Accretive Health - Quality Care - Health Care Quality

33

DECEMBER 3, 2012 Quality and Care Coordination Driving Growth Through Measured Results

-

Upload

accretivehealth -

Category

Documents

-

view

886 -

download

0

description

http://www.accretivehealth.com/AboutUs/CreatingValueinHealthcare/tabid/425/Default.aspx

Transcript of Accretive Health - Quality Care - Health Care Quality

DECEMBER 3, 2012

Quality and Care Coordination

Driving Growth Through Measured Results

Driving Growth Through Measured Results

Certain statements contained in this presentation may be considered forward-looking as

defined by the Private Securities Litigation Reform Act of 1995. In particular, any statements

made about Accretive Health’s expectations for future financial and operational performance,

expected growth, new services, profitability or business outlook are forward-looking

statements. Investors are cautioned not to place undue reliance on such forward-looking

statements. There is no assurance that the matters contained in such statements will occur

since these statements involve various risks and uncertainties that could cause actual

results to differ materially from those expressed in such forward-looking statements. These

risks and uncertainties include those listed under the heading Risk Factors in the company’s

Quarterly Report on Form 10-Q for the quarter ended September 30, 2012, which is available

on the SEC’s website as well as in the investor relations portion of Accretive Health’s website

at www.accretivehealth.com. The forward-looking statements made in this presentation are

based on the company’s beliefs and expectations as of December 3, 2012 only and should

not be relied upon as representing the company’s views as of any subsequent date. While the

company may elect to update these forward-looking statements at some point in the future,

Accretive Health specifically disclaims any obligation to do so, even if its views change.

Safe Harbor

2

Driving Growth Through Measured Results

Use of Non-GAAP Financial Measures

*Reconciliations of non-GAAP measures to their most directly comparable GAAP measures are presented, where possible in the Appendix, as well as in the

Company’s financial press releases and related Form 8-K filings with the Securities and Exchange Commission. This information can be accessed for free in

the Investor Relations section of the Company’s website at www.accretivehealth.com

We believe adjusted EBITDA is useful to stockholders in evaluating our

operating performance for the following reasons:

• these and similar non-GAAP measures are widely used by investors to

measure a company’s operating performance without regard to items that

can vary substantially from company to company depending upon financing

and accounting methods, book values of assets, capital structures and the

methods by which assets were acquired;

• securities analysts often use adjusted EBITDA and similar non-GAAP

measures as supplemental measures to evaluate the overall operating

performance of companies; and

• by comparing our adjusted EBITDA in different historical periods, our

stockholders can evaluate our operating results without the additional

variations of interest income (expense), income tax expense (benefit),

depreciation and amortization expense and share-based compensation

expense.

We understand that, although measures similar to adjusted EBITDA are

frequently used by investors and securities analysts in their evaluation of

companies, these measures have limitations as analytical tools, and you

should not consider it in isolation or as a substitute for analysis of our

results of operations as reported under GAAP. To properly and prudently

evaluate our business, we encourage you to review the GAAP financial

statements included elsewhere in our regulatory filings, including the

Preliminary Prospectus, Form 8-K, and Form 10-K, and not to rely on any

single financial measure to evaluate our business.

In order to provide stockholders with greater insight and to

allow for better understanding of how our management and

board of directors analyze our financial performance and

make operational decisions, we supplement our condensed

consolidated financial statements presented on a GAAP

basis with the adjusted EBITDA and adjusted net income

measures *.

Adjusted EBITDA measure has limitations, as noted below,

and should not be considered in isolation or in substitute for

analysis of our results as reported under GAAP.

Our management uses adjusted EBITDA:

• as a measure of operating performance, because it does not

include the impact of items that we do not consider indicative

of our core operating performance;

• for planning purposes, including the preparation of our

annual operating budget;

• to allocate resources to enhance the financial performance

of our business;

• to evaluate the effectiveness of our business strategies; and

• in communications with our board of directors and investors

concerning our financial performance.

3

Driving Growth Through Measured Results

ACCRETIVE HEALTH OVERVIEW

Driving Growth Through Measured Results

• Our primary goal is to help our healthcare clients strengthen their financial

stability and deliver better care to the communities they serve

• We use technology to drive best practices and best outcomes

• We work collaboratively with clients to create solutions to existing challenges

• We promote an entrepreneurial culture to encourage innovation and

continuously upgrade our functionality with a focus on value creation

Our Guiding Principles

5

Driving Growth Through Measured Results

Founded in 2003, headquartered in Chicago

Win – Win Proposition with our Client Partners

• We are paid based on our results; no upfront costs for Quality or Revenue Cycle Services

• We have partnered with some of the most well-respected health systems in the U.S.

We Drive Measured Results for our Partners

• Since inception we have delivered $1.5 billion in cash benefits to clients

Innovation and Operational Excellence is at the Core of What We Do

• Success of our RCM offering is driven by applying technology and innovative process

improvements to drive measurable results

• Seeded Physician Advisory Services in 2009, now a $60 million run-rate business

• Developed unique offerings to improve care quality at lower costs – Intra-Stay Quality and

