Accounting challenges due to implementation of Corporate Social Responsibility and impact of IPSAS

12

ACCOUNTING CHALLENGES DUE TO IMPLEMENTATION OF “CSR” – UNDER SECTION 135 OF COMPANIES ACT TOGETHER WITH THE IMPACT OF IPSAS Loyola College,- Dr. T. Joseph M.Com., M.Phil., MBA.,Phd., Chennai Associate Profession, Commerce Department - Sundar A. Rodriguez M.Com.,FCA.,DISA.,CFSA(USA)., Research Scholar, Commerce Department

-

Upload

sundar-rodriguez-fca-cfsafaiacfa -

Category

Government & Nonprofit

-

view

85 -

download

1

Transcript of Accounting challenges due to implementation of Corporate Social Responsibility and impact of IPSAS

ACCOUNTING CHALLENGES DUE TO IMPLEMENTATION OF “CSR” – UNDER

SECTION 135 OF COMPANIES ACT TOGETHER WITH THE IMPACT OF IPSAS

Loyola College, - Dr. T. Joseph M.Com., M.Phil., MBA.,Phd.,

Chennai Associate Profession, Commerce Department

- Sundar A. Rodriguez M.Com.,FCA.,DISA.,CFSA(USA).,

Research Scholar, Commerce Department

CORPORATE SOCIAL RESPONSIBILITY

CSR is “the responsibility of enterprises for their impacts on society”.

To completely meet their social responsibility, enterprises “should have in place a process to integrate social, environmental, ethical human rights and consumer concerns into their business operations and core strategy in close collaboration with their stakeholders” .

Ref: (http://ec.europa.eu/enterprise/policies/sustainable-business/corporate-social-responsibility/index_ en.htm)

CSR – DEFINITION IN COMPANIES ACT 2013

SECTION 135

1) Every company having a net worth of rupees five hundred crore or more (100 million $ or more), or a turnover of rupees one thousand crore or more (200 million $ or more) , or a net profit of rupees five crore or more (1 million $ or more) during any financial year shall constitute a Corporate Social Responsibility Committee of the Board consisting of three or more directors, out of which at least one director shall be an independent director;

AMOUNT TO BE SPENT FOR CSR

Section 135 (5)

The Board of every company covered under CSR shall ensure for every financial year that:

At least 2% of average net profits of the company made during 3 immediately preceding financial years is spent on CSR.

This spending to be made in pursuance of its laid CSR Policy.

INCOMPATIBLE MARRIAGE

• The company has been used to account for its core activities – to carry on the business.

• Now the company has to also enter into not for profit or social sector, as the activities under CSR falls under it

• The accounting standards for each of these two incompatible marriage is different, the jargons used are also different, and above all in some case the same concept means differently.

CONVERGENCE – INDIAN SCENARIO

• The Ministry of Corporate Affairs had not come up with specific standards exclusively for the accounting and reporting of the CSR activities.

• If the company is an Indian Company the standards mandated by MCA is to be followed, which does not address the uniqueness of the CSR related accounting process.

• As of now the companies are expected to follow the standards propounded by MCA for reporting by the companies, hence the activities under CSR are also to be covered by it, which is going to create lots of problem.

INTERNATIONAL SCENARIO

• For reporting of the business activities the international community has come up with IFRS – International Financial Reporting Standards.

• For the reporting of the Public Sector Activities (under which the CSR falls) it has the IPSAS – International Public Sector Accounting Standards.

