ACSDA International Seminar Johannesburg, South Africa November 19-21,2003 Corporate Governance and...

33

ACSDA International Seminar ACSDA International Seminar Johannesburg, South Africa November 19-21,2003 Johannesburg, South Africa November 19-21,2003 Corporate Governance Corporate Governance and Transparency and Transparency Amarílis Prado Sardenberg Amarílis Prado Sardenberg November 21, 2003 November 21, 2003

-

Upload

claud-stevens -

Category

Documents

-

view

215 -

download

1

Transcript of ACSDA International Seminar Johannesburg, South Africa November 19-21,2003 Corporate Governance and...

ACSDA International SeminarACSDA International Seminar

Johannesburg, South Africa November 19-21,2003 Johannesburg, South Africa November 19-21,2003

Corporate Governance Corporate Governance

and Transparencyand Transparency

Amarílis Prado SardenbergAmarílis Prado Sardenberg

November 21, 2003 November 21, 2003

Corporate Corporate

Governance Governance

at CBLCat CBLC

CORPORATE GOVERNANCE AT CBLCCORPORATE GOVERNANCE AT CBLCCBLCCBLC

• Self-regulatory organization under the supervision of the Self-regulatory organization under the supervision of the Brazilian Securities Commission (CVM) and the Central Brazilian Securities Commission (CVM) and the Central BankBank

• For-profit corporationFor-profit corporation

• Entity owned by market participantsEntity owned by market participants

CORPORATE GOVERNANCE AT CBLCCORPORATE GOVERNANCE AT CBLC

OWNERSHIP STRUCTUREOWNERSHIP STRUCTURE

Banks38%

Bovespa Serv&Part

23%

O thers2% Brokers/

Dealers37%

CORPORATE GOVERNANCE AT CBLCCORPORATE GOVERNANCE AT CBLC

MANAGEMENT STRUCTUREMANAGEMENT STRUCTURE

• General Assembly - shareholdersGeneral Assembly - shareholders

• Board of Directors – 7 membersBoard of Directors – 7 members

• Executive Board – 3 membersExecutive Board – 3 members

CORPORATE GOVERNANCE AT CBLCCORPORATE GOVERNANCE AT CBLC

BOARD OF DIRECTORS’ COMPOSITIONBOARD OF DIRECTORS’ COMPOSITION

7 effective members7 effective members

• 6 shareholders representatives 6 shareholders representatives

• 3 banks (2 effective members and 1 alternate)3 banks (2 effective members and 1 alternate)

• 3 brokers (2 effective members and 1alternate)3 brokers (2 effective members and 1alternate)

• 3 BOVESPA representatives3 BOVESPA representatives

• 2 effective members and 1 alternate2 effective members and 1 alternate

• CBLC’s Chief Executive OfficerCBLC’s Chief Executive Officer

CORPORATE GOVERNANCE AT CBLCCORPORATE GOVERNANCE AT CBLC

ACCESS CONDITIONSACCESS CONDITIONS

All criteria for participation are publicly All criteria for participation are publicly

disclosed and clearly defined, assuring market disclosed and clearly defined, assuring market

participants the same access conditions in participants the same access conditions in

accordance with their functionsaccordance with their functions

CORPORATE GOVERNANCE AT CBLCCORPORATE GOVERNANCE AT CBLC

COMMON REQUIREMENTS FOR DIRECT PARTICIPANTS - COMMON REQUIREMENTS FOR DIRECT PARTICIPANTS -

DEPOSITORY AGENTS AND CLEARING AGENTS :DEPOSITORY AGENTS AND CLEARING AGENTS :

• Institution approved by the Central Bank and the Brazilian Securities Institution approved by the Central Bank and the Brazilian Securities & Exchange Commission& Exchange Commission

• Compliance with the capital requirements defined by the regulatory Compliance with the capital requirements defined by the regulatory bodies and by CBLC itselfbodies and by CBLC itself

• Agreement with CBLC rulesAgreement with CBLC rules

• Admission approved by the Board of Governors / Board of DirectorsAdmission approved by the Board of Governors / Board of Directors

