AEM 4160 April 28, 2015 COFFEE SHOP INDUSTRY Kyle Brumm | Sarah Le Cam | Zach Leighton | Stephanie...

40

AEM 4160 April 28, 2015 COFFEE SHOP INDUSTRY Kyle Brumm | Sarah Le Cam | Zach Leighton | Stephanie Ou

-

Upload

beryl-fields -

Category

Documents

-

view

216 -

download

1

Transcript of AEM 4160 April 28, 2015 COFFEE SHOP INDUSTRY Kyle Brumm | Sarah Le Cam | Zach Leighton | Stephanie...

AEM 4160April 28, 2015

COFFEE SHOP INDUSTRY

Kyle Brumm | Sarah Le Cam | Zach Leighton | Stephanie Ou

AGENDA

Background

Competitive Landscape

Industry Organization

Major Competitors

Pricing Strategies

Raw Data Analysis

Recommendations

WHY COFFEE?

Introduction Industry Pricing Strategies

Recommendations

Millions of Americans on a daily

basis

Several innovative changes in the past 20

years

Customers are more

sophisticated,

knowledgeable

INDUSTRY STRUCTURE

Retail coff ee industry $28 billion in revenue in the United States Two major categories

At-home Direct sale

Industry at a Glance – Coff ee & Snack Shops Revenue +$12bn from coffee shops Businesses +22,000 coffee shops

INDUSTRY BACKGROUND

Introduction Industry Pricing Strategies

Recommendations

KEY DRIVERS

Introduction Industry Pricing Strategies

Recommendations

• Consumer Spending

• Health Consciousness

• Increased Consumer Confidence

• Growth of Consumption

EXTERNAL• Clear Market

Position

• Effective Cost Controls

• Ability to Franchise

• High-Profile Locations

• Multiskilled Workforce

INTERNAL

CUSTOMER BASE

Introduction Industry Pricing Strategies

Recommendations

Four Firm Concentration Ratio

58.3 Highly concentrated at

the top

Top 20 players control 70% of the coffee shop market

INDUSTRY COMPETITION

Introduction Industry Pricing Strategies

Recommendations

Threat of New Entrants MODERATE

Threat of Substitutes HIGH

Bargaining Power of Buyers LOW/MODERATE

Bargaining Power of Suppliers LOW/MODERATE

Intensity of Competitive RivalryHIGH/MODERATE

PORTER’S FIVE FORCES

Introduction Industry Pricing Strategies

Recommendations

INDUSTRY ORGANIZATION

Introduction Industry Pricing Strategies

Recommendations

SUPPLY CHAIN

Introduction Industry Pricing Strategies

Recommendations

CoffeeFarm

Factory forWashing

Freight &Transportati

on

Factory forProcessing

Factory for

Roasting

CoffeeBar

Consumers

1 2 3 4

5 6 7

FAIR TRADE

• Support local, small-scale farmers• Long-term sustainability• Links farmers directly with importers

MAJOR PLAYERS

Revenue (2014)$16.5bn

US Stores: 7,303

Ithaca LocationsDowntown/CommonsCollegetown Ithaca MallCampus Dining

STARBUCKS CORPORATION

Introduction Industry Pricing Strategies

Recommendations

Revenue (2014)$748 million

US Stores: 8,047

Ithaca LocationsDowntown/CommonsEast Hill PlazaCollegetown (May ‘15)

DUNKIN’ BRANDS

Introduction Industry Pricing Strategies

Recommendations

LOCAL COMPETITORS – ITHACA MARKET

Introduction Industry Pricing Strategies

Recommendations

Collegetown BagelsCollegetown

Downtown/CommonsEast Hill Plaza

Gimme! CoffeeCollegetown

Downtown/Commons (2)[Other locations in New York State]

Stella’s CafeCollegetown

Manndible CafeCornell Campus

PRICING STRATEGIES &

RAW DATA ANALYSIS

Off ers products at diff erent prices Regular drinks (coffee, iced coffee, latte) – CHEAP Specialty drinks (cappuccino, mocha) – EXPENSIVE

Who can engage in this?Example: Starbucks in the Recession

Lowered the price of regular drinks ($0.05 - $0.15) Increased the price of premium drinks (+$0.30)

PREMIUM PRICING

Introduction Industry Pricing Strategies

Recommendations

$2.58

Iced Coffee (16 oz)