Population Health Management Infrastructure

Accretive Health Snapshot

6

Driving Growth Through Measured Results 7

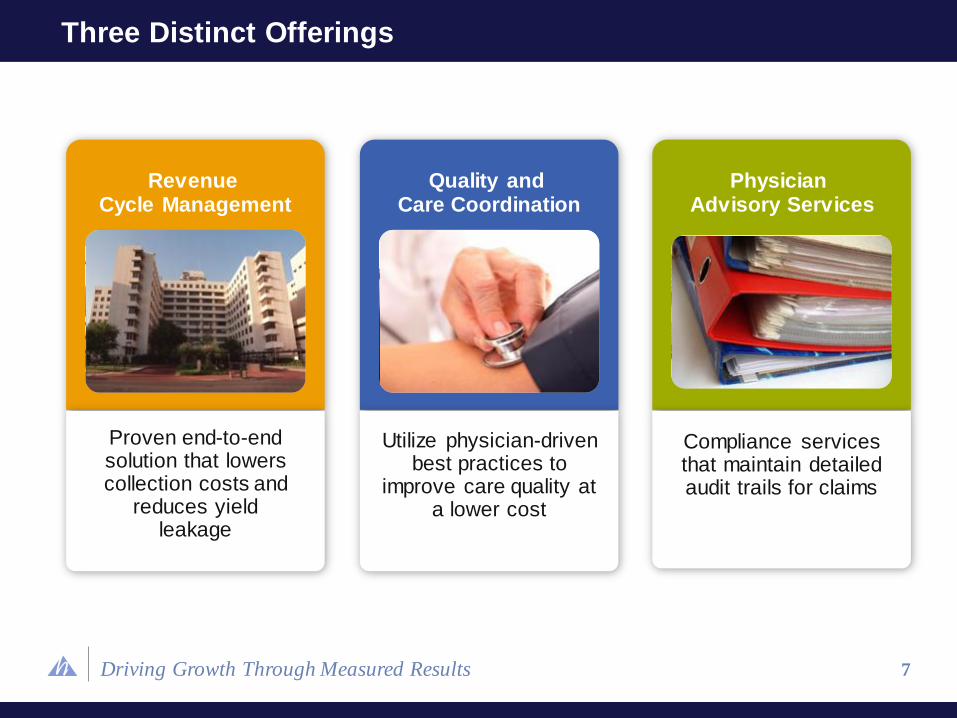

Three Distinct Offerings

Proven end-to-end solution that lowers collection costs and

reduces yield leakage

Utilize physician-driven best practices to

improve care quality at a lower cost

Compliance services that maintain detailed audit trails for claims

Physician Advisory Services

Quality and Care Coordination

Revenue Cycle Management

Driving Growth Through Measured Results

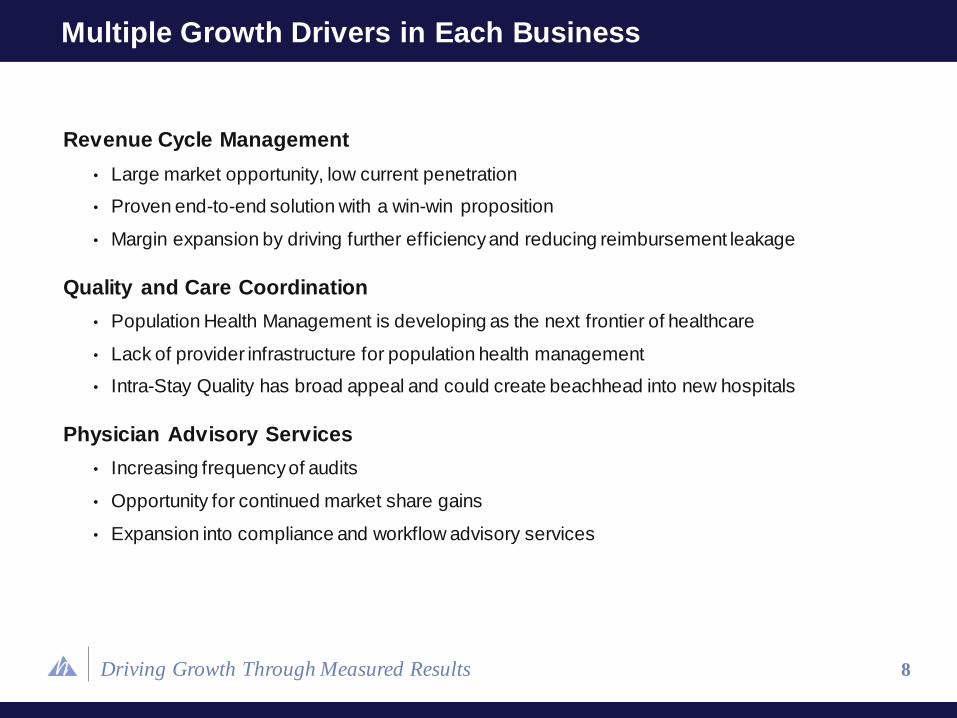

Revenue Cycle Management

• Large market opportunity, low current penetration

• Proven end-to-end solution with a win-win proposition

• Margin expansion by driving further efficiency and reducing reimbursement leakage

Quality and Care Coordination

• Population Health Management is developing as the next frontier of healthcare

• Lack of provider infrastructure for population health management

• Intra-Stay Quality has broad appeal and could create beachhead into new hospitals

Physician Advisory Services

• Increasing frequency of audits

• Opportunity for continued market share gains

• Expansion into compliance and workflow advisory services

Multiple Growth Drivers in Each Business

8

Driving Growth Through Measured Results 9

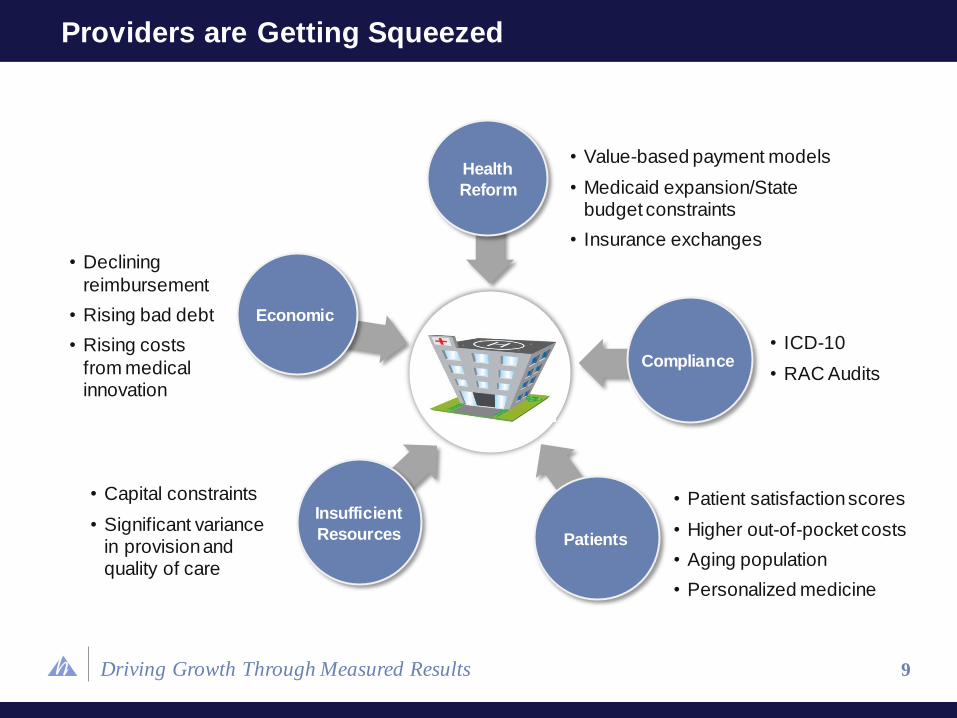

Providers are Getting Squeezed

• Capital constraints

• Significant variance in provision and quality of care

• Declining

reimbursement

• Rising bad debt

• Rising costs

from medical innovation

• Value-based payment models

• Medicaid expansion/State budget constraints

• Insurance exchanges

• ICD-10

• RAC Audits

• Patient satisfaction scores

• Higher out-of-pocket costs

• Aging population

• Personalized medicine

Patients

Compliance

Health

Reform

Economic

Insufficient

Resources

Driving Growth Through Measured Results

Market Size

% to AH Revenue

Revenue Opportunity

Sources: CMS National Healthcare Expenditures, September 2011 and Definitive Healthcare

