Accounting for Indirect Taxes - Update on ASC 450 · Ohio Tax Workshop N Accounting for Indirect...

195

Ohio Tax Workshop N Accounting for Indirect Taxes - Update on ASC 450 Thursday, January 27, 2011 3:00 p.m. to 4:00 p.m.

-

Upload

trinhhuong -

Category

Documents

-

view

221 -

download

0

Transcript of Accounting for Indirect Taxes - Update on ASC 450 · Ohio Tax Workshop N Accounting for Indirect...

Ohi

o T

ax

Workshop N

Accounting for Indirect Taxes -

Update on ASC 450

Thursday, January 27, 2011 3:00 p.m. to 4:00 p.m.

Biographical Information

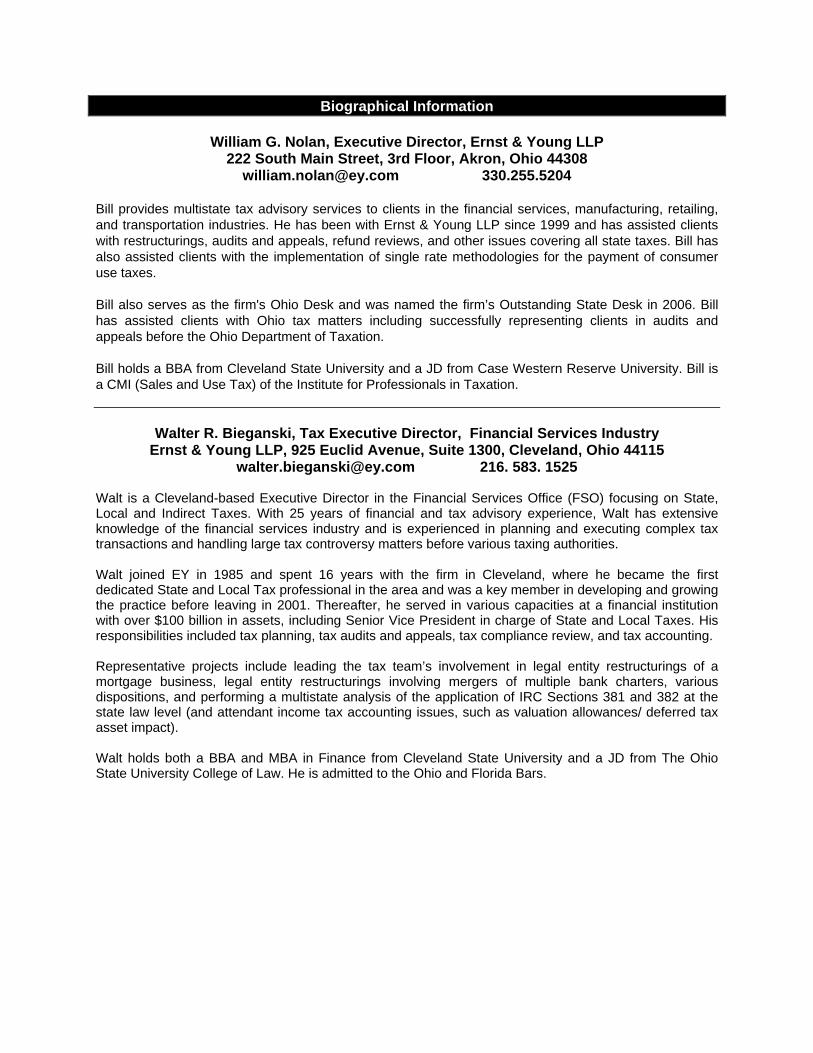

William G. Nolan, Executive Director, Ernst & Young LLP 222 South Main Street, 3rd Floor, Akron, Ohio 44308

[email protected] 330.255.5204

Bill provides multistate tax advisory services to clients in the financial services, manufacturing, retailing, and transportation industries. He has been with Ernst & Young LLP since 1999 and has assisted clients with restructurings, audits and appeals, refund reviews, and other issues covering all state taxes. Bill has also assisted clients with the implementation of single rate methodologies for the payment of consumer use taxes. Bill also serves as the firm's Ohio Desk and was named the firm’s Outstanding State Desk in 2006. Bill has assisted clients with Ohio tax matters including successfully representing clients in audits and appeals before the Ohio Department of Taxation. Bill holds a BBA from Cleveland State University and a JD from Case Western Reserve University. Bill is a CMI (Sales and Use Tax) of the Institute for Professionals in Taxation.

Walter R. Bieganski, Tax Executive Director, Financial Services Industry Ernst & Young LLP, 925 Euclid Avenue, Suite 1300, Cleveland, Ohio 44115

[email protected] 216. 583. 1525 Walt is a Cleveland-based Executive Director in the Financial Services Office (FSO) focusing on State, Local and Indirect Taxes. With 25 years of financial and tax advisory experience, Walt has extensive knowledge of the financial services industry and is experienced in planning and executing complex tax transactions and handling large tax controversy matters before various taxing authorities. Walt joined EY in 1985 and spent 16 years with the firm in Cleveland, where he became the first dedicated State and Local Tax professional in the area and was a key member in developing and growing the practice before leaving in 2001. Thereafter, he served in various capacities at a financial institution with over $100 billion in assets, including Senior Vice President in charge of State and Local Taxes. His responsibilities included tax planning, tax audits and appeals, tax compliance review, and tax accounting. Representative projects include leading the tax team’s involvement in legal entity restructurings of a mortgage business, legal entity restructurings involving mergers of multiple bank charters, various dispositions, and performing a multistate analysis of the application of IRC Sections 381 and 382 at the state law level (and attendant income tax accounting issues, such as valuation allowances/ deferred tax asset impact). Walt holds both a BBA and MBA in Finance from Cleveland State University and a JD from The Ohio State University College of Law. He is admitted to the Ohio and Florida Bars.

ASC 450 Implications Related I di S Tto Indirect State Taxes

2011 Ohio Tax Conference2011 Ohio Tax Conference

January 27, 2011

Agenda

► ASC 450 basics► Liabilities and contingencies► Estimation► Disclosure

ASC 450 E D ft► ASC 450 Exposure Draft► Questions

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 2

ASC 450 basics

ASC 450 requirements

► ASC 450 requires that a loss contingency must be di l d if th l i “ b bl ” it t bdisclosed if the loss is “probable” or its amount can be “reasonably estimated”

► If both elements are satisfied, the loss must be recognized► If both elements are satisfied, the loss must be recognized and the nature and amount of the accrual must be disclosed

“ f f► The term “probable” is not assigned any specific definition ► A contingency generally will be deemed to be “probable” if it is

“likely to occur” (i.e., there is a 65% to 75% or greater likelihood that the contingency will occur)

► Consistent with a “should” level of opinion

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 4

Indirect taxes significant to ASC 450 analysis

► Sales & Use Taxes► Gross Receipts Taxes (e.g., Washington B&O, Ohio CAT)► Property Taxes

P ll T► Payroll Taxes ► Capital Stock and Franchise Taxes► Non-US Taxes (e g Canadian GST/PST/HST VAT)► Non-US Taxes (e.g., Canadian GST/PST/HST, VAT)► Withholding Taxes► Customs Duties► Other taxes not covered by FAS 109

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 5

Differences between ASC 450 and IFRS on t t t f ti itreatment of contingencies► For companies governed by IFRS, guidance in IAS 37 is

ll i l t t US GAAP ASC 450generally equivalent to US GAAP, ASC 450► Threshold

► MLTN v Probable► MLTN v. Probable

► Measurement and Reserves► Best estimate v. Probable Outcome

► Disclosure► Only general nature of dispute and reason that information is not

disclosed v. GAAP more restrictive disclosure requirementsG q

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 6

Liabilities and contingencies

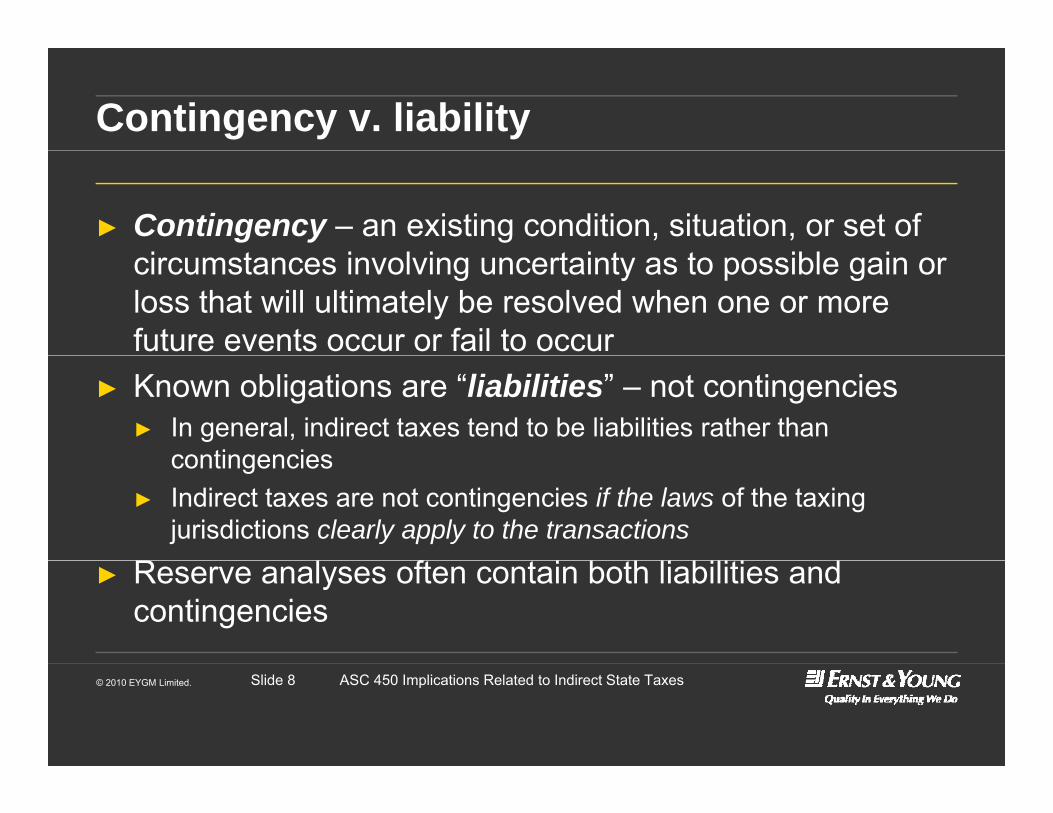

Contingency v. liability

► Contingency – an existing condition, situation, or set of i t i l i t i t t ibl icircumstances involving uncertainty as to possible gain or

loss that will ultimately be resolved when one or more future events occur or fail to occur

► Known obligations are “liabilities” – not contingencies► In general, indirect taxes tend to be liabilities rather than

contingenciescontingencies► Indirect taxes are not contingencies if the laws of the taxing

jurisdictions clearly apply to the transactions

R l f i b h li bili i d► Reserve analyses often contain both liabilities and contingencies

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 8

“Liabilities” and ASC 450 “contingencies”

► Examples of indirect taxes representing “contingencies” d ASC 450under ASC 450:

► Uncertainty about whether certain transactions are subject to the tax (e.g., questions of classification or of nexus)► Leasing► Consignment► Home officesU t i t b t th t f th t ( ti t d► Uncertainty about the amount of the outcome (e.g., negotiated settlements, litigated amounts)

► Class action lawsuitsI di t t t bli h d t f h ti► Indirect tax reserves established as part of purchase accounting

► Uncertainly about whether certain activities require VAT registration

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 9

Sales and use tax examples

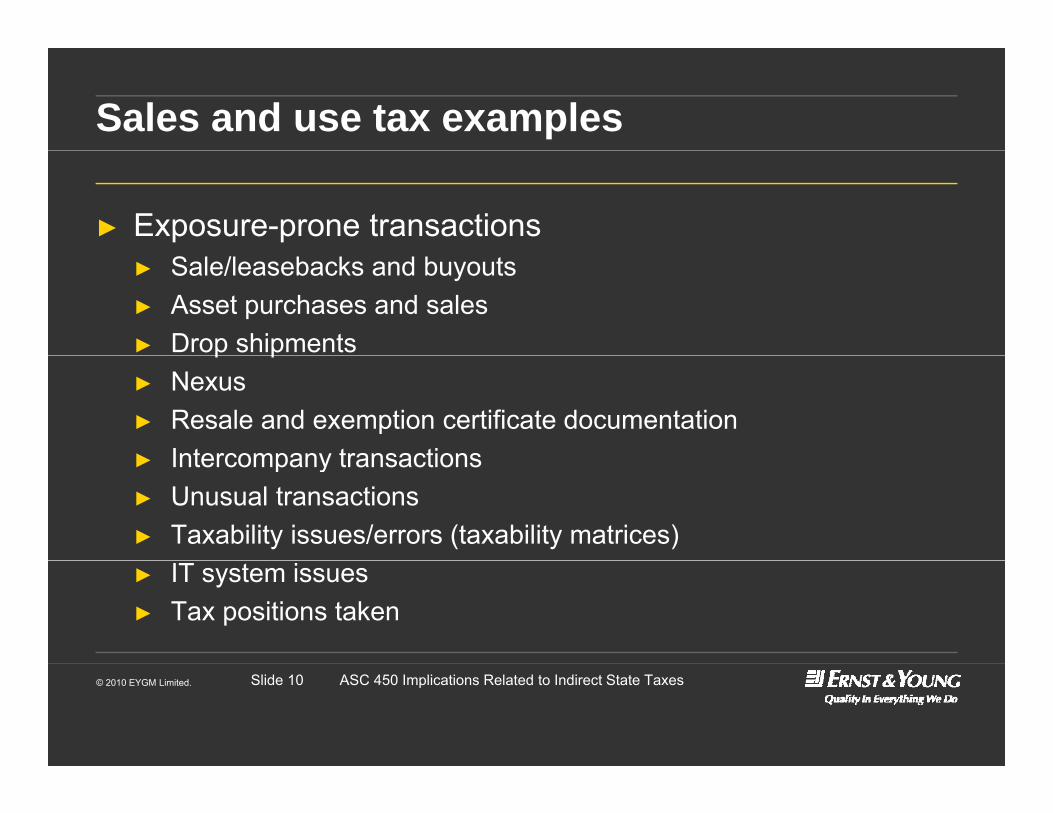

► Exposure-prone transactions► Sale/leasebacks and buyouts► Asset purchases and sales► Drop shipmentsp p► Nexus► Resale and exemption certificate documentation► Intercompany transactions► Intercompany transactions► Unusual transactions► Taxability issues/errors (taxability matrices)► IT system issues ► Tax positions taken