$2.10

Coffee (16 oz)

$4.23

Mocha (16 oz)

PREMIUM PRICING

Introduction Industry Pricing Strategies

Recommendations

PREMIUM PRICING

Introduction Industry Pricing Strategies

Recommendations

PREMIUM PRICING

Introduction Industry Pricing Strategies

Recommendations

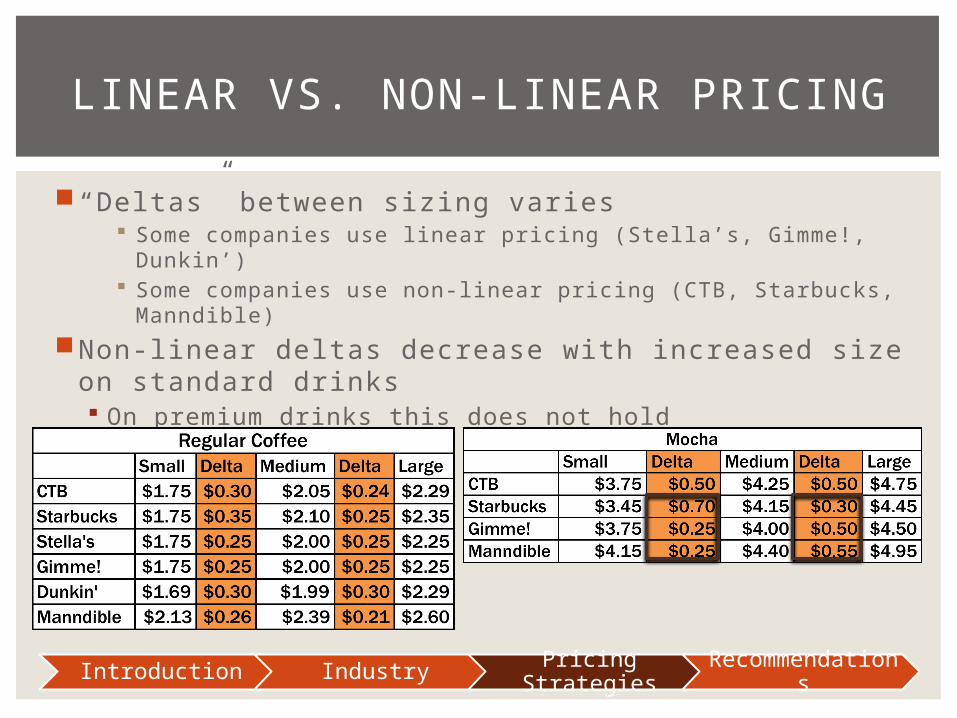

“Deltas” between sizing varies Some companies use linear pricing (Stella’s, Gimme!, Dunkin’) Some companies use non-linear pricing (CTB, Starbucks,

Manndible)

Non-linear deltas decrease with increased size on standard drinks On premium drinks this does not hold

LINEAR VS. NON-LINEAR PRICING

Introduction Industry Pricing Strategies

Recommendations

LINEAR VS. NON-LINEAR PRICING

Introduction Industry Pricing Strategies

Recommendations

LINEAR VS. NON-LINEAR PRICING

Introduction Industry Pricing Strategies

Recommendations

LINEAR VS. NON-LINEAR PRICING

Introduction Industry Pricing Strategies

Recommendations

More coff ee More time

Cold brewing technique

Greater expenses Plastic cups more expensive

than paper cups Use of straws Condensation leads to more

napkins per customer

HOT BREWED VS. ICED COFFEE

Introduction Industry Pricing Strategies

Recommendations

Small CTB Starbucks Stella'sHot $0.15 $0.15 $0.15Iced $0.14 $0.19 $0.19

% Difference -3.6% 28.6% 28.6%

Medium CTB Starbucks Stella'sHot $0.11 $0.12 $0.11Iced $0.10 $0.15 $0.14

% Difference -11.3% 25.5% 22.2%

Large CTB Starbucks Stella'sHot $0.13 $0.13 $0.13Iced $0.10 $0.17 $0.16

% Difference -18.7% 26.2% 25.0%

Punch cardsDiscount for using own

mug Increases customer

loyalty

CUSTOMER LOYALTY DISCOUNTS

Introduction Industry Pricing Strategies

Recommendations

GIMME! VS. MANNDIBLE CAFE

Introduction Industry Pricing Strategies

Recommendations

Gimme! 8 oz $1.75 12 oz $2.00 16 oz $2.25

Manndible 12 oz $2.13 16 oz $2.39 20 oz $2.60

GIMME! VS. MANNDIBLE CAFE

Introduction Industry Pricing Strategies

Recommendations

Off er small, medium, and large (and even extra large) options Starbucks – Trenta (30 oz) Dunkin Donuts – XL (24 oz)