RCM market scope includes net patient revenue at all hospitals based on CMS 2014 projected expenditures

Quality market scope includes all hospital and physician expenditures

PAS market scope includes all hospitals with >$250 million in net patient revenue

10

Market Opportunity

$50 Billion

$100 Billion

$850 Million

0.12% 6.25% 5.0%

$1.0 Trillion $1.6 Trillion $ 710 billion

PAS Quality RCM

Driving Growth Through Measured Results

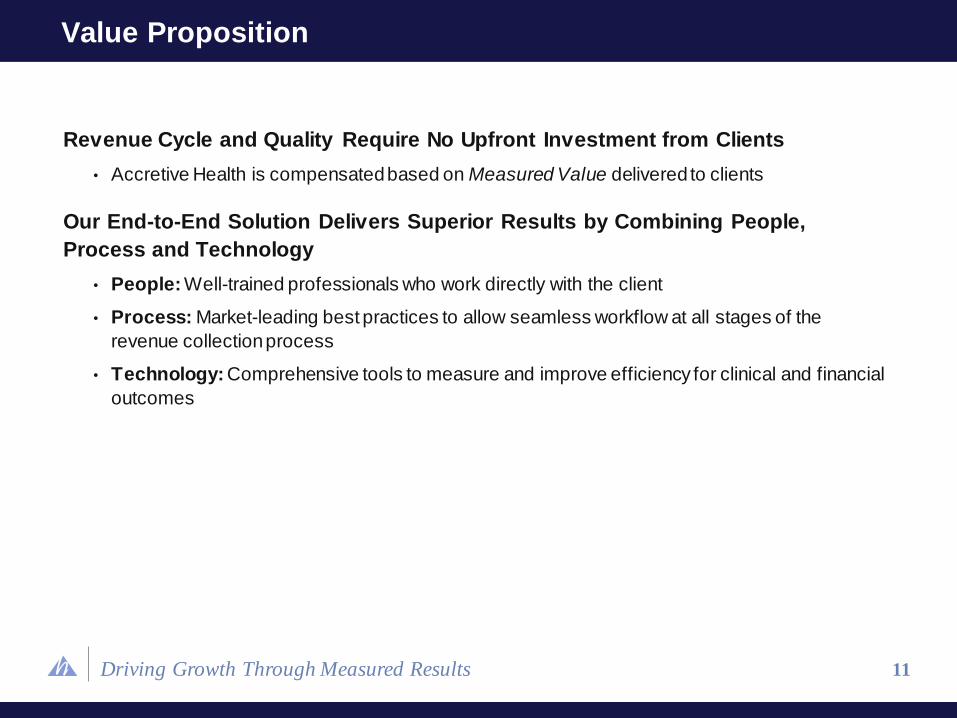

Revenue Cycle and Quality Require No Upfront Investment from Clients

• Accretive Health is compensated based on Measured Value delivered to clients

Our End-to-End Solution Delivers Superior Results by Combining People,

Process and Technology

• People: Well-trained professionals who work directly with the client

• Process: Market-leading best practices to allow seamless workflow at all stages of the

revenue collection process

• Technology: Comprehensive tools to measure and improve efficiency for clinical and financial

outcomes

Value Proposition

11

Driving Growth Through Measured Results

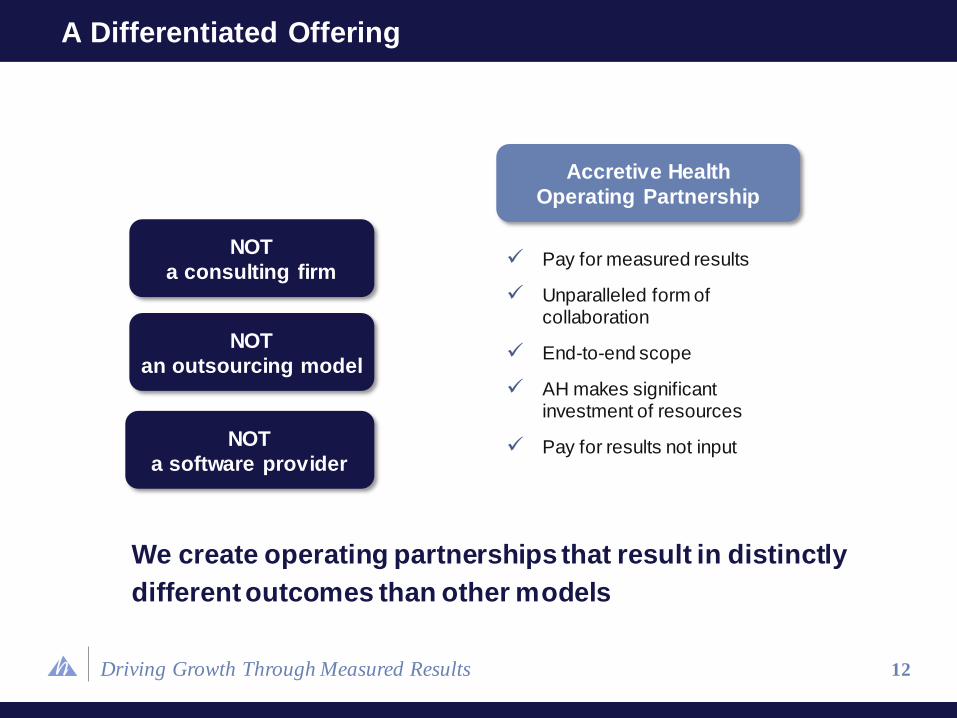

Pay for measured results

Unparalleled form of collaboration

End-to-end scope

AH makes significant investment of resources

Pay for results not input

12

A Differentiated Offering

We create operating partnerships that result in distinctly

different outcomes than other models

NOT

a consulting firm

Accretive Health

Operating Partnership

NOT

a software provider

NOT

an outsourcing model

Driving Growth Through Measured Results

SaaS /

Technology- Supported RCM

Consulting

IT Outsourcing /

Non-HC BPO

Payor Follow-Up

Patient Advocacy

Patient Share

Lost Charges

Compliance

4-6% (Measured)

