Accounting & Auditing Update Let’s Talk About CECL Accounting & Auditing Update Accounting...

54

© 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC Accounting & Auditing Update Let’s Talk About CECL Risk Management and Internal Audit Seminar

Transcript of Accounting & Auditing Update Let’s Talk About CECL Accounting & Auditing Update Accounting...

© 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Accounting & Auditing Update Let’s Talk About CECL Risk Management and Internal Audit Seminar

2 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

This material was used by Elliott Davis during an oral presentation; it is not a complete record of the discussion. This presentation is for informational purposes and does not contain or convey specific advice. It should not be used or relied upon in regard to any particular situation or circumstances without first consulting the appropriate advisor. No part of the presentation may be circulated, quoted, or reproduced for distribution without prior written approval from Elliott Davis.

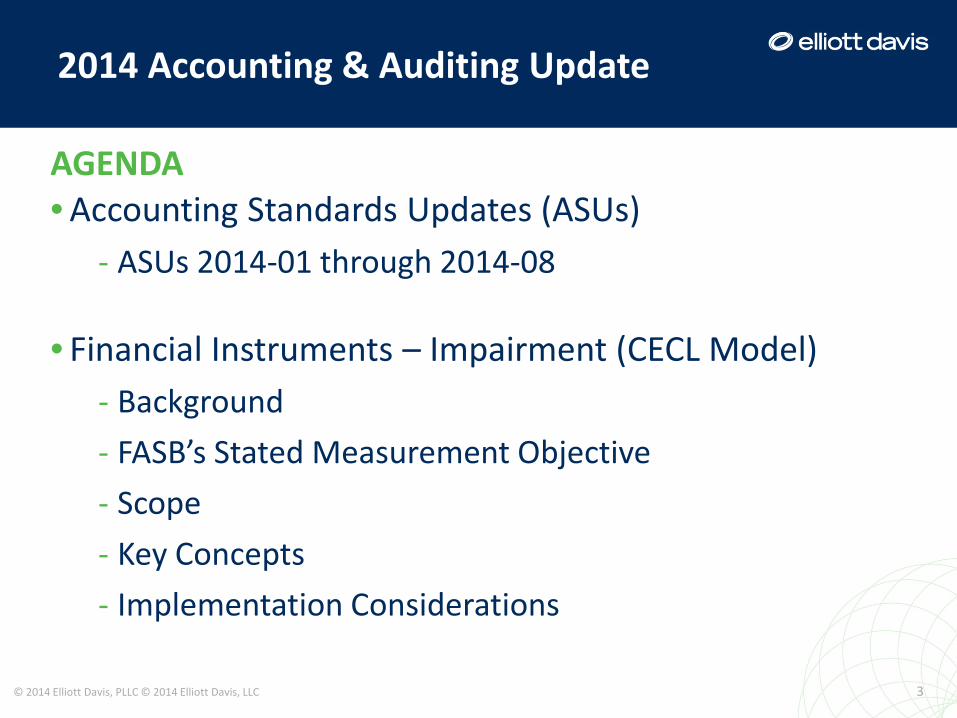

2014 Accounting & Auditing Update

AGENDA • Accounting Standards Updates (ASUs)

- ASUs 2014-01 through 2014-08

• Financial Instruments – Impairment (CECL Model) - Background - FASB’s Stated Measurement Objective - Scope - Key Concepts - Implementation Considerations

3 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update

4 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Accounting Standards Updates (ASUs)

