Accounting for debts

30

THE SYSTEM OF ACCOUNTING ACCOUNTING FOR DEBT Volume III WRITTEN BY: SYED AQEEL RAZA MASTER OF COMMERCE & POLITICS

-

Upload

aqeel-raza -

Category

Education

-

view

44 -

download

0

Transcript of Accounting for debts

THE SYSTEM OF ACCOUNTING

ACCOUNTING FOR DEBTVolume III

WRITTEN BY:SYED AQEEL RAZAMASTER OF COMMERCE & POLITICS

ACCOUNTING FOR DEBIT

The debt is an amount of money which is borrowed by one party from another party under the condition to pay back at a later date with or without interest and it may be borrowed by individual, bank for personal loan like auto loan, house loan, credit card loan etc. and for business loan on mark up, debt against selling of goods or services with our without interest. It may have mortgage, personal and assets’ guarantee.

Most of the companies are operating them to take loan from financial institution for meeting their financial demands or increasing their volume. This is right that the debt or loan may increase the efficiency of any business in many ways one side as to increase production, to purchase assets; plant and machineries, equipment, raw materials, and to purchase finished goods for trading; to pay the salaries of employee, bills of suppliers and to get the rid of many other financial difficulties in the operation of any business but on the other side may become the cause of financial troubles in future because of paying huge amount in shape of mark-up or interest. The profit is generated against investment involves more investment more profit and less investment less profit and if the investment of his own, the profit is of his own but the investment acquired from other sources, the profit is distributed among others. The result is same means profit earned of that amount of his own but change of growing and loss of his own assets are under questions.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

All debts involve cash and other than trade are considered as loan or some time sundry debtors as the trade involves goods which are given to sellers on credit or cash, the seller is bound to pay debt of goods to the party time to time revolving sales and purchase. The seller who took goods on credit is called trade debtor.

Trade debtor and creditors

A trade debtor is an entity that owes a debt to another entity during the course of business in shape of goods or services. The trade debtor credits the account of the entity that supplied goods or services to him under account payable controlled by trade creditors and the entity who supplied goods and services to the debtor must debit his account under account receivable which is controlled by trade debtor’s account.

Generally, the account of individual party’s receivable is opened in general ledger but in case of various parties, another ledger called subsidiary ledger is created named trade debtors under controlled by account receivable or debtors ‘control account in general ledger account.

The subsidiary ledger is sub book of the particular account involving journals like sales journal, sales return and allowances journal, cash receipt journal and adjustments through journal voucher.

The subsidiary ledger for sale either on cash or credit may be useful to control the variety of units sold under control account sale.

Trade debtors relate to goods or services for doing business.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

The trade debtors are who they purchased goods for doing business and the party from whom the trade debtor purchased goods is called trade creditors. The goods sold on cash to parties doing trade are also considered debtors because the goods are supplied on taking advance against sale come under advance from customers under debtors account.

Then, the trade creditor will have to maintain accounts of the parties to whom the goods sold on credit.

We know that all individual debtor’s account go in the debtor’s ledger and creditor’s account in creditor’s ledger under control general ledger account receivable and account payable or debtors and creditors control account and for making subsidiary ledger of accounts receivable or debtor accounts, we have to maintain journals like sales journal, sales return and allowances journal, cash receipt journal and adjustments through journal vouchers of those transactions that do not belong to journals or come after positing of entries from journals as shown in our volume II Chapter III Ledger Making.

And for this, Accounts payable refers to creditors who deliver goods for business and get payment after sometime. The amount of invoice is journalized as inventory account debit and party’s account credit in ledger account directly or through purchase journal. The purchases in business may be from different persons or firm may require separate account of the separate book of accounts like subsidiary ledger which provide detailed information of each person or firm to accountant. It is controlled in general ledger by Account payable control account as referred to our volume II Chapter III Ledger Making.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

Therefore, debtors are ascertained by accounts receivable and creditors by account payable.

