Addendum to the ECB Guide on options and … to the ECB Guide on options and discretions available...

17

Addendum to the ECB Guide on options and discretions available in Union law August 2016

Transcript of Addendum to the ECB Guide on options and … to the ECB Guide on options and discretions available...

Addendum to the ECB Guide on options and discretions available in Union law

August 2016

Addendum to the ECB Guide on options and discretions available in Union law 1

Introduction

(1) This document sets out the ECB’s approach to the exercise of some options and discretions provided for in Regulation (EU) 575/2013 of the European Parliament and of the Council1 (CRR) and Directive 2013/36/EU of the European Parliament and of the Council2 (CRD IV) and granted to competent authorities. It aims to provide coherence, effectiveness and transparency regarding the supervisory policy that will be applied in the supervisory assessment of applications from significant supervised entities within the Single Supervisory Mechanism. The assessment will be carried out according to the relevant provisions of the CRR and Commission Delegated Regulation (EU) 2015/61 of 10 October 2014 to supplement Regulation (EU) No 575/2013 of the European Parliament and the Council with regard to liquidity coverage requirement for Credit Institutions (Commission Delegated Regulation (EU) 2015/61) and in line with national legislation transposing the relevant provisions of CRD IV.

1 Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on

prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012 (OJ L 176, 27.6.2013, p. 1).

2 Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms, amending Directive 2002/87/EC and repealing Directives 2006/48/EC and 2006/49/EC.

Addendum to the ECB Guide on options and discretions available in Union law 2

Section II The ECB’s policy and criteria for the exercise of options and discretions in the CRR and CRD IV

Chapter 1 Consolidated supervision and waivers of prudential requirements

3. CAPITAL WAIVERS (Article 7 of the CRR)

In the subparagraph “Article 7(1) of the CRR, on the waiver of requirements for subsidiary institutions”, after number (4)(i) at page 7 insert a new sentence: “In assessing an application for a capital waiver the ECB is minded to also take into account considerations related to the leverage ratio, given that pursuant to Article 6(5) of the CRR granting such waiver will also automatically waive the leverage requirement at the same level of the group structure. The ECB will take into account such considerations within the assessment of applications for waivers under Article 7 of the CRR, once a minimum level for the leverage ratio is introduced in Union law as a Pillar 1 requirement. However, the ECB will immediately take into account leverage-related considerations with regard to reporting and disclosure requirements, given that these requirements are already in force, pursuant to applicable legislation.3”.

In the subparagraph “Article 7(3) of the CRR, on the waiver of requirements for parent institutions”, after number (iii) at page 8 insert a new sentence: “In assessing an application for a capital waiver the ECB is minded to also take into account considerations related to the leverage ratio, given that pursuant to Article 6(5) of the CRR granting such waiver will also automatically waive the leverage requirement at the same level of the group structure. The ECB will take into account such considerations within the assessment of applications for waivers under Article 7 of the CRR, once a minimum level for the leverage ratio is introduced in Union law as a Pillar 1 requirement. However, the ECB will immediately take into account leverage-

3 It should be noted that, even where an Article 7 CRR waiver that also encompasses the leverage

requirements has been granted, credit institutions are still required to have in place policies and processes for the identification, management and monitoring of the risk of excessive leverage within the framework set out by the competent authority pursuant to Article 87 of CRD IV and national implementing legislative provisions.

Addendum to the ECB Guide on options and discretions available in Union law 3

related considerations with regard to reporting and disclosure requirements, given that these requirements are already in force, pursuant to applicable legislation.4”.

4. EXCLUSION OF INTRAGROUP EXPOSURES FROM THE CALCULATION OF THE LEVERAGE RATIO (Article 429(7) of the CRR as introduced by Commission Delegated Regulation (EU) 2015/62)

In the exercise of the discretion provided for in Article 429(7) of the CRR the ECB will assess applications from supervised entities taking into account the specific aspects highlighted below in order to ensure a prudent implementation of the relevant regulatory framework.

In particular, the assessment aims to ensure that the leverage ratio accurately measures leverage, controls the risk of excessive leverage and constitutes an adequate backstop to risk-weighted capital requirements (see Recitals 91 and 92 of the CRR as well as Article 4(1), subparagraphs (93) and (94), of the CRR, especially the definition of “risk of excessive leverage”), with due regard, however, to the smooth flow of capital and liquidity within the group at the domestic level. Moreover, where the exemption is granted, it is considered of fundamental importance that the “risk of excessive leverage”, as defined by the legislation, should not be concentrated within one subsidiary of the group under assessment.

To these ends, the ECB will verify at least the following factors.

(1) The potential impact on the credit institution of a change in economic and market conditions, especially with regard to its funding position.

