Advance cost and management Accounting ABC costing

17

ACMA TRADITIONAL & ABC COSTING M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 1 Project of Advanced Cost & Management Accounting Dated 7 th March, 2015 Presented to: Prof. Aziz-ur-Rehman

-

Upload

umair-mohsin -

Category

Business

-

view

106 -

download

6

Transcript of Advance cost and management Accounting ABC costing

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 1

Project of Advanced Cost & Management Accounting

Dated 7th March, 2015

Presented to: Prof. Aziz-ur-Rehman

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 2

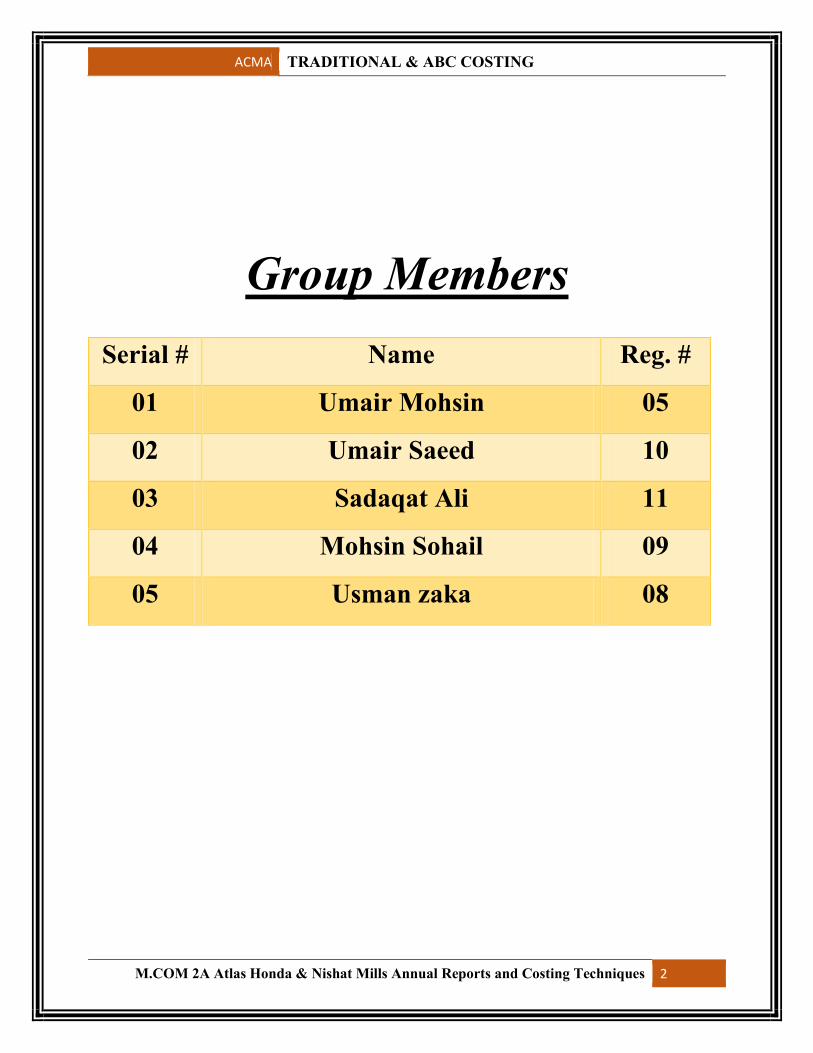

Group Members

Serial # Name Reg. #

01 Umair Mohsin 05

02 Umair Saeed 10

03 Sadaqat Ali 11

04 Mohsin Sohail 09

05 Usman zaka 08

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 3

Acknowledgement

First of all we would like to thank the Almighty Allah for giving us the

strength and the aptitude to complete this Project within due time. We

are deeply indebted to our course teacher Prof. Aziz-ur-Rehman for

assigning us such an interesting topic named “Comparison of

Traditional and ABC costing in Pakistani companies”. We also

express the depth of our appreciation to our honorable course teacher for

his suggestions and guidelines, which helped us in completing this

project.

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 4

Executive Summary This project helped us a lot to understand the costing systems prevailing in the current era. We learnt about the absorption costing system and ABC costing system in our subject of advanced cost and management accounting. We applied these systems to the top Pakistani companies of “Atlas Honda” and “ Nishat Mills” and experience the practical life working in this regard.

We are sure that this project will help us in future in computation of cost of products and we can apply this practice for our preparation of final exams also. At the end we will say that overall very interesting and real life experience it was.

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 5

Vision

Market leader in the motorcycle industry, emerging as a global competitive center of production and exports.

Mission

A dynamic growth oriented company through market leadership, excellent in quality and service and maximizing export, ensuring attractive returns to equity holders, rewarding associates according to their ability and performance, fostering a network of engineers and researchers ensuing unique contribution to the development of the industry, customer satisfaction and protection of the environment by producing emission friendly green products as a good corporate citizen fulfilling its social responsibilities in all respects.

