ADB Investor Presentation - May 2018 · $498 million Guarantees ... Support 6 ADB has raised ... $...

66

Asian Development Bank May 2018

Transcript of ADB Investor Presentation - May 2018 · $498 million Guarantees ... Support 6 ADB has raised ... $...

Asian Development BankMay 2018

▪ Asian Development Bank

▪ Funding Operations

▪ Green Bond Framework

▪ Appendices

2

An Asia and Pacific region free of poverty

ADB’s Mission

ADB’s Vision

To help our developing member countries

reduce poverty and improve quality of life

ADB’s Mode of OperationADB finances projects and programs in the territories of its developing

members.

Main instruments comprise loans, equity investments, guarantees, grants,

and technical assistance.

ADB also provides policy dialogues and advisory services and mobilizes

financial resources through its cofinancing operations.

3

• An international development finance

institution

• President Takehiko Nakao

• Headquartered in Manila, Philippines

• Founded in 1966

• Owned by 67 members:

48 regional, 19 non-regional

• 31 field offices1

• 3,134 staff from 60 countries1

1/ As of 31 December 2017.

Total

commitments in

2017:

$32.2 billion

Our Structure How We Helped in 2017

$18,717 millionLoans

$11,922 million

Cofinancing

including Trust Funds

$597 millionGrants

$498 millionGuarantees

$201 millionTechnical Assistance

$287 millionEquity Investments

4

The Region’s

Poverty Challenge

▪ It remains home to a large share of

the world’s poor

▪ 330 million people are still living on less than $1.90 a day

▪ Approximately 1.2 billion people are below the poverty line of

$3.10 a day

▪ 0.3 billion people live without safe drinking water

▪ 1.5 billion people lack access to proper sanitation

▪ $1.7 trillion per year in infrastructure investments is needed up

to 2030

5

Shareholdings1 Shareholdings1

Non-Borrowing Shareholders Ratings2 2017 Borrowing Shareholders Ratings

2 2017

Japan A1/A+ 15.6% People's Republic of China A1/A+ 6.4%

United States Aaa/AA+ 15.6% India Baa2/BBB- 6.3%

Australia Aaa/AAA 5.8% Indonesia Baa2/BBB- 5.4%

Canada Aaa/AAA 5.2% Malaysia A3/A- 2.7%

Republic of Korea Aa2/AA 5.0% Philippines Baa2/BBB 2.4%

Germany Aaa/AAA 4.3% Pakistan B3/B 2.2%

France Aa2/AA 2.3% Thailand Baa1/BBB+ 1.4%

United Kingdom Aa2/AA 2.0% Bangladesh Ba3/BB- 1.0%

Italy Baa2/BBB 1.8% Others 5.4%

New Zealand AAA/AA 1.5%

Others 7.4%

27 Countries 66.8% 40 Countries 33.2%

Totals may not add up because of rounding.

1/ Percent of Total Subscribed Capital as of 31 December.

2/ Moody’s and Standard & Poor’s ratings are as of 25 May 2018. (Source: Bloomberg)

Strong Shareholder

Support

6

▪ ADB has raised its capital

base five times since 1966

▪ Callable capital is available

for the protection of ADB’s

bondholders

▪ ADB has never made a call

on its callable capital

Growth in ADB’s capital base

-10.0

10.0

30.0

50.0

70.0

90.0

110.0

130.0

150.0

19711976

19831994

20082017

GCI-I1.0

GCI-II3.7

GCI-III11.5

GCI-IV30.2

Pre-GCI-V54.9

GCI-V151.2

$ bn

Callable Capital Paid-In Capital

$billion

Paid-in capital 7.6

Callable capital 143.6

Subscribed capital 151.2

ADB Capital Structure as of 31 December 2017

Solid Capital

Structure

7

TOTAL – $264.4 billion

Cumulative OCR regular and concessional

lending1, as of 31 December 2017

Legend:

$0 - $500 million $5,001 - $10,000 million

$501 - $2,000 million $10,001 - $15,000 million

$2,001 - $5,000 million $15,001 million - and above

Indonesia

$34,587 mn

Papua New Guinea

$2,649 mn

Fiji

$509 mn

Nauru

$5 mn

Federated States

of Micronesia

$84 mn

Marshall

Islands

$93 mn

Regional

$561 mn

Republic of Korea

$6,338 mn

People’s Republic

of China

$38,424 mn

Thailand

$6,683 mn

Malaysia

$1,998 mn

Lao PDR

$1,794 mnIndia

$42,031 mn

Sri Lanka

$8,818 mn

Pakistan

$30,826 mn

Nepal

$4,498 mnAfghanistan

$952 mn

Kazakhstan

$5,003 mn

Uzbekistan

$6,789 mn

Mongolia

$2,041 mn

Azerbaijan

$4,177 mn

Hong Kong, China

$102 mn

Singapore

$181 mn

Philippines

$17,962 mnViet Nam

$15,844 mn

Taipei,China

$100 mnBangladesh

$19,916 mn

Cambodia

$2,373 mn

Georgia

$2,323 mn

Republic of the

Maldives

$158 mn

Bhutan

$499 mn

Republic

of the

Union of

Myanmar

$2,099 mn

Cook Islands

$102 mn

Armenia

$1,336 mn

Palau

$70 mn

Turkmenistan

$125 mnKyrgyz Republic

$1,113 mn

Timor-Leste

$228 mn

Tajikistan

$498 mn

Approved Loans

by Borrower

Kiribati

$35 mnSamoa

$191 mn

Solomon Islands

$123 mn

Tonga

$69 mn

Tuvalu

$8 mn

Vanuatu

$96 mn

1/ Includes concessional loans that were transferred from ADF to OCR effective 1 January 2017. OCR sovereign regular ($189.8 bn), OCR sovereign concessional ($57.3 bn) and nonsovereign ($17.3 bn).

8

India

1/ Includes concessional loans that were transferred from ADF to OCR effective 1 January 2017.2/ OCR Committed Loans include Loans Outstanding at $101.3 billion (gross) and Undisbursed Effective Loans at $40.0 billion. Regular sovereign at $97.0 billion (69%), concessional sovereign at $36.7 billion (26%)and nonsovereign at $7.6 billion (5%).

$141.3 billion1,2 as of 31 December 2017

Committed Loans

By

Borrower

By

Sector

8.4%

Viet Nam

8.8%

Indonesia

9.0%

Bangladesh

10.6%

Pakistan

16.7%

People’s Republic of China

17.0%

24.8%

Others 21.1%

Energy

9.9%

Public Sector

Management

10.3%

Water Urban

Infrastructure

7.7%

Agriculture and

Natural Resources

8.6%Finance4.6%

Education

31.4%Transport

3.2%Others

3.2%

Multi-Sector

Philippines

4.7%

9

Uzbekistan

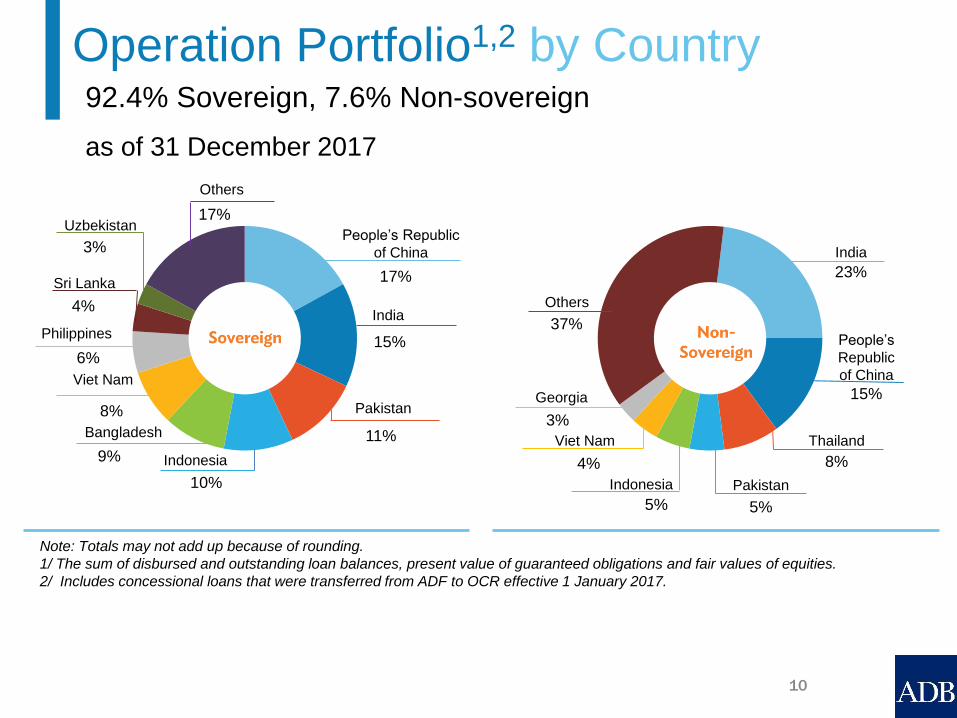

Note: Totals may not add up because of rounding.

1/ The sum of disbursed and outstanding loan balances, present value of guaranteed obligations and fair values of equities.

2/ Includes concessional loans that were transferred from ADF to OCR effective 1 January 2017.

92.4% Sovereign, 7.6% Non-sovereign

as of 31 December 2017

Operation Portfolio1,2 by Country

15%

India

11%

Pakistan

10%

Indonesia9%

Bangladesh

17%

Others

17%

People’s Republic

of China

37%

Others

5%

Indonesia

5%

Pakistan

23%

India

15%

People’s

Republic

of China

8%

Thailand

10

Viet Nam

8%

Philippines

6%

Sri Lanka

4%

3%

Viet Nam

4%

Georgia

3%

1/ Includes Loans Outstanding and Undisbursed Effective Loans as of 31 December 2017.

