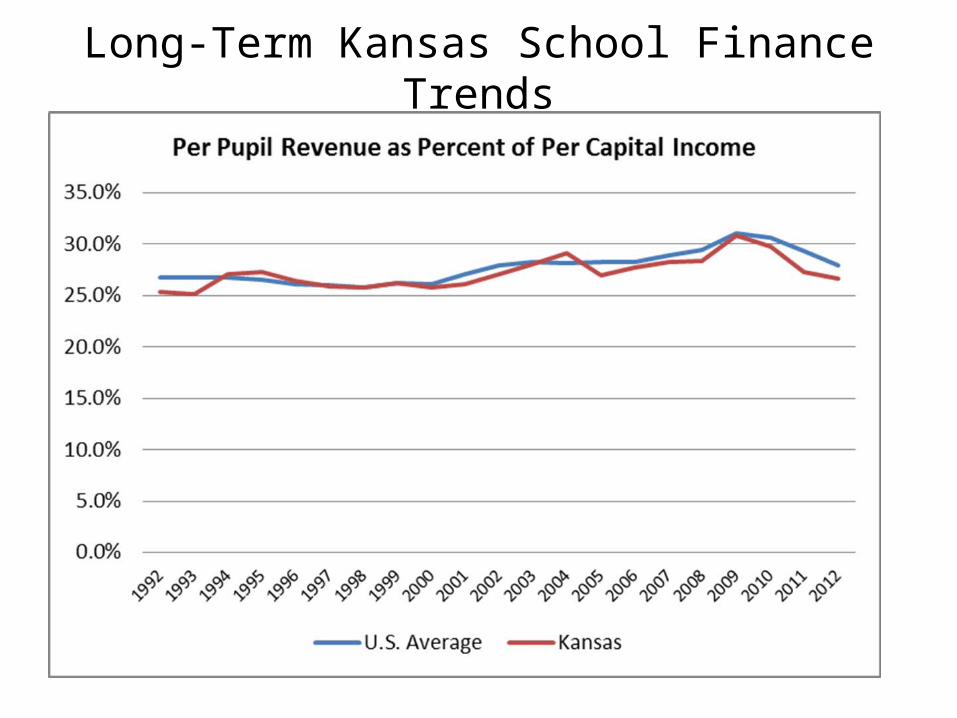

Long-Term Kansas School Finance Trends

Long-Term Kansas School Finance Trends

Long-Term Kansas School Finance Trends

Long-Term Kansas School Finance Trends

Long-Term Kansas School Finance Trends

Long-Term Kansas School Finance Trends

Long-Term Kansas School Finance Trends

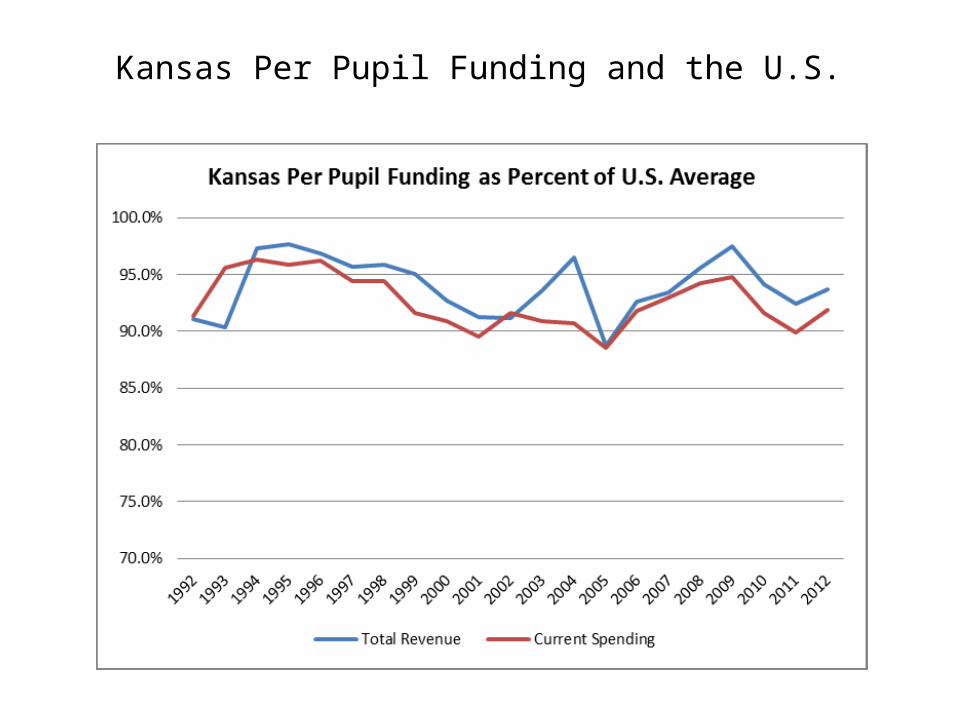

Kansas Per Pupil Funding and the U.S.