Corporate Goals:

Customers

Our Customers are the reason and the source of our business. It is our joint aim with our dealers to ensure that the customers enjoy the highest level of satisfaction from use of Honda motorcycles.

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 6

Quality

To ensure that our products and services meet the set standards of excellence.

Local Manufacturing

To be the industry leader in indigenization of motorcycle parts.

Technology

To develop and maintain distinct business advantages through continuous induction of improved hard and soft technologies.

Shareholders

To ensure health and viability of business and thus safeguarding shareholders’ interest by maximizing profit. Payment of regular satisfactory dividends and adding value to the shares.

Employees

To enhance and continuously update each member’s capabilities and education and to provide an environment which encourages practical expression of the individual potential in goal directed team efforts and compensate them attractively according to their abilities and performance.

Corporate Citizen

To comply with all Government laws, rules and regulations and to maintain a high standard of ethics in all operations and to act as a responsible member of the society.

Quality Policy:

Commitment to provide high quality motorcycles and parts. Right work in first attempt and on time. Maintain and continuously improve quality. Training of manpower and acquisition of latest technology. Safe, clean and healthy environment. Market leadership and prosperity for all.

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 7

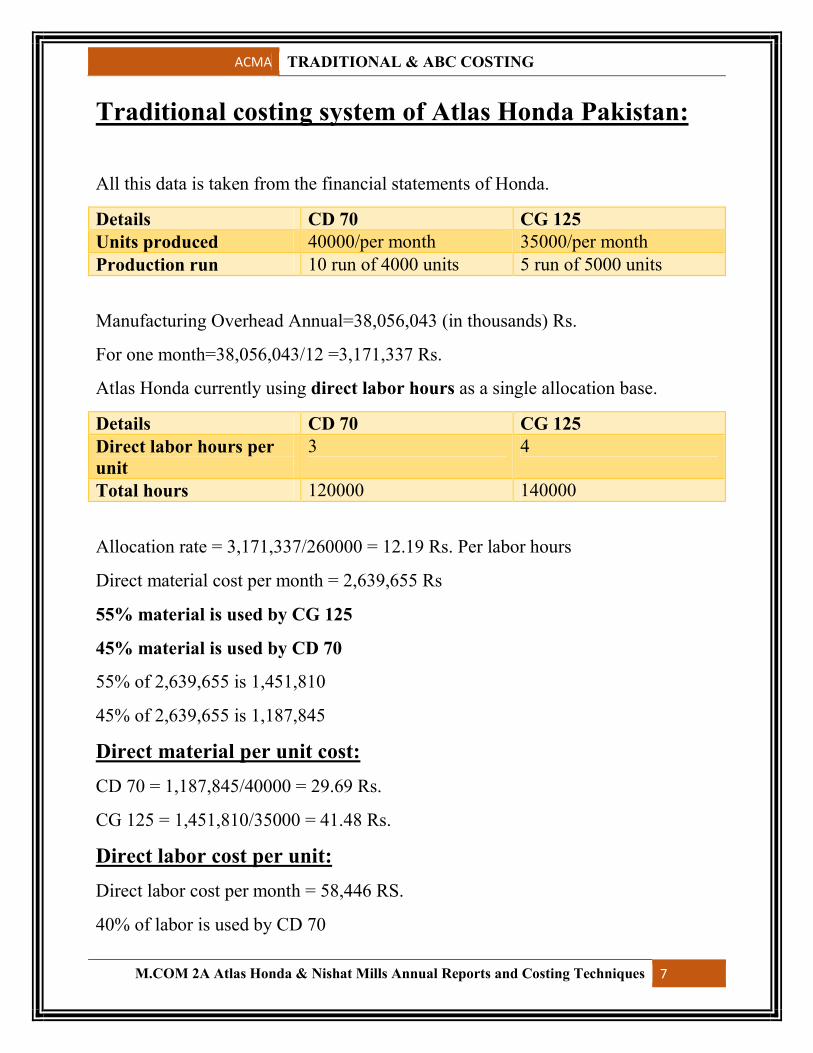

Traditional costing system of Atlas Honda Pakistan:

All this data is taken from the financial statements of Honda.

Details CD 70 CG 125 Units produced 40000/per month 35000/per month Production run 10 run of 4000 units 5 run of 5000 units

Manufacturing Overhead Annual=38,056,043 (in thousands) Rs.

For one month=38,056,043/12 =3,171,337 Rs.

Atlas Honda currently using direct labor hours as a single allocation base.

Details CD 70 CG 125 Direct labor hours per unit

3 4

Total hours 120000 140000

Allocation rate = 3,171,337/260000 = 12.19 Rs. Per labor hours

Direct material cost per month = 2,639,655 Rs

55% material is used by CG 125

45% material is used by CD 70

55% of 2,639,655 is 1,451,810

45% of 2,639,655 is 1,187,845

Direct material per unit cost:

CD 70 = 1,187,845/40000 = 29.69 Rs.