Value Proposition

(% revenue lift)

Est. 0.5-1% (Not Measured)

Est. 0.5-1% (Measured)

Est. 0.5-1.5% (Not Measured)

Note: Based on Accretive Health’s estimates

13

End-to-End RCM Solution Provides Competitive Advantages

Driving Growth Through Measured Results 14

Partnering with Innovative Leaders

Driving Growth Through Measured Results

QUALITY AND CARE COORDINATION

Driving Growth Through Measured Results

DR. WALTER ETTINGER

TIM BARRY President, Quality and Care Coordination

Chief Medical Officer

16

Driving Growth Through Measured Results 17

Market Overview

$148 $356

$1,102

$2,851

$4,791

$8,223

$78 $187

$628

$1,185

$1,888

$3,265

5.1%

7.1%

9.0%

12.4%

13.7%

17.6%

3.8%

5.1%

6.6%

6.9%

7.8%

9.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

1960 1970 1980 1990 2000 2009

He

alt

hcare

Sp

en

d a

s a

% o

f G

DP

He

alt

hcare

Sp

en

d p

er

Cap

ita (U

SD

)

USA OECD

Source: The Organization for Economic Cooperation and Development (OECD) Health Expenditure Data

2010

Healthcare Spend in the U.S. is Unsustainable…

Driving Growth Through Measured Results

IRE

18

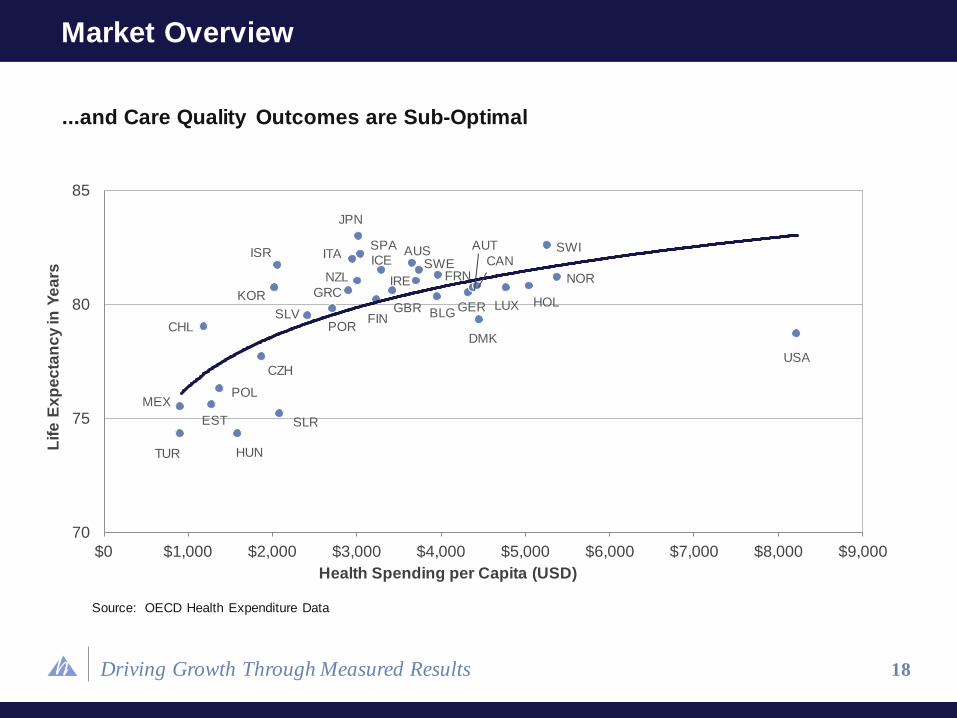

Market Overview

...and Care Quality Outcomes are Sub-Optimal

70

75

80

85

$0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000

TUR

MEX

HUN

SLR EST

POL

CHL

CZH

ISR

KOR

SLV

JPN

ITA SPA

NZL

GRC

POR

ICE

FIN GBR

AUS SWE

FRN

BLG

DMK

GER

AUT

CAN SWI

NOR

HOL LUX

USA

Source: OECD Health Expenditure Data

Health Spending per Capita (USD)

Lif

e E

xp

ec

tan

cy

in Y

ea

rs

“If home building were like healthcare,

carpenters, electricians, and plumbers each

would work with different blueprints, with very

little coordination.”

19

–Institute of Medicine 2012 Report on Best Care at Lower cost

Driving Growth Through Measured Results

Market Drivers

• Shift away from fee-for-service model to population-based accountability

• Provider performance standards tied to total patient quality and cost

• Systems required to provide insight into total patient medical history

• Requires significant investment and expertise for population-based delivery

Accretive Health Solution

• Turn-key accountability-based model that improves quality of patient care

• Strengthens relationship between hospitals and physicians

• Creates aligned interest between payors, hospitals, physicians and Accretive Health