In particular, the assessment should corroborate that the institution would not be imminently exposed to adverse market developments (when they occur), including an adverse change in funding conditions. Market shocks should be of such significance as to lead the credit institution to discharge other balance sheet items on the asset side, because available funding is employed to maintain the financing of intragroup exposures. In contrast, where the assessment suggests that there are sufficient grounds to assume that such a possibility could materialise and the intragroup exposure may give rise to leverage risk as defined in Article 4(1)(94) of the CRR as it may induce “unintended corrective measures” or “distressed selling of assets”, the waiver will not be granted. In fact, under such circumstances the exclusion of the intragroup exposures from the leverage ratio would imply that leverage risk is no longer fully reflected in the ratio, thus impairing the identification of this risk as required under the processes referred to in Article 87 of the CRD as well as the supervisory evaluation under Article 98(6) of the CRD.

4 It should be noted that, even where an Article 7 CRR waiver that also encompasses the leverage

requirements has been granted, credit institutions are still required to have in place policies and processes for the identification, management and monitoring of the risk of excessive leverage within the framework set out by the competent authority pursuant to Article 87 of CRD IV and national implementing legislative provisions.

Addendum to the ECB Guide on options and discretions available in Union law 4

The analysis should be based on the assessment by the Joint Supervisory Team (JST) of the liquidity and funding risks of the credit institution in the context of the Supervisory Review and Evaluation Process (SREP).

For such factors to be considered not to be relevant in individual cases, this assessment should conclude that the liquidity and funding position of the credit institution is strong and resilient to adverse changes in economic and market conditions, thus implying that the entity will not have to engage in “unintended corrective measures” or “distressed selling of assets” in order to preserve intragroup exposure(s).

(2) The materiality of the intragroup exposures of the applying entity, in terms of overall balance sheet size, off-balance-sheet obligations and contingent obligations to pay or deliver or provide collateral.

The ECB intends to carry out a forward-looking assessment to ascertain that the exemption of intragroup exposures does not have the effect that “leverage”, as defined in Article 4(1)(93) of the CRR, would no longer be adequately measured by the leverage ratio. A forward-looking assessment implies that the ECB also examines whether there are reasons (e.g. business model analysis, sector concentration, etc.) to assume that the bank’s balance sheet will expand and/or intragroup exposures will increase in the future, even where they appear relatively small when the application is submitted.

(3) The effect that the exclusion of the intragroup exposures would have on the leverage ratio’s function as an effective supplementary measure to risk-based capital requirements (backstop).

This assessment should also take into account that, if the conditions of Article 113(6) of the CRR are met and the waiver is granted (see below, Chapter 3.3), the institution will not hold any capital against the risks associated with intragroup exposures under the risk-based capital requirements.

(4) Whether the decision on the application concerning Article 429(7) of the CRR would have disproportionate negative effects on the recovery and resolution plan.

Once a minimum requirement for the leverage ratio is introduced in Union law, the ECB will assess whether any adjustments to the current policy stance are required.

10. VALUATION OF ASSETS AND OFF-BALANCE-SHEET ITEMS – USE OF IFRS FOR PRUDENTIAL PURPOSES (Article 24(2) of the CRR)

The ECB has determined not to exercise in a general manner the option set out in Article 24(2) of the CRR, which allows competent authorities to require credit institutions to effect, for prudential purposes, the valuation of assets and off-balance-sheet items and the determination of own funds in accordance with the International Accounting Standards, also in cases where the national applicable accounting

Addendum to the ECB Guide on options and discretions available in Union law 5

framework requires the use of n-GAAP (see also Article 24(1) of the CRR). Banks can therefore continue reporting to the supervisor according to their national accounting standards.

However, the ECB will assess applications to use International Accounting Standards for prudential reporting (also in cases of applicability of n-GAAP under the national accounting framework) pursuant to Article 24(2) of the CRR.

To that end, the ECB would expect that:

(1) the application should be submitted by the legal representatives of all the legal entities within any banking group that will actually apply the International Accounting Standards for prudential reporting as a consequence of the request being granted;

(2) for prudential purposes the same accounting framework will apply to all reporting entities within a banking group, in order to ensure consistency between subsidiaries established in the same Member State or also in different Member States. For the purposes of this exercise, a banking group is a group composed of all the significant supervised entities included in the group defined in the significance decision applicable to the requesting entities.

(3) a statement should be submitted by the external auditor, certifying that the International Financial Reporting Standards (IFRS) data reported by the institution as a consequence of the application being granted are in line with the applicable IFRS endorsed by the European Commission. This statement must be submitted to the ECB along with the reporting data which the auditor certifies at least once a year.

