Acquisition Finance in Brazil Considerations & Case Study · Acquisition Finance in Brazil...

18

Corporate & Investment Banking Deutsche Bank Acquisition Finance in Brazil Considerations & Case Study Considerations & Case Study October 2010

-

Upload

duongkhuong -

Category

Documents

-

view

217 -

download

0

Transcript of Acquisition Finance in Brazil Considerations & Case Study · Acquisition Finance in Brazil...

Corporate & Investment BankingDeutsche Bank

Acquisition Financein BrazilConsiderations & Case StudyConsiderations & Case StudyOctober 2010

Acquisition

Deutsche BankCorporate & Investment Banking

Acquisition Finance in BrazilConsiderations

Corporate & Investment BankingDeutsche Bank

1

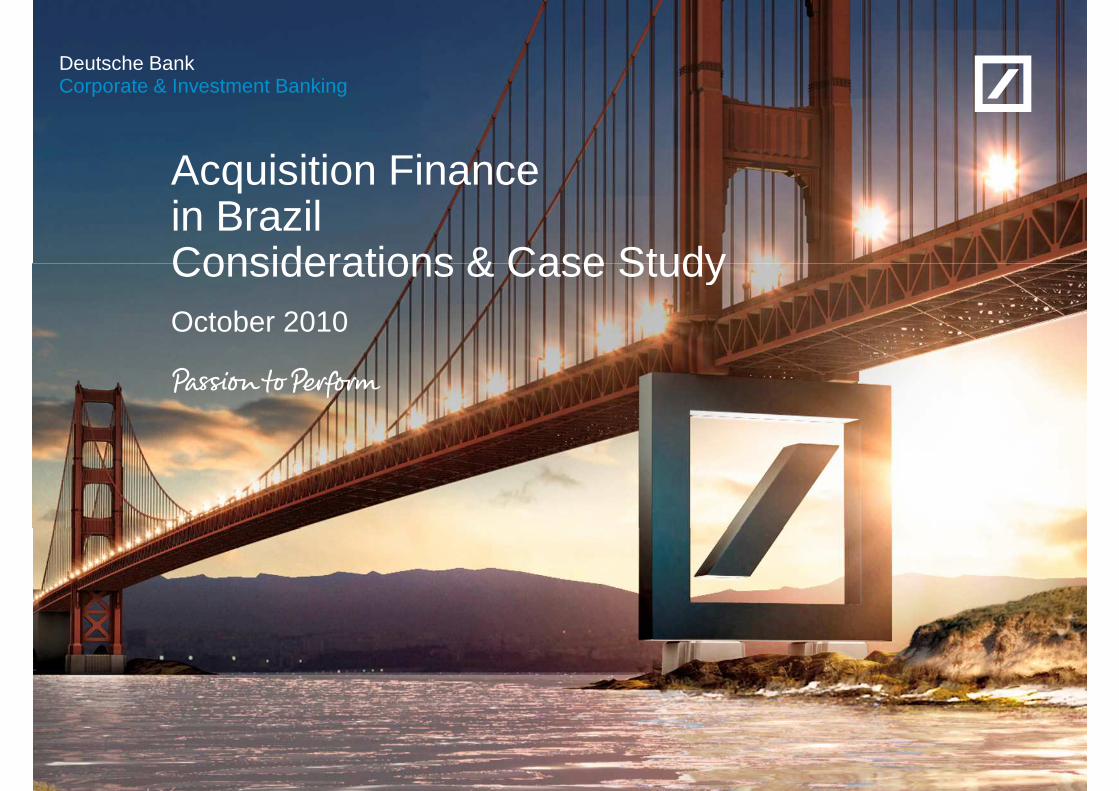

Deutsche Bank’s quest for leadership in Brazilian M&A

Ranking by volume (in USD mn) Deutsche Bank transactions in 2010YTD

1H 2010

1. Deutsche Bank 6,048

1. Deutsche Bank 6,048

2. Estáter 4,084

3. JP Morgan 3,642

4. BB 2,715

5. HSBC 2,654

6. Itaú BBA 2,445

7. Singular Partners 2,427

Devon Energy Corporation

USD7.0 billion

Sale of Devon’s offshore operations in

Brazil, operations in Azerbaijan and

deepwater business in Gulf of Mexico

to British Petroleum

March 2010

Brazil

Abengoa Brazil

BRL273.7 million

Sale of a 25% stake in ETEE and

ETIM to State Grid

May 2010

Brazil

Votorantim Cimentos

Brenco

Undisclosed Value

