ACTEX STAM EXAM MANUAL - TABLE OF CONTENTSsheldon/ACT451-2019/Sections-1-6.pdf · Actex Learning...

94

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics ACTEX STAM EXAM MANUAL - TABLE OF CONTENTS INTRODUCTORY COMMENTS NOTES AND PROBLEM SETS SECTION 1 - Preliminary Review - Probability 1 PROBLEM SET 1 9 SECTION 2 - Preliminary Review - Random Variables I 19 PROBLEM SET 2 29 SECTION 3 - Preliminary Review - Random Variables II 33 PROBLEM SET 3 43 SECTION 4 - Preliminary Review - Random Variables III 51 PROBLEM SET 4 59 SECTION 5 - Parametric Distributions and Transformations 65 PROBLEM SET 5 73 SECTION 6 - Distribution Tail Behavior 81 PROBLEM SET 6 85 SECTION 7 - Mixture of Two Distributions 87 PROBLEM SET 7 93 SECTION 8 - Mixture of Distributions 101 8 PROBLEM SET 8 107 SECTION 9 - Continuous Mixtures 115 PROBLEM SET 9 121 SECTION 10 - Frequency Models 129 PROBLEM SET 10 137 SECTION 11 - Policy Limits 155 PROBLEM SET 11 159 SECTION 12 - Policy Deductible (1), The Cost Per Loss 161 PROBLEM SET 12 167 SECTION 13 - Policy Deductible (2), The Cost Per Loss 179 PROBLEM SET 13 185 SECTION 14 - Deductibles Applied to the Uniform, Exponential and Pareto Distributions 197 PROBLEM SET 14 205

Transcript of ACTEX STAM EXAM MANUAL - TABLE OF CONTENTSsheldon/ACT451-2019/Sections-1-6.pdf · Actex Learning...

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

ACTEX STAM EXAM MANUAL - TABLE OF CONTENTS

INTRODUCTORY COMMENTS

NOTES AND PROBLEM SETS

SECTION 1 - Preliminary Review - Probability 1PROBLEM SET 1 9

SECTION 2 - Preliminary Review - Random Variables I 19PROBLEM SET 2 29

SECTION 3 - Preliminary Review - Random Variables II 33PROBLEM SET 3 43

SECTION 4 - Preliminary Review - Random Variables III 51PROBLEM SET 4 59

SECTION 5 - Parametric Distributions and Transformations 65PROBLEM SET 5 73

SECTION 6 - Distribution Tail Behavior 81PROBLEM SET 6 85

SECTION 7 - Mixture of Two Distributions 87PROBLEM SET 7 93

SECTION 8 - Mixture of Distributions 1018PROBLEM SET 8 107

SECTION 9 - Continuous Mixtures 115PROBLEM SET 9 121

SECTION 10 - Frequency Models 129PROBLEM SET 10 137

SECTION 11 - Policy Limits 155PROBLEM SET 11 159

SECTION 12 - Policy Deductible (1), The Cost Per Loss 161PROBLEM SET 12 167

SECTION 13 - Policy Deductible (2), The Cost Per Loss 179PROBLEM SET 13 185

SECTION 14 - Deductibles Applied to the Uniform, Exponential and Pareto Distributions 197PROBLEM SET 14 205

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 15 - Combined Limit and Deductible 209PROBLEM SET 15 215

SECTION 16 - Additional Policy Adjustments 231PROBLEM SET 16 235

SECTION 17 - Models for the Aggregate Loss, Compound Distributions (1) 243PROBLEM SET 17 247

SECTION 18 - Compound Distributions (2) 271PROBLEM SET 18 277

SECTION 19 - More Properties of the Aggregate Loss Random Variable 291PROBLEM SET 19 295

SECTION 20 - Stop Loss Insurance 313PROBLEM SET 20 321

SECTION 21 - Risk Measures 331PROBLEM SET 21 335

SECTION 22 - Data and Estimation Review 339

SECTION 23 - Maximum Likelihood Estimation Based on Complete Data 343PROBLEM SET 23 347

SECTION 24 - Maximum Likelihood Estimation Based on Incomplete Data 355PROBLEM SET 24 363

SECTION 25 - Maximum Likelihood Estimation for the Exponential Distribution 369PROBLEM SET 25 375

SECTION 26 - MLE Applied to Pareto and Weibull Distributions 383PROBLEM SET 26 393

SECTION 27 - MLE Applied to STAM Exam Table Distributions 403PROBLEM SET 27 413

SECTION 28 - Review of Mathematical Statistics 423PROBLEM SET 28 431

SECTION 29 - Properties of Maximum Likelihood Estimators 437PROBLEM SET 29 441

SECTION 30 - Hypothesis Tests For Fitted Models 451PROBLEM SET 30 463

SECTION 31 - Graphical Methods for Evaluating Fitted Models 485PROBLEM SET 30 489

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 32 - Limited Fluctuation Credibility 495PROBLEM SET 32 509

SECTION 33 - Bayesian Estimation, Discrete Prior 527PROBLEM SET 33 537

SECTION 34 - Bayesian Credibility, Discrete Prior 553PROBLEM SET 34 563

SECTION 35 - Bayesian Credibility, Continuous Prior 593PROBLEM SET 35 601

SECTION 36 - Bayesian Credibility Applied to Distributions in STAM Exam Table 625PROBLEM SET 36 635

SECTION 37 - Buhlmann Bayesian 655PROBLEM SET 37 665

SECTION 38 - Empirical Bayes Credibility 713PROBLEM SET 38 721

SECTION 39 - Major Medical and Dental Coverage 749

SECTION 40 - Property and Casualty Coverages 751

SECTION 41 - Loss Reserving 755PROBLEM SET 41 765

SECTION 42 - Ratemaking 779PROBLEM SET 42 787

SECTION 43 - Additional Casualty Insurance Topics 793PROBLEM SET 43 797

PRACTICE EXAMS

PRACTICE EXAM 1 801

PRACTICE EXAM 2 819

PRACTICE EXAM 3 835

PRACTICE EXAM 4 853

PRACTICE EXAM 5 871

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Actex Learning SOA STAM Exam - Short Term Actuarial Mathematics

INTRODUCTORY COMMENTS

This study guide is designed to help in the preparation for the Society of Actuaries STAM Exam.

The first part of this manual consists of a summary of notes, illustrative examples and problem sets withdetailed solutions. The second part consists of 5 practice exams.

The practice exams all have 35 questions. The level of difficulty of the practice exams has been designedto be similar to that of the past 3.5-hour exams. Some of the questions in the problem sets are taken fromthe relevant topics on SOA exams that have been released prior to 2009 but the practice exam questionsare not from old SOA exams.

I have attempted to be thorough in the coverage of the topics upon which the exam is based, andconsistent with the notation and content of the official references. I have been, perhaps, more thoroughthan necessary on a couple of topics, such as maximum likelihood estimation and Bayesian credibility.

Because of the time constraint on the exam, a crucial aspect of exam taking is the ability to work quickly.I believe that working through many problems and examples is a good way to build up the speed at whichyou work. It can also be worthwhile to work through problems that have been done before, as this helpsto reinforce familiarity, understanding and confidence. Working many problems will also help in beingable to more quickly identify topic and question types. I have attempted, wherever possible, to emphasizeshortcuts and efficient and systematic ways of setting up solutions. There are also occasional commentson interpretation of the language used in some exam questions. While the focus of the study guide is onexam preparation, from time to time there will be comments on underlying theory in places that I feelthose comments may provide useful insight into a topic.

The notes and examples are divided into 42 sections of varying lengths, with some suggested time framesfor covering the material. There are almost 200 examples in the notes and over 900 exercises in theproblem sets, all with detailed solutions. The 5 practice exams have 35 questions each, also with detailedsolutions. Some of the examples and exercises are taken from previous SOA exams. Some of the in theproblem sets that have come from previous SOA exams. Some of the problem set exercises are more indepth than actual exam questions, but the practice exam questions have been created in an attempt toreplicate the level of depth and difficulty of actual exam questions. In total there are almost 1300examples/problems/sample exam questions with detailed solutions. ACTEX gratefully acknowledges theSOA for allowing the use of their exam problems in this study guide.

I suggest that you work through the study guide by studying a section of notes and then attempting theexercises in the problem set that follows that section. The order of the sections of notes is the order that Irecommend in covering the material, although the material on pricing and reserving in Sections 39 to 42is independent of the other material on the exam. The order of topics in this manual is not the same as theorder presented on the exam syllabus.

It has been my intention to make this study guide self-contained and comprehensive for the STAM Examtopics, however there are some exam topics for which the study notes are essentially summaries ofconcepts. For that material, I have attempted to summarize concepts as well, but it is best to refer tooriginal reference material on all topics.

While the ability to derive formulas used on the exam is usually not the focus of an exam question, it isuseful in enhancing the understanding of the material and may be helpful in memorizing formulas. Theremay be an occasional reference in the review notes to a derivation, but you are encouraged to review theofficial reference material for more detail on formula derivations.

Actex Learning SOA STAM Exam - Short Term Actuarial Mathematics

In order for the review notes in this study guide to be most effective, you should have some backgroundat the junior or senior college level in probability and statistics. It will be assumed that you are reasonablyfamiliar with differential and integral calculus. The prerequisite concepts to modeling and modelestimation are reviewed in this study guide. The study guide begins with a detailed review of probabilitydistribution concepts such as distribution function, hazard rate, expectation and variance.

Of the various calculators that are allowed for use on the exam, I am most familiar with theBA II PLUS. It has several easily accessible memories. The TI-30X IIS has the advantage of a multi-line display. Both have the functionality needed for the exam.

There is a set of tables that has been provided with the exam in past sittings. These tables consist of somedetailed description of a number of probability distributions along with tables for the standard normal andchi-squared distributions. The tables can be downloaded from the SOA website www.soa.org .

If you have any questions, comments, criticisms or compliments regarding this study guide, pleasecontact the publisher ACTEX, or you may contact me directly at the address below. I apologize inadvance for any errors, typographical or otherwise, that you might find, and it would be greatlyappreciated if you would bring them to my attention. ACTEX will be maintaining a website for errata thatcan be accessed from www.actexmadriver.com .

It is my sincere hope that you find this study guide helpful and useful in your preparation for the exam. Iwish you the best of luck on the exam.

Samuel A. Broverman Department of Statistical Sciences www.sambroverman.comUniversity of Toronto E-mail: [email protected] or [email protected]

NOTES

AND

PROBLEM SETS

SECTION 1 - PRELIMINARY REVIEW - PROBABILITY STAM-1

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 1 - PRELIMINARY REVIEW - PROBABILITYBasic Probability, Conditional Probability and Independence

A significant part of the STAM Exam involves probability and statistical methods applied to various aspects ofloss modeling and model estimation. A good background in probability and statistics is necessary to fullyunderstand models and the modeling that is done. In this section of the study guide, we will review fundamentalprobability rules.

1.1 Basic Probability Concepts

Sample point and probability spaceA sample point is the simple outcome of a random experiment. The probability space (also called sample space) isthe collection of all possible sample points related to a specified experiment. When the experiment is performed,one of the sample points will be the outcome. An experiment could be observing the loss that occurs on anautomobile insurance policy during the course of one year, or observing the number of claims arriving at aninsurance office in one week. The probability space is the "full set" of possible outcomes of the experiment. In thecase of the automobile insurance policy, it would be the range of possible loss amounts that could occur duringthe year, and in the case of the insurance office weekly number of claims, the probability space would be the setof integers .Ö!ß "ß #ß ÞÞÞ×

EventAny collection of sample points, or any subset of the probability space is referred to as an event. We say "event Ehas occurred" if the experimental outcome was one of the sample points in .E

Union of events and E FE ∪ F E F E F denotes the union of events and , and consists of all sample points that are in either or .

A B Union of events E ßE ß ÞÞÞßE" # 8

E ∪ E ∪â∪E œ ∪ E E ßE ß ÞÞÞß E3 œ "

8" # 8 3 " # 8 denotes the union of the events , and consists of all sample points

that are in at least one of the 's. This definition can be extended to the union of infinitely many events.E3

STAM-2 SECTION 1 - PRELIMINARY REVIEW - PROBABLITY

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Intersection of events E ßE ß ÞÞÞßE" # 8

E ∩ E ∩â∩E œ ∩ E E ßE ß ÞÞÞß E3 œ "

8" # 8 3 " # 8 denotes the intersection of the events , and consists of all sample

points that are simultaneously in all of the 's.E3

A B Mutually exclusive eventsE ßE ß ÞÞÞßE" # 8

Two events are mutually exclusive if they have no sample points in common, or equivalently, if they have emptyintersection. Events are mutually exclusive if for all , where denotes the emptyE ßE ß ÞÞÞß E E ∩ E œ g 3 Á 4 g" # 8 3 4

set with no sample points. Mutually exclusive events cannot occur simultaneously.

Exhaustive eventsF ßF ß ÞÞÞßF" # 8

If , the entire probability space, then the events are referred to asF ∪ F ∪â∪F œ W F ßF ß ÞÞÞß F" # 8 " # 8

exhaustive events.

Complement of event EThe complement of event consists of all sample points in the probability space that are . TheE not in Ecomplement is denoted or and is equal to . When the underlying randomEß µ Eß E E ÖB À B Â E×

w -

experiment is performed, to say that the complement of has occurred is the same as saying that has notE Eoccurred.

Subevent (or subset) of event E FIf event contains all the sample points in event , then is a subevent of , denoted . The occurrenceF E E F E § Fof event implies that event has occurred.E F

Partition of event EEvents form a partition of event if and the 's are mutually exclusive.G ßG ß ÞÞÞß G E E œ ∪ G G

3 œ "

8" # 8 3 3

DeMorgan's Laws (i) , to say that has not occurred is to say that has not occurredÐE ∪ FÑ œ E ∩ F E ∪ F Ew w w

has not occurred ; this rule generalizes to any number of events;and F

∪ E œ Ð3 œ "

83

w

E ∪ E ∪â∪E Ñ œ E ∩ E ∩â∩E œ ∩ E3 œ "

8" # 8

w w w w w" # 8 3

(ii) , to say that has not occurred is to say that either has notÐE ∩ FÑ œ E ∪ F E ∩ F Ew w w

occurred has not occurred (or both have not occurred) ; this rule generalizes to any or F

number of events, ∩ E œ Ð3 œ "

83

w

E ∩ E ∩â∩E Ñ œ E ∪ E ∪â∪E œ ∪ E3 œ "

8" # 8

w w w w w" # 8 3

SECTION 1 - PRELIMINARY REVIEW - PROBABILITY STAM-3

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Indicator function for event E

The function is the indicator function for event , where denotes a sample point. is 1M ÐBÑ œ E B M ÐBÑE E

" B−E

! BÂE if

if

if event has occurred.E

Some important rules concerning probability are given below.