ACCOUNTS RECEIVABLE:

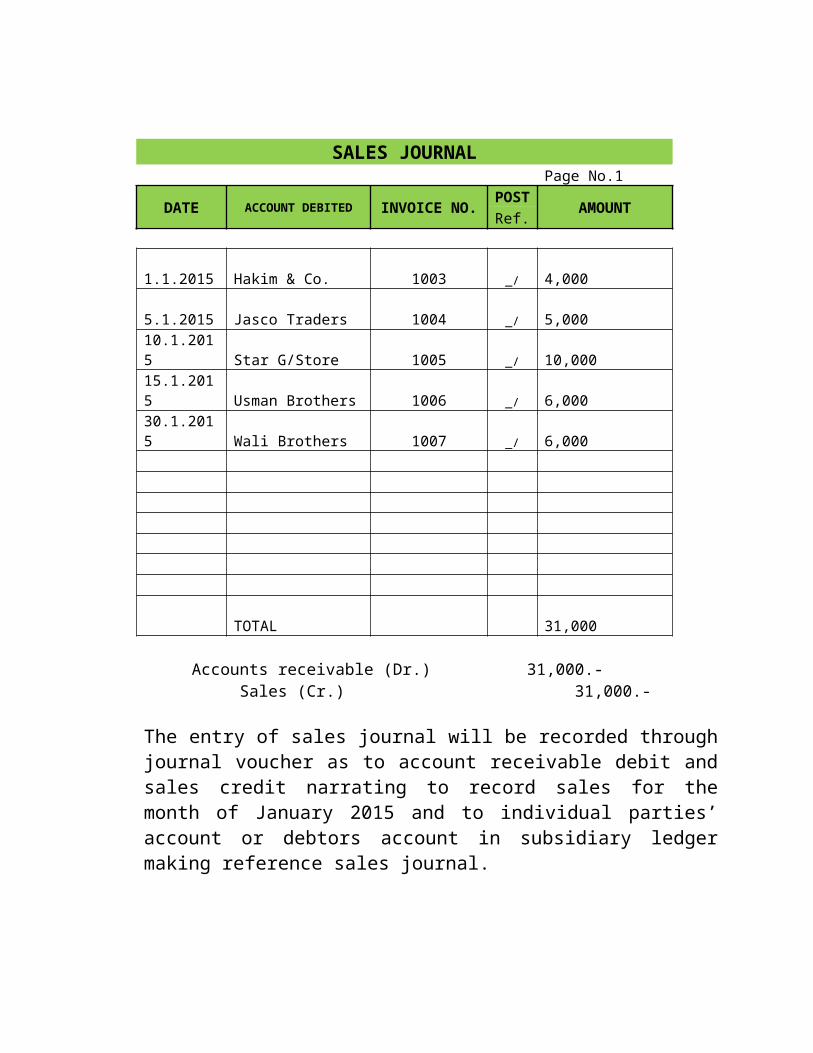

Account receivable means to receive the amount from parties to whom the goods sold on credit or from the purchaser of goods and have to maintain parties’ ledger account individually as well as sales journal and sales return journal as illustrated below;

Jan 1. 2015 Sold merchandise to Hakim & Co. Rs.4, 000/= vide Invoice No1003.Jan 5. Sold merchandise to Jasco Traders for Rs.5, 000/= vide invoice No.1004.Jan 10. An Invoice No.1005 for Rs.10, 000/- was issued against merchandise sold to Star G/Store.Jan 15. Sold merchandise to Usman Brothers on credit for Rs.6, 000/- against Invoice No.1006.Jan 30. Merchandise consigned to Wali Brothers Rs.6, 000/= vide Invoice No. 1007.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

SALES JOURNALPage No.1

DATE ACCOUNT DEBITED INVOICE NO.POST

AMOUNTRef.

1.1.2015 Hakim & Co. 1003 _/ 4,000 5.1.2015 Jasco Traders 1004 _/ 5,000 10.1.2015 Star G/Store 1005 _/ 10,000 15.1.2015 Usman Brothers 1006 _/ 6,000 30.1.2015 Wali Brothers 1007 _/ 6,000 TOTAL 31,000

Accounts receivable (Dr.) 31,000.-Sales (Cr.) 31,000.-

The entry of sales journal will be recorded through journal voucher as to account receivable debit and sales credit narrating to record sales for the month of January 2015 and to individual parties’ account or debtors account in subsidiary ledger making reference sales journal.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

In case of sold goods returns, the following sales return journal is made to record sales returns from the selected transactions below;

Jan 20. Merchandise returned from Jasco Traders Rs.500/- vide credit memo No.1050.Jan 30. Received merchandise from Star G/Store vide credit memo No. 1055 for Rs.1000/=

SALES RETURNS AND ALLOWANCES JOURNALPage No.1

DATE ACCOUNT CREDITEDCREDIT POST

AMOUNTMEMO Ref.