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

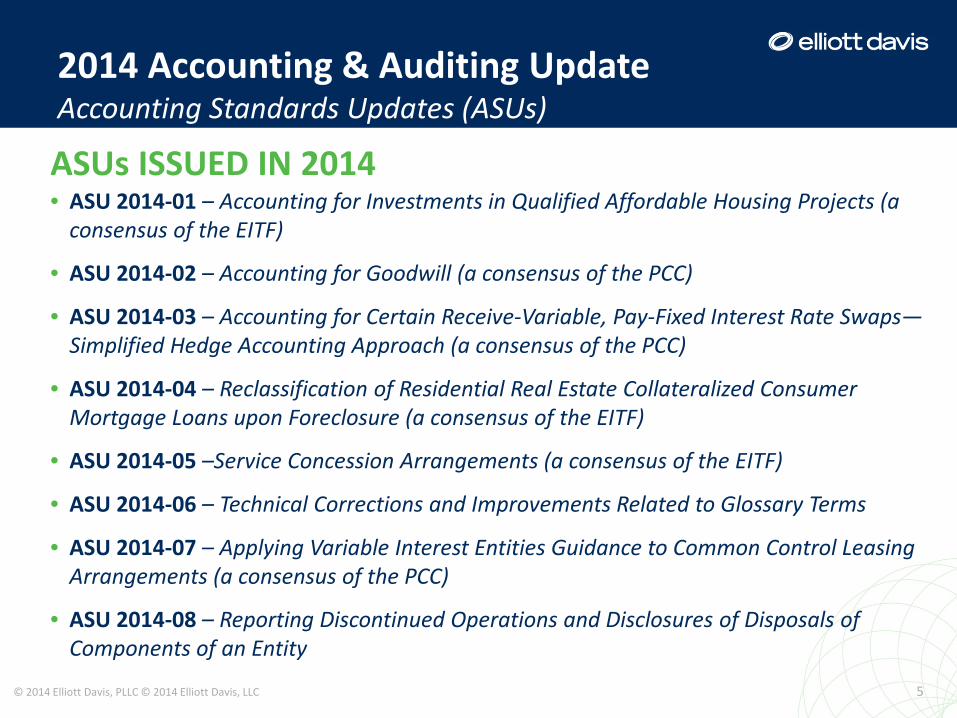

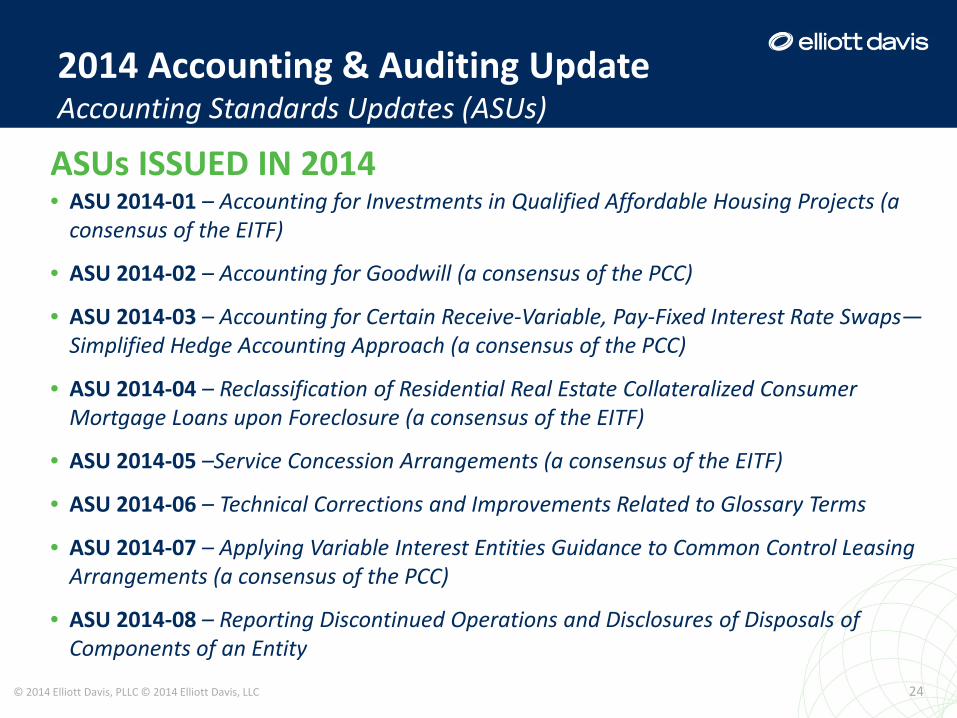

ASUs ISSUED IN 2014 • ASU 2014-01 – Accounting for Investments in Qualified Affordable Housing Projects (a

consensus of the EITF)

• ASU 2014-02 – Accounting for Goodwill (a consensus of the PCC)

• ASU 2014-03 – Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach (a consensus of the PCC)

• ASU 2014-04 – Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure (a consensus of the EITF)

• ASU 2014-05 –Service Concession Arrangements (a consensus of the EITF)

• ASU 2014-06 – Technical Corrections and Improvements Related to Glossary Terms

• ASU 2014-07 – Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements (a consensus of the PCC)

• ASU 2014-08 – Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

5 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

PRIVATE COMPANY COUNCIL • The Financial Accounting Foundation (“FAF”) Board of

Trustees has established the Private Company Council (“PCC”) in an effort to improve the process of setting accounting standards for private companies.

• Intended to put in place a system for recognizing differences in the needs of public and private company financial statement users and preparers that will avoid creation of a ‘two-GAAP’ system.

6 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

7 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-02 Accounting for Goodwill (a consensus of the PCC)

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASU 2014-02 – Accounting for Goodwill • Issued on January 16, 2014 • Allows an accounting alternative for the subsequent

measurement of goodwill for private companies. • If elected, the accounting alternative requires the entity

to amortize goodwill on a straight-line basis over 10 years, or less than 10 years if the entity demonstrates that another useful life is more appropriate.

8 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

9 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-03 Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate

Swaps—Simplified Hedge Accounting Approach

(a consensus of the PCC)

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASU 2014-03 – Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach

• Issued on January 16, 2014 • Provide an additional hedge accounting alternative to

private companies that are not financial institutions (simplified hedge accounting approach) for certain types of swaps if certain conditions are met.

