Accounting Maintenance Report 111113

81

5th Year Accounting Maintenance Report Prepared for the AACSB Peer Review Team Visit

Transcript of Accounting Maintenance Report 111113

5th

Year

Acc

ount

ing

Mai

nten

ance

Rep

ort

Prep

ared

for t

he A

ACSB

Pee

r Rev

iew T

eam

Visi

t

5th Y

ear

Acc

ount

ing

Mai

nten

ance

Rep

ort

Dr. W. Rhea IngramDean

Dr. Judith KamnikarDepartment Head

School of BusinessAuburn University at Montgomery

P.O. Box 244023Montgomery, AL 36124

334-244-3478

Prep

ared

for t

he A

ACSB

Pee

r Rev

iew T

eam

Visi

t

i | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

EXECUTIVE SUMMARY

The Department of Accounting received AACSB initial accounting accreditation on April 29, 2012. Uniquely, the Department of Accounting, School of Business, Auburn University at Montgomery (AUM), was the first school in the state of Alabama to earn AACSB accounting accreditation for a program offering only an undergraduate concentration. The department is dedicated to maintaining its AACSB International accounting accreditation as evidence of its commitment to quality education and continuous improvement. Background Auburn University at Montgomery (AUM) was established as a metropolitan campus of Auburn University in the capitol city of Montgomery, Alabama by an act of the Alabama Legislature in 1967 and opened its doors to students in 1969. Since this date, the accounting program has been an integral part of the University’s curricular offerings as a unit within the School of Business. The School of Business offers a Bachelor of Science in Business Administration degree (BSBA) with specializations in 8 areas, including Accounting, plus multiple graduate offerings. The Alabama Commission on Higher Education has approved all business degree programs. The School received its initial AACSB accreditation in 1988, with reaffirmations in 1994, 2004, 2009 and is currently applying for reaffirmation in 2013. At the time of application for accounting accreditation, the administrative unit was the Department of Accounting and Finance. Upon receiving initial accreditation, the Dean with support of faculty and university administration reorganized the department structure. The finance program was moved to the Department of Economics (currently the Department of Economics and Finance) where it had originally been established. The Department of Accounting became a unit within the School of Business as of January 1, 2012. The Department of Accounting would have had its first five-‐year maintenance review in 2017, yet, the accounting faculty elected to apply for the fifth year maintenance of accreditation during the 2013 year to articulate with the accreditation cycle of the School of Business. The department has a long tradition of delivering a superior education to its students. The mission of the department, therefore, includes a commitment to providing high quality accounting education to its students, as well as to making intellectual contributions that can be applied to the business environment and classroom instruction. The department strives to produce a mix of scholarly works focused on contributions to practice, learning and pedagogical research, as well as some discipline-‐based research. In addition, the faculty provides strong support of student organizations that facilitate students' introduction to the accounting profession. The department is committed to maintaining strong ties with the business community, especially the accounting profession, and to providing responsible service to its various stakeholders. As a result of the department’s quality education focus, it enjoys an excellent regional reputation. The accounting professional community not only supports the program with donations of time and funds but also through the employment of its graduates for internships, part-‐time and full-‐time positions. Graduates of the AUM accounting program are employed by international, regional and local CPA firms, government agencies, industry, and nonprofit organizations. Further, its faculty members are committed to teaching excellence and have won state-‐wide teaching-‐related awards. The faculty members manage to do this while meeting the School’s research requirements and participating in service to various stakeholders. The department’s reputation assists in attracting

ii | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

students who are academically strong and compete successfully for employment, internships and success on the CPA examination. The students participate in the department’s two student organizations’ activities, ones that are geared to their professional development. Alumni of the department are valuable assets to the continuous improvement process. Many hold partnership/principle status in public practice firms, CFO positions in government and business, as well as senior management positions in industry and nonprofit organizations. These alumni have provided significant support both financially and as members of our Accounting Advisory Board. This Board provides valuable input to the department’s strategic plan, curriculum development, student development, fund-‐raising, and promotion. The alumni contacts also result in invitations to the faculty to participate in seminars and continuing professional education sessions that are essential to the department’s mission and accreditation. Degree Program The Department of Accounting offers a Bachelor of Science in Business Administration degree (BSBA) with a specialization in accounting. The program is delivered primarily on campus and by 7 full-‐time faculty members (all tenured or tenure-‐track) and one or two part-‐time adjuncts, as needed. The Bachelor’s degree requires 24 hours of accounting in addition to the 6 hours of accounting principles taken as part of the requirements of the business core for all business majors. During the five year review period, academic years 2008-‐2009 through 2012-‐2013, there were 177 BSBAs with an accounting specialization awarded, representing 18.8% of all BSBA degrees awarded during that time. The average fall enrollment in undergraduate accounting courses for the review period was 214, which represents 18% of all undergraduate School of Business enrollments for that census period. Strategic Management Planning Process The department’s strategic planning process includes the faculty and department head drafting a plan which incorporates the University’s and the school’s strategic plans. Then, feedback is received from the dean, the school’s leadership team, the Accounting Advisory Board members and officers of the two student organizations. Their input is taken into consideration with appropriate modifications made by the accounting faculty for the final strategic plan. Financial Strategies The accounting department head has administrative and budgetary responsibility for all matters concerning the department. The head manages the various resources (money, other assets and people) that are allocated to the department by the University and the Dean. The funding is provided by the state, student tuition, accounting firms, alumni and friends of the department. Annual allocations, distributed by the University through the Dean’s office, are primarily to pay for the department’s operating expenses and travel-‐related expenditures. The department also has generated scholarship funds provided by friends and alumni, subject to rules of the University’s foundation office, which provide scholarship awards to juniors and seniors. In addition, the department has access to funds generated from two CPE programs jointly sponsored with the Alabama Society of CPAs (ASCPA) and the Association of Government Accountants – Montgomery Chapter (AGA). These funds have been used to promote department academic programs and faculty development, research, and travel.

iii | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Assurance of Learning The Department of Accounting had three learning goals during the census period for initial accounting accreditation. The AACSB peer review team made the following recommendation for continuous improvement: “While AUMs assurance of learning program is adequate, the department should

continue to develop the program by considering whether more learning goals and learning objectives would be helpful in guiding curricular development…..the department continue to evaluate whether other learning goals could be useful, whether those learning goals could be supported by additional or revised learning objectives, and whether the analysis of measures could be improved….”

The department has revisited its assurance of learning program with the result of (1) modifying the learning goals and objectives; (2) improving assessment measurements; and (3) restructuring the entire process. Participants Many of the policies and procedures related to the department’s faculty management are provided by the University’s Faculty Handbook and School of Business Policies. The standards for Academic Qualification (AQ) and Professional Qualification (PQ) for accreditation purposes are part of the School Policies. During the reporting year (fall 2012 – spring 2013), the full-‐time accounting faculty was 100% participating faculty with the department head being PQ and the other faculty all AQ. In the period following initial accounting accreditation, 7 adjuncts (6 PQ and 1 AQ) taught a total of 15 courses over six academic semesters/terms which resulted in an average 85.71% qualification ratio. For Fall 2012, the sufficiency ratio for the Department of Accounting is 93.9%.

| Page AACSB Business Maintenance Report iv

TABLE OF CONTENTS SITUATIONAL ANALYSIS 1 University Background and Governance 1 Environmental and Internal Analysis 1 PROGRESS UPDATE ON CONCERNS FROM PREVIOUS REVIEW 7 STRATEGIC MANAGEMENT 9 Department of Accounting Mission 9 Department Vision 10 Departmental Goals 10 Mission Focused 10 Strategic Planning Process 12 Selected Accomplishment (2008-‐2013) 13 Financial Strategies 14 Next Five Years 16 PARTICIPANTS 18 Students 18 Faculty 22 ASSURANCE OF LEARNING 26 Curricula Developments 27 Learning Goals 27 Assessment Results 30 Learning Goals and Curricula Impact 35

| Page AACSB Business Maintenance Report v

APPENDICES

Appendix A: Government Financial Management Program 37 Appendix B: Accounting Advisory Board

38

Appendix C: Undergraduate Enrollment Data Appendix D: Accounting Department Strategic Plan, 2007-‐2012

39

42 Appendix E: Faculty Participation 51 Appendix F: Financial Data 54 Appendix G: Internship Form 55 Appendix H: Student Curriculum Sheet 57 Appendix I: Student Advising Guidelines for Accounting Majors 58 Appendix J: EBI Survey Results – Advising 2011-‐2012 61 Appendix K: Delta Epsilon Kappa: Accounting Honor Society 63