The use of IFRS for prudential reporting requirements will apply permanently to all relevant prudential reporting requirements after the credit institution has been notified of the ECB decision granting the application.

The ECB may consider the application of a transitional period, as appropriate and on a case-by-case basis, for the full implementation of the above-mentioned conditions.

Chapter 3 Capital requirements

3. CALCULATION OF RISK-WEIGHTED EXPOSURE AMOUNTS – INTRAGROUP EXPOSURES (Article 113(6) of the CRR)

The ECB is of the view that a request not to apply the requirements of Article 113(1) of the CRR may be approved, following a case-by-case assessment, for credit institutions that submit a specific application. As clearly established in Article 113(6)(a), the counterparty of the credit institution must be another credit institution or an investment firm, a financial institution or an ancillary services undertaking

Addendum to the ECB Guide on options and discretions available in Union law 6

subject to appropriate prudential requirements. Moreover, the counterparty must be established in the same Member State as the credit institution (Article 113(6)(d)).

For the purposes of this assessment, the ECB will consider the following factors.

(4) To assess compliance with the requirement, as laid down in Article 113(6)(b) of the CRR, that the counterparty is included in the same consolidation as the institution on a full basis, the ECB will take into account whether the group entities under assessment are included within the same consolidation on a full basis in a participating Member State, using the methods for prudential consolidation set out in Article 18 of the CRR.

(5) In order to assess compliance with the requirement laid down in Article 113(6)(c) of the CRR that the counterparty is subject to the same risk evaluation, measurement and control procedures as the institution, the ECB will take into account whether:

(i) the senior management of the entities in the scope of application of Article 113(6) of the CRR is responsible for risk management and risk measurement is regularly reviewed;

(ii) regular and transparent communication mechanisms are established within the organisation, so that the management body, senior management, business lines, the risk management function and other control functions can all share information about risk measurement, analysis and monitoring;

(iii) internal procedures and information systems are consistent and reliable throughout the consolidated group so that all sources of relevant risks can be identified, measured, and monitored on a consolidated basis and also, to the extent necessary, separately by entity, business line, and portfolio;

(iv) key risk information is regularly reported to the central risk management function of the parent undertaking to enable appropriate centralised evaluation, measurement and control of risk across the relevant group entities.

(6) To assess compliance with the requirement laid down in Article 113(6)(e) of the CRR that there is no current or foreseen material, practical or legal impediment to the prompt transfer of own funds or repayment of liabilities from the counterparty to the institution5, the ECB will take into account whether:

(i) the shareholding and legal structure of the group does not hamper the transferability of own funds or repayment of liabilities;

5 Beyond the limitations stemming from national company laws.

Addendum to the ECB Guide on options and discretions available in Union law 7

(ii) the formal decision-making process regarding the transfer of own funds between the institution and its counterparty ensures prompt transfers;

(iii) the by-laws of the institution and of the counterparty, any shareholders’ agreement, or any other known agreements do not contain any provisions that may obstruct the transfer of own funds or repayment of liabilities by the counterparty to the institution;

(iv) there have been no previous serious management difficulties or corporate governance issues that might have a negative impact on the prompt transfer of own funds or the repayment of liabilities;

(v) no third parties6 are able to exercise control over or prevent the prompt transfer of own funds or repayment of liabilities;

(vi) the COREP “Group Solvency” template (Annex I to Commission Implementing Regulation (EU) No 680/20147), which aims to provide a global view of how risks and own funds are distributed within the group, shows no discrepancy in this regard.

• Documentation related to approval decisions under Article 113(6)

For the purpose of the assessment(s) under Article 113(6) of the CRR, the credit institution presenting the application is expected to submit the following documents, unless they have already been provided to the ECB pursuant to other regulations, decisions or requirements:

(i) an up-to-date organisation chart of the entities of the consolidated group included within the scope of consolidation on a full basis in the same Member State, the prudential qualification of the individual entities (credit institution, investment firm, financial institution, ancillary services undertaking) and the identification of the entities that intend to apply Article 113(6) of the CRR;

(b) a description of the risk management policies and controls and how they are centrally defined and applied;

(c) the contractual basis – if any – for the group-wide risk management framework together with additional documentation such as the group company risk policies in the areas of credit risk, market risk, liquidity risk and operational risk;

(d) a description of the possibilities for the parent institution/undertaking to enforce group-wide risk management;

6 A third party is any party that is not the parent, the subsidiaries, the members of their decision-making

bodies or their shareholders. 7 Commission Implementing Regulation (EU) No 680/2014 of 16 April 2014 laying down implementing

technical standards with regard to supervisory reporting of institutions according to Regulation (EU) No 575/2013 of the European Parliament and of the Council (OJ L 191, 28.6.2014, p. 1).

