Accrual Accounting Concepts Chapter 3. Why is Accrual Accounting Needed? Cash received or paid...

17

Accrual Accounting Concepts Chapter 3

-

Upload

debra-morgan-richards -

Category

Documents

-

view

225 -

download

2

Transcript of Accrual Accounting Concepts Chapter 3. Why is Accrual Accounting Needed? Cash received or paid...

Accrual Accounting Concepts

Chapter 3

Why is Accrual Accounting Needed?

Cash received or paid

Revenue earned

Expense incurred

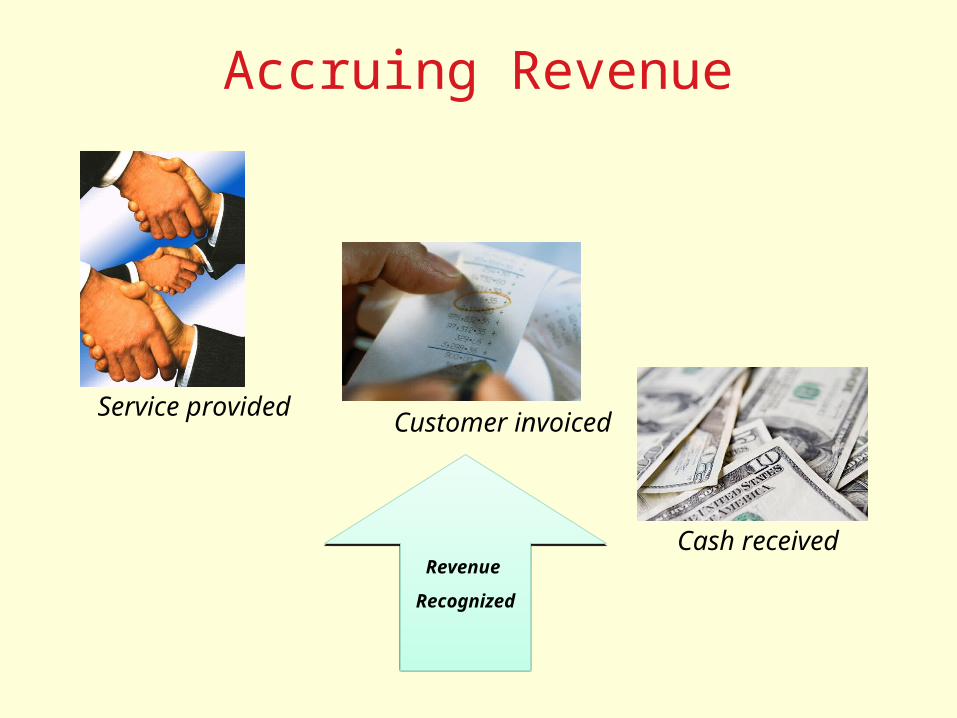

Accruing Revenue

Revenue

Recognized

Revenue

Recognized

Service providedCustomer invoiced

Cash received

Accruing Expense

Receive invoice for purchase

Materials purchased

Invoice paidExpense

Recognized

Expense

Recognized

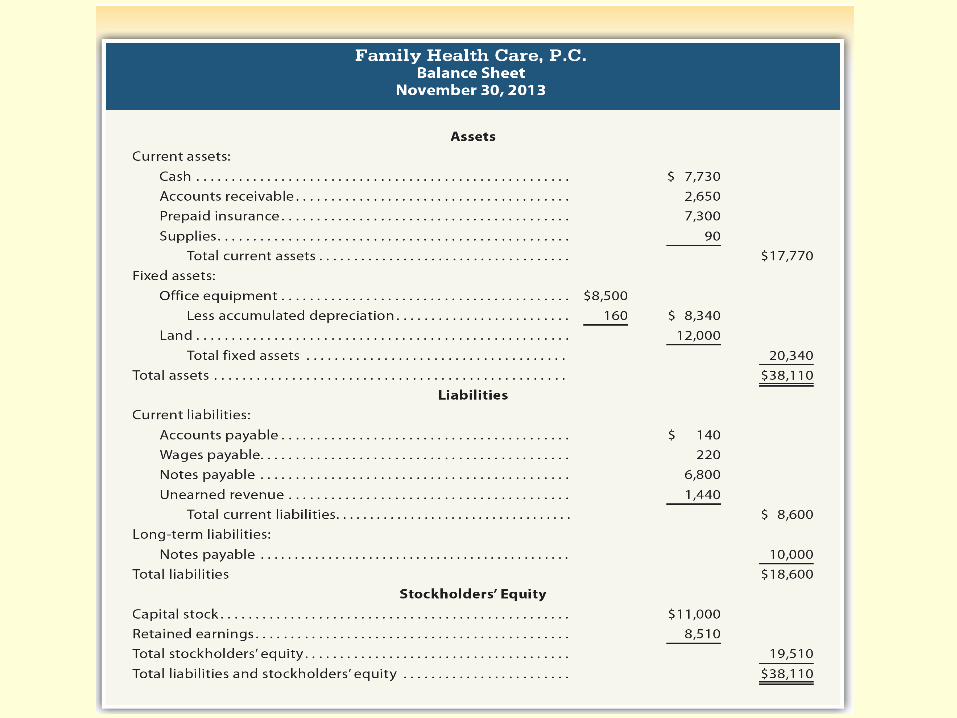

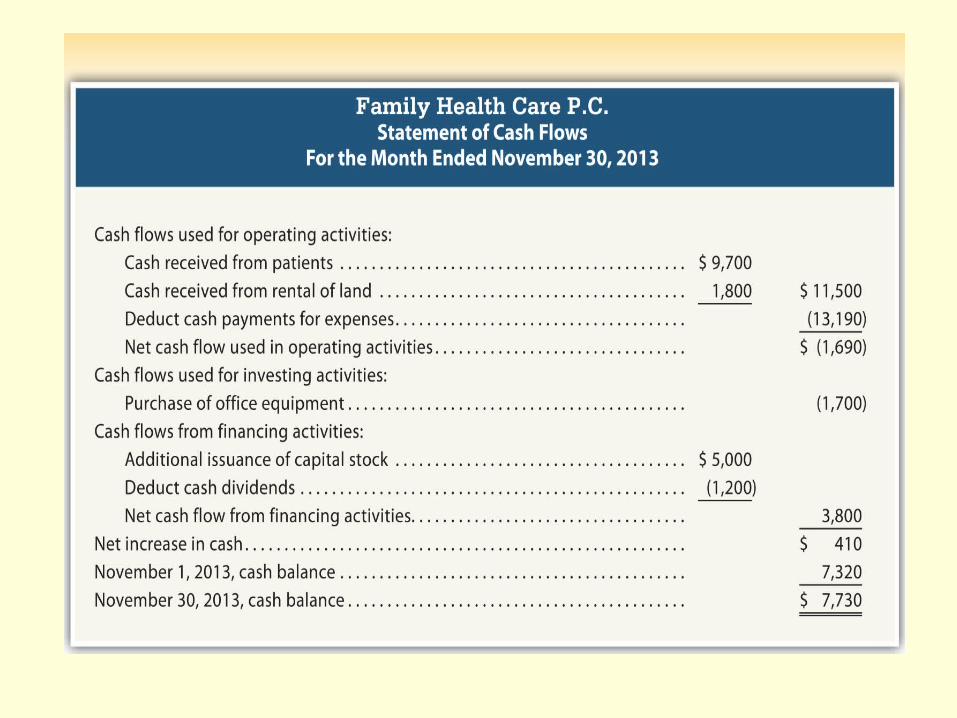

Family Health Care’s November Transactions

To illustrate accrual concepts of accounting, we will use the following November 2013 Family Health Care transactions.

a.On November 1, received $1,800 from ILS Company as rent for the use of Family Health Care’s land as a temporary parking lot from November 2013 through March 2014.b.On November 1, paid $2,400 for an insurance premium on a 2-year, general business policy.c.On November 1, paid $6,000 for an insurance premium on a six-month medical malpractice policy.d.Dr. Landry invested an additional $5,000 in the business in exchange for capital stock.e.Purchased supplies for $240 on account.

Family Health Care’s November Transactions Cont.

f.Purchased $8,500 of office equipment. Paid $1,700 cash as a down payment, with the remaining $6,800 ($8,500 - $1,700) due in five monthly installments of $1,360 ($6,800/5) beginning January 1. g.Provided services $6,100 to patients on account.h.Received $5,500 for services provided to patients who paid cash.i.Received $4,200 from insurance companies, which paid on patients’ accounts for services that have been provided.j.Paid $100 on account for supplies that had been purchased.k.Expenses paid during November were as follows: wages, $2,790; rent, $800; utilities, $580; interest, $100; and miscellaneous, $420.l.Paid dividends of $1,200 to stockholders (Dr. Landry).