2/ Includes concessional loans that were transferred from ADF to OCR effective 1 January 2017.

ADB has strict policy with regard to non-accrual loans. If loan is overdue by:

• 60 days – no new loans

• 90 days – suspension of disbursements

• 6 months – non-accrual status

ADB lends primarily to the governments of member countries

who afford ADB preferred creditor status.

High Asset Quality

95%

Sovereign1,2

5%

Nonsovereign1 100%

Fully

Performing

Loans

0%

Loans innon-accrual

status

11

Net Loans 1

$101.0bn

Other 2

$44.9bn

Investments

$36.5bn

TOTAL = $182.4bn

Assets

Borrowings

$87.3bn

Other 2

$44.8bn

Equity

$50.3bn

TOTAL = $182.4bn

Liabilities and Equity

1/ Sovereign regular ($66.6 bn), sovereign concessional ($29.2 bn) and nonsovereign ($5.3 bn) less

allowance for loan losses ($0.1 bn).

2/ Mostly derivative assets and liabilities. Net derivative liability is $2.1 billion.

31 December 2017

Balance Sheet

Overview

12

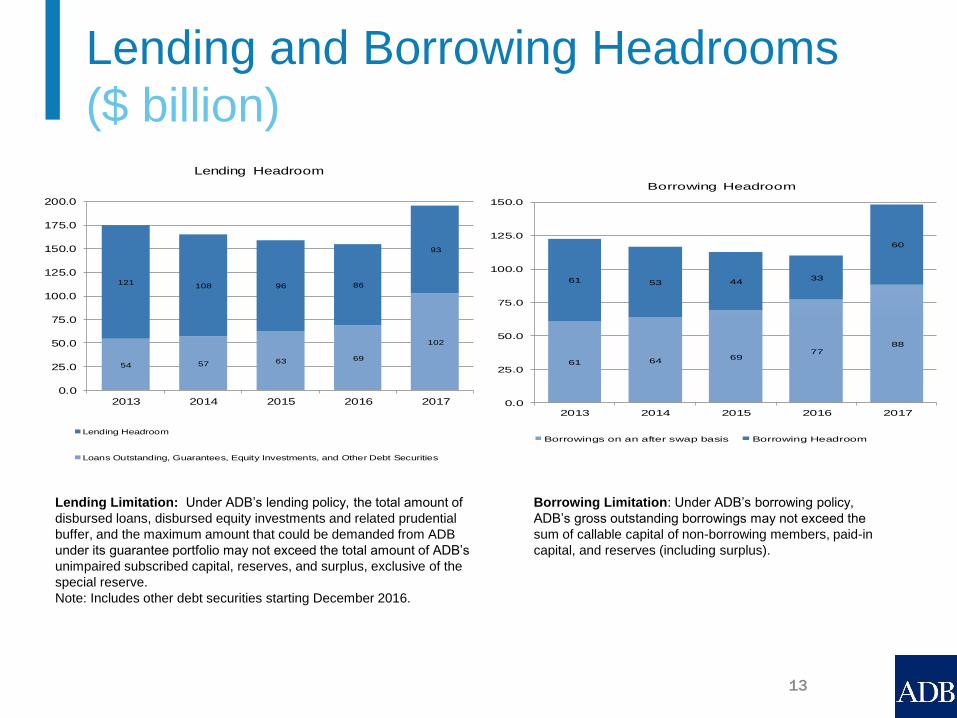

Lending and Borrowing Headrooms

($ billion)

54 57 63 69

102

121108 96 86

93

0.0

25.0

50.0

75.0

100.0

125.0

150.0

175.0

200.0

2013 2014 2015 2016 2017

Lending Headroom

Lending Headroom

Loans Outstanding, Guarantees, Equity Investments, and Other Debt Securities

Lending Limitation: Under ADB’s lending policy, the total amount of

disbursed loans, disbursed equity investments and related prudential

buffer, and the maximum amount that could be demanded from ADB

under its guarantee portfolio may not exceed the total amount of ADB’s

unimpaired subscribed capital, reserves, and surplus, exclusive of the

special reserve.

Note: Includes other debt securities starting December 2016.

61 6469

7788

61 53 44 33

60

0.0

25.0

50.0

75.0

100.0

125.0

150.0

2013 2014 2015 2016 2017

Borrowing Headroom

Borrowings on an after swap basis Borrowing Headroom

Borrowing Limitation: Under ADB’s borrowing policy,

ADB’s gross outstanding borrowings may not exceed the

sum of callable capital of non-borrowing members, paid-in

capital, and reserves (including surplus).

13

CONTENTS

▪ Asian Development Bank

▪ Funding Operations

▪ Green Bond Framework

▪ Appendices

14

“Our ratings on the Asian Development Bank (AsDB) reflect

our assessment of the bank's extremely strong business

profile and financial profile. A transfer of Asian Development

Fund (ADF) loans and certain other assets to AsDB's

Ordinary Capital Resources (OCR) took effect on Jan. 1,

2017. The move boosted AsDB's total lending capacity

substantially due to the addition of nonleveraged ADF equity

to the OCR.”– Standard and Poor’s, July 2017

“..credit profile reflects the bank's strong capital adequacy,

ample liquidity buffers and unfettered market access.

Additionally, the bank's preferred creditor status and strong

shareholder support enhance its financial performance. The

ADB’s credit strengths, which have remained intact through

recent periods of global and regional economic stress, reflect

in part its prudent financial management, including an

effective risk management framework.” – Moody’s, August

2017

“Capitalisation and concentration metrics in particular have

improved considerably, and have further enhanced the

AsDB’s solvency assessment.”

– FitchRatings, August 2017

AAA Rating based on

Strong Fundamentals▪ ADB is a leading AAA borrower in international and domestic capital markets, having issued bonds across various

markets in 35 currencies.

▪ Borrowings finance regular Ordinary Capital Resources (OCR) operations. Regular OCR loans are generally made

to developing members that have attained a higher level of economic development.

▪ ADB’s debt securities carry the highest possible investment ratings from major international credit rating agencies.

Capital Adequacy: Very HighLiquidity: Very HighStrength of Member Support: Very High

SACP: aaaRating: AAABusiness Profile: Extremely StrongFinancial Profile: Extremely Strong

Consolidation Credit PositiveExcellent CapitalisationMedium-Risk Business EnvironmentExcellent Liquidity

15

Source: S&P Global Ratings. Supranationals Special Edition October 2017.

Supranationals Ratings and Rating

Factors Summary SACP Rating* Outlook Business

ProfileFinancial Profile Financial Profile

with extraordinary shareholder support

AsianDevelopment Bank

aaa AAA Stable Extremely Strong

Extremely Strong

Extremely Strong

African Development Bank

aa+ AAA Stable Very Strong Very Strong Extremely Strong

Inter-AmericanDevelopment Bank

aa+ AAA Stable Very Strong Very Strong Extremely Strong

InternationalFinance Corporation

aaa AAA Stable Very Strong Extremely Strong

Extremely Strong

International Bank forReconstruction and Development

aaa AAA Stable Extremely Strong

Very Strong Extremely Strong

16

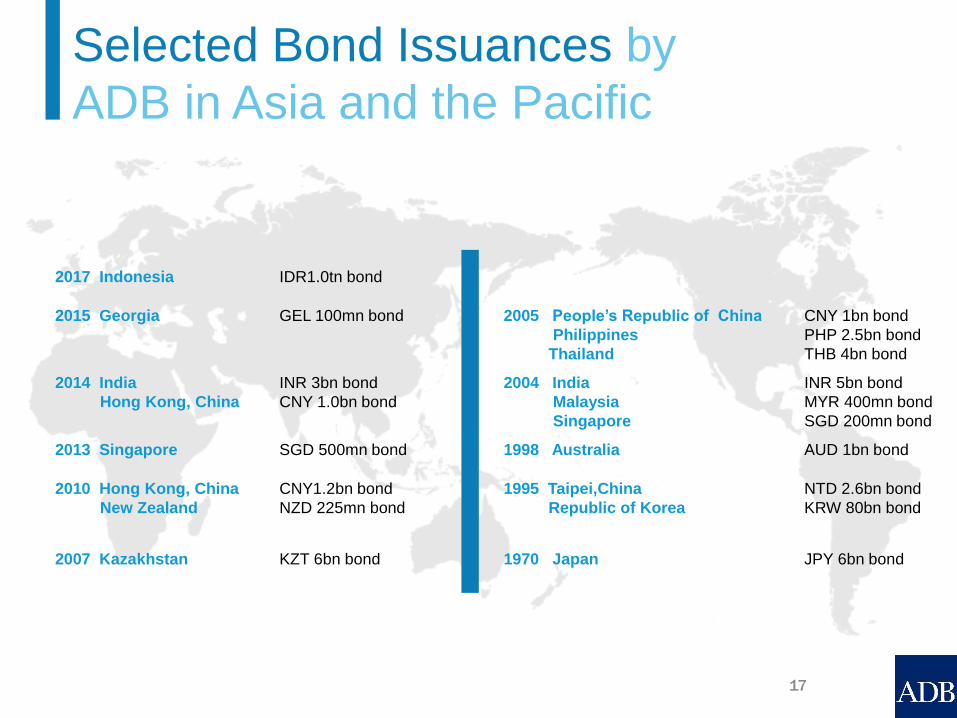

Selected Bond Issuances by

ADB in Asia and the Pacific

2017 Indonesia IDR1.0tn bond

2015 Georgia GEL 100mn bond 2005 People’s Republic of China

Philippines

Thailand

CNY 1bn bond

PHP 2.5bn bond

THB 4bn bond

2014 India

Hong Kong, China

INR 3bn bond

CNY 1.0bn bond

2004 India

Malaysia

Singapore

INR 5bn bond

MYR 400mn bond

SGD 200mn bond

2013 Singapore SGD 500mn bond 1998 Australia AUD 1bn bond

2010 Hong Kong, China

New Zealand

CNY1.2bn bond

NZD 225mn bond

1995 Taipei,China

Republic of Korea

NTD 2.6bn bond

KRW 80bn bond

2007 Kazakhstan KZT 6bn bond 1970 Japan JPY 6bn bond

17

OUTSTANDING BORROWINGS1 – $87.3 billion

1/ As of 31 December 2017

United States

Canada

Norway

United Kingdom Netherlands

Germany

LuxembourgSwitzerland

Italy

Belgium

AustriaKuwait

Saudi

Arabia

Brazil

People’s

Republic of

China

IndiaThailand

Malaysia

Singapore

Philippines

New Zealand

Australia

Japan

Hong Kong, China

Republic

of Korea Taipei,China

Kazakhstan

Mexico

South Africa

Turkey

Euro

Georgia

ADB Borrowings

across Currencies

Russian Federation

Sweden

18

Indonesia

1/ YTD 2018 figures include trades up to 25 May 2018.