Allows customers to self selectAdd-ons / Substitutes

2ND DEGREE PRICE DISCRIMINATION

Introduction Industry Pricing Strategies

Recommendations

Collegetown Bagels

3RD DEGREE PRICE DISCRIMINATION

Introduction Industry Pricing Strategies

Recommendations

Coffee Collegetown Commons East Hill Plaza12 oz $1.75 $1.75 $1.7516 oz $2.05 $2.05 $2.0520 oz $2.29 $2.29 $2.29

Iced Coffee Collegetown Commons East Hill Plaza16 oz $2.25 $1.94 $2.2524 oz $2.50 $2.42 $2.5032 oz $3.25 $2.99 $2.75

Latte Collegetown Commons East Hill Plaza12 oz $3.25 $3.25 $3.2516 oz $3.75 $3.75 $3.7520 oz $4.25 $4.25 $4.25

Bundle with complementary goods (i.e. baked goods or sandwiches)

Cheaper to purchase as a bundle or “combo” than separately

Lower prices for coff ee to incentivize consumers to buy higher priced complementary products

PRICE BUNDLING / COMPLEMENTARY PRICING

Introduction Industry Pricing Strategies

Recommendations

Housemade muffin or scone$2.25

16 oz Gimme! drip coffee $2.39Buying separately

$4.64

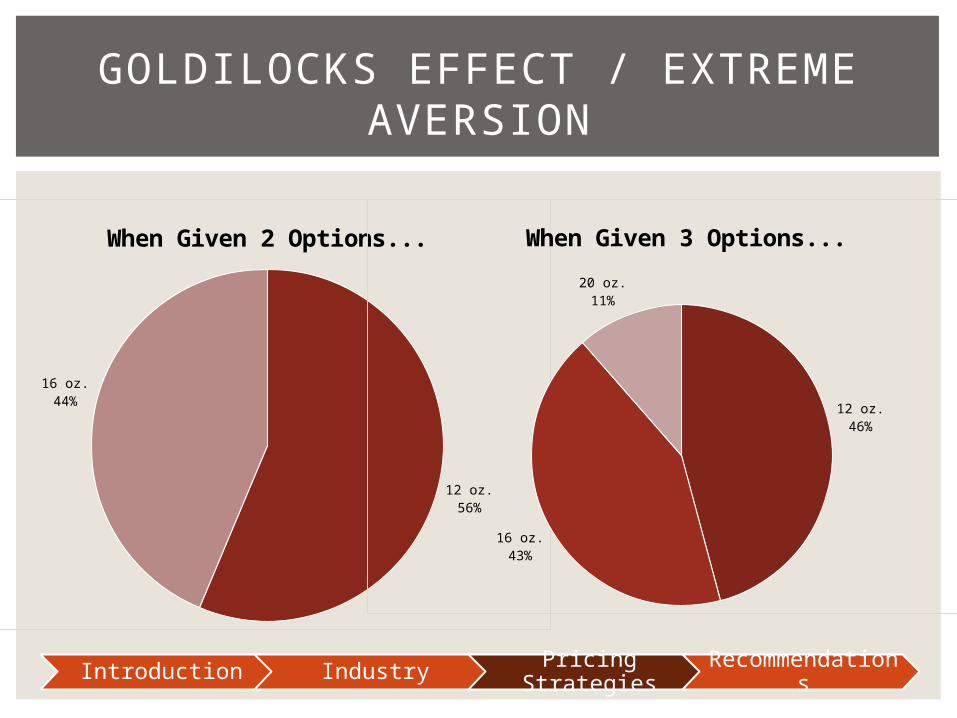

GOLDILOCKS EFFECT / EXTREME AVERSION

Introduction Industry Pricing Strategies

Recommendations

Survey 112 vs. 16 oz

N = 64

Survey 212 vs. 16 vs. 20 oz

N = 61

A few times a month 19%1-3 cups a week 23%4-6 cups a week 14%1 cup a day 22%2 cups a day 14%More than 2 cups a day 10%

GOLDILOCKS EFFECT / EXTREME AVERSION

Introduction Industry Pricing Strategies

Recommendations

12 oz.56%

16 oz.44%

When Given 2 Options...

