Accounting Problem Book 2011

103

Principles of Accounting Problem book V.V. Dobrynskaya, V.V. Poleshchuk 2011 International College of Economics and Finance

-

Upload

sveta-chernica -

Category

Documents

-

view

408 -

download

4

Transcript of Accounting Problem Book 2011

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 1/103

Principles of Accounting

Problem book

V.V. Dobrynskaya, V.V. Poleshchuk

2011

International College of Economics and Finance

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 2/103

2

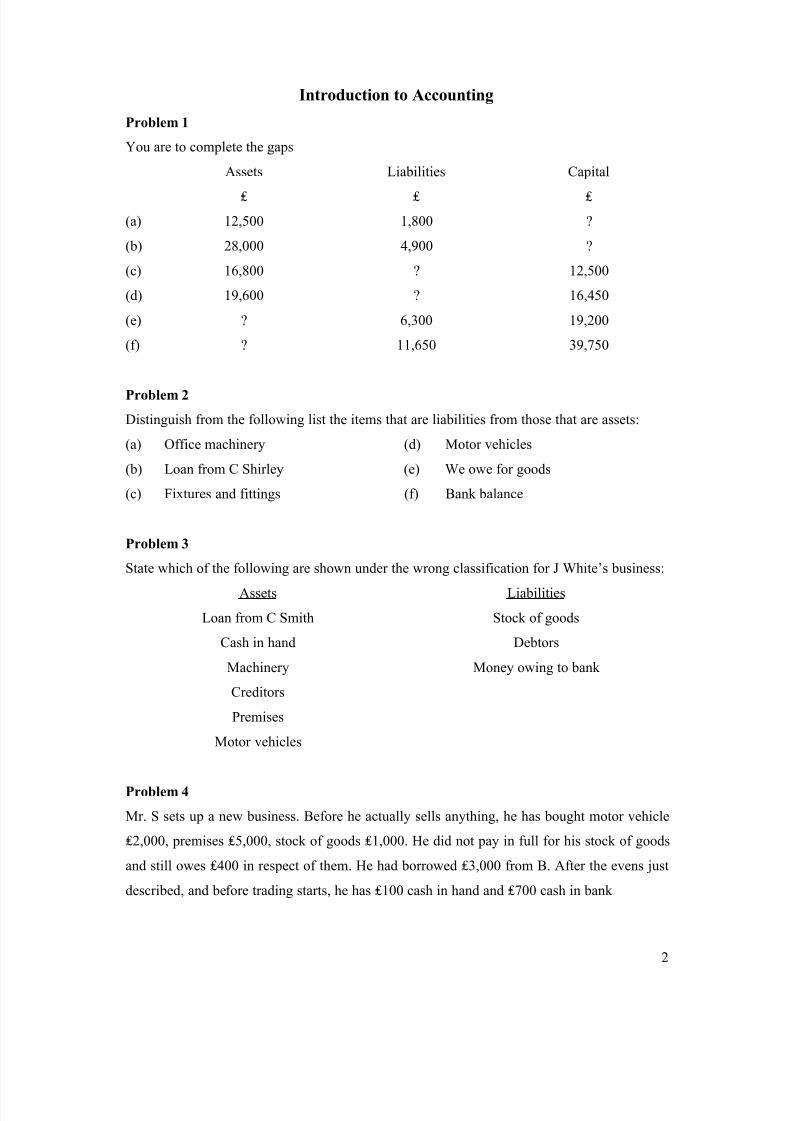

Introduction to Accounting

Problem 1

You are to complete the gaps

Assets₤

Liabilities₤

Capital₤

(a) 12,500 1,800 ?

(b) 28,000 4,900 ?

(c) 16,800 ? 12,500

(d) 19,600 ? 16,450

(e) ? 6,300 19,200

(f) ? 11,650 39,750

Problem 2

Distinguish from the following list the items that are liabilities from those that are assets:

(a) Office machinery (d) Motor vehicles

(b) Loan from C Shirley (e) We owe for goods

(c) Fixtures and fittings (f) Bank balance

Problem 3

State which of the following are shown under the wrong classification for J White‟s business:

Assets Liabilities

Loan from C Smith Stock of goods

Cash in hand Debtors

Machinery Money owing to bank

Creditors

Premises

Motor vehicles

Problem 4

Mr. S sets up a new business. Before he actually sells anything, he has bought motor vehicle

₤2,000, premises ₤5,000, stock of goods ₤1,000. He did not pay in full for his stock of goods

and still owes ₤400 in respect of them. He had borrowed ₤3,000 from B. After the evens just

described, and before trading starts, he has ₤100 cash in hand and ₤700 cash in bank

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 3/103

3

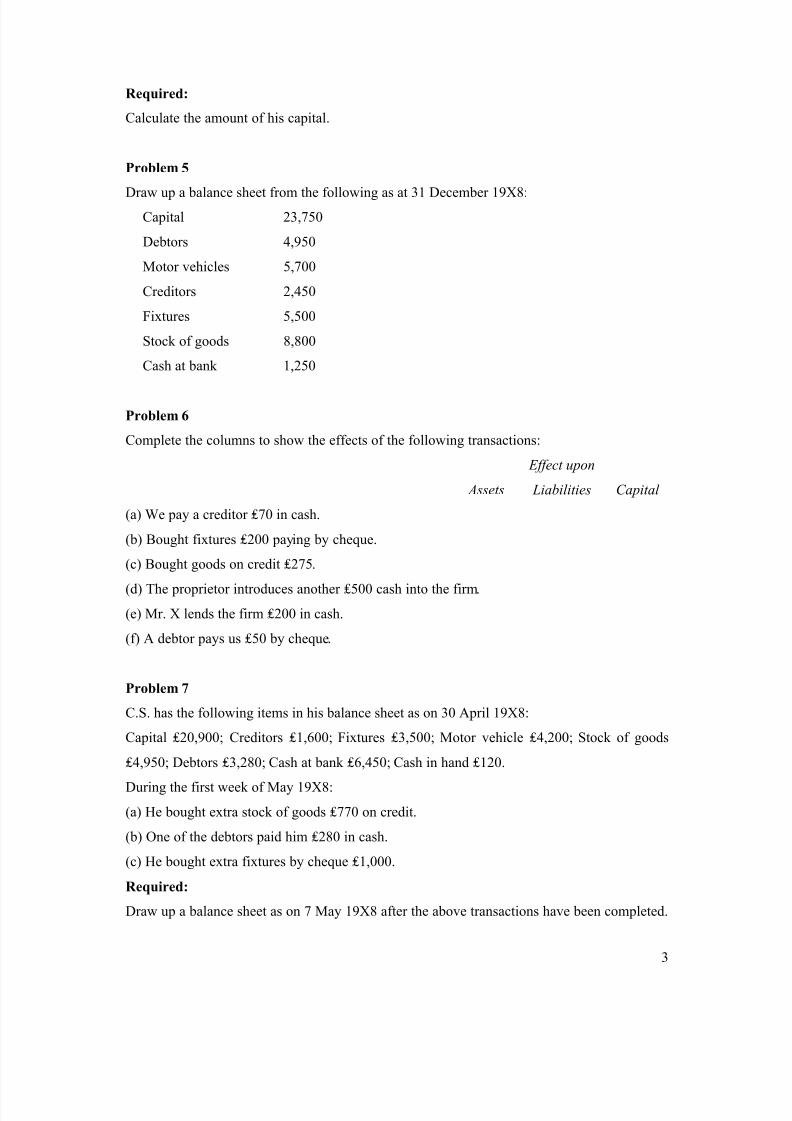

Required:

Calculate the amount of his capital.

Problem 5

Draw up a balance sheet from the following as at 31 December 19X8:

Capital 23,750

Debtors 4,950

Motor vehicles 5,700

Creditors 2,450

Fixtures 5,500

Stock of goods 8,800

Cash at bank 1,250

Problem 6

Complete the columns to show the effects of the following transactions:

Effect upon

Assets Liabilities Capital

(a) We pay a creditor ₤70 in cash.

(b) Bought fixtures ₤200 paying by cheque.

(c) Bought goods on credit ₤275.

(d) The proprietor introduces another ₤500 cash into the firm.

(e) Mr. X lends the firm ₤200 in cash.

(f) A debtor pays us ₤50 by cheque.

Problem 7

C.S. has the following items in his balance sheet as on 30 April 19X8:

Capital ₤20,900; Creditors ₤1,600; Fixtures ₤3,500; Motor vehicle ₤4,200; Stock of goods

₤4,950; Debtors ₤3,280; Cash at bank ₤6,450; Cash in hand ₤120.

During the first week of May 19X8:

(a) He bought extra stock of goods ₤770 on credit.

(b) One of the debtors paid him ₤280 in cash.

(c) He bought extra fixtures by cheque ₤1,000.

Required:

Draw up a balance sheet as on 7 May 19X8 after the above transactions have been completed.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 4/103

4

Problem 8

The following are transactions of the business for a period. You are required to state the effect

of each on the balance sheet items. Be detailed where the capital is affected, showing the type

of effect:

(a) Bought stock in trade on credit terms for ₤1,200.

(b) The owner paid a trade creditor ₤1,500 for some stock in trade bought on credit recently.

Since the owner did not have the business bank account cheque book with him, he drew a

cheque on his personal account.

(c) Stock in trade, which had cost ₤1,700, was sold on credit for ₤2,500.

(d) The owner withdrew ₤500 by drawing a cheque on the business bank account, payable to

himself.

(e) Paid wages of ₤750 by cheque.

(f) Paid bank interest of ₤100 by having amount charged on the business bank account.

(g) Received a ₤2,000 cheque from a trade debtor.

(h) Paid a trade creditor ₤1,200 by a cheque drawn on the business bank account.

Problem 9

Explain:

(a) What is a revenue?

(b) What is an expense?

(c) What is a profit?

(d) The owner pays himself a regular ₤100 from the business account each week, is it an

expense?

(e) Why is the purchase of some stock in trade not an expense?

Problem 10

Explain and provide comments:

(a) Why is it necessary to put a date in the heading of the balance sheet?

(b) Jim just bought a new motor van. Will this have an effect on the balance sheet of his

business?

(c) Comment : “Why is it that my capital is shown with the liabilities in the balance sheet of

my business? Surely it is an asset”.

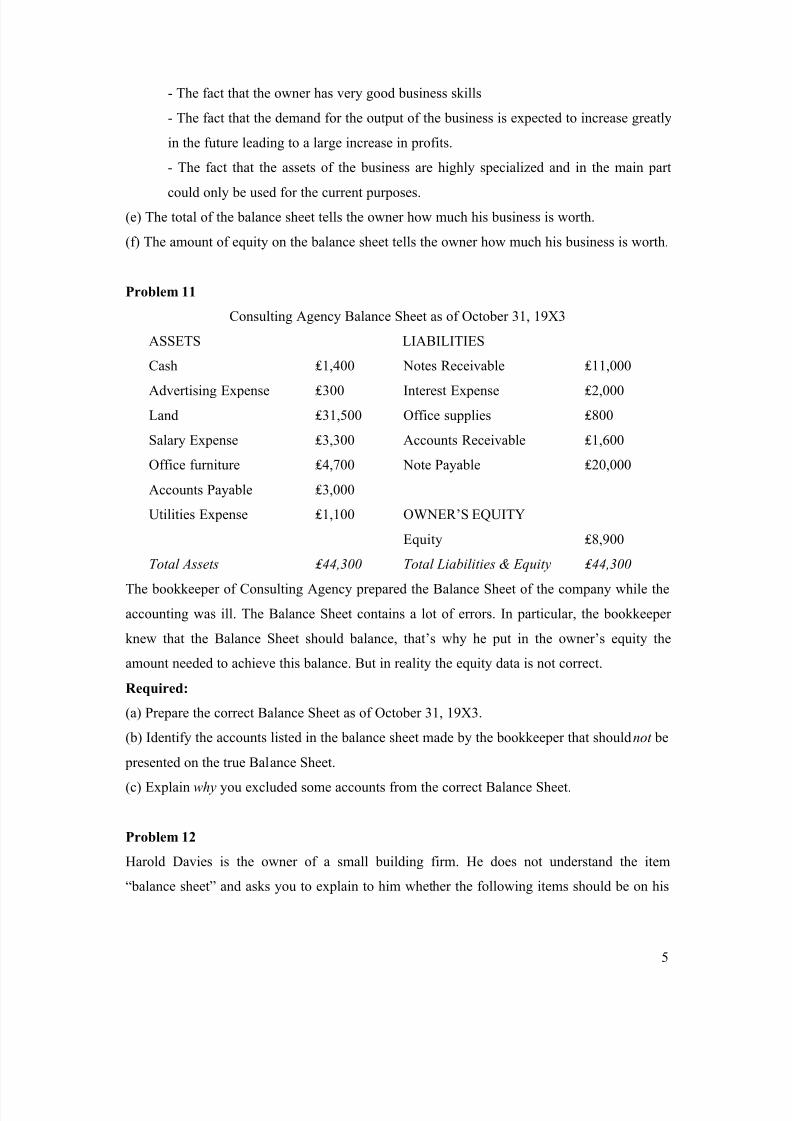

(d) Which of the following would you expect to find among the items of the balance sheet:- The fact that the business owes money

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 5/103

5

- The fact that the owner has very good business skills

- The fact that the demand for the output of the business is expected to increase greatly

in the future leading to a large increase in profits.

