Advac Ipt-Inventory (Ch.5) Gs 2013

25

Ch. 5 Intercompany Profit Transactions-Inventory

-

Upload

alief-vidi -

Category

Documents

-

view

232 -

download

0

description

Advac Ipt-Inventory (Ch.5) Gs 2013 th

Transcript of Advac Ipt-Inventory (Ch.5) Gs 2013

Ch. 5 Intercompany Profit Transactions-

Inventory

The Reporting Entity

SubsidiaryFinancialStatements_____ __________ __________ __________ _____

SubsidiaryFinancialStatements_____ __________ __________ __________ _____

ConsolidatedFinancialStatements_____ _____ ____ __________ __________ _____

ConsolidatedFinancialStatements_____ _____ ____ __________ __________ _____

ParentFinancialStatements_____ __________ __________ __________ _____

ParentFinancialStatements_____ __________ __________ __________ _____

Identifiable NAIntangible excess

EliminateReciprocal Account

Down-stream

Up-stream

20

24 24

30 30

204

6

P S

Inventory

CoS Sales

20 20

20 24

Inventory

CoS Sales

24 24

24 30

Profit P = 4 recognized all

Intercompany Transactions

• Consolidated Financial Statement:– "intercompany balances and transaction"

• As if this transaction (IPT-Inventory) had never occured

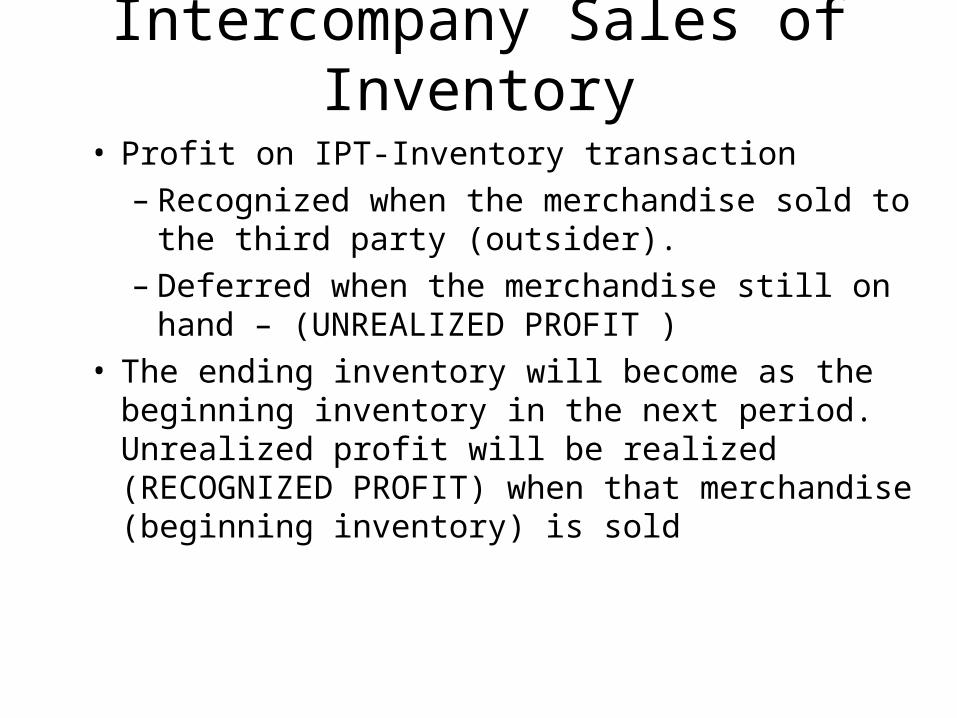

Intercompany Sales of Inventory

• Profit on IPT-Inventory transaction– Recognized when the merchandise sold to the

third party (outsider).– Deferred when the merchandise still on hand –

(UNREALIZED PROFIT )• The ending inventory will become as the beginning

inventory in the next period. Unrealized profit will be realized (RECOGNIZED PROFIT) when that merchandise (beginning inventory) is sold