Merger of Brenco and ETH Bioenergia

February 2010

Brazil

Votorantim Cimentos Vale

Corporate & Investment BankingDeutsche Bank

Source: Anbima, announced transactions

Singular Partners 2,427

8. Rothschild 1,670

9. Santander 1,057

10. Bradesco BBI 1,052

EUR154 million

Acquisition of 3.9% stake in Cimpor

February 2010

Brazil

EUR717 million

Acquisition of 17.3% stake in Cimpor

from Lafarge

February 2010

Brazil

USD5.7 billion

Acquisition of Bunge's upstream

fertilizer assets and stake in Fosfertil

February 2010

Brazil

Regulatory framework – Financing in Brazil

� Tax on financings [“IOF”, Imposto sobre Operaçoes Financeiras] is at least 38bps flat

Principles

All financing subject to taxation

Operaçoes Financeiras] is at least 38bps flat

� Also applied to FX transactions (in and out)

� Also applied to short-term investments

Financing of exports is tax exempt

� No IOF tax on export financings� No IOF tax on FX for exports� No IOF tax on FX for imports of goods � But, IOF tax on imports of services

1.

2.

Corporate & Investment BankingDeutsche Bank

3

True sale of assets is tax exempt � No IOF tax on sale of receivables3.

Case study – Local tax impact on overdraft

Day 3Day 0 Day 20Day 17 Day 30Day 27

Example: Overdraft BRL 100,000

Balance0

Balance(100,000)

Interest20% p.a.=217

Balance0

Balance(100,000)

Interest20% p.a.=217

Balance0

Balance(100,000)