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 10

VAT examples

► Exposure-prone issues► Failure to register for VAT► VAT liabilities through in-country presence of subsidiary► Paying non-recoverable VAT on goods imported on behalf of y g g p

clients/customers► Improperly classifying goods

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 11

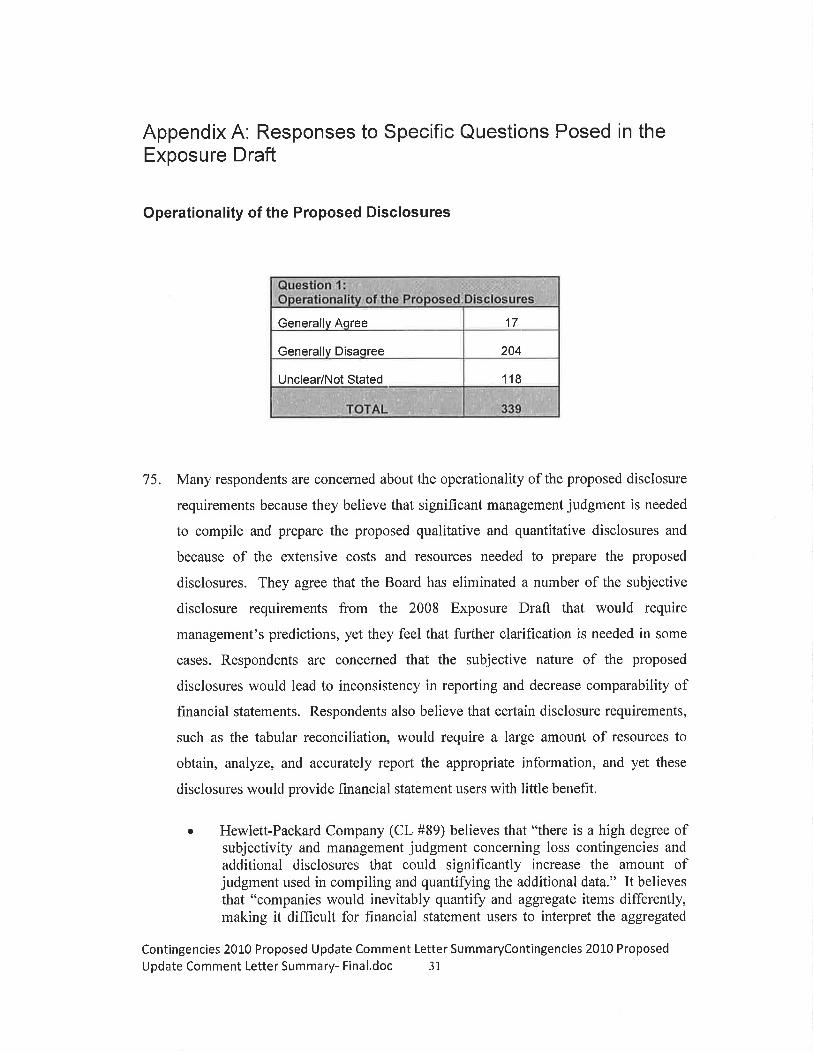

Employment tax/property tax/customs lexamples

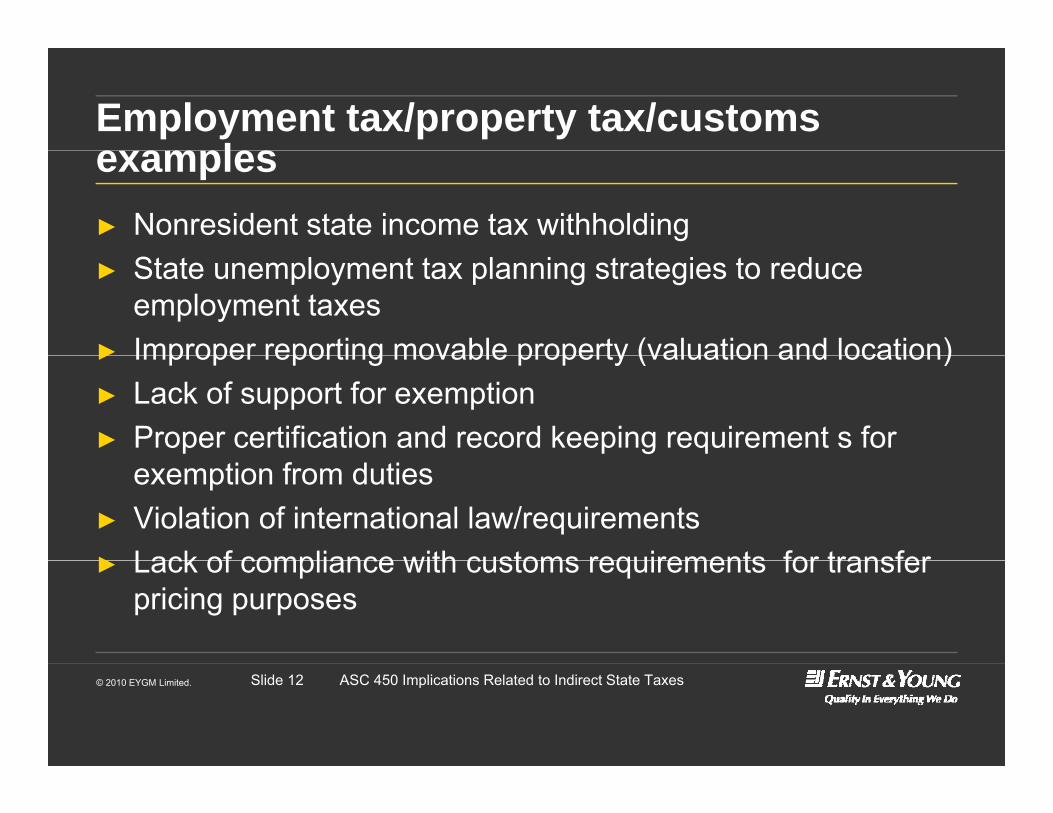

► Nonresident state income tax withholding► State unemployment tax planning strategies to reduce

employment taxes► Improper reporting movable property (valuation and location)► Improper reporting movable property (valuation and location)► Lack of support for exemption► Proper certification and record keeping requirement s for

exemption from duties► Violation of international law/requirements► Lack of compliance with customs requirements for transfer► Lack of compliance with customs requirements for transfer

pricing purposes

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 12

Other examples

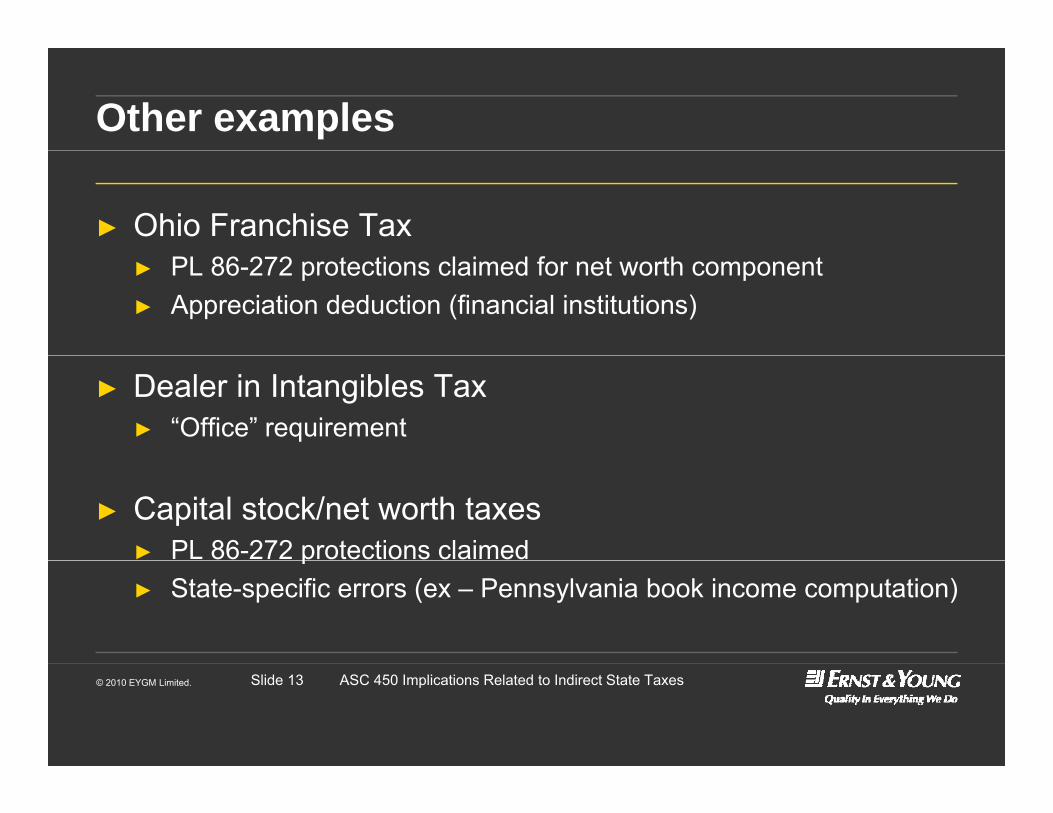

► Ohio Franchise Tax► PL 86-272 protections claimed for net worth component► Appreciation deduction (financial institutions)

► Dealer in Intangibles Tax► “Office” requirement

► Capital stock/net worth taxes► PL 86-272 protections claimedp► State-specific errors (ex – Pennsylvania book income computation)