• This accounting alternative is not available to financial institutions

10 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

11 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-07 Applying Variable Interest Entities

Guidance to Common Control Leasing Arrangements

(a consensus of the PCC)

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASU 2014-07 – Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements

• Issued on March 20, 2014 • Allows a private company to elect—when certain

conditions exist—not to apply VIE guidance to a lessor under common control

• Requires certain disclosures about the lessor and the leasing arrangement

12 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASUs ISSUED IN 2014 • ASU 2014-01 – Accounting for Investments in Qualified Affordable Housing Projects (a

consensus of the EITF)

• ASU 2014-02 – Accounting for Goodwill (a consensus of the PCC)

• ASU 2014-03 – Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach (a consensus of the PCC)

• ASU 2014-04 – Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure (a consensus of the EITF)

• ASU 2014-05 –Service Concession Arrangements (a consensus of the EITF)

• ASU 2014-06 – Technical Corrections and Improvements Related to Glossary Terms

• ASU 2014-07 – Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements (a consensus of the PCC)

• ASU 2014-08 – Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

13 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

14 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-01 Accounting for Investments in Qualified Affordable Housing

Projects (a consensus of the EITF)

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASU 2014-01 – Accounting for Investments in Qualified Affordable Housing Projects

• Issued on January 15, 2014

• Provides guidance on accounting for investments by a reporting entity in flow-through limited liability entities that manage or invest in affordable housing projects that qualify for the low-income housing tax credit.

• The ASU permits reporting entities to make an accounting policy election to account for their investments in qualified affordable housing projects using the proportional amortization method if certain conditions are met.

15 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASU 2014-01 – Accounting for Investments in Qualified Affordable Housing Projects

• Under the proportional amortization method, an entity amortizes the initial cost of the investment in proportion to the tax credits and other tax benefits received and recognizes the net investment performance in the income statement as a component of income tax expense (benefit).

• If elected, must be applied consistently to all qualifying affordable housing project investments rather than a decision to be applied to individual investments.

16 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

17 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-04 Reclassification of Residential Real

Estate Collateralized Consumer Mortgage Loans upon Foreclosure

(a consensus of the EITF)

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

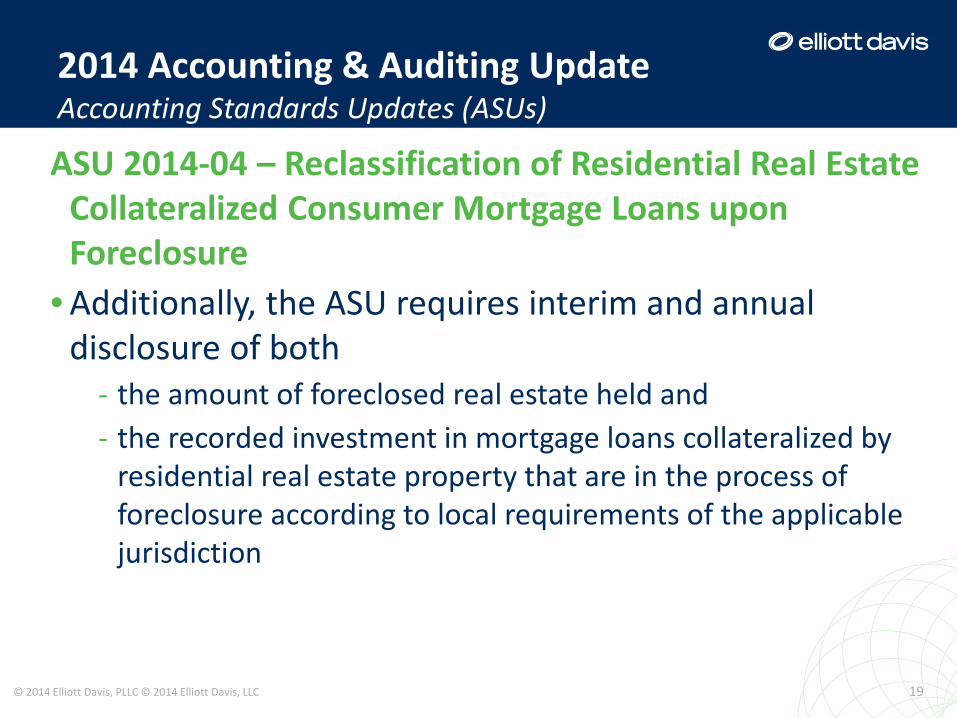

ASU 2014-04 – Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure

• Issued on January 17, 2014 • Clarifies when an in substance repossession or

foreclosure occurs: - Specifically, a creditor is considered to have received physical

possession of residential real estate property collateralizing a consumer mortgage loan, upon either (1) obtaining legal title upon completion of a foreclosure or (2) obtaining interest in the property in satisfaction of the loan through a deed in lieu of foreclosure or through a similar legal agreement.