(i) if is the entire probability space (when the underlying experiment isT ÒWÓ œ " W performed, some outcome must occur with probability 1).

(ii) (the probability of no face turning up when we toss a die is 0).T ÒgÓ œ !

(iii) If events are mutually exclusive (also called disjoint) thenE ßE ß ÞÞÞß E" # 8

(1.1)T Ò ∪ E Ó œ T ÒE ∪ E ∪â∪E Ó œ T ÒE Ó T ÒE Ó â TÒE Ó œ T ÒE Ó3 œ "

83 " # 8 " # 8 3

3œ"

8

This extends to infinitely many mutually exclusive events.

(iv) For any event , E ! Ÿ T ÒEÓ Ÿ "

(v) If then E § F TÒEÓ Ÿ T ÒFÓ

(vi) For any events , and , (1.2)E F G T ÒE ∪ FÓ œ T ÒEÓ T ÒFÓ T ÒE ∩ FÓ

(vii) For any event , (1.3)E TÒE Ó œ " T ÒEÓw

(viii) For any events and , (1.4)E F TÒEÓ œ T ÒE ∩ FÓ T ÒE ∩ F Ów

(ix) For exhaustive events , (1.5) F ßF ß ÞÞÞß F T Ò ∪ F Ó œ "3 œ "

8" # 8 3

If are exhaustive and mutually exclusive, they form a partition of the entireF ßF ß ÞÞÞß F" # 8

probability space, and for any event ,E

(1.6)T ÒEÓ œ T ÒE ∩ F Ó T ÒE ∩ F Ó â TÒE ∩ F Ó œ T ÒE ∩ F Ó" # 8 33œ"

8(x) The words "percentage" and "proportion" are used as alternatives to "probability". As an example, if we are

told that the percentage or proportion of a group of people that are of a certain type is 20%, this is generallyinterpreted to mean that a randomly chosen person from the group has a 20% probability of being of thattype. This is the "long-run frequency" interpretation of probability. As another example, suppose that we aretossing a fair die. In the long-run frequency interpretation of probability, to say that the probability of tossinga 1 is is the same as saying that if we repeatedly toss the die, the proportion of tosses that are 1's will"

'

approach ."'

STAM-4 SECTION 1 - PRELIMINARY REVIEW - PROBABLITY

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

1.2 Conditional Probability and Independence of Events

Conditional probability arises throughout the STAM Exam material. It is important to be familiar and comfortablewith the definitions and rules of conditional probability.

Conditional probability of event given event E F

If , then is the conditional probability that event occurs given that event TÐFÑ ! E FTÐElFÑ œTÐE∩FÑT ÐFÑ

has occurred. By rewriting the equation we get .TÐE ∩ FÑ œ TÐElFÑ † T ÐFÑ

Partition of a Probability SpaceEvents are said to form a partition of a probability space ifF ßF ß ÞÞÞß F W" # 8

(i) and (ii) for any pair with .F ∪ F ∪â∪F œ W F ∩ F œ g 3 Á 4" # 8 3 4

A partition is a disjoint collection of events which combines to be the full probability space.A simple example of a partition is any event and its complement .F Fw

If is any event in probability space and is a partition of probability space , thenE W ÖF ßF ß ÞÞÞß F × W" # 8

T ÐEÑ œ TÐE ∩ F Ñ TÐE ∩ F Ñ â TÐE ∩ F Ñ" # 8 .A special case of this rule is for any two events and .TÐEÑ œ TÐE ∩ FÑ TÐE ∩ F Ñ E Fw

A B

A B A B

1B2B

1A B

3B 4B

2A B3A B

4A B

Bayes rule and Bayes Theorem

For any events and with , E F TÐEÑ ! TÐFlEÑ œ TÐElFÑ‚TÐFÑT ÐEÑ (1.7)

If form a partition of the entire sample space , thenF ßF ß ÞÞÞß F W" # 8

for each (1.8)TÐF lEÑ œ 4 œ "ß #ß ÞÞÞß 84T ÐElF Ñ‚TÐF Ñ

T ÐElF Ñ‚TÐF Ñ

4 4

3œ"

8

3 3

The values of are called prior probabilities, and the value of is called a posterior probability.TÐF Ñ T ÐF lEÑ4 4

Variations on this rule are very important in Bayesian credibility.

SECTION 1 - PRELIMINARY REVIEW - PROBABILITY STAM-5

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Independent events and E FIf events and satisfy the relationship , then the events are said to beE F TÐE ∩FÑ œ TÐEÑ ‚ TÐFÑindependent or stochastically independent or statistically independent. The independence of (non-empty) eventsE F TÐElFÑ œ TÐEÑ T ÐFlEÑ œ TÐFÑ and is equivalent to or .

Mutually independent events E ßE ß ÞÞÞßE" # 8

The events are mutually independent if

(i) for any and , , andE E TÐE ∩ E Ñ œ TÐE Ñ ‚ TÐE Ñ3 4 3 4 3 4

(ii) for any , and , ,E E E TÐE ∩ E ∩ E Ñ œ TÐE Ñ ‚ TÐE Ñ ‚ TÐE Ñ3 4 5 3 4 5 3 4 5

and so on for any subcollection of the events, including all events:

(1.9)TÐE ∩ E ∩â∩E Ñ œ TÐE Ñ ‚ TÐE Ñ ‚â‚ TÐE Ñ œ TÐE Ñ" # 8 " # 8 33œ"

8

Here are some rules concerning conditional probability and independence. These can be verifiedin a fairly straightforward way from the definitions given above.

(i) for any events and (1.10)TÐE ∪ FÑ œ TÐEÑ TÐFÑ TÐE ∩ FÑ E F

(ii) for any events and (1.11)TÐE ∩ FÑ œ TÐFlEÑ ‚ TÐEÑ œ TÐElFÑ ‚ TÐFÑ E F

(iii) If form a partition of the sample space , then for any event F ßF ß ÞÞÞß F W E" # 8

(1.12)TÐEÑ œ TÐE ∩ F Ñ œ TÐElF Ñ ‚ TÐF Ñ 3œ" 3œ"

8 8

3 3 3

As a special case, for any events and , we haveE F

(1.13)TÐEÑ œ TÐE ∩ FÑ TÐE ∩ F Ñ œ TÐElFÑ ‚ TÐFÑ TÐElF Ñ ‚ TÐF Ñw w w

(iv) If , thenTÐE ∩ E ∩â∩E Ñ !" # 8"

TÐE ∩ E ∩â∩E Ñ œ TÐE Ñ ‚ TÐE lE Ñ ‚ TÐE lE ∩ E Ñ ‚â‚ TÐE lE ∩ E ∩â∩E Ñ" # 8 " # " $ " # 8 " # 8"

(v) and (1.14)TÐE Ñ œ " TÐEÑ T ÐE lFÑ œ " TÐElFÑw w

(vi) if then , and E § F TÐElFÑ œ œ TÐFlEÑ œ "TÐE∩FÑ T ÐEÑT ÐFÑ T ÐFÑ

(vii) if and are independent events then and are independent events, and are independentE F E F E Fw w

events, and and are independent eventsE Fw w

(viii) since for any event , it follows that is independent ofTÐgÑ œ TÐg ∩ EÑ œ ! œ TÐgÑ † T ÐEÑ E g any event E

STAM-6 SECTION 1 - PRELIMINARY REVIEW - PROBABLITY

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Example 1-1:Suppose a fair six-sided die is tossed. We define the following events:

"the number tossed is " , "the number tossed is even"E œ Ÿ $ œ Ö"ß #ß $× F œ œ Ö#ß %ß '× "the number tossed is a or a "G œ " # œ Ö"ß #× "the number tossed doesn't start with the letters 'f' or 't'"H œ œ Ö"ß '×

The conditional probability of given isE F

TÐElFÑ œ œ œ œTÐÖ"ß#ß$×∩Ö#ß%ß'×Ñ T ÐÖ#×Ñ "Î'

T ÐÖ#ß%ß'×Ñ T ÐÖ#ß%ß'×Ñ "Î# $" .

Events and are not independent, sinceE F œ TÐE ∩ FÑ Á TÐEÑ ‚ TÐFÑ œ œ ," " " "' # # %†

or alternatively, events and are not independent since .E F TÐElFÑ Á TÐEÑ

T ÐElGÑ œ Á œ TÐEÑ E G" "# , so that and are not independent.

TÐFlGÑ œ œ TÐFÑ F G"# , so that and are independent

(alternatively, ).TÐF ∩ GÑ œ TÐÖ#×Ñ œ œ œ TÐFÑ † T ÐGÑ" " "' # $†

It is not difficult to check that both and are independent of . E F H

IMPORTANT NOTE: The following manipulation of event probabilities arises from time to time:T E œ T ElF † T ÐFÑ T ElF TÐF Ñ( ) ( ) ( )w w‚ E. If we know the conditional probabilities for event givensome other event and its complement , and if we know the (unconditional) probability of event , then weF F Fw

can find the probability of event . One of the important aspects of applying this relationship is the determinationEof the appropriate events and .E F

Example 1-2:Urn I contains 2 white and 2 black balls and Urn II contains 3 white and 2 black balls. An Urn is chosen at random, and aball is randomly selected from that Urn. Find the probability that the ball chosen is white.Solution:Let be the event that Urn I is chosen and is the event that Urn II is chosen. The implicit assumption is thatF Fw

both Urns are equally likely to be chosen (this is the meaning of "an Urn is chosen at random"). Therefore,TÐFÑ œ TÐF Ñ œ E" "

# #and Let be the event that the ball chosen in white. If we know that Urn I was chosen,w .

then there is probability of choosing a white ball (2 white out of 4 balls, it is assumed that each ball has the "#

same chance of being chosen); this can be described as .TÐElFÑ œ "#

In a similar way, if Urn II is chosen, then (3 white out of 5 balls). We can now apply theTÐElF Ñ œw $&

relationship described prior to this example. , andTÐE ∩ FÑ œ TÐElFÑ T ÐFÑ œ œ‚ Ð ÑÐ Ñ" " "# # %

T ÐE ∩ F Ñ œ TÐElF Ñ T ÐF Ñ œ œw w w‚ Ð ÑÐ Ñ$ " $& # "! . Finally,

TÐEÑ œ TÐE ∩ FÑ TÐE ∩ F Ñ œ œw " $ ""% "! #! .

The order of calculations can be summarized in the following table EF TÐE ∩ FÑ œ TÐElFÑ ‚ TÐFÑ 1.

Fw 2. TÐE ∩ F Ñ œ TÐElF Ñ ‚ TÐF Ñw w w

3. TÐEÑ œ TÐE ∩ FÑ TÐE ∩ F Ñw

SECTION 1 - PRELIMINARY REVIEW - PROBABILITY STAM-7

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Example 1-3:Urn I contains 2 white and 2 black balls and Urn II contains 3 white and 2 black balls. One ball is chosen atrandom from Urn I and transferred to Urn II, and then a ball is chosen at random from Urn II. The ball chosenfrom Urn II is observed to be white. Find the probability that the ball transferred from Urn I to Urn II was white.Solution:Let denote the event that the ball transferred from Urn I to Urn II was white and let denote the event that theF Eball chosen from Urn II is white. We are asked to find .TÐFlEÑ

From the simple nature of the situation (and the usual assumption of uniformity in such a situation, meaning allballs are equally likely to be chosen from Urn I in the first step), we have

TÐFÑ œ T ÒF Ó œ" "# # (2 of the 4 balls in Urn I are white), and by implication, it follows that .w

If the ball transferred is white, then Urn II has 4 white and 2 black balls, and the probability ofchoosing a white ball out of Urn II is ; this is . # #

$ $T ÐElFÑ œ

If the ball transferred is black, then Urn II has 3 white and 3 black balls, and the probability ofchoosing a white ball out of Urn II is ; this is . " "

# #T ÐElF Ñ œw

All of the information needed has been identified. We do calculations in the following order:

1. T ÒE ∩ FÓ œ T ÒElFÓ T ÒFÓ œ œ‚ Ð ÑÐ Ñ# " "$ # $

2. T ÒE ∩ F Ó œ T ÒElF Ó T ÒF Ó œ œw w w‚ Ð ÑÐ Ñ" " "# # %

3. T ÒEÓ œ T ÒE ∩ FÓ T ÒE ∩ F Ó œ œw " " ($ % "#

4. T ÒFlEÓ œ œ œTÒF∩EÓ "Î$T ÒEÓ (Î"# (

%

Example 1-4:Three dice have the following probabilities of throwing a "six": : ß ; ß < ßrespectively. One of the dice is chosen at random and thrown (each is equally likely to be chosen). A "six"appeared. What is the probability that the die chosen was the first one?Solution:The event " a 6 is thrown" is denoted by "6"

T Ò "l ' Ó œ œ œdie " "T ÒÐ "Ñ∩Ð ' ÑÓ T Ò ' l "Ó T Ò "Ó

T Ò ' Ó T Ò ' Ó T Ò ' Ó

:†die " " " " die die" " " " " "

‚"$

But " " " " die " " die " " dieT Ò ' Ó œ T ÒÐ ' Ñ ∩ Ð "ÑÓ T ÒÐ ' Ñ ∩ Ð #ÑÓ T ÒÐ ' Ñ ∩ Ð $ÑÓ " " die die " " die die " " die dieœ TÒ ' l "Ó ‚ T Ò "Ó T Ò ' l #Ó ‚ T Ò #Ó T Ò ' l $Ó ‚ T Ò $Ó

die " " œ : ‚ ; ‚ < ‚ œ p T Ò "l ' Ó œ œ œ" " "$ $ $

‚ ‚:;< :$ T Ò ' Ó :;<

: :

Ð:;<ц

" "$ $

"$

" "

STAM-8 SECTION 1 - PRELIMINARY REVIEW - PROBABLITY

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 1 PROBLEM SET STAM-9

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 1 PROBLEM SETPreliminary Review - Probability

1. A survey of 1000 people determines that 80% like walking and 60% like biking, and all like at least one ofthe two activities. How many people in the survey like biking but not walking?