• Contract with CBLCContract with CBLC

• Minimum technological standards and a contingency planMinimum technological standards and a contingency plan

CORPORATE GOVERNANCE AT CBLCCORPORATE GOVERNANCE AT CBLC

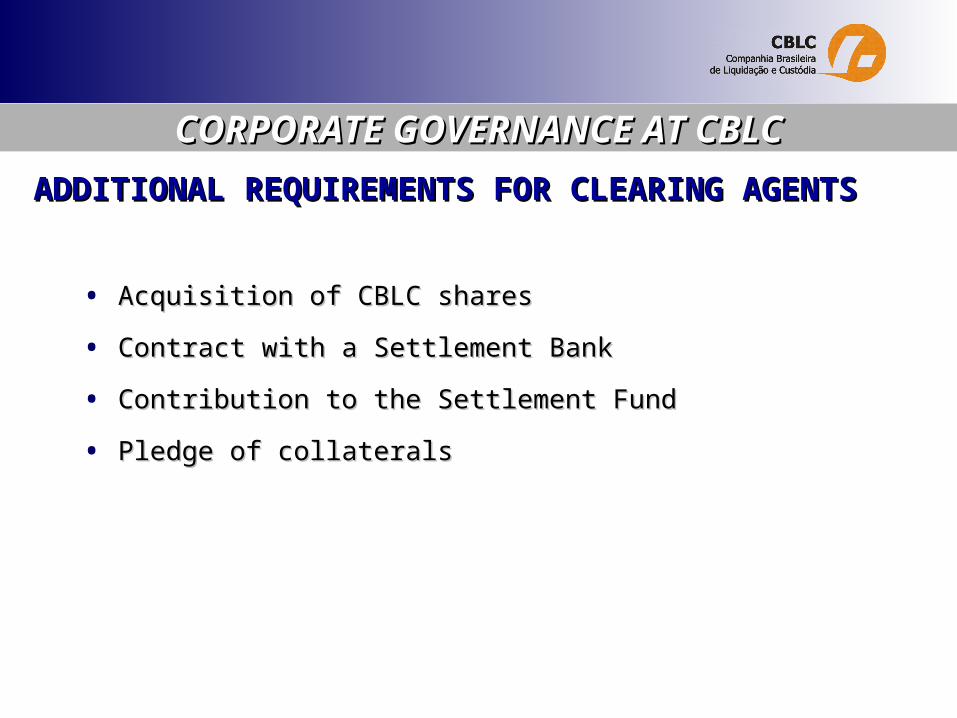

ADDITIONAL REQUIREMENTS FOR CLEARING AGENTSADDITIONAL REQUIREMENTS FOR CLEARING AGENTS

• Acquisition of CBLC sharesAcquisition of CBLC shares

• Contract with a Settlement BankContract with a Settlement Bank

• Contribution to the Settlement FundContribution to the Settlement Fund

• Pledge of collateralsPledge of collaterals

““New Market” New Market”

and the and the Corporate Corporate

Governance SegmentsGovernance Segments

WHY SÃO PAULO STOCK EXCHANGE (BOVESPA) WHY SÃO PAULO STOCK EXCHANGE (BOVESPA) CREATED THE NEW CORPORATE GOVERNANCE CREATED THE NEW CORPORATE GOVERNANCE SEGMENTS?SEGMENTS?

• The Corporations Law reform ( Law nº. 9457, 1997) did not go The Corporations Law reform ( Law nº. 9457, 1997) did not go far enough in what concerns:far enough in what concerns:

• minority shareholders rightsminority shareholders rights

• information disclosureinformation disclosure

• enforcement of rulesenforcement of rules

NEW CORPORATE GOVERNANCE SEGMENTSNEW CORPORATE GOVERNANCE SEGMENTS

WHY SÃO PAULO STOCK EXCHANGE (BOVESPA) WHY SÃO PAULO STOCK EXCHANGE (BOVESPA) CREATED THE NEW CORPORATE GOVERNANCE CREATED THE NEW CORPORATE GOVERNANCE SEGMENTS?SEGMENTS?