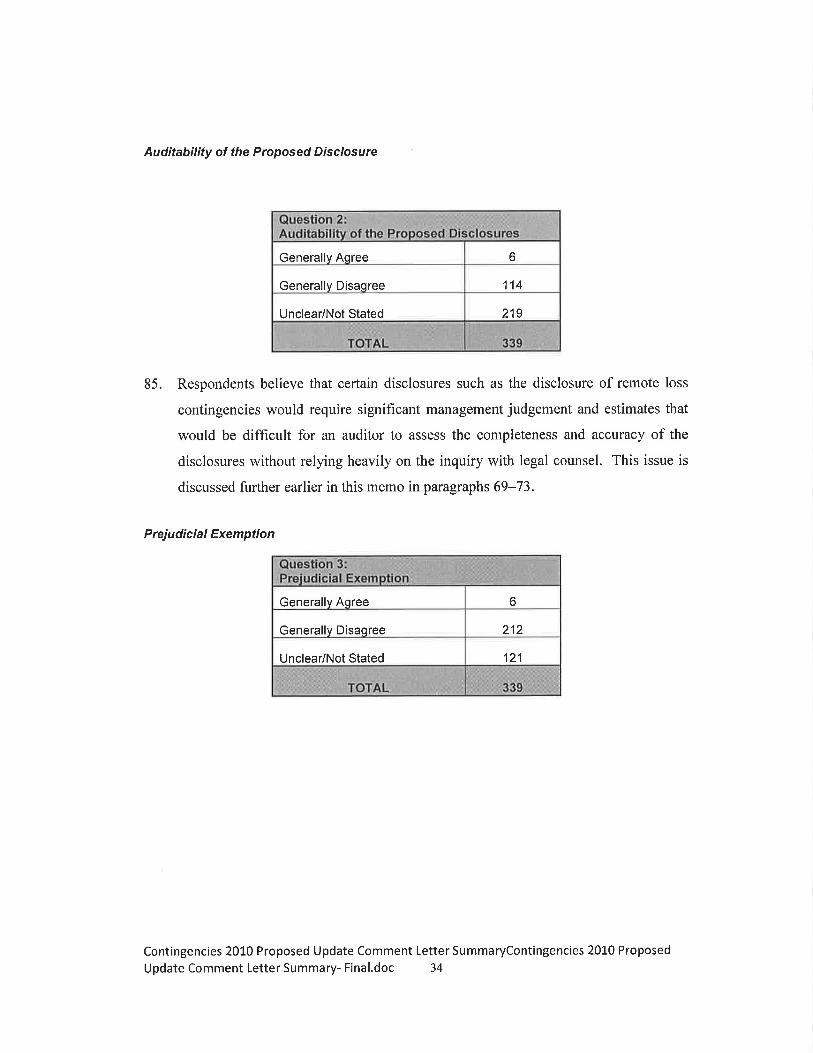

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 13

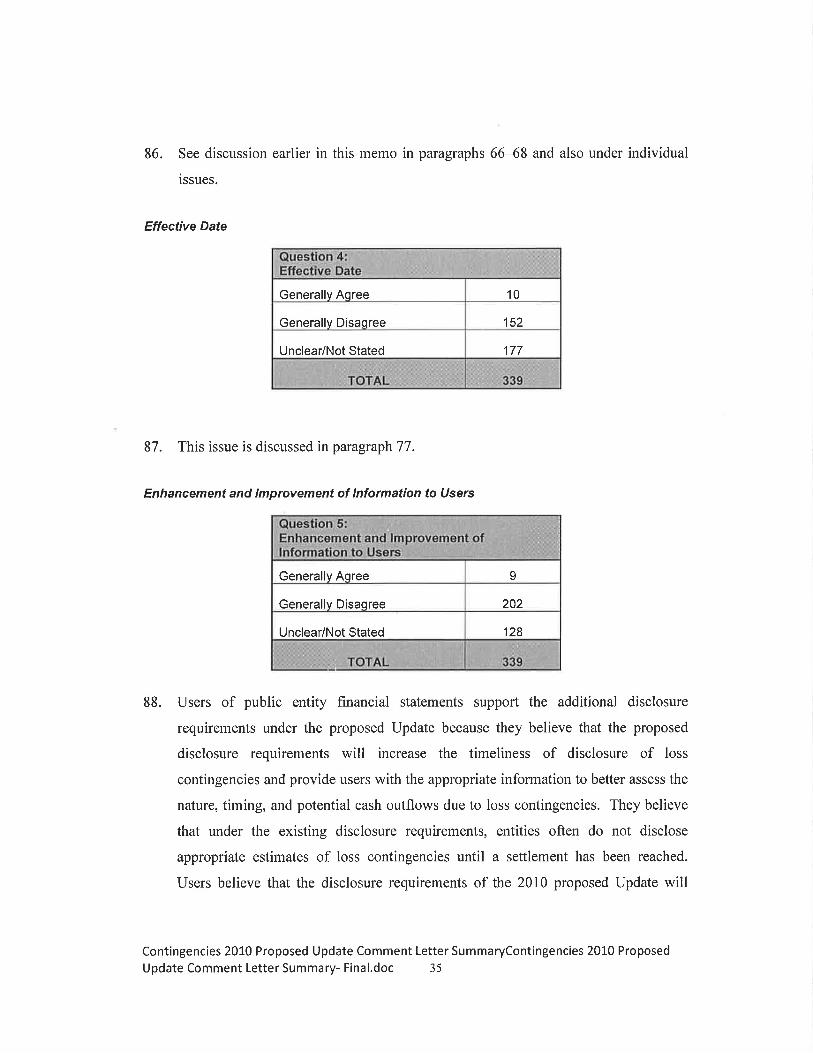

When reserves are appropriate

► The likelihood that the future event or events will confirm th i f th li bilit f b bl tthe incurrence of the liability can range from probable to remote:► Probable – The future event or events are likely to occur y

(accounting firms differ on percentage but generally greater than 65% - 75% – higher level of likelihood than more likely than not contained in FIN 48)

► Reasonably Possible – The chance of the future event or events occurring is more than remote, but less than likely

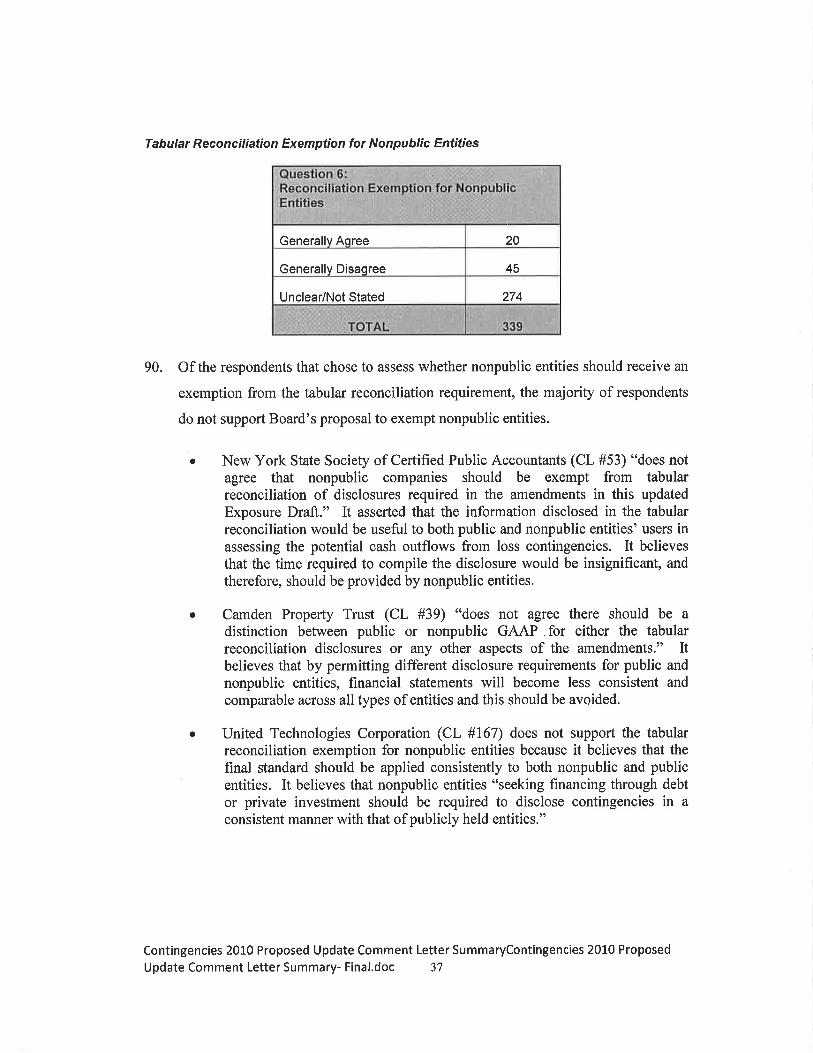

► Remote – The chance of the future event or events occurring is gslight.

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 14

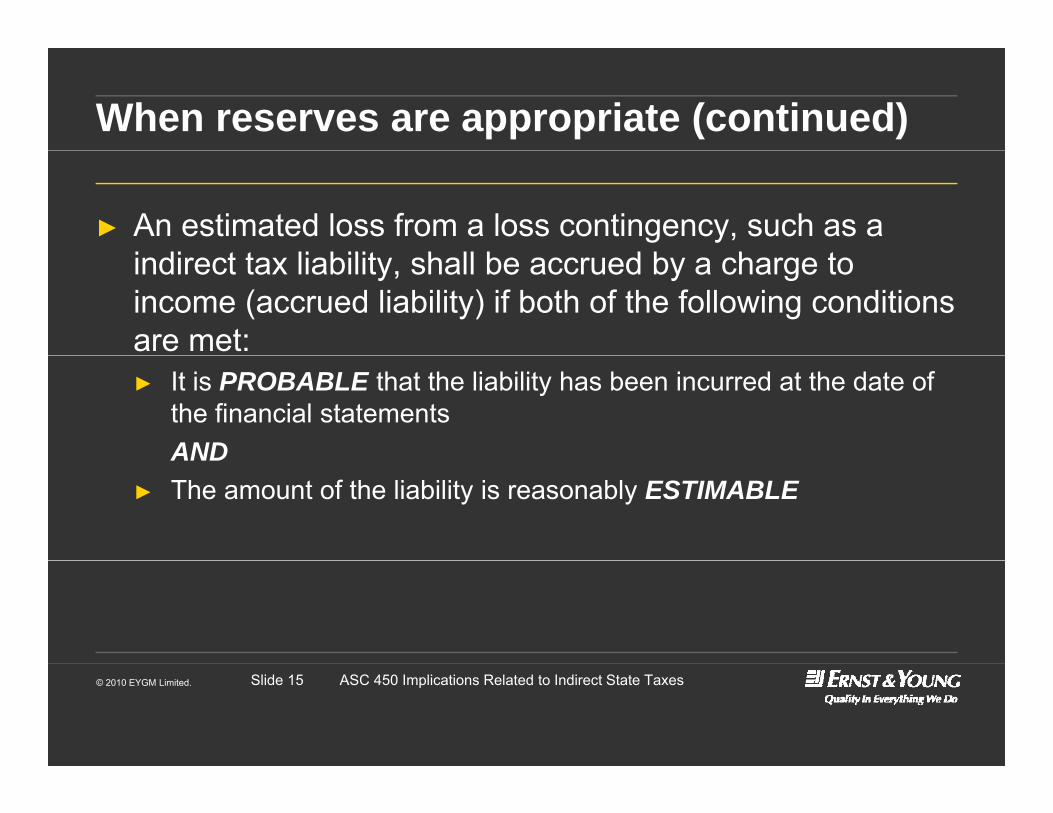

When reserves are appropriate (continued)

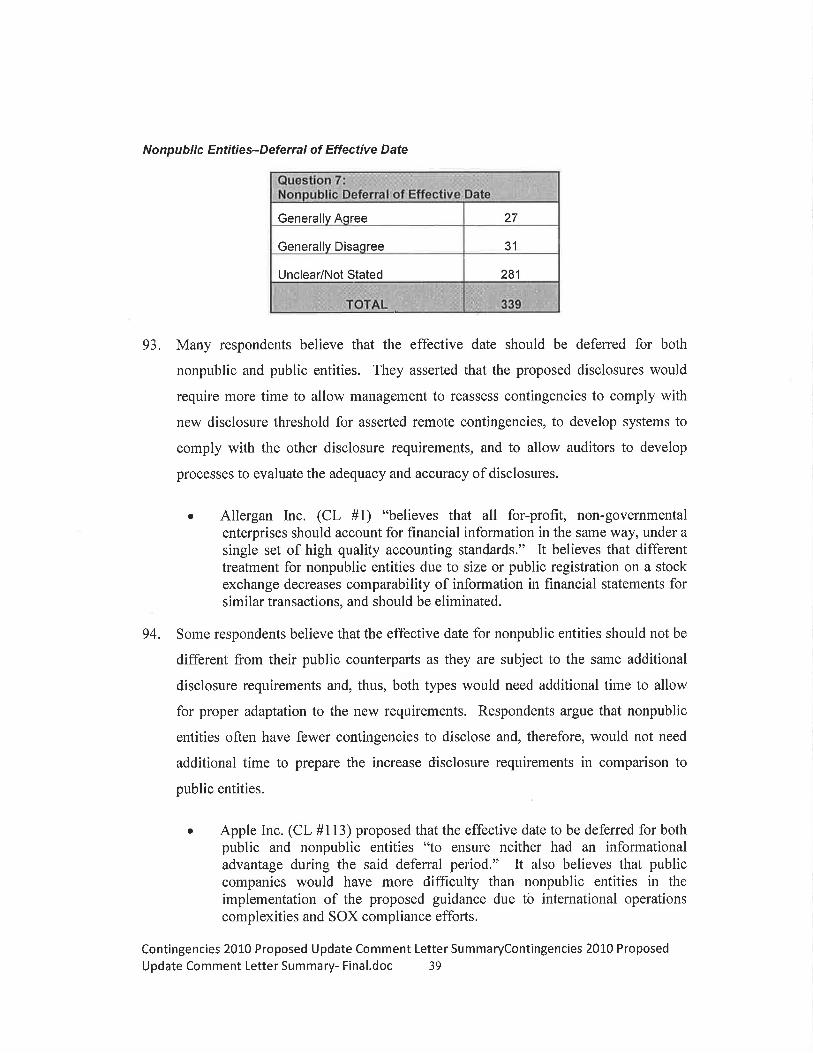

► An estimated loss from a loss contingency, such as a i di t t li bilit h ll b d b h tindirect tax liability, shall be accrued by a charge to income (accrued liability) if both of the following conditions are met:► It is PROBABLE that the liability has been incurred at the date of