A) 0 B) 0.1 C) 0.2 D) 0.3 E) 0.4

2. A life insurer classifies insurance applicants according to the following attributes: - the applicant is maleQ - the applicant is a homeownerL Out of a large number of applicants the insurer has identified the following information: 40% of applicants are male, 40% of applicants are homeowners and 20% of applicants are female homeowners. Find the percentage of applicants who are male and do not own a home. A) .1 B) .2 C) .3 D) .4 E) .5

3. Let and be events such that , andEß Fß G H F œ E ß G ∩ H œ gw

, , , , , T ÒEÓ œ T ÒFÓ œ T ÒGlEÓ œ T ÒGlFÓ œ T ÒHlEÓ œ T ÒHlFÓ œ" $ " $ " "% % # % % )

Calculate .T ÒG ∪ HÓ

A) B) C) D) E)& " #( $$# % $# % "

4. You are given that and .T ÒEÓ œ Þ& T ÒE ∪ FÓ œ Þ( Actuary 1 assumes that and are independent and calculates based on that assumption.E F TÒFÓ Actuary 2 assumes that and mutually exclusive and calculates based on that assumption. FindE F TÒFÓ

the absolute difference between the two calculations. A) 0 B) .05 C) .10 D) .15 E) .20

5. A test for a disease correctly diagnoses a diseased person as having the disease with probability .85. Thetest incorrectly diagnoses someone without the disease as having the disease with a probability of .10. If 1%of the people in a population have the disease, what is the chance that a person from this population whotests positive for the disease actually has the disease?

A) B) C) D) E) !Þ!!)& !Þ!(*" !Þ"!(& !Þ"&!! !Þ*!!!

6. Two bowls each contain 5 black and 5 white balls. A ball is chosen at random from bowl 1 and put intobowl 2. A ball is then chosen at random from bowl 2 and put into bowl 1. Find the probability that bowl 1still has 5 black and 5 white balls.

A) B) C) D) E) # $ ' " '$ & "" # "$

7. People passing by a city intersection are asked for the month in which they were born. It is assumed that thepopulation is uniformly divided by birth month, so that any randomly passing person has an equally likelychance of being born in any particular month. Find the minimum number of people needed so that theprobability that no two people have the same birth month is less than .5.

A) 2 B) 3 C) 4 D) 5 E) 6

STAM-10 SECTION 1 PROBLEM SET

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

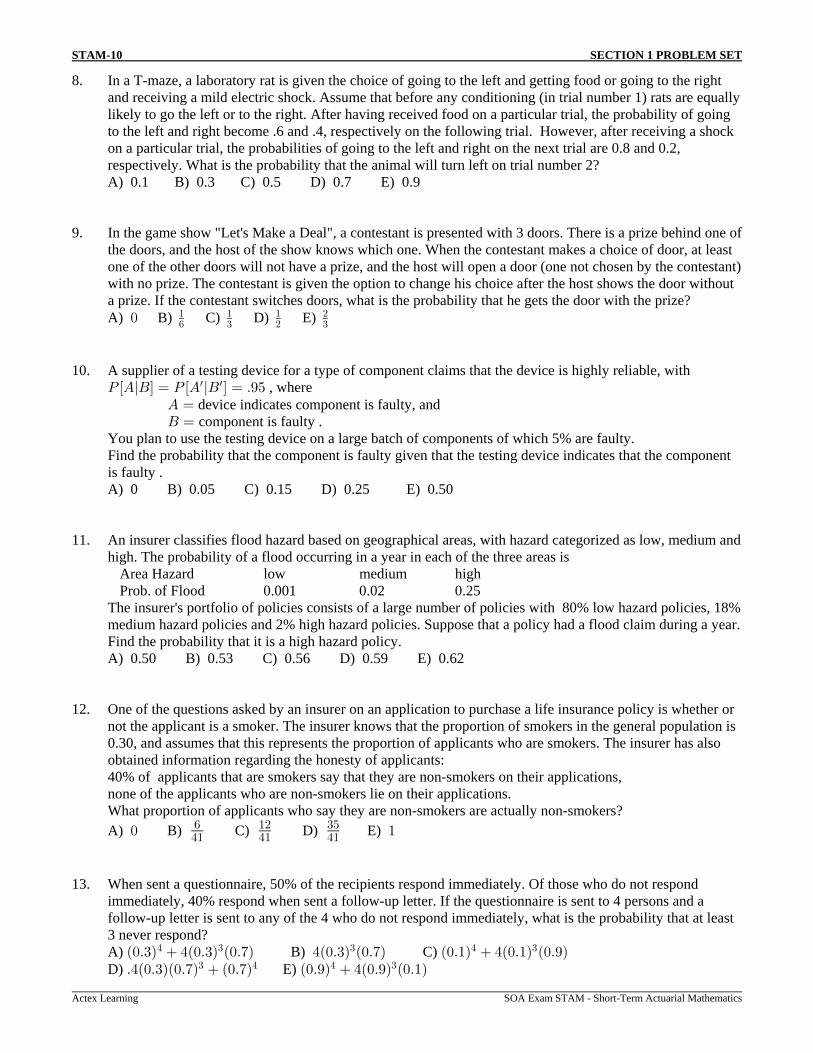

8. In a T-maze, a laboratory rat is given the choice of going to the left and getting food or going to the rightand receiving a mild electric shock. Assume that before any conditioning (in trial number 1) rats are equallylikely to go the left or to the right. After having received food on a particular trial, the probability of goingto the left and right become .6 and .4, respectively on the following trial. However, after receiving a shockon a particular trial, the probabilities of going to the left and right on the next trial are 0.8 and 0.2,respectively. What is the probability that the animal will turn left on trial number 2?

A) 0.1 B) 0.3 C) 0.5 D) 0.7 E) 0.9

9. In the game show "Let's Make a Deal", a contestant is presented with 3 doors. There is a prize behind one ofthe doors, and the host of the show knows which one. When the contestant makes a choice of door, at leastone of the other doors will not have a prize, and the host will open a door (one not chosen by the contestant)with no prize. The contestant is given the option to change his choice after the host shows the door withouta prize. If the contestant switches doors, what is the probability that he gets the door with the prize?

A) B) C) D) E)! " " " #' $ # $

10. A supplier of a testing device for a type of component claims that the device is highly reliable, withT ÒElFÓ œ T ÒE lF Ó œ Þ*&w w , where

device indicates component is faulty, andE œ component is faulty .F œ You plan to use the testing device on a large batch of components of which 5% are faulty. Find the probability that the component is faulty given that the testing device indicates that the component

is faulty . A) 0 B) 0.05 C) 0.15 D) 0.25 E) 0.50

11. An insurer classifies flood hazard based on geographical areas, with hazard categorized as low, medium andhigh. The probability of a flood occurring in a year in each of the three areas is

Area Hazard low medium high Prob. of Flood 0.001 0.02 0.25 The insurer's portfolio of policies consists of a large number of policies with 80% low hazard policies, 18%

medium hazard policies and 2% high hazard policies. Suppose that a policy had a flood claim during a year.Find the probability that it is a high hazard policy.

A) 0.50 B) 0.53 C) 0.56 D) 0.59 E) 0.62

12. One of the questions asked by an insurer on an application to purchase a life insurance policy is whether ornot the applicant is a smoker. The insurer knows that the proportion of smokers in the general population is0.30, and assumes that this represents the proportion of applicants who are smokers. The insurer has alsoobtained information regarding the honesty of applicants:

40% of applicants that are smokers say that they are non-smokers on their applications, none of the applicants who are non-smokers lie on their applications. What proportion of applicants who say they are non-smokers are actually non-smokers? A) B) C) D) E) ! "' "# $&

%" %" %"

13. When sent a questionnaire, 50% of the recipients respond immediately. Of those who do not respondimmediately, 40% respond when sent a follow-up letter. If the questionnaire is sent to 4 persons and afollow-up letter is sent to any of the 4 who do not respond immediately, what is the probability that at least3 never respond?

A) B) C) Ð!Þ$Ñ %Ð!Þ$Ñ Ð!Þ(Ñ %Ð!Þ$Ñ Ð!Þ(Ñ Ð!Þ"Ñ %Ð!Þ"Ñ Ð!Þ*Ñ% $ $ % $

D) E) Þ%Ð!Þ$ÑÐ!Þ(Ñ Ð!Þ(Ñ Ð!Þ*Ñ %Ð!Þ*Ñ Ð!Þ"Ñ$ % % $

SECTION 1 PROBLEM SET STAM-11

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

14. A fair coin is tossed. If a head occurs, 1 fair die is rolled; if a tail occurs, 2 fair dice are rolled. If is the]total on the die or dice, then T Ò] œ 'Ó œ

A) B) C) D) E) " & "" " ""* $' (# ' $'

15. In Canada's national 6-49 lottery, a ticket has 6 numbers each from 1 to 49, with no repeats. Find theprobability of matching exactly 4 of the 6 winning numbers if the winning numbers are all randomlychosen.

A) 0.00095 B) 0.00097 C) 0.00099 D) 0.00101 E) 0.00103

STAM-12 SECTION 1 PROBLEM SET

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 1 PROBLEM SET SOLUTIONS

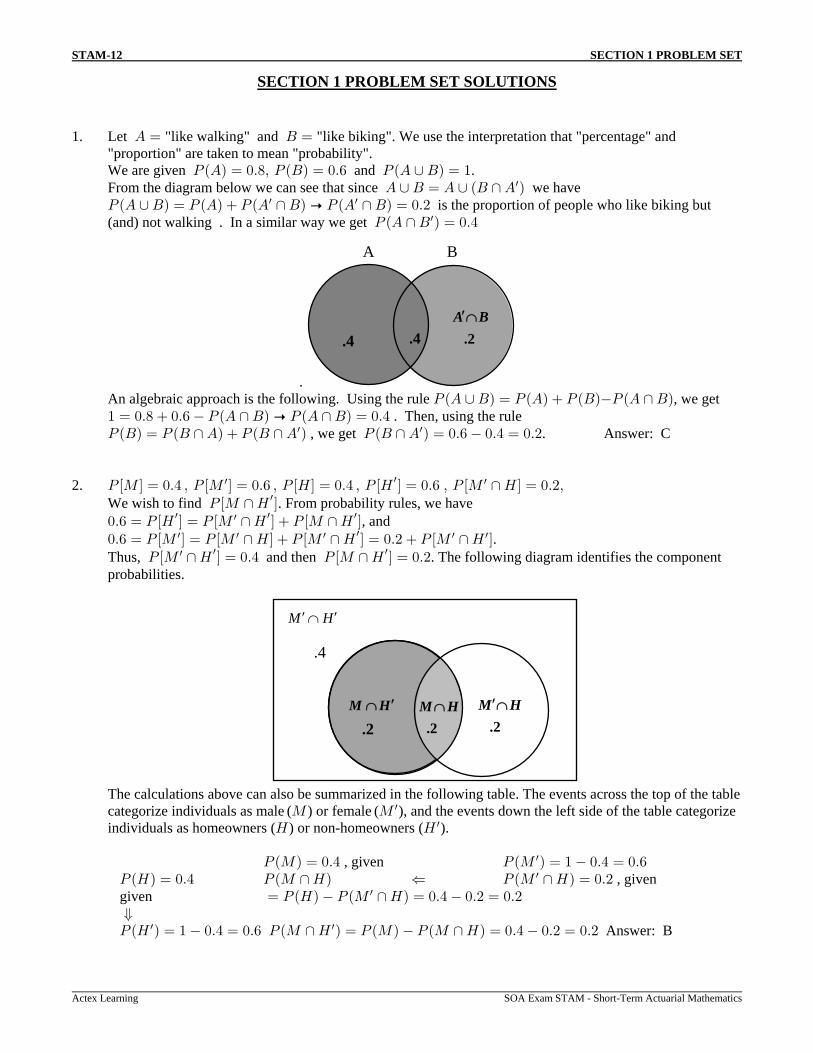

1. Let "like walking" and "like biking". We use the interpretation that "percentage" andE œ F œ"proportion" are taken to mean "probability".

We are given and .TÐEÑ œ !Þ)ß T ÐFÑ œ !Þ' T ÐE ∪ FÑ œ " From the diagram below we can see that since we haveE ∪ F œ E ∪ ÐF ∩ E Ñw

is the proportion of people who like biking butTÐE ∪ FÑ œ TÐEÑ TÐE ∩ FÑ p TÐE ∩ FÑ œ !Þ#w w

(and) not walking . In a similar way we get TÐE ∩ F Ñ œ !Þ%w

.4 .2

A B.4

BA

. An algebraic approach is the following. Using the rule , we getTÐE ∪ FÑ œ TÐEÑ TÐFÑTÐE ∩ FÑ

" œ !Þ) !Þ' TÐE ∩ FÑ p TÐE ∩ FÑ œ !Þ% . Then, using the rule , we get . Answer: CTÐFÑ œ TÐF ∩ EÑ TÐF ∩ E Ñ TÐF ∩ E Ñ œ !Þ' !Þ% œ !Þ#w w

2. T ÒQÓ œ !Þ% ß T ÒQ Ó œ !Þ' ß T ÒLÓ œ !Þ% ß T ÒL Ó œ !Þ' ß T ÒQ ∩LÓ œ !Þ#ßw ww

We wish to find . From probability rules, we haveT ÒQ ∩L Ów

, and!Þ' œ T ÒL Ó œ T ÒQ ∩L Ó T ÒQ ∩L Ów w ww

!Þ' œ T ÒQ Ó œ T ÒQ ∩LÓ T ÒQ ∩L Ó œ !Þ# T ÒQ ∩L Ów w w w ww . Thus, and then . The following diagram identifies the componentT ÒQ ∩L Ó œ !Þ% T ÒQ ∩L Ó œ !Þ#w w w

probabilities.

.2 .2

M HM H

.2

M H

.4

M H

The calculations above can also be summarized in the following table. The events across the top of the tablecategorize individuals as male ( ) or female ( ), and the events down the left side of the table categorizeQ Qw

individuals as homeowners ( ) or non-homeowners ( ).L Lw

, given TÐQÑ œ !Þ% T ÐQ Ñ œ " !Þ% œ !Þ'w

, givenTÐLÑ œ !Þ% T ÐQ ∩LÑ É TÐQ ∩LÑ œ !Þ#w

given œ TÐLÑ TÐQ ∩LÑ œ !Þ% !Þ# œ !Þ#w

Ì Answer: BTÐL Ñ œ " !Þ% œ !Þ' T ÐQ ∩L Ñ œ TÐQÑ TÐQ ∩LÑ œ !Þ% !Þ# œ !Þ#w w

SECTION 1 PROBLEM SET STAM-13

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

3. Since and have empty intersection, G H TÒG ∪ HÓ œ T ÒGÓ T ÒHÓÞ

Also, since and are "exhaustive" events (since they are complementary events, their union is the entireE Fsample space, with a combined probability of

T ÒE ∪ FÓ œ T ÒEÓ T ÒFÓ œ " ).