20

24 24

30 30

204

P S

6

Parent Subsidiary CFS

Sales 24 30 30

Cost of Sales 20 24 20

Gross Profit 4 6 10

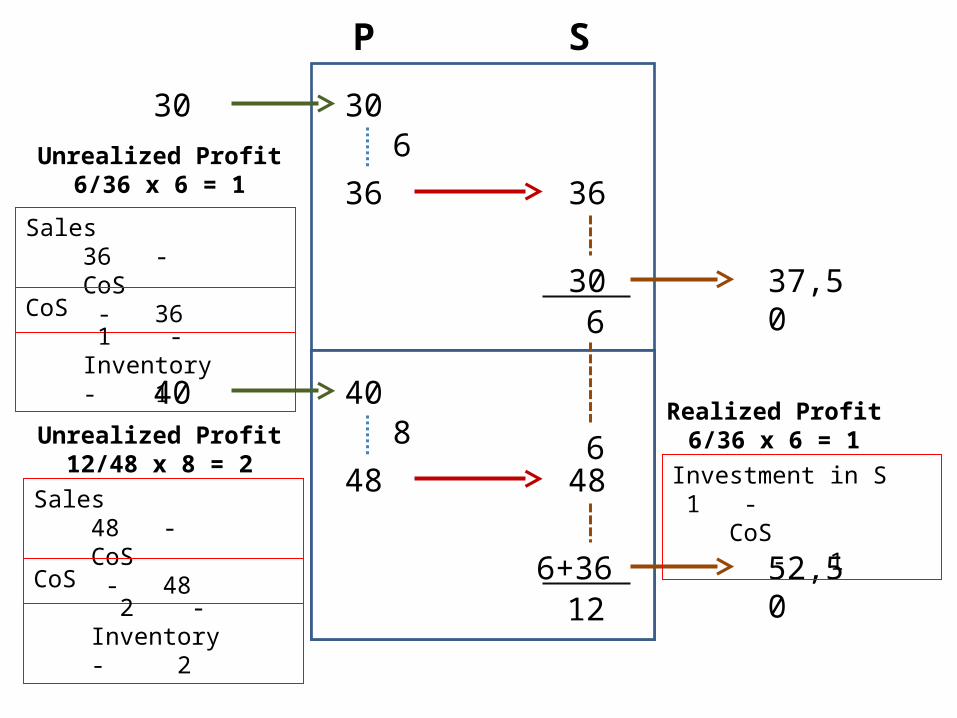

30

36 36

30 37,50

306

P S

6

P profit recognized partly, the rest is the

Unrealized Profit

End. Invent S =6 P profit that unrealized = 6/36 x 6 = 1

UnRealized Profit = 1UnRealized Profit = 1

Sales-purchase transactions between P and S as if never happenned (36)

30

36 36

30 37,50

306

P S

6

Unrealized Profit6/36 x 6 = 1

40

48 48

6+36 52,50

408

12

6Unrealized Profit12/48 x 8 = 2

Realized Profit6/36 x 6 = 1

Sales 36 - CoS - 36

CoS 1 - Inventory - 1

Sales 48 - CoS - 48

CoS 2 - Inventory - 2

Investment in S 1 - CoS - 1

Parent Subsidi Adjust & Elim CFS

INCOME STAT

Sales 36 37,5 a. 36 37.5

Cost of Sales 30 30 b. 1 a. 36 25

Gross Profit 6 7,5 12,5

BALANCE SHT

Inventory 6 b 1

a Sales 36 - CoS - 36

b CoS 1 - Inventory - 1

Parent Subsidi debit credit CFS

Sales 48 52,5 a. 48 52.5

Cost of Sales 40 42 b. 2 a 48c 1

35

Gross Profit 8 10.5 17,5

Balance Sheet

Inventory 6 b 2

Investment in S c 1

a Sales 48 - CoS - 48

b CoS 2 - Inventory - 2

c Investment in S 1 - CoS - 1

Adjust & Elim

DOWN-STREAM dan UPSTREAM

P

SThe merchandise (EI) in S

The merchandises (EI) in PURP belongs to PIFS will be effectedNCI share will NOT be effected

URP belongs to SShare of P and NCI will be effected

DS US

Effects of DS & US to ShareParent Subsidiary

80%

Sales 600 300Cost of Sales (300) (180) Gross Profit 300 120Expenses (100) (70) Parent’s separate income 200 Subsidiary Net Income 50

Sales between afiliated company $100,000

UNREALIZED Profit in EI 20,000

Effects of DS & US transactions to NI-S Share

DS

US

NI-S Share

NI-S Share

80% x (50,000) = 40,000

20% x 50,000 = 10,000

80% x (50,000-20,000) = 24,000

20% x (50,000-20,000) = 6,000

P

NCI

P

NCI

P profit is deducted by URP 20,000

How is the impact when the company has the BEGINNING INVENTORY?