the financial statements ANDAND

► The amount of the liability is reasonably ESTIMABLE

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 15

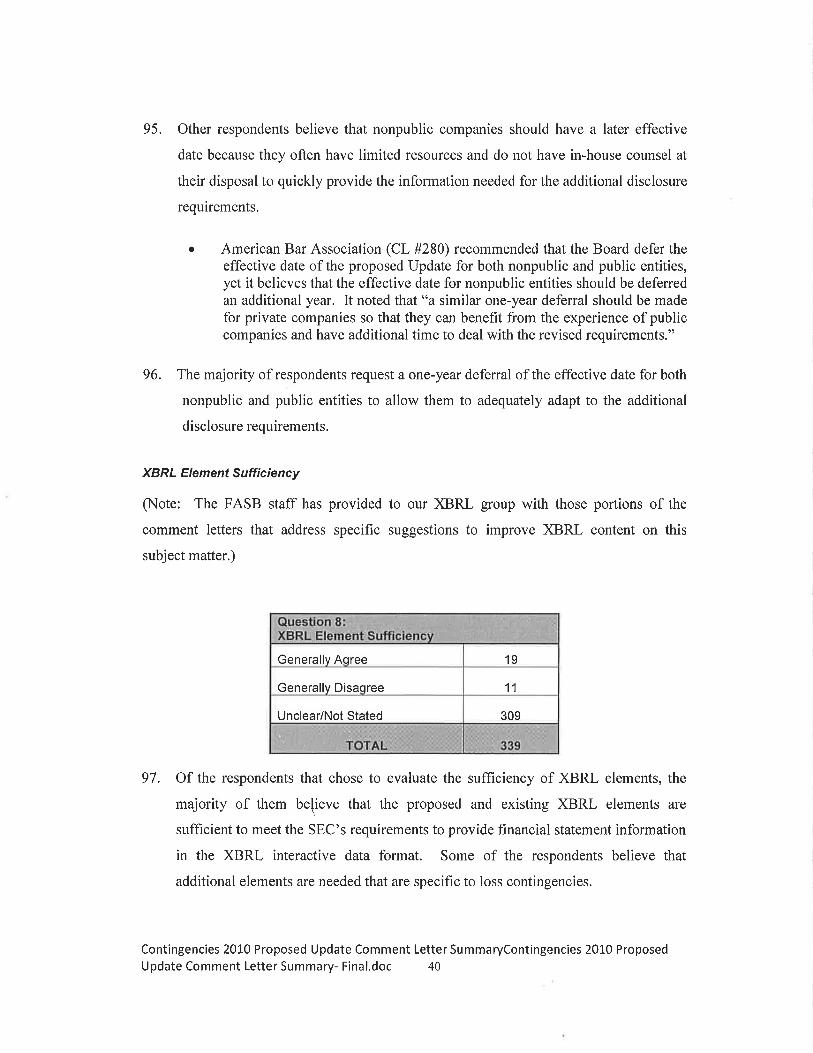

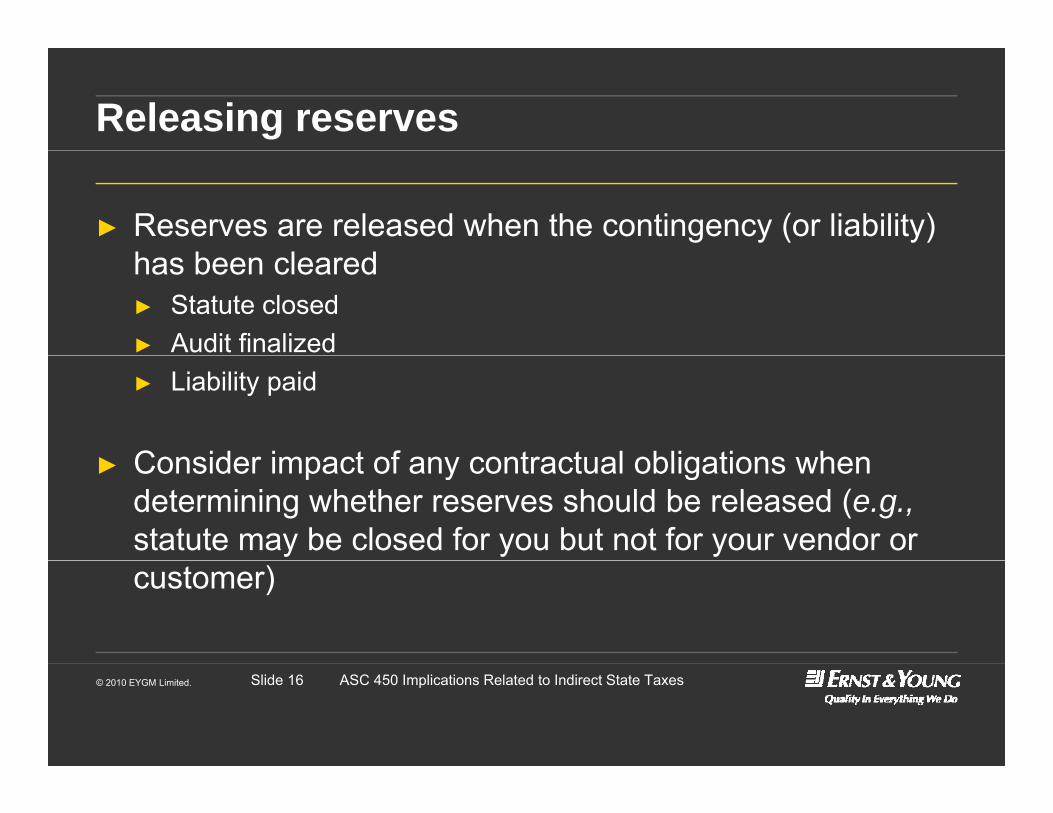

Releasing reserves

► Reserves are released when the contingency (or liability) h b l dhas been cleared► Statute closed► Audit finalized► Liability paid

► Consider impact of any contractual obligations when► Consider impact of any contractual obligations when determining whether reserves should be released (e.g., statute may be closed for you but not for your vendor or customer)

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 16

Releasing reserves (continued)

► Auditor will review the support for the release and d t i i t f ldetermine appropriateness of reserve release

► Reserves may be released based on new information► Current period effect on financial statements► Current period effect on financial statements► Reserves released based on errors in reserves in prior

periods may lead to restatement of prior periods

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 17

Estimation

Estimation: Overview

► Estimation used for audited financial statements are d t i d b th li t d dit d d fi li d b thdetermined by the client and audited and finalized by the audit team

► Tax can assist with the estimation process if provided with all relevant information

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 19

Estimation methodologies

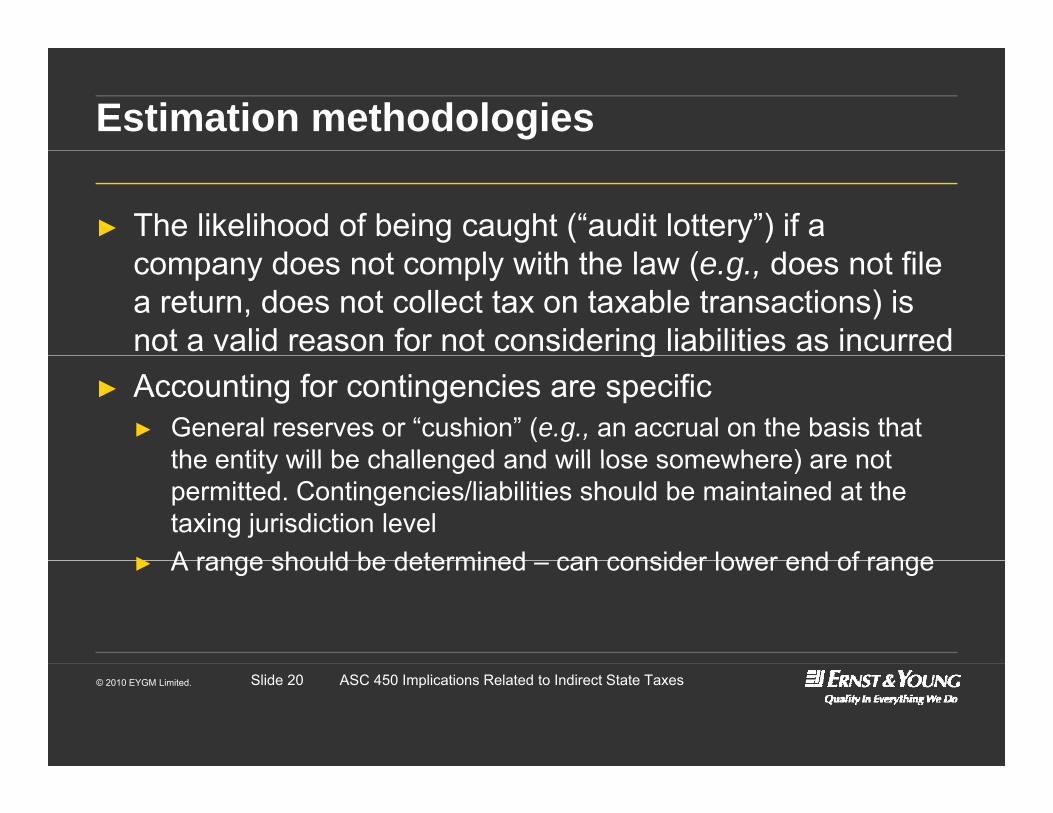

► The likelihood of being caught (“audit lottery”) if a d t l ith th l ( d t filcompany does not comply with the law (e.g., does not file

a return, does not collect tax on taxable transactions) is not a valid reason for not considering liabilities as incurredg

► Accounting for contingencies are specific► General reserves or “cushion” (e.g., an accrual on the basis that

the entity will be challenged and will lose somewhere) are notthe entity will be challenged and will lose somewhere) are not permitted. Contingencies/liabilities should be maintained at the taxing jurisdiction level

► A range should be determined can consider lower end of range► A range should be determined – can consider lower end of range

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 20

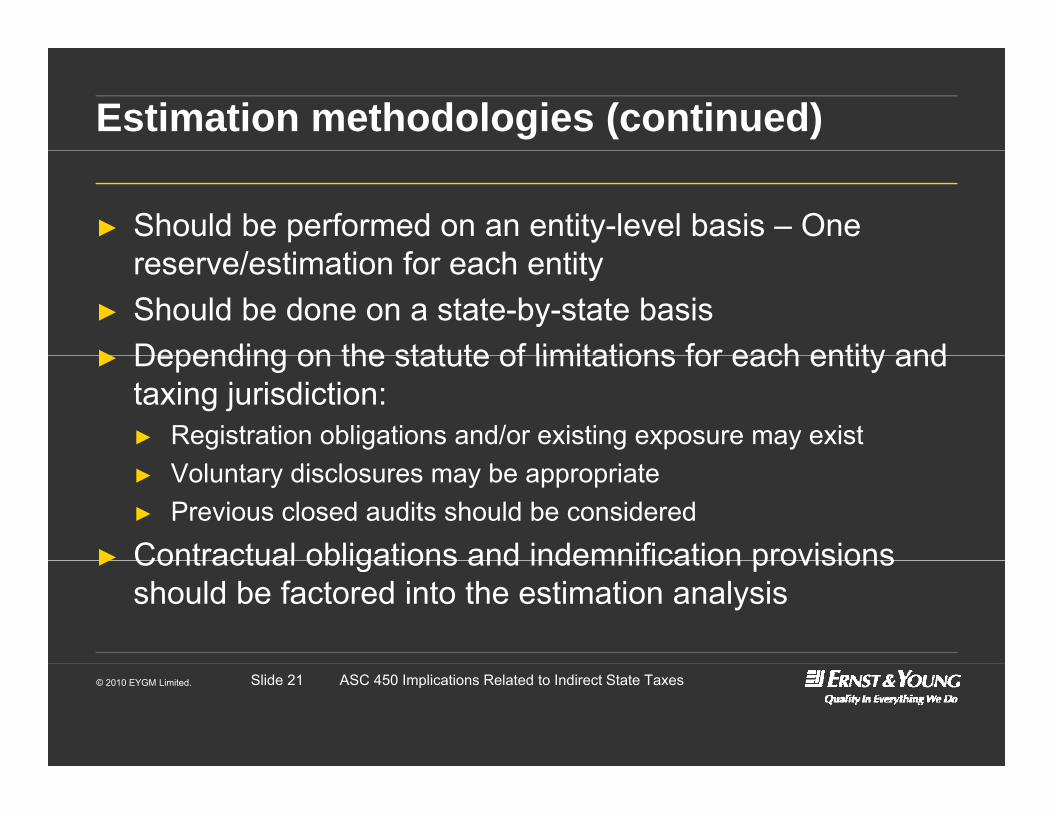

Estimation methodologies (continued)

► Should be performed on an entity-level basis – One / ti ti f h titreserve/estimation for each entity

► Should be done on a state-by-state basis► Depending on the statute of limitations for each entity and► Depending on the statute of limitations for each entity and

taxing jurisdiction:► Registration obligations and/or existing exposure may exist► Voluntary disclosures may be appropriate► Previous closed audits should be considered

► Contractual obligations and indemnification provisions► Contractual obligations and indemnification provisions should be factored into the estimation analysis

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 21

Estimation methodologies (continued)

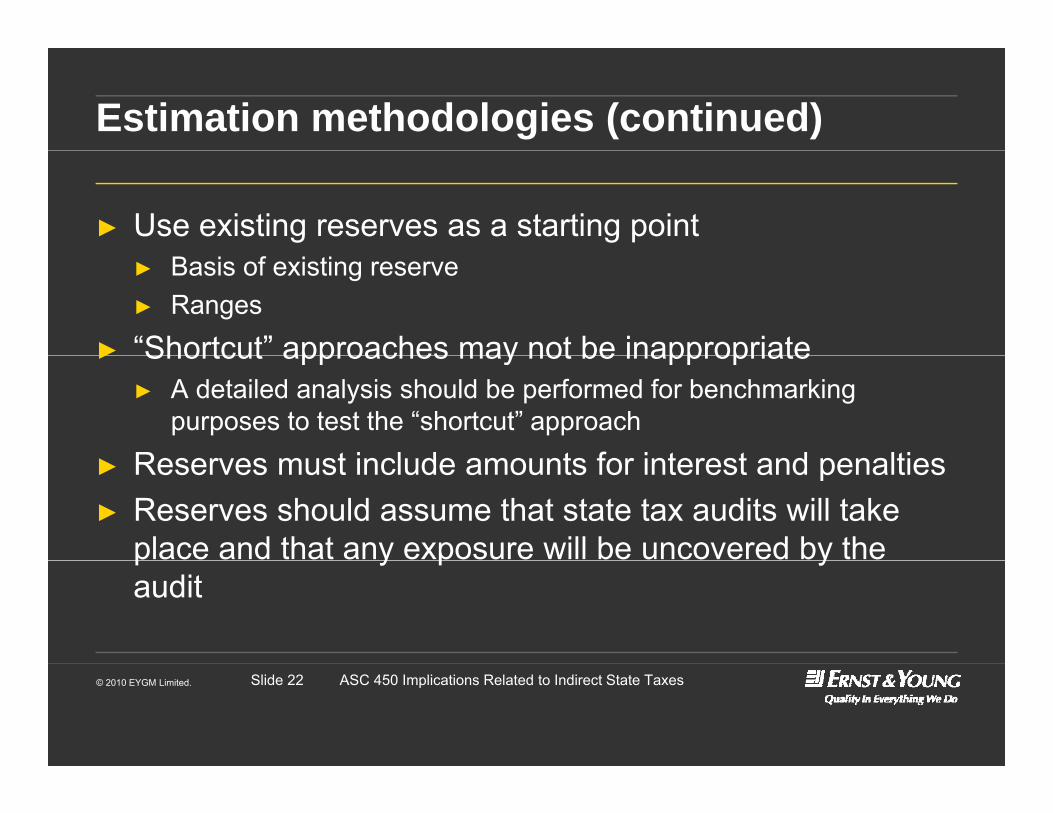

► Use existing reserves as a starting point► Basis of existing reserve► Ranges

► “Shortcut” approaches may not be inappropriate► Shortcut approaches may not be inappropriate► A detailed analysis should be performed for benchmarking

purposes to test the “shortcut” approach

Reser es m st incl de amo nts for interest and penalties► Reserves must include amounts for interest and penalties► Reserves should assume that state tax audits will take

place and that any exposure will be uncovered by the p y p yaudit

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 22

Estimation methodologies (continued)