Interest20% p.a.=217

Interest

= 651

Corporate & Investment BankingDeutsche Bank

4

IOF + 380+ 3 * 4.10= 392

IOF + 380+ 3 * 4.10= 392

IOF + 380+ 3 * 4.10= 392

IOF

=1,176

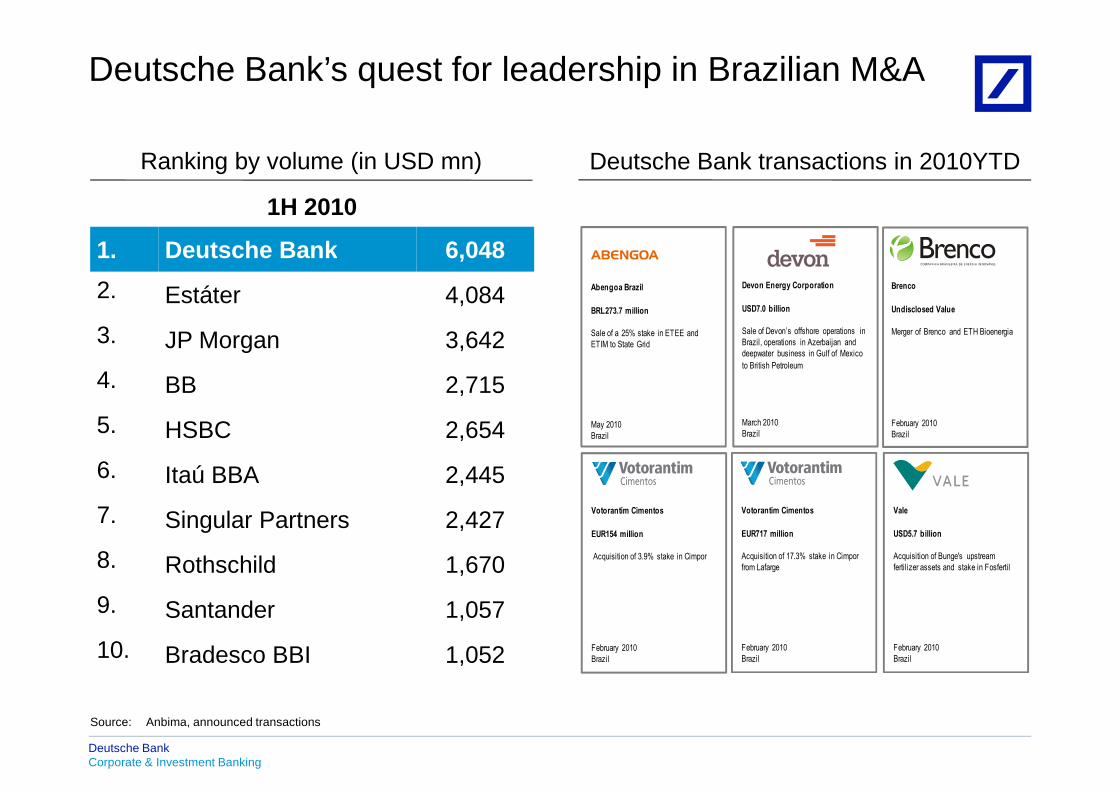

Export pre-shipment

(NCE/ACC)

Export post-

shipment (ACE)

Export Pre-

payment

Local Receivables

FinanceOverdraft Loan

Import Finance

Selected Financing Instruments – Brazil

(NCE/ACC)(ACE)

paymentFinance

BRL / Foreign

Currency

Foreign Currency

Foreign Currency

BRLBRL BRL

NCE any tenor

ACC max 360 days

Max 360 days

Any tenor(typically 3-5 years)

Any tenor (typically 180 days)

Typically less than 30 days

Any tenor

BRL / Foreign

Currency

Any tenor (typically 180 -360

days)

Corporate & Investment BankingDeutsche Bank

No IOF No IOF No IOFNo IOFIOF 38bps flat +0.41bps per

day

IOF 38bps flat +0.41bps per

day

Notes:

No IOF ¹)

Notes: 1) 15% Withholding tax on interest remittance

5

Acquisition

Deutsche BankCorporate & Investment Banking

Acquisition Finance in BrazilCase Study

Corporate & Investment BankingDeutsche Bank

6

Case Study – Georgsmarienhuette (GMH) (1)

GMH is active in: steel production, forging technology, railway systems and castings