- The fact that the assets of the business are highly specialized and in the main part

could only be used for the current purposes.

(e) The total of the balance sheet tells the owner how much his business is worth.

(f) The amount of equity on the balance sheet tells the owner how much his business is worth.

Problem 11

Consulting Agency Balance Sheet as of October 31, 19X3

ASSETS LIABILITIES

Cash ₤1,400 Notes Receivable ₤11,000

Advertising Expense ₤300 Interest Expense ₤2,000

Land ₤31,500 Office supplies ₤800

Salary Expense ₤3,300 Accounts Receivable ₤1,600

Office furniture ₤4,700 Note Payable ₤20,000

Accounts Payable ₤3,000

Utilities Expense ₤1,100 OWNER‟S EQUITY

Equity ₤8,900

Total Assets ₤44,300 Total Liabilities & Equity ₤44,300

The bookkeeper of Consulting Agency prepared the Balance Sheet of the company while the

accounting was ill. The Balance Sheet contains a lot of errors. In particular, the bookkeeper

knew that the Balance Sheet should balance, that‟s why he put in the owner‟s equity the

amount needed to achieve this balance. But in reality the equity data is not correct.

Required:

(a) Prepare the correct Balance Sheet as of October 31, 19X3.

(b) Identify the accounts listed in the balance sheet made by the bookkeeper that should not be

presented on the true Balance Sheet.

(c) Explain why you excluded some accounts from the correct Balance Sheet.

Problem 12

Harold Davies is the owner of a small building firm. He does not understand the item

“balance sheet” and asks you to explain to him whether the following items should be on his

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 6/103

6

balance sheet. Indicate the nature of the item (e.g., current asset, long-term liability, not

applicable) and give the reason for your answer.

(a) Inventory of sand and cement

(b) Air compressor purchased for cash

(c) Air compressor hired for three weeks

(d) Wages paid to labourer

(e) Lorry used for transporting materials

(f) Diesel fuel in lorry fuel tanks

(g) Washing machine bought for Mrs. Davies

(h) Bank overdraft

(i) Petty cash in hand

(j) ₤2,000 owing to an uncle who says Harold need not pay until five years later

Problem 13

King Pharmaceuticals plc has just spent £50 million on developing a new medicine that is

expected to yield substantial profits over the next four years. Use this example to help explain

the distinction between the terms 'relevance' and 'reliability' when preparing financial

statements for shareholders. Why are 'relevance' and 'reliability' seem to be important

qualitative characteristics of accounting information?

You should structure your answer well. Your answer should not exceed 250 words.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 7/103

7

Double-Entry Bookkeeping

Problem 14

The transactions of Wheels Repair Shop for January 19X9 are shown below:

January 3 – Debby Star opened a bank account under the name of her new businessand deposited ₤30,000 in cash.

January 4 – She rented a temporary shop and paid ₤300 for the January rent, issued

cheque.

January 5 – Rented automotive tools and equipment until the firm could purchase its

own. Rent in the amount of ₤80 was paid for January, issued cheque.

January 5 – Purchased motorcycle parts and supplies described on invoice from the

Southern Supply Company for ₤400 on account.

January 10 – Purchased land as a prospective building site for ₤10,000. Paid ₤4,000 in

cash and issued a one-year note payable for the balance.

January 12 – Made repairs on George Shipman‟s motorcycle for ₤40. Shipman asked

that a charge account be opened in his name. He promised to settle the account within 30

days. This arrangement was authorized by service manager.

January 26 – Made repairs on Jay Munson‟s motorcycle for ₤180. A charge account

was opened in his name.

January 29 – Purchased motorcycle parts and supplies from Delco Supply House for

₤250 on account

January 29 – Paid the Southern Supply ₤300 on account (cheque)

January 31 – Paid electricity and water bills of ₤80 for January

January 31 – Paid ₤1,700 in salaries for the month

January 31 – Made motorcycle repairs for various cash customers for ₤4,800

January 31 – Debby Star withdrew ₤300 in cash in anticipation that at least as much

income had been earned

January 31 – Purchased automotive tools and equipment for cash ₤4,000. The list price

was 5,000.

January 31 – Paid a premium of ₤600 on a 12 months insurance policy, it becomes

effective on February 1, 19X9.

January 31 – Received a cheque for ₤10 from George Shipman.

Required:

(a) Analyze the transactions using extended accounting equation formula

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 8/103

8

(b) Journalize the transactions

(c) Post to the ledger

(d) Prepare a trial balance sheet / footing

(e) Explain adjusting entries

Problem 15

Bill Cashing sets up practice as an architect, transferring ₤20,000 of his own money on 1 June

2003 from this personal bank account into a new business bank account with NatMid Bank

plc to represent the opening capital of the business. The following transactions took place

during June 2003:

June 1 – Paid rent for office for June ₤400 by cheque.

June 1 – Purchased office equipment for ₤2,000, from Equipit Ltd on credit.

June 1 – Purchased office supplies, costing ₤300 from W Brown on credit.

June 1 – Employed an office junior at a monthly wage of ₤500.

June 5 – Surveyed a property for A Bond and sent out and invoice for ₤200.

June 7 – Decided to transfer his own car to the business at a value of ₤4,000.

June 9 – Bought petrol for the car costing ₤20, paying by cheque.

June 12 – Took a client, P Brosnan, to lunch at a cost of ₤40, paying by cheque, and

was asked to prepare plans for a new factory, for which work he estimated he would earn

₤5,000.

June 16 – Carried out another property sur vey for A Bond and invoiced him for ₤240.

June 20 – Took another possible client to lunch at a cost of ₤60, paying by cheque, but

found that he would not be able to undertake work for that client.

June 23 – Bought further office supplies from W Brown on cr edit for ₤100.

June 30 – Paid the office junior her monthly wage.

June 30- Sent a cheque to Equipit Ltd for ₤2,000.

June 30 – Sent a cheque to W Brown for office supplies for ₤300.

June 30 – Banked a cheque received from A Bond for ₤200.

June 30 – Drew out ₤500 from the bank for personal living expenses.

Required:

Enter these transactions in Bill Cashing‟s accounting records, and test the arithmetical

accuracy of your work by preparing a trial balance when you have completed the necessary

entries.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 9/103

9

Problem 16

The following transactions took place during May 19X6:

May 1 – Started firm with capital in cash of ₤250.

May 2 – Bought goods on credit from the following persons: D ₤54; C ₤87; K ₤25; B

₤76; L ₤64.

May 4 – Sold goods on credit to: CB ₤43; BH ₤62; HS ₤176.

May 6 – Paid rent by cash ₤10

May 9 – CB paid us his account by cheque ₤43.

May 10 – HS paid us ₤150 by cheque.

May 12 – We paid the following by cheque: K ₤25; D ₤54.

May 15 – Paid carriage by cash ₤23.

May 18 – Bought goods on credit from C ₤43; B ₤110.

May 21 – Sold goods on credit to BH ₤67.

May 31 Paid rent by cheque ₤18.

Required:

Enter these transactions in a company‟s accounting records, and then balance off the accounts

and extract a trial balance as at 31 May 19X6.

Problem 17

B‟s Trial Balance as on 31 December 19X6

Dr

₤

Cr

₤

Sales 18,462

Purchases 14,629

Salaries 2,150

Motor expenses 520

Rent 670

Insurance 111

General expenses 105

Premises 1,500

Motor vehicles 1,200

Debtors 1,950

Creditors 1,538

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 10/103

10

Cash at bank 1,654

Cash in hand 40

Drawings 895

Capital _____ 5,424

25,424 25,424

Stock at 31 December 19X6 was ₤2,548.

Required:

Using the trial balance of B that was extracted after one year‟s trading, prepare a trading and

profit and loss account for the year ended 31 December 19X6 and a balance sheet as on 31

December 19X6.

Problem 18

The following transactions took place during March 19X6:

March 1 – Started business with ₤800 in the bank.

March 2 – Bought goods on credit from the following persons: K ₤76; M ₤27; B ₤56.

March 5 – Cash sales ₤87.

March 6 – Paid wages in cash ₤14.

March 7 – Sold goods on credit to: H ₤35; L ₤42; J ₤72.

March 9 – Bought goods for cash ₤46

March 10 – Bought goods on credit from M ₤57; B ₤98.

March 12 – Paid wages in cash ₤14.

March 13 – Sold goods on credit to: L ₤32; J ₤23.

March 15 – Bought shop fixtures on credit from B Ltd ₤50.

March 17 – Paid M by cheque ₤84.

March 18 – We returned goods to B ₤20.

March 21 – Paid B Ltd a cheque for ₤50.

March 24 – J paid us his account by cheque ₤95.

March 27 – We returned goods to K ₤24.

March 30 – J lent us ₤60 by cash.

March 31 – Bought a motor van paying by cheque ₤400.

Required:

Enter these transactions in a company‟s accounting books, and then balance off the accounts

and extract a trial balance as at 31 March 19X6.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 11/103

11

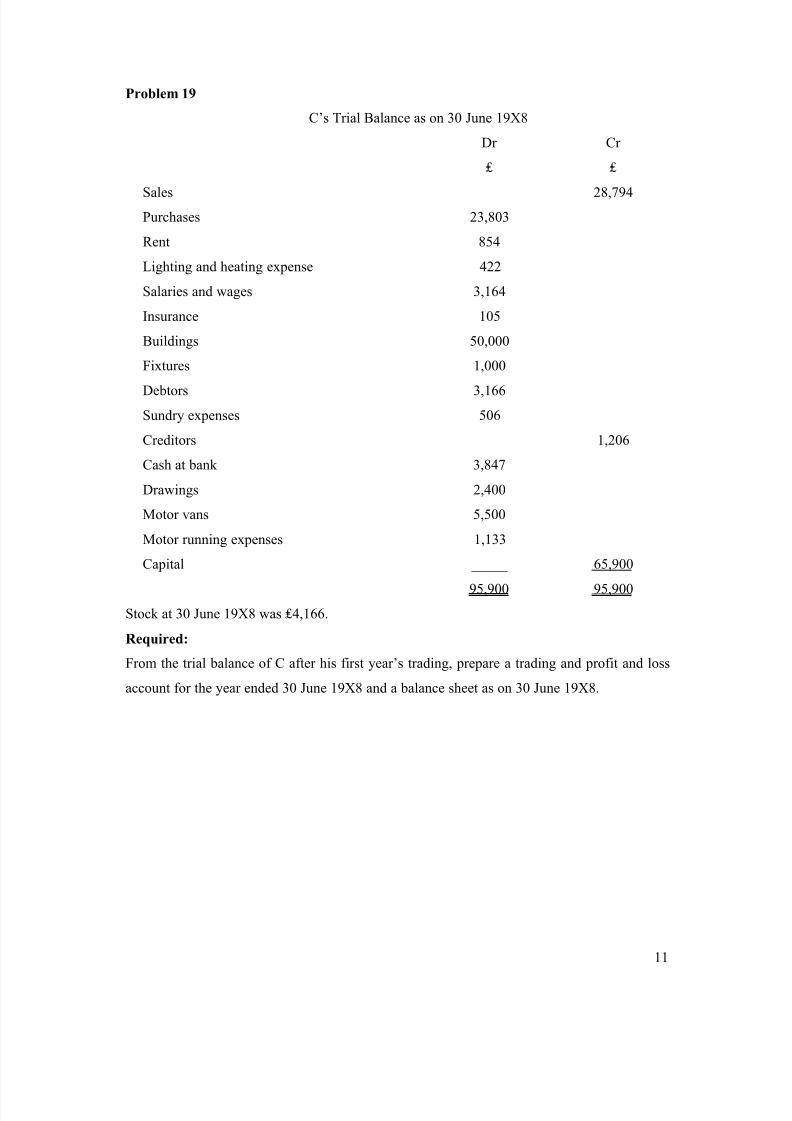

Problem 19

C‟s Trial Balance as on 30 June 19X8

Dr

₤

Cr

₤

Sales 28,794

Purchases 23,803

Rent 854

Lighting and heating expense 422

Salaries and wages 3,164

Insurance 105

Buildings 50,000

Fixtures 1,000

Debtors 3,166

Sundry expenses 506

Creditors 1,206

Cash at bank 3,847

Drawings 2,400

Motor vans 5,500

Motor running expenses 1,133

Capital _____ 65,900

95,900 95,900

Stock at 30 June 19X8 was ₤4,166.