Appendix L: Assurance of Learning 64 Appendix M: Exhibit AOL.J 71 Appendix N: Miscellaneous 73

| Page AACSB Business Maintenance Report vi

LIST OF FIGURES & TABLES

Tables: AUM Accounting Graduates – Current Employment 4 Percentage of Students Enrolled Full-‐Time and Part-‐Time 10 Percentage of Enrollments by Course Level and by Day and Night Offerings 11 Department of Accounting Instructional Budgets 14 Accounting Program Non-‐University Generated and Unrestricted Funds 15 Accounting Scholarship Donors 16 AUM and Accounting Program Enrollment and Graduates 18 Accounting Completers 18 ACT Scores of Graduates Receiving Undergraduate Degrees 19 Firms/Businesses Providing Internships 20 School of Business EBI Survey

23

Five-‐Year Summary of Developmental Activity Supporting PQ 24 Accounting Certifications Held by the Accounting Faculty 25 Selected Service/Leadership Activities of the AUM Accounting Faculty 25 Department of Accounting Learning Goals 29 Goal 1 Assurance of Learning 31 Goal 2 Assurance of Learning 32 Goal 3 Assurance of Learning 33 Goal 4 Assurance of Learning 34

1 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

SITUATIONAL ANALYSIS

The Accounting Program in the School of Business, Auburn University at Montgomery, was granted AACSB accounting accreditation April 29, 2012. The accounting faculty unanimously elected to submit a fifth-‐year Accounting Accreditation Maintenance Review in 2013, articulating with the School of Business accreditation reporting cycle. This Accounting Accreditation Maintenance Report provides information for a five-‐year period (i.e., 2008-‐2009 through 2012-‐2013); however, the information presented in this report focuses on the two years following the initial accreditation report. University Background and Governance Established in 1967 as the metropolitan campus of Auburn University in Montgomery Alabama by an act of the Alabama Legislature in 1967, AUM was accredited by the Southern Association of Colleges and Schools as an operationally separate institution in 1973 and is scheduled for its next SACS review in 2014. The School of Business degree programs have been approved by the Alabama Commission on Higher Education and accredited by AACSB since 1988. The School of Business is scheduled for reaffirmation in 2014. Additional information about the University Background and Governance is available in the School of Business Fifth Year Maintenance Report, pages 1-‐2. The accounting program is a vital part of the School of Business and is administratively housed in the Department of Accounting. Resources from the university and various external sources provide the department with continued viability. The process for AACSB accounting accreditation started with the Application for Accounting Eligibility/Pre-‐candidacy for AUM on February 5, 2003. On May 23, 2006 the Accounting Accreditation Plan was submitted to AACSB. On October 2-‐4, 2011 an AACSB team visited campus for an evaluation. The team made a positive recommendation to the Accounting Accreditation Committee and initial accounting accreditation was granted April 29, 2012. Environmental and Internal Analysis A key success factor for the Department of Accounting is its excellent relationship with alumni and accounting professionals in private practice, corporate, and governmental accounting. The accounting faculty is committed to this relationship because of the professionalism it brings to the accounting curriculum and the opportunities for the accounting students. With feedback from these stakeholders, the Accounting Accreditation Maintenance Report provides information to highlight the strengths, challenges, and opportunities that drive its strategic planning process.

Strengths

High Standards A major strength is the AACSB International Accounting Accreditation. AUM was the first public school in Alabama to receive accounting accreditation of an undergraduate only program. This distinction allows AUM to provide a program based on the high quality standards set by the AACSB not only in accounting but as part of the only AACSB-‐accredited business school in the highly competitive academic market in Montgomery. The accounting program meets students’ needs in a variety of ways to obtain the necessary education requirements to compete for entry-‐level accounting positions. Although the education

2 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

requirements to take the Uniform CPA Examination as an Alabama candidate are higher than the minimum requirements for the BSBA Accounting Specialization, these additional requirements can be satisfied through the AUM’s MBA program or by completing additional undergraduate courses. Quality Curriculum Driven by the department’s mission statement, the accounting curriculum “provides high quality accounting education to our students with opportunities for them to develop the skills necessary to participate effectively in a competitive global environment”. It is a comprehensive and rigorous curriculum that has aided in the success of our graduates. The undergraduate curriculum is comprehensive in nature consisting of 24 semester hours of accounting including two accounting electives. The courses are offered on a systematic basis so that the students may attend the program during the day, in the evening, or both. The students have access to a full array of classroom technology and related software programs to aid in the learning process. The department has developed an on-‐line governmental financial management (GFM) program and offers the GFM courses online or hybrid format (See Appendix A: Governmental Financial Management Program). The department’s faculty has made strides in upgrading its course learning goals and objectives allowing assessment of student outcomes. The upgrade has taken place for the lower division accounting courses included in the business undergraduate core as well as the upper division accounting core courses and electives. The upper division accounting courses address the department learning goals and objectives including technical knowledge, use of technology, and professional ethics and internal control (See Assurance of Learning section). Productive and Engaged Faculty All full-‐time accounting faculty members are academically qualified using standards developed by the School of Business. Each member of the accounting faculty develops and publishes quality peer-‐reviewed research in journals that can be used to enhance classroom performance. In addition, the Department of Accounting has:

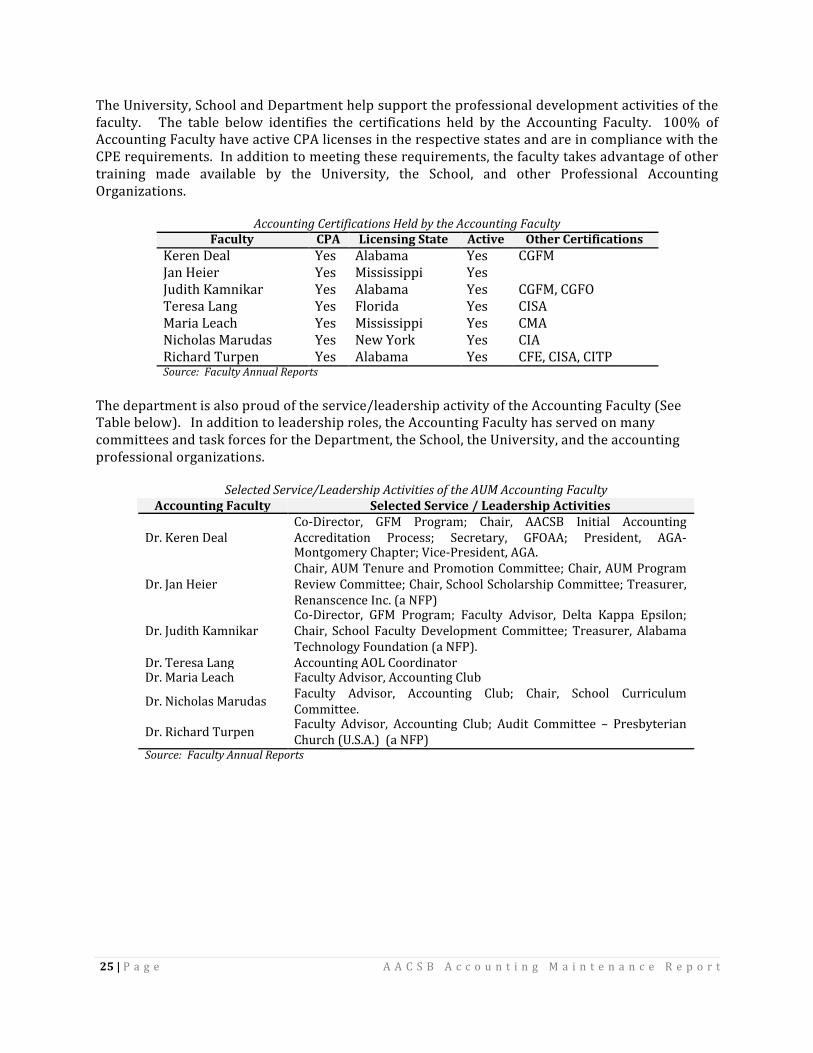

• faculty members that are nationally known for their research and business interactions, especially in the area of governmental accounting;

• all 7 faculty members are licensed CPAs with some having additional certifications, • a faculty with professional and business interaction on a regular basis evidenced by

attendance at professional meetings, conferences, or consultant activities; • a stable core of faculty with all but the newest member tenured; • a strong reputation that enhances faculty recruitment to replace those who leave, which is

due primarily to retirement; and, • professionally qualified adjunct instructors with regard to education, work experience and

certifications. Even though AUM has a research requirement like other similar schools, faculty members see their teaching responsibilities and serving the students as their first priority.

