Aegon adviser attitudes report 2019€¦ · Aegon adviser attitudes report 2019 Trends in...

22

Aegon adviser attitudes report 2019 Trends in investment strategies and portfolio building For adviser use only – not approved for use with clients

Transcript of Aegon adviser attitudes report 2019€¦ · Aegon adviser attitudes report 2019 Trends in...

Aegon adviser attitudes report 2019Trends in investment strategies and portfolio building

For adviser use only – not approved for use with clients

Page 2 of 22

Foreword – investing in a changing market 3

Building investment propositions 5

Assessing risk appetite 8

Investment strategies 10

Passive and active management 15

Retirement income investing 16

Conclusion – trends of the future 21

About Aegon 22

The value of investments may go down as well as up. Investors may get back less than they invest. The information in this report is based on our current understanding of markets and legislation and may have changed since publication.

Contents

The findings in this report are based on the views of 250 financial advisers from across the UK. Research conducted by Opinium between 25 February and 1 March 2019.

Page 3 of 22

Nick DixonInvestment Director, Aegon UK.

In this report we’ve collated the views of over 250 financial advisers from across the country to better understand how advisers and their clients invest on platforms.

We’re seeing significant changes in how people save, and how advisers work with their clients. Auto-enrolment has created millions of new savers. There is a decreasing reliance on defined benefit (DB) pensions as defined contribution (DC) pensions become the primary vehicle. And pension freedoms legislation means many more remain invested during a retirement that can now last for 30-40 years.

At the same time, the asset management industry is under regulatory pressure to justify fund costs. MIFID II has elevated the requirement for clear and transparent portfolio management and reporting.

Digital developments are also changing the way we administer investments. Platforms offer greater flexibility than ever before, improving the ways advisers can create and maintain investment propositions. Platform technology is streamlining model portfolio management, is allowing faster access to investment data, and is making it easy to set up online panels of approved investments. Platforms also offer access to a vastly wider range of investment options.

These positive forces create a challenging context for advisers. They are having to meet the changing needs of their clients, satisfy regulators, and leverage new technology to build streamlined, scalable investment propositions to grow their businesses and improve efficiency.

There is an expanding need for centralised processes, especially in larger firms, to demonstrate regulatory compliance and drive efficiency. As a result, advice firms are becoming increasingly reliant on external service providers to ensure consistency and robustness in their investment recommendations.

Foreword – investing in a changing market

We’re seeing significant changes in how people save,

and how advisers work with their clients.

Page 4 of 22

I trust you will find this report interesting. And more importantly, I trust you will have a top-quartile year in 2019.

Nick DixonInvestment Director, Aegon UK.

Key research findings:

Outsourcing is commonplace and increasing – a trend that cuts across fund range management, portfolio building and risk assessment.

Most firms have a centralised investment proposition – but their advisers retain the ability to make investment recommendations outside of it.

Cost is an increasingly dominant factor – with track record and cost the most important factors looked at when assessing a fund’s quality.

Many investors have a poor understanding of investment risk / return – their discussions with advisers improve understanding and frequently impact risk appetites.

Multi-asset funds are the most used investment type – although in-house and outsourced model portfolios also feature heavily and DFM use continues to grow. Less industrialised, fund picking approaches are becoming increasingly rare.

Passive strategies account for nearly a quarter of assets – however, they are often used alongside active strategies.

A ‘pretirement’ stage is now the norm – with three quarters transitioning gradually into retirement and most opting for drawdown.

Page 5 of 22

Building investment propositions Centralised investment propositions (CIPs) are now used by the vast majority of advice firms, aiming to improve the consistency and robustness of fund recommendations.

90% of the advisers we surveyed tell us their firm operates a company-wide investment process. The notable exceptions are very small firms managing less than £5 million, where only 58% report a company-wide investment process.

Many of these centralised propositions are likely to include a tiered approach. For example recommending different options based on the value of a client’s savings, or whether they’re aiming for growth or income. Often these propositions will include multi-asset funds or models that sit across a risk/return spectrum.

Interestingly, firms generally allow their advisers a lot of flexibility over their investment recommendations. 67% told us that they have whole of market choice, while the remaining third must select from a pre-approved fund range. In reality it is likely that a large proportion of assets, where the client has mainstream needs, are directed towards the central tiers of a firm’s CIP even where whole of market choice exists.

Creating a CIP means firms can offer a more consistent approach, reduce duplication of effort and let their advisers focus on identifying and meeting client needs. However, our results suggest that most firms value a balance between centralisation and letting advisers have the latitude to make suitability calls where needed. The investments in the primary tier of a firm’s investment proposition may be used by most, but they are rarely mandatory.

Almost half outsource fund range managementLooking in more detail at how fund ranges are managed, the market is split, with 44% saying they outsource this task (either entirely or in part) and 46% stating they rely wholly on in-house expertise.

What size of fund range do you choose from?

0 % 10 % 20 % 30 % 40 % 50 % 60 % 70 % 80 %

I choose from a panel of less than50 pre-approved investments

I choose from a panel of50-250 pre-approved investments

I choose from a panel of more than250 pre-approved investments

I have whole of market choice

12%

15%

6%

67%

have a company-wide investment process

90%

say they outsource fund range management

44%

Page 6 of 22

These outsourced options either use research from a specialist firm when creating and monitoring fund ranges, invite independent experts to sit on their governance committee, or give full responsibility for fund range creation to a third party. With thousands of investment options now available to the retail market, this approach provides access to more comprehensive research than they may be able to conduct in-house. It can also help advisers standardise their fund monitoring processes, and reduce the costs associated with fund research. However, it does mean passing an element of control to a third party.