• Bovespa aimed to build up a benchmark on corporate Bovespa aimed to build up a benchmark on corporate governance standardsgovernance standards

NEW CORPORATE GOVERNANCE SEGMENTSNEW CORPORATE GOVERNANCE SEGMENTS

NEW MARKET: THE STATE-OF-THE-ARTNEW MARKET: THE STATE-OF-THE-ART

NEW CORPORATE GOVERNANCE SEGMENTSNEW CORPORATE GOVERNANCE SEGMENTS

WHAT ARE THE NEW CORPORATE GOVERNANCE LISTING WHAT ARE THE NEW CORPORATE GOVERNANCE LISTING

SEGMENTS?SEGMENTS?

• Set of rules over and above the Corporations Law reflecting Set of rules over and above the Corporations Law reflecting market demands and requirements Companies commitment market demands and requirements Companies commitment to the highest standards of corporate governanceto the highest standards of corporate governance

• Companies commitment to the highest standards of Companies commitment to the highest standards of corporate governancecorporate governance

• Private sector initiative, based on and enforced by a contract Private sector initiative, based on and enforced by a contract established between the issuer and BOVESPAestablished between the issuer and BOVESPA

• Adhesion is voluntary and market drivenAdhesion is voluntary and market driven

NEW CORPORATE GOVERNANCE SEGMENTSNEW CORPORATE GOVERNANCE SEGMENTS

OBJECTIVES:OBJECTIVES:

Assure minority shareholders protectionAssure minority shareholders protection

Increase transparency and market confidence Increase transparency and market confidence

Provide companies with lower cost of capitalProvide companies with lower cost of capital

Increase stock market liquidityIncrease stock market liquidity

NEW CORPORATE GOVERNANCE SEGMENTSNEW CORPORATE GOVERNANCE SEGMENTS

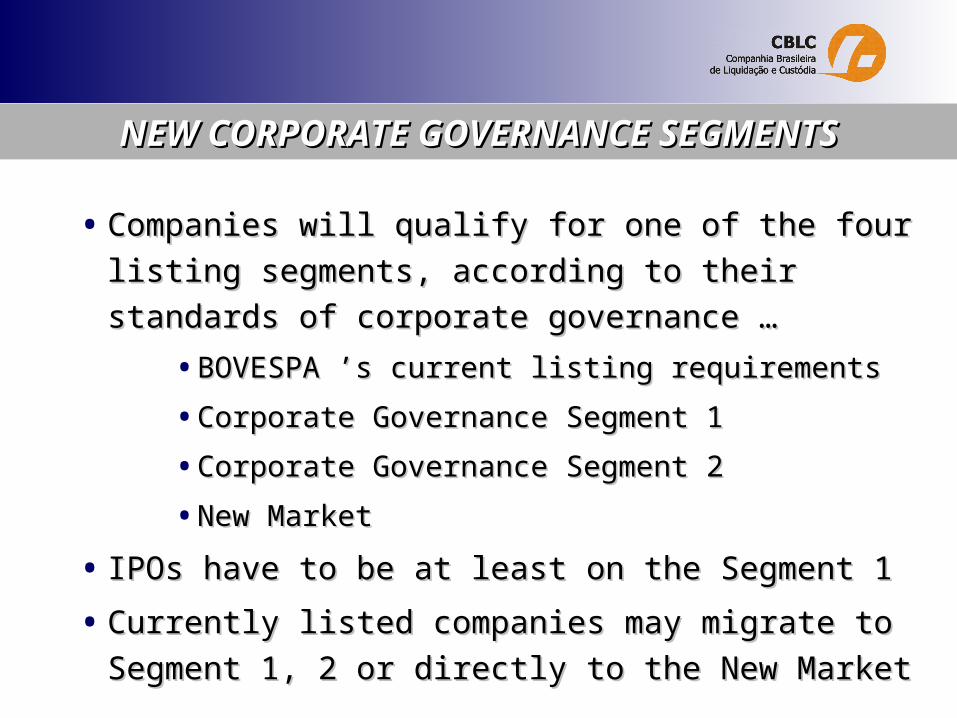

• Companies will qualify for one of the four listing Companies will qualify for one of the four listing

segments, according to their standards of corporate segments, according to their standards of corporate

governance …governance …

• BOVESPA ’s current listing requirements BOVESPA ’s current listing requirements