Kansas and U.S. Per Pupil Revenue

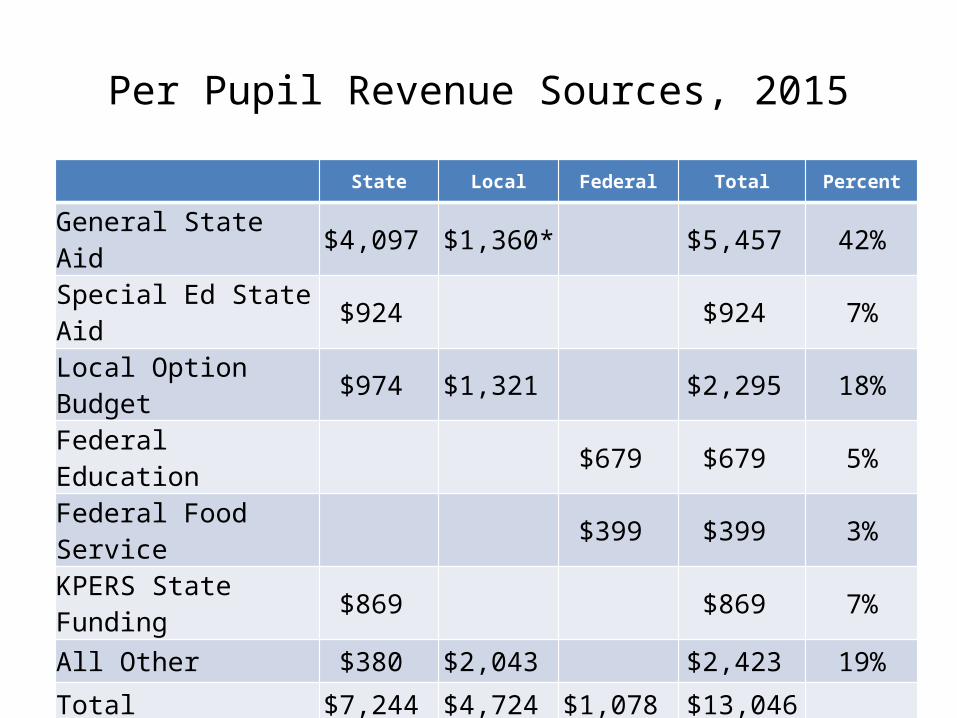

Per Pupil Revenue Sources, 2015

State Local Federal Total Percent

General State Aid $4,097 $1,360* $5,457 42%

Special Ed State Aid $924 $924 7%

Local Option Budget $974 $1,321 $2,295 18%

Federal Education $679 $679 5%

Federal Food Service $399 $399 3%

KPERS State Funding $869 $869 7%

All Other $380 $2,043 $2,423 19%