Summary of Accruals and Deferrals

Deferrals

Cash received or paid

Cash received or paid

Revenue earned

or expense

incurred

Revenue earned

or expense

incurred

Deferrals

Accruals

Cash received

or paid

Cash received

or paid

Revenue earned

or expense

incurred

Revenue earned

or expense

incurred

Accruals

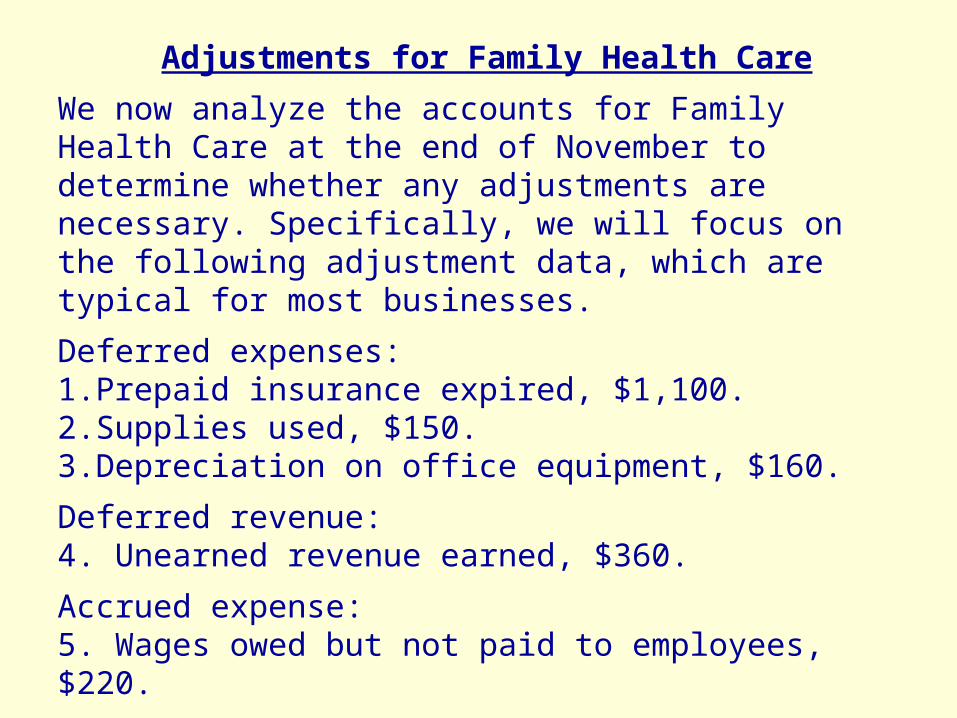

Adjustments for Family Health Care

We now analyze the accounts for Family Health Care at the end of November to determine whether any adjustments are necessary. Specifically, we will focus on the following adjustment data, which are typical for most businesses.

Deferred expenses:1.Prepaid insurance expired, $1,100.2.Supplies used, $150.3.Depreciation on office equipment, $160.

Deferred revenue:4. Unearned revenue earned, $360.

Accrued expense:5. Wages owed but not paid to employees, $220.

Accrued revenue:6. Services provided but not billed to insurance companies, $750.

Summary of Transactions for Family Health Care

Accrual Accounting and the Accounting Cycle

The Accounting CycleThe Accounting Cycle

Identify

Transactions

Identify

Transactions

Prepare

Financial

Statements

Prepare

Financial

Statements

Record

Transactions

Record

Transactions

Record

Adjustments

Record

Adjustments

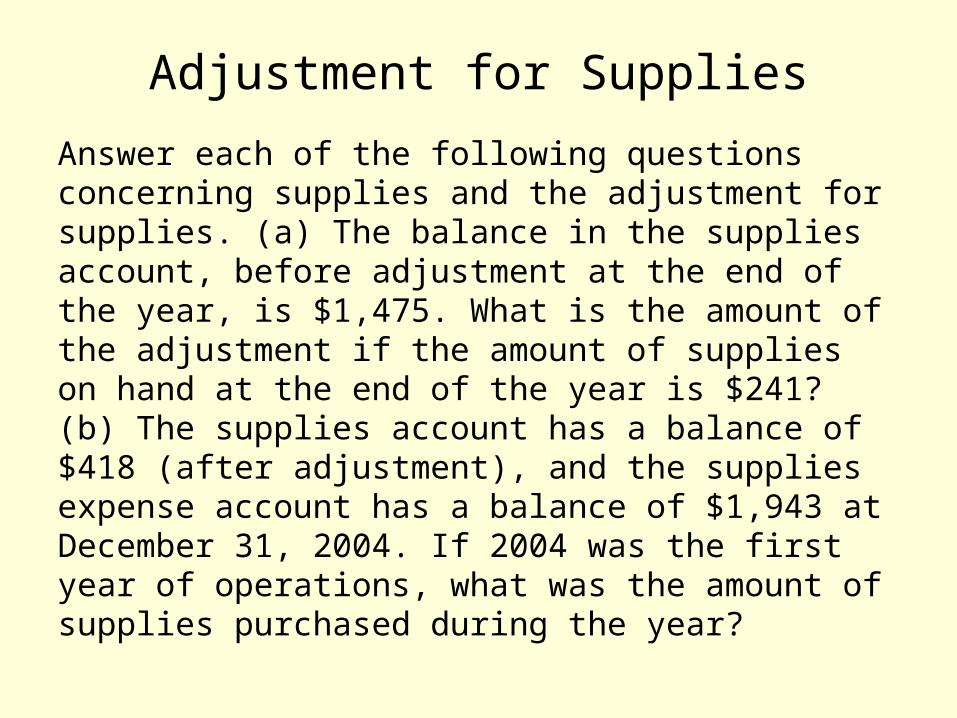

Adjustment for Supplies

Answer each of the following questions concerning supplies and the adjustment for supplies. (a) The balance in the supplies account, before adjustment at the end of the year, is $1,475. What is the amount of the adjustment if the amount of supplies on hand at the end of the year is $241? (b) The supplies account has a balance of $418 (after adjustment), and the supplies expense account has a balance of $1,943 at December 31, 2004. If 2004 was the first year of operations, what was the amount of supplies purchased during the year?

Wages

The balances of the two wages accounts at December 31, after adjustments at the end of the first year of operations, are Wages Payable, $1,960, and Wages Expense, $87,430.

Determine the amount of wages paid in cash during the year.