• Corporate Governance Segment 1Corporate Governance Segment 1

• Corporate Governance Segment 2 Corporate Governance Segment 2

• New MarketNew Market

• IPOs have to be at least on the Segment 1IPOs have to be at least on the Segment 1

• Currently listed companies may migrate to Segment 1, 2 Currently listed companies may migrate to Segment 1, 2

or directly to the New Marketor directly to the New Market

CORPORATE GOVERNANCE SEGMENTS 1 & 2CORPORATE GOVERNANCE SEGMENTS 1 & 2

CORPORATE GOVERNANCE SEGMENTS 1 & 2CORPORATE GOVERNANCE SEGMENTS 1 & 2

CORPORATE GOVERNANCE SEGMENT 1CORPORATE GOVERNANCE SEGMENT 1

Segment 1 companies have most of the same Segment 1 companies have most of the same

requirements as the existing BOVESPA listing rulesrequirements as the existing BOVESPA listing rules

But Segment 1 companies will be required to improve But Segment 1 companies will be required to improve

their disclosure, liketheir disclosure, like More comprehensive financial statementsMore comprehensive financial statements

Information on trading by the insiders and on self dealingInformation on trading by the insiders and on self dealing

Plus: 25% free floatPlus: 25% free float

CORPORATE GOVERNANCE SEGMENTS 1 & 2CORPORATE GOVERNANCE SEGMENTS 1 & 2

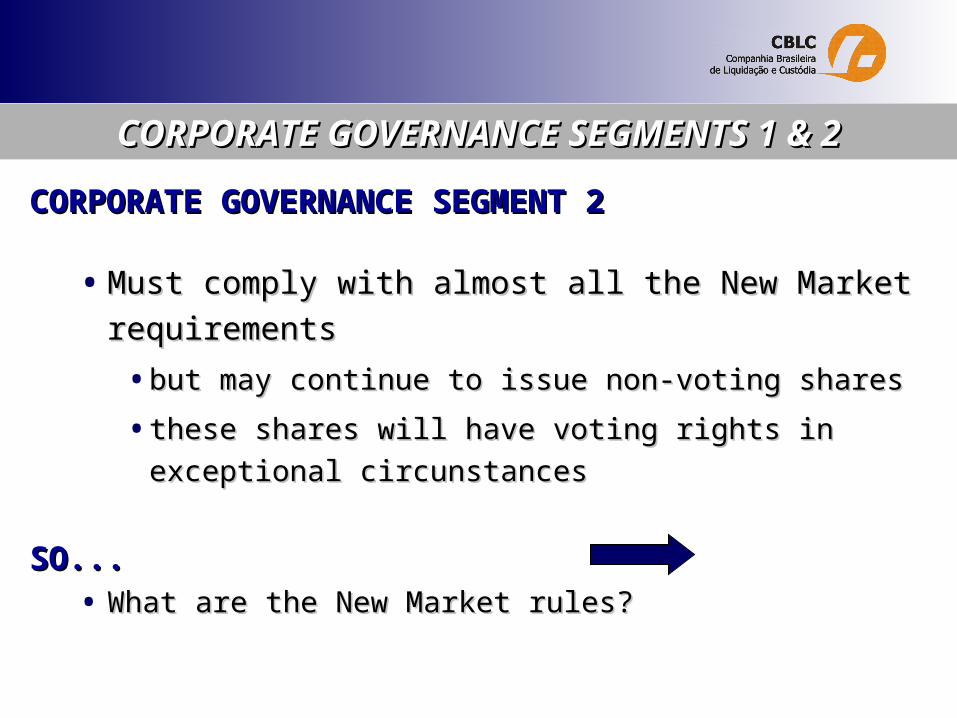

CORPORATE GOVERNANCE SEGMENT 2CORPORATE GOVERNANCE SEGMENT 2

• Must comply with almost all the New Market requirementsMust comply with almost all the New Market requirements

• but may continue to issue non-voting sharesbut may continue to issue non-voting shares

• these shares will have voting rights in exceptional these shares will have voting rights in exceptional

circunstancescircunstances

SO...SO...• What are the New Market rules?What are the New Market rules?