Total $7,244 $4,724 $1,078 $13,046

Percent 55.5% 36.2% 8.3%

*20 mill levy now sent to state, redistributed as state aid

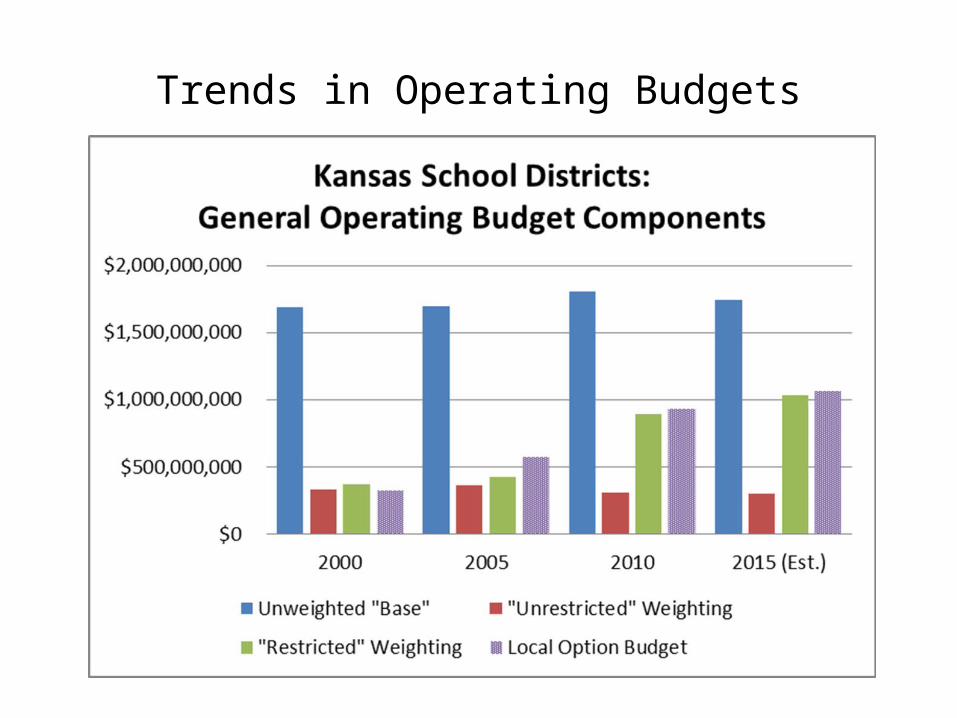

Trends in Operating Budgets

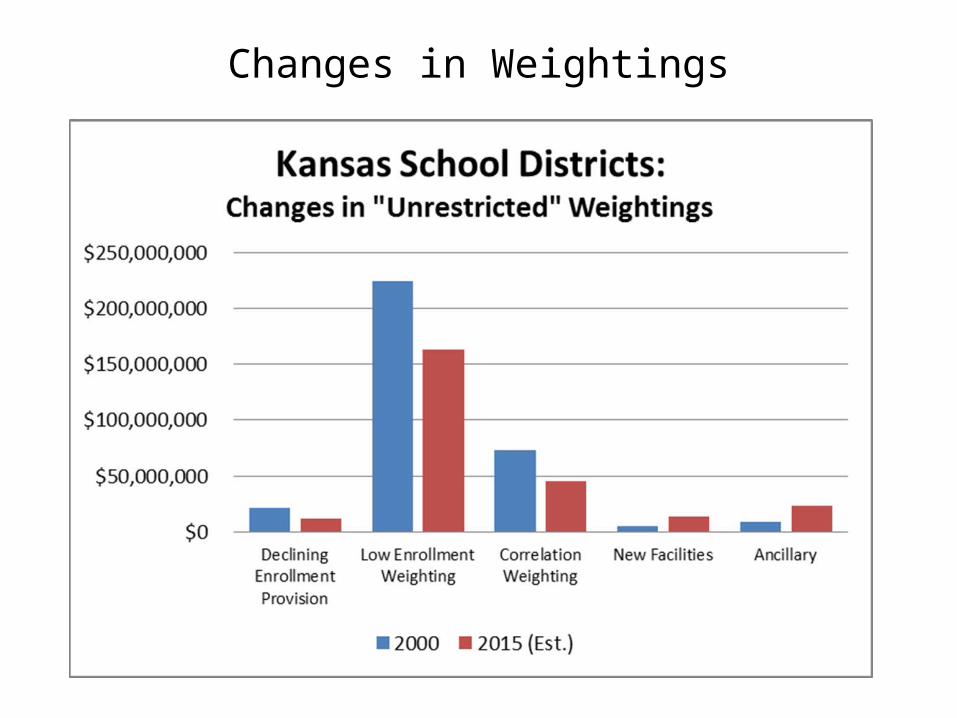

Changes in Weightings

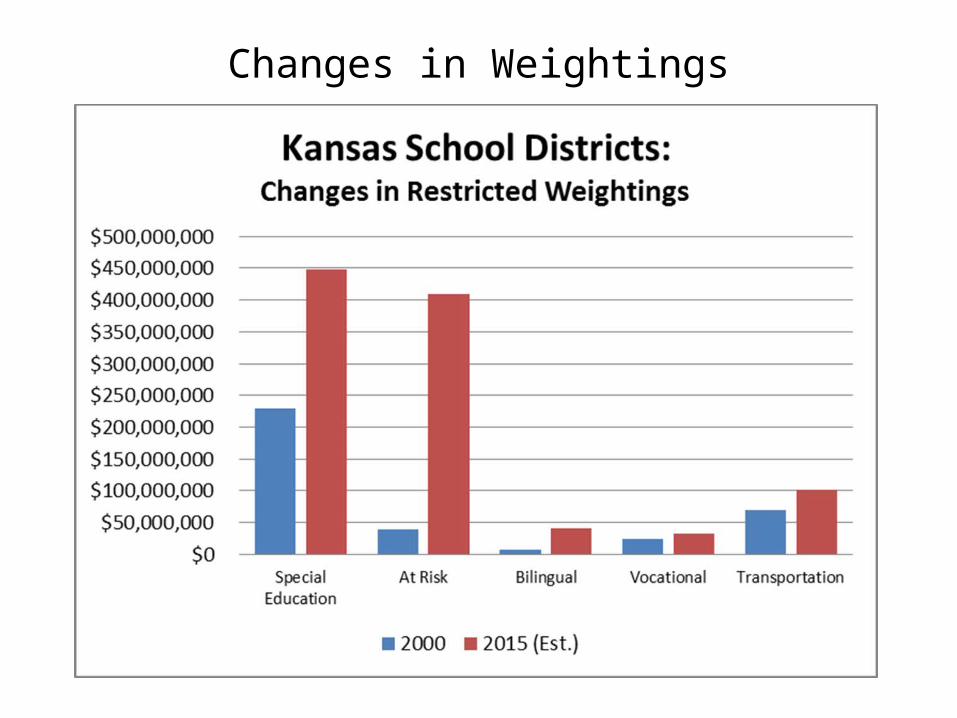

Changes in Weightings

Economic ImpactKansas Personal Income (Millions)

Previous Estimates

Annual Change New Esimates

Annual Change

2010 $110,956,678 1.03% $110,956,678 1.03%2011 $120,801,179 8.87% $120,801,179 8.87%2012 $125,168,000 3.61% $126,189,704 4.46%2013 $128,541,000 2.69% $128,314,517 1.68%2014 $132,267,000 2.90% $130,364,095 1.60%2015 $136,764,078 3.40% $134,796,474 3.40%2016 $142,781,697 4.40% $140,727,519 3.90%2017 $149,064,092 4.40% $146,919,530 4.20%

Reduction for 2017: $2,144,562 Average percent for K-12, 1990-15 (4.72%) $101,223

