ACHC Implementation Guide

30

ACH Implementation Guide ACH Commerce, LLC 8920 B Transport Lane, Suite 1 Ooltewah, TN 37363 800-724-8780 – Toll Free 423-238-5187 – Fax

description

Critical to smooth acceptance of payment instruments

Transcript of ACHC Implementation Guide

ACH Implementation Guide

ACH Commerce, LLC 8920 B Transport Lane, Suite 1

Ooltewah, TN 37363

800-724-8780 – Toll Free 423-238-5187 – Fax

ACH Commerce Implementation Guide Page - 2 -

TABLE OF CONTENTS

ACH PARTICIPANTS.......................................................................... 4

ACH TRANSACTION TYPES ............................................................ 5

TRANSACTION CREATION & DELIVERY OPTIONS................ 9

SENDING A FILE FOR PROCESSING........................................... 15

AUTHENTICATION AND VERIFICATION SERVICES................. 17

AUTHORIZATIONS & DISCLOSURES......................................... 19

TIMING................................................................................................. 22

MANAGING ACH RETURN ITEMS............................................... 25

RETRIEVING YOUR RETURN FILES........................................... 26

REPORTS & SPECIAL SERVICES ................................................. 28

CONTACT INFORMATION............................................................. 30

ACH Commerce Implementation Guide Page - 3 -

INTRODUCTION

Thank you for choosing ACH Commerce, LLC as your ACH service provider. We are dedicated to providing you with excellent customer service throughout our relationship. We have created numerous tools and methods to allow you to create and transmit a variety of ACH transactions. The implementation guide will introduce each transaction creation and delivery option in order to help you determine which method will work best for your business. This guide will also:

• Introduce the participants of the ACH network • Describe the various types of ACH transactions • Introduce authorization and disclosure requirements • Introduce the current authentication and verification tools offered by ACH Commerce • Provide samples for each authorization and disclosure requirement • Address timing of transaction delivery, returns and settlement • Explain the various file creation and transmission methods offered by ACH Commerce • Provide instructions to securely send and receive information to ACH Commerce • Discuss ACH returns • Provide sample reports and confirmations • Present special services offered by ACH Commerce • Provide ACH Commerce contact information

If you have any questions when reviewing the guide, please feel free to contact us via telephone at 423-238-5184 or via e-mail at [email protected]. We look forward to a long and mutually beneficial relationship.

ACH Commerce Implementation Guide Page - 4 -

ACH PARTICIPANTS

Originator – (Your Company) The originator is the entity that agrees to initiate ACH entries into the payment system according to an arrangement with a Receiver. The Originator is usually a company directing a transfer from a consumer’s or another company’s account. Third Party Service Provider -(ACH Commerce, LLC) The entity that acts as the collection point for transactions created by the Originator and then forwards the transactions to the ACH Operator on behalf of the ODFI. Originating Depository Financial Institution -(ODFI) – The ODFI is the financial institution that warrants all transactions created by the Originator that are forwarded to the ACH Operator. ACH Operator -(Federal Reserve Bank) – An Automated Clearing House (ACH) Operator is the central clearing facility operated by EPN or the Federal Reserve Bank. The ACH Operator performs the settlement function and transaction delivery between ODFI’s and RDFI’s. Receiving Depository Financial Institution (RDFI) -(Your Customers Bank) – The Receiving Depository Financial Institution is the financial institution that receives ACH entries from the ACH Operator and posts the entries to the accounts of its’ depositors (Receivers). Receiver –(Your Customer)- A Receiver is a natural person or an organization that has authorized an Originator to create an ACH entry to their account with the RDFI. A Receiver may be either a company or a consumer, depending on the type of transaction.

NACHA –(National Automated Clearing House Association)-The entity that governs the framework and the Rules of the ACH network. All participants are obligated by legal agreement to abide by the Rules set forth by NACHA.

ACH Commerce Implementation Guide Page - 5 -

ACH TRANSACTION TYPES

ACH transaction types are easily identified by (SEC) or Standard Entry Class Code. Proper use of SEC codes is crucial in insuring that your company and the ODFI are in compliance with NACHA rules. Each SEC code has different rules, authorization and/or disclosure requirements. Samples can be found in the section entitled Authorizations & Disclosures. Below you will find a list of transaction types, (with referenced SEC code), that are supported by ACH Commerce, LLC. Direct Debit & Direct Deposit = (PPD-Prearranged Payment/Deposit)

• Direct Debit-Your company (Originator) may debit the account of your customer (Receiver) for goods or services as they become due, provided you have obtained written authorization from your customer.

• Direct Deposit-Your company (Originator) may credit the account of your employees or customers (Receiver) for payroll, interest, dividends or pensions. Although written authorization is not required, it is recommended as a method of obtaining valid routing and account numbers.

• This type of transaction can only be submitted to Consumer accounts. Corporate Collection/Payment = (CCD Corporate Cash Deposit/Disbursement)

• CCD-Your company (Originator) can collect, distribute or consolidate funds between corporate entities provided that you have obtained written authorization or have an agreement in place with the corporate entity.

• This type of transaction can only be submitted to Corporate accounts.

Check Conversion-Mail In/Drop Box = (ARC-Accounts Receivable Conversion) • ARC-Your company (Originator), may convert checks received by mail or in a drop box

from your customers (Receivers) into ACH items, provided that you: o Properly disclose this practice on your invoice, statement or agreement o Retain an image of the front and back of the check for 2 years o Destroy the paper item after 14 days o DO NOT convert Corporate Checks, Money Orders, Cashiers Checks or

Third Party Checks

Check Conversion-In Person = (POP- Point of Purchase Check Conversion) • POP-Your company (Originator) may convert checks presented in person by your

customers (Receiver) into ACH items, provided that you: o Capture MICR information with an electronic device o Void the check and give back to the customer upon receipt o DO NOT convert Corporate Checks, Money Orders, Cashiers Checks or

Third Party Checks

ACH Commerce Implementation Guide Page - 6 -

Telephone Check = (TEL-Telephone Initiated Entry) • TEL-Your company (Originator) can accept payments over the phone from your

customers (Receiver) using their savings or checking account information when there is either;

o An existing relationship between your company (Originator) and your customer (Receiver).

o No existing relationship between the Originator and Receiver, but the Receiver has initiated the telephone call.

o Oral authorization is obtained via recording or notice is sent prior to debit entry posting to customers account.

o TEL entries are for one-time payments, recurring payments authorized in this manner are not permitted.

On-Line Check Acceptance = (WEB-Web Initiated Entry) • WEB-Your company (Originator) can accept payments, both single or recurring, over

the Internet from your customers (Receiver) using their savings or checking account information provided that you;

o Obtain electronic authorization by posting of appropriate disclosure on the site. o Have incorporated commercially reasonable authentication and verification

methods. o Are providing a secure session for the transaction.

Electronically Collect NSF Paper Checks = (RCK-Returned Check Re-Presentment) • RCK-Your company (Originator) can collect paper checks that have been returned for

NSF or Uncollected funds by creating an ACH item provided that you; o Post signage at the point of sale indicating that if a check is returned it will be

collected electronically. o Initiate the item for the face value of the check only o DO NOT DEPOSIT the paper item after you have created an electronic

item. o DO NOT attempt to collect Corporate Checks electronically

• NSF fees may be collected electronically, however the NSF fee must be created as a PPD entry and written authorization must have been obtained at the point the check was presented.