Initial situation and challenges

Corporate & Investment BankingDeutsche Bank

10/1/2010 2010 DB Blue template

7

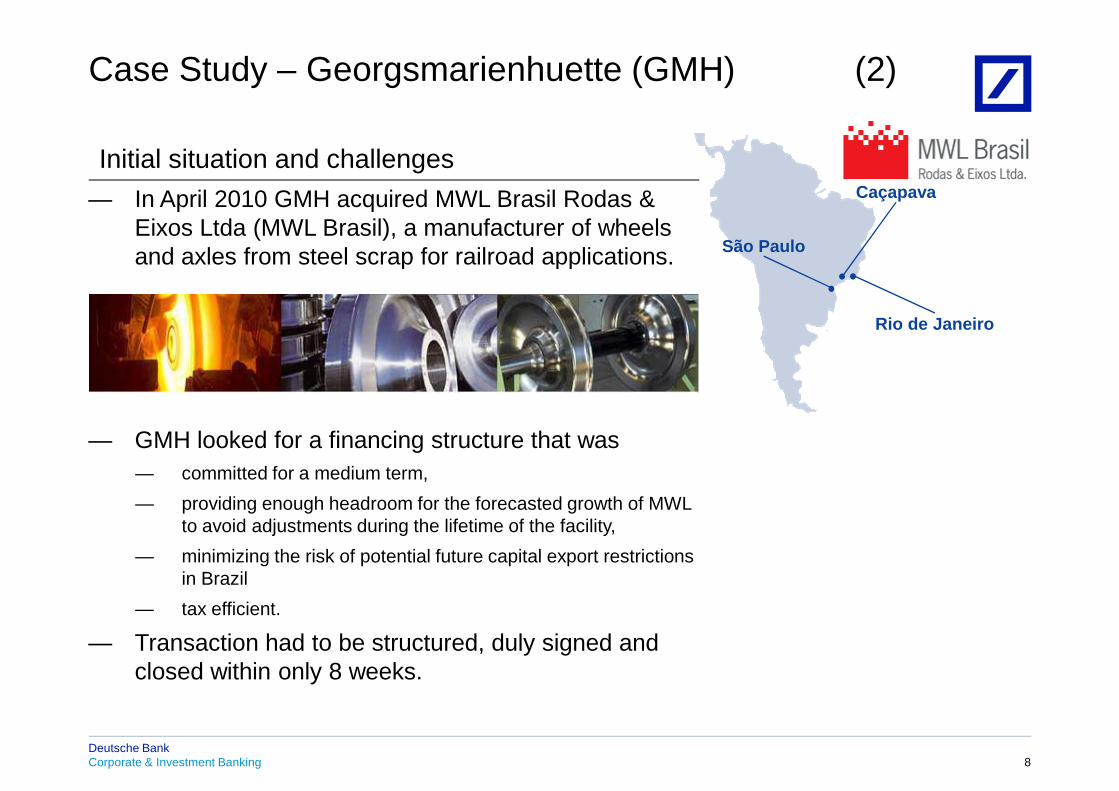

Case Study – Georgsmarienhuette (GMH) (2)

São Paulo

Caçapava— In April 2010 GMH acquired MWL Brasil Rodas & Eixos Ltda (MWL Brasil), a manufacturer of wheels and axles from steel scrap for railroad applications.

Initial situation and challenges

and axles from steel scrap for railroad applications.

— GMH looked for a financing structure that was— committed for a medium term,

— providing enough headroom for the forecasted growth of MWL to avoid adjustments during the lifetime of the facility,

Rio de Janeiro

Corporate & Investment BankingDeutsche Bank

10/1/2010 2010 DB Blue template

8

to avoid adjustments during the lifetime of the facility,

— minimizing the risk of potential future capital export restrictions in Brazil

— tax efficient.

— Transaction had to be structured, duly signed and closed within only 8 weeks.

Case Study – Georgsmarienhuette (GMH) (3)

— US$ 67.5mn bilateral Export Pre-payment (Prépagamento) facility

— Borrower: GMH Brasil Participações (GMH Brasil).

— Mandated lead arranger: Deutsche Bank

Solution

— Mandated lead arranger: Deutsche Bank

— Tenor: 4.5 years

— 2 Tranches:— Tranche A: US$ 30.0mn Revolving Working Capital Tranche

— Tranche B: US$ 37.5mn Amortizing Tranche

— Both tranches were structured under a Prépagamento structure with both the principal and interest of the loan repaid from the collection of exports receipts with a group of off-takers.

Corporate & Investment BankingDeutsche Bank

10/1/2010 2010 DB Blue template

9

— In addition the working capital facility is structured as a borrowing base facility with additional securities against inventory and receivables on a revolving basis. The other tranche amortises on a quarterly basis.

— No IOF-Tax applicable

Case Study – Georgsmarienhuette (GMH) (4)

— There are IOF-Tax efficient financing solutions

— Deutsche Bank has solutions to enhance Prépagamento structures to comply with growth and/or acquisition scenarios

Conclusion / Take aways

growth and/or acquisition scenarios

— Even complex transactions can be structured in a short time frame

— It is crucial to success that the client is well prepared and the Bank has to have a cross border Deal Team in place to comply with both brazilian and home country requirements

— To optimize handling of the structure the Mandated Bank should also be able to deliver world wide day to day business in the field of Trade Finance and Cash Management Solutions and Trust & Security Services

— DEUTSCHE BANK IS PREPARED TO DO SO!

Corporate & Investment BankingDeutsche Bank

10/1/2010 2010 DB Blue template

10

— DEUTSCHE BANK IS PREPARED TO DO SO!

