Capturing emerging market equity exposure with index investing

1

Hans Janssen Daalen

General Director DUFAS

Stockholm, May 16, 2011

Active investing

and

Index investing

2

‘The vast majority of fund investors suffer from

punitive fee structures, overtrading, fund

proliferation and closet indexing.

The net result is poor performance.’

Terry Smith, Fundsmith

3

Ladies and gentlemen, this is your wake-up call! A clear message from an active manager, Terry Smith. And many will

agree with him. It is very true to say that the competition from alternative investment products is moving on. The

competition is not only coming from alternative investment products. In the fund arena itself, index funds and ETF’s are

becoming a greater threat for active managers that produce UCITS. With the AIFM directive coming into force within

a couple of years, also alternative managers will profit from a more harmonized European playground. Like in sports, it

is more difficult to maintain your top position, rather than getting there. The success of UCITS has made traditional

fund managers lazy. Many fund managers lost the ability to listen to the needs of their clients. Instead of that, they kept

on creating new products, new funds, simply because they could. Long time ago, fund investing was meant to be a

cheap and simple solution for people, who did not have the means nor the expertise to get investment advice.

Therefore, fund managers created easy accessible investment solutions by offering truly risk spreaded, because

worldwide investing, funds in equity, fixed income and real estate. People only needed to bother of their asset

allocation. Nowadays, we have created in Europe a very diversified fund marketplace, comprised of over 50,000 funds,

offering concentrated investments in almost any tiny market or asset class. Fund investors, more and more, became in

need of qualified investment advisors, and fund managers started to include the costs of investment advice in their

management fees too. The result is what we see in this quote from Terry Smith. No wonder competitors move ahead in

our market place, acquiring greater market share day by day. Institutional investors started to find their way to index

investing many years ago. But nowadays, even regulators make public pleads for better and cheaper investment

solutions, one of which is index investing, the topic I want to address to you today. In my home country, The

Netherlands, the regulator started to challenge the fund industry back in 2009, at the aftermath of the credit crisis.

Index funds were mentioned as a cheap, default solution for the public. So called active managers where not able to

beat their benchmark index anyway, so why pay more for poor performance? DUFAS accepted the challenge from the

regulator and conducted a research about the merits from index investing opposite to active investment styles. As one

of the results of this research paper, I am standing here today in front of you. Let us find out if our regulators are right.

4

The case for index investing according to proponents

Costs of index investing are lower

Risk of index investing is lower

Index investing is simpler & easier to understand

Scientific research demonstrates that active investing

cannot beat the benchmark / index

5

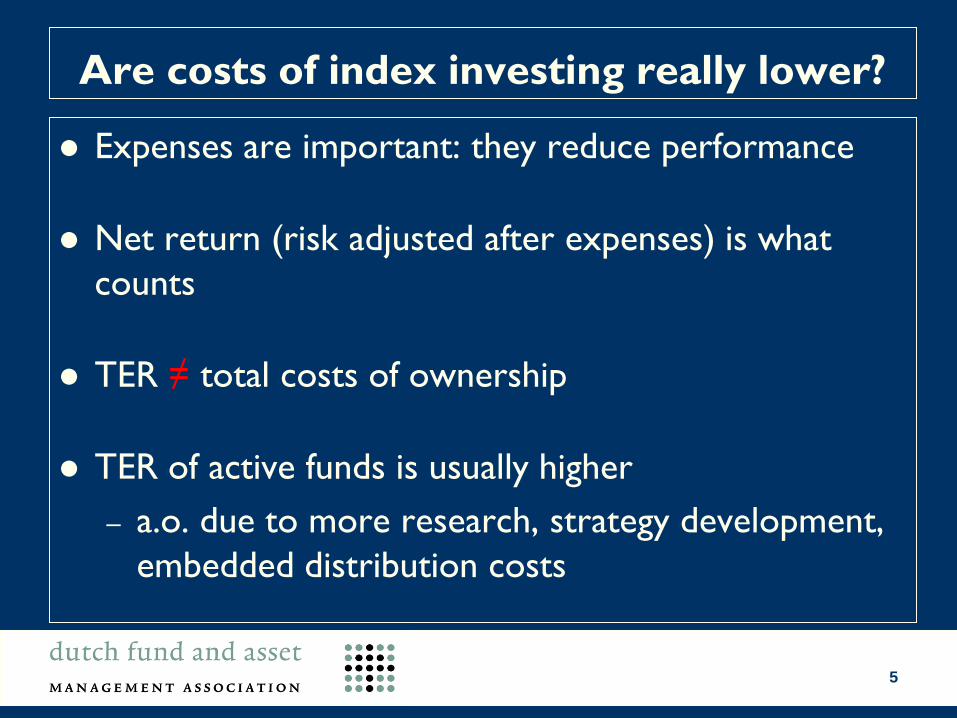

Are costs of index investing really lower?