Addendum to the ECB Guide on options and discretions available in Union law 8

(e) a description of the mechanism that ensures a prompt transfer of own funds and the repayment of liabilities in the event of financial distress by one of the group entities;

(f) a cover letter signed by the legal representative of the parent undertaking pursuant to applicable law, with approval from the management body, stating that the significant supervised credit institution complies with all conditions as set out in Article 113(6) of the CRR at the group level;

(g) a legal opinion, issued by an external independent third party or by an internal legal department and approved by the management body of the parent undertaking, demonstrating that beyond the limitations set out in company law there are no obstacles to fund transfer or repayment of liabilities resulting from either applicable legislative or regulatory acts (including fiscal legislation) or legally binding agreements;

(h) a statement signed by the legal representatives and approved by the management bodies of the parent undertaking and of the group entities that intend to apply Article 113(6) of the CRR declaring that there are no practical impediments to fund transfer or repayment of liabilities.

Chapter 5 Liquidity

4. ADDITIONAL COLLATERAL OUTFLOWS FROM DOWNGRADE TRIGGERS (Article 30(2) of Commission Delegated Regulation (EU) 2015/61)

The ECB will assess the materiality of outflows notified by credit institutions with regard to additional outflows and collateral needs for all contracts under which the contractual conditions will lead to outflows within 30 calendar days of a downgrade in the credit institution’s external credit assessment by 3 notches.

When credit institutions do not have an external credit assessment, it is expected that they will notify the impact on their outflows of a material deterioration of their credit quality corresponding to a 3-notch downgrade. The JST will assess how this impact is determined on a case-by-case basis, depending on the specificities of each contractual provision.

In general, and based on the information currently available from regulatory reporting to date, the ECB would be inclined to consider as material, among the amounts of outflows notified by credit institutions, those outflows which represent at least 1% of the gross outflows of a given institution (i.e. including those additional outflows triggered by the above-mentioned deterioration in credit quality).

Institutions are expected to notify these outflows directly via the regular reports submitted to the ECB in accordance with Article 415(1) of the CRR.

Addendum to the ECB Guide on options and discretions available in Union law 9

The ECB will reconsider the appropriateness of this threshold (1% of gross liquidity outflows) within one year of the final adoption of this Guide once an EU harmonised reporting framework in line with the Liquidity Coverage Requirement (LCR) Delegated Act (DA) is enacted.

14. CAP ON INFLOWS (Article 33(2) of Commission Delegated Regulation (EU) 2015/61)

The ECB is aware that under certain conditions the exercise of this specific option on liquidity requirements, when considered in combination with the option in Article 34 of Commission Delegated Regulation (EU) 2015/61 (see paragraph 5, above, in this Chapter), could, from the liquidity receiving entity’s perspective, produce a comparable effect to an Article 8 CRR waiver (i.e. where, in the case that the above-mentioned options are combined, the liquidity buffer requirement for the exempted institution is reduced to zero, or close to zero), while the two exemptions are subject to different specifications.

Consequently, in exercising the combination of those options and granting the related waivers, the ECB will make sure that this does not create any inconsistencies or conflicts with the policy defined in paragraph 5 of Chapter 1 of this Guide for granting an Article 8 waiver concerning the same entities within the same perimeter.

Details on the combination of the Article 33(2) exemption and the Article 34 waiver and their interaction with a waiver according to Article 8 of the CRR are provided below in the specifications for the assessment of the inflows under subparagraph (a).

In general, the ECB considers that the cap on inflows set out in Article 33(1) of Commission Delegated Regulation (EU) 2015/61 can be fully or partially waived following a specific assessment of the applications submitted by the supervised entities pursuant to Article 33(2) of the same Regulation. This assessment will be carried out according to the factors specified below for each type of exposure.

• Assessment for granting the exemption from the cap on inflows under Article 33(2)(a) of Commission Delegated Regulation (EU) 2015/61 (intragroup inflows)

(i) Inflows where the provider is a parent or subsidiary of the credit institution or another subsidiary of the same parent or linked to the credit institution by a relationship within the meaning of Article 12(1) of Directive 83/349/EEC.

Parent institution should be understood as a parent undertaking, as defined in Article 4(1)(15) of the CRR, and subsidiary should be understood as defined in Article 4(1)(16) of the CRR.

Both entities should also belong to the same scope of consolidation as defined in Article 18(1) of the CRR, unless they have a relationship within the meaning of Article 12(1) of Directive 83/349/EEC.

