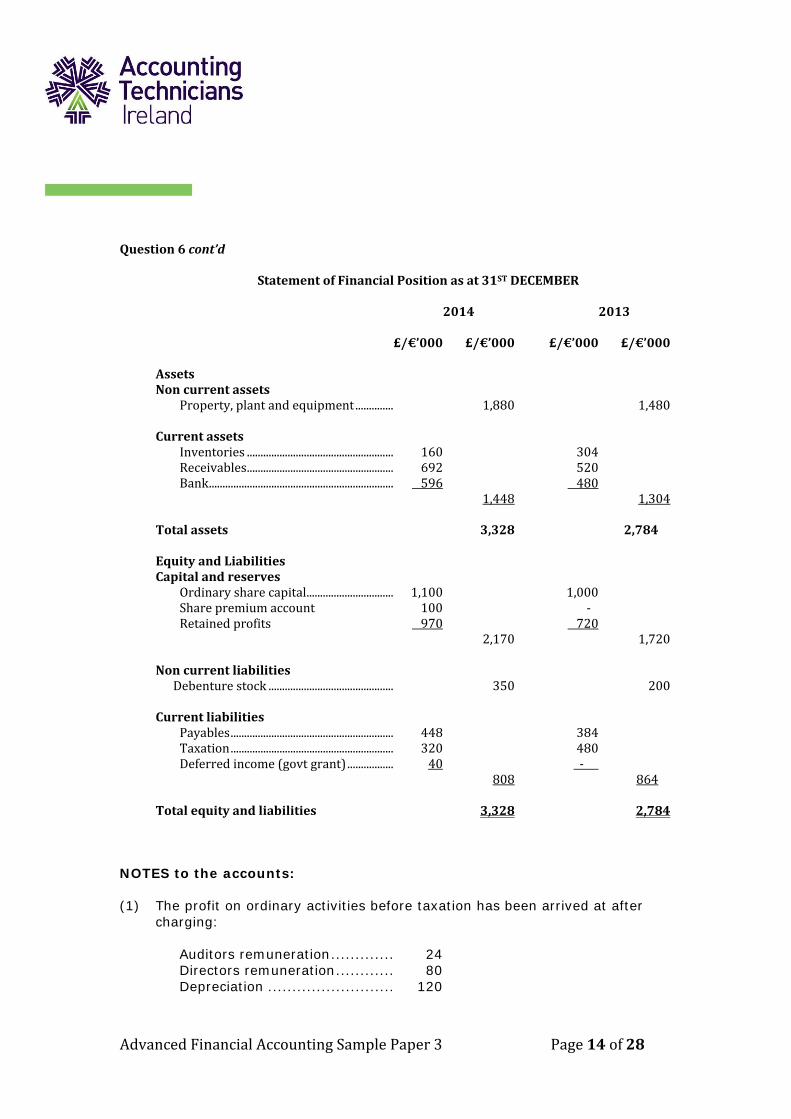

Advanced Financial · PDF fileAdvanced Financial Accounting Sample Paper 3 Page 3 of 28...

28

Page 1 of 28 Advanced Financial Accounting Sample Paper 3 Questions & Suggested Solutions

-

Upload

truongquynh -

Category

Documents

-

view

216 -

download

1

Transcript of Advanced Financial · PDF fileAdvanced Financial Accounting Sample Paper 3 Page 3 of 28...

Page1of28

Advanced Financial Accounting Sample Paper 3 Questions & Suggested Solutions

AdvancedFinancialAccountingSamplePaper3 Page2of28

NOTES TO USERS ABOUT SAMPLE PAPERS

Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance to students and their teachers regarding the style and type of question, and their suggested solutions, in our examinations. They are not intended to provide an exhaustive list of all possible questions that may be asked and both students and teachers alike are reminded to consult our published syllabus (see www.AccountingTechniciansIreland.ie) for a comprehensive list of examinable topics. There are often many possible approaches to the solution of questions in professional examinations. It should not be assumed that the approach adopted in these solutions is the only correct approach, particularly with discursive answers. Alternative answers will be marked on their own merits. This publication is copyright 2015 and may not be reproduced without permission of Accounting Technicians Ireland. © Accounting Technicians Ireland, 2015.

AdvancedFinancialAccountingSamplePaper3 Page3of28

INSTRUCTIONSTOCANDIDATES

PLEASEREADCAREFULLY

Candidates must indicate clearly whether they are answering the paper in accordance with the law and practice of Northern Ireland or the Republic of Ireland. In this examination paper the €/£ symbol may be understood and used by candidates in Northern Ireland to indicate the UK pound sterling by candidates in the Republic of Ireland to indicate the Euro. AnswerALLTHREEquestionsinSectionAandTWOoftheTHREEquestionsinSectionB.IfmorethanTWOquestionsisansweredinSectionB,thenonlythefirstTWOquestions,intheorderfiled,willbecorrected.Candidatesshouldallocatetheirtimecarefully.Allworkingsshouldbeshown.Allfiguresshouldbelabelled,asappropriate,e.g.€’s,£’s,unitsetc.Answersshouldbeillustratedwithexamples,whereappropriate.Question1beginsonPage2overleaf.