2/ ECP dealers include Banc of America Securities Limited, Barclays, Citigroup Global Markets

Limited, Goldman Sachs, ING Bank N.V., and UBS.

Ensure availability of funds at all times to meet operational needs

Benchmark issuance Public bond issuesStructured private placements

and other reverse inquiriesRetail targeted transactions Local currency bond issuance ECP $8 billion Program2

Funding Availability

at all times Borrowings: 2006 – YTD 20181

0.0

5.0

10.0

15.0

20.0

25.0

30.020

06

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

1.6

3.1 2.9

0.3 0.0 0.6

5.7

2.5 2.4

4.1

8.37.5

2.3

5

9 910

1514

1312

14

19

21

29

13

Indicative, 24

ECP Medium-Long-term borrowings$ billion

19

Denominated in US Dollar and

Euro

In 2, 3, 5, 7, 10, and 20-year

maturities

Typically about $1 billion to $4.0

billion in size1

Issued at least once a year

Documentation

GMTN Programme

Clearing

Federal Reserve Book-Entry

System

Euroclear and Clearstream

GLOBAL

BENCHMARK BONDS

ADB bonds issued in Australia, Canada,

New Zealand, Singapore, Switzerland, and

UK are repo-eligible

ADB Euro bonds are ECB-eligible

Included in various indices:

➢ Barclays Capital Global Aggregate Index

➢ Citigroup WBIG

➢ JPM Euro Sterling Index

➢ Markit iBoxx USD Indices

➢ UBS Composite Bond Index – Australia

➢ UBS Supra-Sovereign Index

Documentation and Clearing

GMTN Programme - Euroclear and

Clearstream; DTC

AUD MTN Programme - Austraclear;

Euroclear and Clearstream

NZD MTN Programme - Austraclear NZ

System; NZ Clearing System

ACN Programme - CDP; HKMA; BNM;

PDEx (if applicable), TDCC; Euroclear and

Clearstream

MYR MTN Programme – Bank Negara

Malaysia

FUNDING

PLATFORMS

Tailor-fit to meet investor

requirements (currency, size, tenor,

structure)

Thematic bonds: Water, Clean

Energy, Green, Health and Gender

bonds

Uridashi notes

Retail-targeted bonds

Structured notes

Documentation

GMTN Programme

ACNP Programme

PRIVATE

PLACEMENTS

Financing

Instruments

1/ Green bonds are typically $500 million and above.

20

0

1

2

3

4

5

6

7

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017May-18

Ave. maturity in years

$bn

Global $/€ Benchmark Bonds

Public Bond Issues

Local Currency

Other private placements(institutional,Uridashi,retail-targeted)Structured privateplacements

Average maturity(based on first call date)

Borrowings by Type: 2006 – YTD 2018

Note: Excluding Euro-Commercial Paper issuances (ECPs). Year 2018 figures include trades up to 25 May 2018.

Diversified Product

and Currency Mix

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 YTD 2018

No. of Currencies 13 13 7 7 9 9 8 10 11 11 14 15 10

No. of Transactions 51 94 113 44 92 68 77 58 50 56 74 91 56

21

2.102.00

1.151.25 1.25

3.25

1.00

1.50

0.65

1.05

0.80

2.25

1.151.00

2.20

3.10

2.25

1.50

0.50

1.00

0.50

3.15

4.00

1.9

1.1

1.35

3.75

0.75

4.00

1.10

0.50

1.50

3.75

1.0

3.25

1.6

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

201

8

201

8

201

8

201

8

201

8

201

9

201

9

201

9

201

9

201

9

201

9

202

0

202

0

202

0

202

0

202

0

202

0

202

1

202

1

202

1

202

1

202

1

202

1

202

2

202

2

202

2

202

2

202

3

202

5

202

5

202

6

202

6

202

7

202

7

202

7

202

8

Year of Maturity

22

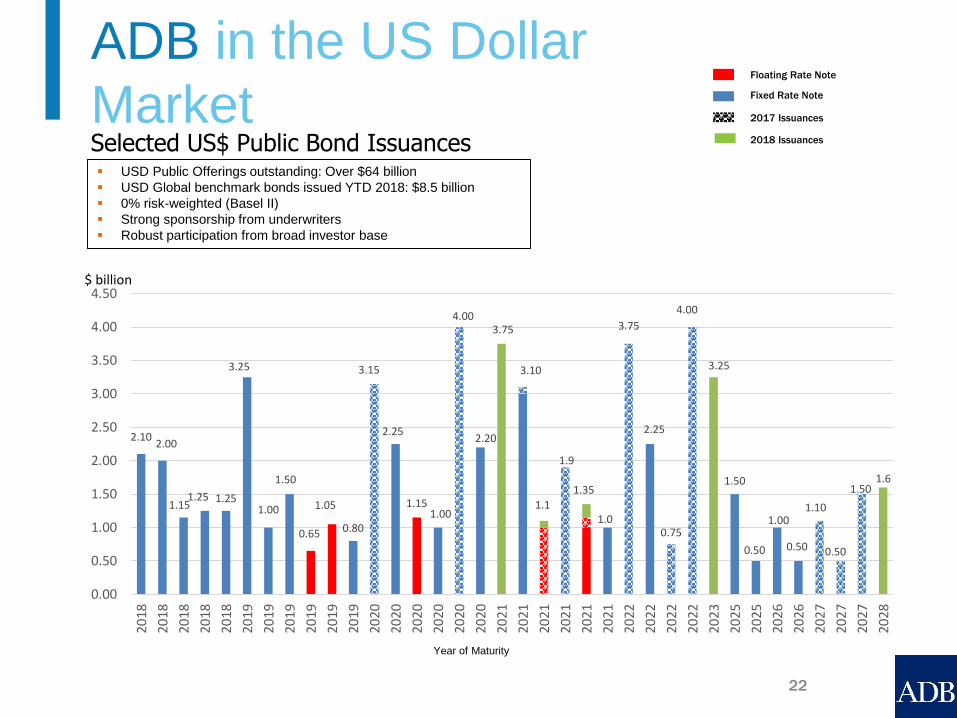

ADB in the US Dollar

MarketSelected US$ Public Bond Issuances

Floating Rate Note

Fixed Rate Note

2017 Issuances

$ billion

▪ USD Public Offerings outstanding: Over $64 billion

▪ USD Global benchmark bonds issued YTD 2018: $8.5 billion

▪ 0% risk-weighted (Basel II)

▪ Strong sponsorship from underwriters

▪ Robust participation from broad investor base

2018 Issuances

ADB in the US Dollar Market

Confidential 23

Note: Circle size represents issuance volume.

$4 bi llion $2 bi llion $1 bi llion

BY GEOGRAPHY (%) BY INVESTOR TYPE (%)

Notes: Distribution based on demand.

Includes fixed, floating rate note (FRN) and reopenings on Global format.

Investor Demand

for USD Global Bonds

40

27

29

32

33

33

23

37

29

29

27

28

12

9

8

9

4

7

19

21

19

20

27

21

6

6

15

10

9

11

2013

2014

2015

2016

2017

2018

Asia Europe Americas

ex-US

Middle East

and Africa

US Central Banks/

Official Institutions

Banks Fund Managers/

Insurance/Pension

Others

53

46

52

55

52

64

26

32

34

26

25

22

16

15

11

17

21

14

5

7

3

3

2

2013

2014

2015

2016

2017

2018

24

25

0.650

1.000

0.200

1.200

1.000

0.550

0.350

0.700

1.0501.000

0.600

0.800

0.185

0.400

0.800

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

2018 2019 2019 2020 2020 2021 2022 2022 2023 2023 2025 2026 2027 2028 2032

Year of Maturity

Floating Rate Note

Fixed Rate Note

2017 Issuances

2018 Issuances

A$ billion

▪ ADB has maintained a consistent presence in the Kangaroo market since 2006 with at least

one issuance per year. As of 25 May 2018, ADB has A$10.5 billion principal outstanding.

▪ Year to date, ADB has issued about A$1.2 billion in Kangaroo bonds.

ADB in the Kangaroo Market

Investors Demand

for Kangaroo Offerings

Note: Distribution based on demand.