We use the rule , and the rule to getT ÒGÓ œ T ÒG ∩ EÓ T ÒG ∩ E Ó T ÒGlEÓ œw T ÒE∩GÓT ÒEÓ

andT ÒGÓ œ T ÒGlEÓ ‚ T ÒEÓ T ÒGlE Ó ‚ T ÒE Ó œ ‚ ‚ œw w " " $ $ ""# % % % "'

T ÒHÓ œ T ÒHlEÓ ‚ T ÒEÓ T ÒHlE Ó ‚ T ÒE Ó œ ‚ ‚ œ Þw w " " " $ &% % ) % $#

Then, Answer: C.T ÒG ∪ HÓ œ T ÒGÓ T ÒHÓ œ Þ#($#

4. Actuary 1: Since and are independent, so are and .E F E Fw w

.T ÒE ∩ F Ó œ " T ÒE ∪ FÓ œ !Þ$w w

But .!Þ$ œ T ÒE ∩ F Ó œ T ÒE Ó † T ÒF Ó œ Ð!Þ&ÑT ÒF Ó p T ÒF Ó œ !Þ' p T ÒFÓ œ !Þ%w w w w w w

Actuary 2: .!Þ( œ T ÒE ∪ FÓ œ T ÒEÓ T ÒFÓ œ !Þ& T ÒFÓ p T ÒFÓ œ !Þ# Absolute difference is . Answer: E l!Þ% Þ#l œ !Þ#

5. We define the following events: - a person has the disease,H - a person tests positive for the disease. We are given and andXT T ÒXT lHÓ œ Þ)& T ÒXT lH Ó œ Þ"!w

T ÒHÓ œ Þ!" T ÒHlXT Ó. We wish to find .

Using the formulation for conditional probability we have .T ÒHlXT Ó œT ÒH∩XT ÓT ÒXT Ó

But , andT ÒH ∩ XT Ó œ T ÒXT lHÓ ‚ T ÒHÓ œ Ð!Þ)&ÑÐ!Þ!"Ñ œ !Þ!!)& . Then,T ÒH ∩ XT Ó œ T ÒXT lH Ó ‚ T ÒH Ó œ Ð!Þ"!ÑÐ!Þ**Ñ œ !Þ!**w w w

.T ÒXT Ó œ T ÒH ∩ XT Ó T ÒH ∩ XT Ó œ Þ"!(& p T ÒHlXT Ó œ œ !Þ!(*"w !Þ!!)&!Þ"!(&

The following table summarizes the calculations.

, given T ÒHÓ œ !Þ!" Ê TÒH Ó œ " T ÒHÓ œ !Þ**w

Ì Ì T ÒH ∩ XT Ó T ÒH ∩ XT Ów

œ TÒXT lHÓ ‚ T ÒHÓ œ !Þ!!)& œ T ÒXT lH Ó ‚ T ÒH Ó œ !Þ!**w w

Ì T ÒXT Ó œ T ÒH ∩ XT Ó T ÒH ∩ XT Ó œ !Þ"!(&w

Ì

. Answer: BT ÒHlXT Ó œ œ œ !Þ!(*"T ÒH∩XT ÓT ÒXT Ó Þ"!(&

Þ!!)&

STAM-14 SECTION 1 PROBLEM SET

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

6. Let be the event that bowl 1 has 5 black balls after the exchange.G Let be the event that the ball chosen from bowl 1 is black, and let be the event that the ball chosenF F" #

from bowl 2 is black.

Event is the disjoint union of and (black-black or white-white picks), so thatG F ∩ F F ∩ F" # " #w w

T ÒGÓ œ T ÒF ∩ F Ó T ÒF ∩ F Ó" # " #w w .

The black-black combination has probability , since there is a chance of picking black fromÐ ÑÐ Ñ' " &"" # "!

bowl 1, and then (with 6 black in bowl 2, which now has 11 balls) is the probability of picking black'""

from bowl 2. This is

T ÒF ∩ F Ó œ T ÒF lF Ó ‚ T ÒF Ó œ Ð ÑÐ Ñ" # # " "' """ # .

In a similar way, the white-white combination has probability .Ð ÑÐ Ñ' """ #

Then . Answer: CT ÒGÓ œ Ð ÑÐ Ñ Ð ÑÐ Ñ œ' " ' " '"" # "" # ""

7. event that second person has different birth month from the first.E œ#

TÐE Ñ œ œ !Þ*"'(Þ#"""#

event that third person has different birth month from first and second.E œ$

Then, the probability that all three have different birthdays is .T ÒE ∩ E Ó œ T ÒE lE Ó † T ÐE Ñ œ Ð ÑÐ Ñ œ !Þ('$*$ # $ # #

"! """# "#

event that fourth person has different birth month from first three.E œ%

Then, the probability that all four have different birthdays is T ÒE ∩ E ∩ E Ó œ T ÒE lE ∩ E Ó † T ÒE ∩ E Ó% $ # % $ # $ #

.œ TÒE lE ∩ E Ó † T ÒE lE Ó † T ÐE Ñ œ Ð ÑÐ ÑÐ Ñ œ !Þ&(#*% $ # $ # #* "! """# "# "#

event that fifth person has different birth month from first four.E œ&

Then, the probability that all five have different birthdays is T ÒE ∩ E ∩ E ∩ E Ó œ T ÒE lE ∩ E ∩ E Ó ‚ T ÒE ∩ E ∩ E Ó& % $ # & % $ # % $ #

œ TÒE lE ∩ E ∩ E Ó ‚ T ÒE lE ∩ E Ó ‚ T ÒE lE Ó ‚ TÐE Ñ& % $ # % $ # $ # #

. œ Ð ÑÐ ÑÐ ÑÐ Ñ œ !Þ$)"*) * "! """# "# "# "#

Answer: D

8. turn left on trial 1, turn right on trial 1, turn left on trial 2 .P" œ V" œ P# œ

We are given that .T ÒP"Ó œ T ÒV"Ó œ !Þ& since form a partition .T ÒP#Ó œ T ÒP# ∩ P"Ó T ÒP# ∩ V"Ó P"ßV" (if the rat turns left on trial 1 then it gets food and has a 0.6 chance of turning left on trialT ÒP#lP"Ó œ !Þ'

2). Then .T ÒP# ∩ P"Ó œ T ÒP#lP"Ó ‚ T ÒP"Ó œ Ð!Þ'ÑÐ!Þ&Ñ œ !Þ$

In a similar way, .T ÒP# ∩ V"Ó œ T ÒP#lV"Ó ‚ T ÒV"Ó œ Ð!Þ)ÑÐ!Þ&Ñ œ !Þ%

Then, . Answer: DT ÒP#Ó œ !Þ$ !Þ% œ !Þ(

SECTION 1 PROBLEM SET STAM-15

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

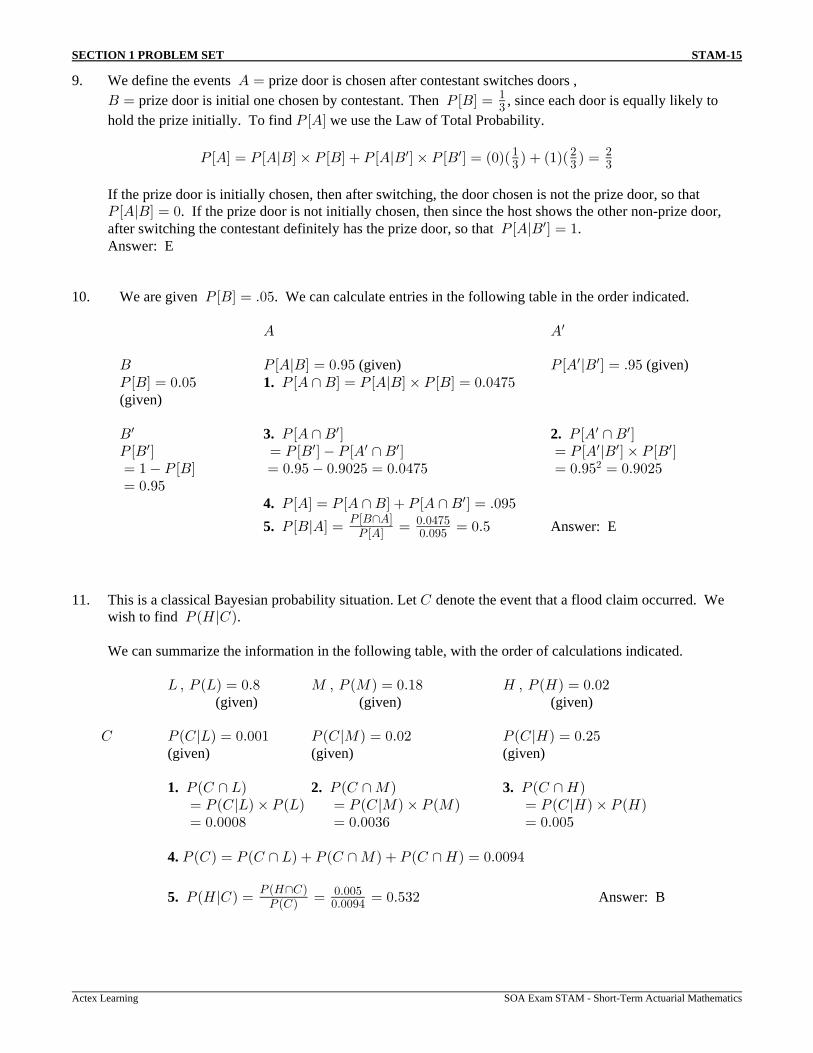

9. We define the events prize door is chosen after contestant switches doors ,E œ

prize door is initial one chosen by contestant. Then , since each door is equally likely toF œ TÒFÓ œ "$

hold the prize initially. To find we use the Law of Total Probability.T ÒEÓ

T ÒEÓ œ T ÒElFÓ ‚ T ÒFÓ T ÒElF Ó ‚ T ÒF Ó œ Ð!ÑÐ Ñ Ð"ÑÐ Ñ œw w " # #$ $ $

If the prize door is initially chosen, then after switching, the door chosen is not the prize door, so thatT ÒElFÓ œ !. If the prize door is not initially chosen, then since the host shows the other non-prize door,after switching the contestant definitely has the prize door, so that .T ÒElF Ó œ "w

Answer: E

10. We are given . We can calculate entries in the following table in the order indicated.T ÒFÓ œ Þ!&

E Ew

(given) (given)F TÒElFÓ œ !Þ*& T ÒE lF Ó œ Þ*&w w

T ÒFÓ œ !Þ!& T ÒE ∩ FÓ œ T ÒElFÓ ‚ T ÒFÓ œ !Þ!%(&1. (given)

F TÒE ∩ F Ó T ÒE ∩ F Ów w w w3. 2. T ÒF Ó œ T ÒF Ó T ÒE ∩ F Ó œ T ÒE lF Ó ‚ T ÒF Ów w w w w w w

œ " T ÒFÓ œ !Þ*& !Þ*!#& œ !Þ!%(& œ !Þ*& œ !Þ*!#&#

œ !Þ*& 4. T ÒEÓ œ T ÒE ∩ FÓ T ÒE ∩ F Ó œ Þ!*&w

5. T ÒFlEÓ œ œ œ !Þ&T ÒF∩EÓT ÒEÓ !Þ!*&

!Þ!%(& Answer: E

11. This is a classical Bayesian probability situation. Let denote the event that a flood claim occurred. WeGwish to find .TÐLlGÑ

We can summarize the information in the following table, with the order of calculations indicated.

P ß T ÐPÑ œ !Þ) Q ß T ÐQÑ œ !Þ") L ß T ÐLÑ œ !Þ!# (given) (given) (given)

G TÐGlPÑ œ !Þ!!" T ÐGlQÑ œ !Þ!# T ÐGlLÑ œ !Þ#& (given) (given) (given)

1. 2. 3.TÐG ∩ PÑ TÐG ∩QÑ TÐG ∩ LÑ œ TÐGlPÑ ‚ TÐPÑ œ TÐGlQÑ ‚ TÐQÑ œ TÐGlLÑ ‚ TÐLÑ œ !Þ!!!) œ !Þ!!$' œ !Þ!!&

4. TÐGÑ œ TÐG ∩ PÑ TÐG ∩QÑ TÐG ∩ LÑ œ !Þ!!*%

5. Answer: BTÐLlGÑ œ œ œ !Þ&$#TÐL∩GÑT ÐGÑ !Þ!!*%

!Þ!!&

STAM-16 SECTION 1 PROBLEM SET

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

12. We identify the following events:

- the applicant is a smoker, - the applicant is a non-smokerW RW œ Ww

- the applicant declares to be a smoker on the applicationHW - the applicant declares to be non-smoker on the application .HR œ HWw

The information we are given is . WeT ÒWÓ œ !Þ$ ß T ÒRWÓ œ !Þ( ß T ÒHRlWÓ œ !Þ% ß T ÒHWlRWÓ œ !

wish to find .T ÒRWlHRÓ œT ÒRW∩HRÓ

T ÒHRÓ

We calculate ,!Þ% œ T ÒHRlWÓ œ œ p T ÒHR ∩ WÓ œ !Þ"#T ÒHR∩WÓ T ÒHR∩WÓ

T ÒWÓ Þ$

and .! œ T ÒHWlRWÓ œ œ p T ÒHW ∩ RWÓ œ !T ÒHW∩RWÓ T ÒHW∩RWÓ

T ÒRWÓ Þ(

Using the rule , and noting that and T ÒEÓ œ T ÒE ∩ FÓ T ÒE ∩ F Ó HW œ HR W œ RWw w w

we have

, andT ÒHW ∩ WÓ œ T ÒWÓ T ÒHR ∩ WÓ œ !Þ$ !Þ"# œ !Þ") , andT ÒHR ∩RWÓ œ T ÒRWÓ T ÒHW ∩ RWÓ œ !Þ( ! œ !Þ( .T ÒHRÓ œ T ÒHR ∩RWÓ T ÒHR ∩ WÓ œ !Þ( !Þ"# œ !Þ)#

Then, . T ÒRWlHRÓ œ œ œTÒRW∩HRÓ

T ÒHRÓ !Þ)# %"!Þ( $&

These calculations can be summarized in the order indicated in the following table.