CG 125 = 1,451,810/35000 = 41.48 Rs.

Direct labor cost per unit:

Direct labor cost per month = 58,446 RS.

40% of labor is used by CD 70

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 8

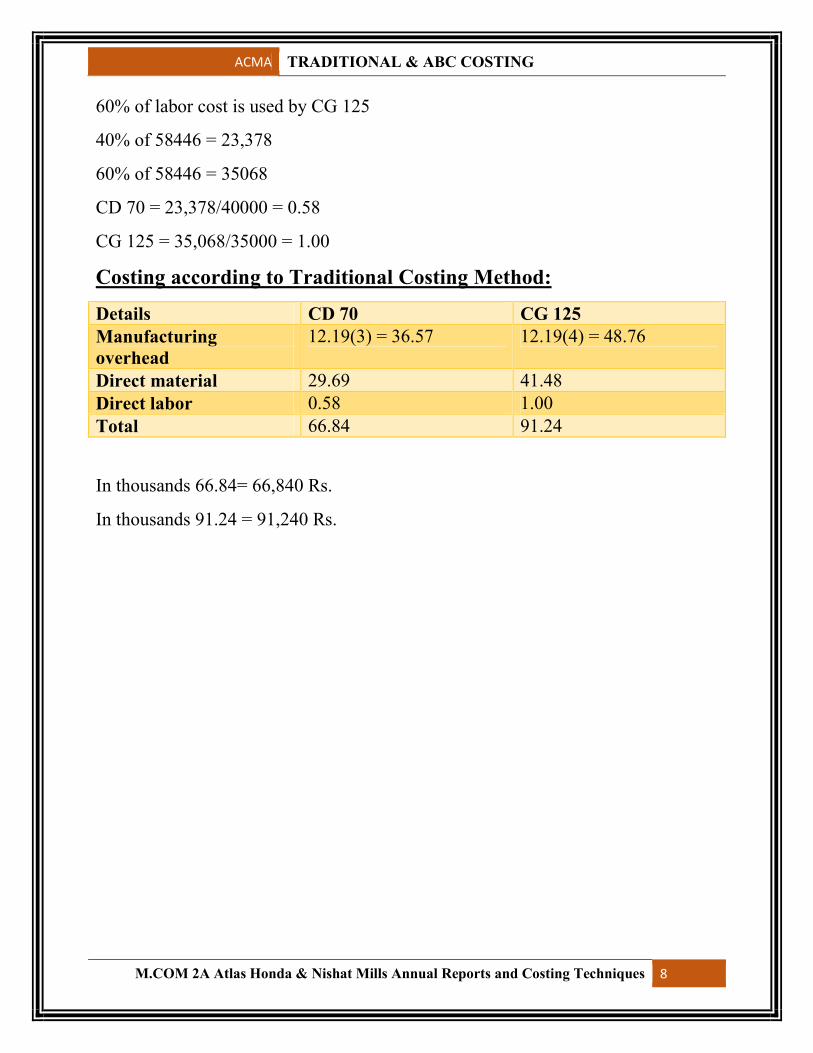

60% of labor cost is used by CG 125

40% of 58446 = 23,378

60% of 58446 = 35068

CD 70 = 23,378/40000 = 0.58

CG 125 = 35,068/35000 = 1.00

Costing according to Traditional Costing Method:

Details CD 70 CG 125 Manufacturing overhead

12.19(3) = 36.57 12.19(4) = 48.76

Direct material 29.69 41.48 Direct labor 0.58 1.00 Total 66.84 91.24

In thousands 66.84= 66,840 Rs.

In thousands 91.24 = 91,240 Rs.