3 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Successful and Generous Alumni Students within the department are an additional strength. They represent a diverse population and enrich the classroom experience for both student and faculty. The students have attained the high academic standards to complete the accounting program and are prepared to enter the profession. According to input from employers, AUM accounting graduates are among the best in their firms and companies. In addition, students graduating from the accounting program have been successful in completing graduate accounting programs at both the masters and doctoral levels. AUM accounting graduates have also graduated with advanced degrees from many universities including but not limited to Auburn University at Montgomery, Auburn University, the University of Alabama, Georgia State University, Troy State University, Case Western Reserve University, the University of Denver, and Yale University. Students graduating from the accounting program have been successful in navigating a career in accounting, government, and business and have moved into top managerial positions, such as partners at CPA firms or controllerships in business and government. The table on page 4 lists selected AUM accounting graduates’ current positions and firm/organization. Strong Partnerships The Department of Accounting has an excellent regional reputation. The alumni identified on page 4, plus more, are generous, not only with their donations of time and funds, but also with their praise for the program. Employers, including international, regional, and local CPA firms, government agencies, and corporations, consistently return to campus to recruit AUM accounting majors for internships, part-‐time, and full-‐time employment. These alumnae and their employers have supported the accounting program with student scholarships (22 scholarships over the past five years), student internships (21 over the past five years), and interaction with students at several academic and/or professional sponsored programs. The department’s faculty members have stayed connected to the practitioners, as well as to other professors, by delivering continuing professional education (Drs. Deal, Kamnikar, Marudas, and Turpen) and participating in various organizations such as the Alabama Society for CPAs, the Government Finance Officers Association of Alabama, the Association of Government Accountants – Montgomery Chapter, the Institute for Management Accountants, and the American Accounting Association and their committees’ work. For example, Dr. Keren Deal participates at the national level with the Association of Government Accountants in the following roles: Vice Chair of the editorial board for the Journal of Government Financial Management, a national AGA publication; member of the Professional Ethics Board; Regional Vice-‐President Elect of the Gulf Region. Dr. Kamnikar has served on national committees of the AICPA, GFOA, and AGA. Dr. Kamnikar has served as President of the state GFOAA and Secretary of the Board for ASCPA; Drs. Deal and Kamnikar have served as President of the AGA – Montgomery Chapters; and Dr. Heier has served as President of the IMA – Montgomery Chapter. Dr. Leach has worked with the IMA to direct IMA scholarships to the AUM students. All of those contacts have promoted the department throughout the region and nationally.

4 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Another advantage of the department is its Accounting Advisory Board (See Appendix B: Accounting Advisory Board). The department head in conjunction with the dean’s strategic planning process expanded and formalized the Accounting Advisory Board to include 24 voting members and 2 ex-‐officio members. The 24 voting member board represents public practice firms (46%), government agencies, state and federal, (33%), and business organizations (21%). The School of Business Dean and the Accounting Department Head are ex-‐officio members of the Accounting Advisory Board. AUM accounting alumni comprise 79% of the voting members of the Accounting Advisory Board. The advisory board provides the necessary stakeholder input throughout the strategic planning process including student learning outcomes, the accounting curriculum, the strategic plan, and the professional accounting issues that will impact the program.

AUM Accounting Graduates – Current Employment Name Position Organization

Bonee Barrow Bailey, CPA Partner

Aldridge, Borden and Company

James Blake, CPA Partner Scott Grier, CPA Partner Jeremy Morehead, CPA Partner Rhonda Sibley, CPA Partner Jason Westbrook, CPA Partner Mathew D. Binns, COA

Bern Butler Capilouto and Massey, CPAs

Helen F. Cleondis, CPA Partner Jerry W. Grant, COA Partner Robert Andy Jones, CPA Partner Clifford E. Massey, CPA Partner Susan M. Patterson, CPA Partner Phyllis Ingram, CPA Partner

Carr, Riggs and Ingram, CPAs David Norris, CPA Partner James Walker, CPA Partner Joe Gary, CPA Partner Diamond, Carmichael, Gary,

Patterson and Duke, PA. Kath Carter, CPA Partner Ernst andYoung Mitch Stroud Manager of Cost Accounting Hyundai Motor Manufacturing AL Dennis Fain, CPA Partner

Jackson Thornton and Company

Rusty Golden, CPA Partner Annamarie Jones, CPA Partner Martin Lee, CPA Partner Patti Perdue, CPA Partner Lyvonnia Poppell, CPA Partner Daniel Thompson, CPA Partner Rena Mears, CPA Partner, Retired KPMG Will Brown, CPA Assistant Division Controller Rheem Manufacturing AL Janice Hamm, CPA Deputy State Comptroller State -‐ AL, Dept. Of Finance Laneita Littleton, CPA Chief Budget Officer State -‐ AL, Dept. of Mental Health Jeffrey M. Wright Chief Accountant State -‐ AL, Dept. of Public Health Fran Copeland, CPA, CGFM Chief Financial Officer State -‐ AL, Dept. of Public Safety Bill Flowers, CGFM, CGFO Chief Financial Officer State -‐ AL, Dept. of Transportation Clynton Hart, Jr., CPA Partner

Warren Averett LLC Daniel Newman, CPA Partner John W. Parrish, CPA Partner Adam Stephenson, CPA Partner

5 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Challenges Increased Competition Montgomery and the River Region is a competitive academic market with three local universities (two public and one private) both offering undergraduate and graduate degrees in accounting. The main campuses of Troy University, Tuskegee University and Auburn University are within a 40-‐mile radius, which is near enough to attract students wanting a traditional campus experience. In addition, there are several proprietary colleges and universities that have entered the Montgomery market over the last five years. Two-‐year schools have become additional major competitors for entering freshmen that has reduced the numbers of sophomore students taking introductory accounting courses. Challenging Staffing Issues The Department of Accounting has been fortunate in hiring new faculty with appropriate qualifications. However, while the department is currently fully staffed by qualified individuals, three faculty members, 42.8% of the accounting faculty (See School of Business Maintenance Report, p. 6), are eligible for retirement. The lack of qualified accounting faculty will be the challenge in replacing the expertise to maintain the quality of the program. In addition, providing adequate funding for continuing faculty development, research efforts and compensation may hamper the department’s ability to retain quality faculty. Decreased funding from the State of Alabama has made funding research and travel difficult. This decreased funding also makes it difficult to maintain competitive salaries, thereby making recruiting and retaining outstanding faculty more of a challenge. While grant availability exists, the AUM business faculty, in general, has limited access to research grants. However, there has been a strong bond among the accounting faculty and a commitment to the purpose of the accounting program provided in an urban environment that initially attracted the faculty and explains the low turnover. Opportunities External Funding To a significant extent, the department relies on resources provided by the University and School for its operations. For example, faculty and staff salaries and benefits are funded through the University budget. Likewise, all the department’s facilities, utilities, support staff, and general operating cost are funded through the University budget. In the 2013 fiscal year, the Accounting Department’s Operations & Maintenance budget totaled approximately $1.13 million. To supplement the budget, the department maintains certain externally generated funds that provide financial support for faculty travel and other activities if needed. The annual contributions from external activities are approximately $13,500 and average balance throughout the year is approximately $40,000. Stakeholder Involvement The department continues to engage the Accounting Advisory Board and other accounting professionals by having them make formal presentations at accounting club meetings and classes, presentations at the annual induction ceremony for Delta Epsilon Kappa (DEK) accounting honor society, providing internship opportunities for students, and networking events for students on campus and/or in the Montgomery professional accounting community. Because AUM has a long

6 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

tradition of providing an excellent accounting education to students with a diverse background, many alumni stakeholders from public practice firms, private companies, and government have been involved in the accounting program at AUM for many years. Finally, employer and alumni stakeholders have been generous with their contributions to the accounting program, especially in the area of accounting scholarships. The program’s stakeholders either provide or support several scholarships for accounting majors and several professional accounting organizations provide annual scholarship opportunities to AUM accounting majors. Enrollment Growth As previously mentioned, the Department of Accounting resides in a competitive academic market with three local universities (two public and one private) offering undergraduate degrees in accounting. The largest competitor is Troy University, which has both undergraduate and graduate accounting programs in two locations: (1) Troy, Alabama (50 miles from AUM) and downtown Montgomery (8 miles from AUM). In addition, Alabama State University has a Master’s in Accounting degree and Huntingdon College, a private institution, offers a 150-‐hour undergraduate degree in Accounting. However, the AUM accounting program attracts the working student, both traditional and non-‐traditional, by offering accounting courses day, night, hybrid, and online. Course planning guides are designed for students who want to take day courses only or evening courses only both of which can be supplemented by hybrid and/or online courses. The department has a history of providing a high quality education for “working” students and should attract students in the future. The accounting specialization in the BSBA degree contributes significantly to the overall University enrollment (See Appendix C: Undergraduate Enrollment Data). For the academic year 2009 – 2013 the accounting program generated 4.74% of the total university enrollment at the undergraduate level. This ranked the accounting program 8 out of the 27 academic units that offer undergraduate courses. The academic units were Liberal Arts, Biology, Secondary Teacher Education, and Elementary Education. Degree Programs Included in the Review This review addresses the Bachelor of Science in Business Administration degree (BSBA) with a specialization in Accounting. The degree does not meet the “accounting concentration” as defined by the Alabama State Board of Public Accountancy. In order to better serve its students, the department does offer graduate level courses in accounting. AUM accounting students can fulfill the State Board’s 150-‐hour education requirement by taking extra accounting classes at either the undergraduate level or enroll in the MBA program that allows three elective courses which can be accounting graduate level courses.