NEW MARKETNEW MARKET

NEW MARKETNEW MARKET

RULES (I)RULES (I)

• Full voting rights for all sharesFull voting rights for all shares

• Much higher disclosure standardsMuch higher disclosure standards

• Delistings: Public tender offer at economic valueDelistings: Public tender offer at economic value

• Tag along rightsTag along rights

• Board of Directors will have a unified mandate of 1 year and a Board of Directors will have a unified mandate of 1 year and a

minimum of 5 members minimum of 5 members

NEW MARKETNEW MARKET

RULES (II)RULES (II)

• 25% minimum free float25% minimum free float

• Announcement of General Meetings of Shareholders at a Announcement of General Meetings of Shareholders at a

minimum period in advanceminimum period in advance

• Improved public offering rulesImproved public offering rules

• Retail distribution of new shares requiredRetail distribution of new shares required

• Prospectus according to international standardsProspectus according to international standards

• Lock up period for controlling shareholders (100% in the first 6 months, Lock up period for controlling shareholders (100% in the first 6 months,

60% in the following 6 months after the IPO)60% in the following 6 months after the IPO)

• Annual financial statements in an internationally recognized Annual financial statements in an internationally recognized

standard (US GAAP or IAS)standard (US GAAP or IAS)

• Enforcement:Enforcement: BOVESPA Supervision and Arbitration Panel BOVESPA Supervision and Arbitration Panel

NEW MARKETNEW MARKET

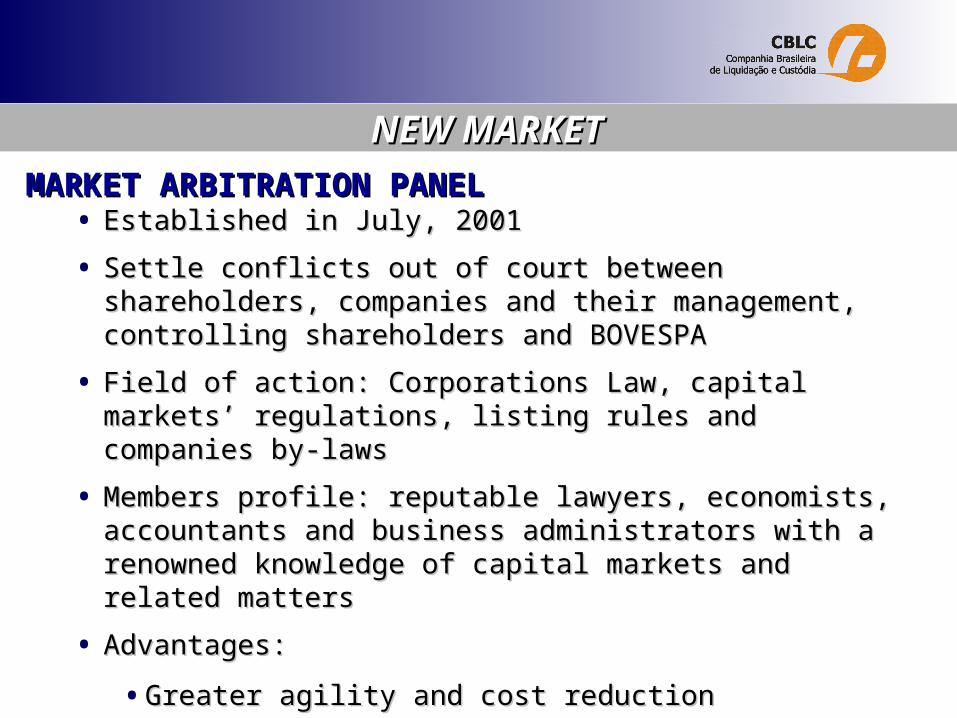

MARKET ARBITRATION PANELMARKET ARBITRATION PANEL• Established in July, 2001Established in July, 2001