DOWNSTREAM-Unrealized ProfitIncome Statement 31 Des 2011

Porter Sorter

90%

Sales 100 50Cost of Sales (60) (25) Gross Profit 40 15Expenses (15) (5) Operating income 25 10 Income from Sorter 9NET INCOME 34 10

P sales incl. transaction with Sorter $15,000 with $6,250 as profit

S Ending inventory incl 40% merchandise from Porter

Entry in Porter’s book 2011

Investment in Sorter 9,000

Income from Sorter 9,000

Income from Sorter 2,500

Investment in Sorter 2,500

IFS = 90% x 10,000 = 9,000

Unrealized Profit 40% x 6,250 = 2,500

DS URP-EI 2011Sot Adjustment & Elim

Pot 90% D C CFSIncome Statement

Sales 100.0 50 a 15.0 135.0 IFS 6.5 c 6.5 - Cost of Sales (60.0) (35) b 2.5 a 15.0 (82.5) Expenses (15.0) (5) (20.0) CNI 32.5 NCI-Share

10%x10,000 (1.0)

CI share 31.5 10 31.5

Balance SheetInventory 7.5 b 2.5

Invest in S xxx c 6.5

DOWNSTREAM- Realized ProfitIncome Statement 31 Des 2012

Porter Sorter

90%

Sales 120 60Cost of Sales (80) (40) Gross Profit 40 20Expenses (20) (5) Operating income 20 15 Income from Sorter 13,5NET INCOME 33.5 15

2010 no transaction between P and S

All beginning Inventory from Porter is sold

Entry on Pot’s book 2012

Investment in Sorter 13,500

Income from Sorter 13,500

Investment in Sorter 2,500

Income from Sorter 2,500

IFS 90% x 15,000 = 13,500

Realized Profit 40% x 6,250 = 2,500

DS URP-EI 2012Sot Adjustment & Elim

Pot 90% D C CFSIncome Statement

Sales 120.0 60 180.0 IFS 16.0 b 16.0 - Cost of Sales (80.0) (40) a 2.5 (117.5) Expenses (20.0) (5) (25.0) CNI 37.5 NCI-Share

10%x15,000 (1.5)

CI share 36.0 15 36.0

Balance SheetInventory 7.5

Invest in S xxx a 2.5 b 16.0

UPSTREAM- UNRealized Profit 2011

During 2011 Sal Co (Subsidiary, 75%) sold its merchandise to Par Co (Parent) $20,000. Cost of sales $7,500. At the end of the year, 40% of that mechandise still on hand.Net Income Sal during 2009 was $50,000

Entries in Par’s book 2011

Investment in Sal 37,500

Income from Sal 37,500

Income from Sal 3,750

Investment in Sal 3,750

IFS 75% x 50,000 = 37,500

Inventory di Par 40% x $20,000 = $8,000Total URP = 40% x ($20,000-$7,500)= $5,000UNRealized Profit 75% x 5,000 = 3,750

US URP-EI 2011Sal Penyesuaian & elim LK

Par 75% D C CFSIncome Statement

Sales 250 150 a 20 380 IFS 33.75 c 33.75 - Cost of Sales (100) (80) b 5 a 20 (165) Expenses (50) (20) (70) CNI 145 NCI-Share

(50,000-5,000)x25% (11.25)

CI share 133.75 50 133.75

Balance SheetInventory 10 b 5

Invest in S xxx c 33.75

UPSTREAM- Realized Profit 2010

2012 No more transactions between

Par and Sal

Par inventory purchased from Sal is sold

Entries in Par’s book 2012

Investment in Sal 45,000

Income from Sal 45,000

Investment in Sal 3,750

Income from Sal 3,750

IFS 75% x 60,000 = 45,000

Realized Profit 75% x 5,000 = 3,750

US RP-BI 2012Sal Adjustment & Elim

Par 75% D C CFSIncome Statement

Sales 275.0 160 435 IFS 48.8 b 48.75 - Cost of Sales (120.0) (85) a 5.00 (200) Expenses (60.0) (15) (75) CNI 160 NCI-Share

(60,000+5,000)x25% (16.25)

CI share 143.8 60 143.75

Balance SheetInvest in S xxx a 3.75 b 48.75

NCI a 1.25