18 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASU 2014-04 – Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure

• Additionally, the ASU requires interim and annual disclosure of both

- the amount of foreclosed real estate held and - the recorded investment in mortgage loans collateralized by

residential real estate property that are in the process of foreclosure according to local requirements of the applicable jurisdiction

19 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

20 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-05 Service Concession Arrangements

(a consensus of the EITF)

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

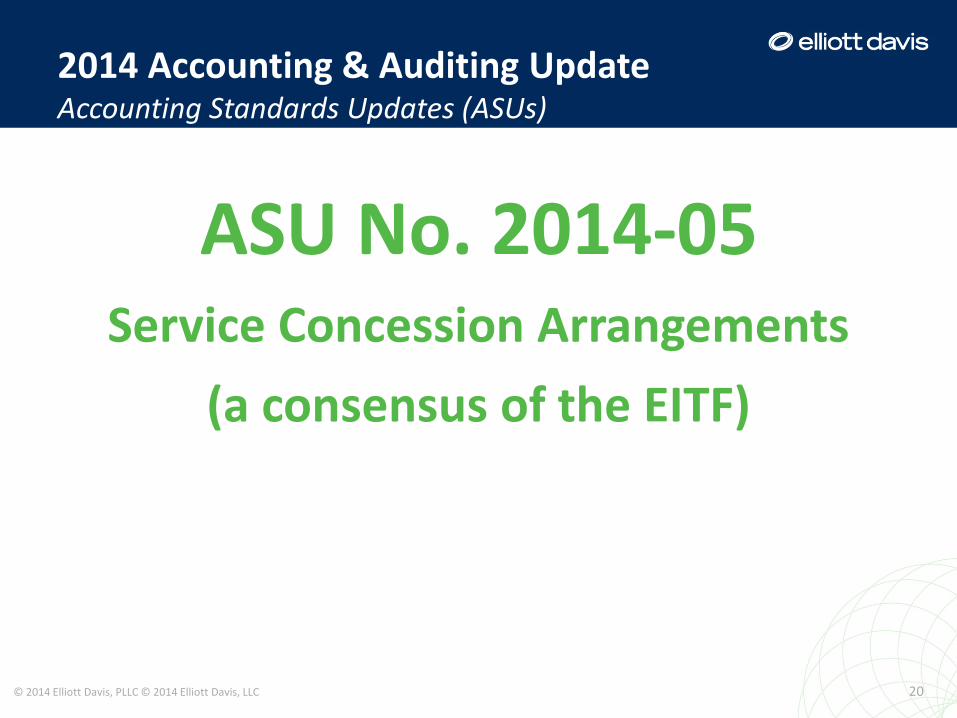

ASU 2014-05 –Service Concession Arrangements • Issued on January 23, 2014 • Specifies that an operating entity should not account for

a service concession arrangement as a lease • The amendments also specify that the infrastructure

used in a service concession arrangement should not be recognized as property, plant, and equipment

NOTE: A service concession arrangement is an arrangement between a public-sector entity grantor and an operating entity under which the operating entity operates the grantor’s infrastructure (for example, airports, roads, and bridges)

21 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

22 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-08 Reporting Discontinued Operations

and Disclosures of Disposals of Components of an Entity

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

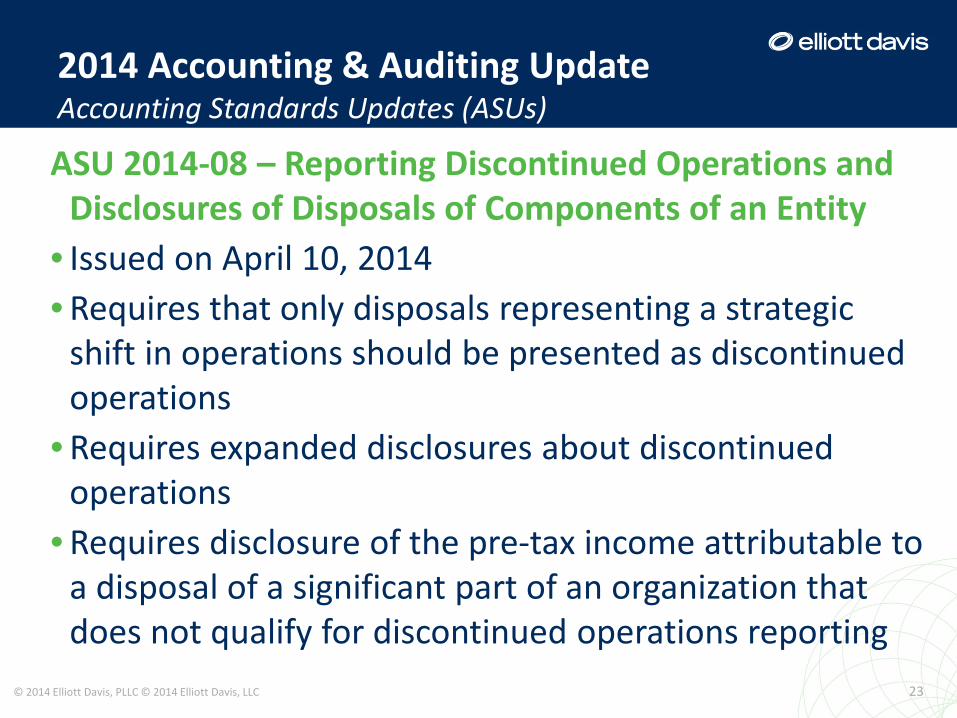

ASU 2014-08 – Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

• Issued on April 10, 2014 • Requires that only disposals representing a strategic

shift in operations should be presented as discontinued operations

• Requires expanded disclosures about discontinued operations

• Requires disclosure of the pre-tax income attributable to a disposal of a significant part of an organization that does not qualify for discontinued operations reporting