• Generates significant savings for the healthcare system

Quality & Care Initiative

20

Driving Growth Through Measured Results

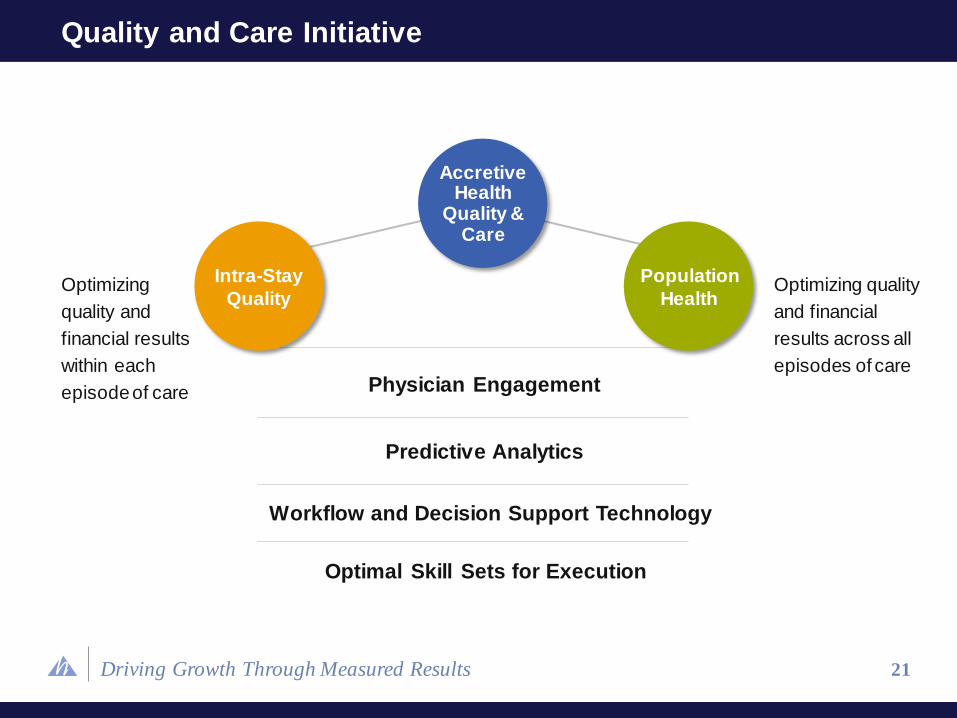

Intra-Stay

Quality

Population

Health

21

Quality and Care Initiative

Optimizing

quality and

financial results

within each

episode of care Physician Engagement

Predictive Analytics

Workflow and Decision Support Technology

Optimal Skill Sets for Execution

Optimizing quality

and financial

results across all

episodes of care

Accretive Health

Quality & Care

Driving Growth Through Measured Results

Continuous care assessment

allows physicians to focus on the

sickest patients and coordinate

care to improve outcomes

22

End-to-end Infrastructure for Population Health Management

Sickest

and most responsive

patients

Patient-

specific care

plans and

care

coordination

workflow

Real-time

clinical

pathway

adjustment

Starting point

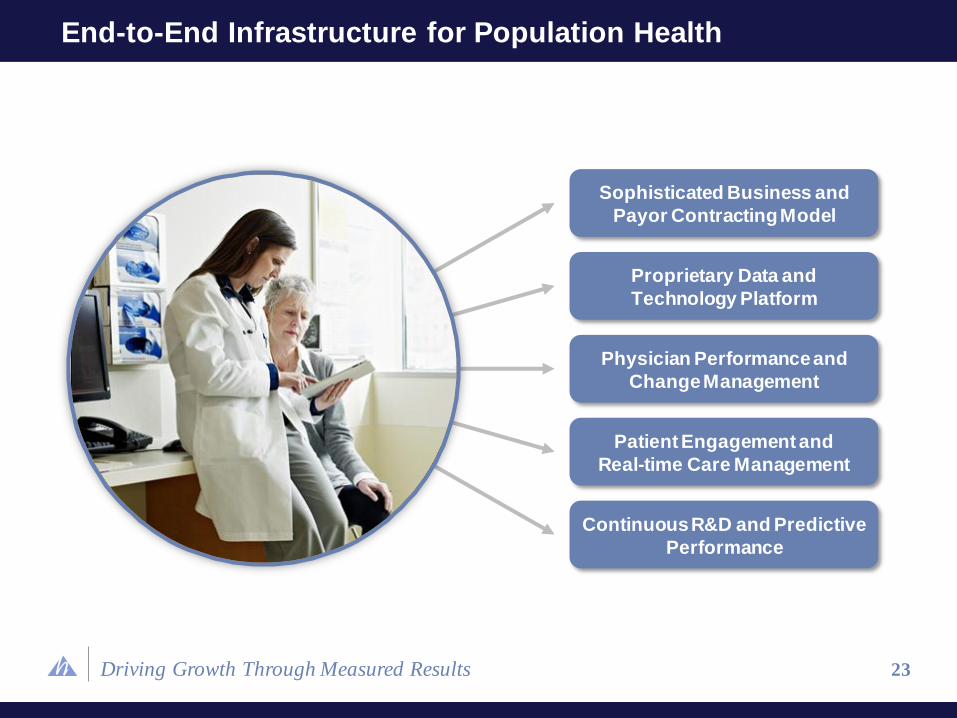

Driving Growth Through Measured Results 23

End-to-End Infrastructure for Population Health

Sophisticated Business and

Payor Contracting Model

Proprietary Data and

Technology Platform

Physician Performance and

Change Management

Patient Engagement and

Real-time Care Management

Continuous R&D and Predictive

Performance

Driving Growth Through Measured Results

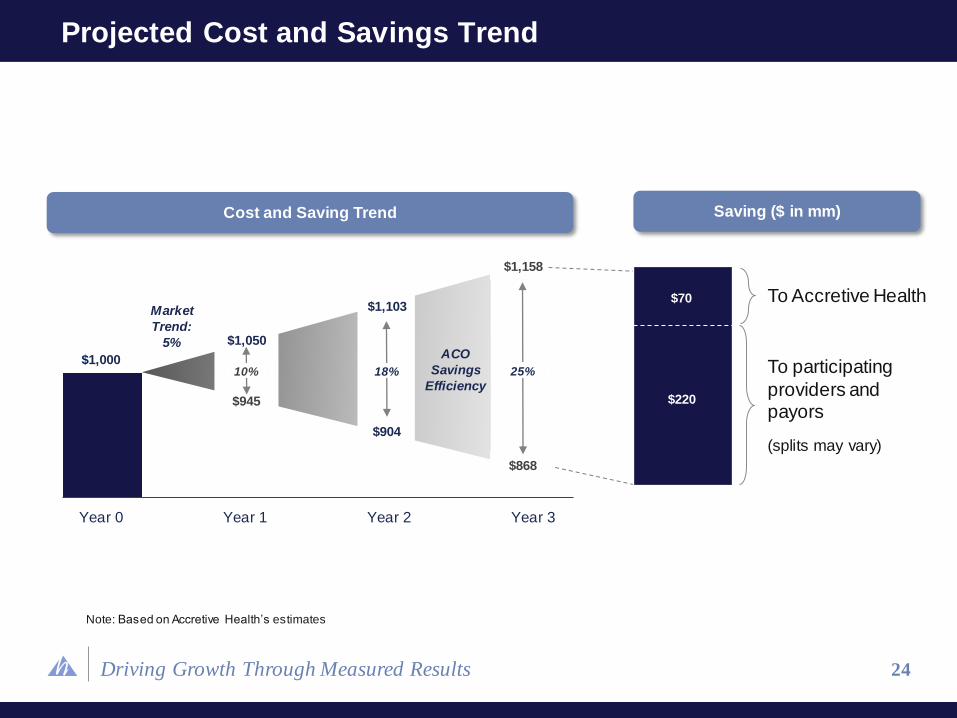

Year 0 Year 1 Year 2 Year 3

Cost and Saving Trend

$1,000

$1,050

$1,158

$1,103

$290

Saving ($ in mm)

$945

$904

$868

10% 18% 25%

Market

Trend:

5% ACO

Savings

Efficiency

To Accretive Health

To participating

providers and payors

(splits may vary)