The level of outsourcing used is heavily affected by the size of firm an adviser works in. 60% of firms with six or more financial advisers utilise external expertise when building fund ranges, compared to a more modest 37% for firms with only one adviser.

It appears that these larger firms benefit from economies of scale, and are more able to afford external input. There is also greater consistency risk with larger firms. These firms, have more advisers, greater numbers of clients and greater sums of money to manage, so they will find it harder to ensure quality control and consistency without enlisting specialist help.

Our results also find that over a quarter (26%) of the advisers surveyed rely on fund ranges that are created and managed by an individual. This rises to nearly half (49%) for firms with a single financial adviser and falls to 0% for firms with six or more advisers. It may be that these firms rely more on multi-asset funds or DFMs, which come with ongoing fund monitoring built in.

Who defines, creates and monitors the fund ranges your firm o�ers?

30%

26%

20%

14%

4% 6% An investment committee made up of members of my company, supported by research from an external investment research firm.

An individual in my company

An investment committee made up of members of my company only

An investment research firm external to my company

Other

Not applicable

Fund range creation split by number of financial advisers in a firm

Not applicable

Other

An investment research firm external to my company

An investment committee made up of members of my company only

An individual in my company

An investment committee made up of members of my company, supported by research from an external investment research firm.

0 % 10 % 20 % 30 % 40 % 50 % 60 % 70 % 80 % 90 %

100 %

1 - sole trader 2-5 6+

Page 7 of 22

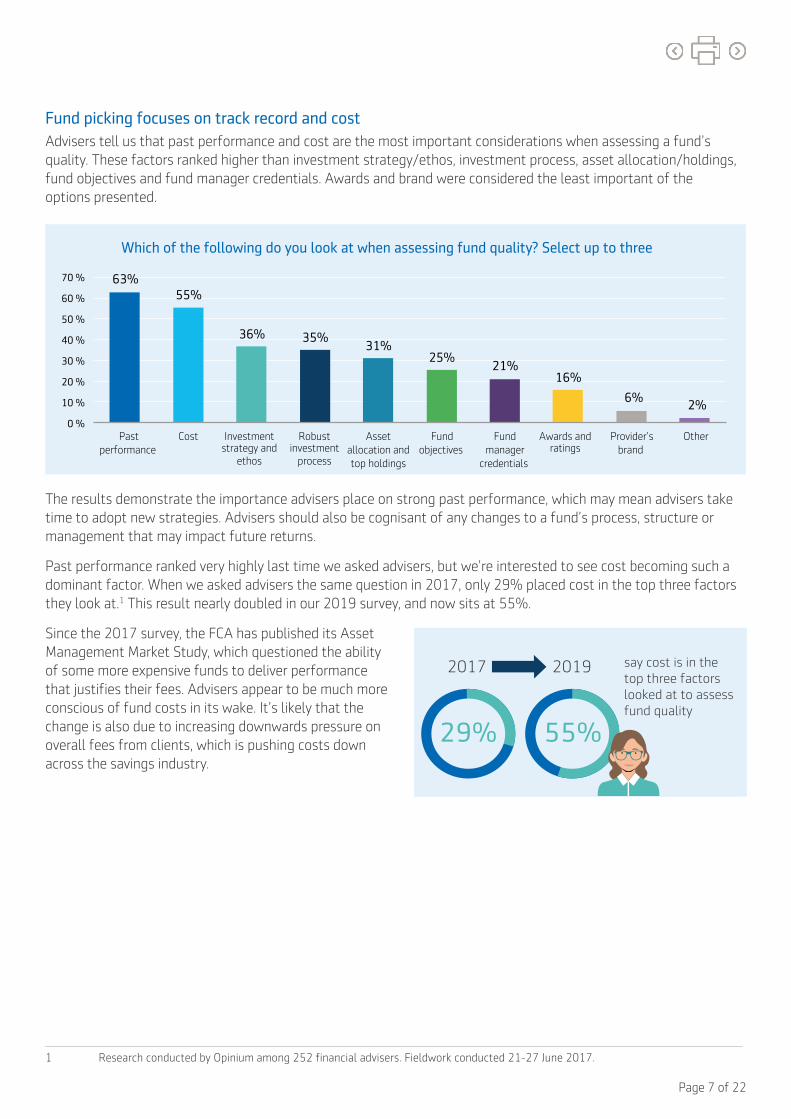

Fund picking focuses on track record and cost Advisers tell us that past performance and cost are the most important considerations when assessing a fund’s quality. These factors ranked higher than investment strategy/ethos, investment process, asset allocation/holdings, fund objectives and fund manager credentials. Awards and brand were considered the least important of the options presented.

The results demonstrate the importance advisers place on strong past performance, which may mean advisers take time to adopt new strategies. Advisers should also be cognisant of any changes to a fund’s process, structure or management that may impact future returns.

Past performance ranked very highly last time we asked advisers, but we’re interested to see cost becoming such a dominant factor. When we asked advisers the same question in 2017, only 29% placed cost in the top three factors they look at.1 This result nearly doubled in our 2019 survey, and now sits at 55%.

Since the 2017 survey, the FCA has published its Asset Management Market Study, which questioned the ability of some more expensive funds to deliver performance that justifies their fees. Advisers appear to be much more conscious of fund costs in its wake. It’s likely that the change is also due to increasing downwards pressure on overall fees from clients, which is pushing costs down across the savings industry.