23 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASUs ISSUED IN 2014 • ASU 2014-01 – Accounting for Investments in Qualified Affordable Housing Projects (a

consensus of the EITF)

• ASU 2014-02 – Accounting for Goodwill (a consensus of the PCC)

• ASU 2014-03 – Accounting for Certain Receive-Variable, Pay-Fixed Interest Rate Swaps—Simplified Hedge Accounting Approach (a consensus of the PCC)

• ASU 2014-04 – Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure (a consensus of the EITF)

• ASU 2014-05 –Service Concession Arrangements (a consensus of the EITF)

• ASU 2014-06 – Technical Corrections and Improvements Related to Glossary Terms

• ASU 2014-07 – Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements (a consensus of the PCC)

• ASU 2014-08 – Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

24 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

25 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

ASU No. 2014-06 Technical Corrections and

Improvements Related to Glossary Terms

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

ASU 2014-06 – Technical Corrections and Improvements Related to Glossary Terms

• Issued on March 14, 2014 • Contains amendments related to the Master Glossary,

including: - technical corrections related to glossary links - changes to glossary terms - conforming the definition selected terms appearing in the

Master Glossary

26 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

EFFECTIVE DATES

27 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Public Companies Private CompaniesASU 2013-02 Comprehensive Income (Topic 220): Reporting of

Amounts Reclassified Out of Accumulated Other Comprehensive Income

Already effective Effective for reporting periods beginning after December 15, 2013*

ASU 2013-04 Liabilities (Topic 405): Obligations Resulting from Joint and Several Liability Arrangements for Which the Total Amount of the Obligation Is Fixed at the Reporting Date (a consensus of the FASB Emerging Issues Task Force)

Effective for fiscal years (including interim periods) beginning after December 15, 2013*

Effective for fiscal years ending after December 15, 2014, and interim and annual periods thereafter*

ASU 2013-11 Income Taxes (Topic 740): Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists (a consensus of the FASB Emerging Issues Task Force)

Fiscal years (including interim periods) beginning after December 15, 2013*

Fiscal years (including interim periods) beginning after December 15, 2014*

ASU 2014-01 Investments—Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Qualified Affordable Housing Projects (a consensus of the FASB Emerging Issues Task Force)

Effective for annual periods and interim reporting periods within those annual periods, beginning after December 15, 2014*

Effective for annual periods beginning after December 15, 2014 and interim periods within annual reporting periods beginning after December 15, 2015*

ASU 2014-02 Intangibles—Goodwill and Other (Topic 350): Accounting for Goodwill (a consensus of the Private Company Council)

N/A – PCC issue – only applies to private companies

Effective for annual periods beginning after December 15, 2014 and interim periods within annual periods beginning after December 15, 2015*

ASU Number DescriptionEffective Dates

* Early adoption permitted.