TÐWÑ ß !Þ$ Ê TÐRWÑ œ " TÐWÑ œ !Þ(1. given Ì

6. 5. 2. HW É TÐHW ∩ WÑ T ÐHWlRWÑ œ ! , given TÐHWÑ œ TÐWÑ TÐHR ∩ WÑ TÐHW ∩ RWÑ œ TÐHW ∩ WÑ œ !Þ$ !Þ"# œ !Þ") œ TÐHWlRWÑ ‚ TÐRWÑ TÐHW ∩ RWÑ œ Ð!ÑÐ!Þ(Ñ œ ! œ !Þ") ! œ !Þ") Ì Ë

7. 4. 3. HR TÐHRlWÑ œ !Þ% T ÐHR ∩RWÑ œ given TÐHRÑ œ TÐRWÑ TÐHW ∩ RWÑ œ " TÐHWÑ TÐHR ∩ WÑ œ !Þ( ! œ !Þ( œ " !Þ") œ TÐHRlWÑ † T ÐWÑ œ !Þ)# œ Ð!Þ%ÑÐ!Þ$Ñ œ Þ"#

Then,

8. Answer: DT ÒRWlHRÓ œ œ œTÒRW∩HRÓ

T ÒHRÓ !Þ)# %"!Þ( $&

SECTION 1 PROBLEM SET STAM-17

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

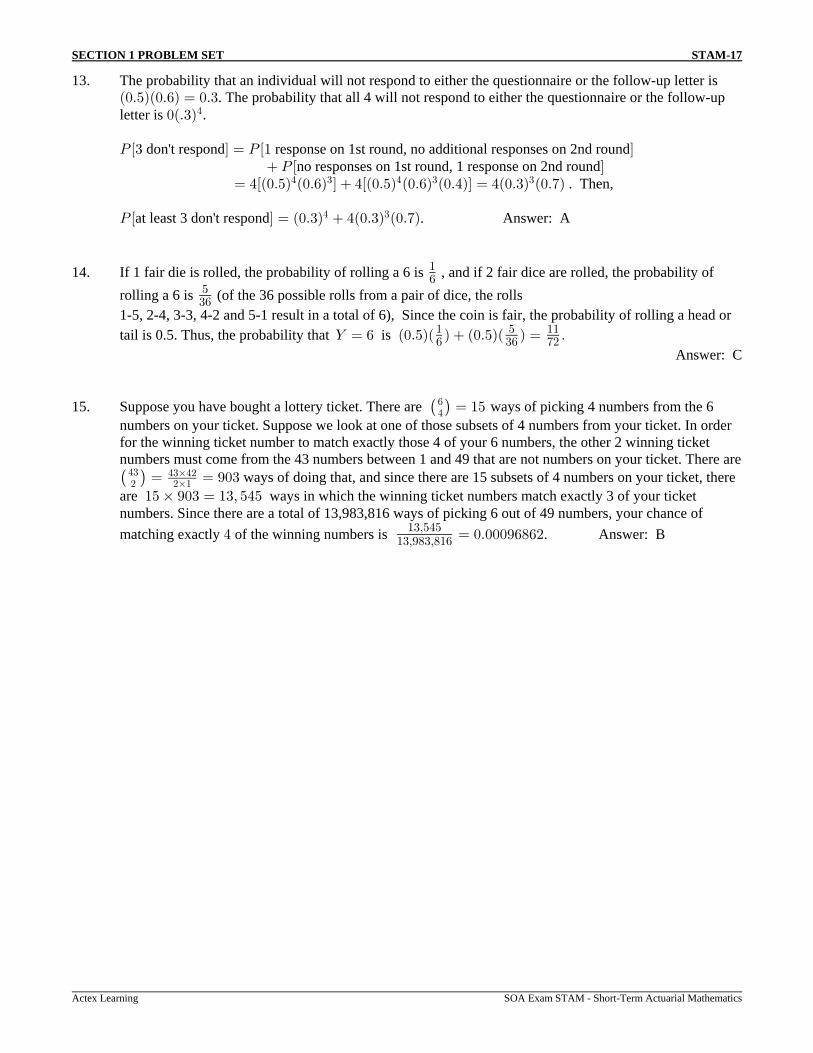

13. The probability that an individual will not respond to either the questionnaire or the follow-up letter isÐ!Þ&ÑÐ!Þ'Ñ œ !Þ$. The probability that all 4 will not respond to either the questionnaire or the follow-upletter is .!ÐÞ$Ñ%

don't respond response on 1st round, no additional responses on 2nd roundT Ò$ Ó œ T Ò" Ó no responses on 1st round, 1 response on 2nd round TÒ Ó . Then,œ %ÒÐ!Þ&Ñ Ð!Þ'Ñ Ó %ÒÐ!Þ&Ñ Ð!Þ'Ñ Ð!Þ%ÑÓ œ %Ð!Þ$Ñ Ð!Þ(Ñ% $ % $ $

at least 3 don't respond . Answer: AT Ò Ó œ Ð!Þ$Ñ %Ð!Þ$Ñ Ð!Þ(Ñ% $

14. If 1 fair die is rolled, the probability of rolling a 6 is , and if 2 fair dice are rolled, the probability of"'

rolling a 6 is (of the 36 possible rolls from a pair of dice, the rolls&$'

1-5, 2-4, 3-3, 4-2 and 5-1 result in a total of 6), Since the coin is fair, the probability of rolling a head ortail is 0.5. Thus, the probability that is ] œ ' Ð!Þ&ÑÐ Ñ Ð!Þ&ÑÐ Ñ œ Þ" & ""

' $' (#Answer: C

15. Suppose you have bought a lottery ticket. There are ways of picking 4 numbers from the 6 '% œ "&

numbers on your ticket. Suppose we look at one of those subsets of 4 numbers from your ticket. In orderfor the winning ticket number to match exactly those 4 of your 6 numbers, the other 2 winning ticketnumbers must come from the 43 numbers between 1 and 49 that are not numbers on your ticket. There are %$

# #‚"%$‚%#œ œ *!$ ways of doing that, and since there are 15 subsets of 4 numbers on your ticket, there

are ways in which the winning ticket numbers match exactly 3 of your ticket"& ‚ *!$ œ "$ß &%&numbers. Since there are a total of 13,983,816 ways of picking 6 out of 49 numbers, your chance of

matching exactly of the winning numbers is . Answer: B% œ !Þ!!!*')'#"$ß&%&

"$ß*)$ß)"'

STAM-18 SECTION 1 PROBLEM SET

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I STAM-19

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES IProbability, Density and Distribution Functions

This section relates to Chapter 2 of "Loss Models". The suggested time frame for covering this section is twohours. A brief review of some basic calculus relationships is presented first.

2.1 Calculus Review

Natural logarithm and exponential functions68ÐBÑ œ 691ÐBÑ / is the logarithm to the base ;

68Ð/Ñ œ " ß 68Ð"Ñ œ !ß / œ " ß!

68Ð/ Ñ œ C ß / œ Bß 68Ð+ Ñ œ C ‚ 68Ð+Ñ ßC 68ÐBÑ C

68ÐC † DÑ œ 68ÐCÑ 68ÐDÑß 68Ð Ñ œ 68ÐCÑ 68ÐDÑ ßCD

(2.1)/ / œ / ß Ð/ Ñ œ /B D BD B A BA

Differentiation

For the function 0ÐBÑß 0 ÐBÑ œ œw

2Ä!

.0

.B 20ÐB2Ñ0ÐBÑ

lim (2.2)

Product rule: (2.3)..B

w wÒ1ÐBÑ2ÐBÑÓ œ 1 ÐBÑ2ÐBÑ 1ÐBÑ2 ÐBÑ

Quotient rule: (2.4)..B 2ÐBÑ Ò2ÐBÑÓ

1ÐBÑ 2ÐBÑ1 ÐBÑ1ÐBÑ2 ÐBÑÒ Ó œw w

#

Chain rule: (2.5) . . ..B 1ÐBÑ .B .B

1 ÐBÑ68Ò1ÐBÑÓ œ ß Ò1ÐBÑÓ œ 8Ò1ÐBÑÓ ‚ 1 ÐBÑ ß + œ + ‚ 68Ð+Ñ

w8 8" w B B

Integration

B .B œ - ß + .B œ - ß .B œ 68Ò+ ,BÓ -8 BB + " "8" 68Ð+Ñ +,B ,

8" B

‚ (2.6)

Integration by parts : + +

, ,?Ð>Ñ .@Ð>Ñ œ ?Ð,Ñ@Ð,Ñ ?Ð+Ñ@Ð+Ñ @Ð>Ñ .?Ð>Ñ

for definite integrals, and ? .@ œ ?@ @ .?

for indefinite integrals (this is derived by integrating both sides of the product rule); note that

and .@Ð>Ñ œ @ Ð>Ñ .> .?Ð>Ñ œ ? Ð>Ñ .>w w

. ..B .B

+ BB ,1Ð>Ñ .> œ 1ÐBÑ ß 1Ð>Ñ .> œ 1ÐBÑ (2.7)

..B

2ÐBÑ4ÐBÑ w w1Ð>Ñ.> œ 1Ð4ÐBÑÑ ‚ 4 ÐBÑ 1Ð2ÐBÑÑ ‚ 2 ÐBÑ (2.8)

if and is an integer (2.9)!∞ 8 5BB / .B œ 5 ! 8 !8x

58"

STAM-20 SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

The word "model" used in the context of a loss model, usually refers to the distribution of a loss random variable.Random variables are the basic components used in actuarial modeling. In this section we review the definitionsand illustrate the variety of random variables that we will encounter in the STAM Exam material.

A random variable is a numerical quantity that is related to the outcome of some random experiment on aprobability space. For the most part, the random variables we will encounter are the numerical outcomes of someloss related event such as the dollar amount of claims in one year from an auto insurance policy, or the number oftornados that touch down in Kansas in a one year period.

2.2 Discrete Random VariableThe random variable is discrete and is said to have a if it can take on values only from a\ discrete distributionfinite or countable infinite sequence (usually the integers or some subset of the integers). As an example, considerthe following two random variables related to successive tosses of a coin:

\ œ " \ œ ! if the first head occurs on an even-numbered toss, if the first head occurs on an odd-numberedtoss;

] œ 8 8, where is the number of the toss on which the first head occurs.

Both and are discrete random variables, where can take on only the values or , and can take on any\ ] \ ! " ]positive integer value.

Probability function of a discrete random variableThe probability function (pf) of a discrete random variable is usually denoted or , and is equal to:ÐBÑ Ð 0ÐBÑÑT Ð\ œ BÑ. As its name suggests, the probability function describes the probability of individual outcomesoccurring.

The probability function must satisfy the following two conditions:

(i) for all , and (ii) (2.10)! Ÿ :ÐBÑ Ÿ " B :ÐBÑ œ "B

For the random variable above, the probability function is \ :Ð!Ñ œ ß :Ð"Ñ œ# "$ $ ,

and for it is for .] :Ð5Ñ œ 5 œ "ß #ß $ß ÞÞÞ"#5

An event is a subset of the set of all possible outcomes of , and the probability of event occurring isE \ E

TÒEÓ œ :ÐBÑB−E

.

For above, is even ,] T Ò] Ó œ T Ò] œ #ß %ß 'ß ÞÞÞÓ œ â œ" " " "# # $## '%

and this is also equal to .TÐ\ œ "Ñ

SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I STAM-21

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

2.3 Continuous Random VariableA continuous random variable usually can assume numerical values from an interval of real numbers, perhaps theentire set of real numbers. As an example, the length of time between successive streetcar arrivals at a particular(in service) streetcar stop could be regarded as a continuous random variable (assuming that time measurementcan be made perfectly accurate).

Probability density functionA continuous random variable has a probability density function (pdf) denoted or (or sometimes\ 0ÐBÑ 0 ÐBÑ\

denoted ), which is a continuous function (except possibly at a finite or countably infinite number of points).:ÐBÑFor a continuous random variable, we do not describe probability at single points. We describe probability interms of intervals. In the streetcar example, we would not define the probability that the next street car will arrivein exactly 1.23 minutes, but rather we would define a probability such as the probability that the streetcar willarrive between 1 and 1.5 minutes from now.

Probabilities related to are found by integrating the density function over an interval.\

TÒ\ − Ð+ß ,ÑÓ œ T Ò+ \ ,Ó 0ÐBÑ .B is defined to be equal to .+

,

A pdf must satisfy (i) for all , and (ii) (2.11)0ÐBÑ 0ÐBÑ ! B 0ÐBÑ .B œ "∞

∞

Often, the region of non-zero density is a finite interval, and outside that interval. If is continuous0ÐBÑ œ ! 0ÐBÑexcept at a finite number of points, then probabilities are defined and calculated as if was continuous0ÐBÑeverywhere (the discontinuities are ignored).

For example, suppose that has density function .\ 0ÐBÑ œ #B !B"

!

for

, elsewhere

Then satisfies the requirements for a density function, since .0 0ÐBÑ .B œ #B .B œ " ∞ !

∞ "

Then, for example . This is illustrated in the shaded are in the graphT ÒÞ& \ "Ó œ #B .B œ B œ !Þ(& !Þ&

" #

!Þ&

"

below.

2

1

( ) 2f x x

0.5 1x

1.5

For a continuous random variable ,\

TÒ+ \ ,Ó œ T Ò+ Ÿ \ ,Ó œ T Ò+ \ Ÿ ,Ó œ T Ò+ Ÿ \ Ÿ ,Ó,

so that when calculating the probability for a continuous random variable on an interval, it is irrelevant whether ornot the endpoints are included. For a continuous random variable, for any point ; non-zeroT Ò\ œ +Ó œ ! +probabilities only exist over an interval, not at a single point.

STAM-22 SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

2.4 Mixed DistributionA random variable may have some points with non-zero and with a continuous pdf elsewhere.probability massSuch a distribution may be referred to as a mixed distribution, but the general notion of mixtures of distributionswill be covered later. The sum of the probabilities at the discrete points of probability plus the integral of thedensity function on the continuous region for must be 1. For example, suppose that has probability of at\ \ !Þ&\ œ ! \ Ð!ß "Ñ 0ÐBÑ œ B, and is a continuous random variable on the interval with density function for! B " \, and has no density or probability elsewhere. This satisfies the requirements for a random variablesince the total probability is

T Ò\ œ !Ó 0ÐBÑ .B œ !Þ& B .B œ !Þ& !Þ& œ " ! !" " .