BY GEOGRAPHY (%) BY INVESTOR TYPE (%)

39

41

38

30

20

11

57

40

45

59

62

71

2

18

12

6

11

10

1

5

5

7

8

22013

2014

2015

2016

2017

2018

Australia Asia Middle East

and Africa

Europe Americas Central Banks/

Official Institutions

Banks Fund Managers/

Insurance/Pension

Others

27

32

43

28

16

12

31

25

25

24

36

7

39

43

32

48

48

81

32013

2014

2015

2016

2017

2018

26

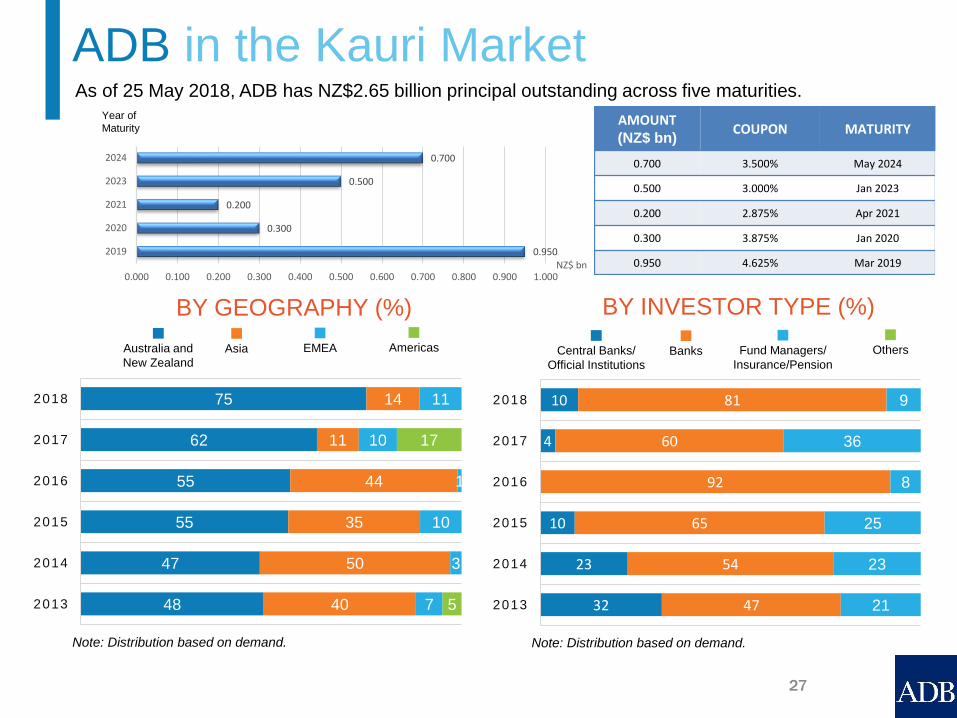

0.950

0.300

0.200

0.500

0.700

0.000 0.100 0.200 0.300 0.400 0.500 0.600 0.700 0.800 0.900 1.000

2019

2020

2021

2023

2024

NZ$ bn

Year of

Maturity

As of 25 May 2018, ADB has NZ$2.65 billion principal outstanding across five maturities.

ADB in the Kauri Market

Note: Distribution based on demand.

BY GEOGRAPHY (%) BY INVESTOR TYPE (%)

Note: Distribution based on demand.

Australia and

New Zealand

Asia EMEA Americas Central Banks/

Official Institutions

Banks Fund Managers/

Insurance/Pension

Others

48

47

55

55

62

75

40

50

35

44

11

14

7

3

10

1

10

11

5

17

2013

2014

2015

2016

2017

2018

32

23

10

4

10

47

54

65

92

60

81

21

23

25

8

36

9

2013

2014

2015

2016

2017

2018

AMOUNT(NZ$ bn)

COUPON MATURITY

0.700 3.500% May 2024

0.500 3.000% Jan 2023

0.200 2.875% Apr 2021

0.300 3.875% Jan 2020

0.950 4.625% Mar 2019

27

0.425

0.250

0.400

0.250

0.000 0.050 0.100 0.150 0.200 0.250 0.300 0.350 0.400 0.450

Dec 2018

Mar 2022

Dec 2022

Dec 2023

£ bn

Year of Maturity

BY GEOGRAPHY (%)

As of 25 May 2018, ADB has £1.325 billion principal outstanding across four

maturities.

ADB in the Sterling Market

BY INVESTOR TYPE (%)

AMOUNT(£ bn)

COUPON MATURITY

0.250 1.375% Dec 2023

0.400 1.000% Dec 2022

0.250 0.750% Mar 2022

0.425 1.000% Dec 2018

Asia UKMiddle East

and Africa

Europe

ex-UK

Americas Central Banks/

Official Institutions

Banks Fund Managers/

Insurance/Pension

Others

16 52

66

88

16

34

11

16

10

0% 20% 40% 60% 80% 100%

2016

2017

2018

31

33

15

60

1

74

9

65

11

1

0% 20% 40% 60% 80% 100%

2016

2017

2018

28

Note: Distribution based on demand.

AMOUNT(RMB bn)

COUPON MATURITY

1.200 2.85% Oct 2020

1.000 4.20% Dec 2019

1.700 3.20% Nov 20191.70

1.0

1.2

0.00 0.50 1.00 1.50 2.00

2019

2019

2020

Year of Maturity

Offshore

Onshore

RMB bn

▪ In 2005, ADB issued its inaugural RMB 1.0bn onshore RMB bonds (the "Panda Bonds")

in China. ADB is the first foreign issuer in the onshore RMB market.

▪ In 2010, ADB successfully launched its first offshore RMB bonds (the "Dimsum Bonds")

with a principal amount of RMB 1.2bn with a 10-year maturity, extending the yield

curve for the offshore RMB market.

▪ To date, ADB has RMB 3.9bn outstanding bonds, of which RMB 2.9bn are issued

offshore.

ADB in the Onshore/Offshore RMB Market

29

5.0

3.0

3.0

18.9

14.0

20.0

5.0

0.0 5.0 10.0 15.0 20.0

2014

2016

2020

Feb2021

Aug2021

2022

2026

Offshore Green BondOffshoreOnshore

AMOUNT COUPON MATURITY

INR20.0 bn 6.20% Oct 2026

INR14.0 bn 5.90% Dec 2022

INR18.9 bn1 6.45% Aug 2021

INR5.0 bn2 6.00% Feb 2021

INR3.0 bn 6.95% Jan 2020

INR3.0 bn 6.35% Aug 2016

INR5.0 bn 5.40% Feb 2014

▪ In 2004 ADB issued its inaugural Indian rupee bond issue: an INR 5.0bn “Maharaja” bond in the domestic market. ADB was the first foreign issuer in the onshore INR market.

▪ In 2014, ADB successfully launched its first offshore INR “Masala” bonds with a principal amount of INR 3.0bn and a 2-year maturity

▪ To date, ADB has issued INR 68.9bn bonds in the domestic and international markets

▪ ADB currently has INR 60.9bn in outstanding bonds all of which were issued offshore.

ADB in the Onshore & Offshore INR Markets

Year of Maturity

INR bn

1 ADB 6.45% bonds due Aug 2021 has been reopened three times since 20162 ADB 6.00% bonds due Feb 2021 is ADB’s first Green Bond issuance in Local currency

30

Responds to investor needs:

▪ Quick execution time

▪ Flexible issue size

▪ Broad maturity range

▪ Varied currency and interest

rate structure

Note: Includes structured notes, institutional and retail-targeted transactions. Year 2018 figures include trades up to 25 May 2018.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD2018

43 issues

84 issues 102 issues

35 issues

72 issues52 issues 60 issues

36 issues24 issues

24 issues 30 issues

48 issues

37 issues

$ bn

Dynamic Participation

in Private Placements

31

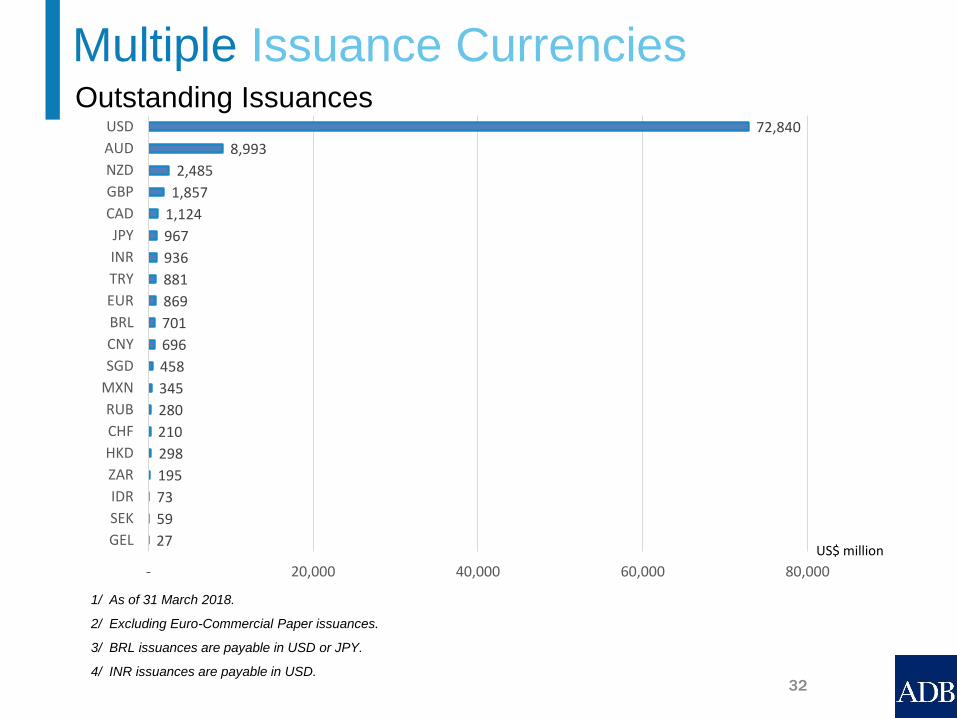

1/ As of 31 March 2018.

2/ Excluding Euro-Commercial Paper issuances.

3/ BRL issuances are payable in USD or JPY.

