Financing Acquisition and Creation of a Community Forest ...

Presenting a live 90‐minute webinar with interactive Q&A

Acquisition Financing: Strategies for D l C lDeal CounselEvaluating Financing Options, Structuring the Deal, Addressing Loan Documentation and Intercreditor Issues

T d ’ f l f

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, APRIL 12, 2011

Today’s faculty features:

Lawrence F. Flick, II, Partner, Blank Rome, New York

Jeffrey A. Beuche, Partner, Perkins Coie, Denver

S. Randy Lampert, President, Lampert Debt Advisors, New York

Brian Schofield, Director, Lampert Debt Advisors, New York

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the blue icon beside the box to send

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-888-450-9970 and enter your PIN when prompted Otherwise please send us a chat or e mail when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Acquisition Financing: S i f D l C lStrategies for Deal Counsel

April 12, 2011

888 Seventh Avenue | New York, NY 10019 | www.lampertdebtadvisors.com

Lampert Debt Advisors is a boutique investment bank specializing in arranging

LAMPERT DEBT ADVISORS

S Randy Lampert – President

Lampert Debt Advisors is a boutique investment bank specializing in arrangingdebt financing for privately-owned, sponsor-backed and publicly-tradedcompanies

S. Randy Lampert – President 30 years of experience in completing debt financings Co-founder of Debt Capital Markets Group and Head of Business

Development at Morgan Joseph Founder and Head of Leveraged Finance at Nomura Securities Founder and Head of Leveraged Finance at Nomura Securities Assistant Head of Communications and Technology at Salomon

Brothers MBA, University of Chicago randy lampert@lampertdebtadvisors com [email protected] 646.367.4660

Brian Schofield – Director Vice President – ICON Capital Corp., engaged in originating andp p , g g g g

structuring asset based transactions in numerous industries Founder of Schofield Realty Group, a real estate development company [email protected] 646.367.4662

66

LEVERAGE FOR LBO’S CONTINUES TO RISE..

51%60%8.0x

Equity %EBITDA Multiple and with it, equity contributions decline

4.8 5.3 5.46.2

4.94 0

4.75.2

33%

43%51%

44%

39% 40%

50%6.0x

4.035% 32%

33%33%

20%

30%

2 0x

4.0x

0%

10%

0.0x

2.0x

2004 2005 2006 2007 2008 2009 2010 1Q11

FLD/EBITDA SLD/EBITDA Other Sr Debt/EBITDA Sub Debt/EBITDA Equity

Source: S&P LCD

77

Source: S&P LCD

STRUCTURAL CONSIDERATIONS

7.0

Avg. Term (yrs)