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 9

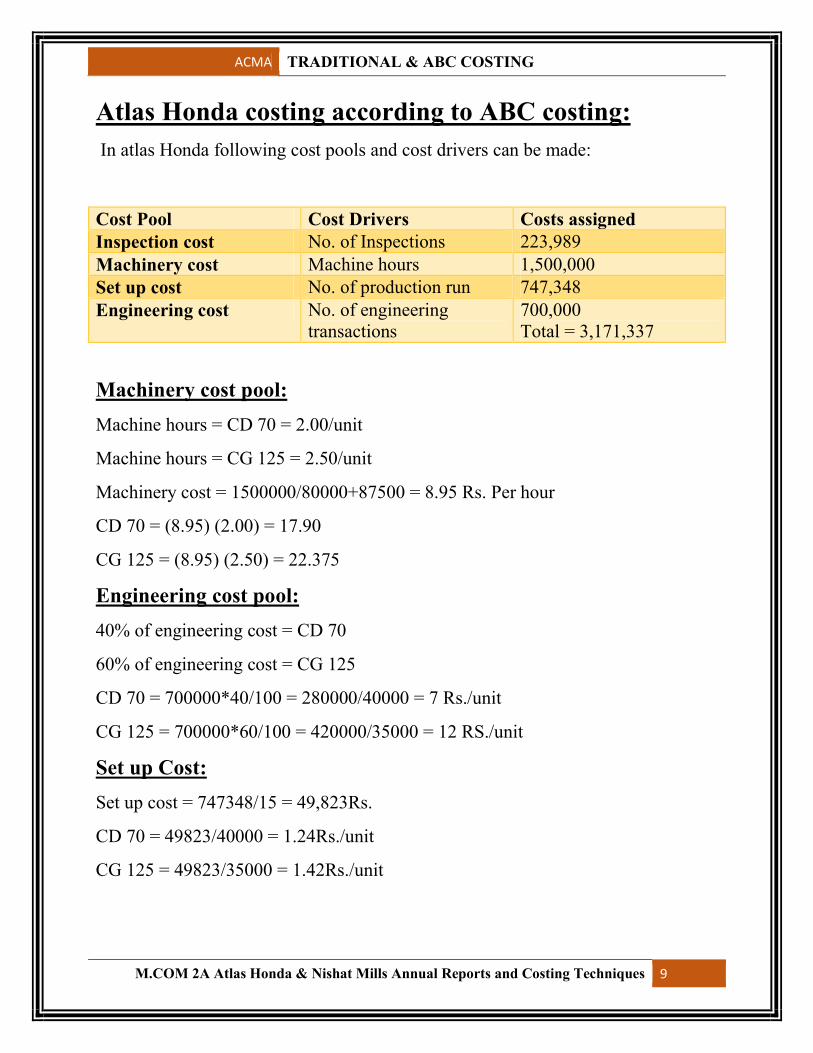

Atlas Honda costing according to ABC costing:

In atlas Honda following cost pools and cost drivers can be made:

Cost Pool Cost Drivers Costs assigned Inspection cost No. of Inspections 223,989 Machinery cost Machine hours 1,500,000 Set up cost No. of production run 747,348 Engineering cost No. of engineering

transactions 700,000 Total = 3,171,337

Machinery cost pool:

Machine hours = CD 70 = 2.00/unit

Machine hours = CG 125 = 2.50/unit

Machinery cost = 1500000/80000+87500 = 8.95 Rs. Per hour

CD 70 = (8.95) (2.00) = 17.90

CG 125 = (8.95) (2.50) = 22.375

Engineering cost pool:

40% of engineering cost = CD 70

60% of engineering cost = CG 125

CD 70 = 700000*40/100 = 280000/40000 = 7 Rs./unit

CG 125 = 700000*60/100 = 420000/35000 = 12 RS./unit

Set up Cost:

Set up cost = 747348/15 = 49,823Rs.