• Settle conflicts out of court between shareholders, companies Settle conflicts out of court between shareholders, companies and their management, controlling shareholders and BOVESPAand their management, controlling shareholders and BOVESPA

• Field of action: Corporations Law, capital markets’ regulations, Field of action: Corporations Law, capital markets’ regulations, listing rules and companies by-lawslisting rules and companies by-laws

• Members profile: Members profile: reputable lawyers, economists, accountants reputable lawyers, economists, accountants and business administrators with a renowned knowledge of and business administrators with a renowned knowledge of capital markets and related matterscapital markets and related matters

• Advantages:Advantages:

• Greater agility and cost reductionGreater agility and cost reduction

• High specialized arbitrators High specialized arbitrators

• ConfidentialityConfidentiality

SUMMING UP…SUMMING UP…

• More DisclosureMore Disclosure

• 29 companies29 companies

• Rights to Rights to InvestorsInvestors

• More DisclosureMore Disclosure

• 3 companies3 companies

• Only Voting Only Voting SharesShares

• Rights to Rights to InvestorsInvestors

• More DisclosureMore Disclosure

• 2 companies2 companies

BRAZILIAN CORPORATE GOVERNANCE REFORM (II)BRAZILIAN CORPORATE GOVERNANCE REFORM (II)

LAW nº. 10.303, 2001LAW nº. 10.303, 2001

• Assured effective rights for the non-voting sharesAssured effective rights for the non-voting shares

• Guaranteed tag-along rights to the holders of voting shares Guaranteed tag-along rights to the holders of voting shares

• Determined that minority shareholders have the right to elect board Determined that minority shareholders have the right to elect board membersmembers

• Established that manipulation and insider trading are criminal offensesEstablished that manipulation and insider trading are criminal offenses

CVM INSTRUCTION Nº. 358, 2002CVM INSTRUCTION Nº. 358, 2002

• Enhanced the information disclosureEnhanced the information disclosure

• Established restrictions on trading by the insiders during sensitive periodsEstablished restrictions on trading by the insiders during sensitive periods

CVM INSTRUCTION Nº. 361, 2002CVM INSTRUCTION Nº. 361, 2002

• Regulated tender offers in case of delistingRegulated tender offers in case of delisting

BRAZILIAN CORPORATE GOVERNANCE REFORM (II)BRAZILIAN CORPORATE GOVERNANCE REFORM (II)

THE NEW CORPORATE GOVERNANCE REFORM THE NEW CORPORATE GOVERNANCE REFORM INCORPORATED SOME OF THE NEW INCORPORATED SOME OF THE NEW

CORPORATE GOVERNANCE SEGMENTS’ RULESCORPORATE GOVERNANCE SEGMENTS’ RULES

BUT NEW MARKET IS BUT NEW MARKET IS STILL A BENCHMARKSTILL A BENCHMARK

Transparency and Transparency and Information DisclosureInformation Disclosure

Relationship among Bovespa, CBLC and IssuersRelationship among Bovespa, CBLC and Issuers

RELATIONSHIP BETWEEN BOVESPA AND THE ISSUERSRELATIONSHIP BETWEEN BOVESPA AND THE ISSUERS

• Issuers are required Issuers are required by lawby law to provide information to the to provide information to the

Brazilian Securities and Exchange Commission (CVM) and to Brazilian Securities and Exchange Commission (CVM) and to

BOVESPABOVESPA

TRANSPARENCY AND INFORMATION DISCLOSURETRANSPARENCY AND INFORMATION DISCLOSURE

CBLC HAS AN AGREEMENT WITH BOVESPA TO RECEIVE CBLC HAS AN AGREEMENT WITH BOVESPA TO RECEIVE ALL THE INFORMATION PROVIDED BY THE ISSUERSALL THE INFORMATION PROVIDED BY THE ISSUERS