Then,T Ò! \ !Þ&Ó œ B .B œ !Þ"#&ß

!Þ&

andT Ò! Ÿ \ !Þ&Ó œ T Ò\ œ !Ó T Ò! \ !Þ&Ó œ !Þ& !Þ"#& œ !Þ'#&.

Notice that for this random variable because there is a probability mass atT Ò! \ !Þ&Ó Á T Ò! Ÿ \ !Þ&Ó\ œ !.

2.5 Cumulative Distribution Function, Survival Function and Hazard FunctionGiven a random variable , the cumulative distribution function of (also called the , or\ \ distribution functioncdf) is (also denoted ).JÐBÑ œ T Ò\ Ÿ BÓ J ÐBÑ\

The cdf is the "left-tail" probability, or the probability to the left of .JÐBÑ Band including

The survival function is the complement of the distribution function,

(2.12)WÐBÑ œ " JÐBÑ œ T Ò\ BÓ

The event is referred to as a "tail" or right tail of the distribution.\ B

For any cdf . (2.13)T Ò+ \ Ÿ ,Ó œ JÐ,Ñ JÐ+Ñß J ÐBÑ œ "ß J ÐBÑ œ !lim limBÄ∞ BÄ∞

For a discrete random variable with probability function , , and:ÐBÑ J ÐBÑ œ :ÐAÑAŸB

in this case is a "step function" (see Example 2-1 below); it has a jump (or step increase) at each point thatJÐBÑhas non-zero probability, while remaining constant until the next jump. Note that for a discrete random variable,JÐBÑ B B includes the probability at the point as well as the total probabilities of all the points to the left of .

If has a continuous distribution with density function , then\ 0ÐBÑ

and (2.14)JÐBÑ œ TÐ\ Ÿ BÑ œ 0Ð>Ñ .> WÐBÑ œ TÐ\ BÑ œ 0Ð>Ñ .> ∞ B

B ∞

and is a continuous, differentiable, non-decreasing function such thatJÐBÑ

..B J ÐBÑ œ J ÐBÑ œ W ÐBÑ œ 0ÐBÑw w .

Also, for a continuous random variable, the or ishazard rate failure rate

(2.15)2ÐBÑ œ œ œ 68WÐBÑ0 ÐBÑ 0 ÐBÑ

"JÐBÑ WÐBÑ .B.

If is continuous and , then the survival function satisfies and \ \ ! WÐ!Ñ œ " WÐBÑ œ / Þ 2Ð>Ñ .>!B

The iscumulative hazard function (2.16)LÐBÑ œ 2Ð>Ñ .>

!B

SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I STAM-23

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

If has a mixed distribution with some discrete points and some continuous regions, then is continuous\ JÐBÑexcept at the points of non-zero probability mass, where will have a jump.JÐBÑ

The region of positive probability of a random variable is called the of the random variable.support

2.6 Examples of Distribution FunctionsThe following examples illustrate the variety of distribution functions that can arise from random variables. The supportof a random variable is the set of points over which there is positive probability or density.

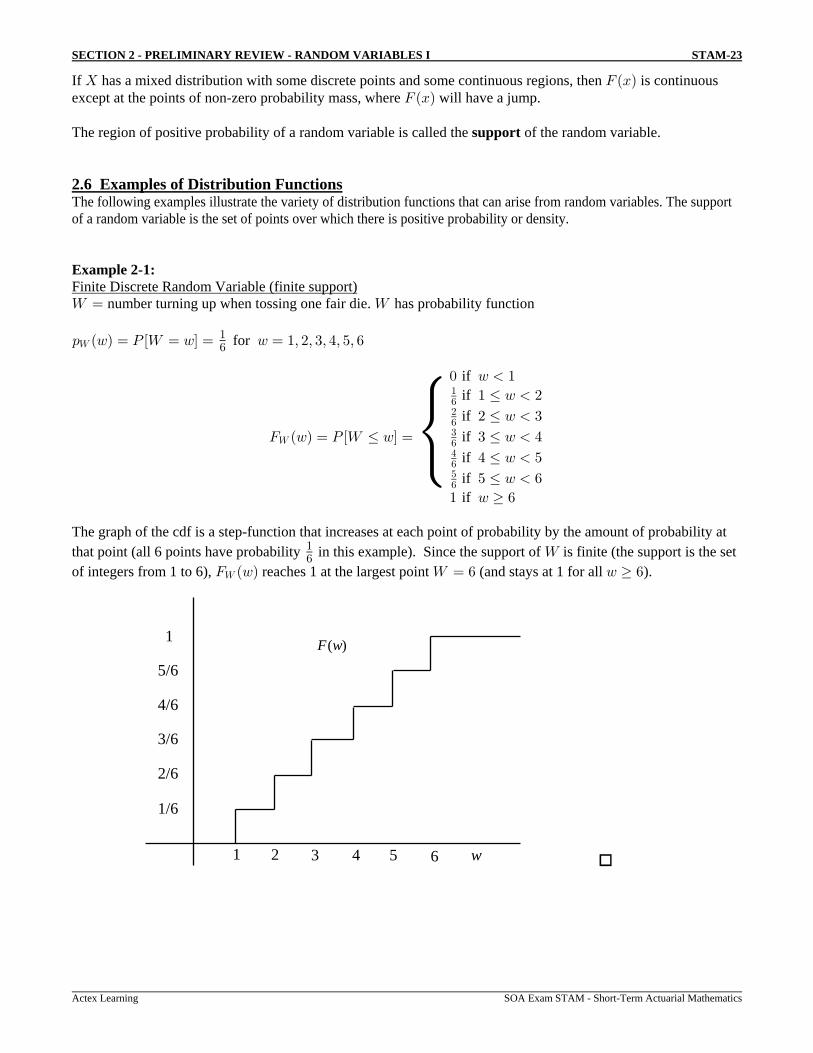

Example 2-1:Finite Discrete Random Variable (finite support)[ œ [number turning up when tossing one fair die. has probability function

: ÐAÑ œ T Ò[ œ AÓ œ A œ "ß #ß $ß %ß &ß '["' for

J ÐAÑ œ T Ò[ Ÿ AÓ œ

! A "

" Ÿ A #

# Ÿ A $

$ Ÿ A %

% Ÿ A &

& Ÿ A '

" A '

[

"'#'$'%'&'

if

if

if

if

if

if if

The graph of the cdf is a step-function that increases at each point of probability by the amount of probability atthat point (all 6 points have probability in this example). Since the support of is finite (the support is the set"

' [

of integers from 1 to 6), reaches 1 at the largest point (and stays at 1 for all ).J ÐAÑ [ œ ' A '[

1

5/6

4/6

3/6

2/6

1/6

1 2 3 4 5

( )F w

6 w

STAM-24 SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

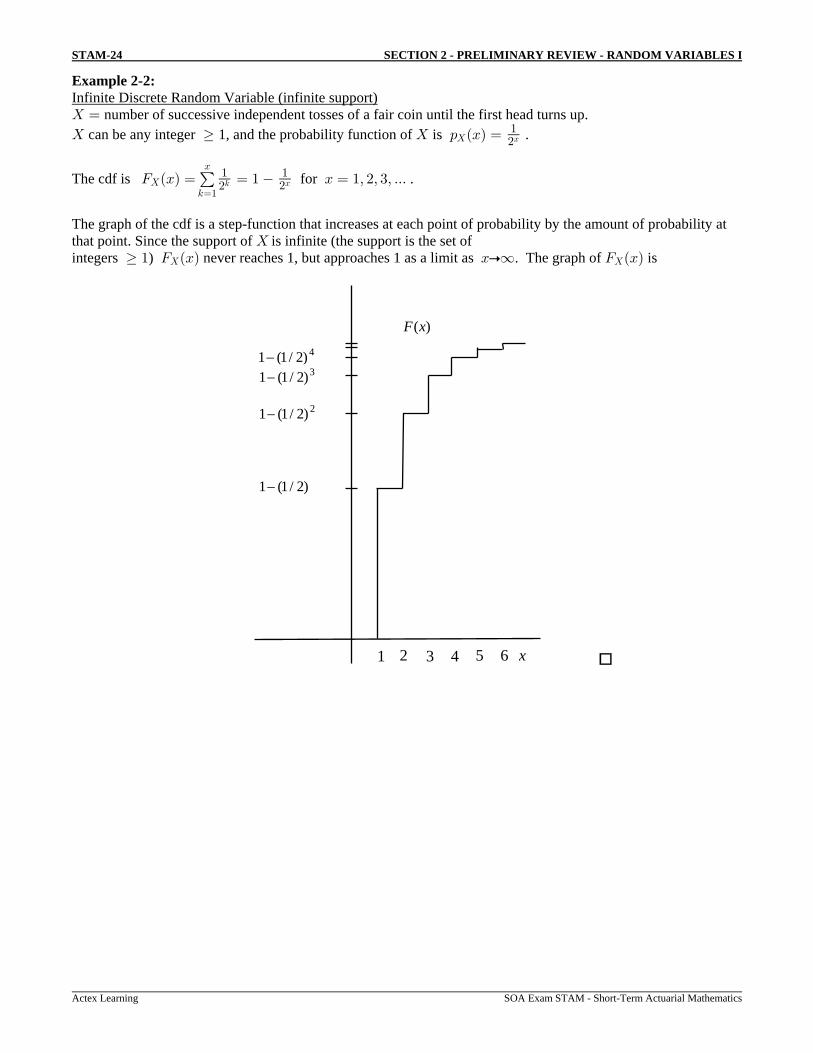

Example 2-2:Infinite Discrete Random Variable (infinite support)\ œ number of successive independent tosses of a fair coin until the first head turns up.\ \ : ÐBÑ œ can be any integer 1, and the probability function of is .\

"#B

The cdf is for .J ÐBÑ œ œ " B œ "ß #ß $ß ÞÞÞ\5œ"

B " "# #5 B

The graph of the cdf is a step-function that increases at each point of probability by the amount of probability atthat point. Since the support of is infinite (the support is the set of\integers ) never reaches 1, but approaches 1 as a limit as . The graph of is " J ÐBÑ Bp∞ J ÐBÑ\ \

( )F x

1 2 3 4 5 6 x

41 (1/ 2) 31 (1/ 2)

21 (1/ 2)

1 (1/ 2)

SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I STAM-25

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

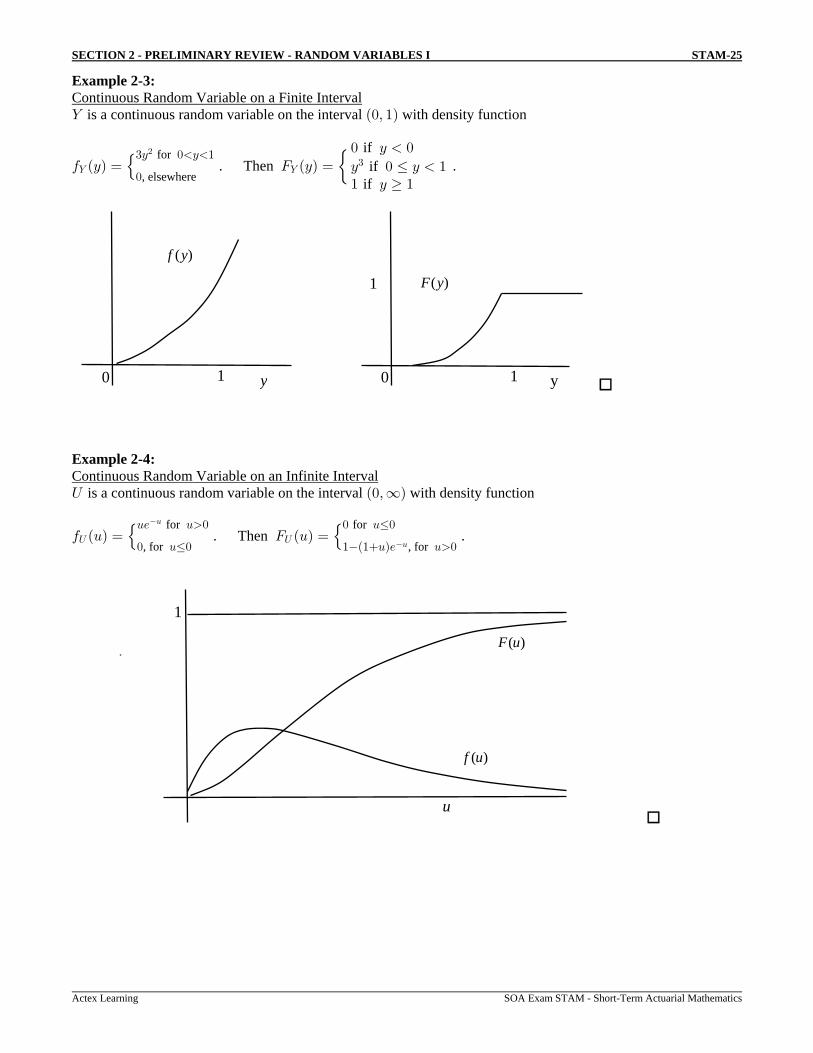

Example 2-3:Continuous Random Variable on a Finite Interval] Ð!ß "Ñ is a continuous random variable on the interval with density function

0 ÐCÑ œ J ÐCÑ œ

! C !

C ! Ÿ C "" C "

] ]$ $C !C"

!

# for

, elsewhere . Then .

if if

if

( )f y

y 1 0

( )F y

y10

1

Example 2-4:Continuous Random Variable on an Infinite IntervalY Ð!ß∞Ñ is a continuous random variable on the interval with density function

0 Ð?Ñ œ J Ð?Ñ œY Y ?/ ?! ! ?Ÿ!

! ?Ÿ! "Ð"?Ñ/ ?!

?

?

for for

, for , for . Then .