► Settlement percentage expectation is an acceptable it i h th b i f th ttl t tcriterion; however the basis of the settlement percentage

must be documented and must be reasonable ► This may be more relevant in certain industries and with► This may be more relevant in certain industries and with

certain types of transactions► For example, a federal contractor in California might claim an

exemption for all consumable supplies if most are used at job sitesexemption for all consumable supplies if most are used at job sites for exempt customers

► Contractor knows the auditor will challenge this position, and that some percentage of the supplies will be deemed subject to taxsome percentage of the supplies will be deemed subject to tax

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 23

Estimation methodologies (continued)

► When the amount of a contingency is believed to fall ithi f l th t lik l t h ld bwithin a range of values, the most likely amount should be

reported in the financial statement ► If no single amount within the range is more likely than► If no single amount within the range is more likely than

others, ASC 450 directs that the minimum amount of the range should be accrued and the estimated range of the potential loss should be disclosedpotential loss should be disclosed

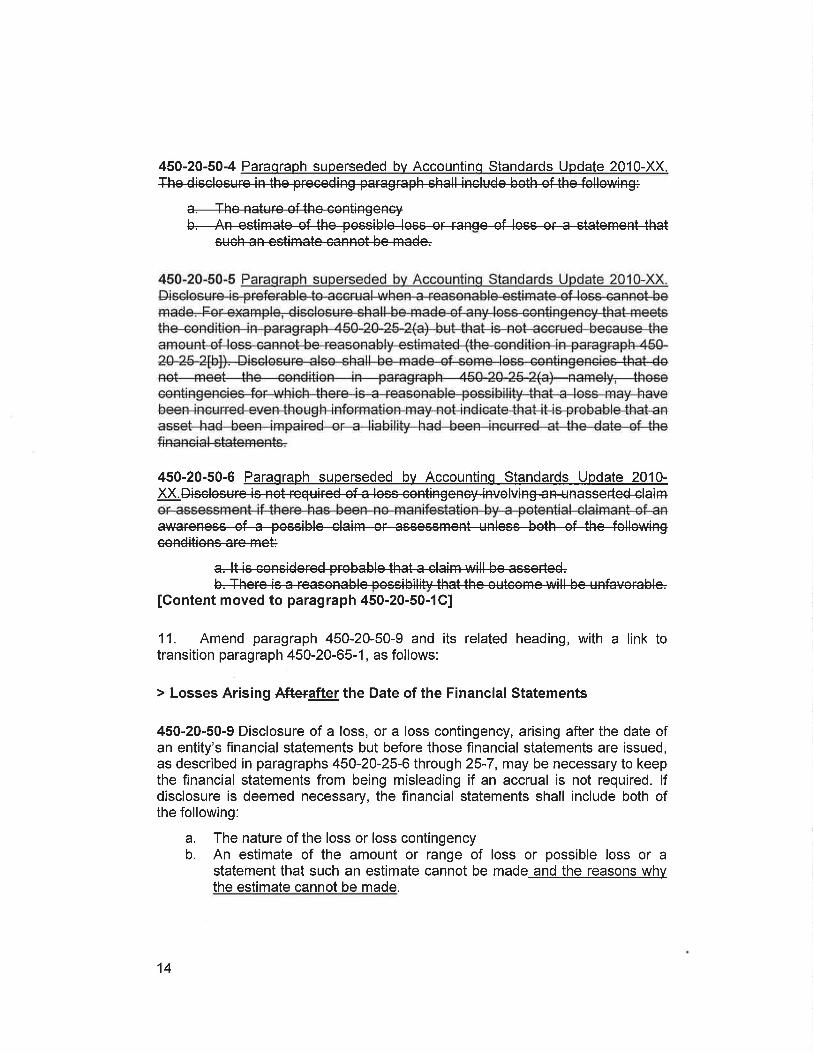

► If no reasonable estimate can be made, ASC 450 requires disclosure of the nature of the contingency and a g ystatement that the amount can not be reasonably estimated

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 24

Disclosures

ASC 450 disclosures

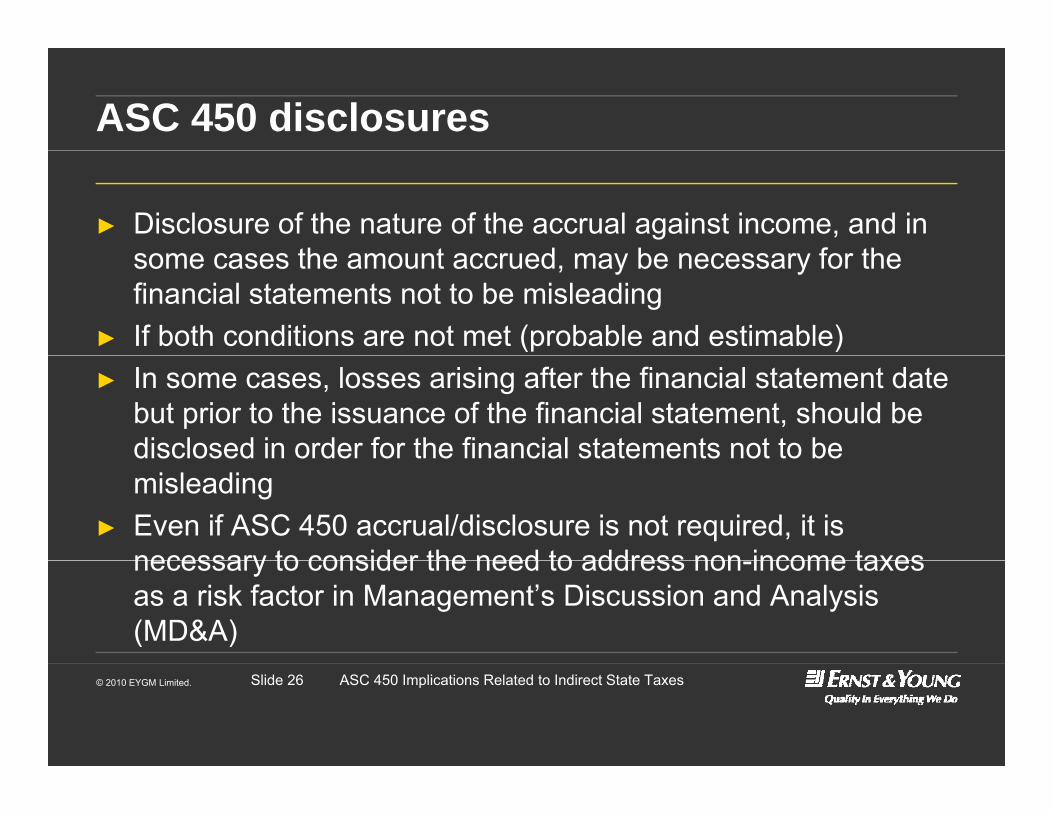

► Disclosure of the nature of the accrual against income, and in th t d b f thsome cases the amount accrued, may be necessary for the

financial statements not to be misleading► If both conditions are not met (probable and estimable) ► In some cases, losses arising after the financial statement date

but prior to the issuance of the financial statement, should be disclosed in order for the financial statements not to bedisclosed in order for the financial statements not to be misleading

► Even if ASC 450 accrual/disclosure is not required, it is necessary to consider the need to address non income taxesnecessary to consider the need to address non-income taxes as a risk factor in Management’s Discussion and Analysis (MD&A)

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 26

ASC 450 disclosures example

► Company is challenging a Washington B&O tax assessment► In preparation for trial, it determines that, based on recent decisions

involving one aspect of the assessment, it is probable that it will have to pay an additional $3 million A th t f th liti ti i l t i► Another aspect of the litigation is less certain

► Depending on the interpretation by the court, the company may be assessed an additional $5 million

U d ASC 450 th t th $3 illi (if► Under ASC 450, the company must accrue the $3 million (if this constitutes a reasonable estimate of the loss)

► The company also must disclose the additional exposure if p y pthere is a reasonable possibility that the additional taxes will be assessed

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 27

ASC 450 Exposure Draft

Summary

► ASC 450 requires disclosure or recognition of certain i di t t li bilitiindirect tax liabilities

► Failure to comply may result in restatement of financials► Proactive involvement is essential► Proactive involvement is essential► Outstanding exposure draft