1 Research conducted by Opinium among 252 financial advisers. Fieldwork conducted 21-27 June 2017.

63% 55%

36% 35% 31%

25% 21%

16%

6% 2%

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

Pastperformance

Cost Investment strategy and

ethos

Robust investment

process

Asset allocation and top holdings

Fundobjectives

Fundmanager

credentials

Awards and ratings

Provider’sbrand

Other

Which of the following do you look at when assessing fund quality? Select up to three

say cost is in the top three factors looked at to assess fund quality

2017 2019

29% 55%

Page 8 of 22

Assessing risk appetiteFinancial advisers play an important role in helping clients understand the trade-offs between risk and growth potential.

Without advice, most investors tend towards investment caution. Many fail to invest or hold significant amounts in cash, which is unlikely to give them the growth potential above inflation that long-term savers need. When we questioned investors directly, a staggering 56% said they had a ‘low’ or ‘zero’ risk appetite, compared to just 13% who said they had a ‘high’ or ‘adventurous’ risk appetite2.

The risk / return trade off

Only 47% of advisers think most investors understand the relationship between risk and growth potential before they explain it to them. A further 40% think that about half understand it, and 12% think the majority don’t.

Related to this low level of understanding, half of the advisers we surveyed say adviser education impacts the risk appetites of most clients. Following their discussions, around a third (34%) say most become less cautious, given the potential for improved investment growth, and 16% say that most become more cautious.

47% 40%

12%

Yes - the majority do

About half of them do

No - the majority don't

Do clients understand the trade-o between risk and return before you explain it?

50%

34%

16%

0 %

10 %

20 %

30 %

40 %

50 %

60 %

Most risk attitudes remain unchanged Most become less cautious Most become more cautious

How do your discussions with clients impact their attitude to risk?

2 Research conducted by Opinium among 2,002 UK adults. Fieldwork conducted 12-15 October 2018.

Page 9 of 22

Risk assessment toolsWhen assessing investment risk, most advisers (97%) use risk profiling tools. These tools can help focus clients’ minds on the factors they need to think about when working out where on the risk spectrum they sit. However, they are best used as part of a wider conversation about risk that also takes into account other factors, such as investment time horizon, financial commitments, savings goals and capacity for financial loss.

Interestingly, the trend towards outsourcing continues here. Risk assessment tools from external providers dominate, with in-house risk assessment tools shrinking very slightly from 28% down to 26% of the market since 20173.

The historic dominance of Dynamic Planner risk ratings continues – nearly 30% of the advisers we surveyed use their risk ratings. Defaqto comes in second place, used by nearly a quarter.

Political uncertainty impacts investor confidence When we explore the factors that impact investor confidence more broadly, 78% of advisers tell us that political uncertainty is expected to have the most significant impact in the next 12 months. Clearly advisers are already facing questions about Brexit, the future of the EU and Trump’s impact on the global economy, and they don’t expect a calming of the political landscape any time soon. These results are hardly surprising in such unprecedented times.

Which of the following risk assessment tools do you use?

24% 29%

10% 7%

5%

16%

26%

7%

13%

3%

0 %

5 %

10 %

15 %

20 %

25 %

30 %

35 %

Defaqto Distribution Technology /Dynamic Planner

EValue FinaMetrica Moody’s Morningstar The fund provider’s own risk

assessment tool

In-house risk

assessment tool

Other provider’s

risk assessment

tool

I don’t use a risk

assessment tool

Which of the following would you expect to have the biggest impacton investor confidence in the next 12 months?