$70

$220

24

Projected Cost and Savings Trend

Note: Based on Accretive Health’s estimates

Driving Growth Through Measured Results 25

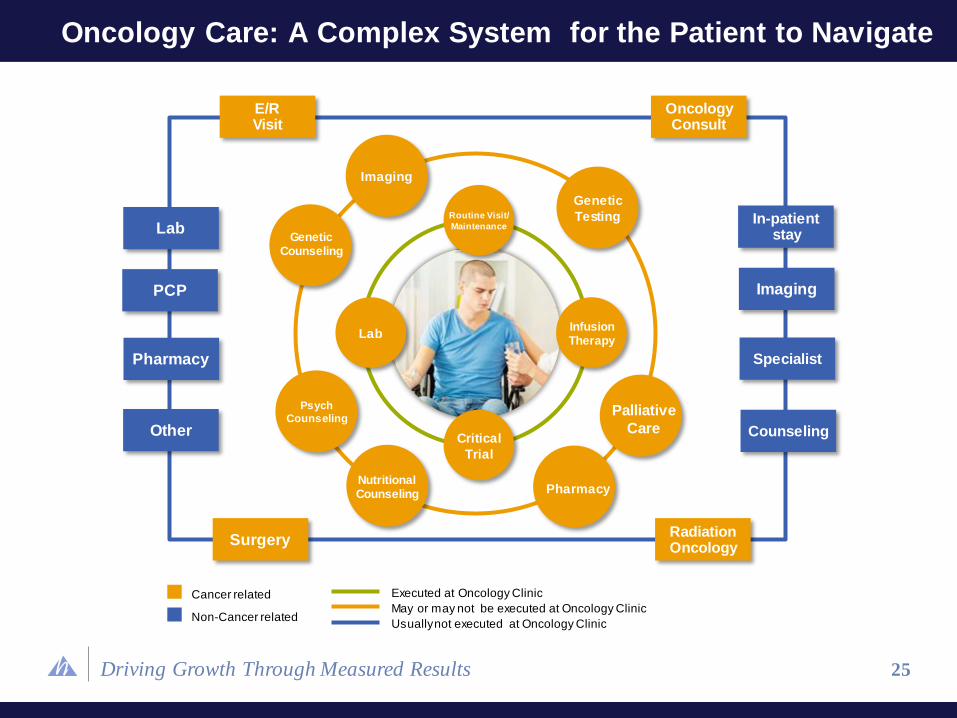

Oncology Care: A Complex System for the Patient to Navigate

Routine Visit/

Maintenance

Critical

Trial

Infusion Therapy

Lab

Psych

Counseling

Pharmacy

Palliative

Care

Nutritional Counseling

Genetic

Testing

Imaging

Genetic Counseling

E/R Visit

Oncology Consult

In-patient stay Lab

Imaging PCP

Pharmacy Specialist

Other Counseling

Surgery Radiation Oncology

Cancer related

Non-Cancer related

Executed at Oncology Clinic

May or may not be executed at Oncology Clinic

Usually not executed at Oncology Clinic

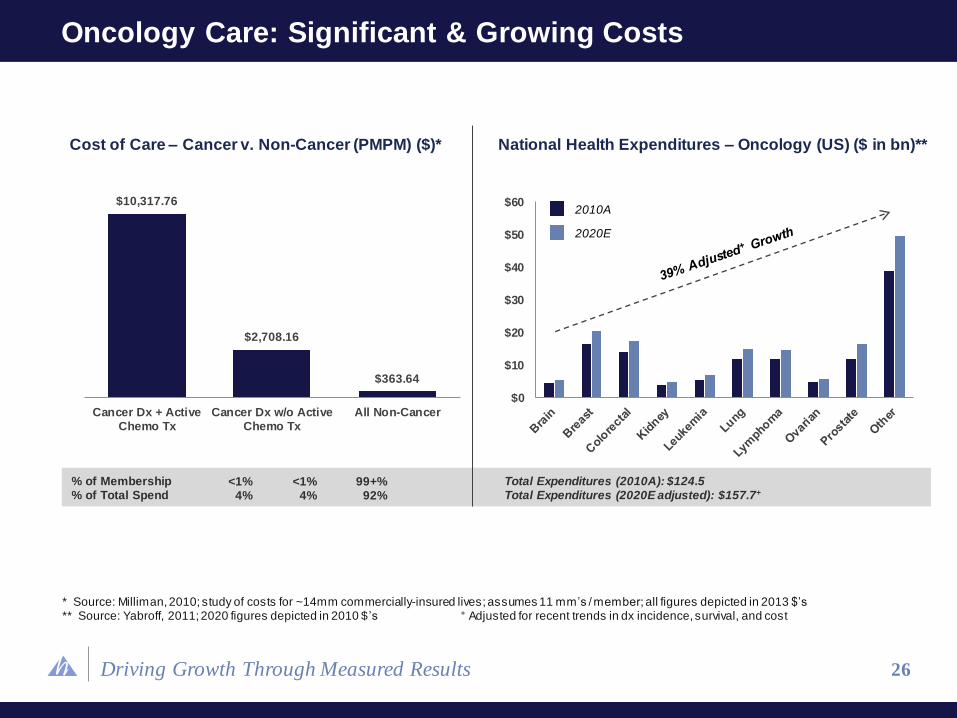

Driving Growth Through Measured Results

% of Membership % of Total Spend

Cost of Care – Cancer v. Non-Cancer (PMPM) ($)*

$0

$10

$20

$30

$40

$50

$602010A

2020E

Total Expenditures (2010A): $124.5 Total Expenditures (2020E adjusted): $157.7+

$10,317.76

$2,708.16

$363.64

Cancer Dx + ActiveChemo Tx

Cancer Dx w/o ActiveChemo Tx

All Non-Cancer

26

Oncology Care: Significant & Growing Costs

<1% 4%

<1% 4%

99+% 92%

National Health Expenditures – Oncology (US) ($ in bn)**

* Source: Milliman, 2010; study of costs for ~14mm commercially-insured lives; assumes 11 mm’s / member; all figures depicted in 2013 $’s ** Source: Yabroff, 2011; 2020 figures depicted in 2010 $ ’s + Adjusted for recent trends in dx incidence, survival, and cost