7 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

PROGRESS UPDATE ON CONCERNS FROM PREVIOUS REVIEW The peer review team report from the initial accreditation visit had only one recommendation to address prior to the next visit:

“Auburn University at Montgomery should closely monitor the following items and incorporate them in your ongoing strategic planning initiatives: While AUMs assurance of learning program is adequate, the Department should continue to develop the program by considering whether more learning goals and learning objectives would be helpful in guiding curricular development. The assurance of learning program is currently based on three learning goals (technical knowledge, effective use of technology, and ability to recognize and analyze ethical issues). These three goals are supported by seven specific learning objectives which are evaluated by measures that occur in three classes. Loop-‐closing examples exist for each learning goal. However, since assurance of learning should always be a continuous improvement process, the PRT recommends that the Department continue to evaluate whether other learning goals could be useful, whether those learning goals could be supported by additional or revised learning objectives, and whether the analysis of measures could be improved.”

In 2006, the department created learning goals and objectives for the accounting curriculum with assessment performed in 2007-‐2008. This process has continued since that time (See Assurance of Learning section). The following is a summary of assessment progress made since the initial accreditation report. The department has revisited its assurance of learning program with the results of: (1) modifying the learning goals and objectives; (2) improving assessment measurements; and (3) restructuring the entire process. Originally, Goal 1 read as follows.

Goal 1: Our students can identify and measure relevant data and report results in formats that meet the needs of the report users and adhere to legal and professional standards.

After reviewing the team’s recommendation, the faculty collaborated and developed three learning objectives for Goal 1 to read as follows. Objective 1a: Students will perform steps in the accounting cycle including the

analysis of data for the preparation of adjusting entries and preparation of general purpose financial statements.

Objective 1b: Students will identify and calculate product costs.

Objective 1c: Students will prepare appropriate tax documents for individuals.

After review, the faculty decided to keep original Goal 2.

Goal 2: Students can effectively use technology in an accounting environment and the related objectives.

8 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Originally, Goal 3 read as follows:

Goal 3: Our students can recognize and analyze ethical issues that occur in the accounting environment.

After reviewing the team’s recommendation, the faculty collaborated and developed two learning objectives to read as follows.

Objective 3a: Students will understand the codes of conduct and ethical guidelines for professional accountants.

Objective 3b. Students can recognize and analyze ethical issues that occur in the accounting environment.

After reviewing the team’s recommendation, the faculty collaborated to create an additional goal to read as follows.

Goal 4: Students will identify internal control weaknesses, their impact and recommend mitigation for weakness.

The Department of Accounting is committed to the assurance of learning process for the established learning goals within the separate accounting program. The accounting program not only has established learning goals for the program but also for each course. These learning goals are listed on the course syllabus and instructors assess the goals in various ways at different points in the semester (See Assurance of Learning section).

9 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

STRATEGIC MANAGEMENT

The Department of Accounting strategic planning process aligns with the Auburn University System, AUM, and the School of Business strategic planning processes (See Appendix D: Accounting Department Strategic Plan, 2007-‐2012). The department and school are mission-‐driven and reflect the three primary responsibilities stated in the University’s mission: teaching, research and service (See School of Business Maintenance Report, pages 13-‐18). The mission of the department supports those of the University and School by emphasizing a high quality, student-‐centered accounting specialization degree. In addition, the department faculty produces quality research and is involved in the professional accounting community as well as the larger Montgomery business community. This faculty-‐stakeholder relationship complements the University’s mission to be “an integral part of the surrounding community, state, and region” (AUM Strategic Plan, 2007-‐2012). Department of Accounting Mission The Department of Accounting has a mission to support diverse constituencies, while directly supporting the mission of both the School and the University. A primary element of the department’s mission is to provide a high quality accounting curriculum and sound instruction in the classroom providing its primary stakeholders (i.e. the students) with the knowledge, skills and ability to be successful in the ever-‐changing accounting profession. The Department of Accounting mission statement reads:

In support of the missions of Auburn University Montgomery and the School of Business, the BSBA-‐Accounting Specialization is intended to provide students with knowledge and skills necessary for entry-‐level positions and advancement in accounting. The program provides an in-‐depth study in the basic areas of accounting and serves a market consisting of full-‐time, part-‐time, and evening students from Montgomery and the Central Alabama region.

The department’s objectives are:

• To provide students with the: o Necessary educational background for entry into and advancement in the accounting

profession, o Skills necessary for success in the accounting profession and o Educational background necessary for entry into a graduate program; and

• To provide intellectual contributions through a mix of discipline-‐based contributions to

practice and pedagogy that can be applied in the business and government environments and in classroom instruction.

Although the education requirements to take the Uniform CPA Examination as an Alabama candidate are higher than the minimum requirements for our BSBA-‐Accounting Specialization, these additional requirements to sit for the CPA exam can be satisfied through the Auburn University Montgomery MBA program or by completing additional undergraduate courses. Our quality is reflected in the success of our students, alumni, and faculty, and in the enhancement of the personal and professional lives of community residents through faculty service and research.

10 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Department Vision

The accounting faculty envision the department being a national and international model for accounting education and a partner of choice for educational and professional opportunities with public practice firms, government, business organizations, and non-‐profit entities including professional accounting organizations.

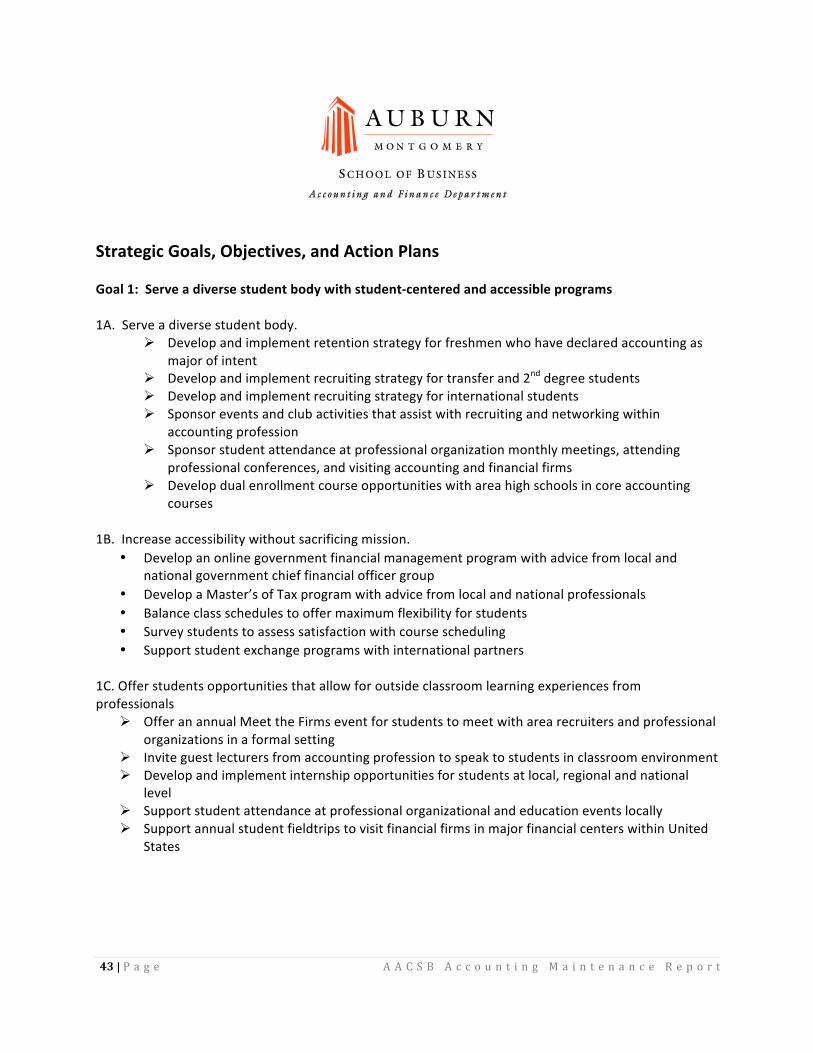

Department Goals

Goal 1: Serve a diverse student body with student-‐centered and accessible programs. Goal 2: Provide a curriculum in the accounting discipline that is current in its content and