• The countries which had approved and following the approved standards has to adhere to the appropriate standards based on which criteria the activities or transactions falls

THE COMPLICATIONS DUE TO THE MAZE

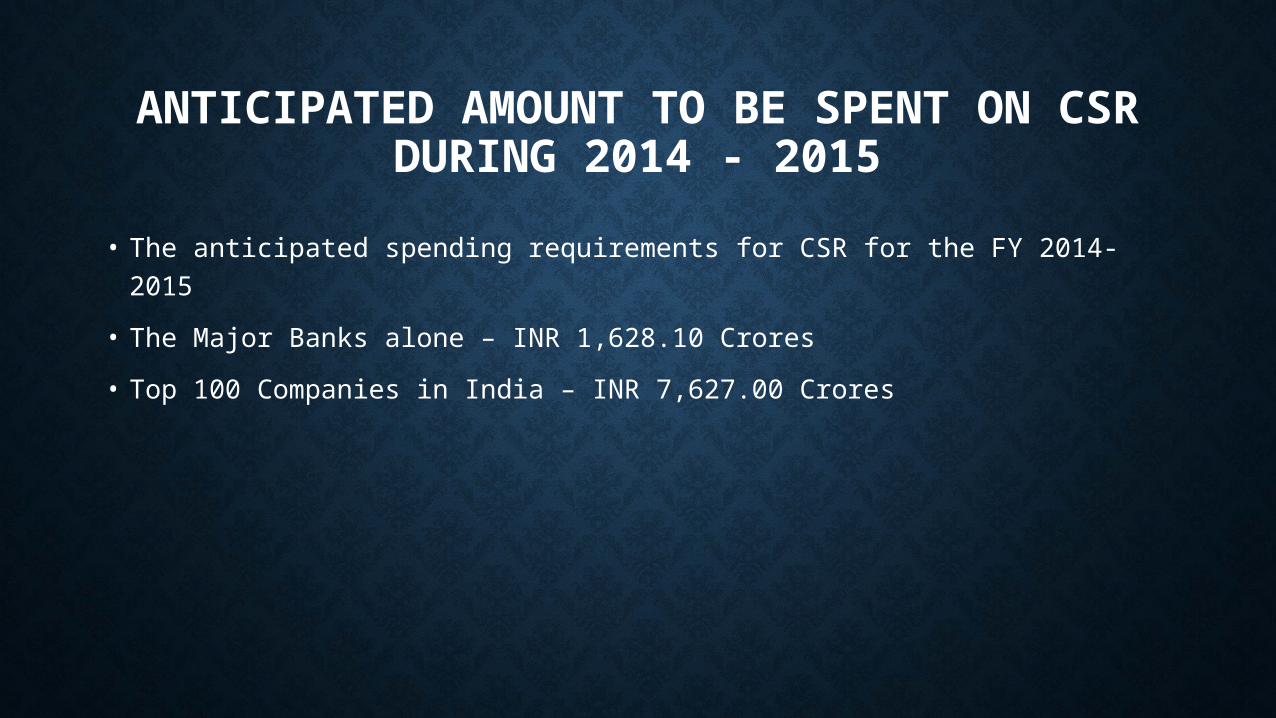

ANTICIPATED AMOUNT TO BE SPENT ON CSR DURING 2014 - 2015

• The anticipated spending requirements for CSR for the FY 2014-2015

• The Major Banks alone – INR 1,628.10 Crores

• Top 100 Companies in India – INR 7,627.00 Crores

RECOMMENDATIONS

• The MCA has to come up with another set of standards which are converged with IPSAS (as the ones which they had now issued converged with IFRS).

• The segmental accounting for the consolidation of the Indian operation with that of the other countries operations, should take appropriate measures to incorporate the CSR activities carried out in India by following the concepts of IPSAS, insofar as it relates to it.

• The oversight mechanism should be given appropriate guidelines, based on the approved and/or suggested standards and guidelines for the accounting and reporting of the CSR activities to enable them to discharge their function more efficiently and effectively. If this is not done then the very spirit of law which spurred the formulation of CSR would be defeated

QUESTIONS

?

THANKS

• Loyola College, - Dr. T. Joseph M.Com., M.Phil., MBA.,Phd.,

• Chennai Associate Profession, Commerce Department

• - Sundar A. Rodriguez M.Com.,FCA.,DISA.,CFSA(USA).,

• Research Scholar, Commerce Department