Deutsche BankCorporate & Investment Banking

Deutsche Bankin South America

Corporate & Investment BankingDeutsche Bank

11

Global means global

Deutsche Bank in South America

— Deutsche Bank has know how of local markets

— Global availability of home credit facilities— Global availability of home credit facilities

— Top tier corporate & investment bank in Latin America

— Local corporate banking in Brazil and Argentina

— Dedicated staff for German & MNC subs in São Paulo and Buenos Aires

São Paulo

Rio de Janeiro (Q4 2010)

Santiago

Buenos Aires

Lima

Corporate & Investment BankingDeutsche Bank

12

Contacts

Burkhard Ziegenhorn

Head of Global Transaction Banking

Brazil

Luis E. Farina

Head of Corporate Banking Coverage

BrazilBrazil

�+55-11-2113-5496 [email protected]

Monica Andrade

Head of Corporate Banking Coverage

Uwe Hadeler

Director

Brazil

�+55-11-2113-5291 [email protected]

Corporate & Investment BankingDeutsche Bank

13

Corporate Banking CoverageGerman Desk Brazil

�+55-11-2113-5327 [email protected]

DirectorGerman MidCaps Osnabrueck

�+49(541)342-226 [email protected]

Appendix

Corporate & Investment BankingDeutsche Bank

10/1/2010 2010 DB Blue template

14

The Investment Banking team in Brazil was built in

2009

As a result of these

Deutsche Bank’s quest for leadership in Brazilian M&A

Brazilian target completed: ranking by volume in USD million Deutsche Bank transactions in 2010YTD

Devon Energy Corporation

USD7.0 billion

Abengoa Brazil

BRL273.7 million

2009 1H 2010

1. Itaú BBA 86,499 1. Deutsche Bank 6,048As a result of these

efforts, Deutsche Bank is already presenting solid results in 2010, having

advised 6 landmark transactions

Deutsche Bank named as the 2010 Best Global Investment

Bank by Euromoney

Sale of Devon’s offshore operations in

Brazil, operations in Azerbaijan and

deepwater business in Gulf of Mexico

to British Petroleum

March 2010

Brazil

Sale of a 25% stake in ETEE and

ETIM to State Grid

May 2010

Brazil

Votorantim Cimentos

EUR154 million

Acquisition of 3.9% stake in Cimpor

February 2010

Brazil

Brenco

Undisclosed Value

Merger of Brenco and ETH Bioenergia

February 2010

Brazil

2. Morgan Stanley 84,491 2. Estáter 4,084

3. Rothschild 78,935 3. JP Morgan 3,642

4. Unibanco 61,288 4. BB 2,715

5. Credit Suisse 28,857 5. HSBC 2,654

6. JP Morgan 26,365 6. Itaú BBA 2,445

7. Bradesco BBI 23,464 7. Singular Partners 2,427

8. Santander 22,124 8. Rothschild 1,670

Corporate & Investment BankingDeutsche Bank

Source: Anbima, announced transactions

2010

Votorantim Cimentos

EUR717 million

Acquisition of 17.3% stake in Cimpor

from Lafarge

February 2010

Brazil

Vale

USD5.7 billion

Acquisition of Bunge's upstream

fertilizer assets and stake in Fosfertil

February 2010

Brazil

9. BTG Pactual 20,568 9. Santander 1,057

10. BB 14,505 10. Bradesco BBI 1,052

(…)

24. Deutsche Bank 175

Deutsche Bank has participated in several

equity offerings in Latin America in the last few

years, with an impressive

Deutsche Bank’s Latin American equity offerings

JB S S.A . B anco Santander (B ras il) S .A .

N atura C o smet ico s SA

H ypermarcas SA B o lsa M exicana de Valo res

C resud S.A . R ipley C o rp S.A .