Required:

From the trial balance of C after his first year‟s trading, prepare a trading and profit and loss

account for the year ended 30 June 19X8 and a balance sheet as on 30 June 19X8.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 12/103

12

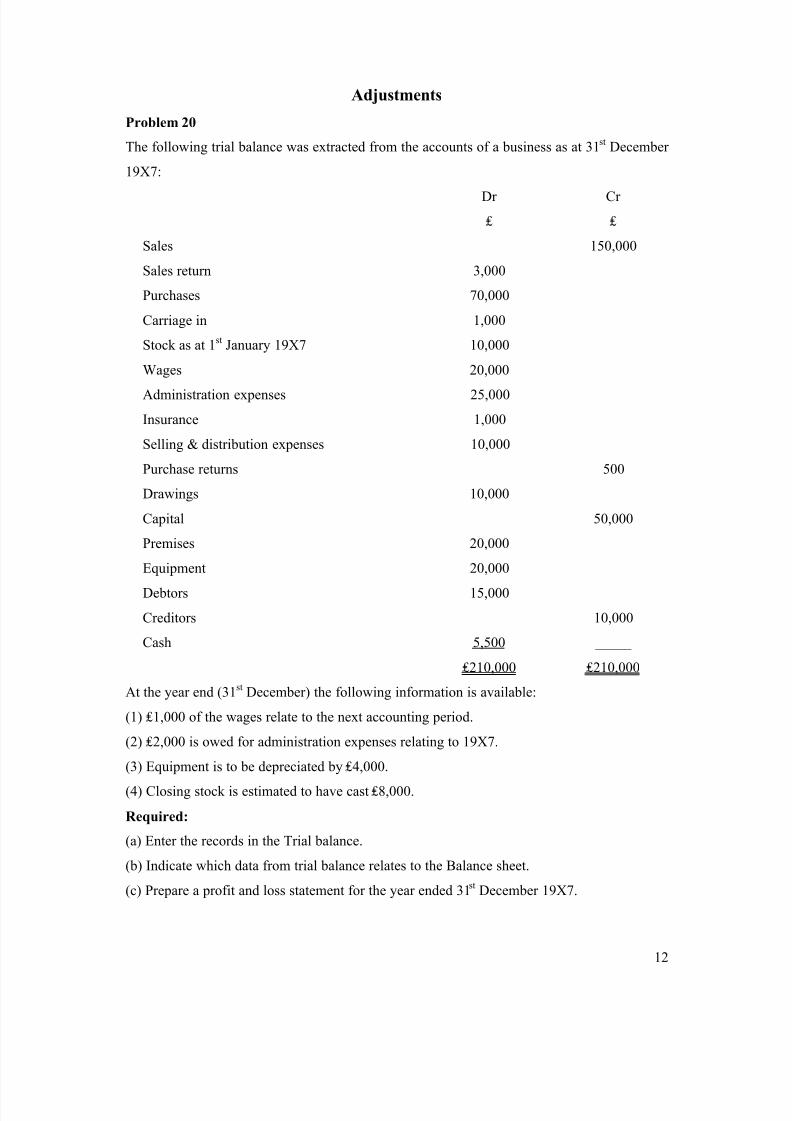

Adjustments

Problem 20

The following trial balance was extracted from the accounts of a business as at 31 st December

19X7:Dr

₤

Cr

₤

Sales 150,000

Sales return 3,000

Purchases 70,000

Carriage in 1,000

Stock as at 1st January 19X7 10,000

Wages 20,000

Administration expenses 25,000

Insurance 1,000

Selling & distribution expenses 10,000

Purchase returns 500

Drawings 10,000

Capital 50,000

Premises 20,000

Equipment 20,000

Debtors 15,000

Creditors 10,000

Cash 5,500 _____

₤210,000 ₤210,000

At the year end (31st December) the following information is available:

(1) ₤1,000 of the wages relate to the next accounting period.

(2) ₤2,000 is owed for administration expenses relating to 19X7.

(3) Equipment is to be depreciated by ₤4,000.

(4) Closing stock is estimated to have cast ₤8,000.

Required:

(a) Enter the records in the Trial balance.

(b) Indicate which data from trial balance relates to the Balance sheet.

(c) Prepare a profit and loss statement for the year ended 31st December 19X7.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 13/103

13

(d) Explain the role of adjustments you made.

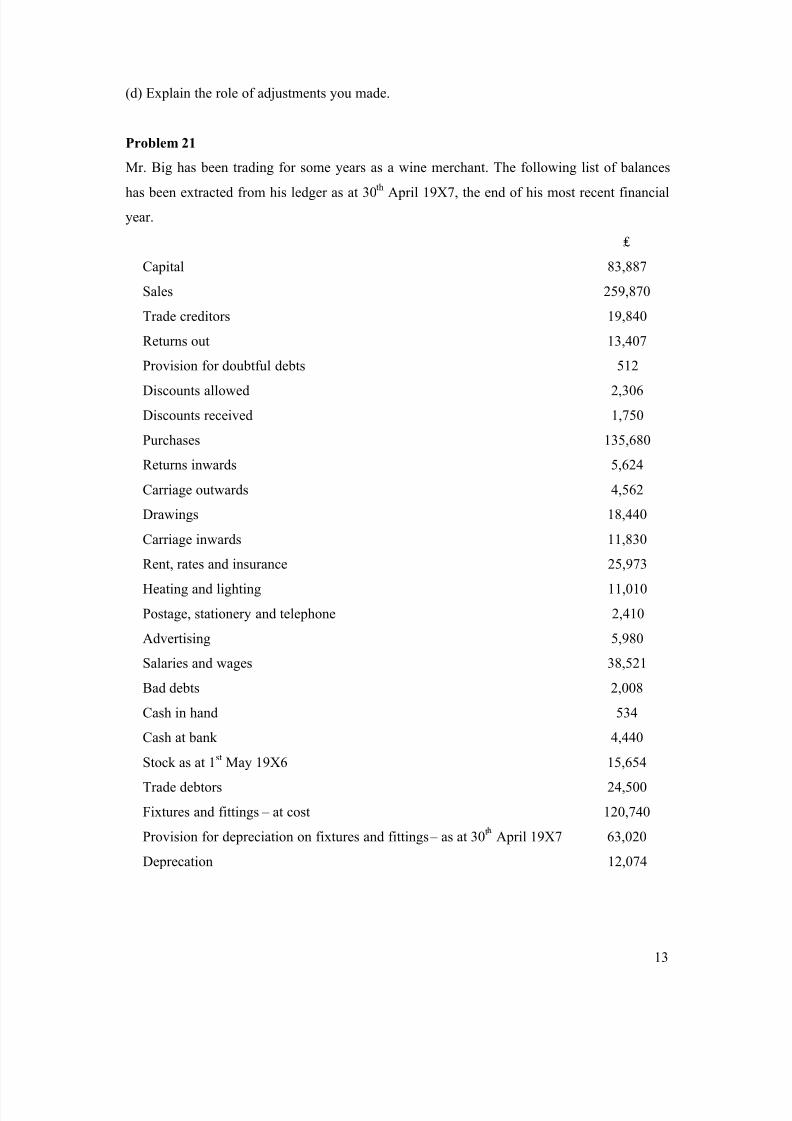

Problem 21

Mr. Big has been trading for some years as a wine merchant. The following list of balances

has been extracted from his ledger as at 30 th April 19X7, the end of his most recent financial

year.

₤

Capital 83,887

Sales 259,870

Trade creditors 19,840

Returns out 13,407

Provision for doubtful debts 512

Discounts allowed 2,306

Discounts received 1,750

Purchases 135,680

Returns inwards 5,624

Carriage outwards 4,562

Drawings 18,440

Carriage inwards 11,830

Rent, rates and insurance 25,973

Heating and lighting 11,010

Postage, stationery and telephone 2,410

Advertising 5,980

Salaries and wages 38,521

Bad debts 2,008

Cash in hand 534

Cash at bank 4,440

Stock as at 1st May 19X6 15,654

Trade debtors 24,500

Fixtures and fittings – at cost 120,740

Provision for depreciation on fixtures and fittings – as at 30t April 19X7 63,020

Deprecation 12,074

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 14/103

14

The following additional information as at 30th April 19X7 is available:

(1) Stock at the close of business was valued at ₤17,750.

(2) Insurances have been prepaid by ₤1,120.

(3) Heating and lighting is accrued by ₤1,360.

(4) Rates have been prepaid by ₤5,435.

(5) The provision for doubtful debts is to be adjusted so that it is 3% of trade debtors.

Required:

Prepare Mr. Big‟s trading and profit and loss account for the year ended 30th April 19X7 and a

balance sheet (in vertical format) as at that date.

Problem 22

The following trial balance was extracted from the books of Charles as the close of business

on 28 February 19X7.

Dr

₤

Cr

₤

Purchases and sales 11,280 19,740

Cash at bank 1,140

Cash in hand 210

Capital account 1st March 19X6 9,900

Drawings 2,850

Office furniture 1,440

Rent 1,020

Wages and salaries 2,580

Discounts 690 360

Debtors and creditors 4,920 2,490

Stock 1st March 19X6 2,970

Provision for doubtful debts 1st March 19X6 270

Delivery van 2,400

Van running costs 450

Bad debts written off 810

₤32,760 ₤32,760

The following additional information as at 28th

February 19X7 is available:(1) Stock at 28th February 19X7 ₤3,510.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 15/103

15

(2) Wages and salaries accrued at 28th February 19X7 ₤90.

(3) Rent prepaid at 28th February 19X7 ₤140.

(4) Van running costs owing at 28th February 19X7 ₤60.

(5) Increase the provision for doubtful debts by ₤60.

(6) Provide for depreciation as follows: Office furniture ₤180; Delivery van ₤480.

Required:

Draw up the trading and profit and loss account for the year ending 28th February 19X7

together with a balance sheet as on 28th February 19X7, using vertical formats throughout.

Problem 23

The balance sheet of Johnson‟s shop as at 1st October 19X7 was as follows:

₤ ₤ ₤ ₤

Fixed assets Capital

Shop premises 45,000 At 1 October 19X7 51,000

Shop fittings 12,000

Delivery van 4,000 61,000

Current assets Current liabilities

Stock in trade 14,000 Trade creditors 12,000

Cash in hand 2,000 16,000 Bank overdraft 14,000 26,000

₤77,000 ₤77,000

The following in a summary of the transactions which took place during the year to 30th

September 19X8:

(1) Sales were made, all for cash, of ₤145,000. The stock in trade sold cost ₤83,000.

(2) Stock in trade was bought, all on credit, for ₤78,000.

(3) Cash of ₤113,000 was taken from the till (cash register) and paid into the bank.

(4) The trade creditors were paid ₤73,000 by cheque.

(5) Johnson borrowed ₤30,000 from Black which was paid into the bank. The loan is for 5

years.

(6) Wages of ₤17,000 were paid by cash.

(7) Rates of ₤2,900 were paid by cheque.