NOTE: Thissamplepaperandsolutionshavebeenpreparedtoreflecttheprovisionsof

FRS102

AdvancedFinancialAccountingSamplePaper3 Page4of28

SECTION A

Answer ALL THREE Questions in this Section (The total marks for section A will be 60, made up of a theory question of 20

marks, a multiple choice question of 15 marks and a further question of 25 marks)

QUESTION 1 (i) The Conceptual Framework for Financial Reporting provides a frame of

reference that outlines generally accepted theoretical principles for financial accounting.

(a) Explain briefly the purpose of the Framework. 6 marks (b) A friend who has not studied accountancy has read the Framework and

is confused by some of the terms and definitions discussed within. Prepare a note setting out your understanding of three of the following four terms:

i. Going concern ii. Accruals iii. Asset iv. Liability

6 marks (ii) Define “Accounting Policies” and outline the circumstances under which an

accounting policy should be changed. 4 marks

Define “Accounting Estimates” and give examples of three items which are usually the subject of accounting estimates.

4 marks Total 20 marks

QUESTION 2 The following multiple choice question consists of TEN parts, each of which is followed by FOUR possible answers. There is ONLY ONE right answer in each part. Each part carries 1½ marks. Requirement Indicate the right answer to each of the following TEN parts. Total 15 Marks N.B. Candidates should answer this question by ticking the appropriate boxes on

the special green answer sheet which is supplied with the examination paper.

AdvancedFinancialAccountingSamplePaper3 Page5of28

QUESTION 2 (cont’d)

BACKGROUND INFORMATION TO PARTS [1] – [5]

The following information relates to ROCK Ltd: £/€

Receivables at 1st January 2014 ..................................... 60,000 Receivables at 31st December 2014................................. 80,000 Payables at 1st January 2014 ......................................... 75,000 Payables at 31st December 2014 ..................................... 85,000 Inventory at 1st January 2014 ........................................ 140,000 Inventory at 31st December 2014 ................................... 170,000 Sales on credit for the year ended 31st December 2014 ..... 1,800,000 Cash sales for the year ended 31st December 2014 ........... 300,000 Purchases (all on credit) for the year ended 31st December 2014 ................................................................................. 1,250,000 Bank overdraft at 31st December 2014 ............................ 60,000 Taxation liability at 31st December 2014 .......................... 70,000 Accrued expenses at 31st December 2014 ........................ 25,000 Prepaid expenses at 31st December 2014 ......................... 30,000

[1] The receivable days outstanding at 31st December 2014 (to the nearest day)

was: - (a) 12 days (b) 14 days (c) 16 days (d) 18 days [2] The payables days outstanding at 31st December 2014 (to the nearest day)

was: - (a) 23 days (b) 24 days (c) 25 days (d) 26 days [3] The current ratio at 31st December 2014 (assuming no other current assets or

liabilities), to two decimal points, was: - (a) 1.65 :1 (b) 1.17 :1 (c) 1.04 :1 (d) 0.16 :1

AdvancedFinancialAccountingSamplePaper3 Page6of28

Question 2 cont’d [4] The inventory turnover (to two decimal places) for the year ended 31st

December 2014 was: - (a) 8.06 times (b) 7.87 times (c) 7.35 times (d) 1.18 times

[5] The gross profit margin for the year ended 31st December 2014, to one

decimal point was: - (a) 32.2 % (b) 38.6 % (c) 41.9 % (d) 44.3 %

[6] FRS 102 provides that a complete set of Financial Statements comprises the following: (a) A Statement of Comprehensive Income and a Statement of Financial

Position. (b) A Statement of Comprehensive Income, a Statement of Financial

Position and A statement of Changes in Equity. (c) A Statement of Comprehensive Income, a Statement of Financial

Position, a statement of Changes in Equity and A Statement of Cash Flows. (d) A Statement of Comprehensive Income, A Statement of Financial

Position, A statement of Changes in Equity and A Statement of Cash Flows, and notes to the Financial Statements.