20.1.2015 Jasco Traders 1050 _/ 500 30.1.2015 Star G/Store 1055 _/ 1,000 TOTAL 1,500

Sales Return & Allowances (Dr.) 1500 Accounts Receivable (Cr.) 1500

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

The entry of sales return and allowances journal will be made by journal voucher narrating to record sales return for the month of January 2015 and to individual accounts of party.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

The total of carry forward balance of customer accounts must be equal to the carry forward balance of account receivable as shown below;

Hakim & Co. 4,000Jasco Traders 4,500Star G/Store 9,000Usman Brothers 6,000Wali Brothers 6,000

TOTAL 29,500.-

ACCOUNT PAYABLE

Accounts payable means to pay the amount to the parties who supplied goods on credit or to the seller of goods.

Account payable account is made like account receivable account as illustrated below’;PURCHASES

Jan 1. Purchased merchandise from Aftab Traders Rs.10, 000/= vide Invoice No. 3201.Jan 10. Purchased merchandise from Iqbal & Co. Rs.5000/= vide Invoice No.1312.Jan 15. Merchandise purchased on account form Jamshed Brothers for Rs.5000/= vide Invoice No. 4242.Jan 20. Received an invoice No.2323 for purchase of Rs.5000/= from Azad TradersJan 30. Goods purchased for Rs.10000/- against Purchase Inv. # 1035 from Amjad Brothers.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

Account payable is recorded by journal voucher narrating to record purchases for the month of January 2015 making reference purchase journal.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

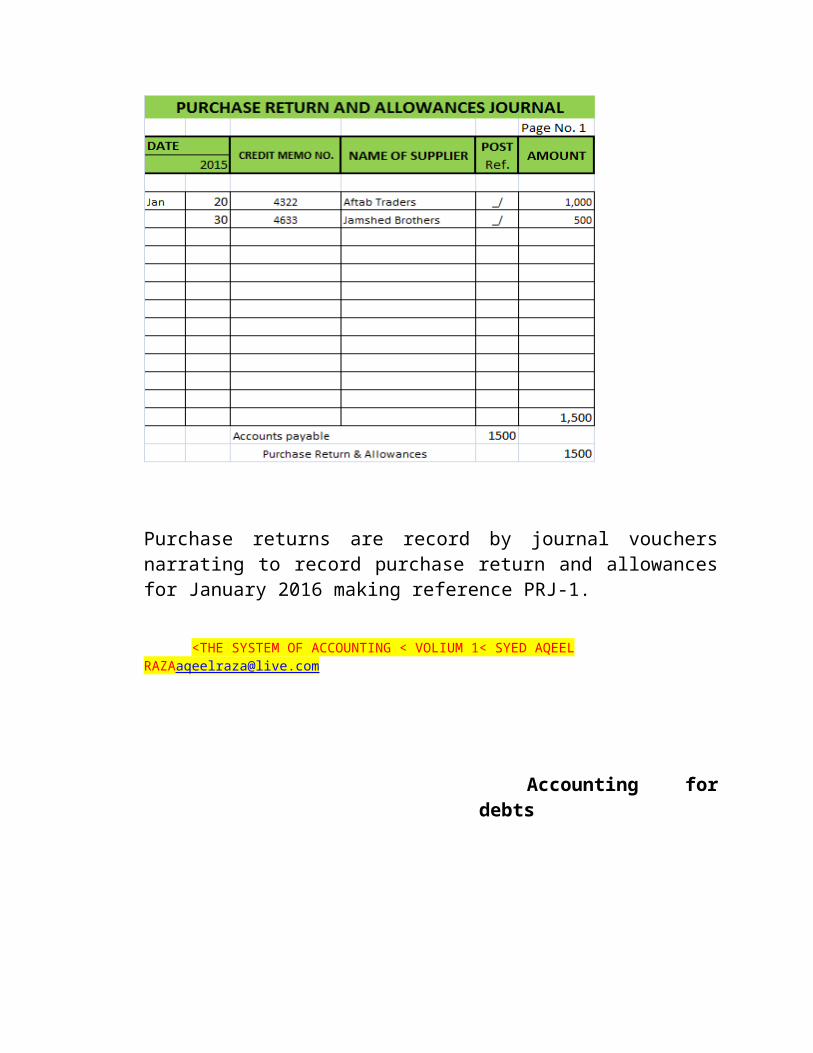

PURCAHSE RETURN

Jan 15. Debit Note Issued to Aftab Traders for Rs.1000/- against damaged goods returns and received credit memo No.4322.Jan 30. Damaged goods returned to Jamshed Brothers for Rs.500/- with Debit Note No.3343 and received credit Note.4633.