4/ INR issuances are payable in USD.

Outstanding Issuances

Multiple Issuance Currencies

32

27

59

73

195

298

210

280

345

458

696

701

869

881

936

967

1,124

1,857

2,485

8,993

72,840

- 20,000 40,000 60,000 80,000

GEL

SEK

IDR

ZAR

HKD

CHF

RUB

MXN

SGD

CNY

BRL

EUR

TRY

INR

JPY

CAD

GBP

NZD

AUD

USD

US$ million

ADB’s thematic bonds highlight its

efforts to support key initiatives such as

its water programs, clean energy

projects and health projects through its

AAA quality notes.

▪ ADB launched its first ever topical bonds (Uridashi) in 2010:

• Two-tranche Water Bonds (total amount of $638 million equivalent)

• Four-tranche Clean Energy Bonds (total amount of $233 million equivalent)

▪ ADB has raised an equivalent of about $192.8 million from its sale of water,

health, and gender bonds in 2017.

▪ ADB has issued approximately $2.5 billion equivalent in clean energy, water,

health, and gender bonds since 2010.

Foray into

Thematic Bonds

33

0.091

0.800

0.003

0.013

0.076

0.013

0.009

0.078

0.030

0.002

0.003

0.032

0.010

0.750

0.500 0.500

0.097

0.050

0.500

0.019

0.090

0.031

0.047

0.001

0.010

0.100

1.000

2019 2019 2019 2020 2020 2020 2020 2021 2021 2022 2022 2022 2022 2022 2025 2026 2027 2027 2027 2027 2027 2028 2028

US$bn equivalent

Year of Maturity

Water Bond issues

Green Bond PP

Gender Bond

Health Bond

Green Bond PO

ADB Outstanding

Thematic Bond Issuances • ADB has issued approximately $5.9 billion equivalent in thematic bonds since 20101.

34

1 As of 25 May 2018, the amount of outstanding topical bonds is approximately $3.7 billion equivalent.

Note: Based on notional amounts. Bonds with put and call options were considered maturing on the first put or call date. Includes ECPs.

Maturity Profile of Outstanding BorrowingsAs of 31 March 2018

Redemption Profile

35

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20182019

20202021

20222023

20242025

20262027

onwards

14.86

11.68

17.29

15.2414.66

4.86

0.942.54

2.52

9.69

US$ bn

CONTENTSCONTENTS

▪ Asian Development Bank

▪ Funding Operations

▪ Green Bond Framework

▪ Appendices

36

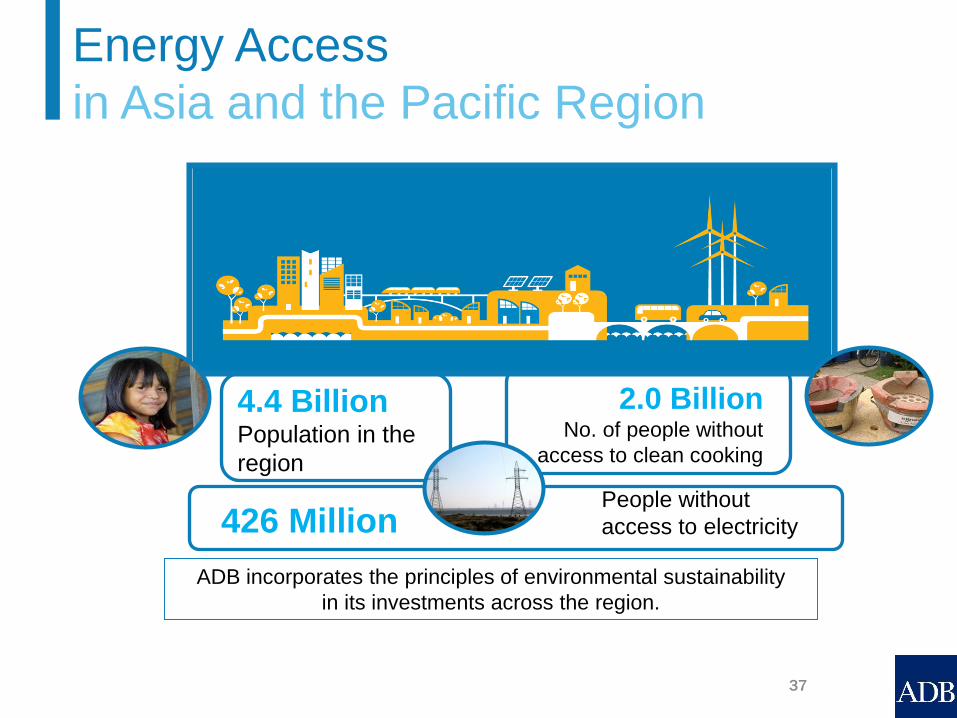

4.4 Billion Population in the

region

2.0 BillionNo. of people without

access to clean cooking

426 MillionPeople without

access to electricity

ADB incorporates the principles of environmental sustainability

in its investments across the region.

Energy Access

in Asia and the Pacific Region

37

▪ Asia’s overall national infrastructure needs

are estimated to be around $26 trillion over

2016-2030 or approximately $1.7 trillion per

year.*

▪ Of the total investment needs over 2016-

2030, $14.7 trillion will be for power and

$8.4 trillion for transport.

▪ ADB recognizes the importance of

sustainable investments in the region and

have been investing over $2 billion in clean

energy projects each year since 2011.

▪ ADB remains committed to scaling up

climate financing of $6 billion per year by

2020, of which $4 billion will target

mitigation and $2 billion adaptation.

* ADB 28 February 2017.

Background

38

1. Country Partnership

Strategy

ADB

Project

Cycle2. Preparation

3. Approval4. Implementation

5. Evaluation

Source: http://www.adb.org/projects/cycle

Overview:

ADB’s Project Cycle

39

1. Project eligibility: ADB’s Green Bond

Framework defines eligible projects to

support developing member countries

seeking to adapt to and mitigate the

consequences of climate change

2. Project Selection: The project selection

criteria will be implemented by sector

specialists in coordination with the treasury

department

3. Proceeds: Green bond proceeds will be

allocated to a subportfolio and tracked

against disbursement of eligible projects

4. Reporting: ADB will make available

eligible project list and green bond annual

newsletter online

1/ With second opinion.

Source: http://www.adb.org/sites/default/files/adb-green-bonds-framework.pdf

Green Bond

Framework1

40

Eligible Project Criteria▪ Eligible Projects: selected pool of projects funded, in whole or in part, by ADB that

promotes the transition to low-carbon and climate resilient growth as determined by ADB

Mitigation– Renewable Energy

• Solar

• Wind

• Geothermal

• Small Hydro ( 20MW and below)

– Energy Efficiency1

– Sustainable Transport (excluding roads)• Urban public transport

• Non-urban railway projects

• Non-motorized transport

Adaptation– Energy1

– Water and other Urban Infrastructure and Services

– Transport

1/ Excludes fossil fuels.

Source: ADB Green Bond Framework.

https://www.adb.org/sites/default/files/adb-green-bonds-framework.pdf

41

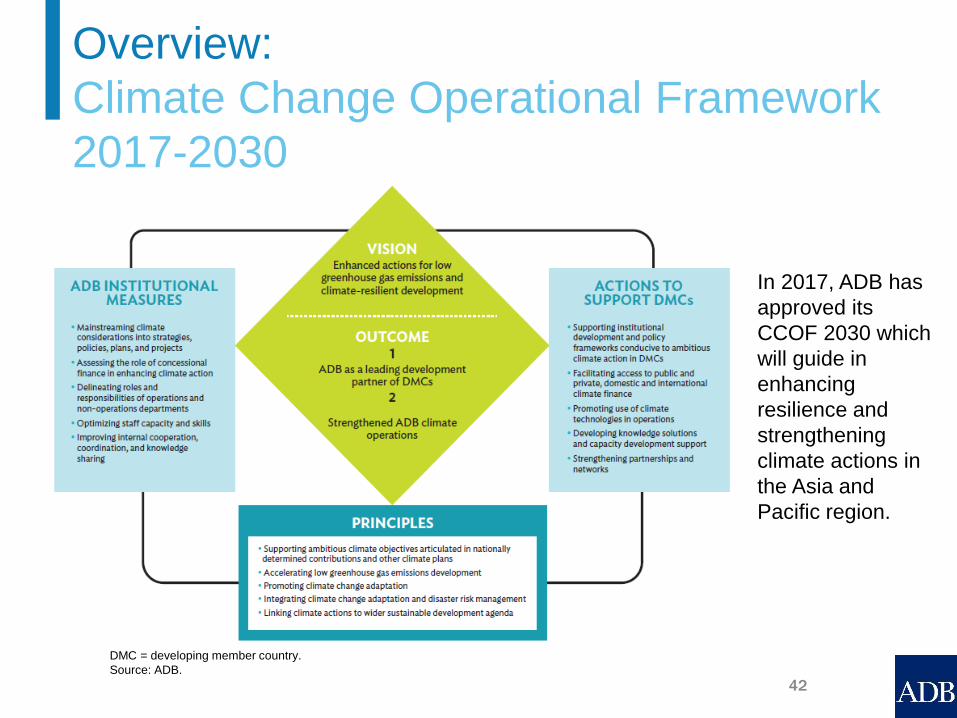

Overview:

Climate Change Operational Framework

2017-2030

DMC = developing member country.

Source: ADB.

In 2017, ADB has

approved its

CCOF 2030 which

will guide in

enhancing

resilience and

strengthening

climate actions in

the Asia and

Pacific region.