CD 70 = 49823/40000 = 1.24Rs./unit

CG 125 = 49823/35000 = 1.42Rs./unit

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 10

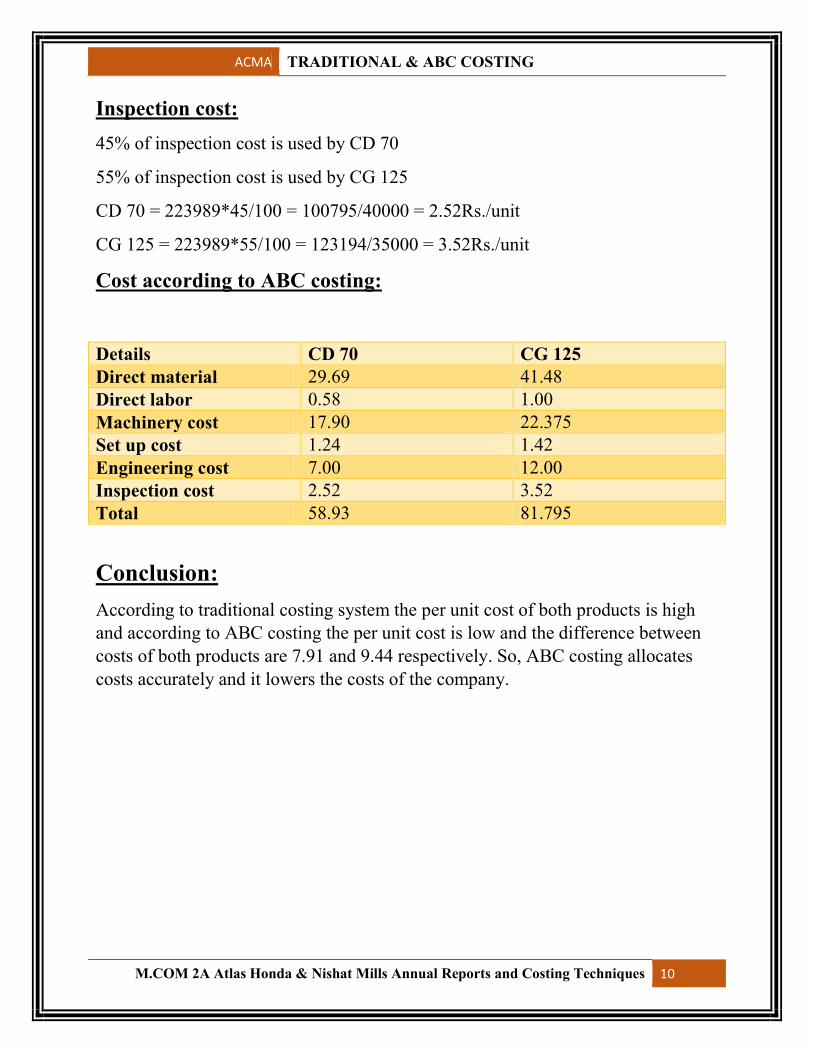

Inspection cost:

45% of inspection cost is used by CD 70

55% of inspection cost is used by CG 125

CD 70 = 223989*45/100 = 100795/40000 = 2.52Rs./unit

CG 125 = 223989*55/100 = 123194/35000 = 3.52Rs./unit

Cost according to ABC costing:

Details CD 70 CG 125 Direct material 29.69 41.48 Direct labor 0.58 1.00 Machinery cost 17.90 22.375 Set up cost 1.24 1.42 Engineering cost 7.00 12.00 Inspection cost 2.52 3.52 Total 58.93 81.795

Conclusion:

According to traditional costing system the per unit cost of both products is high and according to ABC costing the per unit cost is low and the difference between costs of both products are 7.91 and 9.44 respectively. So, ABC costing allocates costs accurately and it lowers the costs of the company.

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 11

Vision Statement

To transform the Company into a modern and dynamic yarn, cloth and processed cloth and finished product manufacturing Company that is fully equipped to play a meaningful role on sustainable basis in the economy of Pakistan. To transform the Company into a modern and dynamic power generating Company that is fully equipped to play a meaningful role on sustainable basis in the economy of Pakistan.

Mission Statement

To provide quality products to customers and explore new markets to promote/expand sales of the Company through good governance and foster a sound and dynamic team, so as to achieve optimum prices of products of the Company for sustainable and equitable growth and prosperity of the Company.

Company Profile

Nishat Mills Limited is the flagship company of Nishat Group. It was established in 1951. It is one of the most modern, largest vertically integrated textile company in Pakistan. Nishat Mills Limited has 198,120 spindles, 655 Toyota air jet looms. The Company also has the most modern textile dyeing and processing units, 2 stitching units for home textile, one stitching unit for garments and Power Generation facilities with a capacity of 89 MW. The Company’s total export for

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 12

the year 2011 was Rs. 36.015 billion (US$ 416 million). Due to the application of prudent management policies, consolidation of operations, a strong balance sheet and an effective marketing strategy, the growth trend is expected to continue in the years to come. The Company's production facilities comprise of spinning, weaving, processing, stitching and power generation.

The Group

Nishat group of companies is a premier business house of Pakistan. The group has presence in all major sectors including Textiles, Cement, Banking, Insurance, Power Generation, Hotel Business, Agriculture, Dairy and Paper Products. Today, Nishat Group is considered to be at par with multinationals operating locally in terms of its quality products and management skills.