2014 Accounting & Auditing Update Accounting Standards Updates (ASUs)

EFFECTIVE DATES

28 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

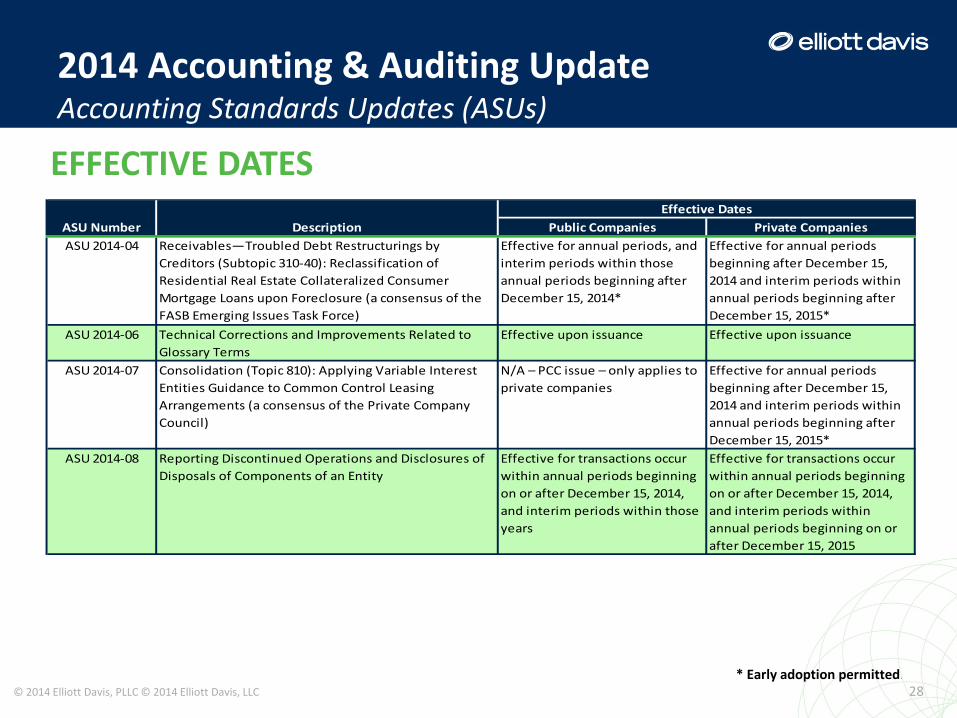

Public Companies Private CompaniesASU 2014-04 Receivables—Troubled Debt Restructurings by

Creditors (Subtopic 310-40): Reclassification of Residential Real Estate Collateralized Consumer Mortgage Loans upon Foreclosure (a consensus of the FASB Emerging Issues Task Force)

Effective for annual periods, and interim periods within those annual periods beginning after December 15, 2014*

Effective for annual periods beginning after December 15, 2014 and interim periods within annual periods beginning after December 15, 2015*

ASU 2014-06 Technical Corrections and Improvements Related to Glossary Terms

Effective upon issuance Effective upon issuance

ASU 2014-07 Consolidation (Topic 810): Applying Variable Interest Entities Guidance to Common Control Leasing Arrangements (a consensus of the Private Company Council)

N/A – PCC issue – only applies to private companies

Effective for annual periods beginning after December 15, 2014 and interim periods within annual periods beginning after December 15, 2015*

ASU 2014-08 Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

Effective for transactions occur within annual periods beginning on or after December 15, 2014, and interim periods within those years

Effective for transactions occur within annual periods beginning on or after December 15, 2014, and interim periods within annual periods beginning on or after December 15, 2015

ASU Number DescriptionEffective Dates

* Early adoption permitted.

2014 Accounting & Auditing Update

29 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Financial Instruments – Impairment

(CECL Model)

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

30 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Proposed ASU No. 2012-260

Financial Instruments – Impairment

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

BACKGROUND • After the financial crisis, the Financial Crisis Advisory Group

(“FCAG”) asked to consider how improvements in financial reporting could enhance investors’ confidence in financial markets and noted the following related to accounting standards and their application:

- Identified weaknesses in today’s model for estimating credit losses (“Incurred Loss” model)

• “Probable incurred” loss threshold that was seen as delaying recognition of losses

- Identified weaknesses in existing accounting standards resulting from the inherent complexity of having multiple credit impairment models

• Exposure Draft issued December 20, 2012 31 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

FASB’s STATED MEASUREMENT OBJECTIVE • Current estimate of all contractual cash flows not expected

to be collected - For financial instruments whose objective to hold the financial

instruments for the collection of contractual cash flows, the FASB believes that the amortized cost measurement objective is consistent with the way an entity expects to realize cash flows from the assets, namely by holding the instrument for the collection of contractual cash flows.

- That amortized cost objective is to reflect the present value of cash flows that an entity expects to collect.

32 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

FASB’s STATED MEASUREMENT OBJECTIVE • Current estimate of all contractual cash flows not expected

to be collected - The FASB believes the proposed guidance achieves that

objective through the combined effect of a) the proposed guidance on classification and measurement

that would result in measurement of the amortized cost basis of the financial asset at a present value, based on contractual cash flows and

b) the proposed guidance on credit losses that would result in an allowance for credit losses at a present value, based on contractual cash flows not expected to be collected, both discounted at the effective interest rate.