Addendum to the ECB Guide on options and discretions available in Union law 10

As a general principle, the ECB does not intend to grant such exemption to institutions that are not affected by the 75% cap on inflows as mentioned in Article 33(1) of Commission Delegated Regulation (EU) 2015/61. The ECB intends to exempt only those institutions which currently have inflows exceeding 75% of their gross outflows, or which reasonably expect to have inflows exceeding 75% of their gross outflows in the foreseeable future, also taking into consideration the potential volatility of the LCR.

(1) As already mentioned, the ECB will pay particular attention to cases where this option is exercised in combination with the option set out in Article 34 of Commission Delegated Regulation (EU) 2015/61, when a preferential treatment on intragroup credit and liquidity facilities has been granted.

Exercising these two options in combination could result in a null LCR for the liquidity-receiving entity. It could, therefore, under certain conditions, have an effect for the liquidity-receiving entity that is comparable to an Article 8 CRR waiver. In this regard, the ECB should ensure that granting applications for a combination of these two options or for the exemption under Article 33(2)(a) in isolation does not conflict with the approved policy for applications for a waiver, under Article 8 of the CRR, which would cover the same entities.

In cases where the conditions for an Article 8 waiver cannot be met for reasons that are not under the control of the institution or the group, or where the ECB is not satisfied that an Article 8 waiver may actually be granted, the ECB will consider instead the possibility of granting a combination of the preferential treatment under Article 34 of Commission Delegated Regulation (EU) 2015/61 and the exemption to the cap on inflows pursuant to Article 33(2)(a) of Commission Delegated Regulation (EU) 2015/61.

As already stated, a combination of the options under Article 33(2)(a) and Article 34 of Commission Delegated Regulation (EU) 2015/61 can only be granted where it does not conflict with the approved policy to be applied to a waiver under Article 8 of the CRR concerning the same entities.

(2) The ECB considers it appropriate, in cases where applications are submitted jointly pursuant to Article 34 of the LCR and Article 33(2)(a) of the LCR DA for the same inflows, that the assessment regarding inflows from undrawn credit and liquidity facilities is carried out according to the specifications under Article 34 of the LCR DA, in order to ensure consistency.

(3) Where the exemption under Article 33(2) of Commission Delegated Regulation (EU) 2015/61 is not requested in combination with a preferential treatment pursuant to Article 34 of the same Regulation (EU), the ECB will consider the potential impact of this exemption on the LCR of the institution and its liquidity buffer, and the type of intragroup inflows that would be exempted from the cap on inflows. In particular, the ECB recognises that, under certain conditions, granting this exemption in isolation could have a similar impact to a waiver granted in accordance with Article 8 of the CRR for the institution exempted from the cap on inflows.

Addendum to the ECB Guide on options and discretions available in Union law 11

The inflows in question should, therefore, meet minimum characteristics that would give sufficient comfort to the ECB that the applicant credit institution could rely on them for its liquidity needs in times of stress. To this end, the ECB considers that the inflows should present the following features.

(i) There are no contractual clauses that require any specific conditions to be met for the inflow to become available.

(ii) There are no provisions that would allow the intragroup counterparty providing the inflows to withdraw from its contractual obligations or impose additional conditions.

(iii) The terms of the contractual agreement giving rise to the inflows cannot be changed substantially without the prior approval of the ECB. An extension or a renewal of contracts under the same provisions as previous contracts does not per se require prior approval. Nonetheless, extensions or renewals of contracts must be notified to the ECB.

(iv) The inflows are subject to a symmetric or more conservative outflow rate when the intragroup counterparty calculates its own LCR. In particular, for intragroup deposits, if the deposit-receiving institution applies an inflow rate of 100%, the applicant entity should demonstrate that the intragroup counterparty does not treat this deposit as operational (as defined in Article 27 of Commission Delegated Regulation (EU) 2015/61).

(v) The applicant entity is able to demonstrate that the inflows are also properly captured in the contingency funding plan of the intragroup counterparty or, in the absence of such contingency funding plan, in the contingency funding plan for the applicant entity.

(vi) The applicant institution should also provide an alternative compliance plan to demonstrate how it intends to meet its fully phased-in LCR in 2018 should the exemption not be granted.

(vii) The applicant institution should be able to demonstrate that the intragroup counterparty has been fulfilling the LCR requirement for at least one year, alongside national liquidity requirements if applicable. Alternatively, where past LCR reports are not available or where no quantitative liquidity requirements are in place, a sound liquidity position could be considered to exist if the liquidity management of both institutions as evaluated in the SREP is deemed to be of high quality.

(viii) The applicant institution should monitor the liquidity position of the intragroup counterparty on a regular basis and demonstrate that it also enables the intragroup counterparty to monitor its own liquidity position on a regular basis. Alternatively, the applicant institution is expected to demonstrate how it has access to the appropriate information on the liquidity positions of the intragroup counterparty – for instance, by sharing daily liquidity monitoring reports.