42

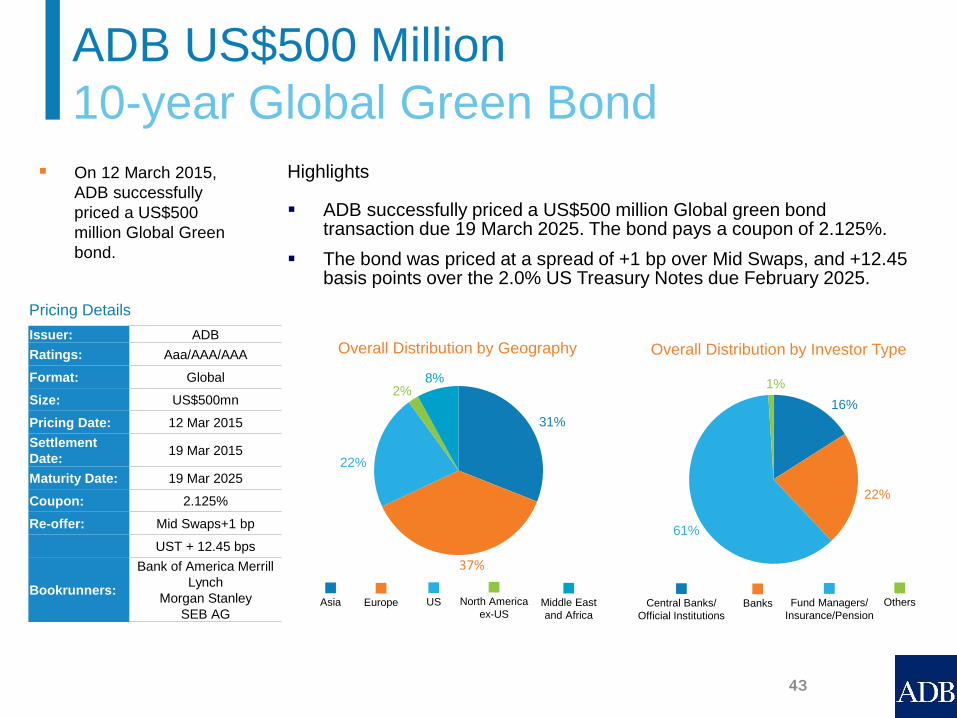

▪ On 12 March 2015,

ADB successfully

priced a US$500

million Global Green

bond.

Overall Distribution by Geography Overall Distribution by Investor TypeIssuer: ADB

Ratings: Aaa/AAA/AAA

Format: Global

Size: US$500mn

Pricing Date: 12 Mar 2015

Settlement

Date:19 Mar 2015

Maturity Date: 19 Mar 2025

Coupon: 2.125%

Re-offer: Mid Swaps+1 bp

UST + 12.45 bps

Bookrunners:

Bank of America Merrill

Lynch

Morgan Stanley

SEB AG

ADB US$500 Million

10-year Global Green Bond

Asia Europe Middle East

and Africa

US North America

ex-USCentral Banks/

Official Institutions

Banks Fund Managers/

Insurance/Pension

Others

31%

37%

22%

2%8%

16%

22%

61%

1%

Highlights

▪ ADB successfully priced a US$500 million Global green bond transaction due 19 March 2025. The bond pays a coupon of 2.125%.

▪ The bond was priced at a spread of +1 bp over Mid Swaps, and +12.45 basis points over the 2.0% US Treasury Notes due February 2025.

Pricing Details

43

58 5 37

▪ On 9 August 2016, ADB

successfully priced the

first ever dual tranche

Green Bond global

transaction by an SSA.

US$800 million 3-year

Distribution by Geography (%)US$800 million 3-year

Distribution by Investor Type (%)

ADB US$1.3 Billion Dual Tranche

Green Bond

Americas Asia Europe, Middle East

and AfricaCentral Banks/

Official Institutions BanksInsurance/

Pension/Others

Fund

Managers

Highlights

▪ ADB successfully priced the first ever dual tranche Green Bond global transaction from an SSA issuer consisting of US$800 million 3-year benchmark due August 2019 and US$500 million 10-year benchmark due August 2026.

▪ The 3-year was priced with a spread of +1bps over mid-swaps, equivalent to +22.75bps over the UST 0.75% due July 2019. The 10-year was priced with a spread of +33bps over Mid Swaps, equivalent to +21.9bps over the UST 1.625% due May 2026.

▪ It is ADB’s second Green Bond issue in benchmark format and its largest to date, which follows from ADB’s inaugural Global Green Bond issued in March 2015.

US$500 million 10-year

Distribution by Geography (%)

US$500 million 10-year

Distribution by Investor Type (%)

Pricing Details

Americas Asia Europe, Middle East

and Africa

Central Banks/

Official InstitutionsBanks

Fund Managers/

Insurance/Pension

Others

19 49 32

32 16 44 8

11 13 46 30

Issuer: ADB

Ratings: Aaa/AAA/AAA

Tranche: 3-year 10-year

Size: US$800

million

US$500

million

Pricing Date: 09-Aug-16 09-Aug-16

Settlement

Date:16-Aug-16 16-Aug-16

Maturity

Dates:16-Aug-19 14-Aug-26

Coupon: 1.00% 1.75%

Bookrunners:

Bank of America Merrill

Lynch

Credit Agricole CIB

J.P. Morgan

44

47 24 29

▪ On 1 August 2017, ADB

priced a dual tranche

Green Bond global

transaction.

US$750 million 5-year

Distribution by Geography (%)US$750 million 5-year

Distribution by Investor Type (%)

ADB US$1.25 Billion Dual Tranche

Green Bond

Americas Asia Europe, Middle East

and AfricaCentral Banks/

Official Institutions BanksInsurance/

Pension/Others

Fund

Managers

Highlights

▪ ADB successfully priced its third global Green Bond benchmark transaction consisting of US$750 million 5-year benchmark due August 2022 and US$500 million 10-year benchmark due August 2027.

▪ The 5-year was priced at 99.531% to yield 16.3 basis points over the 1.875% US Treasury notes due July 2022. The 10-year was priced at 99.172% to yield 20.5 basis points over the 2.375% US Treasury notes due May 2027.

▪ ADB’s third USD Green benchmark transaction reinforces commitment to a regular presence in the Green Bond market.

US$500 million 10-year

Distribution by Geography (%)

US$500 million 10-year

Distribution by Investor Type (%)

Pricing Details

Americas Asia Europe, Middle East

and Africa

Central Banks/

Official InstitutionsBanks

Fund Managers/

Insurance/Pension

Others

18 13 69

38 31 31

25 52 23

Issuer: ADB

Ratings: Aaa/AAA/AAA

Tranche: 5-year 10-year

Size: US$750

million

US$500

million

Pricing Date: 01-Aug-17 01-Aug-17

Settlement

Date:10-Aug-17 10-Aug-17

Maturity

Dates:10-Aug-22 10-Aug-27

Coupon: 1.875% 2.375%

Bookrunners:

Bank of America Merrill

Lynch

Credit Agricole CIB

J.P. Morgan

45

PROJECT CATEGORY: Renewable energy

TOTAL LOAN: $250 million

OUTPUTS:

▪ Approximately 350MW renewable power to

be commissioned

EXPECTED RESULTS:

▪ About 1.3 million tons of CO2 emissions

avoided per year (30 years project life)

Eligible Project: Sarulla Geothermal

Power Development, Indonesia

46

PROJECT CATEGORY: Renewable energy

TOTAL LOAN: $20 million

OUTPUTS:

▪ Installation and operation of 150 MW

utility-scale wind power plant

EXPECTED RESULTS:

▪ Approximately 370 GWh of wind power

delivered to the grid per year, on average,

starting 2015

▪ Over 160,000 tons CO2 equivalent avoided

per annum

Eligible Project: EDC Burgos Wind

Power Corporation, Philippines

47

▪ Asian Development Bank

▪ Funding Operations

▪ Green Bond Framework

▪ Appendices

48

Appendix 1:

ADB in the News

49

Trade & Forfaiting Review

ADB raises US$1.25bn from green bonds NEWS | 4 August 2017

Asian Development Bank (ADB) has raised US$1.25bn through the issue of a US$750m five-year green bond, and a US$500m 10-year dual tranche green bond.

Proceeds from the issues will be used to fund climate change mitigation and adaptation projects.

It follows a growing trend of development finance institutions raising funds by issuing green bonds, with German development bank Kreditanstalt für Wiederaufbau(US$2bn), Turkish development bank Turkiye Sinai Kalkinma Bankasi ( US$300m), and the IFC (US$100) all issuing similar bonds of their own.

“ADB is responding to the rapidly growing demand for green bonds with our second dual-tranche outing and our first 5-year green bond offering,” said ADB treasurer Pierre Van Peteghem.

“We have found the dual-pronged approach taken today to be an efficient means of reaching ethical investors active at different segments of the yield curve. This approach means that ADB is reaching an increasing number of investors who understand the importance of the green label.”

In 2015 ADB set its sights on doubling annual climate change financing from US$3bn to US$6bn by 2020, with US$4bn going to mitigation projects such as renewable energy, energy efficiency, sustainable transport, and for the construction of smart cities.

The five-year bond (US$750m) has a coupon rate of 1.875% per annum, payable semi-annually and a maturity date of 10 August 2022. The 10-year bond (US$500m) has a coupon rate of 2.375% per annum, payable semi-annually and a maturity date of 10 August 2027. Bank of America Merrill Lynch, Crédit Agricole, and JP Morgan were lead managers, while a syndicate group made up of Citi, HSBC, Morgan Stanley, and TD Securities was also formed.

ADB in the News

ADB aims for dollar benchmark in hotly demanded five year tenor

The Asian Development Bank hit screens on Tuesday announcing a dollar benchmark in a maturity that investors have been crying out for.