develops relevant skills as well as certification opportunities. Goal 3: Attract, maintain, and retain a diverse, highly qualified faculty. Goal 4: Provide continuing learning opportunities for our stakeholders. Goal 5: Provide opportunities for stakeholders to participate in strategic planning and

assessment of the accounting program. Mission Focused The department has a published mission statement that directs the department’s commitment to be responsive and adequately serve “a market consisting of full-‐time, part-‐time, and evening students from Montgomery and the Central Alabama region.” In addition, the Accounting Program provides a quality education for those who wish to retrain and further their employment prospects. Historically, students enrolled in AUM accounting courses are nontraditional (ages 24 or older), working (90+%) either part-‐time or full-‐time, post baccalaureates who are changing or enhancing career paths, and individuals completing the educational requirements to sit for the CPA examination as an Alabama candidate. As such, the department attempts to schedule classes to serve this diverse group of students. Knowing that our students wish to carry a full-‐time course load, the department schedules classes to support the students’ academic goals and also provides information through its Student Advising Guidelines to assist students in planning their course schedule as a day or night student. The distribution of enrollments by full-‐time and part-‐time is decided on the number of hours carried (See Table below). Most “full-‐time” students are also working students. These students typically schedule their courses in blocked time slots to allow them to be employed within the region while they are finishing school. Some students prefer to take classes during the day and work in the evening while other students work during the day and take classes during the evening.

Percentage of Students Enrolled Full-‐Time* and Part-‐Time Fall 2008 through Fall 2012

Fall 2008 Fall 2009 Fall 2010 Fall 2011 Fall 2012

Full -‐ Time 62 66 63 65 60 Part -‐ Time 38 34 37 35 40

100 100 100 100 100

*Full-‐Time = 12 or more semester hours Source: AUM Office of Institutional Effectiveness

11 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

The table below indicates that demand for the undergraduate courses is slightly higher for evening and online courses than for day courses. Most graduate courses are cross-‐listed courses that can be used as electives by students in either the undergraduate accounting program or the MBA program or the post baccalaureate students taking accounting courses. The demand for these courses is primarily evening or online. Therefore, the Department attempts to serve its diverse student body by providing courses on a scheduled basis and at times that will facilitate their academic completion. Students enrolled in accounting courses during the census period at AUM were classified as freshmen (5.3%), sophomores (18.9%), juniors (21.8%), seniors (19.8%), and post baccalaureates (34.2%). With approximately 1/3 of enrollments in accounting courses being filled by individuals who wish to change their career path or enhance their career path which can include continuing their education to qualify to sit for the CPA exam, the AUM Accounting Program AUM has been and continues to serve its stakeholders and the broader River Region community.

The department’s mission statement includes the objective, “intellectual contributions will be a mix of contributions to practice, pedagogy and discipline-‐based research that can be applied in the business and government environments and in classroom instruction.” The faculty of the department is expected to remain current in their area of expertise by publishing research and attending

Percentage of Enrollments By Course Level and by Day and Night Offerings

Fall Semesters 2008 through 2013

Fall 2008 Fall 2009 Fall 2010 Fall 2011 Fall 2012

Undergraduate Accounting Enrollments Day 47% 47% 49% 43% 45% Night 53% 53% 52% 40% 43% Online 0% 0% 0% 17% 12%

100% 100% 100% 100% 100%

Graduate Accounting Enrollments Day 17% 0% 2% 0% 0% Night 83% 100% 79% 50% 95% Online 0% 0% 0% 50% 5%

100% 100% 81% 100% 100%

Total Accounting Enrollments Day 42% 40% 42% 32% 35% Night 59% 60% 58% 42% 54% Online 0% 0% 0% 26% 11%

100% 100% 100% 100% 100%

Source: AUM Office of Institutional Effectiveness & AUM Argos Database

12 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

educational programs in conjunction with their teaching responsibilities. The intellectual contributions published by the accounting faculty are primarily projects that advance the knowledge and effective business practices in accounting and are used in the classroom to demonstrate the importance of maintaining competence (continuous improvement) in a very dynamic discipline. The research conducted by the department’s faculty is predominately contributions to practice research (85%) that relates directly to effective professional practice (See Appendix E: Faculty Participation; specifically AACSB Table 2-‐1: A Five Year Summary of Intellectual Contributions).

Because the accounting faculty interacts significantly with the professional community, the focus of their research is current issues and emerging trends in the accounting profession. As such, the intellectual contributions of the faculty are linked closely with the accounting profession with publications in practitioner periodicals such as The Journal of Accountancy, The Journal of Government Financial Management, The Internal Auditor, The Practical Accountant, The Journal of Public Budgeting, Accounting and Financial Management, Financial Accountability and Management, and Journal of Management Accounting. The accounting faculty conducts joint authorship with other accounting and business faculty and business professionals. The School of Business and the Department of Accounting have written guidelines that specify expectations of faculty with regard to intellectual contributions (See School of Business Maintenance Report, pages 27-‐28).

Strategic Planning Process

The School of Business engages in a systematic planning process that is intricately linked to the University’s process (See the School of Business Maintenance Report, pages 15-‐16). Accounting faculties serve on University and School Strategic Planning Committees and Task Forces which provides information to the department for use in its strategic planning process.

The development and review of the department’s mission statement is part of the periodic strategic planning process for the University, School, and Department. This process occurs every five years. Stakeholders at every level (university, school, department, students, community leaders, etc.) are included in the process to provide input to the mission. The strategic plan includes goals, objectives, and action plans. As noted above, the School has a five-‐year strategic plan supported by departmental strategic goals and objectives, including those for the Department of Accounting. Following the spring semester of each year, strategic goals are identified for the University and the School. The department identifies goals and related objectives that are linked to goals of the University and School. These goals and objectives are discussed among the faculty members and the School Leadership Council, which includes the School dean, associate deans, and department heads. At the end of the following year, an assessment is performed of the goals and objectives established for that year. Assessments of the department’s strategic goals for the census period are also provided in Appendix D. Additionally, certain high priority continuous improvement goals have been identified. These goals are as follows:

• Continue to provide students with opportunities for professional interaction in the form of internship opportunities, networking events, and attending professional educational events;

• Continue to conduct assessment of the accounting program learning goals incorporating in action plans for areas identified as less than 70 percent achievement of learning goals;

13 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

• Evaluate the responses of both accounting alumni and employers of accounting graduates from the School of Business survey to determine satisfaction with the AUM accounting program;

• Continue to expand the Accounting Advisory Board to include representatives from the government and managerial areas and continue to hold formal meetings to obtain input on mission, curriculum, quality of graduates, and other important areas; and

• Continue to provide faculty opportunities to interact professionally in the Montgomery business, government, and nonprofit accounting community as well as at the state, regional, national and international level.

Selected Accomplishments (2008-‐2013)

• The Department of Accounting continued to focus on student development with one-‐to-‐one advising by faculty; assisting the students to participate in several events for professional networking with practitioners, and providing student academic course planning guides for both day and night students. Continuous assessment review has resulted in significant improvements to the department learning goals as well as course learning goals and objectives for each accounting core course and electives.

• The department provided experiential learning experience for the student to acculturate them to the real world. AUM accounting students regularly participate in the IRS Vita Program. “In 2013, twenty-‐one trained students from AUM provided critical services at a free tax preparation site that prepared returns for approximately 670 families, which helped them to secure almost $1.5 million in tax refunds and saving them $201,000 in commercial tax preparation fees.”1 In addition, governmental accounting students participated in the AGA national case competitions in fall 2011 and 2012.

• The nationally recognized Governmental Financial Management Accounting Program provided students and career accountants guided education in preparation for the Certified Government Financial Manager (CGFM) examinations and provided continuing profession education required to maintain certification. The Becker CPA Review offered as an accounting elective to MBA students beginning 2011.

• Faculty involvement in international efforts included teaching in Malaysia in 2009, Vietnam in 2010, and China in 2012 as well as traveling with the AUM team in 2008 and 2013 to discuss faculty and student exchanges in China.

• The department successfully hired qualified faculty including Dr. Teresa Lang in fall 2011 to teach tax and accounting information systems; Dr. Richard Turpen in the summer 2012 to teach financial accounting and auditing, and Dr. Dan Hollingsworth in July 2012 as department head.

• The department continued to partner annually with the ASCPA and AGA-‐Montgomery Chapter to provide continuing professional education opportunities for our stakeholders. As a result of the efforts, the department funded faculty research travel, meeting attendance, and professional memberships through the period.

1 Stephan Black ([email protected]) email to AUM Chancellor John Veres.

14 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

• The Accounting Advisory Board was increased to 24 voting members representing public practice firms, government, and business organizations. The Advisory Board has provided guidance which was incorporated into the Department’s Mission and Goal statements for the next review period, 2013-‐2018.