78%

8%

6% 4%

1% 2%

Political uncertainty

Value of the pound

Market prospects

Changes to interest rates

Inflation / deflation

Other

3 Research conducted by Opinium among 252 financial advisers. Fieldwork conducted 21-27 June 2017.

Page 10 of 22

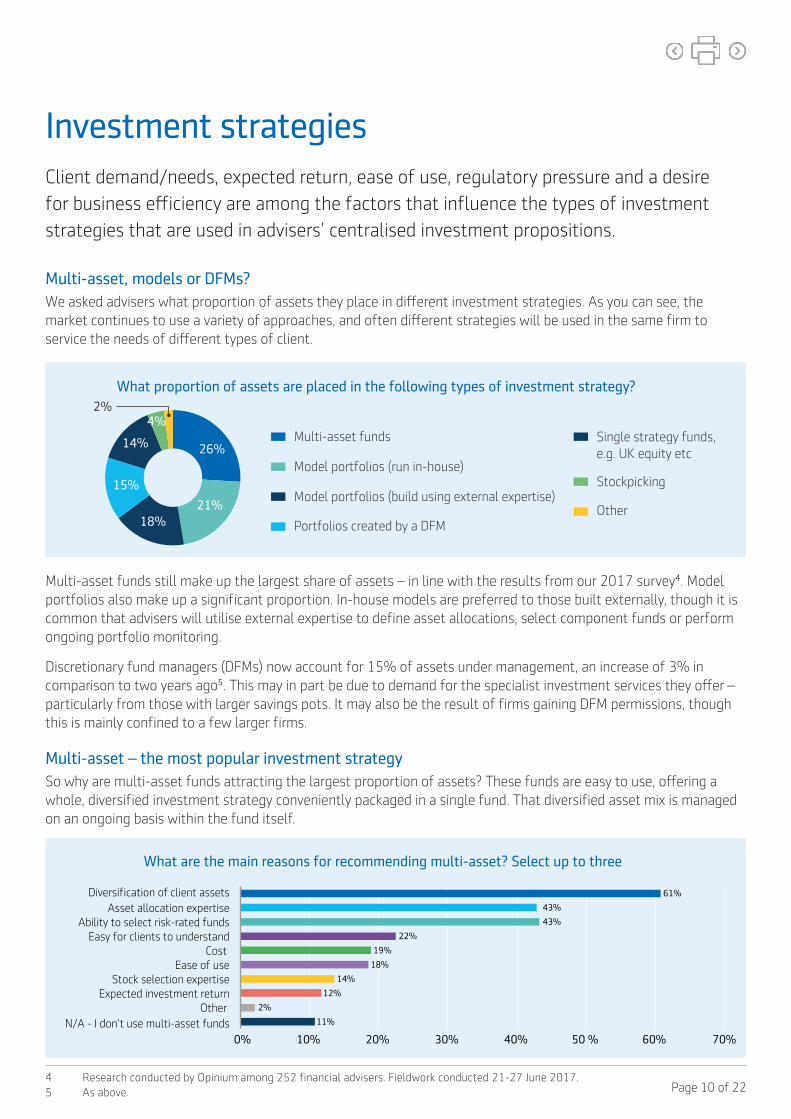

Investment strategies Client demand/needs, expected return, ease of use, regulatory pressure and a desire for business efficiency are among the factors that influence the types of investment strategies that are used in advisers’ centralised investment propositions.

Multi-asset, models or DFMs?We asked advisers what proportion of assets they place in different investment strategies. As you can see, the market continues to use a variety of approaches, and often different strategies will be used in the same firm to service the needs of different types of client.

Multi-asset funds still make up the largest share of assets – in line with the results from our 2017 survey4. Model portfolios also make up a significant proportion. In-house models are preferred to those built externally, though it is common that advisers will utilise external expertise to define asset allocations, select component funds or perform ongoing portfolio monitoring.

Discretionary fund managers (DFMs) now account for 15% of assets under management, an increase of 3% in comparison to two years ago5. This may in part be due to demand for the specialist investment services they offer – particularly from those with larger savings pots. It may also be the result of firms gaining DFM permissions, though this is mainly confined to a few larger firms.

Multi-asset – the most popular investment strategy So why are multi-asset funds attracting the largest proportion of assets? These funds are easy to use, offering a whole, diversified investment strategy conveniently packaged in a single fund. That diversified asset mix is managed on an ongoing basis within the fund itself.

What proportion of assets are placed in the following types of investment strategy?

26%

21% 18%

15%

14%

4% 2%

Multi-asset funds

Model portfolios (run in-house)

Model portfolios (build using external expertise)

Portfolios created by a DFM

Single strategy funds, e.g. UK equity etc

Stockpicking

Other

What are the main reasons for recommending multi-asset? Select up to three

11%

2%

12%

14%

18%

19%

22%

43%

43%

61%

0% 10% 20% 30% 40% 50 % 60% 70% N/A - I don't use multi-asset funds

Other Expected investment return

Stock selection expertise Ease of use

Cost Easy for clients to understand

Ability to select risk-rated funds Asset allocation expertise

Diversification of client assets

4 Research conducted by Opinium among 252 financial advisers. Fieldwork conducted 21-27 June 2017.5 As above.

Page 11 of 22

Advisers also like the ability to select funds that aim to meet different risk appetites. This makes it easier for them to match funds to client needs and to use them alongside risk assessment tools. The asset allocation expertise that sits within these funds was also highlighted as a key benefit by advisers. This allows the mix of investments to be changed to maintain alignment to the stated outcome when markets change.

Around a fifth highlighted that the funds are easy for clients to understand, and a further fifth valued ease of use – with multi-asset funds letting them invest in one fund that can meet a rounded set of needs, rather than building a portfolio from several funds. Cost was also a factor for around a fifth. In general, multi-asset funds tend to cost less than models or DFM portfolios due to the economies of scale that fund providers can often achieve.

Nearly 60% of assets now in outsourced portfolios

Portfolios that rely on outsourcing to one degree or another now account for 59% of advised assets 6. This is up from 55% in 2017.

While outsourcing in this area is now commonplace, it takes a number of forms. In some cases advisers are utilising portfolios – either from multi-asset fund providers or DFMs – that come with investment governance built in. In this case the role of the adviser is focussed on selecting the right solution provider, and ratifying that choice over time. Fund selection, blending, fund changes and ongoing monitoring are all outsourced.

In other examples, advisers are buying-in the services of fund research providers for different aspects of model portfolio building. For example they may rely on a provider to create asset allocations for their model portfolios, to make fund recommendations, or that provider might form part of their investment governance committee or review the decisions of that committee.

These are all services that can be costly to do well within an advice firm itself. Only very large firms will have the depth and breadth of research capability that a dedicated specialist can access.

Some external providers will have greater influence over key decisions than others. Some will be given carte blanche, while others will be subject to a further layer of in-house scrutiny before changes are implemented.

Full outsourcing Asset allocation Fund picking Ongoing governance

For example usinga multi-asset fund or

DFM’s model.

Provided by a specialist to match adviser’s

mandate.

Specialist recommends funds to populate adviser’s models.

To check if portfolios meet objectives over

time.

Types of outsourcing

of assets use outsourcing59%

6 Based on total figures for multi-asset funds, model portfolios (built using external expertise) and portfolios created by a DFM.

Page 12 of 22

Investment strategy use varies by firm sizeWhen we look at different sizes of firm, we see some clear trends in terms of the types of investment strategies used.

Smaller firms tend to rely more on stockpicking, single strategy funds or alternative investment strategies. They tend to offer a more bespoke, less scalable service.