12 oz.46%

16 oz.43%

20 oz.11%

When Given 3 Options...

SURVEY FINDINGS

Introduction Industry Pricing Strategies

Recommendations

Starbucks26%

On-Campus Café22%Dunkin Donuts

14%

CTB14%

Manndible13%

Stella's5%

Other3%

McDonald's2%

Coffee Shop Preferences

Convenience30%

Coffee Fla-vor/Taste

27%

Location16%

Brand11%

Coffee Op-tions8%

Offers Other Products6%

Other2%

Reasons for Coffee Pref-erences

RECOMMENDATIONS

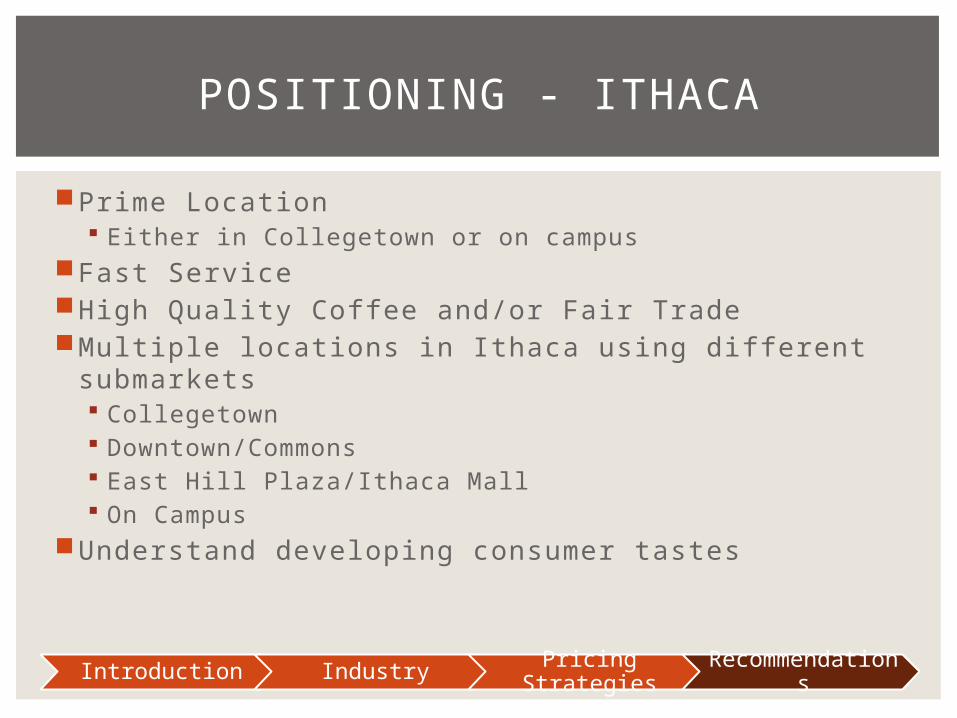

Prime Location Either in Collegetown or on campus

Fast ServiceHigh Quality Coff ee and/or Fair TradeMultiple locations in Ithaca using diff erent submarkets

Collegetown Downtown/Commons East Hill Plaza/Ithaca Mall On Campus

Understand developing consumer tastes

POSITIONING - ITHACA

Introduction Industry Pricing Strategies

Recommendations

Use Premiu

m Pricing

Customer

Loyalty Program

s

Price Bundlin

g

Offer 3 sizes

PRICING STRATEGIES

Introduction Industry Pricing Strategies

Recommendations

Ithaca does NOT show strong signs of third degree price discrimination This changes when the analysis is expanded to include

other geographic locationsCoff ee shops charge higher prices on premium drinks

due to high WTPNational leaders do NOT preclude local players from

the marketCoff ee shops can benefit from diff erentiation

CONCLUSION

Introduction Industry Pricing Strategies

Recommendations

QUESTIONS?