1

( )F u

( )f u

u

STAM-26 SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

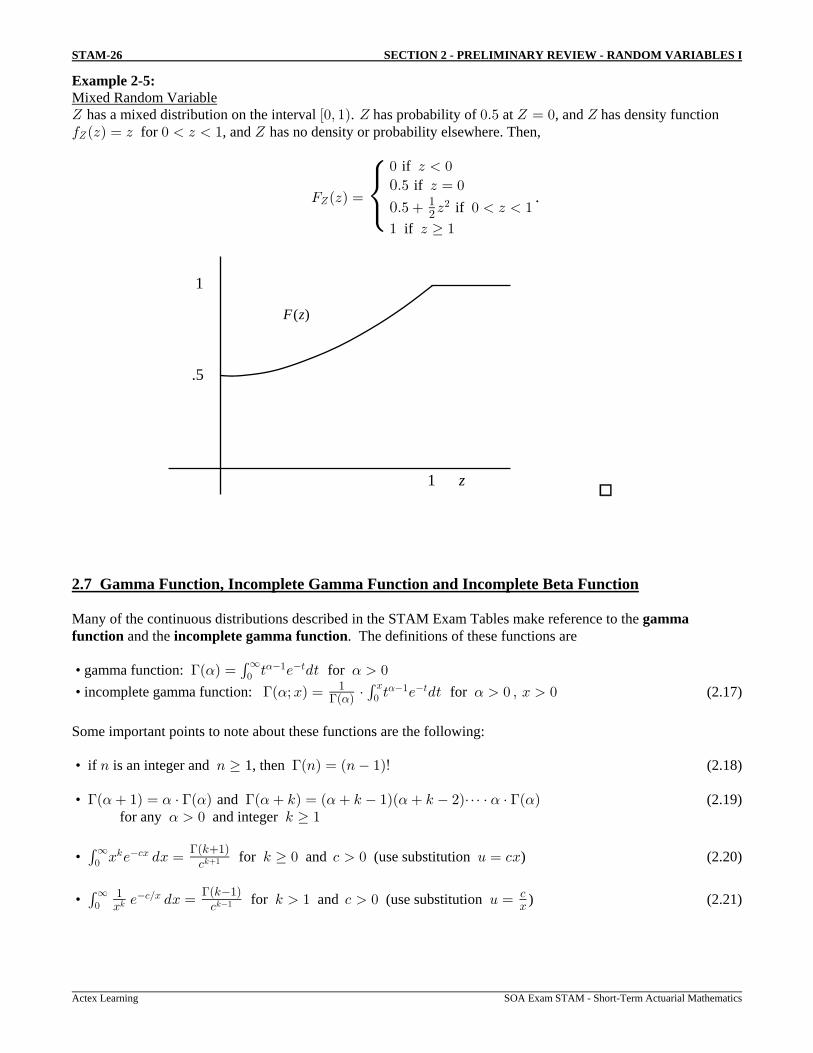

Example 2-5:Mixed Random Variable^ Ò!ß "Ñ ^ !Þ& ^ œ ! ^ has a mixed distribution on the interval . has probability of at , and has density function0 ÐDÑ œ D ! D " ^^ for , and has no density or probability elsewhere. Then,

if if

if

if

J ÐDÑ œ

! D !

Þ& D œ !

Þ& D ! D "

" D "

^ # !

! "#

.

1

.5

( )F z

1 z

2.7 Gamma Function, Incomplete Gamma Function and Incomplete Beta Function

Many of the continuous distributions described in the STAM Exam Tables make reference to the gammafunction incomplete gamma function and the . The definitions of these functions are

• gamma function: for > α αÐ Ñ œ > / .> !!

∞ " >α

• incomplete gamma function: for (2.17)> α αÐ à BÑ œ † > / .> ! ß B !"Ð Ñ> α

!B " >α

Some important points to note about these functions are the following:

• if is an integer and 1, then (2.18)8 8 Ð8Ñ œ Ð8 "Ñx>

• and (2.19)> α α > α > α α α α > αÐ "Ñ œ † Ð Ñ Ð 5Ñ œ Ð 5 "ÑÐ 5 #Ñâ † † Ð Ñ for any and integer α ! 5 "

• for and (use substitution ) (2.20)!

∞ 5 -BB / .B œ 5 ! - ! ? œ -B>Ð5"Ñ-5"

• for and (use substitution ) (2.21)!

∞ -ÎB" -B -

Ð5"ÑB5 5"/ .B œ 5 " - ! ? œ

>

SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I STAM-27

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Some of the table distributions make reference to the , which is defined as follows:incomplete beta function

for , (2.22)"Ð+ß ,à BÑ œ > Ð" >Ñ .> ! Ÿ B Ÿ " +ß , !>> >

Ð+,ÑÐ+Ñ Ð,Ñ

!B +" ,"

References to the gamma function have been rare and the incomplete functions have not been referred to on the

released exams. It is useful to remember the integral relationship !∞ 5 -BB / .B œ>Ð5"Ñ-5" , particularly in the case

in which is a non-negative integer.5

In that case, we get , which can occasionally simplify integral relationships. This!

∞ 5 -BB / .B œ 5x-5"

relationship is embedded in the definition of the gamma distribution in the STAM Exam Table.

The pdf of the gamma distribution with parameters and is , defined on the interval .α ) 0Ð>Ñ œ > !> /Ð Ñ

α )

α

" >Î

) > α

This means that , which can be reformulated as If we let ! !∞ ∞ " >Î> /

Ð Ñ

α )

α

" >Î

) > α .> œ " > / .B œ Ð ÑÞα ) α) > α

) αœ 5 œ ""- and , we get the relationship

(2.23)!

∞ 5 -BB / .B œ>Ð5"Ñ-5"

Looking at the various continuous distributions in the STAM Exam Table gives some hints at calculating anumber of integral forms. For instance, the pdf of the beta distribution with parameters is+ß ,ß œ ")

0ÐBÑ œ ‚ B Ð" BÑ ! B ">> >

Ð+,ÑÐ+Ñ Ð,Ñ

+" ," for .

Therefore, , from which we get!

" +" ,>> >

Ð+,ÑÐ+Ñ Ð,Ñ ‚ B Ð" BÑ .B œ "

!

" +" ,"B Ð" BÑ .B œ> >>Ð+Ñ Ð,ÑÐ+,Ñ .

STAM-28 SECTION 2 - PRELIMINARY REVIEW - RANDOM VARIABLES I

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 2 PROBLEM SET STAM-29

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 2 PROBLEM SETPreliminary Review - Random Variables I

1. Let be a discrete random variable with probability function\

for What is the probability that is even?T Ò\ œ BÓ œ B œ "ß #ß $ß ÞÞÞ \#$B

A) B) C) D) E)" # " # $% ( $ $ %

2. For a certain discrete random variable on the non-negative integers, the probability function satisfies therelationships

and for Find .TÐ!Ñ œ TÐ"Ñ T Ð5 "Ñ œ † T Ð5Ñ 5 œ "ß #ß $ß ÞÞÞ T Ð!Ñ"5

A) B) C) D) E) 68 / / " Ð/ "Ñ / Ð/ "Ñ" " "

3. Let be a continuous random variable with density function\

. Calculate .0ÐBÑ œ T Ò l\ l Ó 'BÐ"BÑ !B"

!

" "# %

for

otherwise A) B) C) D) E) !Þ!&#" !Þ"&'$ !Þ$"#& !Þ&!!! !Þ)!!!

4. Let be a random variable with distribution function\

. Calculate .

for for

for

for for

JÐBÑ œ T Ò" Ÿ \ Ÿ #Ó

! B !! Ÿ B "

" Ÿ B #

# Ÿ B $

" B $

B)" B% )$ B% "#

A) B) C) D) E) " $ ( "$ "*) ) "' #% #%

5. Let and be three independent continuous random variables each with density function\ ß \ \" # $

0ÐBÑ œ #B !B #

!

for

otherwise .

What is the probability that exactly 2 of the 3 random variables exceeds 1?

A) B) C) $# # $ # # $Ð # "ÑÐ# #Ñ #

D) E) Ð #Ñ Ð # Ñ $Ð #Ñ Ð # Ñ$ " $ "# # # #

# #

6. Let and be three independent, identically distributed random variables each with density\ ß \ \" # $

function . Let . Find .0ÐBÑ œ ] œ 7+BÖ\ ß\ ß\ × T Ò] Ó $B !ŸBŸ"

!

"#

# for

otherwise" # $

A) B) C) D) E) " $( $%$ ( &""'% '% &"# ) &"#

7. Let the distribution function of for be .\ B ! JÐBÑ œ " 5œ!

$B /5x

5 B

What is the density function of for ?\ B !

A) B) C) D) E)/ / /B B B B / B / B / B /# ' ' '

# B $ B $ B $ B

STAM-30 SECTION 2 PROBLEM SET

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

8. Let have the density function for , and , otherwise.\ 0ÐBÑ œ ! B 0ÐBÑ œ !$B#

$) )

If , find the value of .T Ò\ "Ó œ () )

A) B) C) D) E) " ( )# ) (

"Î$ "Î$ "Î$Ð Ñ Ð Ñ # #

9. A large wooden floor is laid with strips 2 inches wide and with negligible space between strips. A uniformcircular disk of diameter 2.25 inches is dropped at random on the floor. What is the probability that the disktouches three of the wooden strips?

A) B) C) D) E) " " " " "% )1 1 1 #

10. If has a continuous uniform distribution on the interval from 0 to 10, then what is ?\ TÒ\ (Ó"!\

A) B) C) D) E) $ $" " $* ("! (! # (! "!

11. For a loss distribution where , you are given:B #

i) The hazard rate function: , for 2ÐBÑ œ B #D#B

#

ii) A value of the distribution function: JÐ&Ñ œ !Þ)% Calculate .D A) 2 B) 3 C) 4 D) 5 E) 6

SECTION 2 PROBLEM SET STAM-31

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 2 PROBLEM SET SOLUTIONS

1. is even . T Ò\ Ó œ T Ò\ œ #Ó T Ò\ œ %Ó T Ò\ œ 'Ó â œ † Ò âÓ œ † œ# " " " # " "$ $ $ $ $ %"$ & # "

$#

Answer: A

2. , . . . .TÐ#Ñ œ TÐ"Ñ œ TÐ!Ñ ß T Ð$Ñ œ † T Ð#Ñ œ † T Ð!Ñ T Ð5Ñ œ † T Ð!Ñ" " "# #x Ð5"Ñx

The probability function must satisfy the requirement so that3œ!

∞

TÐ3Ñ œ "

TÐ!Ñ † T Ð!Ñ œ TÐ!ÑÐ" /Ñ œ "3œ"

∞"

Ð3"Ñx

(this uses the series expansion for at ). Then, . Answer: C/ B œ " TÐ!Ñ œB "/"

3. T Ò \ Ÿ Ó œ T Ò Ÿ \ Ÿ Ó œ T Ò Ÿ \ Ÿ Ó œ 'BÐ" BÑ .B " " " " " " $# % % # % % % "Î%

$Î%

. Answer: Cœ Þ')(& p T Ò \ Ó œ " T Ò \ Ó œ !Þ$"#& " " " "# % # %

4. Answer: ET Ò" Ÿ \ Ÿ #Ó œ T Ò\ Ÿ #Ó T Ò\ "Ó œ JÐ#Ñ JÐBÑ œ œ ÞlimBÄ"

"" " "*"# ) #%

5. .T Ò\ Ÿ "Ó œ Ð # BÑ .B œ # ß T Ò\ "Ó œ " T Ò\ Ÿ "Ó œ # !

" " $# #

With 3 independent random variables, and , there are 3 ways in which exactly 2 of the 's\ ß \ \ \" # $ 3

exceed 1 (either or or ).\ ß\ \ ß\ \ ß\" # " $ # $

Each way has probability ÐT Ò\ "ÓÑ † T Ò\ Ÿ "Ó œ Ð #Ñ Ð # Ñ# #$ "# #

for a total probability of . Answer: E$ † Ð #Ñ Ð # Ñ$ "

# # #

6. T Ò] Ó œ " T Ò] Ÿ Ó œ " T ÒÐ\ Ÿ Ñ ∩ Ð\ Ÿ Ñ ∩ Ð\ Ÿ ÑÓ" " " " "# # # # #" # $

Answer: Eœ " ÐT Ò\ Ÿ ÓÑ œ " Ò $B .BÓ œ " Ð Ñ œ Þ" " &""# ) &"#

$ # $ $!"Î#

7. 0ÐBÑ œ J ÐBÑ œ œ / †w B

5œ! 5œ!

$ $ 5B / B / B 5B5x 5x

5" B 5 B 5 5"

Answer: Cœ / † Ò" Ó œ ÞB B" B #B B $B / B" # ' '

# $ # B $

8. Since if , and since , we must conclude that .0ÐBÑ œ ! B T Ò\ "Ó œ ") )()

Then, , or equivalently, . Answer: ET Ò\ "Ó œ 0ÐBÑ .B œ .B œ " œ œ # " ") ) $B " (

)

#

$ $) ) )

STAM-32 SECTION 2 PROBLEM SET

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

9. Let us focus on the left-most point on the disk. Consider two adjacent strips on the floor. Let the interval:Ò!ß #Ó : ! "Þ(& represent the distance as we move across the left strip from left to right. If is between and ,then the disk lies within the two strips.

If is between and , the disk will lie on 3 strips (the first two and the next one to the right). Since: "Þ(& #any point between and is equally likely as the left most point on the disk (i.e. uniformly distributed! # :

between and ) it follows that the probability that the disk will touch three strips is .! # œ !Þ#& "# )

Answer: D

10. Since the density function for is for , we can regard as being positive. Then\ 0ÐBÑ œ ! B "! \""!

T Ò\ (Ó œ T Ò\ (\ "! !Ó œ T ÒÐ\ &ÑÐ\ #Ñ !Ó"!\

#

œ TÒ\ &Ó T Ò\ #Ó

(since if either both Ð> &ÑÐ> #Ñ ! > &ß > # !

or both ) . Answer: E> &ß > # ! œ œ& # ("! "! "!

11. The survival function for a random variable can be formulated in terms of the hazard rate function:WÐCÑWÐCÑ œ /B:Ò 2ÐBÑ .BÓ

∞

C .

In this question, .WÐ&Ñ œ " JÐ&Ñ œ !Þ"' œ /B:Ò .BÓ œ /B:Ò 68Ð ÑÓ#

& D D &#B # #

# #

Taking natural log of both sides of the equation results in , and solving for 68Ð Ñ œ 68Ð!Þ"'Ñ DD &# #

#

results in . Answer: AD œ #

SECTION 3 - PRELIMINARY REVIEW - RANDOM VARIABLES II STAM-33

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

SECTION 3 - PRELIMINARY REVIEW - RANDOM VARIABLES II

This section relates to Sections 3.1 - 3.3 of "Loss Models". The mean and variance of a random variable are twofundamental distribution parameters. In this section we review those and some other important distribution parameters.Chapter 3 of Loss models also introduces deductibles and policy limits. These topics will be considered in detail later inthe study guide.

The suggested time frame for this section is 2 hours.

3.1 Expected Value and Other Moments of a Random VariableFor a random variable , the expected value is denoted , or or . The expected value of is also\ IÒ\Ó \. .\

called the , or the . The expected value is the "average" over the range of values thatexpectation of mean of \ \\ can be, or the "center" of the distribution.