[7] FRS 102 states that a business should prepare its financial statements on the

basis that the business is a going concern: - (a) if it is being liquidated (b) if it has ceased trading (c) if the directors have no realistic alternative but to liquidate the entity or

to cease trading (d) only if none of the above situations exist [8] Under the provisions of the Companies Acts there must be shown in a note to

the accounts:

(a) the average number of people employed during the year (b) the number of people employed on the first day of the year (c) the number of people employed on the last day of the year (d) the number of new employees employed during the year

AdvancedFinancialAccountingSamplePaper3 Page7of28

Question 2 cont’d [9] Partners drawings are: - (a) charged against the partners in their capital accounts (b) charged against the partners in their current accounts (c) credited to the partners in their capital accounts (d) credited to the partners in their current accounts [10] Payments by a lessee in an operating lease are:-

(a) charged in the lessee’s Statement of Comprehensive Income on the reducing balance basis

(b) credited in the lessee’s Statement of Comprehensive Income on the reducing balance basis

(c) charged in the lessee’s Statement of Comprehensive Income on the straight line basis

(d) credited in the lessee’s Statement of Comprehensive Income on the straight line basis

AdvancedFinancialAccountingSamplePaper3 Page8of28

QUESTION3

CABLE Ltd., is a furniture company with an authorized share capital of £/€3,000,000, comprised of 6,000,000 ordinary shares of 50 pence/cent each. The following trial balance was extracted as at 31st December 2014

£/€’000 £/€’000

Ordinary share capital .................................................................... 2,200 Share premium account ................................................................. 180 General reserve .............................................................................. 260 Retained earnings balance at 1 January 2014 ................................ 74 8% debenture stock ........................................................................ 250 Leasehold premises at cost ............................................................ 3,900 Leasehold premises – accumulated depreciation at 1 January 2014 ............ 500 Plant and machinery at cost ........................................................... 820 Plant and machinery – accumulated depreciation at 1 January 2014 ........... 320 Motor vehicles at cost .................................................................... 300 Motor vehicles – accumulated depreciation at 1 January 2014 .................. 80 Receivables .................................................................................... 169 Payables ......................................................................................... 95 Bank ............................................................................................... 120 Sales ............................................................................................... 4,500 Sales returns ................................................................................... 79 Opening inventory ......................................................................... 180 Purchases ....................................................................................... 2,400 Purchases returns ........................................................................... 160 Administration expenses ................................................................ 450 Distribution expenses..................................................................... 340 Bank interest .................................................................................. 60 Deposit interest received ................................................................ 35 Debenture interest .......................................................................... 10 Interim ordinary dividend paid ...................................................... 66 ................................................................................................. ________ ______ 8,774 8,774

ADDITIONAL INFORMATION (1) Goods purchased on 28th December 2014 for £/€70,000 had not been

accounted for or included in the physical stock count at 31st December 2014. (2) Closing inventory, as per the physical stock count at 31st December 2014 was

£/€220,000. (3) Training grants of £/€20,000 in respect of training sales staff were due to the

company at 31st December 2014.

AdvancedFinancialAccountingSamplePaper3 Page9of28

QUESTION 3(Cont’d.) (4) Depreciation is to be charged as follows: Leasehold premises ........... 2% on cost Plant and machinery .......... 10% on cost Motor vehicles ................... 20% on cost

Depreciation on leasehold premises and plant and machinery should be

included as part of administration expenses and depreciation of motor vehicles should be included as part of distribution expenses.

(5) The charge for corporation tax for the year ended 31st December 2014 is

estimated at 50% of the profit before tax. (6) A final dividend of 5 pence/cent per share was paid to the ordinary

shareholders on 31 December 2014 however this payment has not yet been recorded in the accounts.

(7) Half year debenture interest to be provided for.

Requirement (a) Prepare, in accordance with FRS 102, the Statement of Comprehensive Income

of CABLE Ltd., for the year ended 31st December 2014 in as far as the information provided permits.

N.B. You are NOT required to prepare a Statement of Financial Position or notes to the accounts. You are required to submit workings to show the make-up of the figures in the Statement of Comprehensive Income.

20 Marks

(b) Prepare a Statement of Changes in Equity for the year ended 31 December

2014 3 Marks

Presentation: 2 marks Total: 25 Marks

AdvancedFinancialAccountingSamplePaper3 Page10of28

SECTION B Answer TWO of the THREE questions in this Section

QUESTION 4 Geoff, Henry and Ian are in partnership sharing profits and losses in the ratio 4:2:2. The partners receive a salary of £/€5,000, £/€6,000 and £/€7,000 each and are entitled to interest on the balance on their capital accounts at 5% per annum. Ian is entitled to a guaranteed share of profits, in addition to his salary and interest on capital, of £/€6,000 any deficiency to be borne by Geoff and Henry equally. The following is the draft balance sheet of the partnership as at 31 December 2014 (before the profit for the year has been divided between the partners).