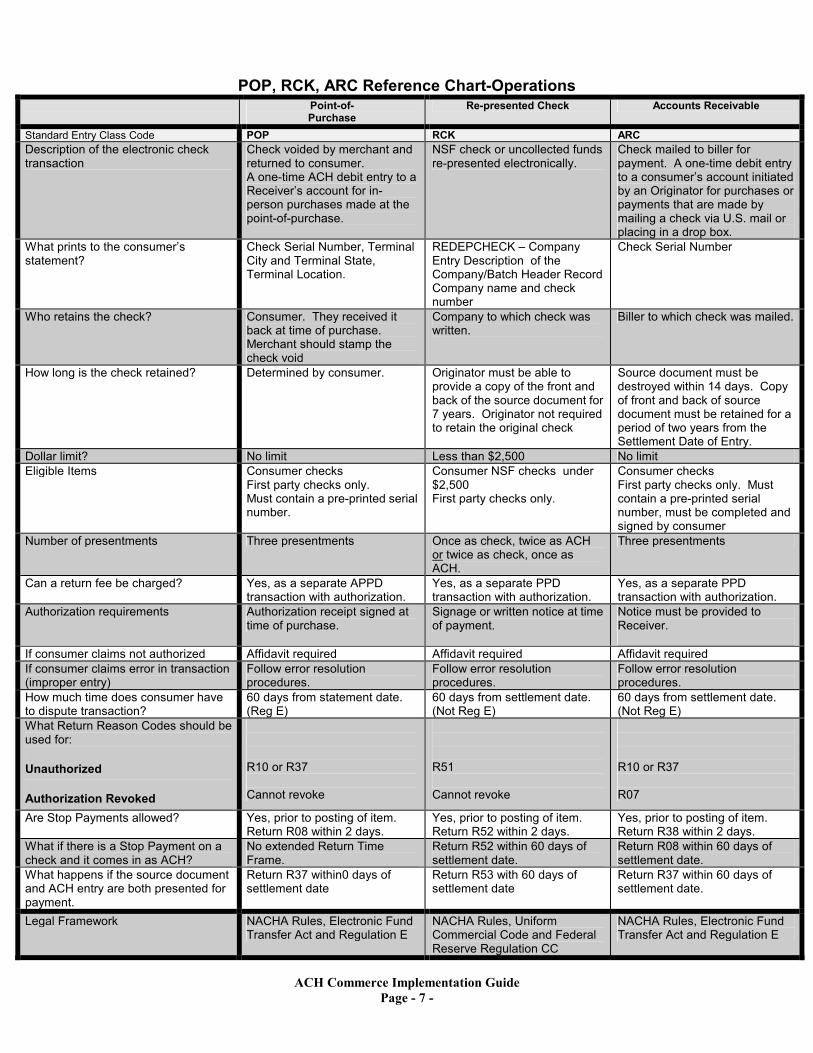

The following quick reference guides are designed to provide additional information regarding POP, RCK, ARC, TEL & WEB entries.

ACH Commerce Implementation Guide Page - 7 -

POP, RCK, ARC Reference Chart-Operations Point-of- Purchase

Re-presented Check Accounts Receivable

Standard Entry Class Code POP RCK ARC Description of the electronic check transaction

Check voided by merchant and returned to consumer. A one-time ACH debit entry to a Receiver’s account for in-person purchases made at the point-of-purchase.

NSF check or uncollected funds re-presented electronically.

Check mailed to biller for payment. A one-time debit entry to a consumer’s account initiated by an Originator for purchases or payments that are made by mailing a check via U.S. mail or placing in a drop box.

What prints to the consumer’s statement?

Check Serial Number, Terminal City and Terminal State, Terminal Location.

REDEPCHECK – Company Entry Description of the Company/Batch Header Record Company name and check number

Check Serial Number

Who retains the check? Consumer. They received it back at time of purchase. Merchant should stamp the check void

Company to which check was written.

Biller to which check was mailed.

How long is the check retained? Determined by consumer. Originator must be able to provide a copy of the front and back of the source document for 7 years. Originator not required to retain the original check

Source document must be destroyed within 14 days. Copy of front and back of source document must be retained for a period of two years from the Settlement Date of Entry.

Dollar limit? No limit Less than $2,500 No limit Eligible Items Consumer checks

First party checks only. Must contain a pre-printed serial number.

Consumer NSF checks under $2,500 First party checks only.

Consumer checks First party checks only. Must contain a pre-printed serial number, must be completed and signed by consumer

Number of presentments Three presentments Once as check, twice as ACH or twice as check, once as ACH.

Three presentments

Can a return fee be charged? Yes, as a separate APPD transaction with authorization.

Yes, as a separate PPD transaction with authorization.

Yes, as a separate PPD transaction with authorization.

Authorization requirements Authorization receipt signed at time of purchase.

Signage or written notice at time of payment.

Notice must be provided to Receiver.

If consumer claims not authorized Affidavit required Affidavit required Affidavit required If consumer claims error in transaction (improper entry)

Follow error resolution procedures.

Follow error resolution procedures.

Follow error resolution procedures.

How much time does consumer have to dispute transaction?

60 days from statement date. (Reg E)

60 days from settlement date. (Not Reg E)

60 days from settlement date. (Not Reg E)

What Return Reason Codes should be used for:

Unauthorized

Authorization Revoked

R10 or R37

Cannot revoke

R51

Cannot revoke

R10 or R37

R07

Are Stop Payments allowed? Yes, prior to posting of item. Return R08 within 2 days.

Yes, prior to posting of item. Return R52 within 2 days.

Yes, prior to posting of item. Return R38 within 2 days.

What if there is a Stop Payment on a check and it comes in as ACH?

No extended Return Time Frame.

Return R52 within 60 days of settlement date.

Return R08 within 60 days of settlement date.

What happens if the source document and ACH entry are both presented for payment.

Return R37 within0 days of settlement date

Return R53 with 60 days of settlement date

Return R37 within 60 days of settlement date.

Legal Framework NACHA Rules, Electronic Fund Transfer Act and Regulation E

NACHA Rules, Uniform Commercial Code and Federal Reserve Regulation CC

NACHA Rules, Electronic Fund Transfer Act and Regulation E

ACH Commerce Implementation Guide Page - 8 -

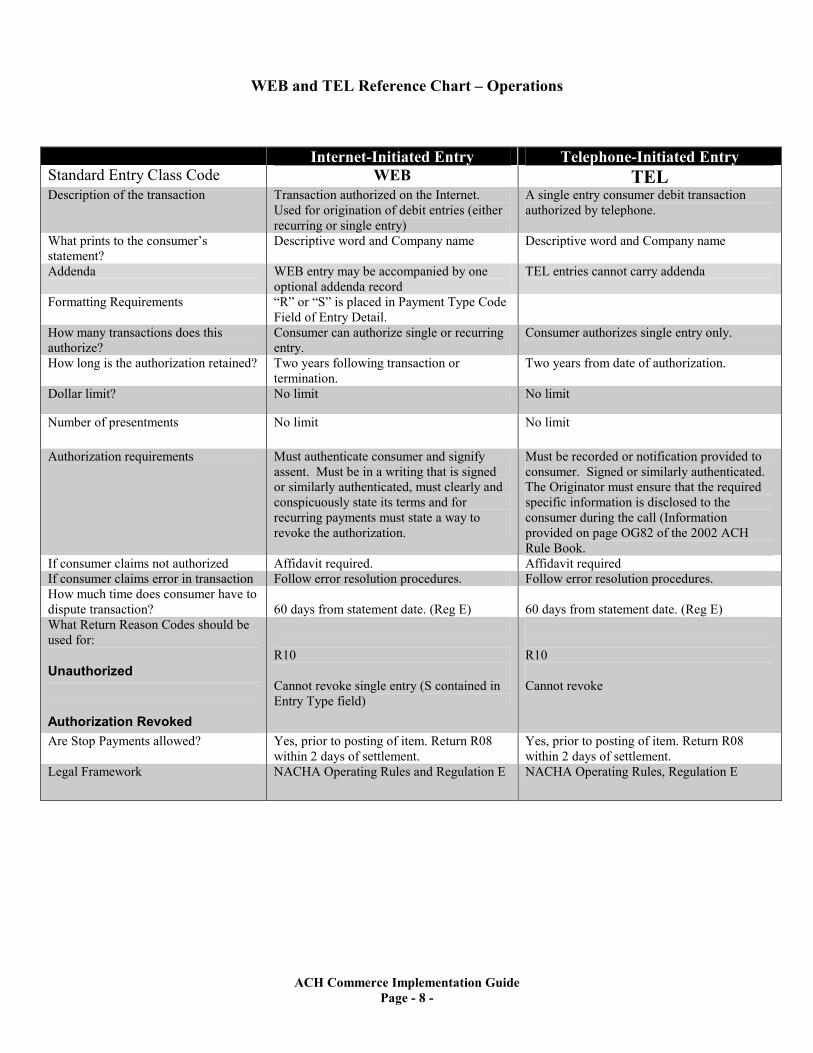

WEB and TEL Reference Chart – Operations

Internet-Initiated Entry Telephone-Initiated Entry Standard Entry Class Code WEB TEL Description of the transaction Transaction authorized on the Internet.