75%

% of New Issues with Pricing Grids and Prepay Fees

Average Tenor of New Issues

4.54.9 5.1 5.1 5.2

4.5 4.6 4.7

5.66.0 6.1 6.0 6.2

5.3

4.4

5.66.0

4 0

5.0

6.0

45%

62%

50%

3.4

2.0

3.0

4.0

32%27% 26% 26%

23%19%

17%15%14%

20% 21%

14%

21% 21%25%

0.0

1.0

2003 2004 2005 2006 2007 2008 2009 2010 1Q11Pro rata Institutional

6%

%%11%

0%2003 2004 2005 2006 2007 2008 2009 2010 1Q11

Pricing Grids Prepay Fees

Source: S&P LCD

88

Source: S&P LCD

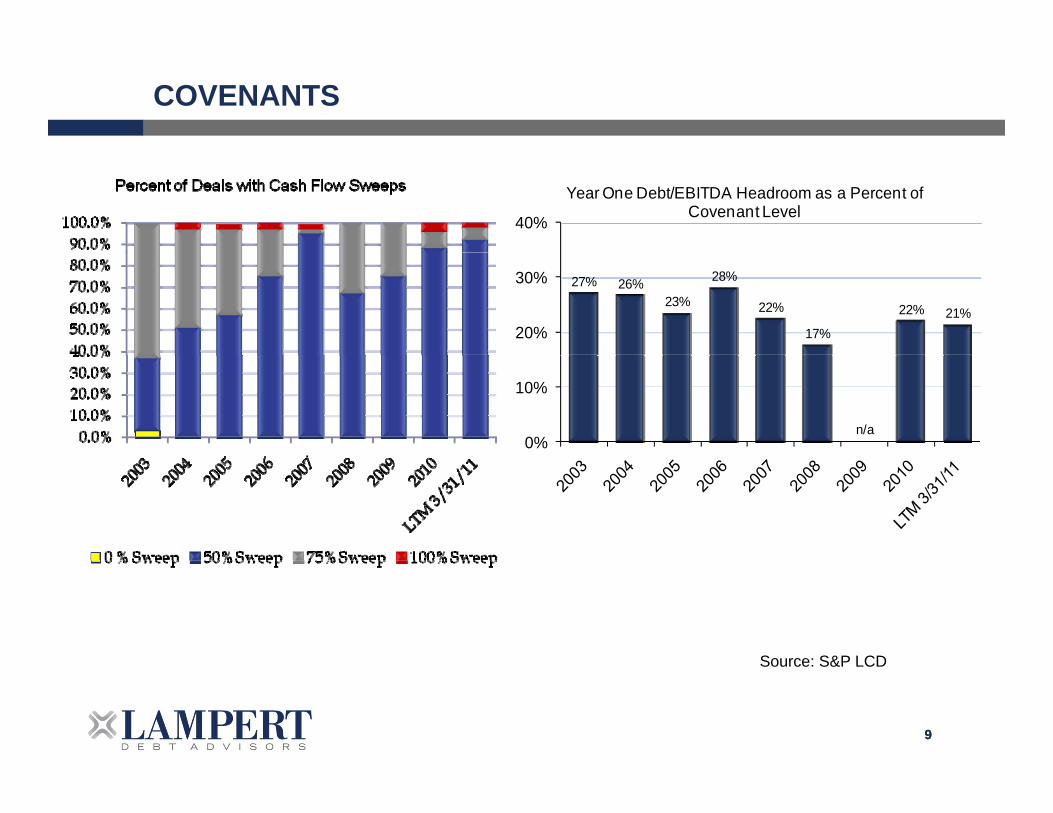

COVENANTS

40%

Year One Debt/EBITDA Headroom as a Percent of Covenant Level

27% 26%23%

28%

22%

17%

22% 21%20%

30%

n/a0%

10%

Source: S&P LCD

99

Source: S&P LCD

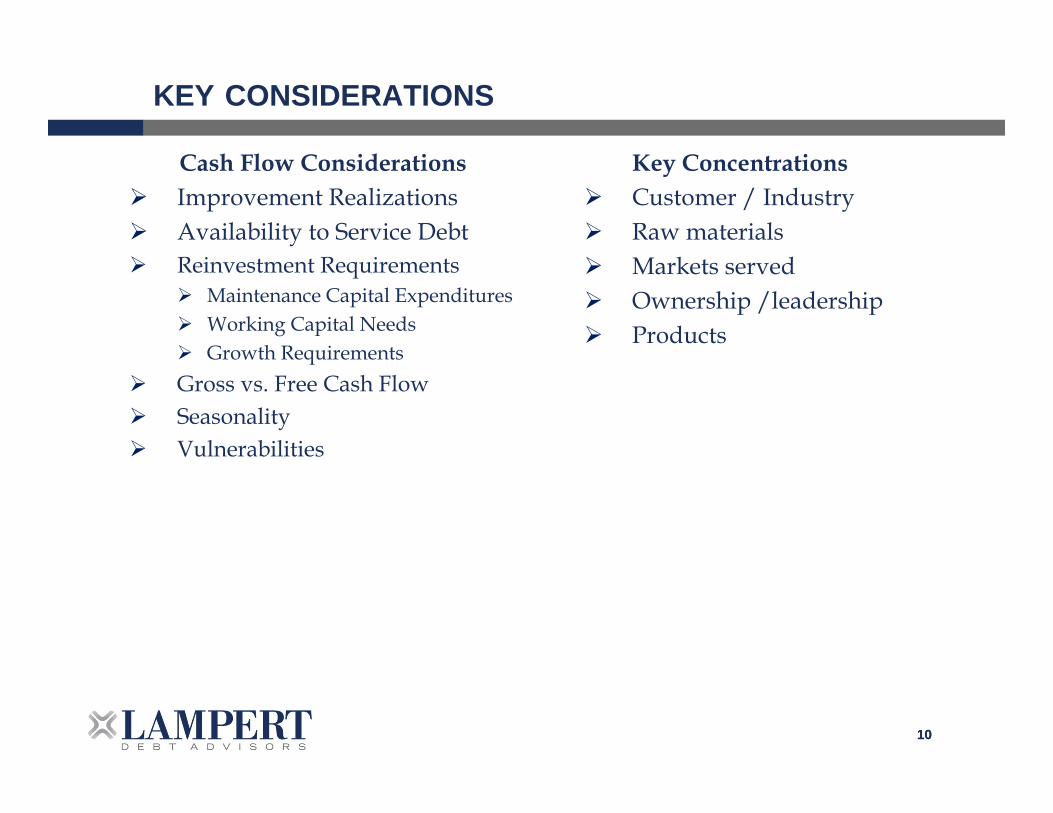

KEY CONSIDERATIONS

Cash Flow Considerations Improvement Realizations Availability to Service Debt

Key Concentrations Customer / Industry Raw materials

Reinvestment Requirements Maintenance Capital Expenditures Working Capital Needs Growth Requirements

Markets served Ownership /leadership Products

Growth Requirements Gross vs. Free Cash Flow Seasonality Vulnerabilities

1010

RISK PROFILE

V l tilit

Given the trials and tribulations of the past 3 years, lenders are placing heavy emphasis on risk and how it can be mitigated.

Volatility exposure Competitive exposure Input costs O t t i Output prices Asset deterioration Technological risk

In soliciting lenders, it is critically important for borrowers (and their important for borrowers (and their representatives) to mollify investor concerns early in the process

1111

CAPITALIZATION STRATEGY

Gear amortization to the specific cash flow characteristics of the borrower

Coordinate financing layers to fully benefit from Coo d ate a c g aye s to u y be e t o various classes of assets

Establish levels of leverage consistent with ownership’s risk toleranceownership s risk tolerance Ownership

Public vs. Private F Fi i l S C bili Future Financial Support Capability Track Record

Use wide, Auction Financing Process to drive: Lowest cost of capital – rates, fees Optimal terms and improved flexibility Looser covenants Looser covenants

1212

INVESTOR LANDSCAPE

%

100%

70%

80%

90%

50%

75%

30%

40%

50%

60%

70%

0%

25%

0%

10%

20%

30%

US Banks Finance Co.Foreign Bank Institutional InvestorSecurities Firm 2008 2009 2010 4Q10 1Q11Securities Firm

Source: S&P LCD

1313

Source: S&P LCD

OUR INVESTOR NETWORK

Banks

Fi C ’ T L

Revolver

LDA possesses a network of over500 investors across multipleclasses of debt and equity securities