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 29

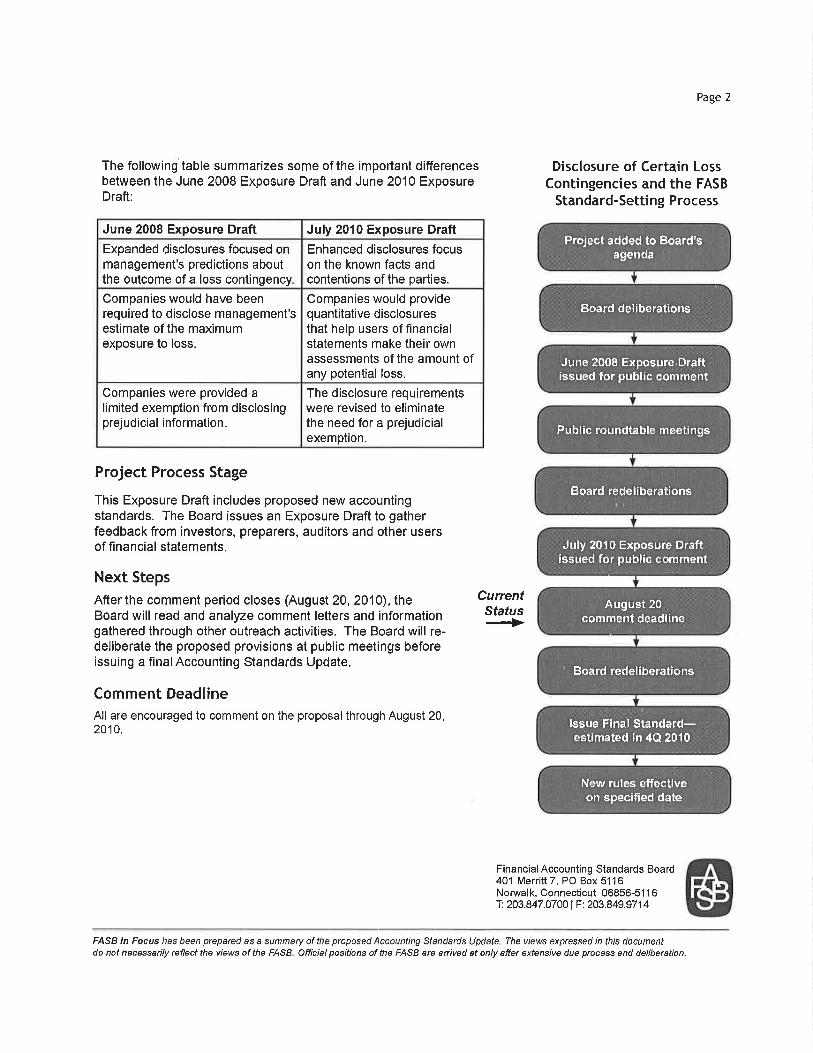

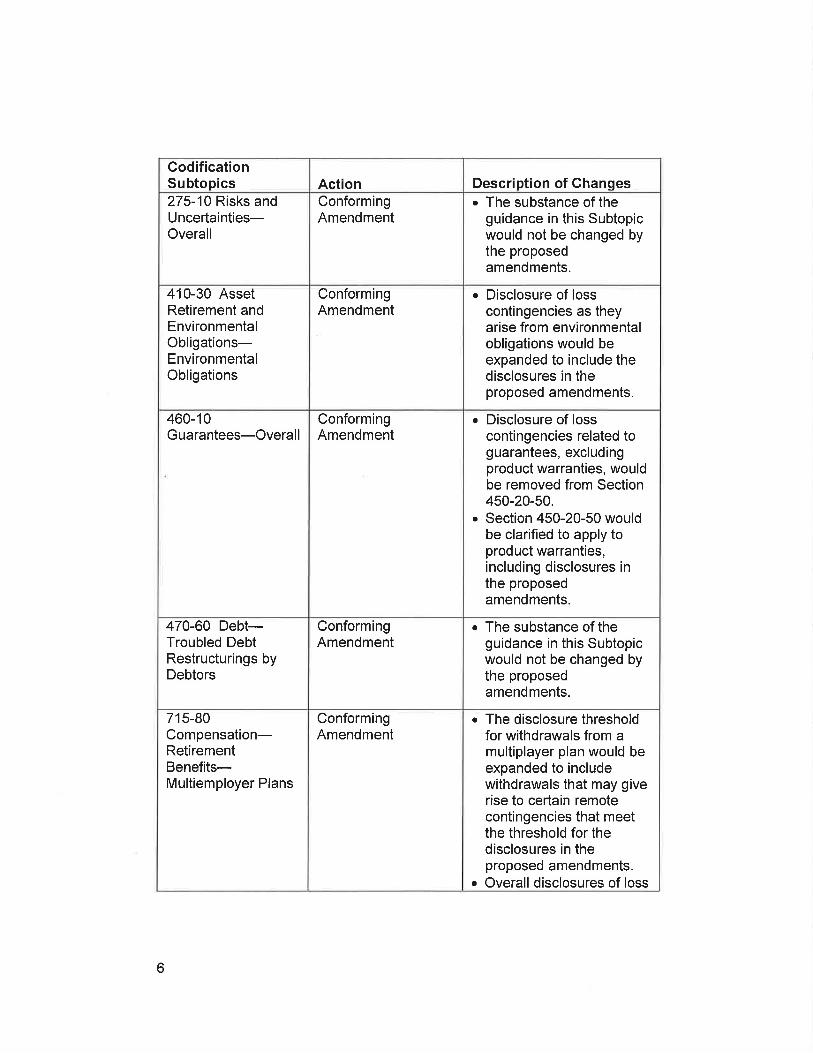

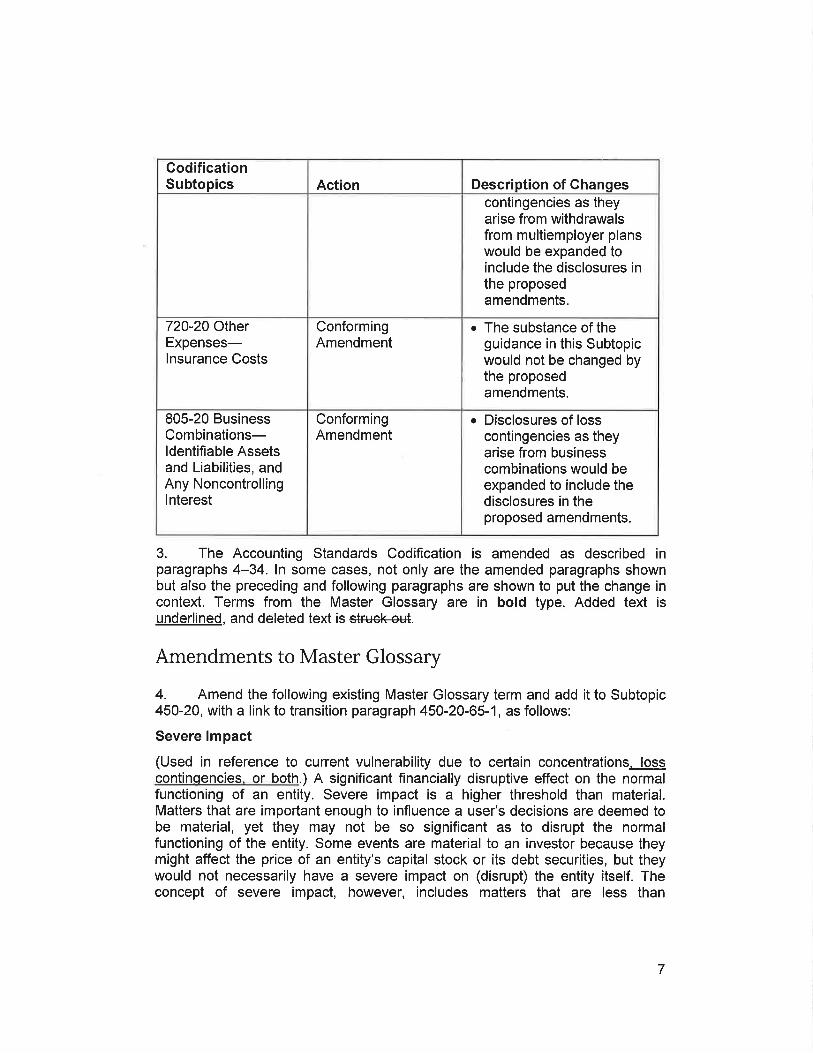

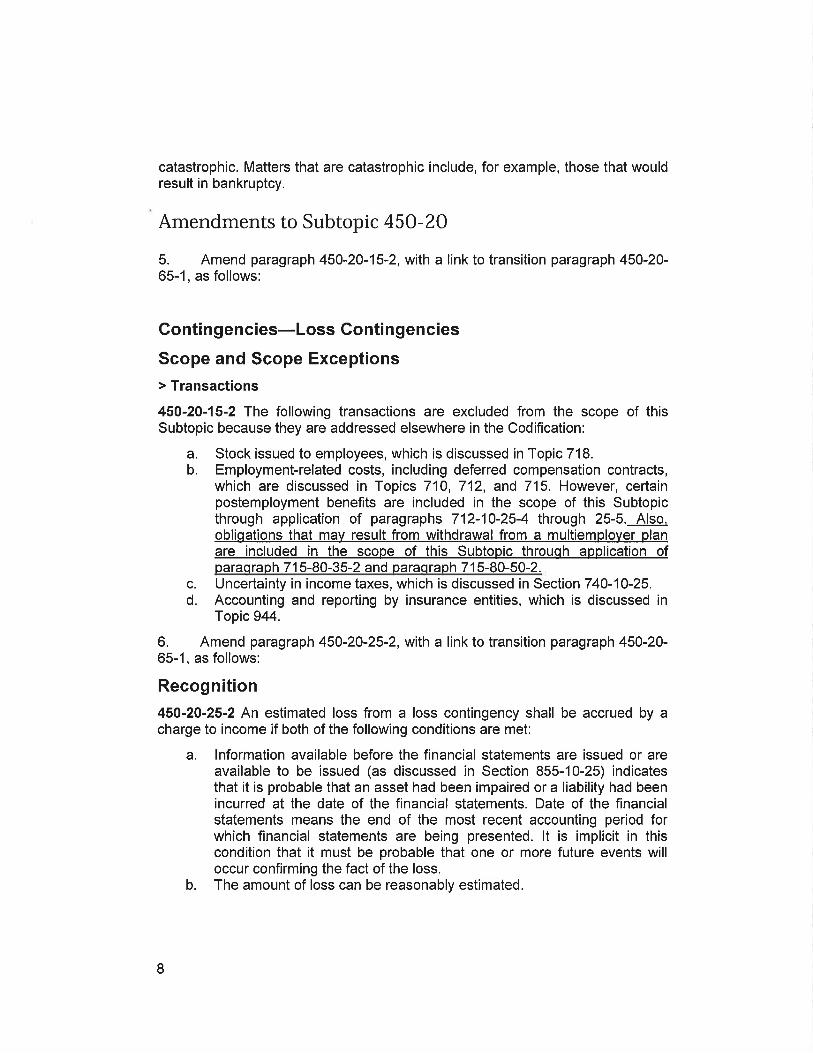

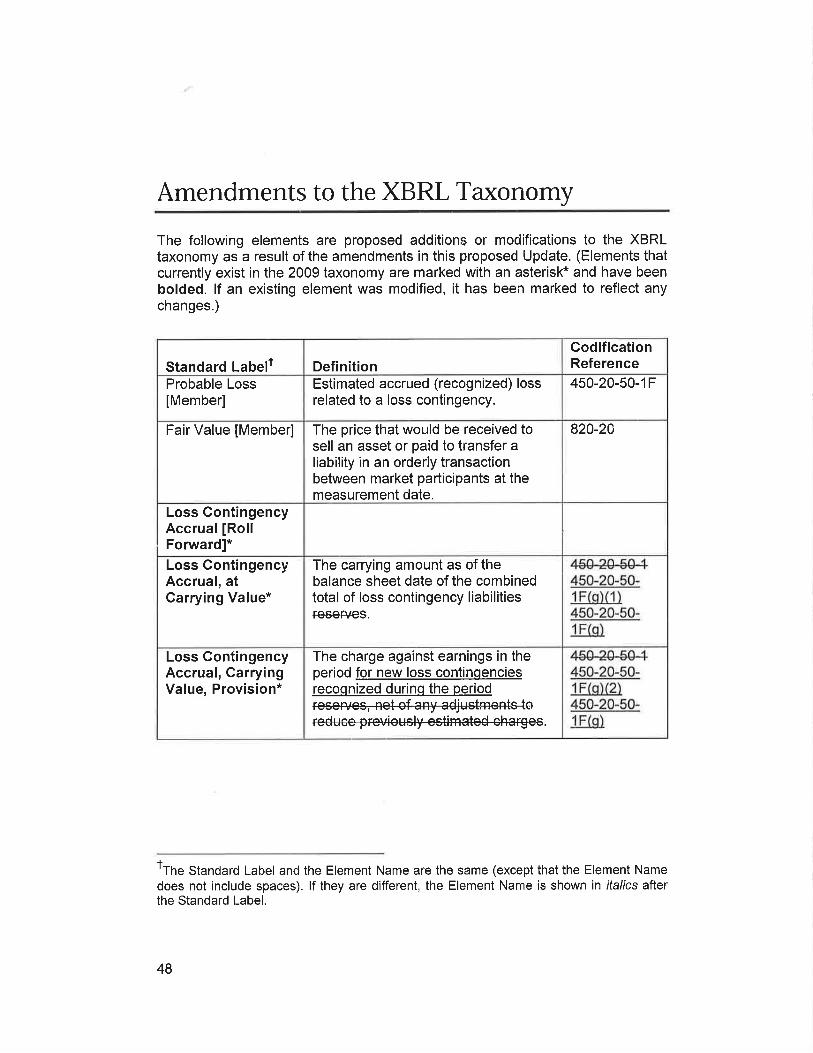

ASC 450 Exposure Draft

► The FASB issued its second exposure draft on loss ti J l 20 2010contingency exposures on July 20, 2010

► Comment period closed September 20, 2010

► Proposed effective dates (deferred on October 27, 2010)► Proposed effective dates (deferred on October 27, 2010)► Public entities – fiscal years ending after December 15, 2010► Non-public entities – first annual period beginning after December

15 201015, 2010

► Scope includes all loss contingencies recorded under ASC 450, including non-income taxes► Proposed disclosure requirements do not change existing

recognition and measurement requirements under ASC 450

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 30

ASC 450 Exposure Draft (continued)

► Expands the population of loss contingencies required to b di l d d d t t l ti ibe disclosed – expanded to remote loss contingencies that could have a “severe impact”

► Does not consider possibility of recoveries from insurance► Does not consider possibility of recoveries from insurance or other indemnification agreements

► Requires disclosure of specific qualitative and quantitative finformation

► Requires a tabular reconciliation of recognized loss contingencies by class of contingencycontingencies by class of contingency