Financial Strategies Although the University has experienced a decline in enrollment which has resulted in less state funding and increased tuition, there has been an increase in University funding for the academic units (see School of Business Maintenance Report, page 6). Data for the School and Department of Accounting Instructional and Support Budgets, including both department-‐level compensation and operating and maintenance budgets is reported in Appendix F. Budget Summary Detail The instructional budget for the Accounting Program only (excluding the Finance Program) includes two items that changed significantly (See Table, p. 14). First, one retirement and one resignation decreased the compensation budget for 2010-‐11. Subsequently, new hires in 2012

!

Department)of)Accounting)Instructional)Budgets)FY)2008/09)–)2012/13)

)!! 08/09% 09/10% 10/11% 11/12% 12/13%

Faculty%9%month%salaries%and%administrative%salaries% $1,250,314! $1,221,956! $979,592! $1,237,540! $1,111,836!%Accounting%%Summer%School%Compensation% $93,022! $122,463! $97,571! $83,054! $113,512!%Total%Accounting%O&M% $6,515! $7,172! $18,201! $16,696! $15,340!Total%Department%of%Accounting%Operating%Budget% $1,349,851! $1,351,591! $1,095,364! $1,337,290! $1,240,688!

!!%%%of%change% na! 0.13%! 218.96%! 22.08%! 27.22%!

%School%of%Business%Operating%Budget% $23,197,262! $23,633,514! $26,652,177! $25,363,126! $26,221,148!%Accounting%%as%a%%%of%School%of%Business%Budget% 5.80%! 5.71%! 4.11%! 5.27%! 4.73%!Source:)))AUM)Budget)Books)

15 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

increased compensation costs in 2011-‐12. Summer school compensation is listed separately and is managed in the Office of the Provost (formerly Vice-‐Chancellor for Academic Affairs). Second, O&M budgets were increased in 2010-‐11 and 2011-‐12 to cover costs related to AACSB initial accounting accreditation. In 2012-‐13, the O&M budget was increased to include faculty travel funds which were previously held in the Dean’s budget. The department’s operating budget has averaged 5.12% of School of Business operating budgets over the five year census period. There is a strong commitment from central administration and the School of Business dean to support the programs offered in the department. The Accounting Program was part of the Department of Accounting and Finance at the time of initial accounting accreditation in 2011-‐12. As of January 1, 2012, the finance program was moved to the Economics Department as were the appropriate share of the operating budget. (See Appendix F for detailed information regarding the Department’s operating budget with and without the finance program). Private Support The Department of Accounting also has autonomous funds that are generated through CPA review courses and CPE seminars and programs that it offers as joint ventures with the Alabama Society of CPAs and the Association of Government Accountants – Montgomery Chapter. The table below highlights the funds that the department has generated outside of university sources. Such funds are used to help defray the cost of academic travel, pay dues for professional organizations in which the faculty belong, and help with student activities. The Becker CPA Review Program no longer makes a financial contribution to the Department of Accounting. Enrollment in the live course on the AUM campus included mostly non AUM students and some AUM MBA students. That enrollment pool has been declining to the point where Becker decided it could no longer make a financial contribution to the AUM Department of Accounting. However, the department, with University permission, agreed to let the Becker Review Course meet in its classroom for which Becker would grant 1 full scholarship and 3 half scholarships to AUM students enrolling in the Becker CPA Review course. The Accounting Faculty Scholarship Committee selects the student recipients of the Becker Scholarships. In addition to these funds, the Department of Accounting has several scholarship funds that are used to assist students. The accounting scholarship donors provide financial awards to students on a competition basis each year. The amount awarded from each scholarship varies but students usually receive between $1,000 and $2,000 per year. Some scholarship funds are large enough to grant scholarships to multiple students.

Accounting Program Non-‐University Generated and Unrestricted Funds (2008 – 2013) 2008-‐09 2009-‐10 2010-‐11 2011-‐12 2012-‐13 5 Year Total

FAAC $11,320 $8,284 $9,211 $10,472 $12,144 $51,431 AGA -‐ $1,289 $5,889 $4,910 $4,144 $16,232

Becker CPA Review $2,146 $149 $3,811 $3,805 $765 $10,676 Donated Funds $2,910 $4,140 $1,785 $285 $825 $9,945

Total $16,376 $13,862 $20,696 $19,472 $17,878 $88,284

16 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Next Five Years

2012 was the planning year for the 2013-‐2018 Auburn University at Montgomery Strategic Plan. Strategic planning activities were conducted at the University and School levels. Accounting faculty served on University and School strategic planning committees. The Department of Accounting was in a period of administrative transition in 2012 and no formal departmental strategic planning occurred. The accounting faculty did, however, start the strategic planning process in summer 2013. The department faculty and student officers, Accounting Club and Delta Epsilon Kappa, will attend the Accounting Advisory Board meeting to discuss the strategic plan for 2013-‐2018. A copy of the 2013-‐2018 Department of Accounting Strategic Plan is available for review in the department office, upon request.

The Department of Accounting as part of the School of Business prepares an annual financial plan that includes projected budgetary needs and sources of funding for operations to accomplish adopted strategic plans. These budgetary funds are not expected to increase dramatically in the next few years. However, the funds are sufficient to maintain the current level of high-‐quality education delivered to AUM accounting students.

To achieve the desired level of excellence the School and Department aspire to have in the future will require external fundraising. The University Office of Advancement is aware and supportive of departmental fundraising to acquire excellence funds needed to advance the accounting program to a level comparable to its aspirant programs. Longer term goals include raising funds for numerous endowed scholarships to use in recruiting and retaining the best and brightest students to the AUM accounting program. In addition, fundraising is needed for endowed professorships and chairs in the department to recognize current faculty and attract new faculty to move the department closer to its aspirant accounting programs.

Accounting Scholarship Donors

Aldridge Borden and Company Annual Scholarship

Bern, Butler, Capilouto and Massey PC Scholarship in Accounting David L. Sayers Endowed Scholarship

Jackson, Thornton and Company, PC Scholarship Mary R. Golden Endowed Scholarship

Wilson, Price, Barranco, Blankenship and Billingsley, PC Scholarship Warren-‐Averett, LLC

Alabama Society of CPAs – Educational Foundation Alabama Society of CPAs – Montgomery Chapter

Association of Government Accountants -‐ Montgomery Chapter Alabama Government Finance Officers Association – Patrick W. Kelly Scholarship

Institute of Management Accountants – Montgomery Chapter Institute of Internal Auditors – Montgomery Chapter

17 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

The department has established no new degree programs since the last AACSB visit. However, the Department of Accounting has developed a minor in accounting that is open to both business and nonbusiness majors. This minor consists of 12 semester hours. The prerequisite for entering the accounting minor program is the successful (grades of B or higher) completion of the following courses:

• ACCT 2010 Introduction to Financial Accounting 3 SH PR Math 1120 • ACCT 2020 Introduction to Managerial Accounting 3 SH PR ACCT 2010

The accounting minor consists of one required course and 3 elective courses: Required Accounting Course

• ACCT 3110 Intermediate Accounting I 3 SH PR ACCT 2010 & 2020

Elective Accounting Courses -‐ select 3

• ACCT 3120 Intermediate Accounting II 3 SH PR ACCT 3110 • ACCT 3200 Accounting Information Systems 3 SH PR ACCT 2010, 2020, &

INFO 2070 • ACCT 3210 Managerial Cost Accounting 3 SH PR ACCT 2010 & 2020 • ACCT 3310 Income Tax Accounting 3 SH PR ACCT 2010 & 2020 • ACCT 4510 Government and Nonprofit

Accounting and Financial Reporting 3 SH PR ACCT 3110

Students pursuing a Minor in Accounting must earn grades of C or higher in all upper division accounting courses taken. Students who receive a D or F in an upper division accounting course have one opportunity to repeat that course. Two D or F grades will result in the student being removed from the Accounting Minor Program. In collaboration with its stakeholders, the Department of Accounting is exploring the need for a master’s degree in accounting. This work includes the development of the master’s degree mission, vision, and program learning goals. Stakeholders will meet November 14 to provide input to the Department’s Strategic Plan for 2013 – 2018 and to the master’s degree proposal. Stakeholders have expressed their desire that the Department offer the advanced degree as it would enable them to recruit professional accountants more easily. As previously reported (see page 10), the high percentage of post baccalaureate students enrolled in accounting courses indicates a significant number of students could be better served through an AUM Master’s Degree in Accounting.