Addendum to the ECB Guide on options and discretions available in Union law 12

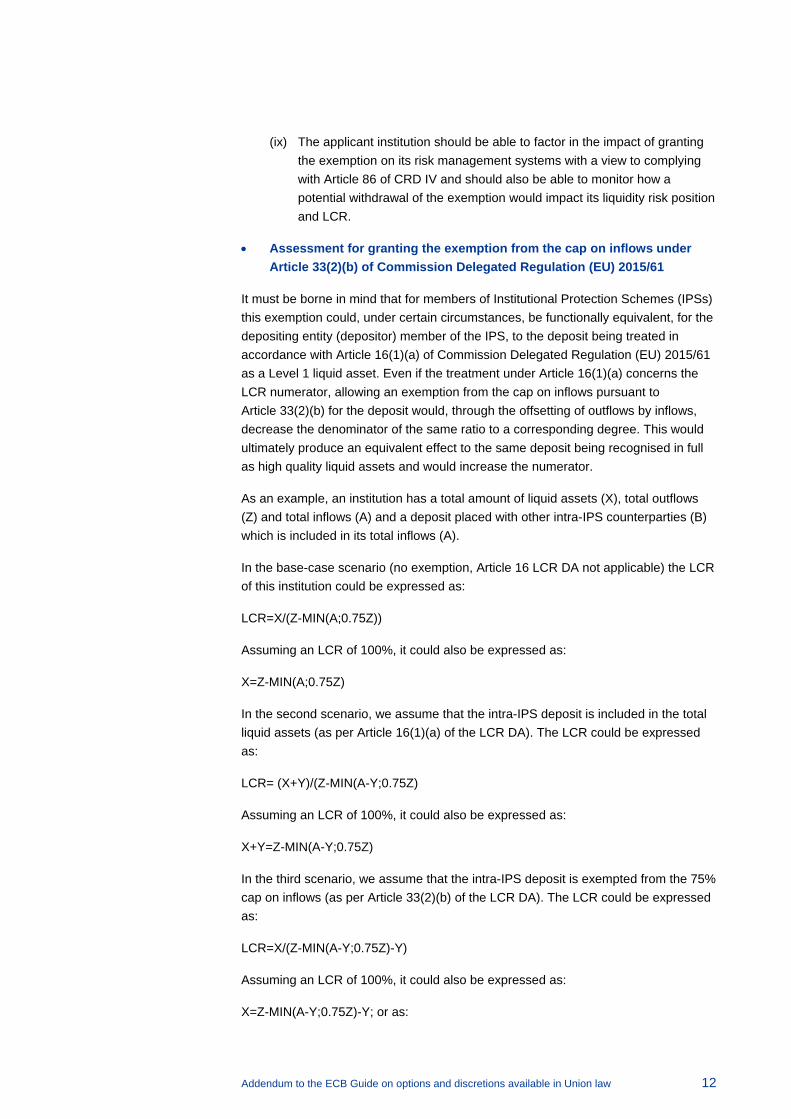

(ix) The applicant institution should be able to factor in the impact of granting the exemption on its risk management systems with a view to complying with Article 86 of CRD IV and should also be able to monitor how a potential withdrawal of the exemption would impact its liquidity risk position and LCR.

• Assessment for granting the exemption from the cap on inflows under Article 33(2)(b) of Commission Delegated Regulation (EU) 2015/61

It must be borne in mind that for members of Institutional Protection Schemes (IPSs) this exemption could, under certain circumstances, be functionally equivalent, for the depositing entity (depositor) member of the IPS, to the deposit being treated in accordance with Article 16(1)(a) of Commission Delegated Regulation (EU) 2015/61 as a Level 1 liquid asset. Even if the treatment under Article 16(1)(a) concerns the LCR numerator, allowing an exemption from the cap on inflows pursuant to Article 33(2)(b) for the deposit would, through the offsetting of outflows by inflows, decrease the denominator of the same ratio to a corresponding degree. This would ultimately produce an equivalent effect to the same deposit being recognised in full as high quality liquid assets and would increase the numerator.

As an example, an institution has a total amount of liquid assets (X), total outflows (Z) and total inflows (A) and a deposit placed with other intra-IPS counterparties (B) which is included in its total inflows (A).