Used for origination of debit entries (either recurring or single entry)

A single entry consumer debit transaction authorized by telephone.

What prints to the consumer’s statement?

Descriptive word and Company name Descriptive word and Company name

Addenda WEB entry may be accompanied by one optional addenda record

TEL entries cannot carry addenda

Formatting Requirements “R” or “S” is placed in Payment Type Code Field of Entry Detail.

How many transactions does this authorize?

Consumer can authorize single or recurring entry.

Consumer authorizes single entry only.

How long is the authorization retained? Two years following transaction or termination.

Two years from date of authorization.

Dollar limit? No limit No limit

Number of presentments No limit No limit

Authorization requirements Must authenticate consumer and signify assent. Must be in a writing that is signed or similarly authenticated, must clearly and conspicuously state its terms and for recurring payments must state a way to revoke the authorization.

Must be recorded or notification provided to consumer. Signed or similarly authenticated. The Originator must ensure that the required specific information is disclosed to the consumer during the call (Information provided on page OG82 of the 2002 ACH Rule Book.

If consumer claims not authorized Affidavit required. Affidavit required If consumer claims error in transaction Follow error resolution procedures. Follow error resolution procedures. How much time does consumer have to dispute transaction?

60 days from statement date. (Reg E)

60 days from statement date. (Reg E)

What Return Reason Codes should be used for:

Unauthorized

Authorization Revoked

R10

Cannot revoke single entry (S contained in Entry Type field)

R10

Cannot revoke

Are Stop Payments allowed? Yes, prior to posting of item. Return R08 within 2 days of settlement.

Yes, prior to posting of item. Return R08 within 2 days of settlement.

Legal Framework NACHA Operating Rules and Regulation E NACHA Operating Rules, Regulation E

ACH Commerce Implementation Guide Page - 9 -

TRANSACTION CREATION & DELIVERY OPTIONS

Transaction Creation

ACH Commerce provides a variety of web-based applications to create and deliver ACH transactions. These are ACHStation©, which supports PPD, CCD and TEL entries for one time, recurring and batch transactions and MobileScan© which supports creation of ARC, POP and RCK transactions. User documentation for these products can be found at http://www.achcommerce.com/support.

However, if your system can create an ACH formatted file, simply deliver it to us for processing. If your system can export data, send it to us and we can provide conversion assistance. ACHStation© ACH Commerce provides a solution for companies that want to create

single, recurring or a batch of transactions. Our Web Based Entry solution allows a user or multiple users to effortlessly enter basic customer information to initiate ACH transactions. ACHStation© is located at gateway.achcommerce.com

ACH Mobile Scan© MobileScan© is a web based check conversion application hosted by ACH Commerce. MobileScan© allows companies to convert paper checks into ACH, image items and capture remittance data using a Mag-Tek or RDM scanning device. ACH Commerce can provide the company with ACH processing services through the Federal Reserve Bank, or simply provide an ACH formatted file for processing through their own financial institution.

ACH Format Most payroll systems can generate a direct deposit file in ACH format. Some accounting systems have this capability to generate direct debit entries. For companies that opt to use this format, specifications for file creation can be found in the ACH Rule Book available for purchase at www.nacha.org

PSV Format ACH Commerce can support conversion of data received in Pipe Separated Value format into ACH format for processing. A sample of this format is shown below:

ACH Commerce Implementation Guide Page - 10 -

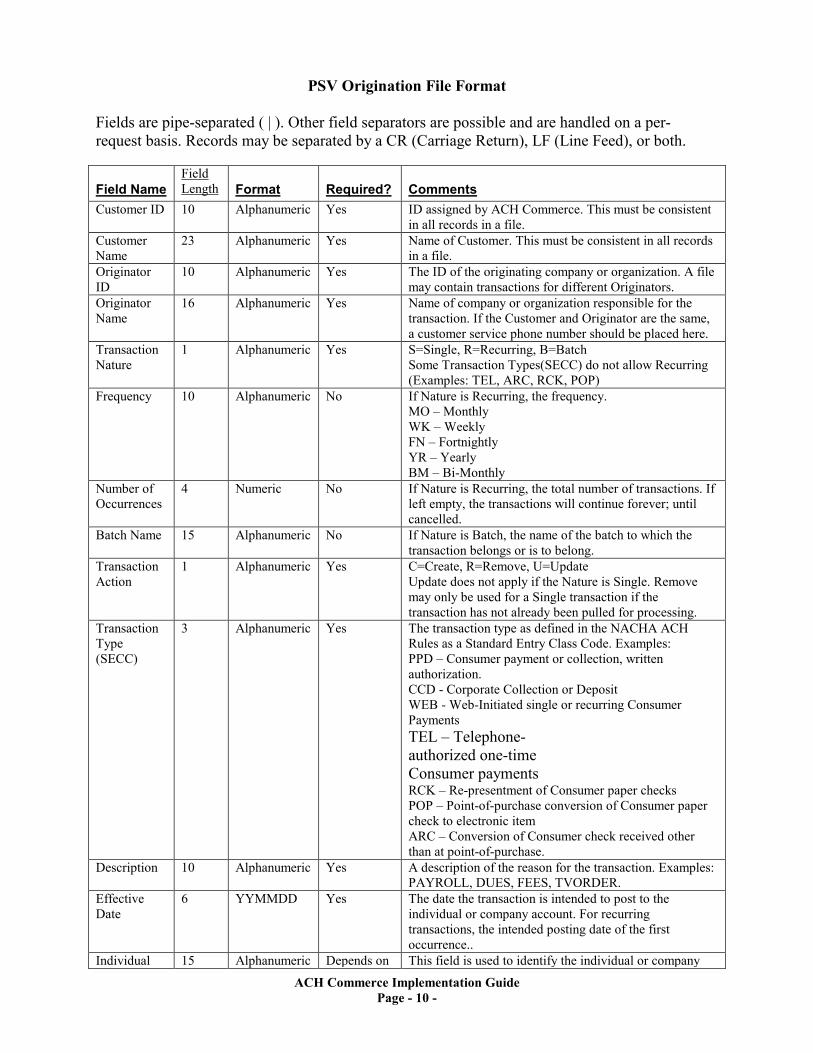

PSV Origination File Format Fields are pipe-separated ( | ). Other field separators are possible and are handled on a per-request basis. Records may be separated by a CR (Carriage Return), LF (Line Feed), or both.

Field NameField Length Format Required? Comments

Customer ID 10 Alphanumeric Yes ID assigned by ACH Commerce. This must be consistent in all records in a file.

Customer Name

23 Alphanumeric Yes Name of Customer. This must be consistent in all records in a file.

Originator ID

10 Alphanumeric Yes The ID of the originating company or organization. A file may contain transactions for different Originators.

Originator Name

16 Alphanumeric Yes Name of company or organization responsible for the transaction. If the Customer and Originator are the same, a customer service phone number should be placed here.

Transaction Nature

1 Alphanumeric Yes S=Single, R=Recurring, B=Batch Some Transaction Types(SECC) do not allow Recurring (Examples: TEL, ARC, RCK, POP)

Frequency 10 Alphanumeric No If Nature is Recurring, the frequency. MO – Monthly WK – Weekly FN – Fortnightly YR – Yearly BM – Bi-Monthly

Number of Occurrences

4 Numeric No If Nature is Recurring, the total number of transactions. If left empty, the transactions will continue forever; until cancelled.

Batch Name 15 Alphanumeric No If Nature is Batch, the name of the batch to which the transaction belongs or is to belong.

Transaction Action

1 Alphanumeric Yes C=Create, R=Remove, U=Update Update does not apply if the Nature is Single. Remove may only be used for a Single transaction if the transaction has not already been pulled for processing.

Transaction Type (SECC)

3 Alphanumeric Yes The transaction type as defined in the NACHA ACH Rules as a Standard Entry Class Code. Examples: PPD – Consumer payment or collection, written authorization. CCD - Corporate Collection or Deposit WEB - Web-Initiated single or recurring Consumer Payments TEL – Telephone-authorized one-time Consumer payments RCK – Re-presentment of Consumer paper checks POP – Point-of-purchase conversion of Consumer paper check to electronic item ARC – Conversion of Consumer check received other than at point-of-purchase.

Description 10 Alphanumeric Yes A description of the reason for the transaction. Examples: PAYROLL, DUES, FEES, TVORDER.