In contrast, firms over £5 million in size tend to use more industrialised investment processes. These firms are more likely to use multi-asset funds, model portfolios or DFMs. The largest companies – those with over £100 million in assets under management – are the most likely to offer their own in-house model portfolios. These firms have the scale required to bear the cost of in-house investment research and monitoring.

Size of savings pot impacts fund recommendationsOur results also show that the size of a client’s savings pot can have an impact on the recommended investment strategy.

Around 40% said the size of savings pot would impact their decision to recommend a multi-asset fund or model portfolio, and this rose to 57% for a DFM recommendation.

Advisers are more likely to recommend multi-asset strategies to those with savings below £250,000. This is most likely down to simple cost-benefit analysis with multi-asset funds generally cheaper and therefore less of a drag on a small pot size.

Conversely, advisers are more likely to recommend DFM strategies to those with savings above the £250,000 threshold. Those with larger savings pots are more likely to be prepared to pay the additional costs generally associated with this specialist service.

Proportion of assets in each investment strategy by firm size

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0 90.0

100.0

Less than £5 million £5 to £9.9 million £10 to £19.9 million £20 to £49.9 million £50 to £99.9 million £100 million +

Stockpicking / single-strategy funds / other

Multi-asset funds

Model portfolios (run in-house)

Model portfolios (built using external expertise)

DFM

Who are you more likely to recommend using the following strategy to?

Those with savings of less than £250,000

Those with savings of more than £250,000

Size of savings pot isn’t relevant

Multi-asset

4% 57%

40%

62%

18%

20%

4%

53%

44%

Modelportfolio

DFM

Page 13 of 22

Model portfolios are the most agnostic of the three options on size of savings pot. 62% of advisers stated that size of pot wouldn’t influence their decision to recommend a model portfolio, and it’s clear that models are widely used regardless of client wealth.

Half have investors in historic model portfoliosConcerns have been raised in recent years about the efficiency of model portfolio management. The requirement to gain permission from a client each time a portfolio change is made comes with a risk that the adviser won’t receive confirmation in a timely fashion, or indeed at all. As a result, client portfolios can be updated too late. Or, in the most severe cases, clients remain in historic versions of the adviser’s model.

It appears that, on the whole, advisers have this risk under management. Around 70% of advisers use model portfolios. 86% of those that do say their firm is always able to quickly gain consent from investors for model portfolio changes. This leaves 14% where the firm isn’t always able to gain consent.

This finding seemed slightly incongruous given the fact that 51% of advisers admit to having clients in historic models.

Where these historic models exist, they present a risk to both the client and the adviser. For the client, they have fallen outside of a managed investment process and may not be aware of the implications of this. Meanwhile the adviser has model portfolios on their books which they no longer actively support.

As a consequence, some advisers now favour multi-asset funds or DFM strategies where consent for asset mix changes is agreed at outset.

Is your firm always able to quickly gain consent for model portfolio changes?

Yes 86% No 14%

No 49%Yes 51%

Does your firm have investors in historic versions of model portfolios, for example where consent for changes hasn’t been received.

Page 14 of 22

12% of advice firms have DFM permissionsMost firms don’t have DFM permissions (77%), and only 6% say they intend to acquire these in the future. Adding this to the 12% who already offer DFM services, this suggests that DFMs could account for a fifth of adviser firms in the future.

As we would expect, firms with £100 million+ under management are more likely to have DFM permissions. 20% of these largest firms have DFM permissions, versus a 12% average.

As we saw in the assets under management figures, there appears to be a steady growth of DFMs use. At present, they remain a small part of the market, focussed mainly on serving the needs of high net-worth clients. However, we expect their audience to broaden further over time.

Does your firm have DFM permissions?

77%

12%

6% 4%

No

Yes

No, but we plan to in the future

I don't know

Page 15 of 22

Passive and active managementPassive and hybrid investment strategies now make up a significant proportion of the market. So, while the active versus passive debate continues, the conversation tends to focus more on when and how different management strategies can be best deployed, and how they can be used in combination.

Active management aims to better the returns of less-expensive passively managed funds. However, the FCA’s Asset Management Market study has brought investment management costs into sharp focus, calling on fund managers to better justify the value they offer where higher fees are charged7. In addition, the market is increasingly cost-aware. As we saw earlier, 55% of the financial advisers we surveyed said cost is one of the top three factors they look at when assessing a fund’s quality.

It is important though that we make a distinction in this area between cost and value for money – and for the most part advisers remain convinced that actively managed strategies do offer value. When asked what proportion of the assets they invest go into different types of strategy, advisers tell us that 67% goes into actively managed investments versus 23% in passively managed strategies, and a further 10% in hybrid strategies that use elements of both passive and active fund management.

The continued high usage of active management suggests that most advisers agree that the additional fees are justified by an ability to generate higher returns. Recent research by Platforum also shows that some believe that active management may outperform in a market downturn, having greater flexibility to adjust the investments it holds8.

However, around a third of assets (33.1%) are now invested in passive or hybrid strategies. Higher customer awareness of passive management appears to be having an impact. And in some cases cost pressure has resulted in the inclusion of passive strategies to bring overall portfolio costs down.

This suggests that, while advisers may favour active management, many see a place for passive management, perhaps to gain exposure to regions (such as the US and other developed markets) where it’s harder for active managers to outperform.

In any case, with such significant amounts going into passive or semi-passive strategies, advisers are clearly looking at how and where they can work alongside active strategies to add value for clients.

What proportion of assets tend to be invested in the following fund types?