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 31

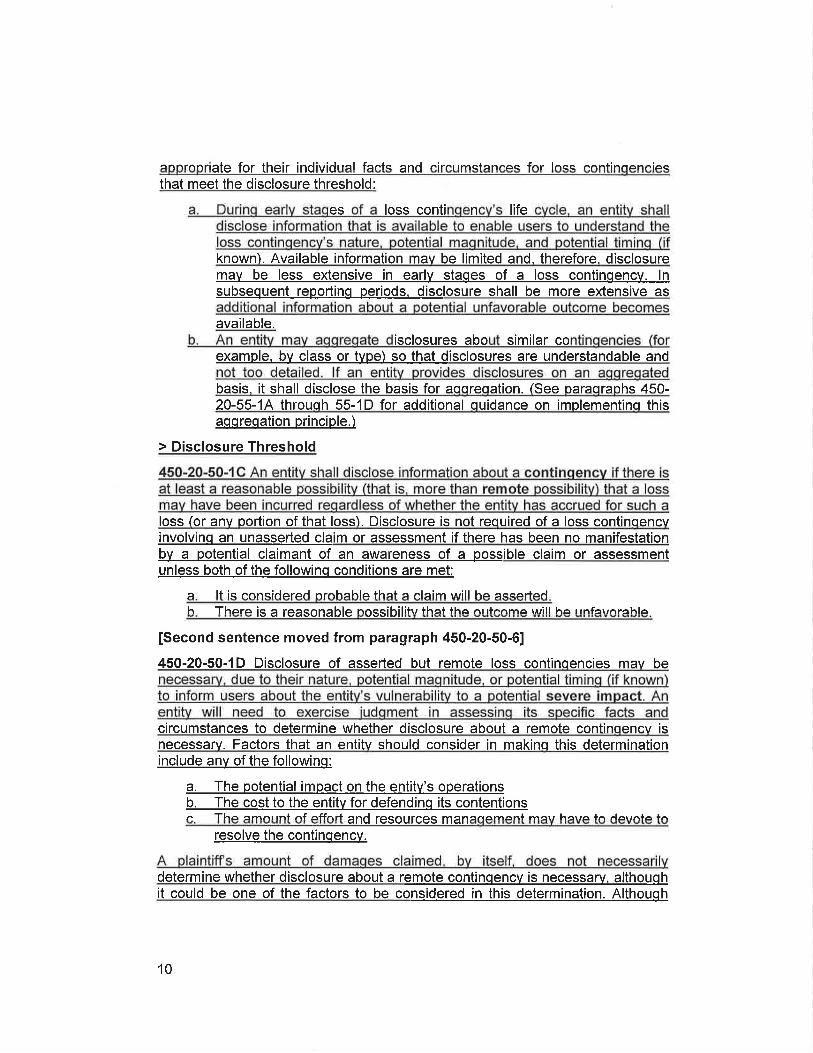

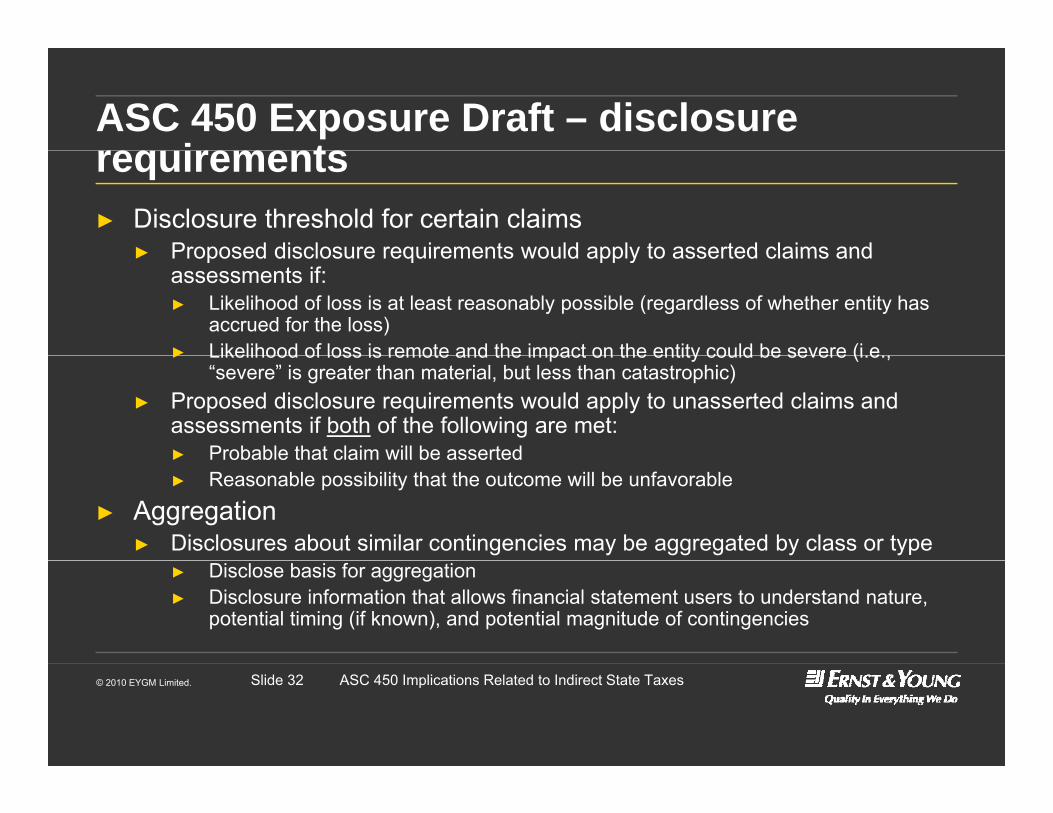

ASC 450 Exposure Draft – disclosure i trequirements

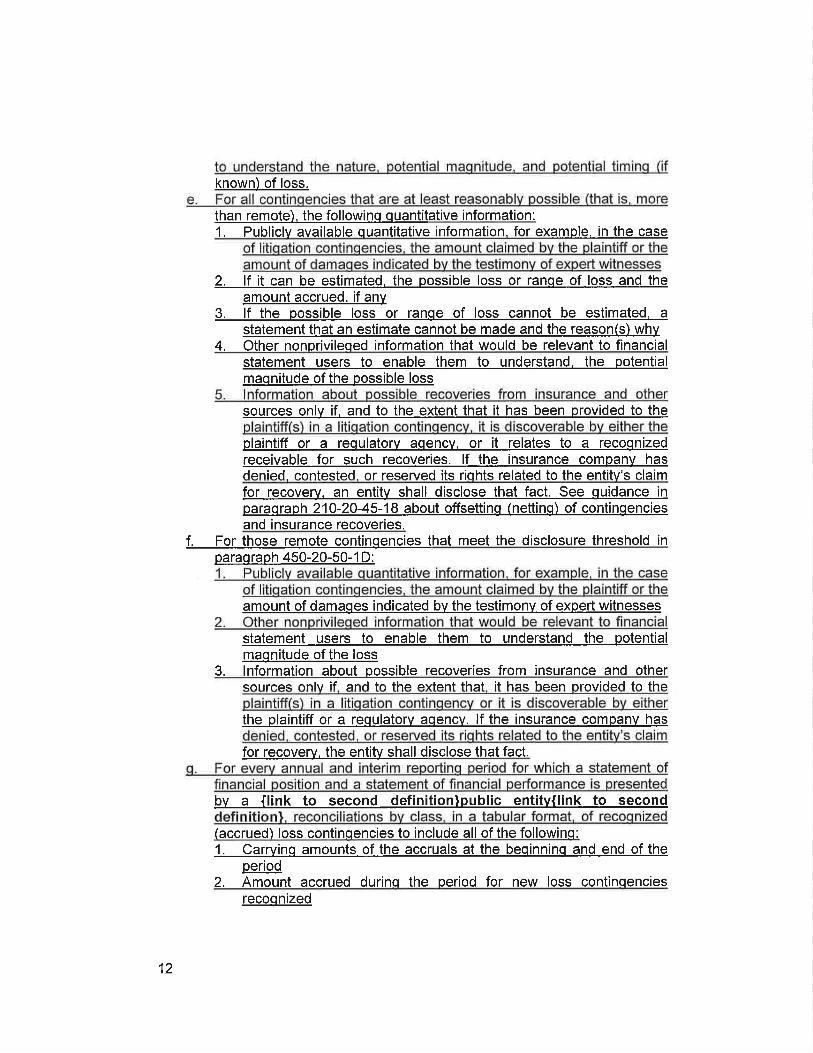

► Disclosure threshold for certain claims► Proposed disclosure requirements would apply to asserted claims and► Proposed disclosure requirements would apply to asserted claims and

assessments if:► Likelihood of loss is at least reasonably possible (regardless of whether entity has

accrued for the loss)► Likelihood of loss is remote and the impact on the entity could be severe (i e► Likelihood of loss is remote and the impact on the entity could be severe (i.e.,

“severe” is greater than material, but less than catastrophic)► Proposed disclosure requirements would apply to unasserted claims and

assessments if both of the following are met:► Probable that claim will be asserted► Probable that claim will be asserted► Reasonable possibility that the outcome will be unfavorable

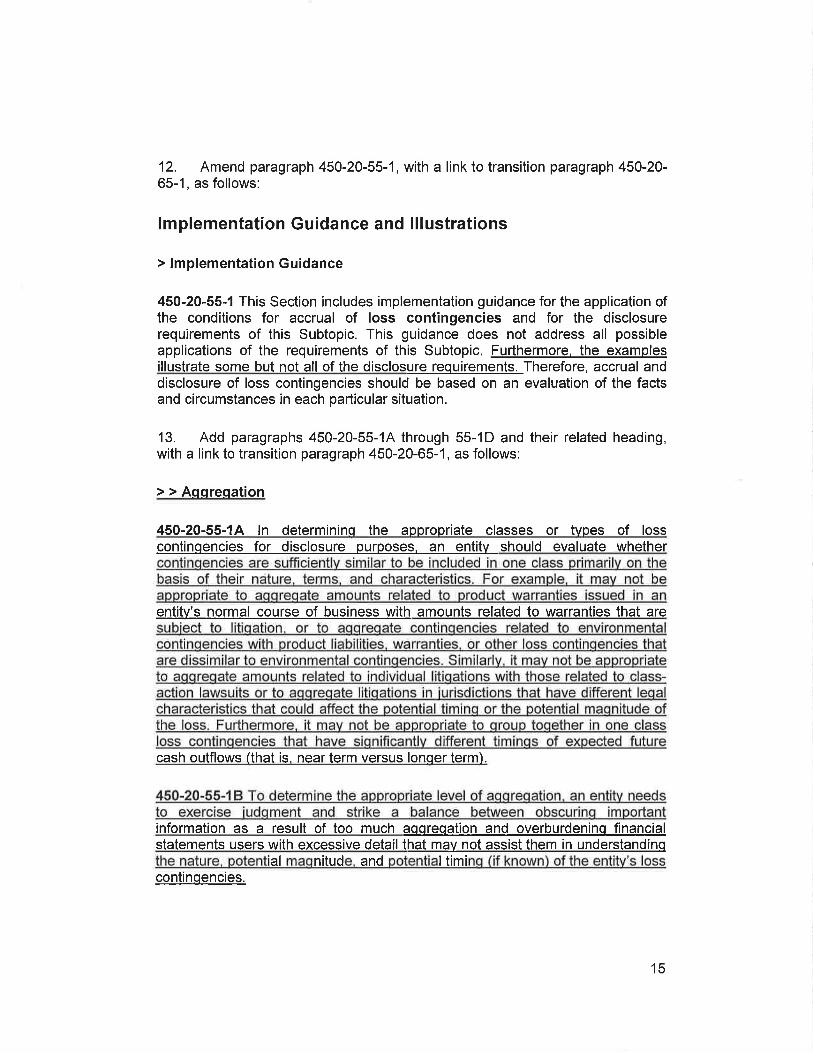

► Aggregation► Disclosures about similar contingencies may be aggregated by class or type

► Disclose basis for aggregation► Disclosure information that allows financial statement users to understand nature,