DRAFT Statement of Financial Position as at 31st DECEMBER 2014

Cost Accumulated Net Book Depreciation Amount £/€ £/€ £/€ Non-current Assets Premises ..................................................... 250,000 50,000 200,000 Plant and machinery .................................. 130,000 65,000 65,000 Furniture and fittings ................................. 25,000 5,000 20,000 405,000 120,000 285,000

Current Assets Inventory .................................................. 30,000 Trade receivables ...................................... 26,000 Bank.......................................................... 12,000 68,000

................................................................... 353,000

Partners Capital Accounts Geoff ......................................................... 80,000 Henry ........................................................ 70,000 Ian ............................................................. 70,000 220,000 Partners Current Accounts Geoff ......................................................... 16,000 Henry ........................................................ (20,000) Ian ............................................................. 10,000 6,000 Profit for the year (not yet divided between the partners) 88,000 Current liabilities Payables .................................................... 26,000 Loan from Simon ...................................... 13,000 39,000 Total capital and liabilities 353,000

AdvancedFinancialAccountingSamplePaper3 Page11of28

QUESTION 4 (Cont’d.) Adjustment is required in respect of the following items: (1) Depreciation for the year has not been provided. It should be provided for as

follows:

Premises ..................... £/€5,000 Plant and machinery ..... £/€26,000 Furniture and fittings ..... £/€5,000 (2) Wages and salaries of £/€14,000 have not been provided for at the year end.

(3) Rent amounting to £/€7,000 has been prepaid at the year end.

Requirement You are required to prepare: (a) a statement setting out the adjustments required to the profit for the year

arising out of items (1) to (3) above;

3 Marks (b) a statement setting out the appropriation of the adjusted profit between the

partners; 3 Marks

(c) the current accounts of the partners;

4 Marks (d) the revised balance sheet after dealing with parts (a) to (c) above.

8 Marks Presentation: 2 marks

Total: 20 Marks

AdvancedFinancialAccountingSamplePaper3 Page12of28

QUESTION 5 JEWEL Limited, a car rental company, had revenue of £/€4,500,000 and made a net profit before taxation of £/€350,000 for the year ended 31st December 2014, as per the draft accounts. During a review of the draft accounts you ascertain the following: (1) A customer who owed the company £/€80,000 at 31st December 2014 has

gone into receivership in January 2015 and is unlikely to be able to pay any part of the debt.

(2) A government grant of £/€50,000 to help meet the cost of wages and salaries

to train staff was treated as deferred income at 31st December 2014. (3) Inventory which cost £/€175,000 was found to be damaged and it is

estimated that it has a net realisable value of £/€125,000. (4) On 6th January 2015 goods costing £/€60,000 were received which had been

ordered from a supplier on 20th December 2014.

(5) A customer of the company is suing the company for £/€600,000 damages on the basis that a car which the customer rented from the company in December 2014 was mechanically deficient and was the cause of the customer being involved in an accident which resulted in the customer being badly injured. The company’s lawyers are unsure as to the company liability. The court case will not take place until after the accounts are approved by the directors.

(6) Wages due to casual workers, who were recruited for the busy Christmas

period, of £/€17,000, were due at 31st December 2014 and not yet accounted for.

Requirement

(a) Prepare the journal entries to show how each of the above items should be dealt with in the final accounts for the year ended 31st December 2014. You should use your understanding of FRS 102 in dealing with each item.

14 marks

(b) Compute the adjusted net profit before taxation for the year ended 31 December 2014 taking into account the adjustments made at [a] above.

4 marks Presentation: 2 marks

Total: 20 Marks

AdvancedFinancialAccountingSamplePaper3 Page13of28

QUESTION6

The Statement of Comprehensive Income of OLIVE Ltd., for the year ended 31st December 2014 and the Statement of Financial Position as at 31st December 2014 (with comparative figures as at 31st December 2007) are as follows:

StatementofComprehensiveIncomefortheyearended31stDecember2014 £/€’000 £/€’000

Revenue.................................................................................. 5,100Less:Costofgoodssold................................................... 3,300GrossProfit........................................................................... 1,800Governmentgrant.............................................................. 10Less:Expenses

LossondisposalofPropertyPlantandEquipment........................................... 10

Depreciation................................................................ 120Otheradministrationexpenses........................... 440Distributionexpenses.............................................. 390 (960)

ProfitfromOperations..................................................... 850

Debentureinterestpaid.................................................. (60)Depositinterestreceived................................................ 20

(40)Profitbeforetax.................................................................. 810

Taxation

Onprofitsfortheyear............................................. (320)Underprovidedinpreviousyears...................... (80)

(400)Totalcomprehensiveincomefortheyear 410

AdvancedFinancialAccountingSamplePaper3 Page14of28

Question6cont’dStatementofFinancialPositionasat31STDECEMBER

2014 2013 £/€’000 £/€’000 £/€’000 £/€’000

AssetsNoncurrentassets

Property,plantandequipment.............. 1,880 1,480Currentassets

Inventories...................................................... 160 304Receivables...................................................... 692 520Bank.................................................................... 596 480 1,448 1,304

Totalassets 3,328 2,784EquityandLiabilitiesCapitalandreserves

Ordinarysharecapital................................ 1,100 1,000Sharepremiumaccount 100 ‐Retainedprofits 970 720 2,170 1,720