18 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

PARTICIPANTS

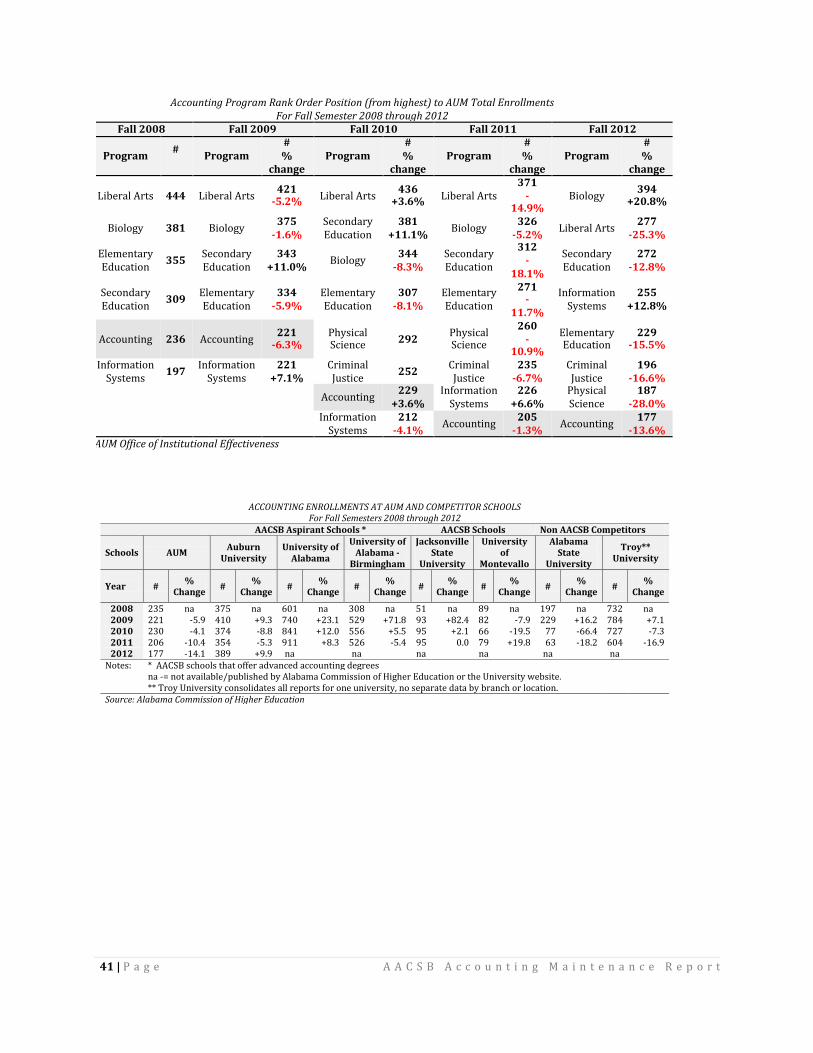

Students Enrollment Trends The accounting program has an averaged approximately 214 majors each year during the five year census period. Generally this group of students accounts for a “critical mass” of business majors. The table below reports the FTE position relative to the School (average of 19.0%) and to the University (average of 4.58%) during a time of declining enrollments. The fall 2012 census data had the greatest decline (-‐ 8%) in University enrollment during the census period. The Accounting Program continues to rank in the top 25% of degree granting programs at AUM. The range of average % of program graduates to total AUM program graduates for the census period was 4.74%(lowest) to 8.6% (highest) (See Appendix C: Undergraduate Enrollment Data, for more detailed enrollment data).

AUM and Accounting Program Enrollment and Graduates AUM

Total FTE Accounting Program FTE

Accounting FTE % of School FTE

Accounting FTE % of AUM FTE

Accounting Graduates per Academic Year

Accounting Graduates

% of School

% of AUM

Fall 2012 3683 177 17.3 4.2 33 21.4 5.9 Fall 2011 3984 205 19.1 4.7 23 14.4 4.2 Fall 2010 4218 229 20.4 4.8 47 23.4 7.3 Fall 2009 4096 221 19.0 4.7 29 13.5 4.4 Fall 2008 3860 236 19.7 4.5 46 21.5 7.1 Source: Five Year Enrollment by CPIC and Completions, AUM Office of Institutional Effectiveness Diversity AUM recognizes a responsibility to serve a diverse student body with a variety of educational needs. The university welcomes applications from all interested students, resulting in slight changes throughout school (See School of Business Maintenance Report, page 14). The Accounting majors at AUM are representative of the diverse AUM student body (See Table below). For the

Accounting)Completers)1)Undergraduates)Summary)1)All)Terms)Summer)2008)1)Spring)2013)

!! !!!!!!!Female! !!!!!!!!Male! !!!!Total!

!#! %! #! %! #! %!

American!Indian!! !

1! 1.3! 1! 0.6!Asian! 6! 5.8! 3! 4! 9! 5.1!Black!or!African!American! 23! 22.5! 7! 9.2! 30! 16.9!Hispanic/Latino! 1! 1.0! 1! 1.3! 2! 1.1!Native!Hawaiian!!Pacific!Island! 2! 2.0! 1! 1.3! 3! 1.6!Other! 1! 1! 2! 2.6! 3! 1.7!Unspecified! 2! 2!

! !2! 1.1!

White! 67! 65.7! 61! 80.3! 128! 71.9!

!102!

!76!

!178!

!Source:)AUM)Office)of)Institutional)Effectiveness)!

19 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

census period, the gender distribution for accounting majors earning their undergraduate degree was 57% female and 43% male. The predominate ethnic groups from high to low are White 71.9%, Black or African American 16.9%, Asian 5.1%, and all others combined 4.5%. Admissions Criteria Students admitted to the School of Business – Accounting Specialization must meet the University admission requirements (See School of Business Maintenance Report, page 20). In addition, all accounting must follow School of Business requirements for all business students which require grades of C or higher in all lower division business core classes: ACCT 2010 Principles of Financial Accounting and ACCT 2020 Principles of Managerial Accounting. Accounting majors have historically scored higher averages on the ACT than overall business students receiving undergraduate degrees (See Table below).

The accounting faculty, after reviewing assessment data of accounting majors, changed the grade requirement for all accounting majors in the lower division courses, ACCT 2010 and ACCT 2020, from a grade of C to a grade of B. The change was made to assure that students are prepared for the rigor of the upper-‐level accounting courses. The School of Business Curriculum Committee approved the change in April 2013 becoming effective January 1, 2014. In addition to requiring a grade of C or higher in all upper division accounting courses, the Accounting Faculty established a policy requiring students to maintain their academic accounting standard throughout the program. Any accounting major who receives two D or F grades in their upper division accounting courses will be dismissed from the accounting program (See Policy below) (AUM Undergraduate Catalog 2012 – 2013 pp. 79). Grade Requirements for Upper Division Accounting Specialization Courses Students enrolled in the B.S.B.A. degree program with a major in accounting must achieve a minimum grade of C in all upper division accounting courses. Students who receive a D or F in an upper division accounting course at AUM have one opportunity to repeat that course and the course must be repeated at AUM. Students who receive a D or F in any two upper division accounting courses at AUM will be dis-‐enrolled from the program and will not be eligible for readmission. Students who have failed (D or F) one course will meet with the Head of the Department of Accounting prior to enrollment in any upper division accounting course. The student must submit a written plan for improving future performance for approval by the Head of the Department of Accounting before permission can be granted to enroll in any upper division accounting courses at AUM.

Source: AUM Undergraduate Catalog

ACT Scores of Graduates Receiving Undergraduate Degrees 2008-‐09 2009-‐10* 2010-‐11 2011-‐12 2012-‐13

Accounting 21.5 n/a 22.6 21.9 19.9 School of Business 20.6 n/a 20.7 21.0 20.9 Source: AUM Office of Institutional Research *data issue for year (will have appropriate data at team visit)

20 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

Internship Opportunities Internships also allow students an opportunity to gain practical experience and assess an employer and/or industry to determine future opportunities. In addition, such opportunities give employers time to observe the students’ knowledge, skills and abilities in advance of a permanent job offer. In the past two years, the school in general and the accounting program specifically have redesigned and upgraded the school’s internship program. Internships for course credit can be either paid or unpaid experience and represent a business elective. The School of Business has a formal internship approval process that includes basic requirements such as a minimum GPA, a required presentation of the work completed, and an evaluation of the student’s learning experiences (See Appendix G: Internship Process). A variety of firms and government agencies have provided accounting internships during the past five years (2008-‐2013). Those organizations are identified in the following table.

Career and Placement Services The Department of Accounting is continuing its practice of managing announcements within the department while collaborating with the school. Direct requests from employers occur frequently in the department for potential full-‐time positions with experience as well as the occasional part-‐time positions. The administrative associate within the department emails appropriate students and/or graduates regarding opportunities as directed by the department head. The administrative associate also maintains a book of job listings, which is located in the departmental suite and is available to students during office hours. For nearly 20 years, the department has participated in the Alabama Society of Certified Public Accountants (ASCPA) Accounting Interview Day held each fall semester. The program, initially

Firms/Businesses+Providing+Internships!2008+82013!