Effective Date

6 YYMMDD Yes The date the transaction is intended to post to the individual or company account. For recurring transactions, the intended posting date of the first occurrence..

Individual 15 Alphanumeric Depends on This field is used to identify the individual or company

ACH Commerce Implementation Guide Page - 11 -

ID SECC being debited or credited. Examples might be a person’s account number at a utility company, or the number of an invoice being paid. This is not required for POP,RCK, and ARC transactions.

Name 22 Alphanumeric Depends on SECC

Name of the individual or company being debited or credited. This is not required for POP and ARC transactions.

Routing# 9 Numeric Yes Routing/ABA number of the individual or company bank. Must be 9 characters in length.

Account# 17 Alphanumeric Yes The account number at the individual or company bank that is to be debited or credited.

Account Action

3 Alphanumeric Yes DR – Debit (Collect) CR – Credit (Pay-out) DRP – Debit Pre-Note CRP – Credit Pre-Note

Account Type

2 Alphanumeric Yes CK – Checking SV – Savings GL – General Ledger LN – Loan

Amount 11 Numeric Yes Amount may include only 2 decimal places. The amount must be zero for Actions DRP and CRP and cannot be zero for CR or DR.

Check # 9 Numeric Depends on SECC

The Check number as captured for RCK, ARC, and POP transactions. Not required for other SEC.

Terminal City

4 Alphanumeric Depends on SECC

An abbreviation for the city where the Point-of-Sale terminal is located. Required for POP transactions.

Terminal State

2 Alphabetic Depends on SECC

The two-character abbreviation for the state where the Point-of-Sale terminal is located. Required for POP transactions.

Transaction ID

20 Alphanumeric Depends on Action

The unique ID assigned to this transaction by the Customer or Originator. This can be used to maintain a unique tracking mechanism between Originated and Return files.

ACH Commerce Implementation Guide Page - 12 -

Transaction Delivery

ACH Commerce, LLC provides two secure methods for transaction delivery. ACHTransit© If your company would like to take advantage of real-time transaction

delivery and verification, ACHTransit© is our solution for server-to-server communication via secure HTTPS post. Detailed specifications for ACH Transit can be found at http://www.achcommerce.com/support

ACH Transport© ACHTransport© allows you to upload your electronic files, either ACH formatted or exported data files, to ACH Commerce via the Internet using secure FTP transmission. Electronic return files will also be downloaded using this same method. Complete documentation for using this method of transmission and obtaining return files can be found in the Guide to Managing ACH Returns or at http://www.achcommerce.com/support.

Electronic files must be accompanied by a transmittal form when using ACHTransport©..Please remember to email a completed transmittal form to [email protected] you submit an electronic file for processing. A sample transmittal is shown below:

ACH Commerce Implementation Guide Page - 13 -

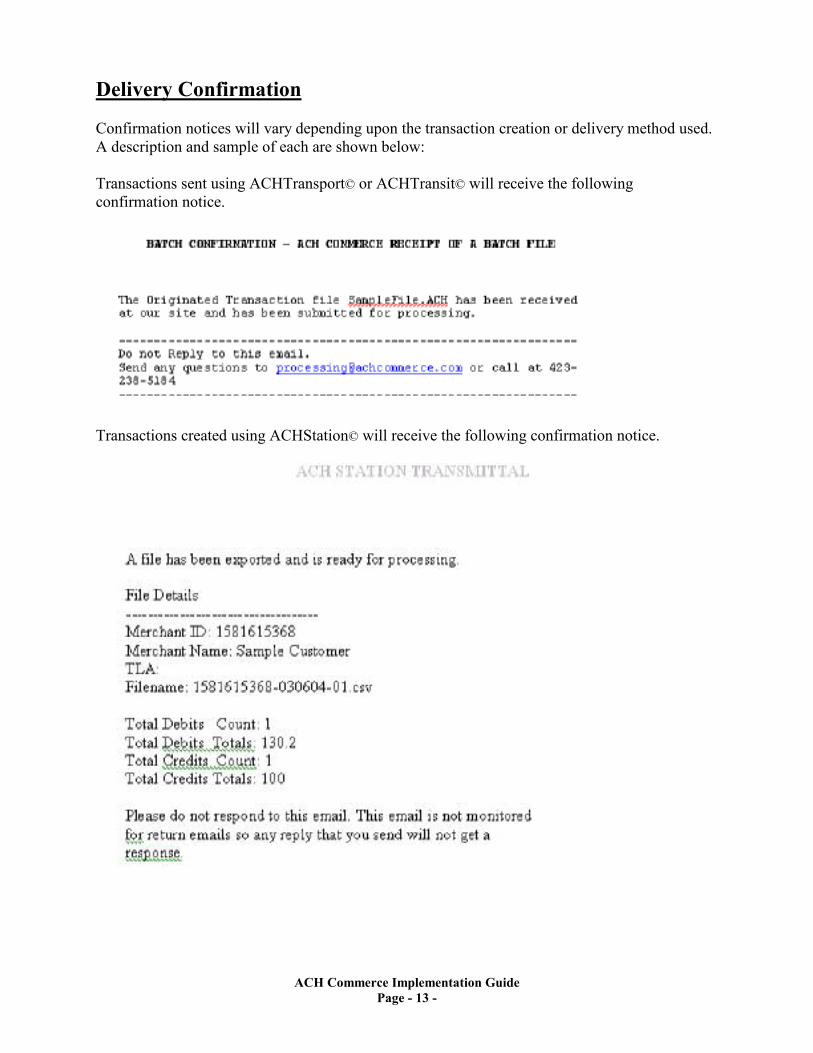

Delivery Confirmation

Confirmation notices will vary depending upon the transaction creation or delivery method used. A description and sample of each are shown below: Transactions sent using ACHTransport© or ACHTransit© will receive the following confirmation notice.

Transactions created using ACHStation© will receive the following confirmation notice.

ACH Commerce Implementation Guide Page - 14 -

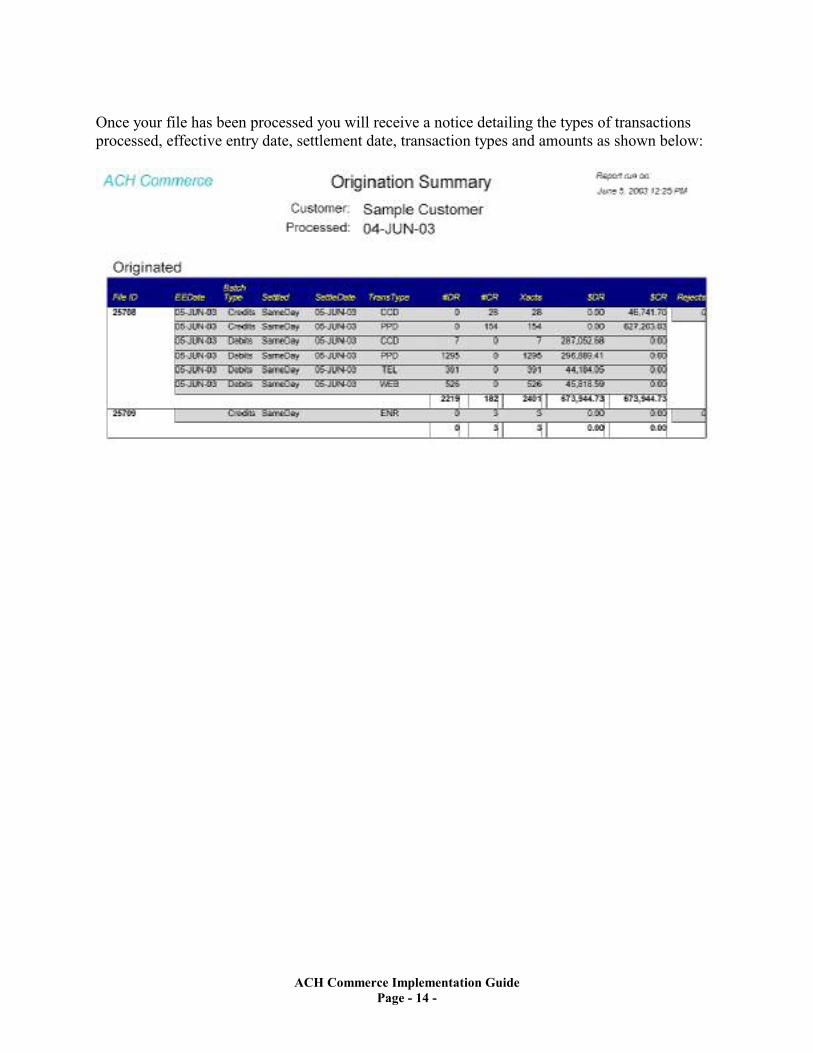

Once your file has been processed you will receive a notice detailing the types of transactions processed, effective entry date, settlement date, transaction types and amounts as shown below:

ACH Commerce Implementation Guide Page - 15 -

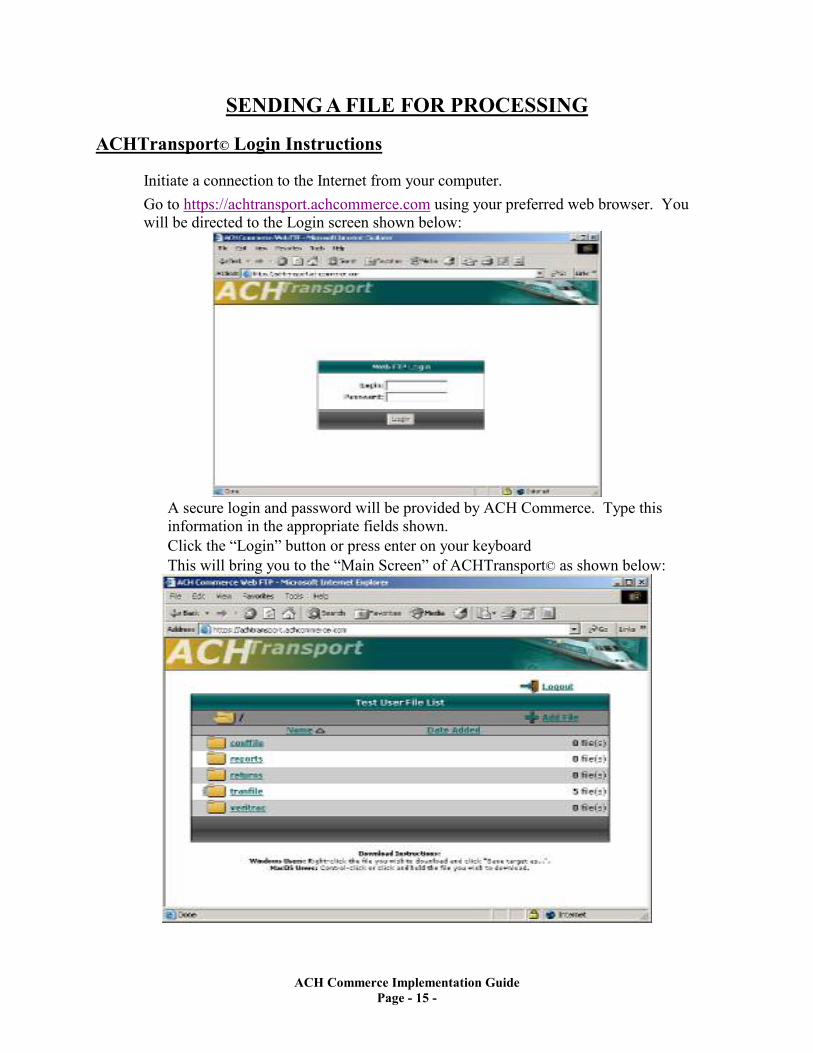

SENDING A FILE FOR PROCESSING

ACHTransport© Login Instructions

• Initiate a connection to the Internet from your computer. • Go to https://achtransport.achcommerce.com using your preferred web browser. You

will be directed to the Login screen shown below:

• A secure login and password will be provided by ACH Commerce. Type this information in the appropriate fields shown.

• Click the “Login” button or press enter on your keyboard • This will bring you to the “Main Screen” of ACHTransport© as shown below:

ACH Commerce Implementation Guide Page - 16 -

Uploading (Sending) a File to ACHTransport©

• Once you’ve signed in to ACHTransport©, you have the ability to send and receive secure information to ACH Commerce.

• Click the folder that corresponds to the type of file you are uploading. (Example: If you are sending a file to ACH Commerce for processing, you will choose the Tranfile folder.)

• Click the “Add File” icon located in the upper right hand corner of the main screen. • The prompt shown below will allow you to choose the file you wish to upload.

• Click the “Browse” button to navigate to where the file is stored on your computer or simply type in the path and filename.

• Then click the “Add” button to upload your file.

ACH Commerce Implementation Guide Page - 17 -

AUTHENTICATION & VERIFICATION SERVICES

Overview

ACH Commerce understands the risk involved with accepting checks electronically. We provide a variety of tools designed to perform commercially reasonable check validation and buyer authentication. Based on the risk profile of your particular business, ACH Commerce can supply the right combination of tools to create a secure environment for you and your customer. These tools include:

• Routing Number Validation • Account Number Validity Check & Status

Product Descriptions

ACH MatchTrac©: This service is designed to verify the validity of a bank routing number. ACH Commerce provides this service through a partnership with the entity that issues routing numbers to financial institutions and maintains the most current information regarding routing number status in a central database. This service is available in “real-time” or by filtering batches prior to processing and can be utilized by all of our data collection and transmission methods.

Features: • Allows lookup of bank name by routing number • Quickly identifies data entry errors of routing number • Identifies inactive or retired routing numbers due to bank merger or acquisition • Identifies financial institutions with valid routing numbers that do not accept ACH

transactions • Identifies credit unions and financial institutions whose rules do not allow debit or

credit ACH transactions to post to savings or checking accounts • Available in real-time or batch filtering

Benefits: • Reduces “administrative” returns, allowing you to identify bad routing numbers and

enables you to make the correction at the point of acceptance instead of after the sale • Reduces cost associated with administrative return items

ACH Commerce Implementation Guide Page - 18 -

ACH VeriTrac©: This service also verifies the validity of routing numbers but is enhanced by the ability to verify that the account number is recognized as an open account and is not currently in overdraft status. Approximately 70% of the financial institutions contribute to this national database and the number is growing daily. This product can be combined with our other verification products and utilized by all of our data collection and transmission methods.

Features: • Recognizes items drawn on closed accounts • Recognizes items drawn on accounts currently in overdraft status • Identifies inactive or retired routing numbers due to bank merger or acquisition • Identifies financial institutions with valid routing numbers that do not accept ACH

transactions • Available in real-time or batch filtering

Benefits: • Reduces “Account Closed” and “NSF” returns • Allows your company to recognize potentially fraudulent transactions • Reduces cost associated with return items and collections

ACH VeriTrac Express©: An alternate method of utilizing ACH Commerce’s Veritrac©product. This web-based application is ideal for single verification of your customers’ accounts. Customer Service Representatives can simply enter the routing and account number of a potential customer into the web-based form for real-time verification of the account status.

ACH Commerce Implementation Guide Page - 19 -

AUTHORIZATIONS & DISCLOSURES

o PPD Debit Sample Authorization

AUTHORIZATION AGREEMENT DIRECT PAYMENTS (ACH DEBITS)

I (we) hereby authorize _____________________________________, hereinafter called COMPANY, to debit entries to my (our) account indicated below and the Financial Institution named below, hereinafter called FINANCIAL INSTITUTION, to debit same to such account. I (we) acknowledge the origination of ACH transactions to my (our) account must comply with the provisions of U.S. law. ___________________________________________________ (Financial Institution) (Branch) ______________________________________________________________________________ (Address) (City-State) (Zip) _____________________ ___________________ ___Checking ____ Savings (Routing/Transit Number) (Account Number) (Account Type)

Recurring Amount________/ Range: Minimum__________Maximum____________

This authority is to remain in full force and effect until COMPANY has received written notification from me (or either of us) of its termination in such time and manner as to afford COMPANY and FINANCIAL INSTITUTION a reasonable opportunity to act on it. _________________________________________ ________________________ (Print Individual Name) (Individual ID Number) _________________________________________ ________________________ (Signature) (Date)

PLEASE ATTACH COPY OF VOIDED CHECK TO THIS FORM

ACH Commerce Implementation Guide Page - 20 -

o PPD Credit Sample Authorization

AUTHORIZATION AGREEMENT DIRECT PAYMENTS (ACH CREDITS)