For a discrete random variable, the expected value of is (3.1)\ all B

B ‚ :ÐBÑ

where the sum is taken over all points at which has non-zero probability. For instance, if is the result ofB \ \

one toss of a fair die, then IÒ\Ó œ " ‚ # ‚ â ' ‚ œ Þ" " " (' ' ' #

For a continuous random variable, the expected value is

∞

∞B 0ÐBÑ .B‚ (3.2)

Although the integral is written with lower limit and upper limit , the interval of integration is the interval∞ ∞of support (non-zero-density) for . For instance, if for , then the mean is\ 0ÐBÑ œ #B ! B "

IÒ\Ó œ B ‚ #B .B œ!

" #$ .

If is a function, then is equal to if is a discrete random variable, and it is equal to2 IÒ2Ð\ÑÓ 2ÐBÑ ‚ :ÐBÑ \B

∞

∞2ÐBÑ ‚ 0ÐBÑ .B \ IÒ2Ð\ÑÓ 2Ð\Ñ if is a continuous random variable. is the "average" value of based on the

possible outcomes of random variable .\

The mean of a random variable might not exist\ , it might be or . For example, the continuous∞ ∞random variable with\

pdf has expected value .0ÐBÑ œ B ‚ .B œ ∞ "B#

#

for

, otherwise

B "

!

"B "

∞

For any constants and and functions and ,+ ß + , 2 2" # " #

(3.3)IÒ+ 2 Ð\Ñ + 2 Ð\Ñ ,Ó œ + IÒ2 Ð\ÑÓ + IÒ2 Ð\ÑÓ ," " # # " " # #

If is a non-negative random variable (defined on or ) then \ Ò!ß∞Ñ Ð!ß∞Ñ

IÒ\Ó œ Ò" JÐBÑÓ . œ WÐBÑ . ! !

∞ ∞B B (3.4)

This relationship is valid for any random variable, discrete, continuous or with a mixeddistribution. Using the example on the previous page, thenif for , 0ÐBÑ œ #B ! B "

JÐBÑ œ ß Ò" JÐBÑÓ .B œ Ò" B Ó .B œ œ IÒ\Ó B !BŸ"

" B"

#$

# for

, for and . ! !

∞ " #

It tends to be more awkward to apply this rule to discrete random variables.

Jensen's Inequality states that if is a function such the on the probability space for , then1 1 ÐBÑ ! \ww

IÒ1Ð\ÑÓ 1ÐIÒ\ÓÑ IÒ\ Ó ÐIÒ\ÓÑ. For example, .# #

STAM-34 SECTION 3 - PRELIMINARY REVIEW - RANDOM VARIABLES II

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Moments of a random variableIf is an integer, then the is (sometimes denoted ) and is8 " IÒ\ Ó8 \th (raw) moment of 8 w

8.

in the discrete case, and in the continuous case. (3.5) all B

8 8∞∞

B ‚ :ÐBÑ B ‚ 0ÐBÑ .B

If the mean of is , then the is defined to be \ IÒÐ\ Ñ Ó. .8 \th central moment of (about the mean ). 8

and may be denoted ..8

For instance, the 3rd central moment of the fair die toss random variable is\

IÒÐ\ Ñ Ó œ Ð" Ñ ‚ Ð# Ñ ‚ â Ð' Ñ ‚ œ !( ( " ( " ( "# # ' # ' # '

$ $ $ $ .

The 2nd central moment of the continuous random variable pdf\ 0ÐBÑ œ #B ! B " for is!" #ÐB Ñ #B .B œ#

$ ‚ "") .

Variance of \The variance of is denoted , , or . It is defined to be equal to\ Z +<Ò\Ó Z Ò\Ó 5 5# #

\

Z +<Ò\Ó œ IÒÐ\ Ñ Ó œ IÒ\ Ó œ IÒ\ Ó ÐIÒ\ÓÑ. .\# # # # #

\ (3.6)

The representation of as is often the most convenient one to use. The variance is theZ +<Ò\Ó IÒ\ Ó ÐIÒ\ÓÑ# #

2nd central moment of ; .\ œ Z +<Ò\Ó œ . . .# #w #

Variance is a measure of the "dispersion" of about the mean. Being the expected value of , the\ Ð\ Ñ.\#

variance is the average squared deviation of from its mean .\ .\

A large variance indicates significant levels of probability or density for points far from . The variance is alwaysIÒ\Ó ! \ ! \ " (the variance of is equal to only if has a discrete distribution with a single point and probability at that

point; in other words, not random at all).

The random variable has mean and variance .prob. .5prob. .5

Y œ IÒY Ó œ & Z +<ÒY Ó œ "%'

The random variable has the same mean as , , but has variance .

prob. .5prob. .5

[ œ Y IÒ[ Ó œ & Z +<Ò[ Ó œ *#)

The higher variance of is indicative of the further dispersion of the outcomes of from the mean 5 as[ [compared to .Y

If and are constants, then .+ , Z +<Ò+\ ,Ó œ + Z +<Ò\Ó#

Here is a useful shortcut for finding the variance of a 2-point discrete random variable.

If is the two-point random variable Prob. Prob.

\ \ œ+ :, " :

then .Z +<Ò\Ó œ Ð, +Ñ ‚ : ‚ Ð" :Ñ# (3.7)

Standard deviation of \The standard deviation of the random variable is the square root of the variance, and is denoted\

5\ œ Z +<Ò\Ó .

SECTION 3 - PRELIMINARY REVIEW - RANDOM VARIABLES II STAM-35

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Coefficient of variationThe coefficient of variation of is\

5.\

\œ

Z +<Ò\Ó

IÒ\Ó . (3.8)

Skewness and kurtosis

The skewness of is , and the kurtosis is (3.9)\ IÒÐ\ Ñ Ó IÒÐ\ Ñ Ó. .5 5

$ %

$ %

Skewness measures the symmetry of a random variable; skewness of 0 indicates a distribution which is symmetricaround its mean. The fair dies toss random variable has skewness of 0. Kurtosis is a measure of the "peakedness"of a distribution. Higher kurtosis suggests that more of the variance is due to less frequent large deviations, ratherthan more frequent smaller deviations.There have been infrequent references to skewness and kurtosis on the STAM Exam.

3.2 Moment generating function of random variable \The moment generating function of (mgf) is denoted or , and it is defined to be\ Q Ð>Ñ ß 7 Ð>Ñ ß QÐ>Ñ 7Ð>Ñ\ \

Q Ð>Ñ œ IÒ/ Ó\>\ , which is either

B

>B >B∞

∞/ :ÐBÑ / 0ÐBÑ .B if is discrete, or if is continuous (3.10)\ \

It is always true that .Q Ð!Ñ œ "\

The moment generating function of might not exist for all real numbers, but usually exists on some interval of\real numbers. The function is called the . The function 68ÒQ Ð>ÑÓ Q Ð68\ \cumulant generating function>Ñ œ IÒ> Ó\ is called the and may be denoted ; the probabilityprobability generating function T Ð>Ñ œ IÒ> Ó\

\

generating function is usually used in the case of a discrete random variable.

Some properties of moment and probability generating functionsSuppose that for the random variable , the moment generating function exists in an interval\ Q Ð>Ñ\

containing the point . Then> œ !

..>

8

8 Q Ð>Ñ œ Q Ð!Ñ œ IÒ\ Ó œ\>œ!

Ð8Ñ\

8 w8 . , the -th moment of , and (3.11)8 \

. ..> Q Ð!Ñ .>

Q Ð!Ñ68ÒQ Ð>ÑÓ œ œ IÒ\Ó 68ÒQ Ð>ÑÓ œ Z +<Ò\Ó\ \

>œ! >œ! \

w

\

#

#, and (3.12)

If and are random variables, and for all values of in an interval containing ,\ \ Q Ð>Ñ œ Q Ð>Ñ > > œ !" # \ \" #

then and have identical probability distributions.\ \" #

If are independent random variables and then\ ß\ ß ÞÞÞß \ W œ \" # 8 33œ"

8 (3.13)Q Ð>Ñ œ Q Ð>Ñ ‚Q Ð>Ñ ‚ † † † ‚Q Ð>Ñ œ Q Ð>ÑW \ \ \ \

3œ"

8

" # 8 3

If has a discrete non-negative integer distribution with , then the probability generating\ : œ T Ò\ œ 5Ó5

function is

(3.14)T Ð>Ñ œ : : ‚ > : ‚ > â œ : ‚ >\ ! " # 5# 5

5œ!

∞and .T Ð!Ñ œ :\ !

STAM-36 SECTION 3 - PRELIMINARY REVIEW - RANDOM VARIABLES II

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

3.3 Percentiles and Quantiles of a distributionIf , then the -th percentile of the distribution of is the number which satisfies the following! : " "!!: \ -:inequalities: J Ò- Ó œ T Ò\ - Ó Ÿ : Ÿ T Ò\ Ÿ - Ó œ J Ò- Ó:

: : : . (3.15)

For a continuous random variable, it is sufficient to find the for which . If , - T Ò\ Ÿ - Ó œ : : œ Þ&: : the 50-thpercentile of a distribution is referred to as the median of the distribution, it is the point for whichQTÒ\ Ÿ QÓ œ Þ& Q Q. The median is the 50% probability point, half of the distribution probability is to the left of andhalf is to the right. The word "quantile" is a general term for the proportion or percent of a distribution below a certaingiven point and is often used interchangeably with "percentile".

3.4 The mode of a distributionThe mode is any point at which the probability or density function is maximized. For the fair die toss7 0ÐBÑrandom variable, each of or would satisfy the requirements of being a mode, since theB œ "ß #ß $ß %ß & 'probability at each point is , which is the maximum probability of any individual point. For the continuous"

'

random variable with for , strictly speaking, there is no mode since the upper bound of the0ÐBÑ œ #B ! B "density of 2 is never reached. The mode could be described as occurring at 1 as a limit.

Example 3-1:Let equal the number of tosses of a fair die until the first "1" appears. Find .\ IÒ\ÓSolution:\ " is a discrete random variable that can take on any integer value . The probability that the first 1 appears on

the -th toss is for ( tosses that are not , followed by a 1). This is theB 0ÐBÑ œ B " B " "Ð Ñ Ð Ñ& "' '

B"

probability function of . Then\

IÒ\Ó œ 5 ‚ 0Ð5Ñ œ 5 ‚ œ Ò" # $ âÓ 5œ" 5œ"

∞ ∞5" #Ð Ñ Ð Ñ Ð Ñ Ð Ñ Ð Ñ& " " & &

' ' ' ' ' .

We use the general increasing geometric series relation ," #< $< â œ# "Ð"<Ñ#

so that . IÒ\Ó œ ‚ œ 'Ð Ñ" "' Ð" Ñ&'

#

Example 3-2:

The moment generating function of is for , where .\ > ! αα> α α

Find .Z +<Ò\ÓSolution:

Z +<Ò\Ó œ IÒ\ Ó ÐIÒ\ÓÑ IÒ\Ó œ Q Ð!Ñ œ# # w\. α

αÐ >Ñ# >œ!

œ "α ,

and .IÒ\ Ó œ œ p Z +<Ò\Ó œ œ# #

>œ!Q Ð!Ñ œww

\#

Ð >Ñα

α $ # # " "α α α α# # #Ð Ñ

Alternatively, 68Q Ð>Ñ œ 68 œ 68 68Ð >Ñ p\ Ð Ñαα α> .> >

. "α α 68ÒQ Ð>ÑÓ œ\

and so that . " . ".> Ð >Ñ .>

# #

# # # #68ÒQ Ð>ÑÓ œ Z +<Ò\Ó œ 68ÒQ Ð>ÑÓ œ Þ\ \>œ!α α

SECTION 3 - PRELIMINARY REVIEW - RANDOM VARIABLES II STAM-37

Actex Learning SOA Exam STAM - Short-Term Actuarial Mathematics

Example 3-3:Given that the density function of is , for , and elsewhere, find the -th moment of ,\ 0ÐBÑ œ / B ! ! 8 \) B)

where is a non-negative integer (assuming that ).8 !)Solution:The -th moment of is . Applying integration by parts, this can be written as8 \ IÒ\ Ó œ B † / .B8 8 B

!∞ ) )

! ! !∞ ∞ ∞8 B 8 B 8" B 8" B

Bœ!

Bϰ

B .Ð / Ñ œ B / 8B / .B œ 8B / .BÞ) ) ) )

Repeatedly applying integration by parts results in . It is worthwhile noting the general form of theIÒ\ Ó œ8 8x)8

integral that appears in this example; if is an integer and , then by repeated applications of5 ! + !

integration by parts, we have , so that in this example!∞ 5 +>> / .> œ 5x

+5"

! !∞ ∞8 B 8 BB / .B œ B / .B œ † œ) ) )) ) 8x 8x

) )8" 8 .

An alternative solution uses the moment generating functionÞ

Q Ð>Ñ œ IÒ/ Ó œ / / .B œ / .B œ\>\ >B B Ð >ÑB

! !

∞ ∞ ) )) ) ))>

(which will be valid for ). Then> )

Q Ð>Ñ œ IÒ\Ó œ Q Ð!Ñ œ Q Ð>Ñ œ IÒ\ Ó œ Q Ð!Ñ œ\ \w w #

\ \Ð#Ñ Ð#Ñ) )

) ) ) )Ð >Ñ Ð >Ñ" # #

# $ # so that , and so that .

It can be shown by induction on that so that . 8 Q Ð>Ñ œ IÒ\ Ó œ Q Ð!Ñ œ\ \Ð8Ñ Ð8Ñ88x 8x

Ð >Ñ)

) )8" 8

Example 3-4:The continuous random variable has pdf for .\ 0ÐBÑ œ / ∞ B ∞"

#lBl

Find the 87.5-th percentile of the distribution.Solution:The 87.5-th percentile is the number for which ., !Þ)(& œ T Ò\ Ÿ ,Ó œ 0ÐBÑ .B œ / .B

∞ ∞

, , lBl"#

Note that this distribution is symmetric about , since , so the mean and median are! 0Ð BÑ œ 0ÐBÑboth . Thus, , and so! , !

∞ ∞ ! !

lBl lBl lBl B! , ,, " " " "# # # #/ .B œ / .B / .B œ !Þ& / .B

œ !Þ& Ð" / Ñ œ !Þ)(& p , œ 68Ð!Þ#&Ñ œ 68 %"#

, .