33 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

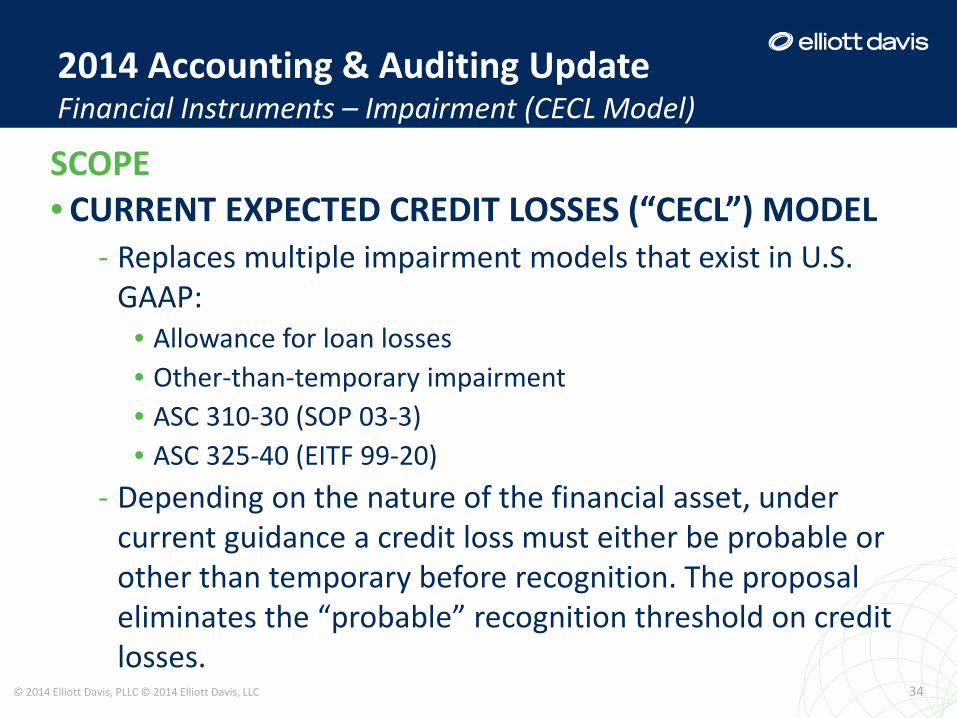

SCOPE • CURRENT EXPECTED CREDIT LOSSES (“CECL”) MODEL

- Replaces multiple impairment models that exist in U.S. GAAP:

• Allowance for loan losses • Other-than-temporary impairment • ASC 310-30 (SOP 03-3) • ASC 325-40 (EITF 99-20)

- Depending on the nature of the financial asset, under current guidance a credit loss must either be probable or other than temporary before recognition. The proposal eliminates the “probable” recognition threshold on credit losses.

34 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

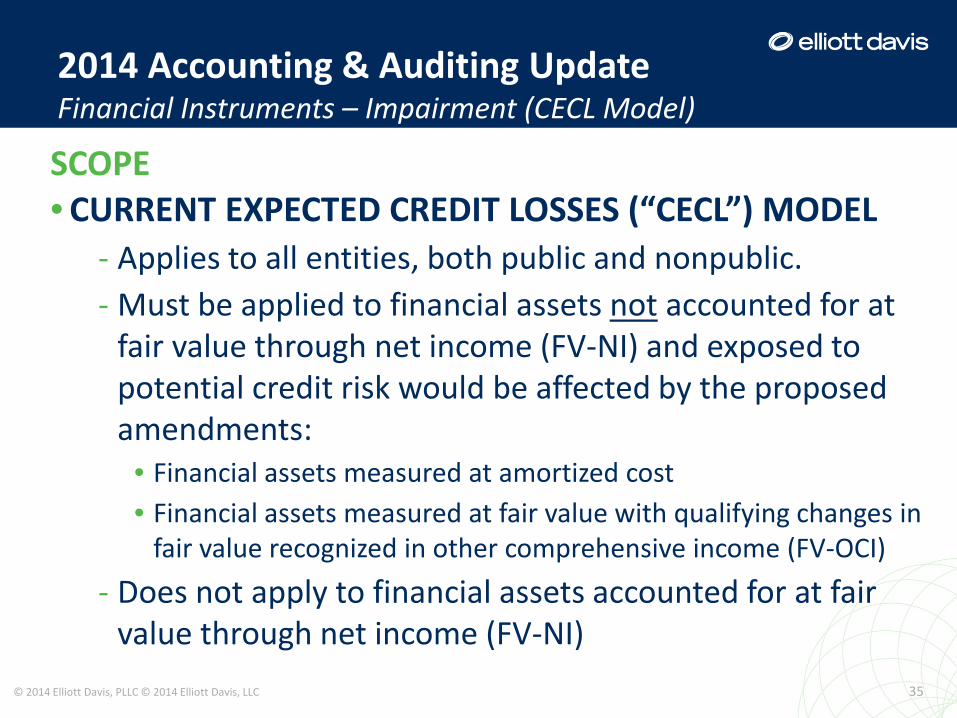

SCOPE • CURRENT EXPECTED CREDIT LOSSES (“CECL”) MODEL

- Applies to all entities, both public and nonpublic. - Must be applied to financial assets not accounted for at

fair value through net income (FV-NI) and exposed to potential credit risk would be affected by the proposed amendments:

• Financial assets measured at amortized cost • Financial assets measured at fair value with qualifying changes in

fair value recognized in other comprehensive income (FV-OCI) - Does not apply to financial assets accounted for at fair

value through net income (FV-NI) 35 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