In the base-case scenario (no exemption, Article 16 LCR DA not applicable) the LCR of this institution could be expressed as:

LCR=X/(Z-MIN(A;0.75Z))

Assuming an LCR of 100%, it could also be expressed as:

X=Z-MIN(A;0.75Z)

In the second scenario, we assume that the intra-IPS deposit is included in the total liquid assets (as per Article 16(1)(a) of the LCR DA). The LCR could be expressed as:

LCR= (X+Y)/(Z-MIN(A-Y;0.75Z)

Assuming an LCR of 100%, it could also be expressed as:

X+Y=Z-MIN(A-Y;0.75Z)

In the third scenario, we assume that the intra-IPS deposit is exempted from the 75% cap on inflows (as per Article 33(2)(b) of the LCR DA). The LCR could be expressed as:

LCR=X/(Z-MIN(A-Y;0.75Z)-Y)

Assuming an LCR of 100%, it could also be expressed as:

X=Z-MIN(A-Y;0.75Z)-Y; or as:

Addendum to the ECB Guide on options and discretions available in Union law 13

X+Y=Z-MIN(A-Y;0.75Z), which is equivalent to the second scenario.

Consequently, the ECB is of the opinion that the exemption from the cap on inflows should not be exercised for deposits from entities (members of IPSs) qualifying for the treatment set out in Article 113(7) of the CRR (see chapter … Par…. of this Guide) that are fully eligible for the treatment pursuant to Article 16(1)(a) of Commission Delegated Regulation (EU) 2015/61.

This being the case, credit institutions are invited (encouraged) to directly apply the treatment set out in Article 16(1)(a) of Commission Delegated Regulation (EU) 2015/61 for the determination of the LCR.

Other deposits that do not qualify for the treatment under Article 16(1)(a) could benefit from the exemption only in the following cases.

(1) Where, in accordance with national law or the legally binding provisions governing IPSs, the deposit-receiving entity is obliged to hold or invest the deposits in Level 1 liquid assets as defined in letters (a) to (d) of Article 10(1) of Commission Delegated Regulation (EU) 2015/61.

or

(2) Where the following conditions are met:

(i) There are no contractual clauses that require any specific conditions to be met for the inflow to become available.

(ii) There are no provisions that would allow the intra-IPS counterparty to not fulfil its contractual obligations or to impose additional conditions on the withdrawal of the deposit.

(iii) The terms of the contractual agreement governing the deposit cannot be changed substantially without the prior approval of the ECB.

(iv) The inflows are subject to a symmetric or more conservative outflow rate when the intra-IPS counterparty calculates its own LCR. In particular, if the deposit-receiving institution applies an inflow rate of 100%, the applicant entity should demonstrate that the intra-IPS counterparty does not treat this deposit as operational (as defined in Article 27 of Commission Delegated Regulation (EU) 2015/61).

(v) The inflows are also properly captured in the contingency funding plan of the intra-IPS counterparty.

(vi) The applicant institution also provides an alternative compliance plan to demonstrate how it intends to meet its fully phased-in LCR in 2018, should the exemption not be granted.

(vii) The applicant institution is able to demonstrate that the intra-IPS counterparty has been fulfilling the LCR requirement for at least one year, alongside national liquidity requirements if applicable. Alternatively, where

Addendum to the ECB Guide on options and discretions available in Union law 14

past LCR reports are not available or where no quantitative liquidity requirements are in place, a sound liquidity position could be considered to exist if the liquidity management of both institutions as evaluated in the SREP is deemed to be of high quality.

(viii) The IPS adequately monitors and reviews the liquidity risk and communicates the review to individual members in terms of its systems according to Article 113(7)(c) and (d) of Regulation (EU) No 575/2013.

(ix) The applicant institution is able to incorporate the impact of granting the exemption in its risk management systems and monitor how a potential withdrawal of the exemption would impact its liquidity risk position and its LCR.

Moreover, for the other category of deposits eligible for exemption from the cap, “groups of entities qualifying for the treatment set out in Article 113(6) of the CRR”, this legislative wording means that the conditions mentioned in Article 113(6) of the CRR must have been met and the corresponding exemption from risk-weighted capital requirements for intragroup exposures must actually have been granted. Therefore, entities that have been excluded from the scope of prudential consolidation in accordance with Article 19 of the CRR should also be excluded from the application of the exemption on the cap on inflows, given that Article 113(6) of the CRR exemption cannot be granted. Consequently, the exemption from the cap on inflows under Article 33(2)(b) of the LCR DA is not allowed either.

In this case, other intragroup deposits could benefit from the exemption only where, in accordance with national law or other legally binding provisions regulating groups of credit institutions, the deposit-receiving entity is obliged to hold or invest the deposits in Level 1 liquid assets as defined in letters (a) to (d) of Article 10(1) of Commission Delegated Regulation (EU) 2015/61.