NoncurrentliabilitiesDebenturestock.............................................. 350 200

Currentliabilities

Payables............................................................ 448 384Taxation............................................................ 320 480Deferredincome(govtgrant)................. 40 ‐

808 864 Totalequityandliabilities 3,328 2,784

NOTES to the accounts: (1) The profit on ordinary activities before taxation has been arrived at after

charging:

Auditors remuneration ............. 24 Directors remuneration ............ 80 Depreciation .......................... 120

AdvancedFinancialAccountingSamplePaper3 Page15of28

(2) Property plant and equipment:

During the year ended 31st December 2014, OLIVE Ltd., sold for £/€40,000 an asset which cost it £/€120,000 in 2011 and which had been depreciated by £/€70,000 at the date of sale. There were no other sales of property plant and equipment during the year.

(3) A government grant of £/€50,000 relating to plant and equipment purchased during the year was received.

(4) Dividends paid during the year amounted to £/€160,000. Requirement

Prepare a Statement of Cash Flow for OLIVE Ltd., for the year ended 31st December 2014, in accordance with FRS 102.

18 marks Presentation: 2 marks

Total: 20 Marks

AdvancedFinancialAccountingSamplePaper3 Page16of28

AccountingFinancialAccounting

SamplePaper3–SuggestedSolutions

NOTE: Thissamplepaperandsolutionshavebeenpreparedtoreflecttheprovisionsof

FRS100–FRS102

AdvancedFinancialAccountingSamplePaper3 Page17of28

Solutiontoquestion1

(i) (a)

TheFRCdevelopedtheConceptualFrameworktoprovideguidancefortheapplicationofgenerallyacceptedaccountingprinciplestofinancialtransactions.Theprinciplesofthe frameworkformthebasis for thedevelopmentofnewaccountingstandardsandtheassessmentandrevisionwherenecessaryofexistingones.TheFrameworkisnotanaccountingstandardhowevernewstandardsissuedfollowingthepublicationoftheFrameworkmustbeinlinewiththeprinciplesoftheFramework.Goingforwardtheincidents of conflict between the Framework and accounting standards will reducethusleadingtoincreasedharmonisationinfinancialaccountingregulations.HoweverastheFrameworkisnotanaccountingstandarditcannotoverridetheprinciplesofanexistingaccountingstandard,wherea conflictexists theprinciplesas laidout in thestandardmustbecompliedwith.The framework also provides very important definitionswhichwere not previouslydefined, including the definitions of such frequently used terms such as asset andliability.Thiseliminatestheneedtoprovidesuchdefinitionsineachstandardtherebydecreasingthetimeittakestodevelopandpublishnewstandards.Overall, the Framework promotes amore consistent regulatory environmentwhichshouldhelpnotonlystandardsettingbodiesbutalsopreparersoffinancialstatementsandusersofsuchfinancialinformation.

(b)Definitions

GoingconcernFinancial statements are normally prepared on the assumption that an entity is a goingconcernandwill continue inoperation for the foreseeable future. Foreseeable future isconsideredtobetwelvemonthsfromthedatethefinancialstatementsaresigned.Intheevent thatmanagement decide that it is no longer appropriate to prepare the financialstatementsonagoingconcernbasisthismustbedisclosed.AccrualsFinancialstatements,withtheexceptionof thecash flowstatement,arepreparedontheaccrualsbasisofaccountingwheretransactionsarerecognisedintheperiodinwhichtheyoccur (are earned or accrued) irrespective of when the cash flow arising from thesetransactionsoccurs.AssetAnasset is a resource controlledby anentity as a result of past events and fromwhichfuture economic benefits are expected to flow to the entity. Future economic benefitsrepresent the potential to contribute to the cash flow of the entity. Examples of assetsincludepremises,equipment,receivables.Liability

AdvancedFinancialAccountingSamplePaper3 Page18of28

A liability isapresentobligationof theentityarising frompastevents, thesettlementofwhich is expected to result in an outflow of resources from the entity. Examples ofliabilitiesincludepayables,financeleaseobligations,accruals.

(ii) AccountingPolicies

FRS102definesAccountingPoliciesas“thespecificprinciples,bases,conventions,rulesandpracticesappliedbyanentityinpreparingfinancialstatements.”Anentityshouldchangeanaccountingpolicyonlyifthechange:

isrequiredbyaStandardoranInterpretation,or resultsinthefinancialstatementsprovidingreliableandmorerelevant

informationabouttheeffectsoftransactions,othereventsorconditionsontheentity’sfinancialposition,financialperformanceorcashflows.