Economic Impact

Kansas Personal Income Consumer Price Index0%

1%

2%

3%

4%

5%

6%

Economic Indicators

1990-2008 2009-2017

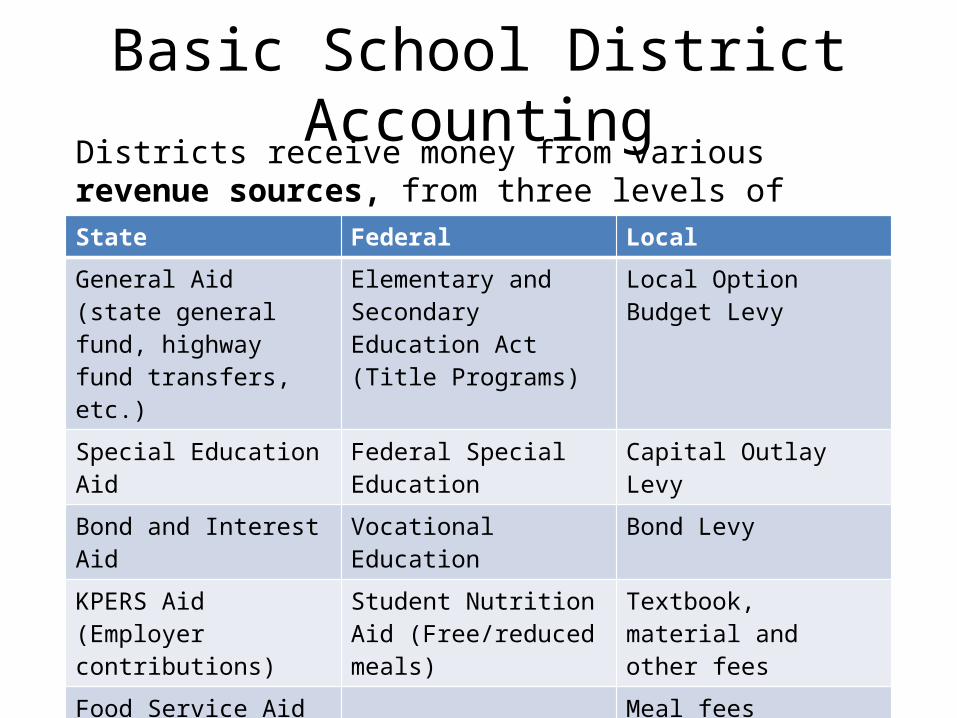

Basic School District AccountingDistricts receive money from various revenue sources, from three levels of government.State Federal Local

General Aid (state general fund, highway fund transfers, etc.)

Elementary and Secondary Education Act (Title Programs)

Local Option Budget Levy

Special Education Aid Federal Special Education Capital Outlay Levy

Bond and Interest Aid Vocational Education Bond Levy

KPERS Aid (Employer contributions)

Student Nutrition Aid (Free/reduced meals)

Textbook, material and other fees

Food Service Aid Meal fees

Other State Grants Other local revenues

Note: 20 mills is levied locally but send to the state and re-appropriated as general state aid. Kansas Supreme Court held this to be a state levy in the 1990s.

Basic School District AccountingExpenditures by revenue source at KSDE.org>Agency>Fiscal and Administrative Service>Budget Information page. Go down the page to USD Expenditure Reports, click on “Total Expenditures by District and Per Pupil” for each district and state totals. http://www.ksde.org/Default.aspx?tabid=428

Basic School District AccountingMoney received goes into various funds. In some cases, the fund is required; in other cases the district has a choice.

Limited by Mill Levies

Other Effectively Limited Funds SB 111 and other Operating Funds

Capital Outlay Federal Funds Special Education* Bilingual* Cost of Living

Bond & Interest 1 Gifts/Grants Textbook* Vocational Ed.* Ancillary

Bond & Interest 2 School Retire. Contingency Reserve*

Parents As Teachers*

Tuition Reimbursement

Special Liability Special Reserve Virtual Ed.* Driver Training* Activities

No Fund Warrants Special Education Co-op Prof. Develop.* Summer School* Extraordinary

School

Special Assess. Food Service At Risk (4yr Old)* Supp. General Area Vocational

Adult Education General Fund** At Risk (K-12)* Declining Enroll. Adult Supp. Ed.

*Districts may transfer SB 111 for other purposes.**Districts may not carry a balance in the general fund.