USD 915 millio n USD 7.5 billio n USD 796 millio n USD 398 mi llio n USD 375 millio n USD 288 millio n USD 161 millio n

years, with an impressive distribution track record

Follow-on Init ital Public Offering Follow-on Follow-on Init ital Public Of fering Rights Offering Follow-on

April 2010 October 2009 July 2009 July 2009 M ay 2008 M arch 2008 December 2007

B anco do B ras il B M &F B o vespa H o lding So co vesa S.A . Univ ers idade Estác io de Sá

B anco P atago nia N II H o ldings Inc

USD 2.0 billio n USD 3.4 billio n USD 3.7 billio n USD 161 mi llio n USD 390 millio n USD 260 millio n USD 1.2 billio n

Follow-on Init ital Public Offering Init ial Public Offering Init ial Public Offering Init ial Public Offering Init ial Public Of fering Convertible Senior Notes

December 2007 November 2007 October 2007 October 2007 July 2007 July 2007 M ay 2007

Corporate & Investment BankingDeutsche Bank

Lo g- in – Lo gis t ica Intermo dal S / A

LA N A irlines S.A . M eta lf rio IT So lut io ns

São M art inho P D G R ealty S.A . P o sit ivo Info rmat ica S.A .

Odo nto prev S.A .

UD S392millio n USD 181 millio n USD 250 millio n USD 175 mil lio n USD 295 millio n USD 264 millio n USD 210 millio n

Init ial Public Of fering Follow-on Init ial Public Offering Init ial Public Offering Init ial Public Offering Init ial Public Of fering Init ial Public Of fering

June 2007 M ay 2007 April 2007 February 2007 January 2007 December 2006 November 2006

Brazil Brazil Brazil Brazil Brazil

"This document is intended for discussion purposes only and does not create any legally binding obligations on the part ofDeutsche Bank AG and/or its affiliates (“DB”). Without limitation, this document does not constitute an offer, an invitation to offer ora recommendation to enter into any transaction. When making an investment decision, you should rely solely on the finaldocumentation relating to the transaction and not the summary contained herein. DB is not acting as your financial adviser or indocumentation relating to the transaction and not the summary contained herein. DB is not acting as your financial adviser or inany other fiduciary capacity with respect to this proposed transaction. The transaction(s) or products(s) mentioned herein may notbe appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understandthe transaction and have made an independent assessment of the appropriateness of the transaction in the light of your ownobjectives and circumstances, including the possible risks and benefits of entering into such transaction. You should also considerseeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with DB, you do so inreliance on your own judgment. The information contained herein does not constitute and shall not be construed to constitute legaland/or tax advice by Deutsche Bank AG or any of its affiliates. Individuals should consult with their advisors regarding theirparticular situation. The information contained in this document is based on material we believe to be reliable; however, we do notrepresent that it is accurate, current, complete, or error free. Assumptions, estimates and opinions contained in this documentconstitute our judgment as of the date of the document and are subject to change without notice. Any projections are based on anumber of assumptions as to market conditions and there can be no guarantee that any projected results will be achieved. Pastperformance is not a guarantee of future results. DB may engage in transactions in a manner inconsistent with the views discussedherein. DB trades or may trade as principal in the instruments (or related derivatives), and may have proprietary positions in theinstruments (or related derivatives) discussed herein. DB may make a market in the instruments (or related derivatives) discussed

Corporate & Investment BankingDeutsche Bank

instruments (or related derivatives) discussed herein. DB may make a market in the instruments (or related derivatives) discussedherein. The distribution of this document and availability of these products and services in certain jurisdictions may be restricted bylaw. You may not distribute this document, in whole or in part, without our express written permission. DB SPECIFICALLYDISCLAIMS ALL LIABILITY FOR ANY DIRECT, INDIRECT, CONSEQUENTIAL OR OTHER LOSSES OR DAMAGES INCLUDINGLOSS OF PROFITS INCURRED BY YOU OR ANY THIRD PARTY THAT MAY ARISE FROM ANY RELIANCE ON THISDOCUMENT OR FOR THE RELIABILITY, ACCURACY, COMPLETENESS OR TIMELINESS THEREOF. DB is authorised and/orregulated by the competent authorities in the jurisdictions in which it operates as appropriate."

17