Expenses are important: they reduce performance

Net return (risk adjusted after expenses) is what

counts

TER ≠ total costs of ownership

TER of active funds is usually higher

– a.o. due to more research, strategy development,

embedded distribution costs

6

Are costs of index investing really lower?

TER ≠ total-costs-of-ownership

Reasons for underperformance opposite to the

relevant index. TER does not include:

– transaction costs of the financial instruments

which the fund buys and sells: broker commissions

– dividend withholding tax

– cost of investment advice

– subscription & redemption fees for units of the

fund itself

7

Are costs of index investing really lower?

TER of index funds is much lower than the actual costs!

Transaction costs can get as high as 33% of total cost

of ownership of index funds (some equity funds)

Transaction costs are f.i. much lower in active fund

with buy-and-hold strategy

Dividend withholding tax reduces real return of

index tracker, compared with TER

Cost of advice is embedded in management fee of

active funds, but normally not in fee of index funds

8

Are costs of index investing really lower?

If you look at TER only: index funds are cheaper

If you look at ‘total-costs-of-ownership’: index funds

cost approximately the same as active funds!

9

Is index investing really less riskier?

Tracking error (volatility compared to market) really

is smaller, but

Tracking error excludes market risk

Market risk is a major risk for both active funds &

index funds

Lower correlation with benchmark = higher risk free

return

Market weighted indices (the standard) invest in

winners of the past (f.i. Greece’s government debt weight

in Euroland Bond Index)

10

Is index investing really less riskier?

Tracking error also does not include:

Securities lending risks

Index arbitrage or index front running

Certain types of index funds have higher than normal

liquidity and tradability risks

– small ETF -- large investor may cause huge NAV impact

– bond index trackers are just as (il)liquid as active bond

funds because of underlying illiquid bond market

Leveraged index trackers magnify both profits &

losses

11

Is index investing really less riskier?

Saying index investing is less riskier than active

investing is misleading the public!

12

Is index investing easier to understand?

YES: the index tells you which investments are made

but

Index funds are not always a replication of the index

There are many index funds for many different markets

Commercial parties create alternative indices: hybrid

active/passive, not based upon market caps

Investment advice required to select appropiate

index funds, just as in case of active managed funds

13

Is index investing easier to understand?

Index funds are not always a full replication of the index:

Representative sampling strategy = 5-20% of fund portfolio

is in derivatives and non-index investments

Agressive sampling = very small percentage of portfolio is

index investment

Synthetic indexing = stock index futures + bonds replicate

the performance of the index

Enhanced indexing = aimed at outperformance

14

Can active investing not beat the benchmark?

Keynes: stock exchange casino full of gamblers

Fama: Efficient Market Hypothesis led to index funds

Fund performance literature: statistical analysis of the

whole market and a very large selection of active

funds to prove EMH

Outcome is consistently positive but

– Confirmation bias: falsification of EMH is easier

– Outperforming strategies are proprietary and not

surrendered to scientists

– Averages of nearly the whole market are meaningless

15

Can active investing not beat the benchmark?

Efficient Market Hypothesis states that:

an active investor can beat the market but, on

average, extra returns will be lower than, or equal to,

the extra costs of beating the market (incl. wages,

information costs and transaction costs)

But: empirical research shows EMH cannot explain all

phenomena in financial markets...

16

Can active investing not beat the benchmark?

Empirical research shows EMH cannot explain:

Irrational exuberance, bubbles, crashes

January effect, July effect, November effect, weekend

effect or Monday effect

End-of-the-month effect; holiday effect (=returns are

higher the day before the holiday starts)

Small-cap effect (= small companies generate relatively large returns)

Index effect (=when a stock is included in an index, its value

immediately goes up significantly, and vice versa)

17

Can active investing not beat the benchmark?

Empirical research shows EMH cannot explain:

Price momentum

Earnings surprise

Mean reversion

Home bias (investors tend to invest close to home)

Herding (=investors follow trends rather than anticipate them)

Irrational but familiar human behaviour as explained

by behavioural finance: overconfidence, overreaction,

representativeness bias, information bias, loss aversion, anchoring, framing,

hyperbolic discounting, the disposition effect and several other predictable human

mistakes in reasoning and information processing and biases.