Basic School District AccountingCash balances by funds at KSDE.org>Agency>Fiscal and Administrative Service> School Finance>Reports and Publications page. Go down the page to “Cash Balances July 1.” Click on school year. For 2015-16, go to: http://www.ksde.org/Portals/0/School%20Finance/reports_and_publications/CashBalance/CASH%20BAL%207-1-2015.xlsx

Basic School District Accounting• Money is spend from funds for various purposes or functions.

These functions are defined by the federal government for reporting purposes.

1000 INSTRUCTION includes the activities dealing directly with the interaction between teachers and students, including sports and activities.* 2000 SUPPORT SERVICES provide support to facilitate and enhance instruction, including transportation.* 3000 OPERATION OF NON-INSTRUCTIONAL SERVICES provide non-instructional services to students, staff, or the community, including food service operations, enterprise operations (such as bookstores) and community services (such as recreation, public library, and historical museum).*4000 FACILITIES ACQUISITION AND CONSTRUCTION include acquiring land and buildings; remodeling buildings; constructing buildings and additions to buildings; initially installing or extending service systems and other built-in equipment; and improving sites.5000 DEBT SERVICE is servicing the long-term debt of the school district, including payments of both principal and interest for bond interest payments, retirement of bonded debt, capital lease payments and other long-term notes. *Generally, these functions are Current Operating Expenditures

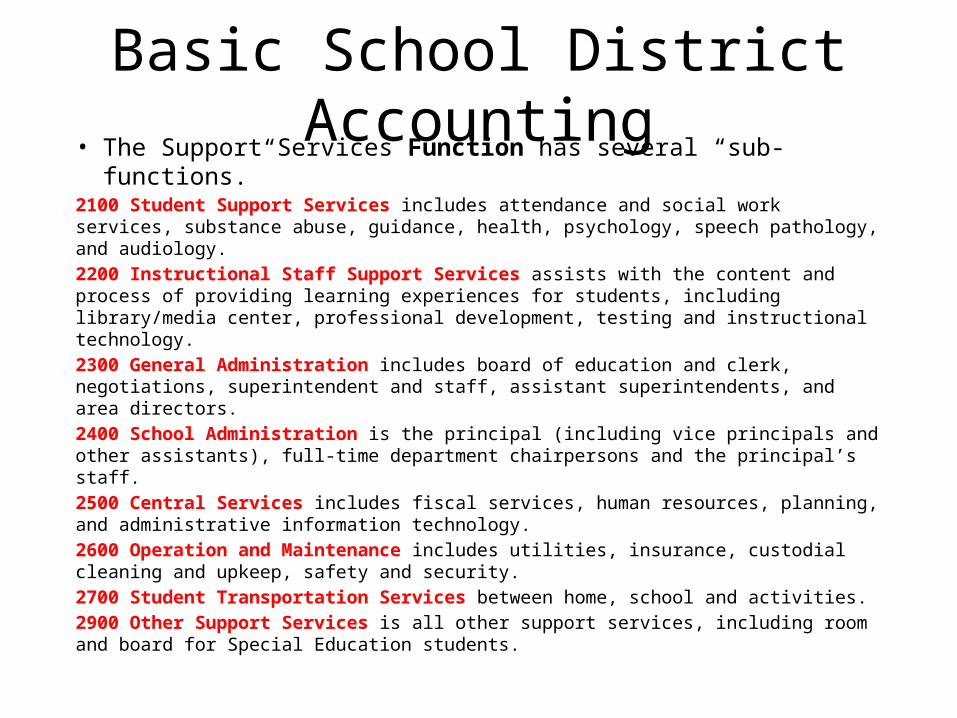

Basic School District Accounting• The Support Services Function has several “sub-functions.”2100 Student Support Services includes attendance and social work services, substance abuse, guidance, health, psychology, speech pathology, and audiology.2200 Instructional Staff Support Services assists with the content and process of providing learning experiences for students, including library/media center, professional development, testing and instructional technology. 2300 General Administration includes board of education and clerk, negotiations, superintendent and staff, assistant superintendents, and area directors. 2400 School Administration is the principal (including vice principals and other assistants), full-time department chairpersons and the principal’s staff.2500 Central Services includes fiscal services, human resources, planning, and administrative information technology.2600 Operation and Maintenance includes utilities, insurance, custodial cleaning and upkeep, safety and security.2700 Student Transportation Services between home, school and activities.2900 Other Support Services is all other support services, including room and board for Special Education students.