Driving Growth Through Measured Results

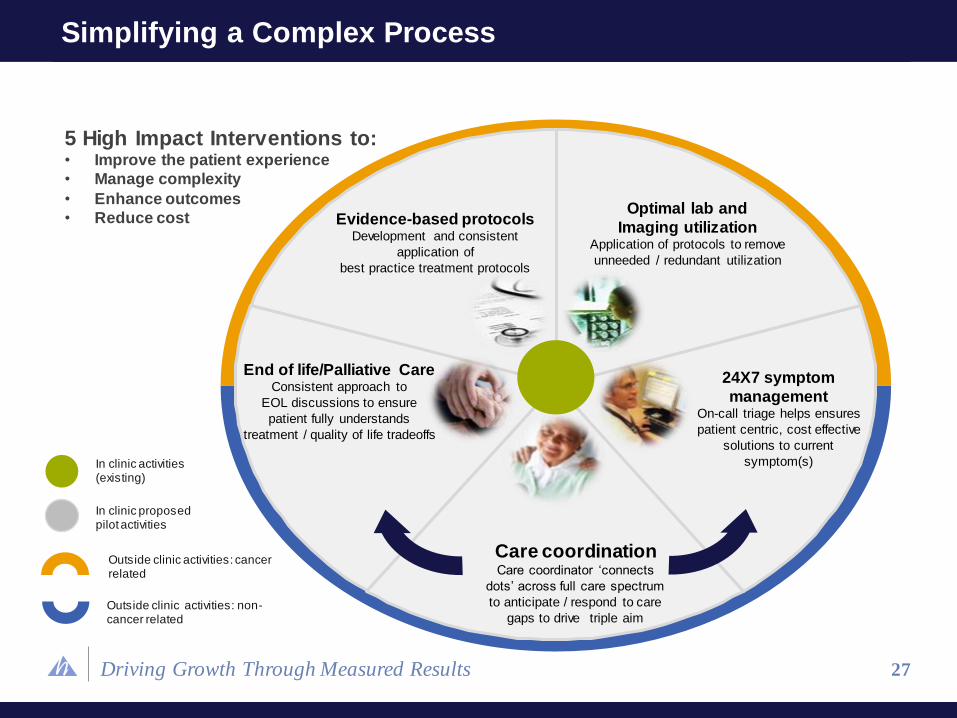

Simplifying a Complex Process

Outside clinic activities: cancer related

Outside clinic activities: non-cancer related

In clinic activities (existing)

In clinic proposed pilot activities

Care coordination Care coordinator ‘connects

dots’ across full care spectrum

to anticipate / respond to care

gaps to drive triple aim

24X7 symptom

management On-call triage helps ensures

patient centric, cost effective

solutions to current

symptom(s)

End of life/Palliative Care Consistent approach to

EOL discussions to ensure

patient fully understands

treatment / quality of life tradeoffs

Evidence-based protocols Development and consistent

application of

best practice treatment protocols

Optimal lab and

Imaging utilization Application of protocols to remove

unneeded / redundant utilization

27

5 High Impact Interventions to: • Improve the patient experience

• Manage complexity

• Enhance outcomes

• Reduce cost

Driving Growth Through Measured Results 28

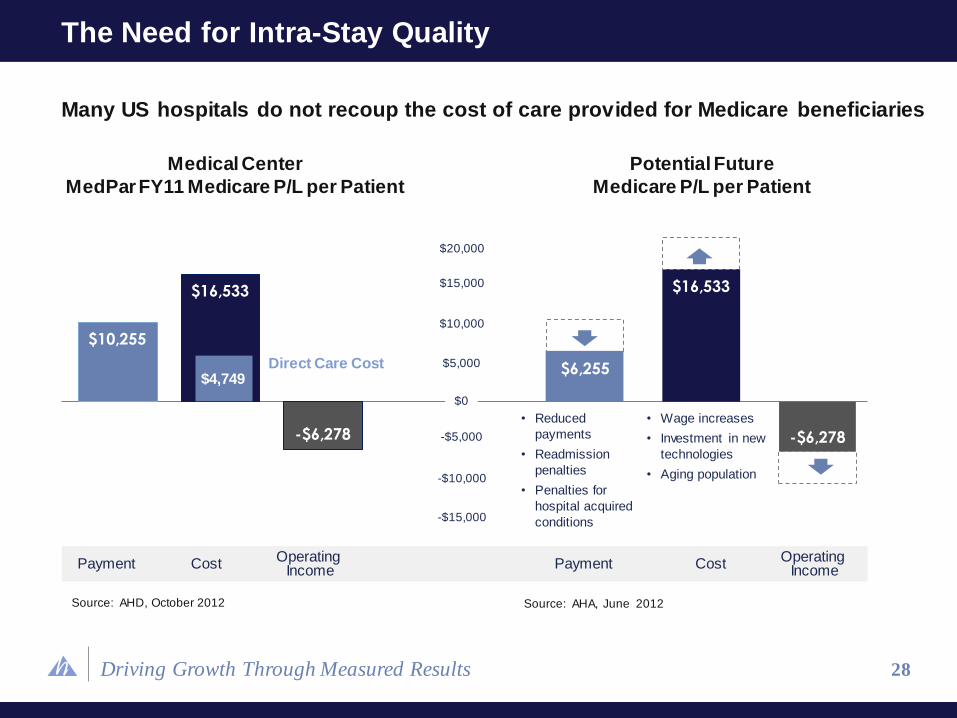

The Need for Intra-Stay Quality

Source: AHD, October 2012

$10,255

$16,533

-$6,278

$6,255

$16,533

-$6,278

• Reduced

payments

• Readmission

penalties

• Penalties for

hospital acquired

conditions

• Wage increases

• Investment in new

technologies

• Aging population

Source: AHA, June 2012

$4,749 Direct Care Cost

Many US hospitals do not recoup the cost of care provided for Medicare beneficiaries