18

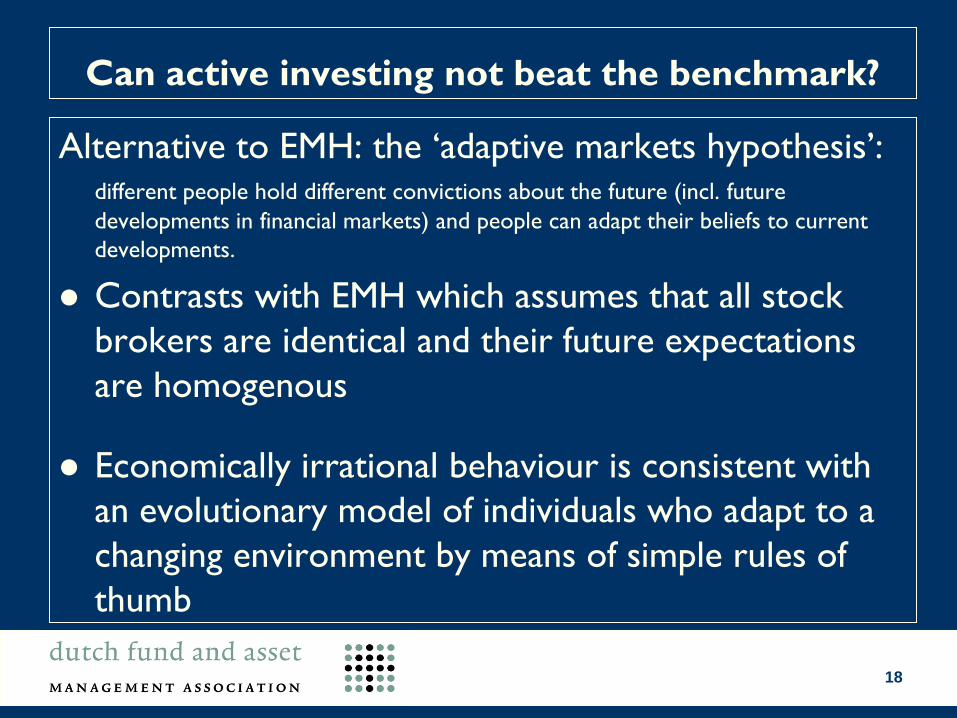

Can active investing not beat the benchmark?

Alternative to EMH: the ‘adaptive markets hypothesis’: different people hold different convictions about the future (incl. future

developments in financial markets) and people can adapt their beliefs to current

developments.

Contrasts with EMH which assumes that all stock

brokers are identical and their future expectations

are homogenous

Economically irrational behaviour is consistent with

an evolutionary model of individuals who adapt to a

changing environment by means of simple rules of

thumb

19

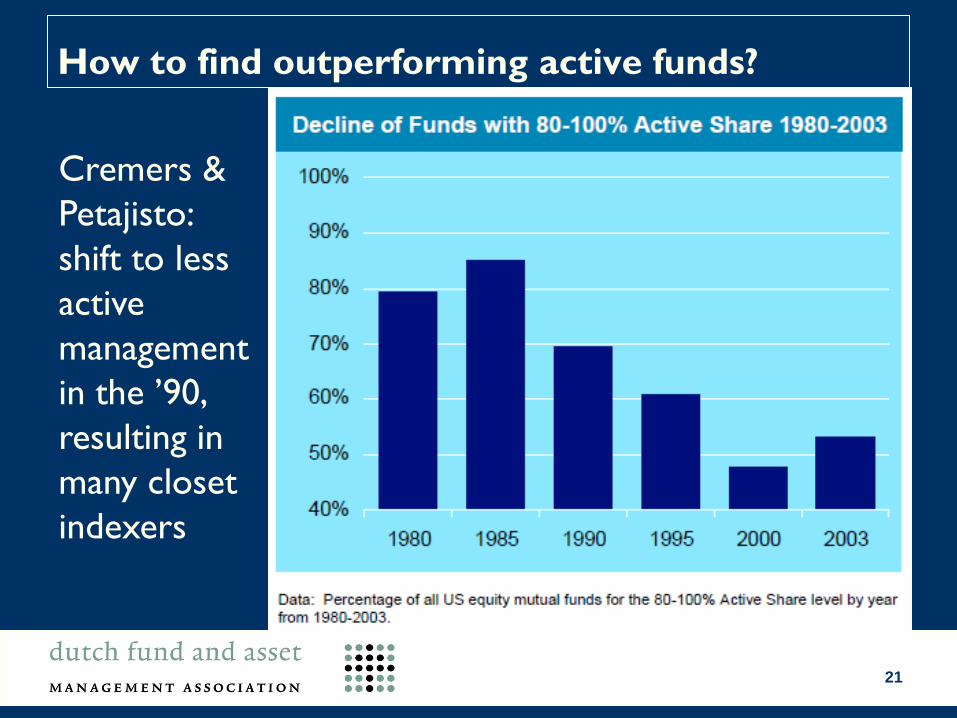

How to find outperforming active funds?