By: Lewis McLellan 05 Sep 2017

50

ADB adds A$350 million to its 2022 Kangaroo

Last Updated on Tuesday, 14 February 2017 16:10

Asian Development Bank (ADB) (AAA/Aaa/AAA) priced a tap to its January 2022 Kangaroo bond on 14 February. The transaction was upsized from A$200 million (US$153.3 million) minimum volume and priced in line with guidance of 40 basis points over semi-quarterly swap.

According to KangaNews data, the tap issue will be the first increase to ADB’s January 2022 Australian dollar line, after it was introduced for A$300 million at 42 basis points over swap on January 10.

ADB in the News

ADB joins $4bn club

The Asian Development Bank on Wednesday hit the $4bn mark for the first time with a dollar benchmark, taking advantage of a dearth of supply and offering a bit of juice to harvest a hefty amount of cash.By Craig McGlashan 26 Apr 2017

Leads BMO Capital Markets, Citi, Deutsche Bank, and RBC Capital Markets priced the $4 billion May 2020 global bond at minus 5bp after taking orders of over $5.4bn.

The deal moved through several pricing steps, first hitting screens on Tuesday with initial price thoughts of minus 4bp area.

“I was a bit surprised because I had the ADB’s January 2020 around minus 13bp and the IADB’s May 2020 [from April] at minus 8bp, so I thought it looked a bit generous in terms of new issue premium,” said a head of SSA DCM away from the trade.

“But in the end I understand ADB wanted size, so it was the right strategy.”

After taking indications of interest of over $2.9bn, books opened officially on

Wednesday morning around 8am with guidance unchanged. Just under two hours later, with orders over $3.7bn, the leads revised guidance to 5bp area before pricing in line with that. The final book was over $5.4bn.

It is the second time this year that ADB has broken its size record for a dollar benchmark, with a $3.75bn five year in February its previous biggest.

“This shows ADB has no problem doing larger deals to face its substantially larger funding programme this year,” said a head of SSA syndicate away from the deal. “It picked a good window, with none of the big guys looking and the capacity for new dollar supply quite high after a lack of deals over the last few weeks.”

51

Appendix 2:

Highlights of

Loan Operations

52

PROJECT SUMMARY:

Meeting the need for reliable and affordable electricity is a challenge for

Bangladesh as the country seeks to consolidate its transition to middle-

income country status by 2021. Apart from addressing infrastructure

constraints and improving the country’s transmission and distribution

networks, the project will also support productive energy usage in rural

areas, enhanced safety for customers, improvements in rural distribution

management, and interventions to support women employees in the

power sector.

The project includes the construction of a 174 kilometer (km) high-

voltage, 400 kV transmission link between southern Bangladesh and

Dhaka, design and installation of control and automation systems to

improve the distribution network in areas serviced by the Dhaka

Electricity Supply Company, rehabilitation and expansion of over 50,000

km of rural distribution network across the country, and support on

project design, investment planning, and regulatory compliance in the

power sector agencies.

The project will contribute to the Government of Bangladesh’s goal of

giving people 100% access to power by 2021, with about 875,000

households benefiting from the distribution investments by 2020. The

total cost of the project is $1.059 billion, with the government contributing

$441 million in counterpart funding.

Power System Enhancement and Efficiency

Improvement Project

Development

impact:

Access to efficient and reliable

electricity supply in Bangladesh

improved

Sector: Energy - Electricity transmission and

distribution- Energy efficiency and

conservation

Drivers of

Change:

Governance and capacity

development

Partnerships

Project Term: 2017 – 2020

ADB

Financing:

$600 million

Bangladesh:

Enhanced Power Systems

53

PROJECT SUMMARY:

The Secondary Road Improvement Project — which will improve a 50

kilometer stretch of road from Dzirula to Chumateleti via Kharagauli

and other short access roads to local communities — will increase the

mobility of and accessibility for local residents and tourists visiting the

area, and increasing economic activity in the region. The road will

provide a vital alternative to the Khevi-Ubisa highway to facilitate

international and national traffic during highway construction.

The secondary road, which serves 30,000 people residing in the area,

will be rehabilitated to improve transport connectivity and road safety.

The road will be upgraded and bridges will be rehabilitated, improving

access to markets and public services for the communities in this

region. Access roads to the nearby Borjomi-Kharagauli National Park

and railway stations along the road will also be improved.

Secondary Road Improvement Project

Development

impact:

Improved road connectivity across

Georgia and broadened access to

economic opportunities

Sector: Transport - Road transport (non-

urban)

Drivers of

Change:

Governance and capacity

development

Knowledge solutions

Partnerships

Private sector development

Project Term: 2017 – 2022

ADB Financing: $80 million

Georgia:

Increased Economic Activity

54

PROJECT SUMMARY:

India, with its massive population and continuously growing power-

hungry economy, has been experiencing power deficits. The lack of a

reliable electricity supply is constraining the country’s growth potential

and making electricity access difficult for 311 million people.

Government efforts to address this increasing energy demand include

the development of solar parks.

The project will improve the capacity and efficiency of interstate

transmission networks, particularly in transmitting the electricity

generated from the new solar parks to the national grid. Apart from

the evacuation of 2,500 megawatts (MW) of power from solar parks

in Bhadla, Rajasthan, and 700 MW from Banaskantha, Gujarat,

POWERGRID is also including two additional subprojects that will

increase solar power generation by 4.2 gigawatt and lessen carbon

emissions by over 7 million tons every year.

The Solar Transmission Sector Project is also the first project to be

implemented following the usage of agency-level country safeguards

and procurement systems for POWERGRID to speed up processes

while providing autonomy and ownership of the project.

Solar Transmission Sector Project

Development

impact:

Increased energy capacity and

supply through renewable

sources

Sector: Energy - Electricity transmission

and distribution

Drivers of

Change:

Governance

Capacity development

Knowledge solutions

Partnerships

Private sector development

Project Term: 2017 – 2022

ADB

Financing:

$175 million

India:

Expanded Supply of Clean Power

55

PROJECT SUMMARY:

The project will facilitate direct and efficient operation of both freight

and passenger train services linking major cities in the Fergana

Valley — home to nearly a third of Uzbekistan’s population — with

Tashkent, the country’s capital. The project will help improve

transport connectivity and encourage growth and job creation in the

Fergana Valley. It will also increase regional trade along CAREC’s

Corridor 2 as well as improve environmental and safety performance

of the railway. An expected 10,000 tons of CO2 will be saved every

year as a result of the project.

The total project cost is estimated at $177.45 million, with

O’zbekiston Temir Yo’llari (UTY) — the public railway company —

and the government contributing $97.45 million. ADB’s investment

will finance supervision consultants, procurement of plant,

procurement of maintenance equipment and machinery, and

procurement of materials for external power supply.

The project is in contribution to the ongoing efforts of UTY and the

government in upgrading Uzbekistan’s Soviet-era railway network. It

builds on the successes of other projects, including one which

recently completed the electrification of a 140 km railway track

between the historical cities of Samarkand and Karshi in the south of

the country.

Central Asia Regional Economic Cooperation

Corridor 2 (Pap-Namangan-Andijan) Railway

Electrification Project

Development

impact:

Level of passenger and freight

service railway line improved

Sector: Transport - Rail transport (non-

urban)

Drivers of

Change:

Knowledge solutions

Project Term: 2017 – 2021

ADB

Financing:

$80 million

Uzbekistan:

Upgraded Railway Infrastructure

56

Appendices 3-9

57

Lending Limitation: Under the policy, the total amount of disbursed loans, disbursed equity investments,

and the related prudential buffer, and the maximum amount that could be demanded from ADB under its

guarantee portfolio may not exceed the total of ADB’s unimpaired subscribed capital, reserves, and surplus,

exclusive of the special reserve.

Borrowing limitation: ADB’s borrowing policy limits ADB’s gross outstanding borrowings to no more than

the sum of callable capital of non-borrowing members, paid-in capital, and reserves (including surplus).

Risk Bearing Capacity: ADB assesses its capital adequacy using a stress test methodology that entails,

among other things, estimated non-accrual shocks and their impact on ADB's capital and income over the

next 5 years. The framework provides ADB with the ability to assess its capital adequacy based on

changes in risk exposure, as well as on its characteristics as an MDB, including callable capital, preferred

creditor status, and developmental mandate.

Conservative Investment Guidelines: The maximum allowable average duration of all investments

outstanding is 4 years, while the target policy duration for the USD core portfolio is 3 years, with +/- one

year allowable deviation. ADB’s investment guidelines permit only high quality instruments such as

government and government-agency debt and highly-rated corporate securities. As a second line of

defense, the Office of Risk Management monitors the investment portfolio on a daily basis and ensures

compliance with prescribed limits.

For further details, please see go to

http://www.adb.org/site/investors/credit-fundamentals/financial-and-risk-management-policies

Appendix 3:

Conservative Financial Policies

58

▪ Approved on 20 July 2009, the new Safeguard Policy Statement reaffirms and strengthens ADB’s

commitment to ensuring that borrowers/clients meet ADB safeguard requirements to avoid, minimize,

mitigate and/or compensate adverse impacts of ADB operations on the environment and project-

affected people.

▪ The policy commits ADB to assessing country safeguard systems, assisting borrowers/clients to

strengthen both their approaches and country capacity to manage environmental and social risks,

and to increasing ADB oversight during implementation.

▪ As a central part of ADB's mission to promote environmentally sustainable and inclusive economic

growth, the new Safeguard Policy Statement consolidates and builds upon current ADB policies on

Environment, Indigenous Peoples and Involuntary Resettlement that are already applied to all bank-

supported projects in developing member countries (DMCs).

▪ The policy ensures that ADB’s safeguards are harmonized with other multilateral development banks

and remain relevant to the evolving needs of DMCs and private sector clients.