Capital'City'Club'Montgomery'County'Revenue'Commissioner'Aldridge'Borden'Wilson'Price'Mark'Jennings,'CPA'Carr,'Riggs'and'Ingram'Hodges'Business'Services'Goodwyn,'Mills'and'Cawood,'Inc.'Hausted'Patient'Handling'Systems,'LLC'Alabama'Retail'Association'Source:+AUM+Accounting+Department++Records+

!

21 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

developed by AUM accounting Professor Dr. Judith Kamnikar, was designed to give students from smaller accounting programs the opportunity to interview with larger firms. In the beginning, students selected to participate in this event were required to view videos about interview skills, dress and comportment. More recently, the ASCPA, along with the Department of Accounting, hosts an Interview Skills Workshop. Another student-‐focused event sponsored by the department is Meet-‐the-‐Firms. Started by Dr. Keren Deal, the on-‐campus “Meet the Firms” event originally helped our students compete with students from other campuses for internships at larger CPA firms. The first “Meet the Firms” was held on September 26, 2006 involving recruiters from five public accounting firms, six areas of Alabama state government, and one bank. In fall 2012 the event was opened to the entire School of Business and included a broad selection of employers interested in hiring students in all business majors. An additional example of a student-‐employer networking event was held on April 18, 2013 on the tenth floor of the Library following the induction ceremony of Delta Epsilon Kappa honor society. Students interacted with firm representatives for an hour long session in a professional setting. Students also accompany faculty members throughout the year to professional accounting organizations’ meetings: Alabama Society of Certified Public Accountants – Montgomery Chapter; Association of Government Accountants – Montgomery Chapter; Institute of Internal Auditors – Montgomery Chapter; Institute of Management Accountants – Montgomery Chapter. These luncheon meetings provide a networking opportunity for the students. Advising Services Advising support for students in the accounting program include the services of the School of Business Information and Advising Office, as well as, Department of Accounting faculty advice and assistance. The Business Information and Advising Office maintains the individual student files to facilitate the advising of students in curriculum matters, course scheduling, registration, and monitoring a student’s progress towards graduation using a curriculum sheet (See Appendix H: Curricular Sheet). A further advising avenue for students is with the accounting department head, who maintains an open-‐door policy to discuss academic and career matters with students. Though the majority of assistance relates to matters such as the grade policy, scheduling conflicts, and future curriculum offerings, the department head’s primary advising activities occur in two areas. First, the department heads advises many students with regard to course requirements and schedules for sitting for the Uniform CPA exam. The second area involves either returning students with liberal arts or sciences degrees or MBA students that cannot secure a satisfactory job. Primarily, the department head discusses curriculum requirements for a returning student that wants to change fields, and then the department head discusses career opportunities in the accounting profession to make the future student aware of the work required to be successful. The Department has developed curriculum planning sheets for both day and night students, course availability schedules, and an articulation document for the AUM Accounting Program and the education requirements to sit for the CPA Exam as an Alabama Candidate (See Appendix I: Student Advising Guidelines for Accounting Majors). Accounting faculty members are involved with advising and student interaction on regular basis. Like the school’s entire full-‐time faculty, accounting faculty is required to have a minimum of eight office hours each week. Because of the day and night teaching schedules, faculty members are

22 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

available to both groups of students. Although the majority of interaction taking place relates to classroom matters, students often come to talk about career opportunities or ask the instructor for a letter of reference. Students have the opportunity to provide feedback on faculty availability using the course evaluation forms (CEFs) that are administered on either the last or second to last day of classes in a semester. The EBI survey administered annually enhances the analysis of student advising effectiveness by showing independently that the accounting students feel that the faculty are both accessible and fair (See Appendix J: EBI Survey Results). Student Development and Organizations The department supports two student organizations. The Accounting Club, which is open to any student who has an interest in the field of accounting, provides opportunities for students to keep current on jobs and curriculum changes and to interact with firms through on-‐campus speakers or sponsored field trips. Through its monthly meetings the club hosts organizations such as the Alabama Society of Certified Public Accountants (ASCPA), Institute of Management Accountants (IMA), Association of Government Accountants (AGA), and others in an effort to help students learn about careers and opportunities. Delta Epsilon Kappa (DEK) is an Accounting Honor Society for students that have shown high academic achievement in the accounting program. Each spring semester, approximately 10 students who meet the following criteria are invited to join DEK (See Appendix K: Accounting Honor Society).

• Overall minimum GPA of 2.75 • Junior, Senior or Graduate status • Must have completed Intermediate Accounting I with a minimum grade of “B”;

completed at least five accounting courses in total, at least two taken at AUM Student Satisfaction Overall, student satisfaction with their experience at AUM and its accounting program has increased as evidenced by the EBI Survey (See Table, p. 23). In the 2011-‐2012 survey periods, the AUM accounting program was rated higher than the AUM School of Business, the Select Six Institutions, the Carnegie Class Institutions, and the total for All Institutions except for Learning Outcomes – Uses and Management of Technology. The department continues to address this issue. Faculty An overview of faculty management policies, including recruitment, hiring, mentoring, evaluation, reward systems, and other items is provided in the School of Business Maintenance Report (pages 25-‐29). The Department of Accounting adheres to the same policies as other departments in the School. There have been three changes in the faculty since the last AACSB visit in 2011. Dr. Fred Jacobs resigned in February 2012 due to health issues. Dr. Jacobs had previously retired from Georgia State University. Dr. Richard A. Turpen was hired after a national search and joined the faculty May 16, 2012. After a second national search, Dr. Dan Hollingsworth was hired as department head effective July 1, 2012. For personal reasons, Dr. Hollingsworth resigned as of June 30, 2013 and is currently Department Head, University of Tennessee – Chattanooga.

23 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t

School of Business EBI Survey

Factor AUM – Accounting Survey Results 2007-‐08 2009-‐10 2011-‐12

1 Required Courses: Quality of Faculty and Instruction 4.64 4.25 5.05

2 Required Courses: Faculty Responsiveness Grades and Student Effort 5.50 5.03 6.31

3 Major Courses: Quality of Faculty and Instruction 4.93 4.60 5.85

4 Major Courses: Faculty Responsiveness Grades and Student Effort 5.54 4.97 6.41 5 Breadth of Curriculum 5.46 4.80 5.89

6 Size of Enrollments for Required and Major Courses 5.93 5.40 6.33

7 Student Organizations and Extracurricular Activity 4.45 4.50 5.89

8 Facilities and Computing Resources 5.27 4.35 5.81 9 Characteristics of Fellow Classmates 5.05 5.10 5.70

10 Placement and Career Services 3.79 3.75 5.47

11 Advisor 5.41 4.78 6.11

12 Learning Outcomes – Effective Communications and Team Work 5.00 5.37 5.59 13 Learning Outcomes – Uses and Management of Technology 4.46 4.55 5.00

14 Learning Outcomes – Management and Leadership Skills 4.73 4.75 6.11

15 Learning Outcomes – Critical Thinking and Problem Solving 5.25 5.35 6.22 16 Overall Program Effectiveness 5.19 4.53 6.19

Administratively, there have been some changes within the department during the census period. Dr. Keren Deal was named Associate Dean for the Undergraduate Program effective January 1, 2012. Dr. Judith Kamnikar, a former Department Head, assumed the role of interim department head. She also assumed the interim Department Head position on July 1, 2013 with the departure of Dr. Hollingsworth. Faculty Work Load Class assignments and teaching loads are set by the department head based on enrollment projections and consultation with the faculty. The typical teaching schedule for a tenure track and tenured accounting faculty member is 18 semester hours per academic year. Faculty who have administrative responsibilities are given release time from teaching. The teaching load for accounting faculty members is governed by the University faculty workload policy as stated in the AUM Faculty Handbook and reiterated in the School of Business Faculty Handbook. When needed, qualified adjunct faculty members are hired to teach classes. There are no adjunct faculty members employed during the 2013-‐14 academic year. Only two adjuncts, teaching two courses, were employed since the initial Accounting Accreditation. Academic assignments other than research are made as equitable as possible among the faculty. All of the members of the accounting faculty are engaged in the development, design, and maintenance of the department’s undergraduate curriculum. They have been meeting twice monthly to improve the assurance of learning process in the accounting program and to explore initiatives that will better serve the School, University, and the professional accounting community in the region. The Accounting Faculty contributes to university governance and initiatives, School governance and initiatives, and professional service activities. In addition, the faculties have served on numerous committees and task forces for the Department, the School, the University, and many professional accounting organizations at the local, state, and national levels. All of these activities help to support the mission and goals of the department.

24 | P a g e A A C S B A c c o u n t i n g M a i n t e n a n c e R e p o r t