AccountingEstimatesAccountingestimatesinvolvejudgementsontheuncertaintiesinherentinbusinessactivitieswhichcannotbemeasuredwithprecisionbutonlyestimated.Examplesofitemsmaywhichrequireaccountingestimatesare:

Provisionforbadanddoubtfuldebts Inventoryobsolescence Usefullifeofdepreciableassets

AdvancedFinancialAccountingSamplePaper3 Page19of28

Solutiontoquestion2(1) C (80,000*365/1,800,0000)(2) C (85,000*365/1,250,000)(3) B (170,000+80,000+30,000)/(85,000+60,000+70,000+25,000)(4) B (140,000+1,250,000–170,000)/((140,000+170,000)/2)(5) C (2,100,000–(140,000+1250,000–170,000)=880,000*100/210,000(6) D(7) D(8) A(9) B(10)C

AdvancedFinancialAccountingSamplePaper3 Page20of28

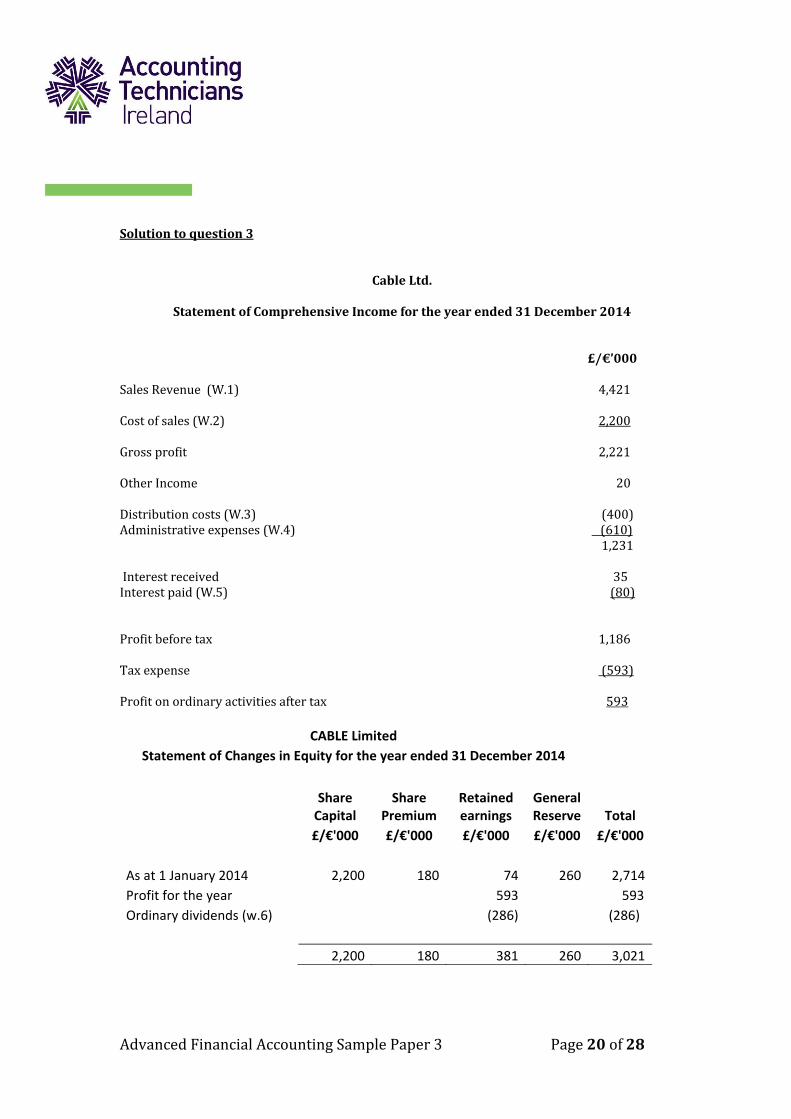

Solutiontoquestion3

CableLtd.

StatementofComprehensiveIncomefortheyearended31December2014

£/€’000SalesRevenue(W.1) 4,421Costofsales(W.2) 2,200Grossprofit 2,221OtherIncome 20 Distributioncosts(W.3) (400)Administrativeexpenses(W.4) (610) 1,231Interestreceived 35Interestpaid(W.5) (80)Profitbeforetax 1,186Taxexpense (593)Profitonordinaryactivitiesaftertax 593

CABLE Limited

Statement of Changes in Equity for the year ended 31 December 2014

Share Capital

Share Premium

Retained earnings

General Reserve Total

£/€'000 £/€'000 £/€'000 £/€'000 £/€'000

As at 1 January 2014 2,200 180 74 260 2,714

Profit for the year 593 593

Ordinary dividends (w.6) (286) (286)

2,200 180 381 260 3,021

AdvancedFinancialAccountingSamplePaper3 Page21of28

Solutiontoquestion3(cont’d)Workings £/€’000 £/€’000(1)Salesrevenue SalesperT/B 4,500 Less:salesreturns 79 4,421(2)Costofsales Openinginventory 180 Purchases 2,400 Less:purchasesreturns (160) 2,240 Add:goodspurchasedon28/12 70 2,310 2,490 Less:ClosingInventory Perphysicalcount (220) Add:notaccountedfor (70) (290)