Purchase returns are record by journal vouchers narrating to record purchase return and allowances for January 2016 making reference PRJ-1.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL [email protected]

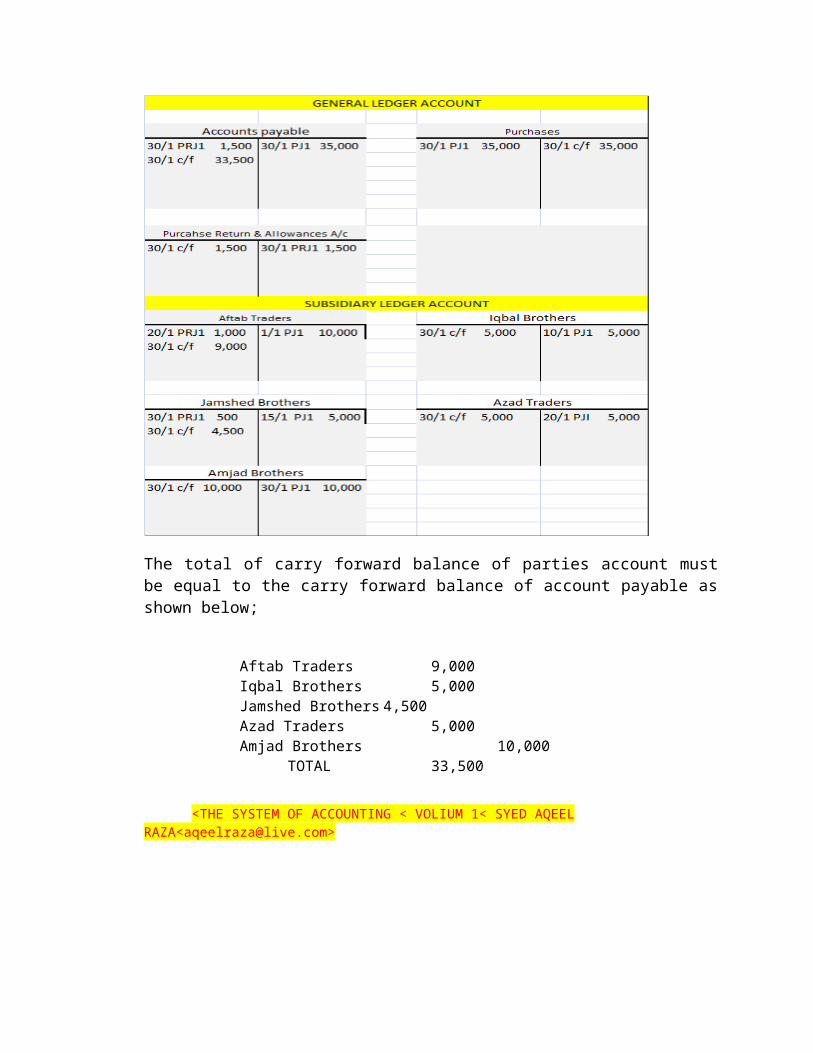

Accounting for debts

The total of carry forward balance of parties account must be equal to the carry forward balance of account payable as shown below;

Aftab Traders 9,000Iqbal Brothers 5,000Jamshed Brothers 4,500Azad Traders 5,000Amjad Brothers 10,000

TOTAL 33,500

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

THE A G I N G

An aging schedule has to design that shows an invoices and its due dates enables to settle or receive invoices on maturity. It can be made for both accounts payable and accounts receivable.

In accounts payable aging, the analysis of payment to suppliers from whom the goods purchased on credit for business indicates which supplier is paid first in order to avoid any credit or supply problem or the maturity of invoice date.