Finance Co’s

CLO’s

BDC’s

Last Out Senior

Term Loan

classes of debt and equity securities.Our active dialogue with thesesources of capital provides us withreal-time market knowledge withrespect to key investment criteria

BDC s

Hedge Funds

Insurance Co’s

TLB

Second Lien TL

such as return, appetite andstructure requirements

Insurance Co s

Private Debt Funds

Mezzanine Funds

Sub Debt

Bridge Financing

Credit Oppty. Funds

Private Equity

Structured Equity

Common Equity

1414

y

DEBT FINANCING AUCTION PROCESS

•Real time knowledge of current market terms•Optimal structure based on market requirements and company needs•Identification of and solution to credit and transaction risks

Structure •Specific covenants and inter-creditor terms established upfront

•Rapid deployment and comprehensive solicitation of investors for each

Solicitation

p p y pfinancing layer

•Concentrated management meetings minimize distraction•Successfully secure multiple proposals and commitments•Secure “back-pocket” bids

•Seamless transition from commitment to closing•Reduction in closing surprises and elimination of “drift” in terms

Closingg p

•Increased likelihood of successful closing

1515

CONCLUSION

Most market participants expect to see M&A activity increase in the 2nd quarter

The supply/demand imbalance, particularly in the loan market, has given rise to tightened spreads and looser terms in the first 3 months of 2011; however, March saw investors push back on a number of very aggressive transactions

Geopolitical events occurring throughout the world and the natural disaster in Japan have created a degree of uncertainty in the long-term view of the economic recovery

Acquisition financing should remain readily available in 2011; however, proper alignment of deal characteristics and the financing being sought will be the main underpinning of

f ll fi d i itisuccessfully financed acquisitions

1616

Acquisition Financing: Strategies for q g gDeal Counsel

Evaluating Financing Options, Structuring the Deal, Addressing Loan Documentation and Intercreditor IssuesLoan Documentation and Intercreditor Issues

April 12, 2011

Lawrence F. Flick, II, Partner, Blank Rome, New York

212.885.5556 [email protected]@

Jeffrey A. Beuche, Partner, Perkins Coie, Denver

303 291 2321 JBe che@perkinscoie com303.291.2321 [email protected]

Structuring the Transaction• Cash Flow vs. ABL; Layers of Financing; y g

– During downturn, cash flow loans largely disappeared and traditional cash flow lenders became ABL lenders.