(8) Additional shop fittings costing ₤9,000 were bought and paid for by cheque

(9) The bank charged overdraft interest of ₤2,000 direct to the account.(10) Sundry expenses of ₤6,000 were paid in cash.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 16/103

16

(11) Electricity bills of ₤1,600 were paid by cheque.

(12) The owners of the business withdrew ₤9,000 in cash.

At 30th September 19X8 you discover the following:

(13) Interest ₤2,500 due to Black for the year was unpaid.

(14) Shop fittings are to be depreciated at 10% per annum on the total at the year end; the

delivery van is to be depreciated by 20% per annum of the total at the year end.

(15) The rates payments during the year included ₤1,000 in respect of the period 1.10.19X8 to

31.3.19X9.

(16) The electricity bill for the quarter to 30.9.19X8 for ₤500 was unpaid.

Required:

Prepare a balance sheet (in vertical format) as at 30th September 19X8 and a profit and loss

account for the year to that date.

Problem 24

Adagio plc. is a wholesale supplier of musical instruments to the retail and educational

sectors. The bookkeeper has extracted the following balances from the accounting records for

the year ended 31st May 2010. The totals of the debit and credit balances did not agree, and

the balancing figure was placed in a suspense account.

£000

Freehold property, at cost 3,600

Plant, equipment and vehicles, at cost 2,060

Provision for depreciation at 1st June 2009

Freehold buildings 440

Plant, equipment and vehicles 1,080

Purchases 13,100

Sales 21,180

Distribution and selling costs 2,300

Administration costs 1,240

Directors remuneration 1,110

Inventories at 1st June 2009 1,320

Trade creditors 972

Trade debtors 1,834

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 17/103

17

Bank balances 95

Ordinary share capital (£1 shares, fully paid) 3,300

Retained earnings at 1st June 2009 222

Loan interest paid 30

10% loan, repayable in 2015 500

Suspense account (debit balance) 1,005

The following information is available.

(1) The accountant of Adagio plc. has now reviewed the accounting records and has

discovered the following errors which require adjustment:

(i) On 31st May 2010 stocks were valued at £1,280,000. This figure has been credited to the

purchases account but no other entries have been made.

(ii) A motor vehicle was sold for cash on 1st June 2009 for £15,000. The cash received has

been recorded in the cash book but no other entries have been made. The motor vehicle

originally cost £40,000 on 1st June 2008.

(iii) A debtor balance of £130,000 was eliminated from the trade debtors balance as it was

considered to be irrecoverable. No other entries have been made.

(iv) A directors‟ bonus of £390,000 was calculated on the basis of expected profits and was

added to the directors‟ remuneration account but no other entries were made.

(2) No provision has been made at the year-end for the following:

(i) Depreciation on plant, equipment and vehicles at 10% on the straight line method. There

are no fully depreciated assets in this category.

(ii) Depreciation at 5% on cost of freehold buildings which represent 25% of the cost of

freehold property.

Depreciation charges and profits or losses on asset disposals are allocated 50% to cost of sales

and 25% each to distribution costs and administration costs.

(3) Directors‟ remuneration is allocated as 80% to administration and 20% to selling costs.

Bad debts written off are treated as selling costs.

(4) Provision is required at the year-end for:

(i) outstanding loan interest,

(ii) auditors‟ remuneration of £80,000, (treated as administration costs),

(iii) corporation tax for the year of £600,000

(5) The company has paid insurance premiums of £20,000 relating to periods after the year

end. Insurance is included in administration costs.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 18/103

18

Required:

(a) Prepare a profit and loss account for Adagio plc. for the year ended 31 st May 2010 and a

balance sheet as at that date in a form suitable for the directors.

(b) During the year the company had paid £40,000 training costs which were included in

administration costs. The human resources director has argued that this should not be seen as

an expense but as an asset. Briefly discuss her proposal.

Problem 25

The draft accounts prepared for the directors of Snodrop plc. for the year ended 31 December

1999 show a profit before taxation of £573,580. In the course of subsequent checking, the

following errors and omissions were found:

(1) During the year the company had acquired an additional factory unit at an annual rent of

£64,000, payable quarterly in advance commencing on 31 March 1999. By 31 December

1999 four quarterly payments had been made. The total paid during the year had been treated

as capital expenditure and included in fixed assets. No depreciation had been provided on the

factory unit.

(2) Some goods were included in the closing stock valuation at their selling price of £9,750.

The gross profit margin on these goods was 30%.

(3) A delivery vehicle held as a fixed asset had been sold during the year for £5,200. The

original cost was £16,000 and, at 1 January 1999, depreciation of £9,600 had been provided.

The proceeds of sale had been credited to sales account. The company depreciates delivery

vehicles at 20% per year using straight-line basis. Its policy is to provide for depreciation in

the year of purchase but not in the year of sale.

(4) The brought forward balance of £1,700 for the accrued telephone charges at 1 January

1999 had been omitted when calculating the year‟s telephone charge.

(5) £9,820, being the total of returns inwards for the year, had been credited to purchases and

debited to trade creditors.

(6) At 1 January 1999 there was a provision for doubtful debts of £29,320. Snodrop plc. has a

policy of making a 3% provision for doubtful debts based on closing trade debtors. The entry

for 31 December had not been made and the trade debtors then totaled £1,260,500.

(7) Items included in closing stock at £7,900, and which would normally be sold for £10,200,

were in a damaged state and were worth only £6,850.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 19/103

19

(8) A legal action brought against the company during 1999 for damage to property was

decided shortly after the balance sheet date and, as a result, it will have to pay costs and

damages totaling £24,000. No provision had been made in the accounts for this event.

(9) Salaries paid for October 1999 of £24,530 had been incorrectly recorded as £42,530.

There was a compensating error affecting trade creditors which meant that the end of year

trial balance agreed.

Required:

(a) Calculate the correct figure for Snodrop plc. for profit before taxation for 1999. Show each

adjustment separately and indicate which entries in the draft trading and profit and loss

account are affected. If you consider that any of the above information does not affect profit

explain clearly why this is the case.

(b) Identify, and briefly explain, the reasons for your adjustments relating to (1), (2), (6) and

(8) above. Refer to accounting concepts where relevant.

Problem 26

Ko-Furn Limited is an office furniture manufacturer. The following is a list of balances

extracted from its accounting records at 31 December 2009:

Dr Cr

000$ 000$

Land, at valuation 240

Buildings: cost 500

Buildings: accumulated depreciation at 1.1.09 180

Equipment: cost 392

Equipment: accumulated depreciation at 1.1.09 152

Vehicles: cost 568

Vehicles: accumulated depreciation at 1.1.09 264

Inventory at 1.1.09 214

Trade receivables 366

Provision for doubtful debts at 1.1.09 16

Prepayment at 1.1.09 12

Accrual at 1.1.09 18

Cash 408

Trade payables 248

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 20/103

20

Share capital: ordinary 50c shares 50

Share premium 350

Retained earnings 606

Sales 2,924

Purchases 976

Wages and salaries 540

Distribution costs 200

Other administrative expenses 360

Corporation tax 12

Disposal account 20

Dividend paid 40

4,828 4,828

You are given the following information:

(1) Ko-furn prices its furniture using a normal 30% mark-up policy. A stock count carried out

at 31 December 2009 valued stock at selling price of $325,000. This included two board

tables at normal selling price of $20,800 each, which the directors have decided should be

reduced in price to $5,000 each.

(2) The land was valued at $600,000 at 31 December 2009. The directors decided to reflect

the revalued amount in the balance sheet.

(3) On 1 February 2009, the company sold a vehicle for $20,000. While the proceeds of sale

were credited to the Disposal account, no other entries were made in the books of account in

relation to this transaction. The vehicle had cost $88,000 in August 2006. The company

charges a full year‟s depreciation in the year of acquisition and no depreciation in the year of

disposal.

(4) The company‟s depreciation policy is as follows:

Land: nil

Buildings: 4% straight line

Equipment: 40% reducing balance

Vehicles: 25% straight line.

(5) Trade receivables at 31 December 2009 include a debt of $16,000 from a customer

recently declared bankrupt. The company has decided to maintain the provision for doubtful

debts at 4% of remaining trade receivables.

(6) The balance of prepayments at 1.1.09 refers to insurance charges. Prepaid insurance,included in general distribution costs at 31 December 2009 amounted to $24,000.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 21/103

21

(7) The balance of accruals at 1.1.09 refers to electricity charges. After the year end, the

company received an electricity invoice for $30,000 covering the period 1 November 2009 to

31 January 2010. Electricity charges are included in other administrative expenses.

(8) Corporation tax for the year ended 31 December 2009 is estimated to be $190,000.

(9) The company issued 100,000 additional shares at 50c each on 30 December 2009 for

$140,000. This transaction has not been recorded in the accounting records.

Required:

Prepare an income statement for the year ended 31 December 2009 and a balance sheet at that

date, in good style, for the directors.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 22/103

22

Accounting for Current Assets

Problem 27

Bought Sold

January 10 at ₤30 each April 8 for ₤46 each March 10 at ₤34 each December 12 for ₤56 each

September 20 at ₤40 each

Required:

(a) Calculate the closing stock-in-trade that would be shown using (i) FIFO, (ii) LIFO, (iii)

AVCO methods on a perpetual inventory basis.

(b) Draw up the trading account for the year showing the gross profits that would have been

reported using (i) FIFO, (ii) LIFO, (iii) AVCO methods.

Problem 28

Bought Sold

January 24 at ₤10 each June 30 for ₤16 each

April 16 at ₤12.50 each November 34 for ₤18 each

October 30 at ₤13 each

Required:

(a) Calculate the closing stock-in-trade that would be shown using (i) FIFO, (ii) LIFO, (iii)

AVCO methods on a perpetual inventory basis.

(b) Draw up the trading account for the year showing the gross profits that would have been

reported using (i) FIFO, (ii) LIFO, (iii) AVCO methods.

Problem 29

An evaluation of a physical stock count on 30 th April, 19X2 in respect of the financial year

ending on that date at Cranfleet Commodities has produced a figure of ₤187,033.

The firm‟s book-keeper has approached you, as the accountant, for assistance in dealing with

the following matters to enable him to arrive at a final figure of closing stock for inclusion in

the annual accounts:

(1) 320 components included at their original cost of ₤11 each can now be bought in for only

₤6 each due to over production by the manufacturer. This drop in price is expected to be only

temporary and the purchase price is expected to exceed its original figure within 12 months.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 23/103

23

Cranfleet Commodities intends to continue selling the existing stock at the present price of

₤15 each.

(2) It has been discovered that certain items which had cost ₤5,657 have been damaged. It will

cost ₤804 to repair them after which they can be sold for ₤6,321.

(3) On one stock sheet a sub-total of ₤9,105 has been carried forward as ₤1,095.

(4) 480 units which cost ₤1.50 each have been extended at ₤15.00 each.

(5) The firm has sent goods with a selling price of ₤1,500 (being cost plus 25%) to a customer

on a sale or return basis. At 30th April 19X2, the customer had not signified acceptance, but

the goods have not been returned, and consequently had not been included in the physical

stock count.

(6) Included in stock were goods bought on credit for ₤4,679 from Byfleet Enterprises. At 30th

April 19X2, Cranfleet Commodities had not paid this account.

(7) Byfleet Enterprises had also sent some free samples (for advertising purposes only). These

have been included in stock at their catalogue price of ₤152.

Required:

Taking account of such of the above facts as are relevant, calculate a closing stock figure for

inclusion in the 19X2 annual accounts of Canfleet Commodities, giving reasons for the action

you have taken in each individual case.

Problem 30

The draft accounts of Trayderrs plc for the year ended 31 st December 1998 show a net profit

before tax of ₤543,350 and closing stock at cost of ₤316,740 following a physical stock count.

During the audit of the accounts the following matters have come to light:

(1) Stock costing ₤25,000 has been omitted from the closing stock figure.

(2) Items included in stock at ₤10,200, and which would normally be sold for ₤18,350, were

in a damaged state and were worth only ₤7,600.

(3) Trayderrs plc received an order on 27th December 1998 to supply goods at a total price of

₤52,000. The goods, which had cost ₤34,000, were moved on the following day from the

warehouse to the packing department and were dispatched on 3rd January 1999 when the

customer was invoiced. Trayderrs plc had included the order in sales for 1998 and had

excluded the goods from closing stock.