I (we) hereby authorize _____________________________________, hereinafter called COMPANY, to credit entries to my (our) account indicated below and the Financial Institution named below, hereinafter called FINANCIAL INSTITUTION, to debit same to such account. I (we) acknowledge the origination of ACH transactions to my (our) account must comply with the provisions of U.S. law. ___________________________________________________ (Financial Institution) (Branch) ______________________________________________________________________________ (Address) (City-State) (Zip) _____________________ ___________________ ___Checking ____ Savings (Routing/Transit Number) (Account Number) (Account Type)

Recurring Amount________/ Range: Minimum__________Maximum____________

This authority is to remain in full force and effect until COMPANY has received written notification from me (or either of us) of its termination in such time and manner as to afford COMPANY and FINANCIAL INSTITUTION a reasonable opportunity to act on it. _________________________________________ ________________________ (Print Individual Name) (Individual ID Number) _________________________________________ ________________________ (Signature) (Date)

PLEASE ATTACH COPY OF VOIDED CHECK TO THIS FORM

ACH Commerce Implementation Guide Page - 21 -

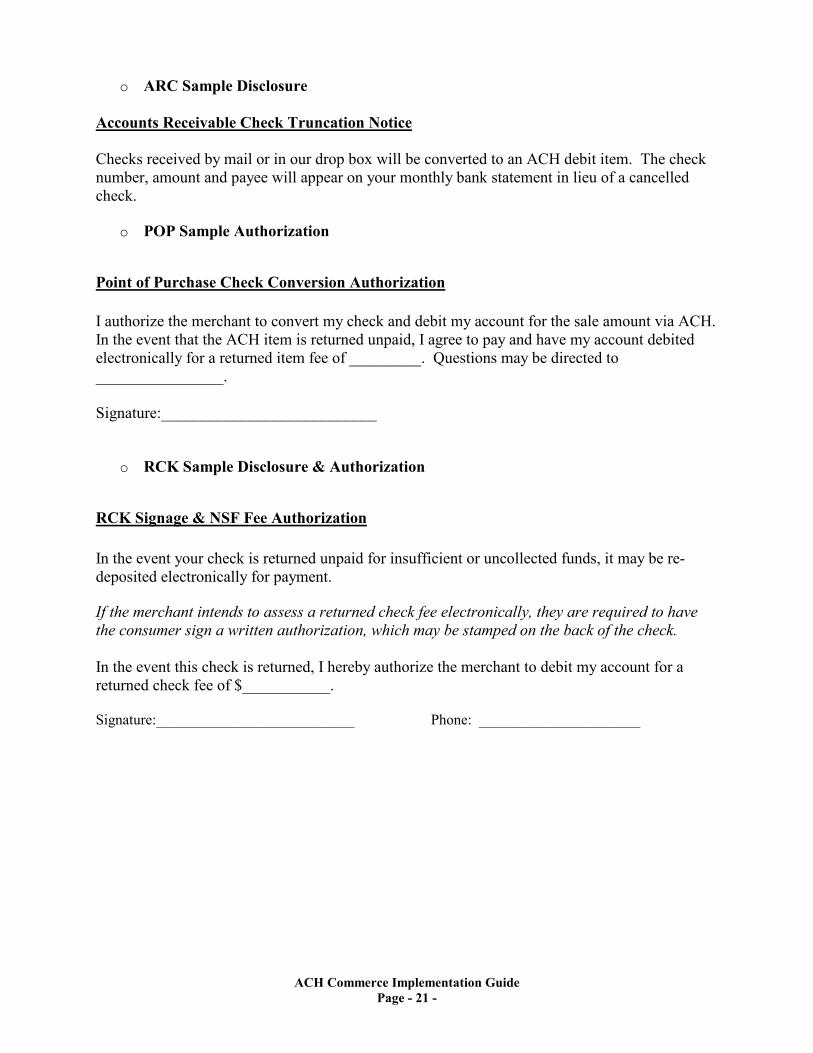

o ARC Sample Disclosure

Accounts Receivable Check Truncation Notice

Checks received by mail or in our drop box will be converted to an ACH debit item. The check number, amount and payee will appear on your monthly bank statement in lieu of a cancelled check.

o POP Sample Authorization

Point of Purchase Check Conversion Authorization

I authorize the merchant to convert my check and debit my account for the sale amount via ACH. In the event that the ACH item is returned unpaid, I agree to pay and have my account debited electronically for a returned item fee of _________. Questions may be directed to ________________. Signature:___________________________

o RCK Sample Disclosure & Authorization

RCK Signage & NSF Fee Authorization

In the event your check is returned unpaid for insufficient or uncollected funds, it may be re-deposited electronically for payment. If the merchant intends to assess a returned check fee electronically, they are required to have the consumer sign a written authorization, which may be stamped on the back of the check. In the event this check is returned, I hereby authorize the merchant to debit my account for a returned check fee of $___________. Signature:___________________________ Phone: ______________________

ACH Commerce Implementation Guide Page - 22 -

TIMING

Origination Timing

The ACH rules govern timing of transaction delivery to the ACH Operator and timeframes for returning an item for NSF or Unauthorized. Timing of Settlement entries to your company’s (Originator) account is typically determined by the ODFI based on a risk evaluation conducted through the underwriting process. It is important to note that numerous dates and times are often referred to when processing ACH items. These are outlined below:

1. Cut-Off Time: The daily time established as a deadline to insure transactions are processed that day. Your cut-off time for processing is established in your ACH Origination Agreement. Files submitted after the cut-off time are not processed until the next processing day unless. Processing of late files is permitted but late file fees are assessed upon approval.

2. Process Date: The date transactions received by the cut-off time are processed and

forwarded to the ACH Operator by the Third Party Service Provider or ODFI.

3. Effective Entry Date: The date your company (Originator) intends payment or collection to post to your customer’s (Receiver) account. Effective entry dates may be adjusted if they are stale dated, fall on a holiday or weekend. The diagram below illustrates the Process and Effective Entry Dates.

Monday Tuesday Wednesday Thursday Friday Process Date Effective Entry Date (File sent to ACH Commerce for Processing)

(Transactions post to Receiver’s accounts)

4. Non Processing Holidays

ACH Commerce Implementation Guide Page - 23 -

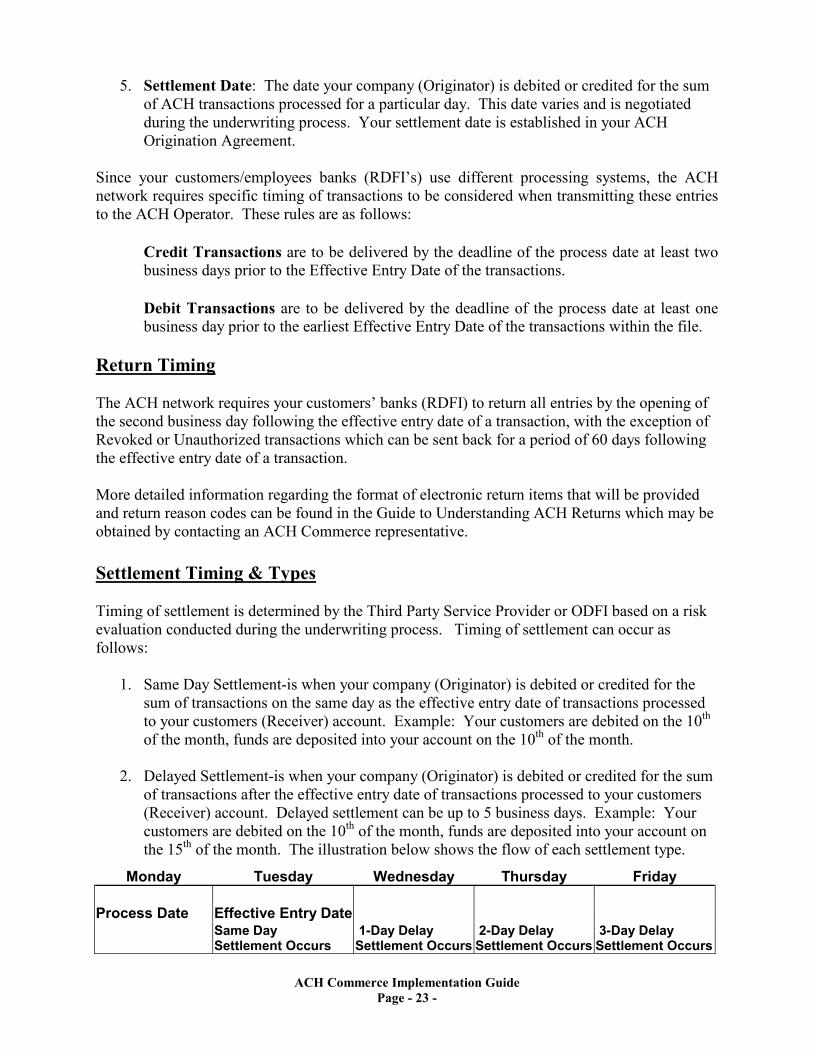

5. Settlement Date: The date your company (Originator) is debited or credited for the sum of ACH transactions processed for a particular day. This date varies and is negotiated during the underwriting process. Your settlement date is established in your ACH Origination Agreement.