• Assessment for granting the exemption from the cap on inflows under Article 33(2)(c) of Commission Delegated Regulation (EU) 2015/61

The ECB is of the opinion that inflows already benefiting from the preferential treatment mentioned in Article 26 of Commission Delegated Regulation (EU) 2015/61 should also be exempted from the cap referred to in Article 33(1) of Commission Delegated Regulation (EU) 2015/61.

In order to grant the exemption for the inflows referred to in the second subparagraph of Article 31(9) of Commission Delegated Regulation (EU) 2015/61, the ECB intends to assess such inflows against the definition of promotional loans in Article 31(9), and against the criteria of Article 26 of Commission Delegated Regulation (EU) 2015/61 and the specifications set out in paragraph 13 of this Chapter.

Addendum to the ECB Guide on options and discretions available in Union law 15

Chapter 9 Governance arrangements and prudential supervision

9.3 COMBINING THE FUNCTIONS OF CHAIRMAN AND CEO (Article 88(1)(e) of CRD IV)

The ECB considers that there should be a clear separation of the executive and non-executive functions in credit institutions and that the separation of the functions of Chairman and CEO should be the rule. Sound principles of corporate governance require that both functions be exercised in line with their responsibilities and accountability requirements. The responsibilities and accountability requirements of the chairman of the management body in its supervisory function (Chair) and of the chief executive officer (CEO) diverge, reflecting the different purposes of each supervisory function and management function respectively.

Moreover, the Corporate Governance principles for banks (Guidelines) of the Basel Committee on Banking Supervision (July 2015) recommend that in order “to promote checks and balances, the chair of the board should be an independent or non-executive board member. In jurisdictions where the chair is permitted to assume executive duties, the bank should have measures in place to mitigate any adverse impact on the bank’s checks and balances, e.g. by designating a lead board member, a senior independent board member or a similar position and having a larger number of non-executives on the board.” (paragraph 62).

The authorisation to combine the two functions should, therefore, be granted only in exceptional cases and only where corrective measures are in place to ensure that the responsibilities and accountability obligations of both functions are not compromised by their being combined. The ECB intends to assess applications for the combination of the two functions in line with the above-mentioned Basel principles and the European Banking Authority’s Guidelines on Internal Governance (GL 44), where it is recommended that in the case of combination of the two functions, “the institution should have measures in place to minimise the potential detriment on its checks and balances”.

More specifically, the ECB considers that such authorisation should be granted only for the period where the justifying circumstances continue to exist, as presented by the applying institution according to Article 88(1)(e) of CRD IV. After a period of 6 months from the adoption of the ECB decision authorising the combination of the two functions, the credit institution should assess whether the justifying circumstances do in fact continue to exist and inform the ECB accordingly. The ECB can withdraw the authorisation, where it determines that the outcome of the assessment regarding the continuing existence of the exceptional circumstances is not satisfactory.

In order to grant the authorisation, the ECB will assess the following factors:

(1) the specific reasons why the situation is exceptional; in this regard, the ECB would not consider the fact that the combination is allowed according to national law to be sufficient;

Addendum to the ECB Guide on options and discretions available in Union law 16

(2) the impact on the checks and balances of the credit institution’s framework of corporate governance and how such impact will be mitigated, taking into account:

(a) the scale, nature, complexity and variety of activities; the particularities of the governance framework with regard to applicable company law or specificities in the by-laws of the institution; and how these allow or prevent the separation of the management function from the supervisory function;

(b) the existence and scale of cross-border activities;

(c) the number, quality and nature of the shareholders: in general, a diversified shareholder base or the admission to listing on a regulated market may not support granting such authorisation, whereas the 100% control of the entity by a parent company which is fully compliant with the separation of functions between its chair and its CEO, and closely monitors its subsidiary, may support granting such authorisation.

It is clearly the responsibility of the credit institution to demonstrate to the ECB that it has put in place effective measures consistent with relevant national law in order to mitigate any adverse impacts on the checks and balances of the credit institution’s corporate governance framework.

The ECB is currently cooperating with the NCAs within the relevant network in order to further specify the above-mentioned factors for the supervisory assessment of applications pursuant to national legislation transposing Article 88 of CRD IV.

9.7 INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS FOR CREDIT INSTITUTIONS PERMANENTLY AFFILIATED TO A CENTRAL BODY (Article 108(1) of CRD IV)

The provision of Article 108(1) (2nd subparagraph) of CRD IV gives competent authorities the option to exempt credit institutions included in Article 10 of the CRR (affiliates and central body) from complying with the ICAAP requirements on a solo basis.

The ECB is inclined to grant such exemption in cases where a capital waiver pursuant to Article 10 of the CRR has already been granted for the credit institutions in question. For the specifications for granting a waiver pursuant to Article 10 of the CRR, please see p….. (chapter 1.7).