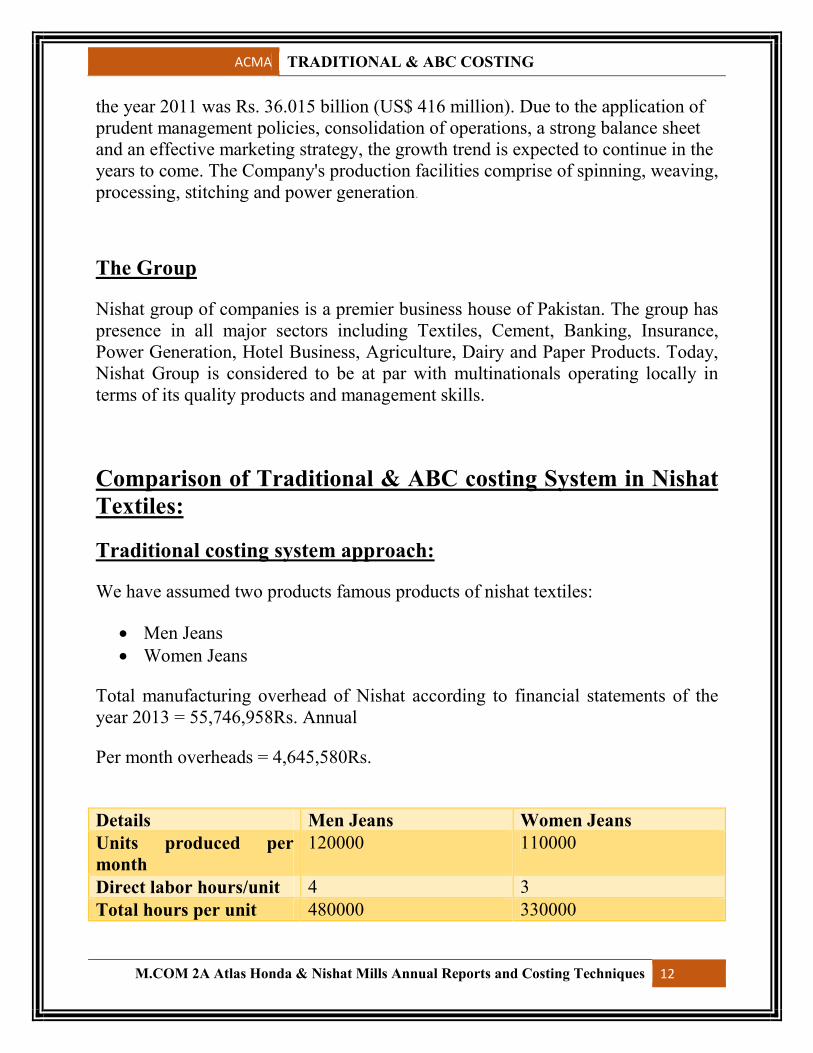

Comparison of Traditional & ABC costing System in Nishat Textiles:

Traditional costing system approach:

We have assumed two products famous products of nishat textiles:

Men Jeans Women Jeans

Total manufacturing overhead of Nishat according to financial statements of the year 2013 = 55,746,958Rs. Annual

Per month overheads = 4,645,580Rs.

Details Men Jeans Women Jeans Units produced per month

120000 110000

Direct labor hours/unit 4 3 Total hours per unit 480000 330000

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 13

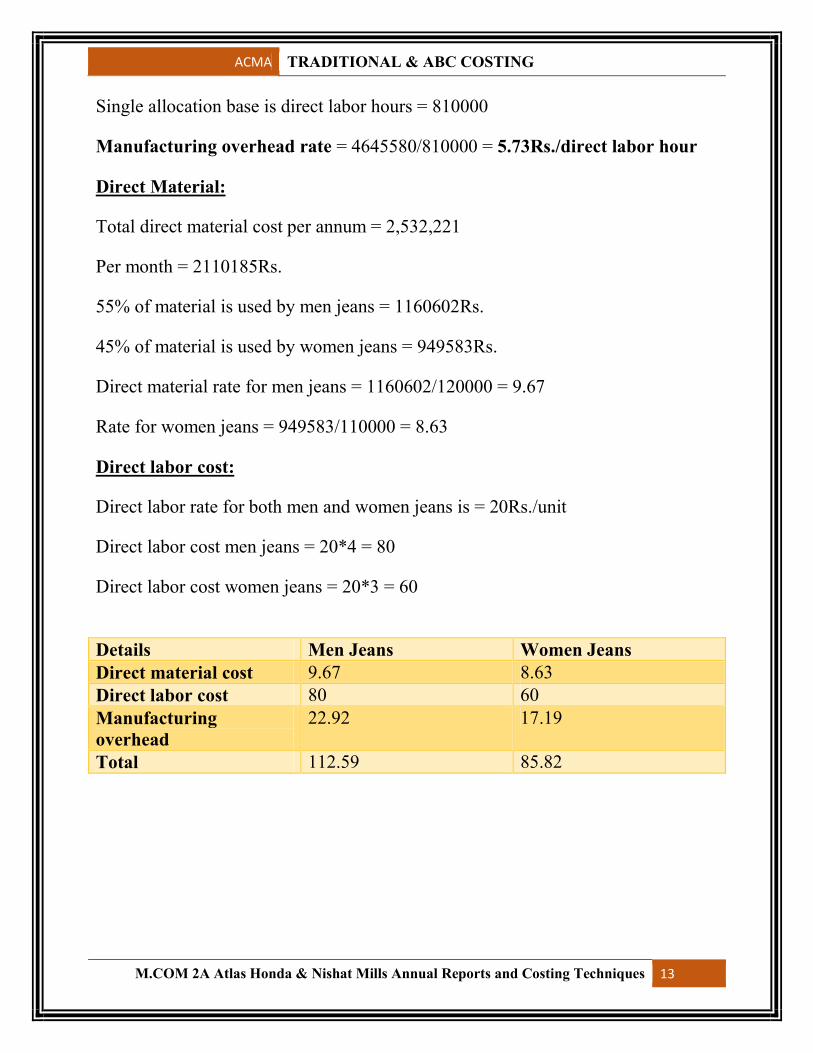

Single allocation base is direct labor hours = 810000

Manufacturing overhead rate = 4645580/810000 = 5.73Rs./direct labor hour

Direct Material:

Total direct material cost per annum = 2,532,221

Per month = 2110185Rs.

55% of material is used by men jeans = 1160602Rs.

45% of material is used by women jeans = 949583Rs.