2,200(3)Distributionexpenses PerT/B 340 Depreciation:MotorVeh. 60 400(4)Administrativeexpenses

PerT/B 450Add:Depreciation:Premises 78 PlantandMach. 82 610

(5)Interestpaid Bankoverdraftinterest 60 Debentureinterest Paid 10 Due 10 20 80

Solutiontoquestion3(cont’d)

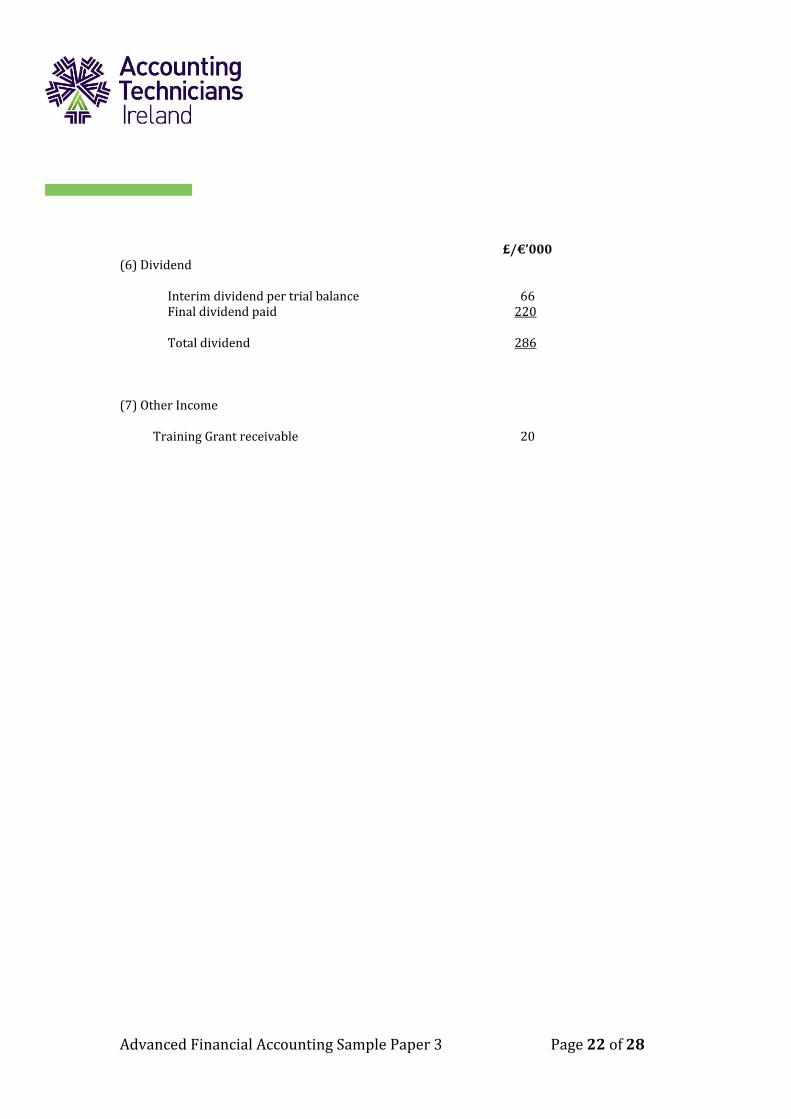

AdvancedFinancialAccountingSamplePaper3 Page22of28

£/€’000(6)Dividend Interimdividendpertrialbalance 66 Finaldividendpaid 220 Totaldividend 286(7)OtherIncome TrainingGrantreceivable 20

AdvancedFinancialAccountingSamplePaper3 Page23of28

Solutiontoquestion4(a) Statementofadjustedprofitfortheyearended31December2014

€/£ €/£ Netprofitasperdraftaccounts 88,000 (1)Depreciation: LeaseholdPremises 5,000

Plant and Machinery 26,000

Furniture & Fittings 5,000

(36,000) (2)Wagesowing (14,000) (3)Rentprepaid 7,000 ______ Adjustednetprofit 45,000 (b) Appropriationaccountfortheyearended31December2014 Netprofit 45,000 Less: Partner’ssalaries Geoff 5,000 Henry 6,000 Ian 7,000 (18,000) Interestoncapital Geoff 4,000 Henry 3,500 Ian 3,500 (11,000) 16,000 Appropriatedasfollows: Geoff 8,000 Less:tomeetguarantee (1,000) 7,000 Henry 4,000 Less:tomeetguarantee (1,000) 3,000 Ian 4,000 Add:tomeetguarantee 2,000 6,000 16,000