66.9% 22.7%

10.4%

Actively managed

Passively managed

Hybrid

7 FCA, Asset Management Market Study Final Report MS15/2.3, June 2017.8 Platforum, Adviser Market: Investment Propositions, October 2018.

Page 16 of 22

Retirement income investingThere has been huge growth in the retirement income advice market since the introduction of Pension Freedoms in April 2015. It’s no longer the case that most retire at a point in time and purchase an annuity. The retirement landscape has become more varied and complex, with retirees now expected to make choices about when they retire, how they invest and how much income they should take.

As a result we’re already seeing shifts in the priorities and requirements of retirees, and many are taking advantage of the ability to choose their own retirement path. It’s worth remembering too that this new landscape remains in its infancy. Most retirees still have defined benefit pensions, and the reliance on defined contribution (DC) pots remains fairly small9. We can only expect the impact of Pension Freedoms to amplify over time as DC pensions become the primary retirement savings vehicle for most.

This growing market creates opportunities for financial advice firms that can get to grips with this changing landscape and develop propositions to help retirees navigate their way to and through retirement.

Over a third retire ‘early’ or ‘late’Nearly two thirds of advisers (63%) told us that the average age of a retiring client is between ages 61-65, broadly in line with the state pension age for those retiring in the last 10 years.

However, a significant number (36%) are finding that on average their clients retire either ‘early’ or ‘late’, i.e. before they are 60 or after age 66, suggesting that retirement ages are becoming more fluid. Interestingly, there is no dominance of either trend, with early and late retirees making up around a fifth of the market apiece.

In a separate piece of research, workers over the age of 50 told us that health issues, income considerations and how they feel about their work are the main factors that will influence their decision to retire. Caring responsibilities, the retirement of a partner or spouse, and recognition at work are also key factors10.

What is the average age of a retiring client?

17%

63%

19% 50-55

56-60

61-65

66-70

71+

2%

9 Retirement Outcomes Review – Final report, June 2018.10 Based on the views of over 1,000 UK workers over the age of 50 who earn £20,000 a year or more.

Research conducted by Opinium between 30 November and 6 December 2018.

Page 17 of 22

The rise of a ‘pretirement’ stage

Notable among the changes we’re seeing is that three quarters of advisers (74%) say most clients retire gradually, moving into semi-retirement or reducing working hours before they retire fully. This compares to just 20% who say most clients go straight from their usual work pattern to full retirement. This trend has been noted for some time, but appears to have accelerated in the light of greater income flexibility.

The savings industry therefore needs to offer strategies that cater for an emerging ‘partial-retirement’ stage, as well as those designed for pre- and post- retirement. These strategies may or may not need to offer some degree of regular income. At the same time, there should be a gradual preparation for retirement, coupled with a recognition that savings may still need to last for 30-40 years.

Retirees worry about running out of moneyIn addition to understanding how and when people retire, it is also important to understand how they feel, and what they worry about, when retiring.

Our survey asked advisers what retiring clients tend to prioritise. The top three by a significant margin were: how to create a retirement income; understanding the options available; and making sure they were saving enough.

Decisions about pension consolidation and defined benefit pensions came fourth, with concerns about how to help children financially a close fifth. Inheritance tax planning, providing for care needs in later life and extracting wealth from property ranked the lowest.

When asked about the financial fears of retirees, a significant 38% of advisers said running out of money was the biggest concern their clients had. This suggests that, although significant numbers are choosing the growth potential of drawdown (and to a lesser degree the flexibility of cash) over a more certain annuity income11, retirees worry about their long-term financial security.

Around a third of advisers (32%) said their clients greatest fear is not being able to have the lifestyle they’d like, while 25% said they worry mainly about not being able to maintain income in retirement. The ability to provide for dependents or fund long-term care ranked significantly lower, mentioned by just 2% apiece.

What are the most common challenges retiring clients face – select up to three

0% 20% 40% 60% 80%

Other

How best to extract wealth from property

Making provision for care needs in later life

Inheritance tax planning

Intergenerational wealth – how best to help their children

Deciding whether to consolidate pensions or transfer out of a DB pension

Saving enough for retirement

Understanding all the options available for them to invest their money

How to create a retirement income

11 FCA Data Bulletin – issue 14, September 2018

say most clients retire gradually

74%

Page 18 of 22

What is the biggest financial fear of retiring clients?

0 %

5 %

10 %

15 %

20 %

25 %

30 %

35 %

40 %

45 %

Running out of moneyin retirement

Not being able to have the lifestyle they’d like

Not being able to maintain income in retirement

Not being able to provide for dependents

Not being able to fund long term care

38%

25%

32%

2% 2%

It is worth reiterating that our results focus on adviser’s clients, and it is likely that the level of concern is likely to be more amplified among a broader population that included non-advised savers.

While clients seem to be taking advantage of greater financial flexibility in retirement, it seems that they do this with some reservations. It is incumbent on advisers to recognise and address these concerns when building retirement income strategies.

Drawdown dominates versus annuities or cashIn its latest Retirement Income bulletin, the FCA reported that 69% of assets were invested into drawdown policies, compared to just 13% used to purchase annuities between October 2017 and March 2018. Cash withdrawals have been popular, but mainly for those with small defined contribution savings pots. 53% of all pots accessed since the new rules came into force have been fully encashed, though 87% of these were worth £30,000 or less. Full cash withdrawals accounted for 12% of assets from October 2017 to March 2018. However, it is worth noting that 60% of new income drawdown policies over that period were zero income (i.e. cash has been withdrawn but no income payments have been made)12.