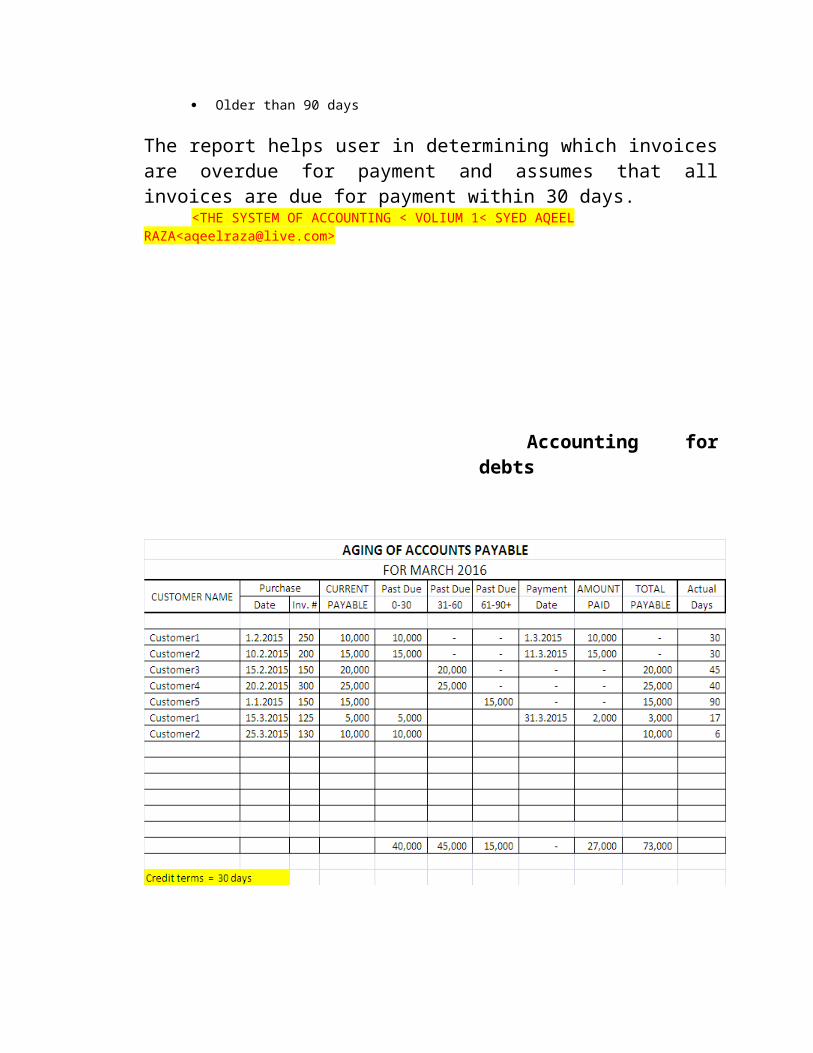

ACCOUNT PAYABLE AGINT REPORT

Accounts payable is the result of all purchases made by a business from regular vendors on credit basis. Many businesses pay for services and materials 30, 60, 90 or 120 days after receipt of invoice for controlling their cash flow. With this information, a company can decide which items can be paid on time based on the amount of cash the company has on hand and which invoices the company may need to pay late.

An account payable aging report lists the due date of payments that a company owes to venders and has generally set up with 30 days time but consists on;

00 to 30 days old 31 to 60 days old 61 to 90 days old Older than 90 days

The report helps user in determining which invoices are overdue for payment and assumes that all invoices are due for payment within 30 days.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

The aging of account payable schedule shows that the company had purchased goods on credit from customer1 and customer2 and paid them within the credit limit of 30 days when customer3, customer4 and customer5 were not paid older than 45, 40 and 90 days.

In case of paying part amount into bill, the balance will be treated older than the date of purchase as shown in customer1.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

ACCOUNTS RECEIVABLE AGING

This report directs management’s attention to accounts that are slow to receive first by customer and then by the date of sales invoice. It is also useful in determining Allowance for doubtful accounts.

AGING OF ACCOUNTS RECEIVABLE

If we assume the credit terms are net 30 days and invoices are within 30 days will be classified as current and;

Any unpaid invoices in April are classified as 1-30 days past due.

Any unpaid invoices in March are classified as 31-60 past due and so on.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

The aging of accounts receivable is used to calculate the estimation of allowance for uncollectable bad debts like;

The estimated amount of uncollectable is recorded in ledger by debiting allowance for uncollectable bad debt and crediting accounts receivable.

The individual account will also affect.

In case of collection some part of uncollectable amount, the balance of accounts receivable and allowance for doubtful accounts will increase by reversing the entry above.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

NOTES PAYABLE AND NOTES RECEIVABLE

In order to enjoy maximum benefit from the business, firms or persons borrow money from banks, financial institutions, friends or relative and mostly against notes which may be interest bearing or non interest bearing depends upon the receiver or payer. Interest bearing notes will be paid on the due date of the note along with the actual amount.

A promissory note is an instrument in writing unconditional undertaking, signed by the maker to pay a certain amount only to, or to the order of, a certain person, or to the bearer of the instrument.

The firm or person who gave amount on promissory note would enjoy the interest at the rate specified on the notes which called interest income and the firm or person who took the amount on promissory notes would pay the interest on notes payable called interest expense.