AdvancedFinancialAccountingSamplePaper3 Page24of28

Partners Current Accounts Geoff Henry Ian Geoff Henry Ian Balanceb/d 20,000 Balb/d 16,000 10,000 Salaries 5,000 6,000 7,000 Interestoncapital 4,000 3,500 3,500 Shareofprofits 7,000 3,000 6,000Balancec/d 32,000 26,500 Balancec/d 7,500 32,000 20,000 26,500 32,000 20,000 26,500Balanceb/d 7,500 Balanceb/d 32,000 26,500

SolutiontoQ4continuedoverleaf

AdvancedFinancialAccountingSamplePaper3 Page25of28

(d)StatementofFinancialPositionasat31December2014

Cost AccumulatedNBV

Depreciation €/£ €/£€/£

Non-current assets

LeaseholdPremises 250,000 55,000 195,000Plantandmachinery 130,000 91,000 39,000Furniture&Fittings 25,000 10,000 15,000 405,000 156,000 249,000

Current Assets

Inventory 30,000Receivables 26,000Prepaidrent 7,000Bank 12,000 75,000 324,000 PartnerscapitalaccountsGeoff 80,000Henry 70,000Ian 70,000 220,000

Partners current accounts

Geoff 32,000 Henry (7,500)Ian 26,500 51,000CurrentliabilitiesPayables 26,000LoanfromSimon 13,000Accruedwagesandsalaries 14,000 53,000 324,000

AdvancedFinancialAccountingSamplePaper3 Page26of28

Solutiontoquestion5(a)Journal Dr. Cr. £/€ £/€(1) IrrecoverableReceivablea/c (SOCI) 80,000 Receivable(SOFP) 80,000 Beingwriteoffofanirrecoverablereceivable(2) DeferredIncome(SOFP) 50,000 OtherIncome(SOCI) 50,000 Beingcorrectionofmis‐posting;‐RevenuegrantpostedinerrortoDeferredGrants(3) Inventory(SOCI) 50,000 Inventory(SOFP) 50,000 BeingreductionofinventoryfromcosttoNRV(4) Noadjustment;anonadjustingeventasperFRS102(5) Contingentliability,apossiblebutuncertainobligation,noprovisionrequiredasper

FRS102.Showasanotetotheaccounts.(6) Wagesexpense(SOCI) 17,000 Accruedexpense(SOFP) 17,000 (Accountingforwagesaccrueddueatyearendnotprovidedfor) (b) Adjustednetprofitbeforetax £/€ £/€ Profitbeforetaxationperdraftaccounts 350,000 Adjustments: (1)IrrecoverableReceivable (80,000) (2)Traininggrant 50,000 (3)Inventorywriteoff (50,000) (6)Wagesexpense (17,000) (97,000) Adjustednetprofit 253,000

AdvancedFinancialAccountingSamplePaper3 Page27of28

Solutiontoquestion6

OLIVELtd.,StatementofCashFlowfortheyearended31stDecember2014

£/€’000 £/€’000Cashflowfromoperatingactivities:Profitonordinaryactivitiesbeforeinterest 850Adjustmentfor:

Governmentgrant.......................................................................... (10)Depreciation..................................................................................... 120Lossondisposalofpropertyplantandequipment....... 10

120 970

Operatingprofitfromworkingcapitalchanges:Decreaseininventories............................................................... 144Increaseinreceivables................................................................ (172)Increaseinpayables...................................................................... 64

36Cashgeneratedfromoperations.......................................................... 1,006Interestpaid................................................................................................... (60)Incometaxpaid(w.1)................................................................................ (560)

Netcashflowfromoperatingactivities............................................. 386 Cash flow from investing activities:

Purchasesofpropertyplantandequipment(w.2)....... (570)Proceedsofsaleofproperty,plantandequipment....... 40Interestreceived........................................................................... 20

Netcashusedininvestingactivities................................................... (510) (124)

Cash flow from financing activities: Proceedsfromissueofshares(100+100).......................... 200Governmentgrantreceived....................................................... 50Proceedsfromlongtermborrowing..................................... 150Dividendspaid................................................................................ (160) 240

Netincreaseincashandcashequivalents....................................... 116Cashandcashequivalentsatbeginningofyear............................ 480

Cashandcashequivalentsatendofyear......................................... 596

AdvancedFinancialAccountingSamplePaper3 Page28of28

Solution to question 6 (Cont’d.) WORKINGS (1) Incometaxpaid £/€’000

Dueat1stJanuary2014............................................ 480Chargeforyear............................................................. 400 880Dueat31stDecember2014.................................... 320Incometaxpaid............................................................ 560

(2) Purchaseofpropertyplantandequipment £/€’000

Netbookamountat1stJanuary2014................ 1,480Less:netbookamountofsaleDuringyear(£/€120,000‐£/€70,000)........... (50) 1430Depreciationchargeforyear................................. (120) 1310Netbookamountat31stDecember2014........ 1880Purchasesduringyear.............................................. 570