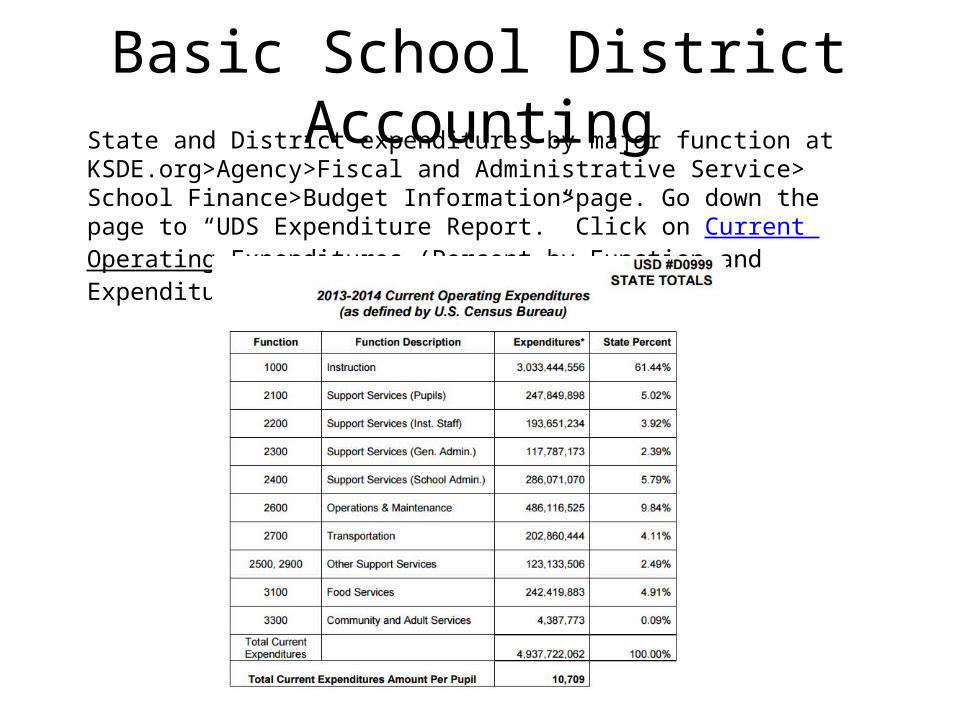

Basic School District AccountingState and District expenditures by major function at KSDE.org>Agency>Fiscal and Administrative Service> School Finance>Budget Information>page. Go down the page to “UDS Expenditure Report.” Click on Current Operating Expenditures (Percent by Function and Expenditures Per Pupil).