Direct material rate for men jeans = 1160602/120000 = 9.67

Rate for women jeans = 949583/110000 = 8.63

Direct labor cost:

Direct labor rate for both men and women jeans is = 20Rs./unit

Direct labor cost men jeans = 20*4 = 80

Direct labor cost women jeans = 20*3 = 60

Details Men Jeans Women Jeans Direct material cost 9.67 8.63 Direct labor cost 80 60 Manufacturing overhead

22.92 17.19

Total 112.59 85.82

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 14

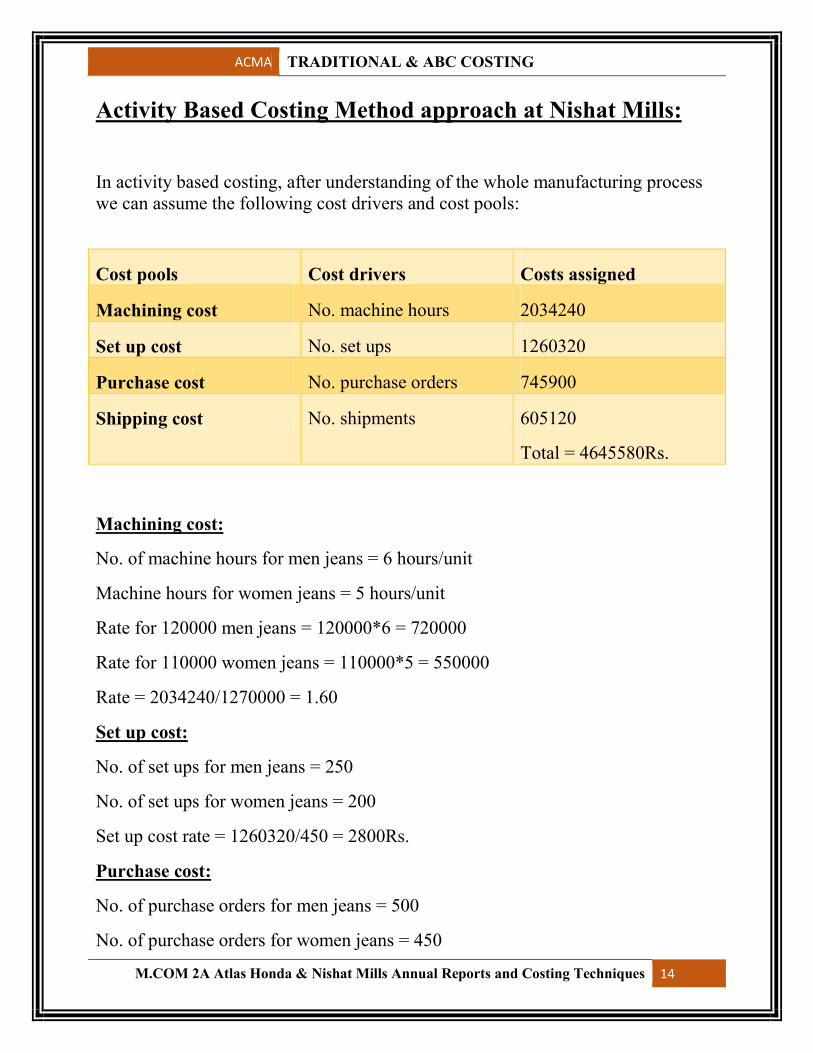

Activity Based Costing Method approach at Nishat Mills:

In activity based costing, after understanding of the whole manufacturing process we can assume the following cost drivers and cost pools:

Cost pools Cost drivers Costs assigned

Machining cost No. machine hours 2034240

Set up cost No. set ups 1260320

Purchase cost No. purchase orders 745900

Shipping cost No. shipments 605120

Total = 4645580Rs.

Machining cost:

No. of machine hours for men jeans = 6 hours/unit

Machine hours for women jeans = 5 hours/unit

Rate for 120000 men jeans = 120000*6 = 720000

Rate for 110000 women jeans = 110000*5 = 550000

Rate = 2034240/1270000 = 1.60

Set up cost:

No. of set ups for men jeans = 250

No. of set ups for women jeans = 200

Set up cost rate = 1260320/450 = 2800Rs.

Purchase cost:

No. of purchase orders for men jeans = 500

No. of purchase orders for women jeans = 450

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 15

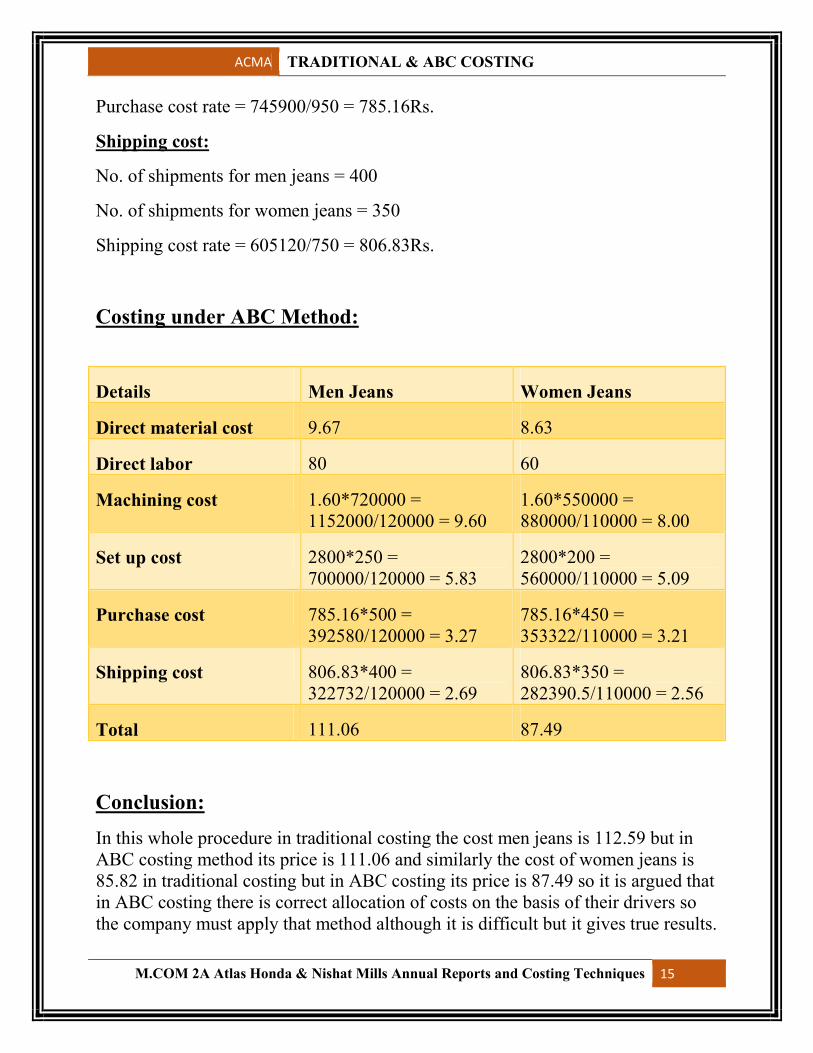

Purchase cost rate = 745900/950 = 785.16Rs.

Shipping cost:

No. of shipments for men jeans = 400

No. of shipments for women jeans = 350

Shipping cost rate = 605120/750 = 806.83Rs.

Costing under ABC Method:

Details Men Jeans Women Jeans

Direct material cost 9.67 8.63

Direct labor 80 60

Machining cost 1.60*720000 = 1152000/120000 = 9.60

1.60*550000 = 880000/110000 = 8.00

Set up cost 2800*250 = 700000/120000 = 5.83

2800*200 = 560000/110000 = 5.09

Purchase cost 785.16*500 = 392580/120000 = 3.27

785.16*450 = 353322/110000 = 3.21

Shipping cost 806.83*400 = 322732/120000 = 2.69

806.83*350 = 282390.5/110000 = 2.56

Total 111.06 87.49

Conclusion:

In this whole procedure in traditional costing the cost men jeans is 112.59 but in ABC costing method its price is 111.06 and similarly the cost of women jeans is 85.82 in traditional costing but in ABC costing its price is 87.49 so it is argued that in ABC costing there is correct allocation of costs on the basis of their drivers so the company must apply that method although it is difficult but it gives true results.

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 16

CONCLUSIONS AND FINDINGS

Globalization and the increasing complexity of business, together with high-powered computing technology, have contributed to the development of new management accounting techniques all over the world. The present study shows that the survey result of the present practices of management accounting in listed manufacturing sector reveals the state of use of the sophisticated technique like Activity Based Costing in Pakistan is not satisfactory.

There are several reasons behind it. First of all in many local offices still they are practicing manual techniques and since the financial officers or chief accountant or top managers are quite old and hence they are quite back dated in some cases. They don’t adopt new technologies and techniques, as they feel happy with their old techniques. This situation is gradually changing when the new blood is entering into the company or they see the practice in other foreign company. In many offices the processes are not well defined and as a result there is no dedicated cost center for a particular operation or the fixed cost and variable cost is defined. Due to have lack of defined process it become difficult in many cases to implement a costing model like ABC. That is why in spite of being well aware of the ABC or such modern cost model many companies couldn’t implement it because it requires changing their whole process, which is little, complicated. Another problem in Pakistan is lack of using software/tools in the different operations. Although new generation guys are well computer educated but the previous generation are not well computer literate and even if they know how to use it, in many cases they are reluctant to use those tools.

To keep pace with the world changing management accounting environment, Pakistani firms should use the newly developed techniques. A well-balanced practice of such techniques irrespective of the sectors may be enhanced through compulsory enactment of cost and management accounting audit in Pakistan .

ACMA TRADITIONAL & ABC COSTING

M.COM 2A Atlas Honda & Nishat Mills Annual Reports and Costing Techniques 17