Since your customers/employees banks (RDFI’s) use different processing systems, the ACH network requires specific timing of transactions to be considered when transmitting these entries to the ACH Operator. These rules are as follows:

• Credit Transactions are to be delivered by the deadline of the process date at least two business days prior to the Effective Entry Date of the transactions.

• Debit Transactions are to be delivered by the deadline of the process date at least one

business day prior to the earliest Effective Entry Date of the transactions within the file. Return Timing

The ACH network requires your customers’ banks (RDFI) to return all entries by the opening of the second business day following the effective entry date of a transaction, with the exception of Revoked or Unauthorized transactions which can be sent back for a period of 60 days following the effective entry date of a transaction. More detailed information regarding the format of electronic return items that will be provided and return reason codes can be found in the Guide to Understanding ACH Returns which may be obtained by contacting an ACH Commerce representative. Settlement Timing & Types

Timing of settlement is determined by the Third Party Service Provider or ODFI based on a risk evaluation conducted during the underwriting process. Timing of settlement can occur as follows:

1. Same Day Settlement-is when your company (Originator) is debited or credited for the sum of transactions on the same day as the effective entry date of transactions processed to your customers (Receiver) account. Example: Your customers are debited on the 10th of the month, funds are deposited into your account on the 10th of the month.

2. Delayed Settlement-is when your company (Originator) is debited or credited for the sum

of transactions after the effective entry date of transactions processed to your customers (Receiver) account. Delayed settlement can be up to 5 business days. Example: Your customers are debited on the 10th of the month, funds are deposited into your account on the 15th of the month. The illustration below shows the flow of each settlement type.

Monday Tuesday Wednesday Thursday Friday Process Date Effective Entry Date

Same Day Settlement Occurs

1-Day Delay Settlement Occurs

2-Day Delay Settlement Occurs

3-Day Delay Settlement Occurs

ACH Commerce Implementation Guide Page - 24 -

3. Pre-Funding-is when your company (Originator) is debited for the sum of credit transactions prior to the effective entry date of transactions to be credited to your customers/employees (Receiver). The illustration below details a 1-day pre-funding scenario.

Monday Tuesday Wednesday Thursday Friday Payroll File is sent to ACH Commerce.

Your account is debited for the total amount of the payroll file.

The payroll credits are sent outto your employees.

Effective Entry Datefor Payroll Credits.

4. Net Settlement-is when your company (Originator) is debited or credited for the sum of transactions due on a delayed settlement date, minus return items received for those transactions, late returns for previously settled transactions, reserves and fees. A sample of a net settlement report is shown below:

Net Settlement Report Sample:

ACH Commerce Implementation Guide Page - 25 -

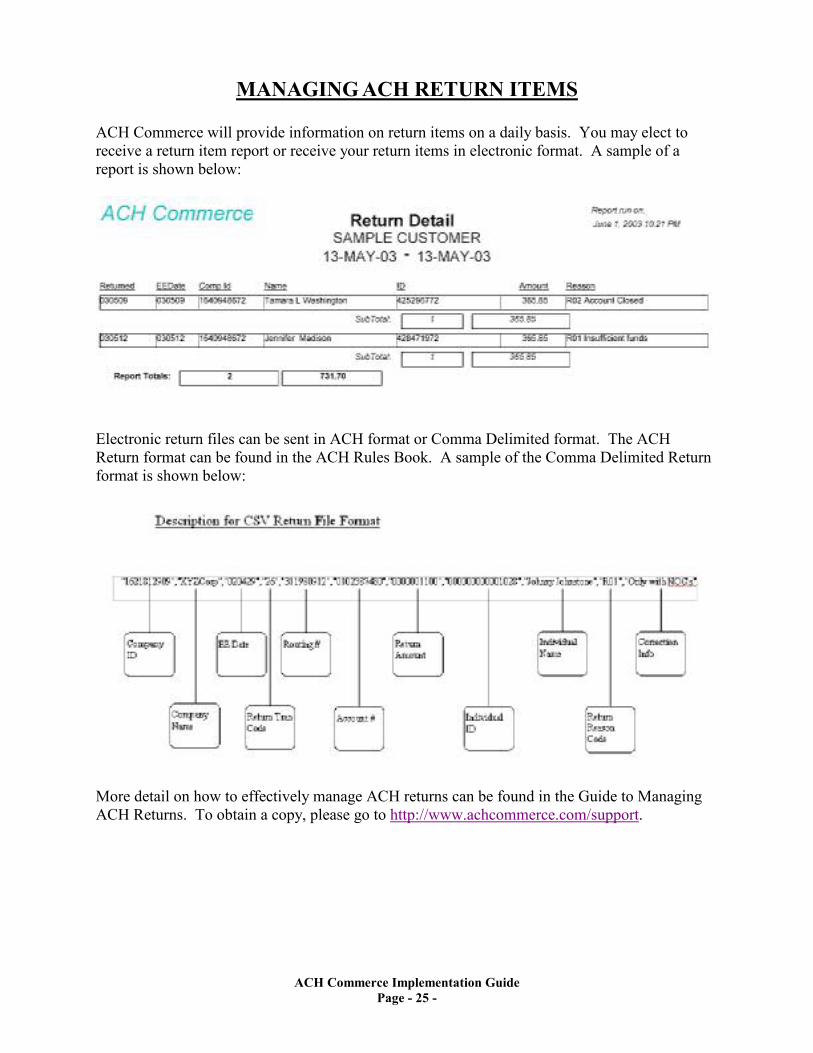

MANAGING ACH RETURN ITEMS

ACH Commerce will provide information on return items on a daily basis. You may elect to receive a return item report or receive your return items in electronic format. A sample of a report is shown below:

Electronic return files can be sent in ACH format or Comma Delimited format. The ACH Return format can be found in the ACH Rules Book. A sample of the Comma Delimited Return format is shown below:

More detail on how to effectively manage ACH returns can be found in the Guide to Managing ACH Returns. To obtain a copy, please go to http://www.achcommerce.com/support.