(4) 3,100 items costing ₤21 each were recorded on the stock sheets in error as 1,300 items at

₤12 each.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 24/103

24

(5) Stock costing ₤10,000 was lost in a fire in the warehouse during the year. The company‟s

insurers have agreed to pay Trayderrs plc ₤11,200 in respect of its insurance claim. No entry

has yet been made in the accounting records.

(6) Included in purchases is ₤41,500 for goods purchased in December and which were

received into the warehouse on 5th January 1999.

(7) Stock costing ₤18,000 has in error been treated as a fixed asset and depreciation of 10% of

cost has been provided for.

(8) Returned stock costing ₤825 has been treated in the accounting records as a return inward

instead of a return outward.

(9) An item is included in the closing stock valuation at its selling price of ₤8,200. The gross

profit margin on this item is 40%.

Required:

(a) Calculations to show the correct figure for Trayderrs plc for

(i) stock at 31st December 1998, and

(ii) net profit before tax for 1998.

(b) Your answer to the following questions posed by the purchasing director of Trayderrs plc:

“Prices are rising all the time and I think we should change our stock valuation method from

FIFO to LIFO or average cost. What do you think about this? Can we do it?”

Problem 31

On 30th April 2009 the closing balance on the creditors control account of Dyson Ltd is

₤2,900. The total of the list of balances from the creditors ledger is ₤3,990. Further

investigation reveals the following errors:

(1) An invoice of ₤600 for goods purchased was included in the creditors ledger but was not

recorded in the purchases day book.

(2) A cash payment of ₤400 to a supplier recorded in the cash book was not recorded in the

creditors ledger.

(3) A cash payment of ₤560 was correctly recorded in the creditors ledger but was recorded as

₤650 in the cash book.

(4) An invoice for ₤250 was not recorded in either the purchase day book or the creditors

ledger.

Required:

Show the corrected total of the list of creditors ledger balances and the corrected balance onthe creditors control account at 30th April 2009.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 25/103

25

Problem 32

Waits opened a business bank account with ₤16,000 on 1st April 2009. During April he issued

cheques totaling ₤72,760 and banked cheques totaling ₤80,060. These transactions were

entered into his cash book up to 30 th April 2009. On receiving his bank statement for April he

discovered the following:

(1) A cheque for ₤4,800, which was banked (and included in the receipts above), had been

returned by the bank marked “No funds available”. No adjustment has been made in the cash

book.

(2) Bank charges debited on the bank statement for April amounted to ₤600. No entries for

these have been made in the cash book.

(3) Cheques totaling ₤16,860 recorded in the cash book and sent to suppliers were not

presented to the bank until May 2009.

(4) Cheques totaling ₤12,100 had been entered into the cash book but not credited by the bank

until May 2009.

Required:

Calculate the corrected bank balance which should appear in the business cash book at 30 th

April 2009 and prepare a bank reconciliation statement at 30 th April 2009.

Problem 33

Miss Leung runs a business selling holidays. At 31 January 2010, the balance on the creditors

control account was $8,700. The total of the list of balances in the creditors ledger was

$11,720. The following information has come to light:

(i) an invoice of $750 was not recorded in the purchase day book

(ii) a cash payment of $1,680 was correctly recorded in the cash book but was recorded as

$1,860 in creditors ledger.

(iii) A cash payment of $1,200 to a supplier was recorded in the cash book but was not

recorded in the creditors ledger.

(iv) A credit note for a price reduction from a supplier of $1,800 was recorded in the purchase

day book but not recorded in the creditors ledger.

(v) In January, the company paid a refund of $200 to a customer for a price reduction. This

was wrongly treated as a payment to a supplier and entered in the Creditors Control Account.

Required:

Show the corrections to the:(a) list of creditors ledger balance at 31 January 2010 and

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 26/103

26

(b) creditors control account at 31 January 2010.

Problem 34

In preparing the trial balance, you notice that the debit side exceeds the credit side by $970.

Upon investigation, you identify the following mistakes:

(1) Goods returned to suppliers amounts to $250 have been entered as a debit in the goods

returns outward account by mistake.

(2) A cash payment for $560 has been entered in the cash book as $650.

(3) A computer purchased for $2,000 as at office machine has been entered as debit in the

purchases account.

(4) A credit note for $220 given to a customer has been credite d twice in the customer‟s

account.

(5) A cheque for $780 from a customer has been entered in the cash book and subsequently

banked before the year end. However, no other entry has been made to the customer‟s

account.

Required:

Explain how each of the above mistakes should be dealt with by means of a suspense account.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 27/103

27

Accounting for Fixed Assets

Problem 35

A company started in business on 1st January 19X1. Bought two motor vans for ₤1,200 each

on 1

st

January 19X1. Bought one motor van for ₤1,400 on 1

st

July 19X1.Required:

Write up the motor vans account and the provision for depreciation account for the year ended

31st December 19X1. Depreciation is at the rate of 20 per cent per annum, using the basis of

one month‟s ownership needs one month‟s depreciation.

Problem 36

A company maintains its fixed assets at cost. Depreciation provision accounts for each asset

are kept. At 31st December 19X8 the position was as follows:

Total cost

to date

Total depreciation

to date

Machinery 52,590 25,670

Office furniture 2,860 1,490

(1) The following additions were made during the financial year ended 31st December 19X9:

Machinery ₤2,480, office furniture ₤320.

(2) Some old machines bought in 19X5 for ₤2,800 were sold for ₤800 during the year.

(3) The rates of depreciation are: Machinery 10 per cent, office equipment 5 per cent, using

the straight line basis, calculated on the assets in existence at the end of each financial year

irrespective of date of purchase.

Required:

Show the asset and depreciation accounts for the year ended 31st December 19X9 and the

balance sheet entries at that date.

Problem 37

A firm buys a fixed asset for ₤10,000. The firm estimates that the asset will be used for 5

years. After exactly 2½ years, however, the asset is suddenly sold for ₤5,000. The firm always

provides a full year‟s depreciation in the year of purchase and no depreciation in the year of

disposal.

Required:

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 28/103

28

(a) Write up the relevant accounts including disposal account but not profit and loss account

for each of Years 1, 2 and 3:

(i) Using the straight line depreciation method (assume 20% p.a.);

(ii) Using the reducing balance depreciation method (assume 40% p.a.);

(b) What is the purpose of deprecation? In what circumstances would each of the two

methods you have used be preferable?

(c) What is the meaning of the net figure for the fixed asset in the balance sheet at the end of

Year 2?

(d) If the asset was bought at the beginning of Year 1, but was not used at all until Year 2 (and

it is confidently anticipated to last until Year 6), state under each method the appropriate

depreciation charge in Year 1, and briefly justify your answer.

Problem 38

A company depreciates its plant at the rate of 20% per year, straight line method, for each

month of ownership. Details:

19X4 bought plant costing 900 on January 1

bought plant costing 600 on October 1

19X6 bought plant costing 550 on July 1

19X7 sold plant which had been bought for 900 on 1st January 19X4 for the sum of 275 on

30th September 19X7.

Required:

Draw up:

(a) the Plant account

(b) the Provision for depreciation account

(c) Disposal account

(d) extracts from the Balance sheet at the end of each year.

Problem 39

Explain:

(a) How is the consistency concept applied to depreciation?

(b) Since the calculation of depreciation is based on estimate, why bother to make this

calculation?

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 29/103

29

Problem 40

At the beginning of the financial year commencing on 1st April 19X5, a company had a

balance on plant account of £372,000 and on provision for depreciation of plant account of

£205,400.

The company‟s policy is to provide depreciation using the reducing balance method applied

to the fixed assets held at the end of the financial year at the rate of 20 % per annum.

On 1st September 19X5 the company sold for £13,700 some plant which it had acquired on 31

October 19X1 at a cost of £36,000. Additionally, installation costs totalled £4,000. During

19X3 major repairs costing £6,300 had been carried out on this plant and, in order to increase

the capacity of the plant, a new motor had been fitted in December 19X3 at a cost of £4,400.

A further overhaul costing £2,700 had been carried out during 19X4.

The company acquired a new replacement plant on 30th November 19X5 at a cost of £96,000,

inclusive of installation charges of £7,000.

Required:

Calculate the following:

(a) the balance of plant at cost at 31 st March 19X6

(b) the provision for depreciation of plant at 31st March 19X6

(c) the profit or loss on disposal of the plant.

Problem 41

On 1 January 1998 Ay Ltd bought some factory equipment for £100,000. There was no

estimated residual value and the equipment is being depreciated using the decreasing-balance

method at the rate of 20% per year.

At the end of 2000 the market value of the equipment is expected to be £40,000 due to a more

advanced design having appeared on the market. The equipment is as efficient in operation as

originally anticipated and there is no intention of replacing it during the next few years.

Required:

(a) Referring to accounting concepts and to the above information, explain whether or not the

annual charge for depreciation of the equipment needs amending and what the charge for

2000 should be.

Problem 42

The Cirrus Company Ltd has the following balances on its books at 31st

December 19X0:

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 30/103

30

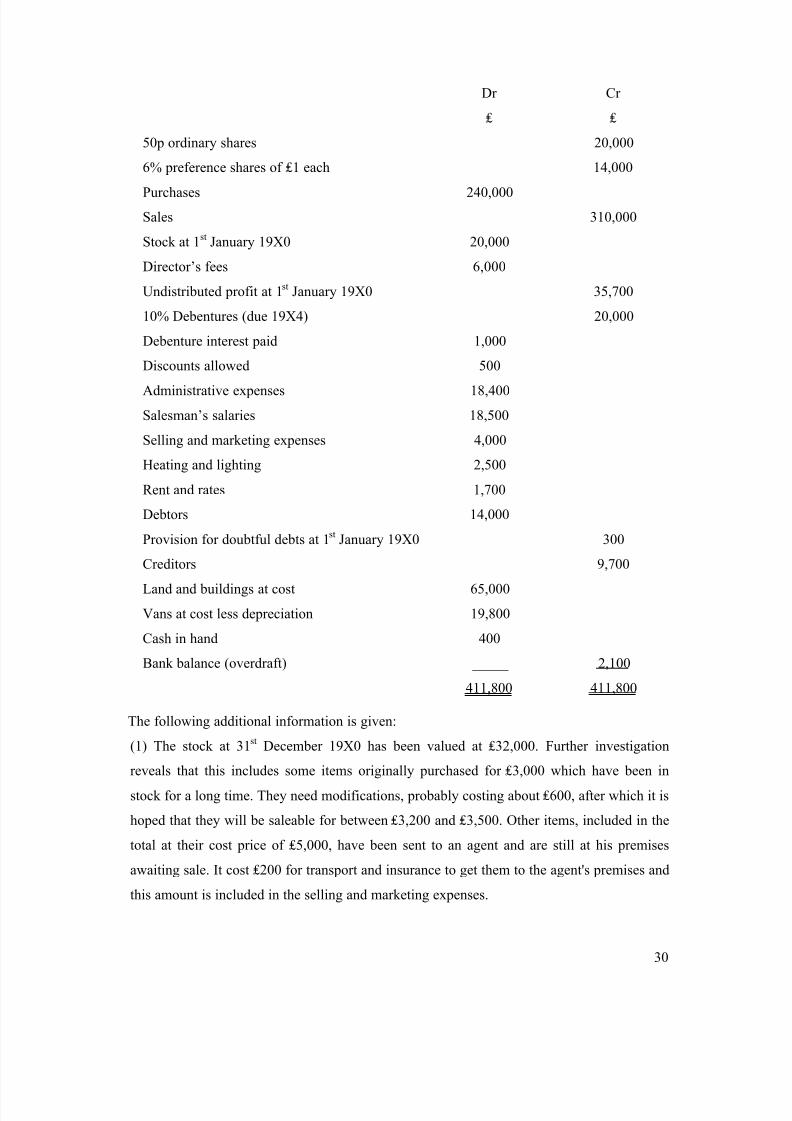

Dr

₤

Cr

₤

50p ordinary shares 20,000

6% preference shares of ₤1 each 14,000

Purchases 240,000

Sales 310,000

Stock at 1st January 19X0 20,000

Director‟s fees 6,000

Undistributed profit at 1st January 19X0 35,700

10% Debentures (due 19X4) 20,000

Debenture interest paid 1,000

Discounts allowed 500

Administrative expenses 18,400

Salesman‟s salaries 18,500

Selling and marketing expenses 4,000

Heating and lighting 2,500

Rent and rates 1,700

Debtors 14,000

Provision for doubtful debts at 1st January 19X0 300

Creditors 9,700

Land and buildings at cost 65,000

Vans at cost less depreciation 19,800

Cash in hand 400

Bank balance (overdraft) _____ 2,100

411,800 411,800

The following additional information is given:

(1) The stock at 31st December 19X0 has been valued at ₤32,000. Further investigation

reveals that this includes some items originally purchased for ₤3,000 which have been in

stock for a long time. They need modifications, probably costing about ₤600, after which it is

hoped that they will be saleable for between ₤3,200 and ₤3,500. Other items, included in the

total at their cost price of ₤5,000, have been sent to an agent and are still at his premises

awaiting sale. It cost ₤200 for transport and insurance to get them to the agent's premises and

this amount is included in the selling and marketing expenses.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 31/103

31

(2) The balance on the vans account (₤19,800) is made up as follows:

Vans at cost (as at 1st January 19X0) ₤30,000

Less: Provision for depreciation to 1st January 19X0 ₤13,800

₤16,200

Addition during the year ₤3,600

₤19,800

Depreciation is provided at 25% per annum on the reducing balance method. The addition

during the year was invoiced as follows:

Recommended retail price ₤3,000

Signwriting on van ₤450

Undersealing ₤62

Petrol ₤16

Number plates ₤12

License which expired 31st December 19X0 ₤60

₤3,600

(3) The directors, having sought at the advice of an independent evaluator, wish to revalue the

land and building at ₤80,000.