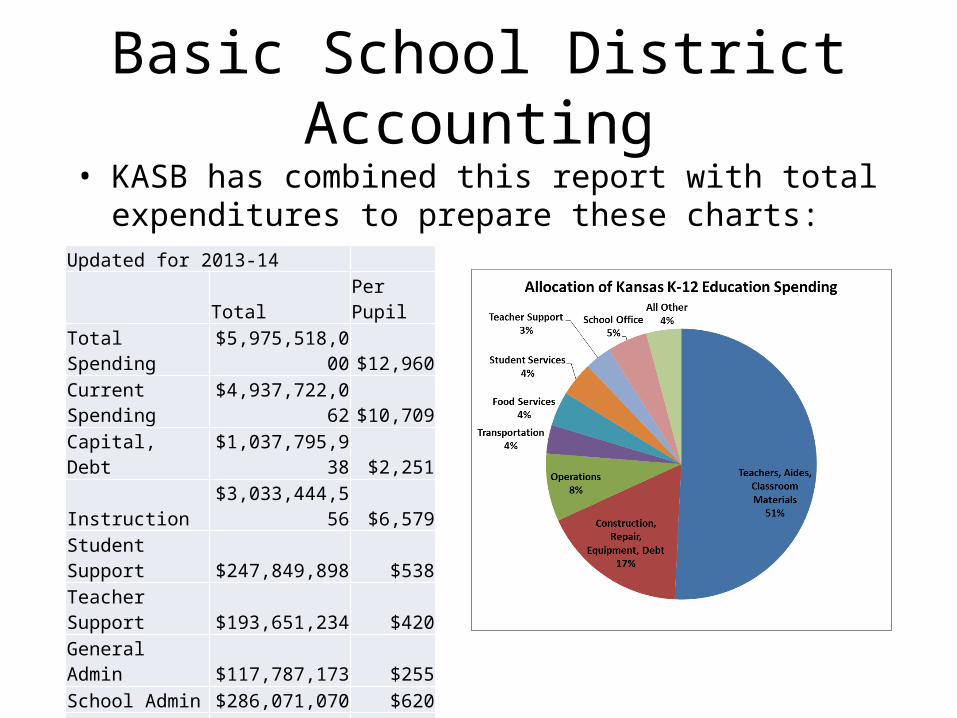

Basic School District Accounting• KASB has combined this report with total expenditures to

prepare these charts:Updated for 2013-14

Total Per PupilTotal Spending $5,975,518,000 $12,960Current Spending $4,937,722,062 $10,709Capital, Debt $1,037,795,938 $2,251Instruction $3,033,444,556 $6,579Student Support $247,849,898 $538Teacher Support $193,651,234 $420General Admin $117,787,173 $255School Admin $286,071,070 $620Operations & M $486,116,525 $1,054Transportation $202,860,444 $440Other Support $123,133,506 $267Food Services $242,419,883 $526Adult & Com Serv $4,387,773 $10

Basic School District Accounting• Finally, money spent from each fund, for each function, is actually spend on

various objects.100 PERSONAL SERVICES - SALARIES –gross salary for personal services rendered.200 EMPLOYEE BENEFITS – Amounts paid on behalf of but not to employees.300 PURCHASED PROFESSIONAL AND TECHNICAL SERVICES – Specialized services of architects, engineers, auditors, dentists, medical doctors, lawyers, consultants, teachers, accountants, etc. not employed by the district.400 PURCHASED PROPERTY SERVICES – Services purchased to operate, repair, maintain, and rent property owned or used by the district, performed by persons other than district employees.500 OTHER PURCHASED SERVICES – Amounts paid for services rendered by organizations or personnel not on the payroll of the district other than Professional and Technical Services or Property Services).600 SUPPLIES – Items that are consumed, worn out, or deteriorated through use. 700 PROPERTY – Expenditures for acquiring fixed assets, including land or existing buildings; improvements of grounds; initial equipment; additional equipment; and replacement of equipment.800 DEBT SERVICE AND MISCELLANEOUS – Items not otherwise classified above.900 OTHER ITEMS (APPROPRIATED FUNDS ONLY)

Basic School District Accounting• Obviously, despite what

some say, there IS a uniform school district accounting system – following federal standards.

• However, districts decide which specific accounting program or software to use – not a single state system.

• Districts only report “high level” data to the state – much more detail is available locally, but not required.

Handbook link: http://www.ksde.org/Portals/0/School%20Finance/guidelines_manuals/Accounting%20Handbook.pdf

School Finance PrioritiesUSA/KASB • Every student in Kansas public

schools will have an equal opportunity to be college and career ready as defined by the Rose Standards.

• Some students will require greater supports to meet (the Rose) standards.

• Legislature and school districts need budgeting predictability.

• Meets constitutional requirements for equity and adequacy.

• Local control and flexibility of funding educational services.

Legislative Leaders• Focus on students and reward

good teachers.• New reporting system for school

spending – focus on “cost centers.”• Policies on cash reserves.• Limit cost of capital expenditures.• Basis of at-risk funding.• Reduce federal role.• Success indicators – definition and

funding.• Delivery of high cost programs.• Administrative realignment.