potential timing (if known), and potential magnitude of contingencies

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 32

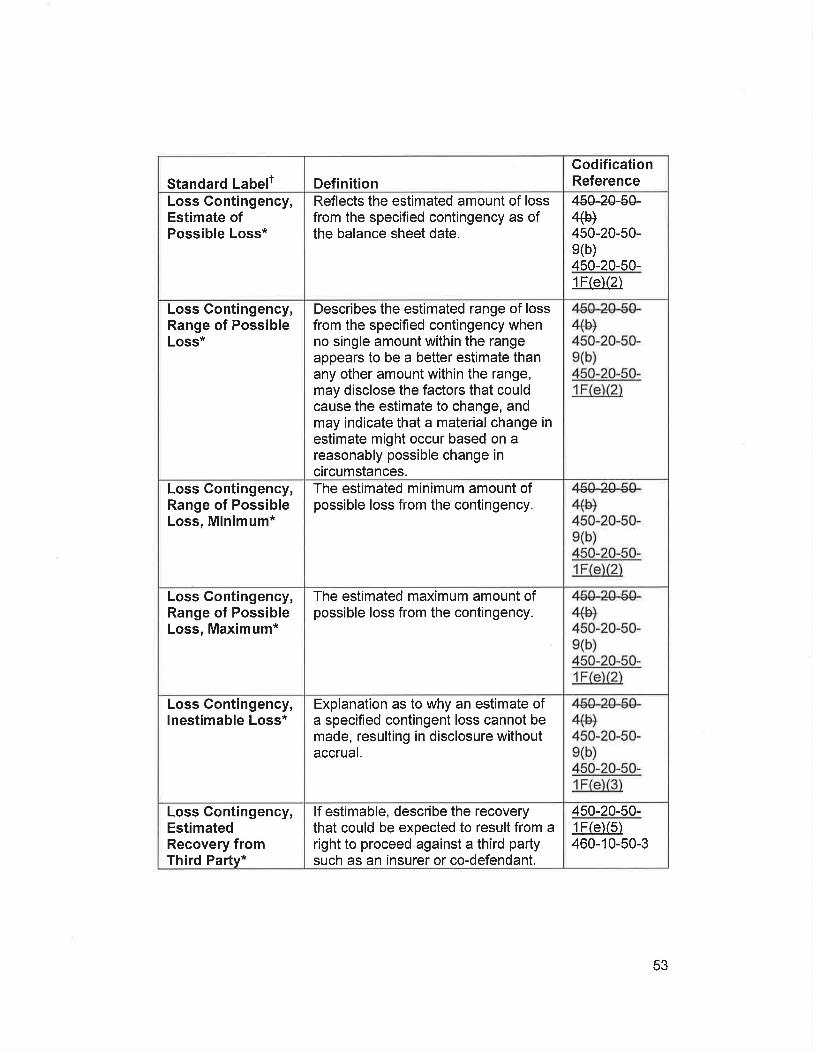

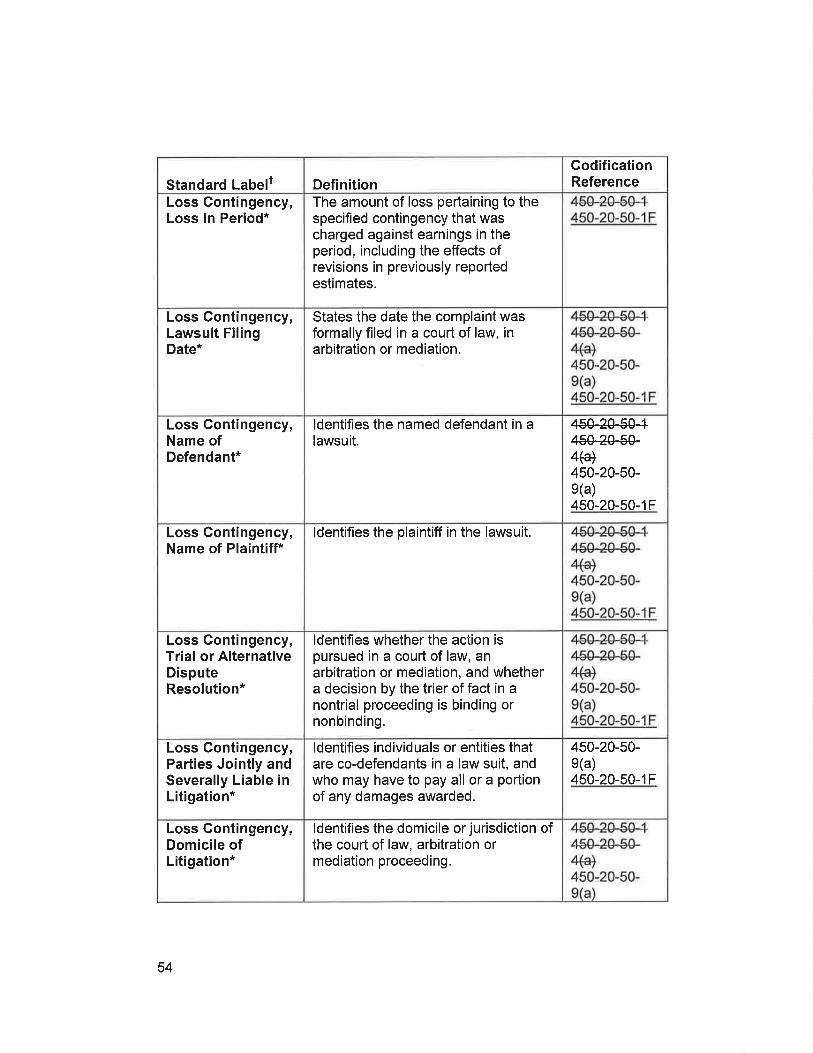

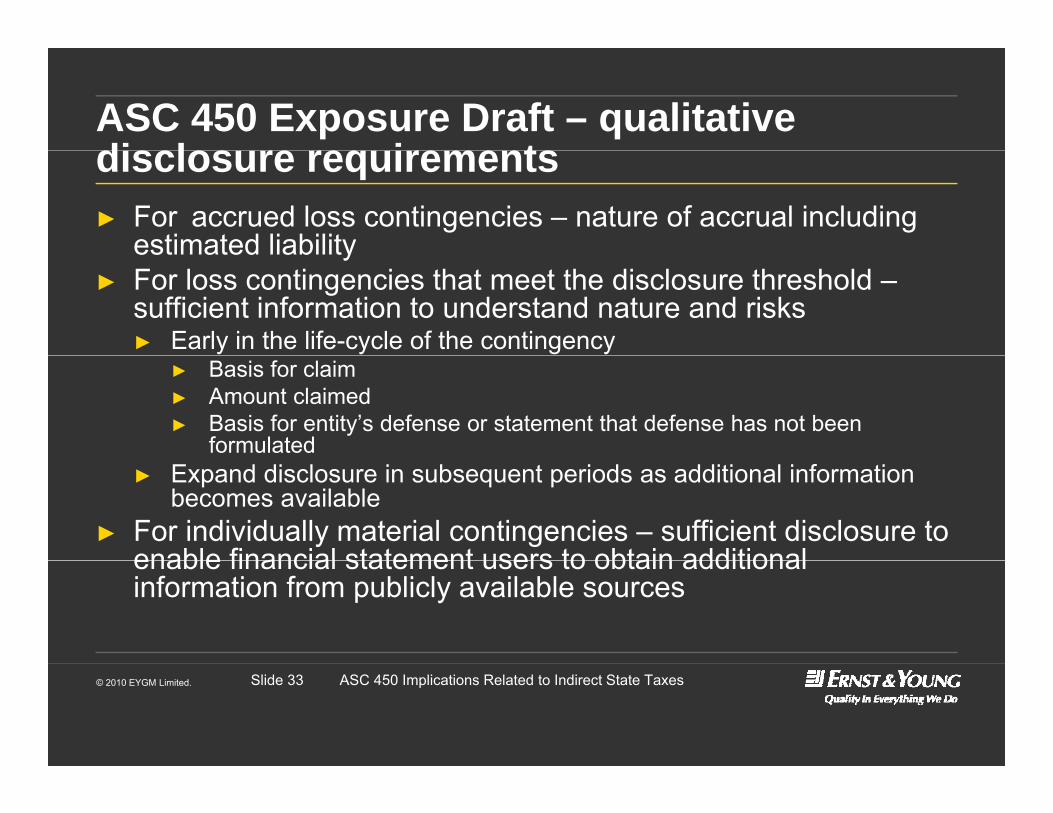

ASC 450 Exposure Draft – qualitative di l i tdisclosure requirements► For accrued loss contingencies – nature of accrual including

estimated liabilityestimated liability► For loss contingencies that meet the disclosure threshold –

sufficient information to understand nature and risks► Early in the life-cycle of the contingency

► Basis for claim► Amount claimed► Basis for entity’s defense or statement that defense has not been

formulated► Expand disclosure in subsequent periods as additional information

becomes available► For individually material contingencies – sufficient disclosure to

enable financial statement users to obtain additionalenable financial statement users to obtain additional information from publicly available sources

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 33

ASC 450 Exposure Draft – qualitative di l i t ( ti d)disclosure requirements (continued)► Remote loss contingencies that meet the disclosure

thresholdthreshold► Publicly available quantitative information► Other nonprivileged information to enable financial statement

users to understand potential magnitude of possible lossusers to understand potential magnitude of possible loss► Information about certain potential recoveries

► Reasonably possible contingencies (i.e., more than t )remote)

► All of the above► Estimate of possible loss or range of loss and amount accrued if

(if ti t t b d t t t th t ti t tany (if estimate cannot be made, a statement that estimate cannot be made and reasons why)

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 34

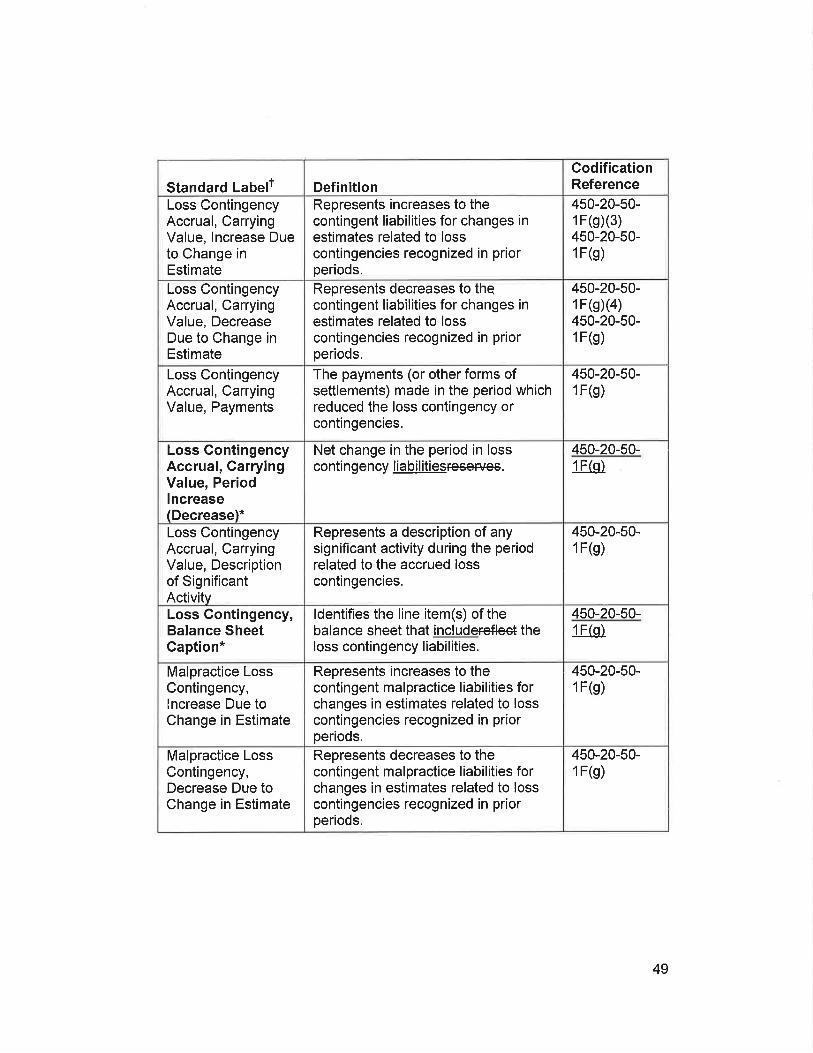

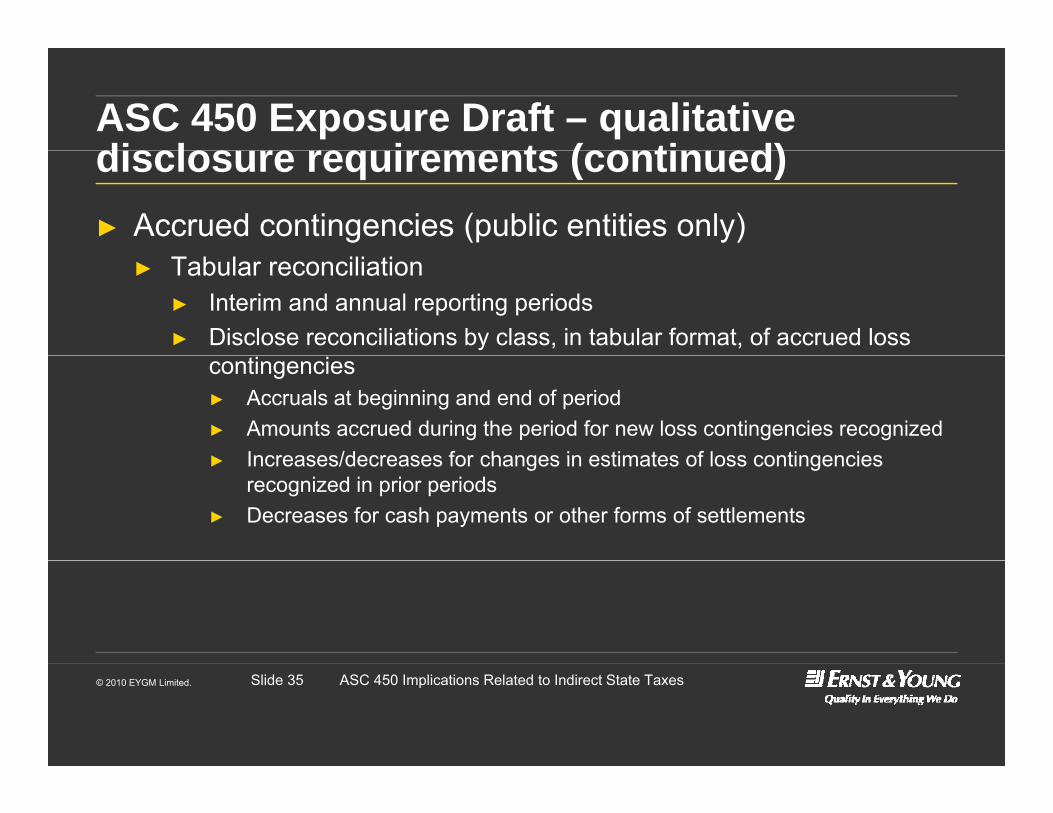

ASC 450 Exposure Draft – qualitative di l i t ( ti d)disclosure requirements (continued)► Accrued contingencies (public entities only)

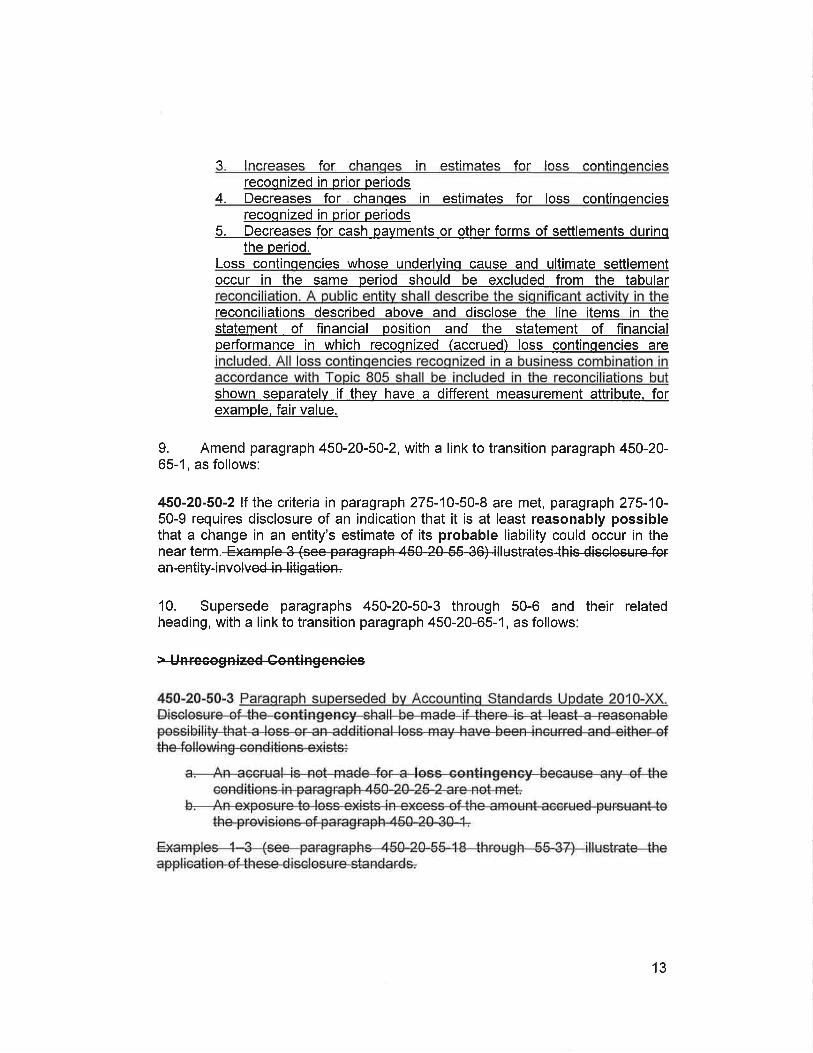

► Tabular reconciliation► Interim and annual reporting periods► Disclose reconciliations by class, in tabular format, of accrued loss

contingencies► Accruals at beginning and end of period► Amounts accrued during the period for new loss contingencies recognized► Increases/decreases for changes in estimates of loss contingencies► Increases/decreases for changes in estimates of loss contingencies

recognized in prior periods► Decreases for cash payments or other forms of settlements

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 35

Questions

© 2010 EYGM Limited. ASC 450 Implications Related to Indirect State TaxesSlide 36