(4) The directors wish to make a provision for doubtful debts of 2.5% of the balances of

debtors at 31st December 19X0.

(5) Rent and rates prepaid at 31st December 19X0 amounted to ₤400, and salesmen's salaries

owing at that date were ₤443.

(6) The directors have proposed an ordinary dividend of 5p per share, and the full preference

dividend.

(7) Ignore taxes.

(8) Debenture interest is paid semi-annually.

Required:

(a) Explain very carefully the reasons for the adjustments you have made in respect of items

1, 2 and 3 above. Show your workings

(b) Prepare P&L account for Cirrus Company Ltd the year ended 31st December 19X0, and

the Balance sheet as at that date.

(b) Explain your treatment of debenture interest and proposed dividends.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 32/103

32

Problem 43

A recent article mentioned that there is currently “a bewildering choice” of accounting

treatments for goodwill and other intangible assets some of which are inconsistent with the

way tangible assets are reported. The balance sheet summary of a well-known successful

multinational group of companies is given below to illustrate how one organization chooses to

report brand names and goodwill that it has purchased:

₤ millions

Fixed assets

Intangible assets 3,840

Tangible assets 1,725

Investments 735 6,300

Net current assets 1,000 7,300

Long-term liabilities (4,197) 3,103

Share capital and reserves

Equity share capital 535

Share premium account 667

Revaluation reserve 94

Goodwill reserve (3,579)

Profit and loss account 5,386 3,103

Intangible assets are brands stated at fair value on acquisition. The negative figure for

goodwill reserve is in respect of purchased goodwill written off.

Required:

(a) Explain the nature of intangible assets and why the method of reporting them seems to be

more problematic than for tangible assets.

(b) For purchased goodwill, consider the method used in the above balance sheet. What are its

good and bad points? Explain one other method that might be used. Which do you personally

prefer and why?

(c) For purchased brand names, consider the method used in the above balance sheet. What

are its good and bad points? Explain one other method that might be used. Which do you

personally prefer and why?

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 33/103

33

Problem 44

Raj Ltd purchased a machine on 1st January 1999 for ₤100,000. Transporting the machine to

its factory cost ₤1,600 and ₤1,000 was spent on installing it. Maintenance of the machine cost

₤750 in 1999 and the expenditure on maintenance increased by ₤200 in each of the following

four years. The machine was expected to last until 31st December 2006 with a scrap (or

residual) value at that date of ₤6,600. The company uses the straight-line method of

depreciation. It provides for a full year‟s depreciation in the year of acquisition and none in

the year of sale.

The machine was sold for ₤34,000 on 30th June 2003.

Required:

Explain briefly what you understand by the term “depreciation” as used by accountants. In

what circumstances would straight-line be the most appropriate method to use for an asset?

Give the following calculations:

(i) the depreciation charge for 1999;

(ii) the profit or loss on sale of the machine in 2003.

Problem 45

According to a survey of investment analysts, more than half of them believe that all

internally generated intangible assets should be capitalized on a company‟s balance sheet.

Discuss the advantages and problems of reporting these assets.

Problem 46

“We live in a society where the real wealth creators are often the intangible assets yet few

companies include these assets in their balance sheets”. Why is this? Explain the issues

involved.

Problem 47

Given that amongst the most significant assets of professional football clubs are its

footballers, it has become more common in recent years for such companies to account for the

cost of players on their balance sheets. Other clubs, however, account for their players as

expenses on their Profit and Loss accounts.

Required:

Express the arguments behind these two alternative treatments, using any principles or conventions you are applying in your explanation and explaining any terms you use.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 34/103

34

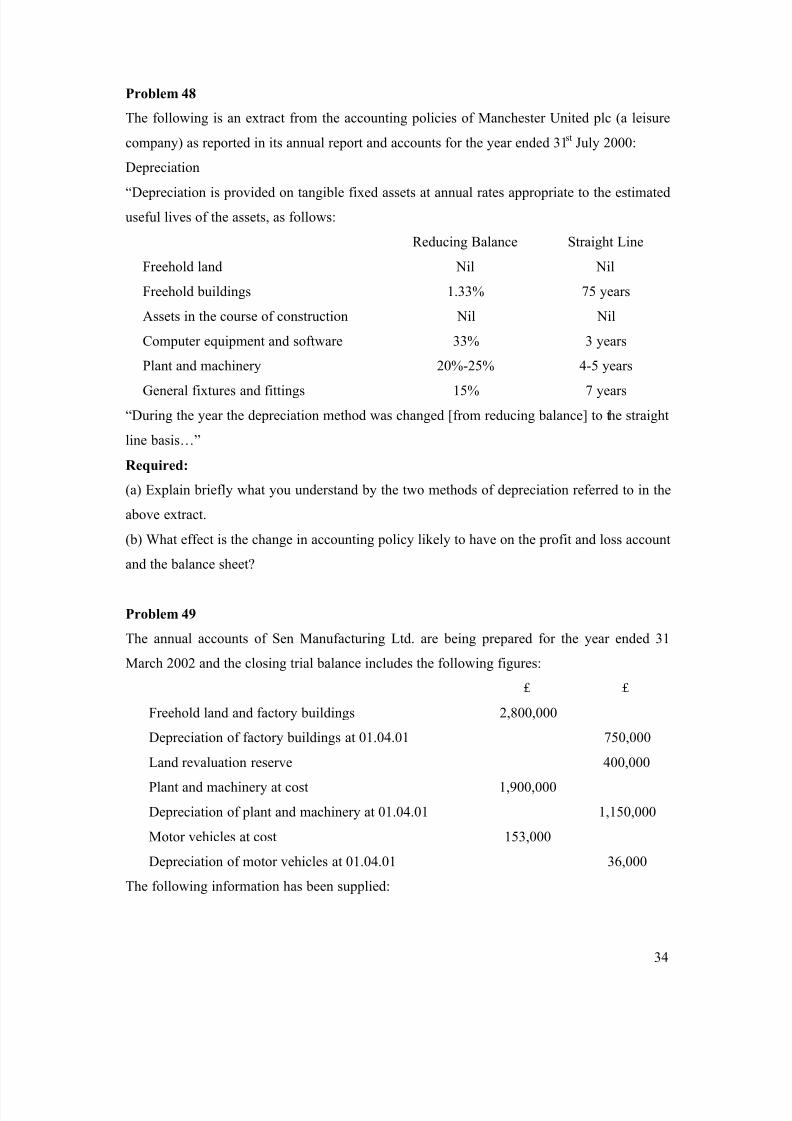

Problem 48

The following is an extract from the accounting policies of Manchester United plc (a leisure

company) as reported in its annual report and accounts for the year ended 31st July 2000:

Depreciation

“Depreciation is provided on tangible fixed assets at annual rates appropriate to the estimated

useful lives of the assets, as follows:

Reducing Balance Straight Line

Freehold land Nil Nil

Freehold buildings 1.33% 75 years

Assets in the course of construction Nil Nil

Computer equipment and software 33% 3 years

Plant and machinery 20%-25% 4-5 years

General fixtures and fittings 15% 7 years

“During the year the depreciation method was changed [from reducing balance] to the straight

line basis…”

Required:

(a) Explain briefly what you understand by the two methods of depreciation referred to in the

above extract.

(b) What effect is the change in accounting policy likely to have on the profit and loss account

and the balance sheet?

Problem 49

The annual accounts of Sen Manufacturing Ltd. are being prepared for the year ended 31

March 2002 and the closing trial balance includes the following figures:

£ £

Freehold land and factory buildings 2,800,000

Depreciation of factory buildings at 01.04.01 750,000

Land revaluation reserve 400,000

Plant and machinery at cost 1,900,000

Depreciation of plant and machinery at 01.04.01 1,150,000

Motor vehicles at cost 153,000

Depreciation of motor vehicles at 01.04.01 36,000

The following information has been supplied:

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 35/103

35

(1) The figure for freehold land and factory buildings comprises land at valuation

(£1,200,000) and buildings at cost (£1,600,000). The land originally cost £800,000 and was

professionally revalued in 1997 and the revaluation reserve created. It was revalued again in

March 2002 and the revised figure of £1,050,000 is to be included in the accounts.

(2) Factory buildings include expenditure in 2001 on constructing a new warehouse

(£220,000), maintenance of buildings (£60,000) and redecoration (£20,000).

(3) Factory buildings owned at 31 March 2002 are to be depreciated for the year at 3% of

cost.

(4) Plant and machinery includes £528,850 for plant constructed by Sen Manufacturing‟s staff

during the year and completed on 30 September 2001. The cost is made up as follows:

Materials £325,000

Labour 122,000

Allocation of company overheads 75,000

Delivery of components to the factory 4,000

Insurance on the machine for the year to 31 May 2002 1,200

Design costs and engineers‟ fees 1,650

(5) Plant and machinery also includes £450,000 being the cost of a machine purchased some

years ago. It had a written down value at 1 April 2001 of £40,000 and was sold on the

following day for £30,000. The proceeds have been debited to cash and credited in error to

sundry income account. No adjustment has been made yet to correct this error.

(6) All plant and machinery owned at 31 March 2002 is to be depreciated for the year at 20%

of cost.

(7) The figure for motor vehicles includes £9,000 paid to Speedy Motors for a new vehicle

costing £17,800 from which was deducted £8,800 for an old vehicle taken in part exchange.

The old vehicle cost £23,000 in April 1998 and three years‟ depreciation, using the decreasing

balance method and an annual rate of 30%, is included in the depreciation figure in the trial

balance.

(8) All motor vehicles owned at 31 March 2002 are to be charged depreciation at the rate of

30% using the decreasing-balance method.

Required:

(a) Prepare a table with eight columns using a separate column for each of the seven balances

shown in the trial balance extract and head the final column “Profit”. For each item numbered

from (1) to (8) above, show on the table which of the seven balances needs correcting, and

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 36/103

36

how (+ or - ), and show the correct balances at 31 March 2002. For each adjustment, show in

the final column by how much the figure of profit for the year will be affected (+ or - ).

(b) Prepare the fixed assets section of Sen Manufacturing Ltd‟s balance sheet as at 31 March

2002 in good style.

(c) Your answer to the following questions put to you by a colleague:

“What is the purpose of having a land revaluation reserve? Why haven‟t the other fixed assets

been revalued? Also, can you explain to me why you asked me to obtain all the detailed

information listed under item (4)?”

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 37/103

37

Accounting in Joint-Stock Companies

Problem 50

GWR Ltd started in business on 1st January 19X6. Its issued share capital was 100,000

ordinary shares of ₤1 each and 50,000 10 per cent preference shares of ₤1 each.Its net profits for the first two years of business were: 19X6 ₤42,005; 19X7 ₤34,831.