– Amend/extends often accompanied by conversion to ABL structure and/or additional covenants. Strongest borrowers were able to extend existing loans, reduce covenant h dl d i f ili i i hhurdles, and upsize facilities to continue growth.

– More cash flow deals getting done, but ABL deals still very common, especially in lower middle market.

– Important to understand real availability in ABL structures. Increasing lender discretion in borrowing base criteria versus borrower's desires for certain of access to capital.in borrowing base criteria versus borrower s desires for certain of access to capital.

– Split collateral package loans.– Increase in sponsors providing mezz/sub debt or even senior debt in order to more

quickly deploy capital; to be determined whether there will be an adequate supply of traditional lender loans to refinance sponsor financing.

• Use of holding companies– Important to understand lender's requirements around org chart early in process.– Most lenders require pledge of equity in borrower/operating company to facilitate

transfer of control in default situation (exercise of pledge rights vs. foreclosure on operating assets)

18

• Fraudulent transfer issues– Traditional lenders increasingly focused on issue, particularly as leverage levels

increase.

– Many approaches: Target as borrower, acquisition entity as borrower with target assuming obligations immediately upon closing, new strategies to limit loans made to operating subsidiaries, stronger solvency representations.

– Does not seem to be a standard approach at this time.pp

• Intercreditor issues– Many possible intercreditor issues, affecting subordinate and second lien lenders,

sponsors (relating to management fees), holders of seller notes and earnout recipients.

19

• Focus on when and to what extent subordinated lenders can exercise enforcement rights and the extent of the senior lender's ability to make decisions binding on subordinated lenders in enforcement proceedings.

• Subordinated lenders focused on an exit strategy, a seat at the table during enforcement proceedings, and objective asset valuations.

• Seller notes and earnouts are often deeply subordinated, which is a key issue to be handled; different approaches on timing of these discussionsto be handled; different approaches on timing of these discussions.

• Seller notes and earnouts often subject to refinancing indebtedness, further prolonging the lifecycle.