Our own survey results restate these trends and show an even stronger preference for income drawdown. On average, advisers tell us that three quarters of retiring clients’ assets are in income drawdown (74%), compared to 16% in annuities and just 10% in cash.

For advised retirees at least, income drawdown is now the primary savings vehicle in retirement.

On average, what proportion of retiring client’s assets are invested in the following strategies?

74%

16% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Income drawdown Annuities Cash

12 FCA Data Bulletin – issue 14, September 2018.

Page 19 of 22

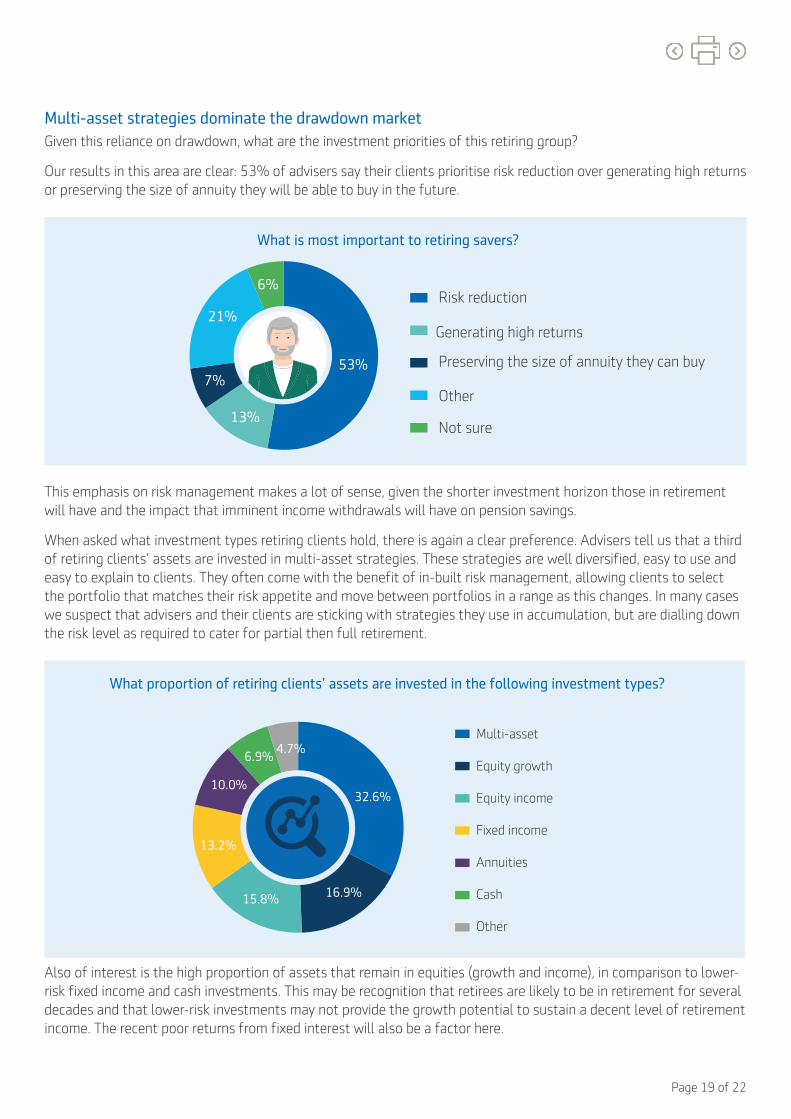

Multi-asset strategies dominate the drawdown marketGiven this reliance on drawdown, what are the investment priorities of this retiring group?

Our results in this area are clear: 53% of advisers say their clients prioritise risk reduction over generating high returns or preserving the size of annuity they will be able to buy in the future.

This emphasis on risk management makes a lot of sense, given the shorter investment horizon those in retirement will have and the impact that imminent income withdrawals will have on pension savings.

When asked what investment types retiring clients hold, there is again a clear preference. Advisers tell us that a third of retiring clients’ assets are invested in multi-asset strategies. These strategies are well diversified, easy to use and easy to explain to clients. They often come with the benefit of in-built risk management, allowing clients to select the portfolio that matches their risk appetite and move between portfolios in a range as this changes. In many cases we suspect that advisers and their clients are sticking with strategies they use in accumulation, but are dialling down the risk level as required to cater for partial then full retirement.

Also of interest is the high proportion of assets that remain in equities (growth and income), in comparison to lower-risk fixed income and cash investments. This may be recognition that retirees are likely to be in retirement for several decades and that lower-risk investments may not provide the growth potential to sustain a decent level of retirement income. The recent poor returns from fixed interest will also be a factor here.

What is most important to retiring savers?

53%

13%

7%

21%

6% Risk reduction

Generating high returns

Preserving the size of annuity they can buy

Other

Not sure

What proportion of retiring clients’ assets are invested in the following investment types?

32.6%

16.9% 15.8%

13.2%

10.0%

6.9% 4.7%

Multi-asset

Equity growth

Equity income

Fixed income

Annuities

Cash

Other

Page 20 of 22

Within equities there is a fairly even split between growth and income funds. The proportion in equity income in particular (15.8%) feels low for an asset class focussed on the provision of income, and is relatively unchanged in comparison to our 2017 survey results. This may in part be due to the well-publicised underperformance of a few high-profile funds, such as the Woodford Equity Income fund.

What is reassuring is the range of investment types being used. In an area of the market where risk management is key, there is particular benefit in taking a diversified approach.

Where next for the retirement income market?This is an area of the market that is changing rapidly, and it’s one where we expect to see continued innovation in years to come. While the Pension Freedoms rules introduced four years ago appear to have been embraced and utilised by many, they will only be tested in earnest when the majority of retirees rely primarily on defined contribution pensions, rather than older defined benefit options.