Preference dividends were paid for each of these years, whilst ordinary dividends were

proposed as 19X6 12 per cent and 19X7 9 per cent.

Corporation tax, based on the profits of these two years, was: 19X6 ₤13,480; 19X7 ₤11,114.

Transfers to general reserve took place as: 19X6 ₤6,000; 19X7 ₤4,000.

Required:

Draw up profit and loss appropriation accounts for each of the years ended 31 st December

19X6 and 19X7.

Problem 51

Badwa plc. has an authorized capital of 500,000 ordinary shares of ₤0.50 each. At the end of

its financial year, 31st May 19X9, the following balances appeared in the company‟s books:

₤

Issued capital: 400,000 shares fully paid 200,000

Freehold land and buildings at cost 320,000

Stock in trade 17,800

10% debentures 30,000

Trade debtors 6,840

Trade creditors 8,500

Expenses prepaid 760

Share premium 25,000

General reserve 20,000

Expenses outstanding 430

Profit and loss account balance (1st June 19X8) 36,200

Bank overdraft 3,700

Fixtures, fittings and equipment

at cost 54,000

provision for depreciation 17,500

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 38/103

38

The com pany‟s trading and profit and loss accounts had been prepared and revealed a net

profit of ₤58,070. However, this figure and certain balances shown above needed adjustment

in view of the following details which had not been recorded in the company‟s books.

(1) It appeared that a trade debtor who owed ₤300 would not be able to pay. It was decided to

write his account off as a bad debt.

(2) An examination of the company‟s stock on 31st May 19X9 revealed that some items

shown in the accounts at a cost of ₤1,800 had deteriorated and had a resale value of only

₤1,100.

(3) At the end of the financial year some equipment which had cost ₤3,600 and which had a

net book value of ₤800 had been sold for ₤1,300. A cheque for this amount had been received

on 31st May 19X9.

Required:

(a) A statement which shows the changes which should be made to the net profit of ₤58,070

in view of these unrecorded details.

(b) The directors proposed to pay a final dividend of 10% and to transfer ₤50,000 to general

reserve on 31st May 19X9. Prepare the profit and loss appropriation account for the year

ended 31st May 19x9 and two extracts from the company‟s balance sheet as at 31st May 19X9,

showing in detail:

(i) the current assets, current liabilities and working capital

(ii) the items which make up the shareholders‟ funds.

(c) The directors are concerned about the company‟s liquidity position. Propose three

transactions which will increase the company‟s working capital. State which balance sheet

items will change as a result of each transaction and whether the item will increase or

decrease in value.

Problem 52

LMS Ltd has an authorized capital of ₤200,000, consisting of 160,000 ordinary shares of ₤1

each and 40,000 8 per cent preference shares of ₤1 each. Of these 120,000 ordinary shares had

been issued and all the preference shares when the business first started trading.

The business has a financial year end of 31st December. The first three years of business

resulted in net profit as follows: 19X7 ₤27,929; 19X8 ₤32,440; 19X9 ₤36,891.

Dividends were paid each year on the preference shares. Dividends on the ordinary shares

were proposed as follows: 19X7 8 per cent; 19X8 10 per cent; 19X9 11 per cent.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 39/103

39

Corporation tax, based on the profits of each year, was: 19X7 ₤8,331; 19X8 ₤10,446; 19X9

₤12,001.

Transfers to reserves were made as: General reserve 19X7 ₤3,000; 19X8 ₤4,000, and Foreign

exchange reserve 19X9 ₤2,000.

Required:

Show the profit and loss appropriation accounts for each of the years 19X7, 19X8 and 19X9.

Problem 53

The stockholders‟ equity section of the balance sheet of P Corporation as December 31, 2004,

appears as follows:

Stockholders‟ Equity amounts in thousand, except share amounts

7% Preferred stock, $100 par; 100,000 shares authorized; 40,000

shares issued

$4,000

Common stock, $1 par; 1,000,000 shares authorized; 600,000

shares issued, of which 50,000 are held in treasury

$600

Additional paid in capital:

From issuance of preferred stock $480

From issuance of common stock $1,410

Retained earnings $4,500

…

Total stockholders‟ equity $10,715

Required:

Answer the following questions related to P Corporation.

(a) What was the average issue price of the preferred stock as of December 31, 2004?

(b) How many shares of common stock are outstanding?

(c) What journal entry was made when the common stock was issued?

(d) What is the amount of the total dividend requirement on preferred stock annually?

(e) Assuming that there are no dividends in arrears, if the company declared a total cash

dividend of $580,000, what would be the dividend per share for the preferred and common

stock?

(f) Assume the company‟s common stock is selling for $80 per share. What journal entry

would be made if the company issues a 10% common stock dividend?

(g) Compute basic earnings per share if the company‟s net income was $1,560,000 during2004. Assume no new shares were issued during the year.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 40/103

40

(h) Refer to the original data. Assume the company declares a 3-for-2 stock split. How many

shares of common stock would be outstanding after the split?

Problem 54

The balance sheet of C Ltd is as follows:

Assets ₤

Sundry net assets ₤1,200,000

Share capital

₤1 ordinary shares fully paid 400,000

Reserves

General reserve 500,000

Profit and loss account (unappropriated profit) 300,000

₤1,200,000

The directors decide to make a 1 for 5 bonus issue. This will be followed by 1 for 3 rights

issue. Rights shares will be offered at a price of ₤1.60 per share.

Required:

Show the revised balance sheet of C Ltd after both share issues have taken place.

Problem 55

Meta Ltd has the following share capital and reserves as at 20th August 19X5:

₤

1,500,000 ordinary shares of 25p, each fully paid 375,000

Share premium 225,000

Retained profit 200,000

800,000

The directors resolve to use the reserves to issue fully-paid bonus shares at par in the ratio of

two shares for every three currently held.

Required:

(a) Show the revised balance sheet (“capital and reserves” section only) after the above

transactions have been carried out.

(b) Assuming that the market value of each share has tended to stay around 50p ex div (i.e.

excluding any dividend expected in the very near future) and the total annual dividend has

been ₤75,000, what would you expect the market price of each share to be after the bonusissue?

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 41/103

41

Problem 56

The S Ltd commenced operations on 1st January 19X6. For the first four years the following

results were achieved:

Year ended 31

December

Trading profit (loss) Profit (loss) on sale

of fixed asset

Profit on revaluation

on land use

₤ ₤ ₤

19X6 (100,000)

19X7 80,000

19X8 90,000 30,000

19X9 60,000 (10,000) 40,000

Required:

State, for each year, the maximum dividend company could pay (assuming a maximum

dividend is paid whenever possible)

Problem 57

Refer to Problem 56 above. Assume that S Ltd issued 300,000 ₤1 Preference Shares with a

10% fixed rate on dividend at the commencement of business.

Required:

State, for each year, maximum dividend the company could pay its ordinary shareholders if:

(i) the preference shares were non-cumulative, and

(ii) the preference shares were cumulative.

Problem 58

A major international company recently reported the worst results in its century-long history

with a 90% fall in net income and the chairman was reported to be worried about keeping his

job. However, the total dividend proposed for the year was 4% up on the previous year‟s.

Required:

Give possible reasons for the dividend increase. How would you check whether the increase

is legal?

Problem 59

Wonda plc. has an issued share capital of two million ₤1 shares. The directors are considering

whether the company should buy back and cancel 10% of its issued share capital at thecurrent market price of 220 pence per share.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 42/103

42

(i) Why would the directors of a company like Wonda plc. wish it to buy back and cancel

some of its shares?

(ii) How do you consider the buyback should be reflected in the balance sheet of Wonda plc.?

(iii) Would you expect the share price of Wonda plc. to remain at 220 pence after the share

buyback? Explain your answer.

Problem 60

“This is certainly the record dividend payment of the year: O‟Mara plc is paying 75 pence for

each ₤1 share! It represents 80% of the company‟s earnings for the year. Even the big banks

are not that generous!”

Required:

Comment on the above quotation which has been adapted from an article in a national

newspaper and explain whether you consider that the company has necessarily been generous

to its shareholders. Specify what further information you would need for your answer, if any,

and what use you would make of it.

Problem 61

Your aunt has held 1,000 ordinary shares in a quoted company for several years. She has very

little understanding of financial matters. She has asked you to write her a short note to explain

the following:

(1) why the company has only paid a dividend of approximately 30% of the profit after tax;

(2) why the company is making a 1 for 1 scrip (or bonus) issue and what effect this is likely to

have on the market value of each share.

Required:

Explain to your aunt:

(a) the factors which determine a company‟s dividend;

(b) the purpose, the effect on the balance sheet and the effect on the market value of each

share of a 1 for 1 scrip issue.

Problem 62

In a recent article on a leading engineering company, a financial journalist drew attention to

the fact that, according to its recent balance sheet, the net asset value per share was £4.15 yet

the company‟s ordinary shares had been quoted on the stock exchange at around £7.80 for the past few months.

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 43/103

43

Required:

Give reasons that might explain why the two figures are different.

Problem 63

The country of Yugalia has experienced a financial crisis over the past year and, for the

typical company, share price has been below net asset value per share yet the company has

reported a profit.

Required:

Do these apparent anomalies necessarily imply that there is something wrong with financial

reporting in Yugalia? Explain the issues involved.

Problem 64

Wizz.com, an online consumer information provider, has seen its share price treble in value

over the past eight months. It has been in business for five years and has never earned a profit.

Last year ‟s pre-tax loss was £32 million on a turnover of £23 million.

Required:

How can the shares of a company with such a poor profitability record and a negative

price/earnings ratio be in such demand?

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 44/103

44

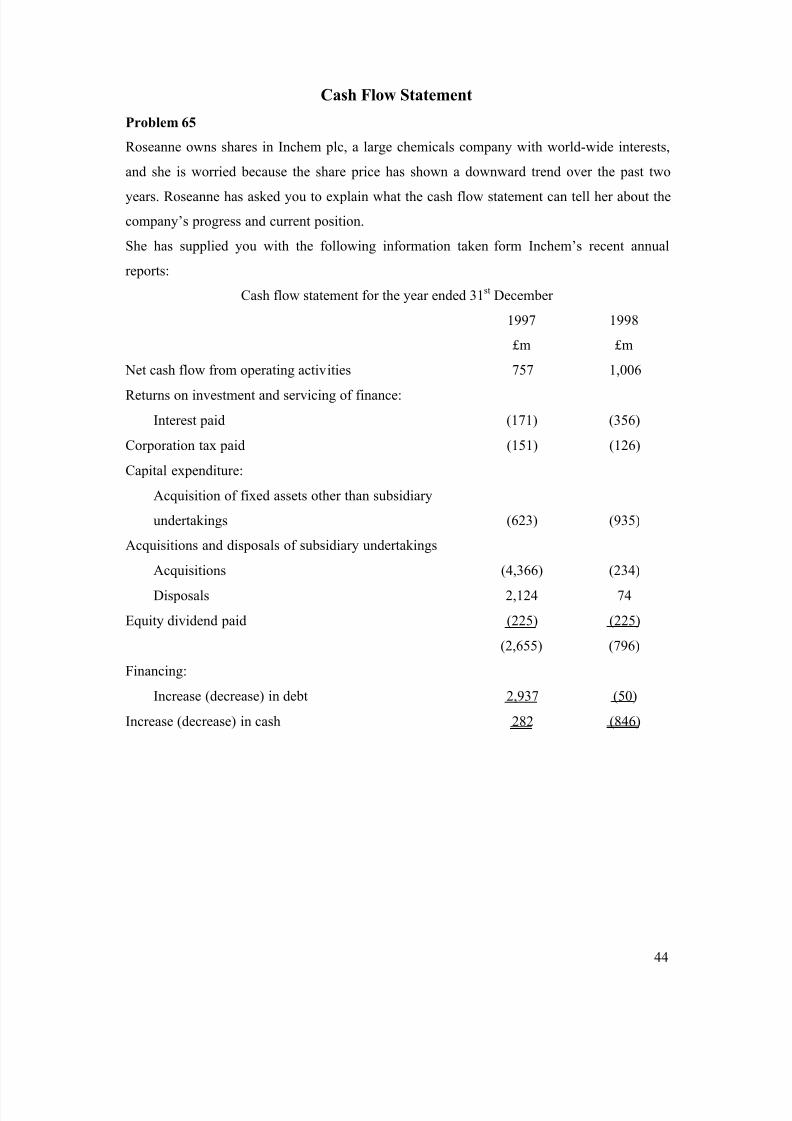

Cash Flow Statement

Problem 65

Roseanne owns shares in Inchem plc, a large chemicals company with world-wide interests,

and she is worried because the share price has shown a downward trend over the past twoyears. Roseanne has asked you to explain what the cash flow statement can tell her about the

company‟s progress and current position.