ACH Commerce Implementation Guide Page - 26 -

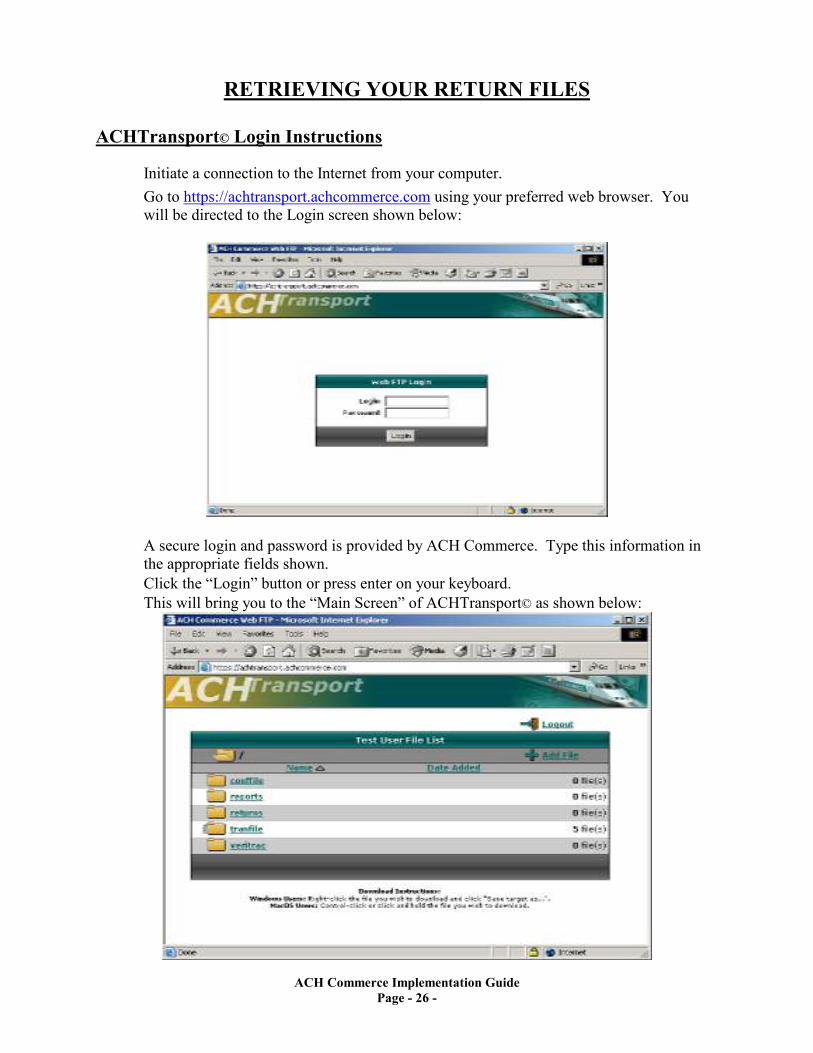

RETRIEVING YOUR RETURN FILES

ACHTransport© Login Instructions

• Initiate a connection to the Internet from your computer. • Go to https://achtransport.achcommerce.com using your preferred web browser. You

will be directed to the Login screen shown below:

• A secure login and password is provided by ACH Commerce. Type this information in the appropriate fields shown.

• Click the “Login” button or press enter on your keyboard. • This will bring you to the “Main Screen” of ACHTransport© as shown below:

ACH Commerce Implementation Guide Page - 27 -

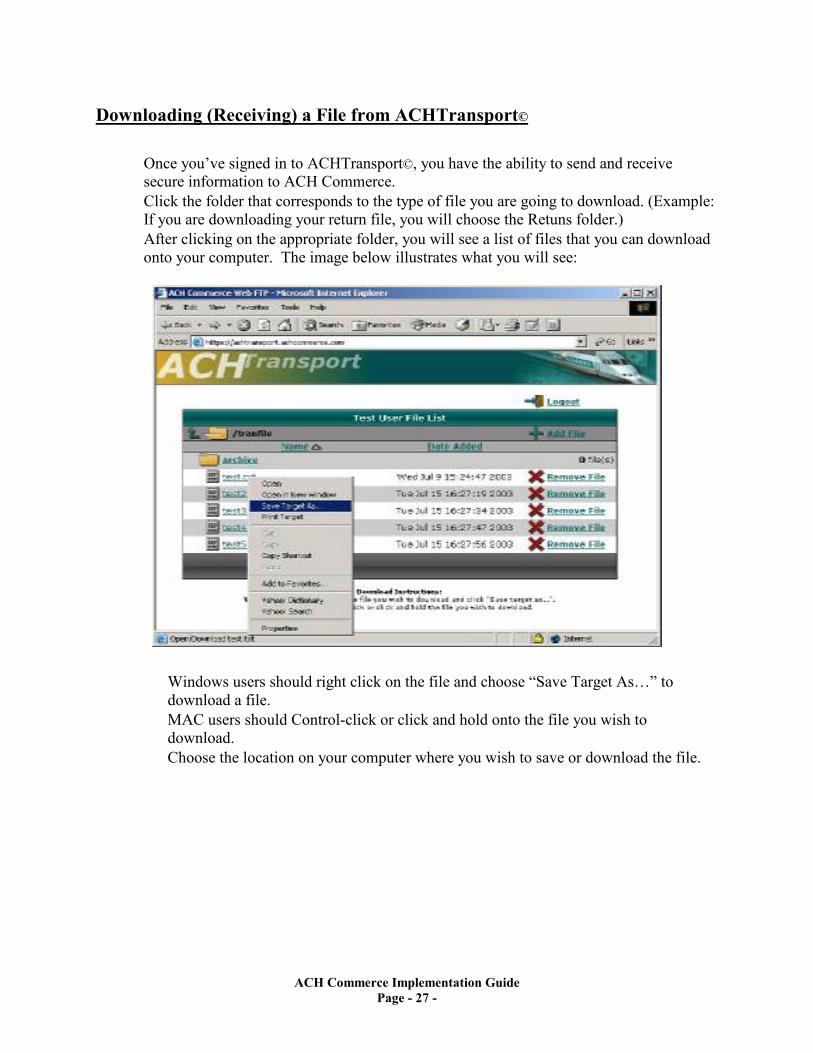

Downloading (Receiving) a File from ACHTransport©

• Once you’ve signed in to ACHTransport©, you have the ability to send and receive secure information to ACH Commerce.

• Click the folder that corresponds to the type of file you are going to download. (Example: If you are downloading your return file, you will choose the Retuns folder.)

• After clicking on the appropriate folder, you will see a list of files that you can download onto your computer. The image below illustrates what you will see:

• Windows users should right click on the file and choose “Save Target As…” to download a file.

• MAC users should Control-click or click and hold onto the file you wish to download.

• Choose the location on your computer where you wish to save or download the file.

ACH Commerce Implementation Guide Page - 28 -

REPORTS & SPECIAL SERVICES

ACH Commerce provides two additional reports upon request. These are the Customer Activity Summary Report (useful for monthly reconcilement) and Return Reason Code Summary (useful in analysis to reduce return item fees). These reports can be provided on a monthly basis for an additional fee of $15.00 per month. We also have many other custom reports that are available upon request. Customer Activity Summary Report

ACH Commerce Implementation Guide Page - 29 -

Return Reason Code Summary

ACH Commerce also provides two verification services to assist you in reducing return items. These services are known as ACH MatchTrac© and ACH VeriTrac©. MatchTrac© is instrumental in reducing administrative type returns such as non-participating financial institution and invalid routing number. VeriTrac© is useful in reducing account closed and NSF return types. More information on these services can be found at in the Authentication and Verification Services portion of this guide or at www.achcommerce.com under Corporate Services.

ACH Commerce Implementation Guide Page - 30 -

CONTACT INFORMATION

Mailing Address : ACH Commerce, LLC. 8920 B Transport Lane, Suite 1 Ooltewah, TN 37363 Phone Numbers : 800-724-8780 – Toll Free 423-238-5184 – Main 423-238-5187 – Fax General E-Mail: [email protected]

[email protected]@[email protected]

Management Personnel Listing

Deborah Hickok, AAP – President Email – [email protected] David Peace – Executive Vice President, Sales & Marketing Email – [email protected] Alan Lane, AAP – Chief Information Officer, Software Development Email – [email protected] Dana Peace Bianculli – Sales, Marketing and Administration Email – [email protected] Michael Clements, AAP – Customer Service Manager, Sales Implementation & Setup Email – [email protected] Clint Blaylock – Processing Manager, Sales Implementation & Setup Email – [email protected] Dan Cummings – Processing Specialist Email – [email protected] Terri Moffett – Processing Specialist Email – [email protected] Valerie Clark – Quality Control, Accounting Email – [email protected]

![ACHC ACCREDITATION STANDARDS ACHC ACCREDITATION GUIDE …€¦ · ACHC ACCREDITATION STANDARDS ACHC ACCREDITATION . GUIDE TO SUCCESS WORKBOOK [ HOME HEALTH ] ÍÍÜÏÎÓÞËÞÓÙØ](https://static.fdocuments.net/doc/165x107/5eac162a083b4c0f86673c3a/achc-accreditation-standards-achc-accreditation-guide-achc-accreditation-standards.jpg)

![ACHC ACCREDITATION STANDARDS ACHC ......WORKBOOK [ HOME HEALTH ] ÍÍÜÏÎÓÞËÞÓÙØ ØÓàÏÜÝÓÞã ÛÍÙ× I 3 Dear Provider, Thank you for your interest in ACHC Accreditation.](https://static.fdocuments.net/doc/165x107/5f99f7598b57277db8661e92/achc-accreditation-standards-achc-workbook-home-health-oe.jpg)