Page 21 of 22

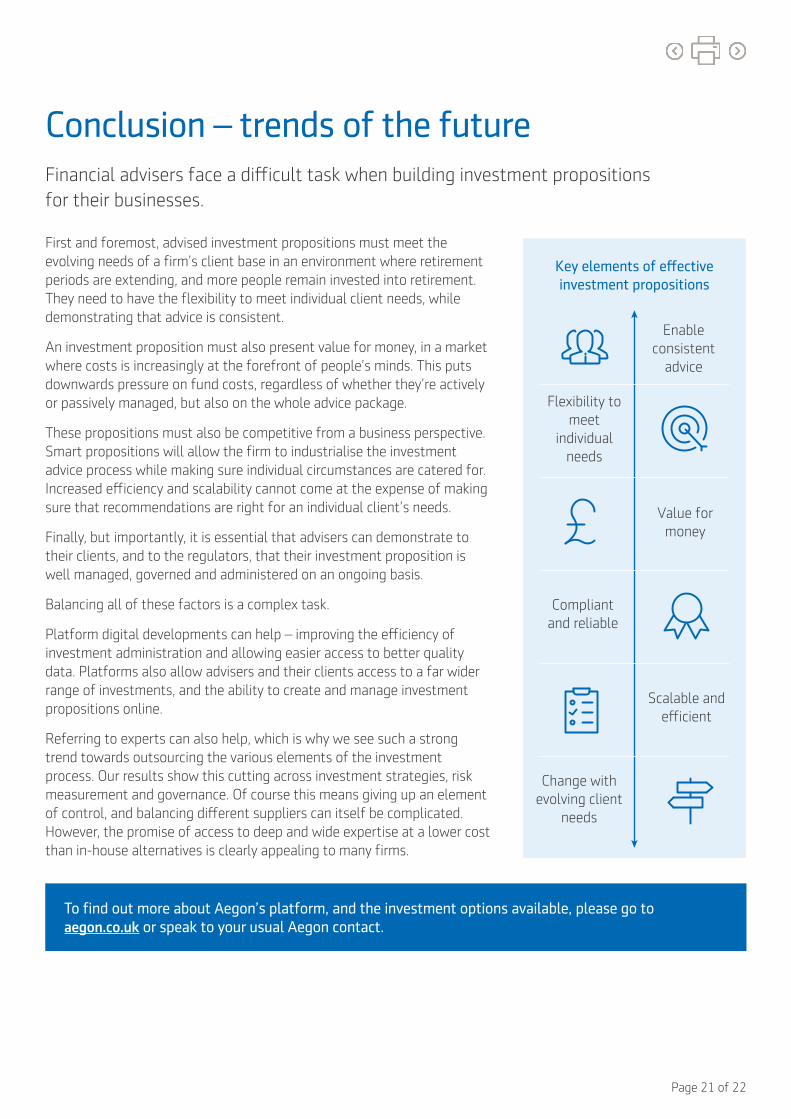

Conclusion – trends of the future Financial advisers face a difficult task when building investment propositions for their businesses.

First and foremost, advised investment propositions must meet the evolving needs of a firm’s client base in an environment where retirement periods are extending, and more people remain invested into retirement. They need to have the flexibility to meet individual client needs, while demonstrating that advice is consistent.

An investment proposition must also present value for money, in a market where costs is increasingly at the forefront of people’s minds. This puts downwards pressure on fund costs, regardless of whether they’re actively or passively managed, but also on the whole advice package.

These propositions must also be competitive from a business perspective. Smart propositions will allow the firm to industrialise the investment advice process while making sure individual circumstances are catered for. Increased efficiency and scalability cannot come at the expense of making sure that recommendations are right for an individual client’s needs.

Finally, but importantly, it is essential that advisers can demonstrate to their clients, and to the regulators, that their investment proposition is well managed, governed and administered on an ongoing basis.

Balancing all of these factors is a complex task.

Platform digital developments can help – improving the efficiency of investment administration and allowing easier access to better quality data. Platforms also allow advisers and their clients access to a far wider range of investments, and the ability to create and manage investment propositions online.

Referring to experts can also help, which is why we see such a strong trend towards outsourcing the various elements of the investment process. Our results show this cutting across investment strategies, risk measurement and governance. Of course this means giving up an element of control, and balancing different suppliers can itself be complicated. However, the promise of access to deep and wide expertise at a lower cost than in-house alternatives is clearly appealing to many firms.

To find out more about Aegon’s platform, and the investment options available, please go to aegon.co.uk or speak to your usual Aegon contact.

Key elements of e�ective investment propositions

Enable consistent

advice

Flexibility to meet

individual needs

Compliant and reliable

Change with evolving client

needs

Scalable and e�cient

Value for money

Aegon UK plc, registered office: Level 26, The Leadenhall Building, 122 Leadenhall Street, London, EC3V 4AB. Registered in England and Wales (No. 03679296). An Aegon company. © 2019 Aegon UK plc

INV384129 05/19

Aegon is one of the world’s leading providers of life insurance, pensions and asset management. Aegon UK started life as Scottish Equitable in 1831 and, over the years, we’ve combined our strong UK heritage with Aegon’s global strength, while staying committed to our original purpose; to help people take responsibility for their future and achieve a lifetime of financial security.

About Aegon

29 millioncustomers

Operate in 20 countries

Over €800 billion invested for customers

As at December 2018, number of customers as at December 2017.