Look at the ‘active share’ of the fund: difference

between the weights in the fund portfolio and the

benchmark

Cremers & Petajisto: the funds with the highest

‘active share’ perform often better than the

benchmark, both before and after expenses

Caveat emptor! This method only filters out the

closet indexers and reduces the chance of

disappointments. No guarantee for outperformance.

20

How to find outperforming active funds?

Cremers &

Petajisto:

Active share

predicts

performance

Higher active

share = higher

performance

21

How to find outperforming active funds?

Cremers &

Petajisto:

shift to less

active

management

in the ’90,

resulting in

many closet

indexers

22

C&P: more AuM and less active management over time

23

How to find outperforming active funds?

Cremers &

Petajisto:

low-active-

share funds

have a far

lower

tracking

error than

high active

share funds

24

How to find outperforming active funds?

Cremers &

Petajisto:

it makes

sense to

weed out the

closet

indexers

from your

portfolio!

25

C&P: High ‘active share' funds outperform market & (closet) index funds

26

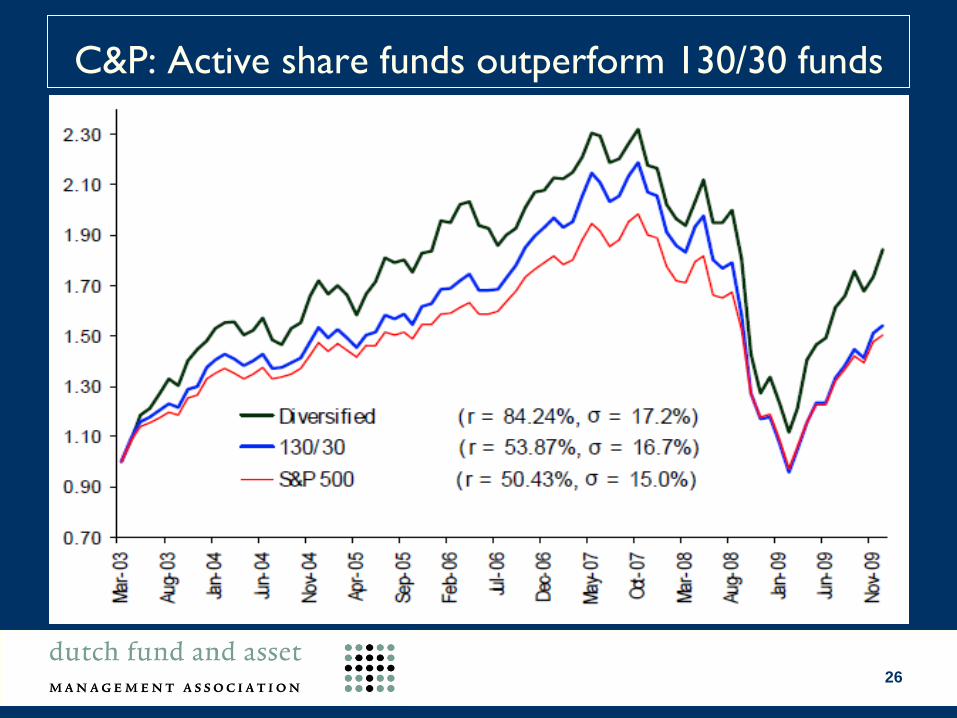

C&P: Active share funds outperform 130/30 funds

27

How to find outperforming active funds?

Cremers &

Petajisto

segment all

types of

funds by

combining

active share

with

tracking

error

28

C&P: stock pickers outperform other fund segments

29

How to find outperforming active funds?

Use ‘active share’ to identify better-performing funds.

Will this hold in the future?

Cremers & Petajisto: yes, for two reasons:

(1) generating alpha requires deviating from the

benchmark, and (2) no data mining in these results.

Long run outlook: any easy rule for earning positive

alphas in the market is an anomaly which should not

exist forever.

30

Symbiosis

Active investors do fundamental analysis

valuation on which stock & bond prices are based

Index trackers rely on active investors’ assessments

Index investors are a multiplier to active investors’

decisions

31

DUFAS – evenhanded approach

Index investing is not superior to active investing

Active investing is not superior to index investing

Both have a legitimate place in a client’s portfolio

Apply core satellite strategies

But: look for Active Share funds!