Medical Center

MedPar FY11 Medicare P/L per Patient

Potential Future

Medicare P/L per Patient

Payment Cost Operating

Income

-$15,000

-$10,000

-$5,000

$0

$5,000

$10,000

$15,000

$20,000

Payment Cost Operating

Income

Driving Growth Through Measured Results 29

Intra-Stay Quality Timeline

ISQ Solution Today Tomorrow

Align Partners • Establish a shared vision

• Prepare for changes from Health Reform

• Administer payment model and disburse

payments

Analytics and

Reporting

• Analyze DRG and service level

performance

• Establish system/hospital scorecard

and targets

• Introduce real time DRG cost buildup tool

• Establish evidence-based plans of care to

reduce variation

Accountability

Across the

Continuum

• Implement defined plan of care

model for high priority patients

• Implement tools and technology to

support efficient through-put

• Establish post discharge relationships and

communication

• Introduce pre-stay communication, education,

and decision support

• Integrate care plans with primary care providers

Operational

Excellence and

Innovation

• Identify enterprise wide and DRG

specific opportunities and implement

solutions

• Identify and implement next wave of enterprise-

wide and DRG opportunities

• Embed CI behaviors and outcomes into

individual performance goals

Driving Growth Through Measured Results

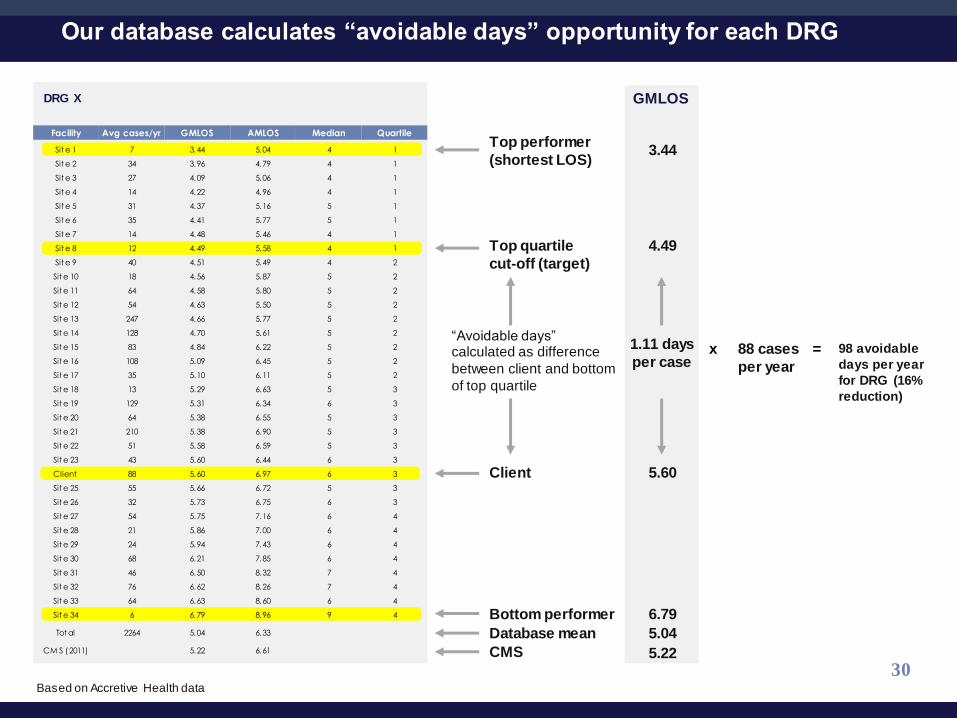

DRG X

98 avoidable

days per year

for DRG (16%

reduction)

Top performer

(shortest LOS)

Bottom performer

Top quartile

cut-off (target)

Client

“Avoidable days” calculated as difference

between client and bottom

of top quartile

Facility Avg cases/yr GMLOS AMLOS Median Quartile

Sit e 1 7 3.44 5.04 4 1

Sit e 2 34 3.96 4.79 4 1

Sit e 3 27 4.09 5.06 4 1

Sit e 4 14 4.22 4.96 4 1

Sit e 5 31 4.37 5.16 5 1

Sit e 6 35 4.41 5.77 5 1

Sit e 7 14 4.48 5.46 4 1

Sit e 8 12 4.49 5.58 4 1

Sit e 9 40 4.51 5.49 4 2

Sit e 10 18 4.56 5.87 5 2

Sit e 11 64 4.58 5.80 5 2

Sit e 12 54 4.63 5.50 5 2

Sit e 13 247 4.66 5.77 5 2

Sit e 14 128 4.70 5.61 5 2

Sit e 15 83 4.84 6.22 5 2

Sit e 16 108 5.09 6.45 5 2

Sit e 17 35 5.10 6.11 5 2

Sit e 18 13 5.29 6.63 5 3

Sit e 19 129 5.31 6.34 6 3

Sit e 20 64 5.38 6.55 5 3

Sit e 21 210 5.38 6.90 5 3

Sit e 22 51 5.58 6.59 5 3

Sit e 23 43 5.60 6.44 6 3

Client 88 5.60 6.97 6 3

Sit e 25 55 5.66 6.72 5 3

Sit e 26 32 5.73 6.75 6 3

Sit e 27 54 5.75 7.16 6 4

Sit e 28 21 5.86 7.00 6 4

Sit e 29 24 5.94 7.43 6 4

Sit e 30 68 6.21 7.85 6 4

Sit e 31 46 6.50 8.32 7 4

Sit e 32 76 6.62 8.26 7 4

Sit e 33 64 6.63 8.60 6 4

Sit e 34 6 6.79 8.96 9 4

Tot al 2264 5.04 6.33

CM S (2011) 5.22 6.61

3.44

4.49

5.60

6.79

1.11 days

per case

Database mean 5.04

CMS 5.22

GMLOS

x 88 cases

per year

=

30

Our database calculates “avoidable days” opportunity for each DRG

Based on Accretive Health data

Driving Growth Through Measured Results 31

ISQ Objectives

Lower Cost of Care

Reduce costs per inpatient encounter due to optimized resource utilization, correct care setting, and reduced practice variation

Improve Quality

Improve quality metrics (readmissions, core measures, falls, hospital-acquired infections, pressure ulcers, adverse drug events, serious safety events, medication management)

Improve Patient Satisfaction

Improve communication with patients about their condition, their care plan, and expectations for their stay and discharge plan, resulting in higher HCAHPS scores

Improve Reimbursement

Improve value-based purchasing and affordable care metrics resulting in reduced hold-backs and increased pay for above-average performance

Lower Cost of Care

Reduce costs per inpatient encounter due to optimized resource utilization, correct care setting, and reduced practice variation

Improve Quality

Improve quality metrics (readmissions, core measures, falls, hospital-acquired infections, pressure ulcers, adverse drug events, serious safety events, medication management)

Improve Patient Satisfaction

Improve communication with patients about their condition, their care plan, and expectations for their stay and discharge plan, resulting in higher HCAHPS scores

Improve Reimbursement

Improve value-based purchasing and affordable care metrics resulting in reduced hold-backs and increased pay for above-average performance

Driving Growth Through Measured Results

• Current episodic care environment offers tremendous opportunity to improve

resource utilization, reduce variation in treatment practices and ensure care is

provided in the optimal setting

• Competitors have not driven successful or sustainable results

• Accretive believes it can favorably impact length of stay and improve quality

through:

• Patient care coordination

• Physician engagement

• Optimal care setting

• Proprietary tools and technology

• Quick deployment upon contract execution

Maximizing Value in Episodic Care

32

Driving Growth Through Measured Results