20

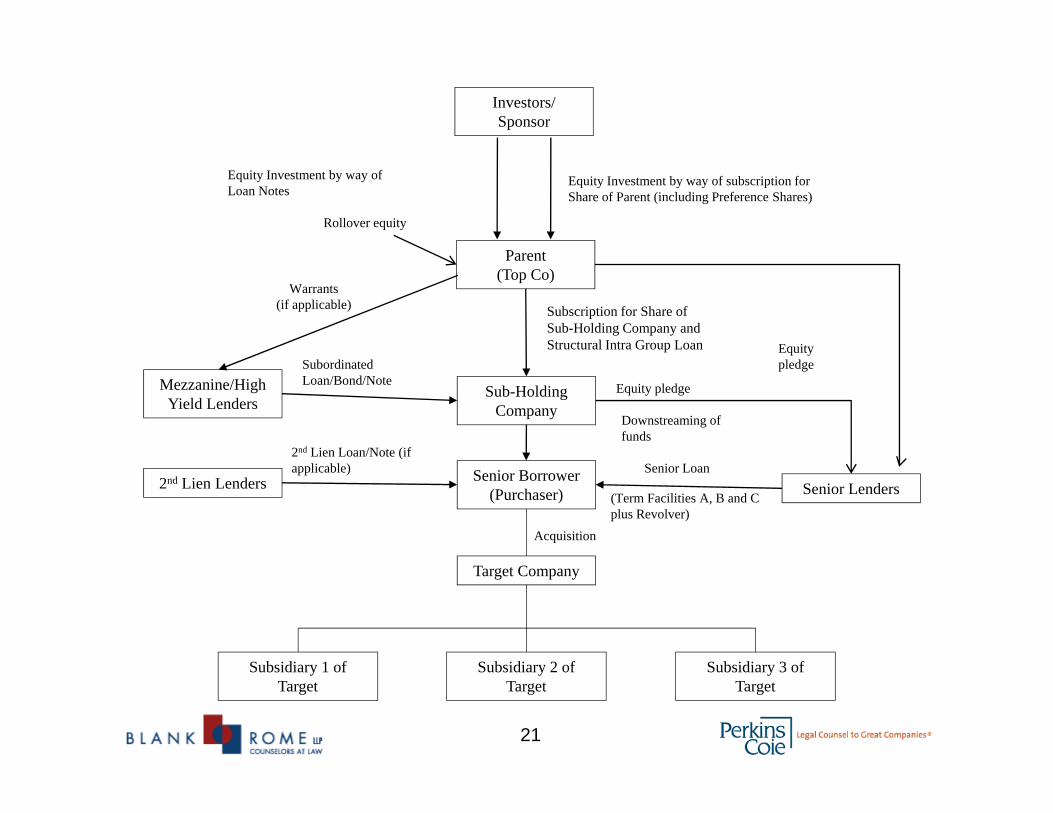

Investors/Sponsor

P t

Equity Investment by way of Loan Notes

Equity Investment by way of subscription for Share of Parent (including Preference Shares)

Rollover equity

Parent(Top Co)

Subscription for Share of Sub-Holding Company and Structural Intra Group Loan

Warrants (if applicable)

Equity

Sub-Holding Company

Mezzanine/High Yield Lenders

Subordinated Loan/Bond/Note

Downstreaming of funds

2nd Lien Loan/Note (if

q ypledge

Equity pledge

Senior Borrower (Purchaser) Senior Lenders2nd Lien Lenders

Senior Loan

Acquisition

(applicable)

(Term Facilities A, B and C plus Revolver)

Target Company

S b idi 1 f S b idi 2 f S b idi 3 f

21

Subsidiary 1 of Target

Subsidiary 2 of Target

Subsidiary 3 of Target

Commitment Letter Issues

• “SunGard” provisions

• Market flex provisions• Market flex provisions– Increased sponsor resistance given increased competition among

lenders.

– Certainty of deal terms and shifting some or all of the syndicationCertainty of deal terms and shifting some or all of the syndication risk to lenders is critical for many sponsors.

22

Documentation Issues• Financial covenant definitions

I d f li d h fl i i ( i– Increased sponsor focus on covenant compliance and cash‐flow sweep provisions (extensive negotiations on EBITDA add‐backs and other inputs driving covenant compliance and cash‐flow sweep numbers).

– Sponsor demands for flexibility to contribute additional capital without mandatory pre‐pays, undertake equipment and other operational financing options, and to execute growth strategy through add‐on acquisitionsthrough add on acquisitions.

– Trend towards negotiating definitions at term sheet/commitment letter stage.• Permitted acquisitions

– Often a critical negotiating point for sponsors, but rarely will lenders provide self‐executing carveouts from negative covenants for material transactions.F i th th th b k t b t li d d t f d t– Focus on issues other than the basket: can process be streamlined, amendment fees agreed to up front or waived, etc.

– For negative covenants generally, sponsor focus on avoiding yet another costly amendment: certainty on covenant compliance, flexibility for growth/ordinary course event, tying together negative covenants so that an exception to one is an exception to all, predetermined amendment fees for non default amendmentsfees for non‐default amendments.

• Permitted distributions– Rarely will pure dividends be permitted, but important to negotiate rights to make tax distributions.– Need to look up the org chart to understand the complete picture around tax distributions.– Consider need for carveouts in respect of dividend accruals on preferred stock, management fees,

earnouts and equity repurchases from departing employeesearnouts, and equity repurchases from departing employees.

23

• Equity cure rights• Equity cure rights– Sponsors have different strategies.– If included, negotiations around amount of cure permitted, number of cures

permitted, and time frame over which cure amounts included in covenant l l ticalculations.

• Solvency representations

D f l i l d i i• Defaulting lender provisions– Typical remedies.– Lead lender(s) commitment to make loans for defaulting lenders.– Impact on availability of swingline loans.

• Consents to assignments– Sponsor focus on the "relationship" and have approval right on new agent or

material change in inter‐lender provisions.Limitations on syndication– Limitations on syndication.

– Assignments during default.

24

• Foreign subsidiaries

• Lender remedies – rights to credit bidLender remedies rights to credit bid

25