▪ The policy contains new provisions on biodiversity conservation, community health and safety, and

physical cultural resources. Key features include emphasis on capacity development of borrowers

and more attention to safeguard implementation and supervision.

▪ The Safeguard Policy Statement became effective on 20 January 2010.

For further details, please see http://www.adb.org/site/safeguards/main

Appendix 4:

Safeguard Policy Statement

59

▪ Developing good governance and fighting corruption are core ADB strategic objectives and are crucial to effective, transparent and

accountable aid, to which ADB committed by endorsing the Paris Declaration on Aid Effectiveness.

▪ ADB’s Office of Anticorruption and Integrity (OAI), an independent body since October 2009, is the initial point of contact for allegations of

integrity violations involving ADB-related activities or ADB staff. Its mission is to ensure ADB and its partners maintain the highest ethical

and professional standards, and prevent resources intended to improve the lives of the poor from being used to line the pockets of the

unscrupulous.

▪ Any party found to have committed fraudulent, corrupt, coercive, collusive, obstructive practices, or other integrity violations identified by

ADB risks being sanctioned with debarment. Debarred entities are ineligible to participate in ADB-financed, administered or supported

activities. A debarred firm’s ineligibility extends to all employees and officers of a firm, and may extend to other principals and contractual

employees of the firm. Debarred individuals may not participate in ADB-related activity, as individuals or through nomination by an eligible

firm, unless they have completely disassociated themselves with an ineligible firm.

▪ Following the Harmonized Framework adopted by MDBs in 2006, the Agreement on Cross-Debarment was signed by ADB, the World Bank

Group, the African Development Bank (AfDB), the Inter-American Development Bank (IADB) and the European Bank for Reconstruction and

Development (EBRD) in Luxembourg on 9 April 2010. An important global milestone in the fight against corruption, this Agreement allows

that an entity debarred by one of the participating MDBs be subsequently cross-debarred by the other participating MDBs, and constitutes an

important step in strengthening global anticorruption efforts.

▪ The base sanction for integrity violations is 3-year debarment. The Integrity Oversight Committee (IOC) may impose a greater or lesser

debarment period depending on the circumstances of each case. The IOC will be guided by the following ranges: 1) First debarments

(including cases where a party has previously been given a reprimand) – 1 year to indefinite for individuals and 1 to 7 years for firms, 2)

Second debarments – up to indefinite for individuals and up to 10 years for firms, 3) Subsequent debarments – up to indefinite for individuals

and up to 20 years for firms.

▪ In accordance with ADB’s Anticorruption Policy, ADB’s zero tolerance to corruption is linked to broader support for governance and

improvement in the quality and capacities of developing member countries (DMCs), with fraud and corruption detection training given to

government agencies in several of these DMCs.

▪ ADB also organizes knowledge support activities to improve integrity awareness and skills. Since 2010 it is mandatory for all ADB staff to be

briefed on the importance of fighting corruption and adherence to ADB’s Anticorruption Policy.

For further details, please see http://www.adb.org/site/integrity/main

Appendix 5:

Anticorruption and Integrity Policies

60

▪ The Investment Climate Facilitation Fund (ICFF) was established by the Government of Japan (GOJ) and the Asian

Development Bank (ADB) in 2008 as a trust fund under the Regional Cooperation and Integration Financing Partnership

Facility (RCIFPF) of ADB.

▪ The objective of ICFF is to promote investments in ADB’s developing member countries (DMCs) and facilitate regional

cooperation and integration (RCI) through the construction of basic infrastructure, improvements in the investment climate,

capacity building, and promotion of good governance, among others.

▪ Activities to be supported by ICFF are projects that:

a. require collective efforts and actions of two or more countries to jointly respond to cross-border issues;

b. are national in nature, but with significant regional dimensions and/or implications;

c. facilitate regional policy dialogue, including the establishment of regional policies for greater RCI;

d. support research and promote knowledge generation and dissemination among DMCs in the area of RCI;

e. strengthen institutional capacity of regional and/or subregional groupings; or

f. support regional partnership building with international institutions.

▪ All ADB DMCs are eligible for support from ICFF. Funding priority will be given to projects that promote financial sector

development and regional investment. Likewise, projects which will promote the visibility of ICFF as well as those which

will be implemented in cooperation with Japanese aid agencies will be prioritized.

▪ ADB has been appointed by GOJ as the administrator of ICFF.

▪ Project implementation, supervision, and monitoring are conducted by the concerned departments and offices following

ADB’s standard policies, procedures, and guidelines, including consulting services and procurement, social and

environmental safeguards, financial management and reporting, and anticorruption and governance, as amended from

time to time.

▪ Total funds committed amounted to approximately $31.5 million as of 31 December 2017.

Appendix 6:

Investment Climate Facilitation Fund

61

ADB’s Strategic Priorities for 2014 – 2020:

A. Sharpening ADB’s Operational Focus 1. Poverty reduction and inclusive economic growth

2. Environment and climate change

3. Regional cooperation and integration

4. Infrastructure development

B. Responding to the New Business

Environment

5. Middle-income countries

6. Private sector development and operations

7. Knowledge solutions

C. Strengthening ADB’s Capacity and

Effectiveness

8. Financial resources and partnerships

9. Delivering value for money in ADB

10. Organizing to meet new challenges

Appendix 7:

Midterm Review of Strategy 2020

62

REGIONAL MEMBERS RatingYear of

MembershipRating

Year of

Membership

Afghanistan NR/NR 1966 Micronesia, Fed. States of NR/NR 1990

Armenia B1/NR 2005 Mongolia B3/B- 1991

Australia Aaa/AAA 1966 Myanmar NR/NR 1973

Azerbaijan Ba2/BB+ 1999 Nauru NR/NR 1991

Bangladesh Ba3/BB- 1973 Nepal NR/NR 1966

Bhutan NR/NR 1982 New Zealand Aaa/AA 1966

Brunei Darussalam NR/NR 2006 Pakistan B3/B 1966

Cambodia B2/NR 1966 Palau NR/NR 2003

People's Republic of China A1/A+ 1986 Papua New Guinea B2/B 1971

Cook Islands NR/B+ 1976 Philippines Baa2/BBB 1966

Fiji Ba3/B+ 1970 Samoa NR/NR 1966

Georgia Ba2/BB- 2007 Singapore Aaa/AAA 1966

Hong Kong, China Aa2/AA+ 1969 Solomon Islands NR/NR 1973

India Baa2/BBB- 1966 Sri Lanka B1/B+ 1966

Indonesia Baa2/BBB- 1966 Taipei,China Aa3/AA- 1966

Japan A1/A+ 1966 Tajikistan NR/NR 1998

Kazakhstan Baa3/BBB- 1994 Thailand Baa1/BBB+ 1966

Kiribati NR/NR 1974 Timor-Leste NR/NR 2002

Republic of Korea Aa2/AA 1966 Tonga NR/NR 1972

Kyrgyz Republic NR/NR 1994 Turkmenistan WR/NR 2000

Lao People's Democratic Rep. NR/NR 1966 Tuvalu NR/NR 1993

Malaysia A3/A- 1966 Uzbekistan NR/NR 1995

Republic of the Maldives NR/NR 1978 Vanuatu NR/NR 1981

Marshall Islands NR/NR 1990 Viet Nam B1/BB- 1966

NON-REGIONAL

MEMBERSRating

Year of

Membership

Austria Aa1/AA+ 1966

Belgium Aa3/AA 1966

Canada Aaa/AAA 1966

Denmark Aaa/AAA 1966

Finland Aa1/AA+ 1966

France Aa2/AA 1970

Germany Aaa/AAA 1966

Ireland A2/A+ 2006

Italy Baa2/BBB 1966

Luxembourg Aaa/AAA 2003

The Netherlands Aaa/AAA 1966

Norway Aaa/AAA 1966

Portugal Ba1/BBB- 2002

Spain Baa1/A- 1986

Sweden Aaa/AAA 1966

Switzerland Aaa/AAA 1967

Turkey Ba2/BB- 1991

United Kingdom Aa2/AA 1966

United States Aaa/AA+ 1966

Note: Moody’s and Standard & Poor’s ratings are as of 25 May 2018.

(Source: Bloomberg)

Appendix 8:

ADB’s Shareholders – 31 December 2017

63

ADB website www.adb.org

Investor relations website www.adb.org/investors

Strategy 2020 www.adb.org/about/policies-and-strategies

Country Operations www.adb.org/countries

Annual Reports www.adb.org/documents/series/adb-annual-reports

Funds and Resources www.adb.org/funds

Sectors and Themes www.adb.org/focus-areas

Data and Research www.adb.org/data

Asian Bonds Monitor asianbondsonline.adb.org

News and Events www.adb.org/news

Bloomberg ADB <GO>

Appendix 9:

Sources of Additional Information

64

This presentation is for informational purposes only and does not constitute an offer to sell or solicitation

of an offer to buy any ADB securities in any jurisdiction to any person to whom it is unlawful to make such

an offer or solicitation.

- The term “country”, as used in the context of ADB, refers to a member of ADB and does not

imply any view on the part of ADB as to the member’s sovereignty or independent status.

- In this publication, $ refer to US dollars.

Disclaimer

Every effort has been made to ensure the accuracy

of the data used in this publication. Variations in

data in the Asian Development Bank (ADB)

publications often result from different publication

dates, although differences may also come from

source and interpretation of data. ADB accepts no

responsibility from any consequence of their use.

65

Asian Development Bank

Treasury Department

Funding Division

6 ADB Avenue, Mandaluyong City

1550 Metro Manila, Philippines

Email [email protected]

Investor Website www.adb.org/investors

Bloomberg ADB <GO>

Tel. No. +632 683-1204

Fax No. +632 632-4120

All images are from the ADB Photo Library.

Asian Development Bank

Fighting Poverty in Asia and the Pacific

66