She has supplied you with the following information taken form Inchem‟s recent annual

reports:

Cash flow statement for the year ended 31 st December

1997

£m

1998

£m

Net cash flow from operating activities 757 1,006

Returns on investment and servicing of finance:

Interest paid (171) (356)

Corporation tax paid (151) (126)

Capital expenditure:

Acquisition of fixed assets other than subsidiary

undertakings (623) (935)

Acquisitions and disposals of subsidiary undertakings

Acquisitions (4,366) (234)

Disposals 2,124 74

Equity dividend paid (225) (225)

(2,655) (796)

Financing:

Increase (decrease) in debt 2,937 (50)

Increase (decrease) in cash 282 (846)

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 45/103

45

Note:

Net cash inflow from operating activities:

Operating profit 378 405

Depreciation 434 402

Stocks decrease 18 62

Debtors increase (31) (86)

Creditors (decrease) increase (42) 223

Net cash inflow from operating activities 757 1,006

Required:

(a) An analysis of the above figures to assist Roseanne in understanding Inchem plc‟s

financial performance in 1998 and its financial position at the year end. Indicate what

additional information you require to help you with your analysis and what use you would

make of it.

(b) Explain to Roseanne what use published financial reports are in explaining share price

movements and indicate what other information might be useful.

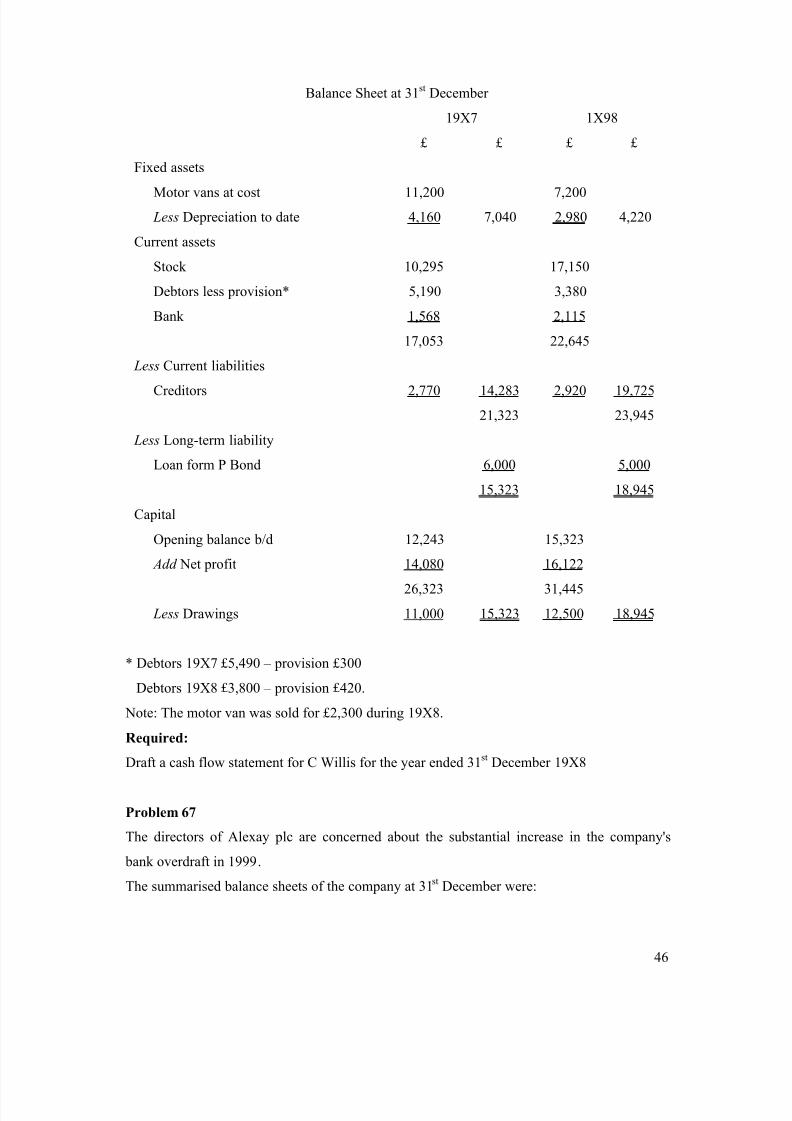

Problem 66

C Willis

Profit and Loss Account for the year ended 31st December 19X8

£ £

Gross profit 29,328

Add Discounts received 298

Add Profit on sale of motor van 570 868

30,196

Less Expenses

Motor expenses 1,590

Wages 8,790

General expenses 2,144

Bad debts 340

Increase in bad debt provision 120

Depreciation: Motor van 1,090 14,074

16,122

7/29/2019 Accounting Problem Book 2011

http://slidepdf.com/reader/full/accounting-problem-book-2011 46/103

46

Balance Sheet at 31st December

19X7 1X98

£ £ £ £

Fixed assets

Motor vans at cost 11,200 7,200

Less Depreciation to date 4,160 7,040 2,980 4,220

Current assets

Stock 10,295 17,150

Debtors less provision* 5,190 3,380

Bank 1,568 2,115

17,053 22,645

Less Current liabilities

Creditors 2,770 14,283 2,920 19,725

21,323 23,945

Less Long-term liability

Loan form P Bond 6,000 5,000

15,323 18,945

Capital

Opening balance b/d 12,243 15,323

Add Net profit 14,080 16,122

26,323 31,445

Less Drawings 11,000 15,323 12,500 18,945

* Debtors 19X7 £5,490 – provision £300

Debtors 19X8 £3,800 – provision £420.

Note: The motor van was sold for £2,300 during 19X8.

Required:

Draft a cash flow statement for C Willis for the year ended 31 st December 19X8

Problem 67

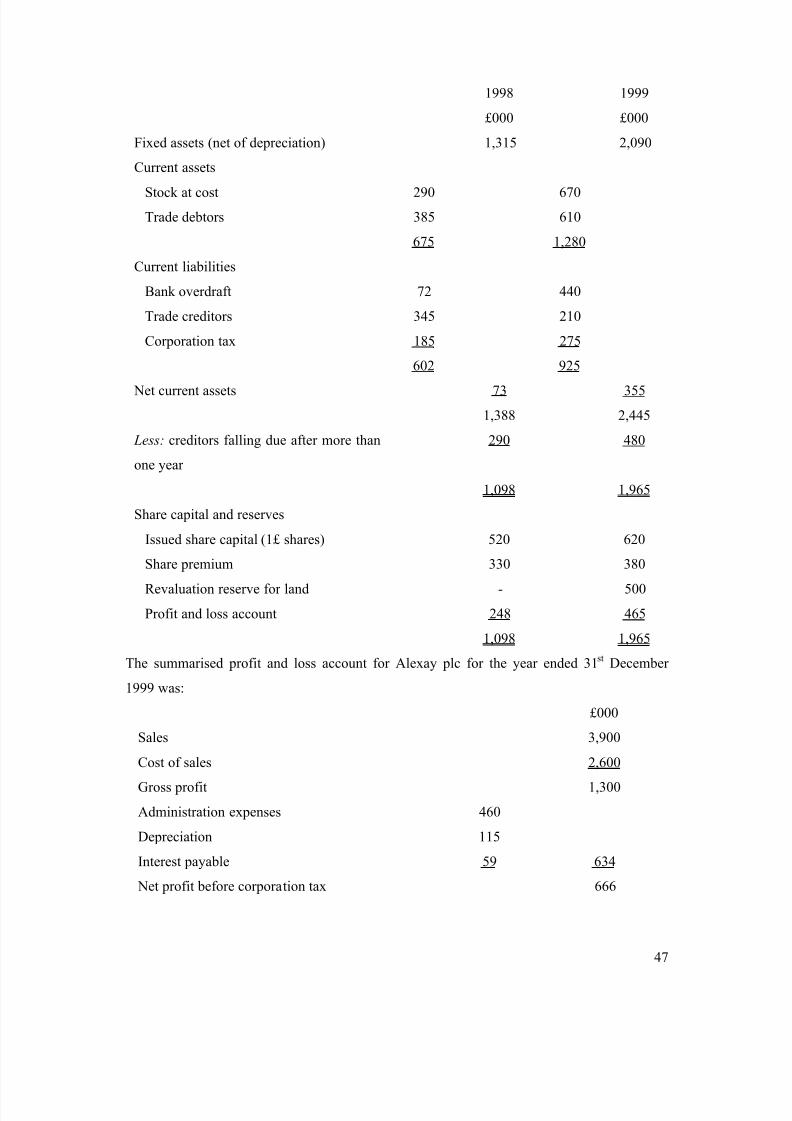

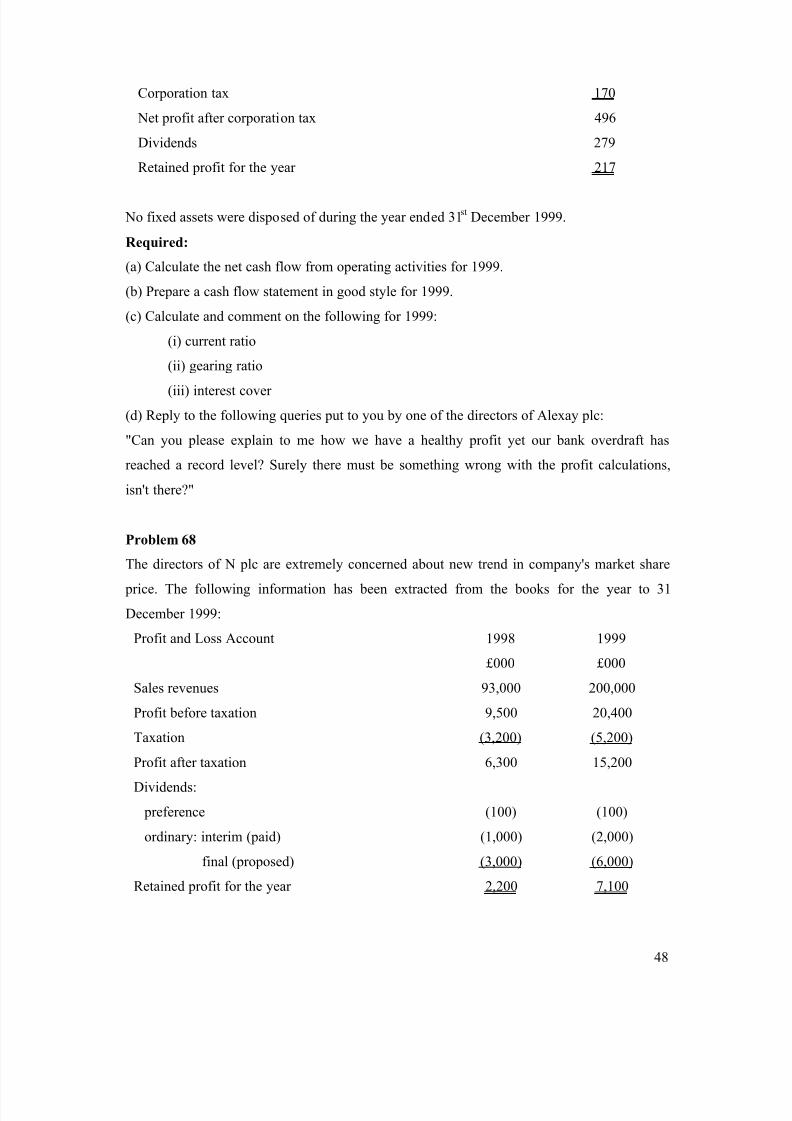

The directors of Alexay plc are concerned about the substantial increase in the company's

bank overdraft in 1999.