RELATIONSHIP BETWEEN BOVESPA AND THE ISSUERSRELATIONSHIP BETWEEN BOVESPA AND THE ISSUERS

• Close relationshipClose relationship

• Development of an institutional, operational and Development of an institutional, operational and

technological infrastructure to support the relationship technological infrastructure to support the relationship

with the issuerswith the issuers

TRANSPARENCY AND INFORMATION DISCLOSURETRANSPARENCY AND INFORMATION DISCLOSURE

ALL INFORMATION IS PROVIDED BY THE ISSUERS IN ALL INFORMATION IS PROVIDED BY THE ISSUERS IN ELECTRONIC FILES (WORD OR PDF) SENT THROUGH A ELECTRONIC FILES (WORD OR PDF) SENT THROUGH A

ELECTRONIC SYSTEM AVALAIBLE IN THE INTERNETELECTRONIC SYSTEM AVALAIBLE IN THE INTERNET

TRANSPARENCY AND INFORMATION DISCLOSURETRANSPARENCY AND INFORMATION DISCLOSURE

Issuer

CVM BOVESPA

CBLC

CVM-BOVESPA ELECTRONIC SYSTEM (Edgar like)CVM-BOVESPA ELECTRONIC SYSTEM (Edgar like)

•The issuer sends the information The issuer sends the information

through the electronic system. Both through the electronic system. Both

CVM and Bovespa receive itCVM and Bovespa receive it

•The information is promptly The information is promptly

available in the CVM websiteavailable in the CVM website

• After an accuracy evaluation the After an accuracy evaluation the

information is available in the information is available in the

Bovespa websiteBovespa website

•The information related to corporate The information related to corporate

actions and reorganizations is sent actions and reorganizations is sent

to CBLCto CBLC

INFORMATION PROVIDED BY THE ISSUERS TO BOVESPAINFORMATION PROVIDED BY THE ISSUERS TO BOVESPA• Financial Statements (trimestrial and annual)Financial Statements (trimestrial and annual)

• Announcements Announcements

• Communications to the market, public releases, etcCommunications to the market, public releases, etc

• Resolutions (of General and Board meetings)Resolutions (of General and Board meetings)

• Press releasesPress releases

• Other InformationOther Information

TRANSPARENCY AND INFORMATION DISCLOSURETRANSPARENCY AND INFORMATION DISCLOSURE

ALL INFORMATION RELATED TO CORPORATE ACTIONS IS ALL INFORMATION RELATED TO CORPORATE ACTIONS IS SENT TO CBLC DEPOSITORY SERVICE WITHIN THE SENT TO CBLC DEPOSITORY SERVICE WITHIN THE

ELECTRONIC SYSTEM IN A REAL TIME BASISELECTRONIC SYSTEM IN A REAL TIME BASIS

INFORMATION PROVIDED BY CBLCINFORMATION PROVIDED BY CBLC

• CBLC provides to the custodians:CBLC provides to the custodians:

• information on corporate actions to be paid to their information on corporate actions to be paid to their

clients in the level of the beneficial ownerclients in the level of the beneficial owner

• information on instructions and operational procedures information on instructions and operational procedures

to be adopted in case of voluntary corporate actionsto be adopted in case of voluntary corporate actions

• Issuers and custodians receive information related to Issuers and custodians receive information related to

taxes obligations calculated for each final investortaxes obligations calculated for each final investor

TRANSPARENCY AND INFORMATION DISCLOSURETRANSPARENCY AND INFORMATION DISCLOSURE

INFORMATION PROVIDED BY CBLCINFORMATION PROVIDED BY CBLC

• Information, deadlines and forms related to cash and Information, deadlines and forms related to cash and

securities corporate actions and reorganizations are securities corporate actions and reorganizations are

available in the CBLC proprietary network (daily updated)available in the CBLC proprietary network (daily updated)

Alerts sent by e-mailAlerts sent by e-mail

TRANSPARENCY AND INFORMATION DISCLOSURETRANSPARENCY AND INFORMATION DISCLOSURE

GENERAL CONCLUSIONSGENERAL CONCLUSIONS

• New Market became a international reference to market players and regulators regarding corporate governance

• BOVESPA and CBLC have a close and comprehensive relationship with issuers

HIGH STANDARDS OF INFORMATION DISCLOSURE HIGH STANDARDS OF INFORMATION DISCLOSURE AND MARKET TRANSPARENCYAND MARKET TRANSPARENCY