The note is treated as an asset by the holder and liability by the payer.

NOTE PAYABLE

The note payable is current liability taken in any of the following cases;

- To receive cash as a loan- To clear the liabilities- To purchase assets- To pay for expenses

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL RAZA<[email protected]>

Accounting for debts

Suppose that;

- To receive cash as loan;Cash xxxx

Notes Payable xxxx

- To clear the liability by notes for 90 days at 5% interest;

Accounts payable xxxx5% Notes payable xxxx

- Purchase machinery against notes for 60 dyas

Machine xxxxNotes payable xxxx

- The payment of expenses;

Advertising expenses xxxxNotes Payable xxxx

At the time of maturity or due date, the money lender pays the liability, if the note is non-interest bearing as;

Notes Payable xxxCash/Bank xxxx

If the note is interest bearing means face value of note along with interest for the cost of furniture Rs.10000 issued a note for 3 months @ 6% p.a. interest;

Furniture 100006% Notes payable 10000

6% notes payable 10000Interest expense 150

Cash/bank 10150

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL [email protected]

Accounting for debts

NOTES RECEIVEABLE

The principal amount of notes receivable is current asset and the interest on interest bearing notes is interest income under calculation; principal amount x interest rate x time period = interest earned.

The payee is the party who receives the amount of the note and the maker is the party who give notes to the payee. The principal amount is to be paid on the maturity date of the note.

The notes receivable is given on the following cases;

- To pay cash as loan- To receive acceptance of note in payment of an account- To sale assets

- A loan provided to others against a noteNotes receivable

Cash/bank

- Received a note in payment of an accountNotes receivable

Account receivable (customer)

- A sale of asset/merchandise against a noteNotes receivable

Sales<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL [email protected]

Accounting for debts

A note can be endorsed to others in payment of his liabilities, it means that the holder can transfer /endorse notes to others, the entry will be;

Account payable (party)Notes receivable

The holder of the note may keep it till maturity, and collect the amount on the due date

1- In cash of non interest bearing note ta. Cash

i. Notes receivable

In case of interest bearing note;Cash/bank

Notes receivableInterest income

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL [email protected]

Accounting for debts

THE BILL OF EXCHANGE

A bill of exchange is an unconditional duly written and signed order form given one to another directing to pay the certain sum of money to a person or firm, either on demand or at a fixed or future date and time.

The bill of exchange is similar to cheque and promissory note drawn able by individual or bank and/or transferable by endorsement. If the bill is issued by the bank, it can be referred to as bank draft and by individual as trade draft.

BILLS RECEIVABLE/PAYABLE

Like account receivable and account payable, the account of bill of exchange is maintained as exampled below;

On May 1, 2015 – Hameed sold goods to Karim on credit for Rs.3000/= and sent him a draft of a bill for 3 months after date. Karim accepted the bill and returned duly singed it to Hameed on May 10. Hameed presents the bill for payment and met the bill.

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL [email protected]

Accounting for debts

JOURNAL ENTIRES OF HAMEED - RECEIVER

May 1, 2015 – Hameed sold goods on credit to Karim for Rs.3, 000/=Accounts Receivable (Karim) 3,000

Sales 3,000May 10, Hameed received a bill for Rs.3, 000/=

Bills Receivable 3,000/=Accounts Receivable (Karim)

July 10, 2015 – Hameed received cash against bill

CashBills receivable

JOURNAL ENTRIES OF KARIM (PAYER)

May 1, 2015 – Karim goods on credit from Hameed for Rs.3, 000/=Purchases 3,000

Accounts Payable (Hameed) 3,000

May 10, Karim paid a bill for Rs.3, 000/=

Account payable (Hameed) 3,000/=Bills payable 3000/=

July 10, 2015 – Karim paid cash against billBills payable

Cash

<THE SYSTEM OF ACCOUNTING < VOLIUM 1< SYED AQEEL [email protected]

The accounting for debts involves two parties receiver and payer wherein who gives money will receive and who takes it will pay with or without interest as agreed mutually. The receiver will maintain account receivable and payer account payable.

In trade, the debt is given to increase sales volume in shape of goods and services as well as for paying liabilities and purchasing assets against negotiable instruments with or without interest.

The business man is forced to work more and more to gain profit to pay debt against borrowed money. One side the debt increases the volume of business and other side opens the door of employment but sometime caused the trouble in business due to mismanagement.

WRITER’S VIEW

WRITTEN BY:

SYED AQEEL RAZAMASTER OF COMMERCE & POLITICS