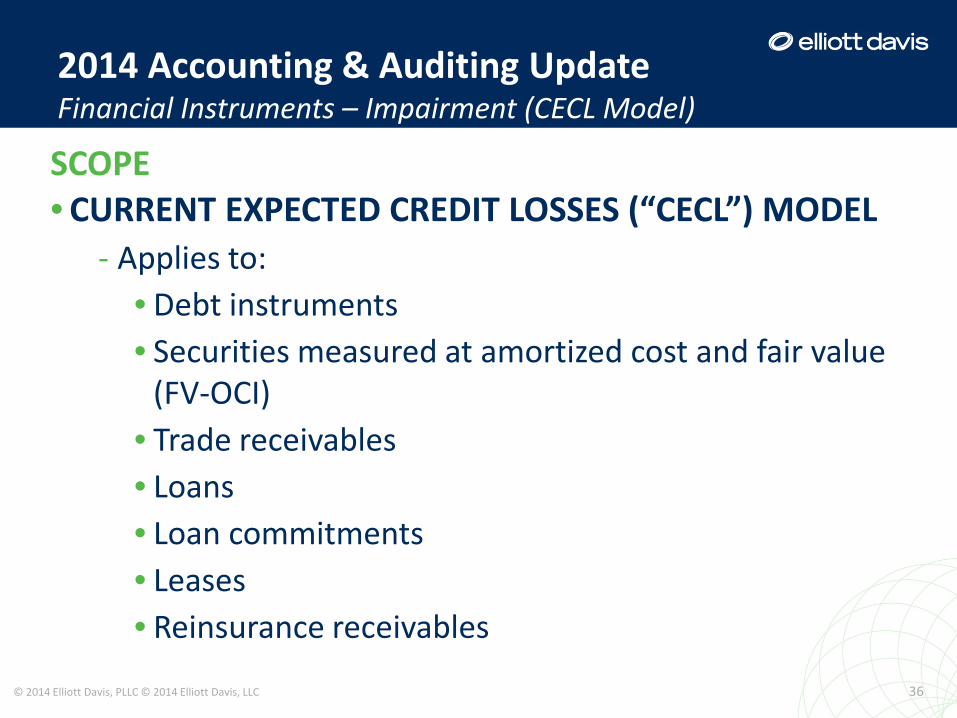

SCOPE • CURRENT EXPECTED CREDIT LOSSES (“CECL”) MODEL

- Applies to: • Debt instruments • Securities measured at amortized cost and fair value

(FV-OCI) • Trade receivables • Loans • Loan commitments • Leases • Reinsurance receivables

36 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

SCOPE • CURRENT EXPECTED CREDIT LOSSES (“CECL”) MODEL

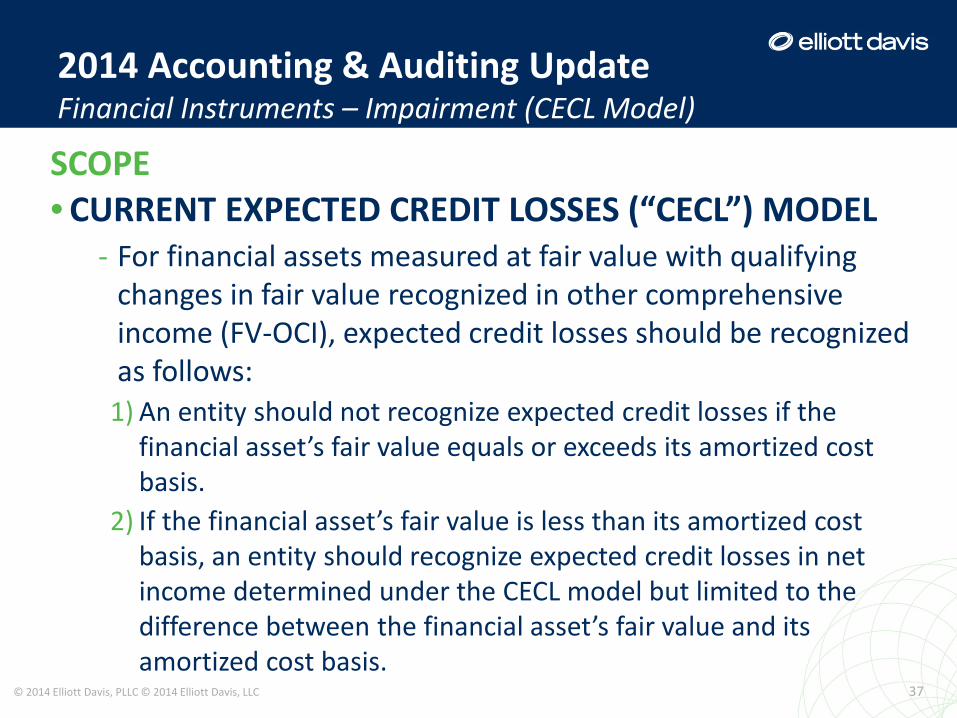

- For financial assets measured at fair value with qualifying changes in fair value recognized in other comprehensive income (FV-OCI), expected credit losses should be recognized as follows:

1) An entity should not recognize expected credit losses if the financial asset’s fair value equals or exceeds its amortized cost basis.

2) If the financial asset’s fair value is less than its amortized cost basis, an entity should recognize expected credit losses in net income determined under the CECL model but limited to the difference between the financial asset’s fair value and its amortized cost basis.

37 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

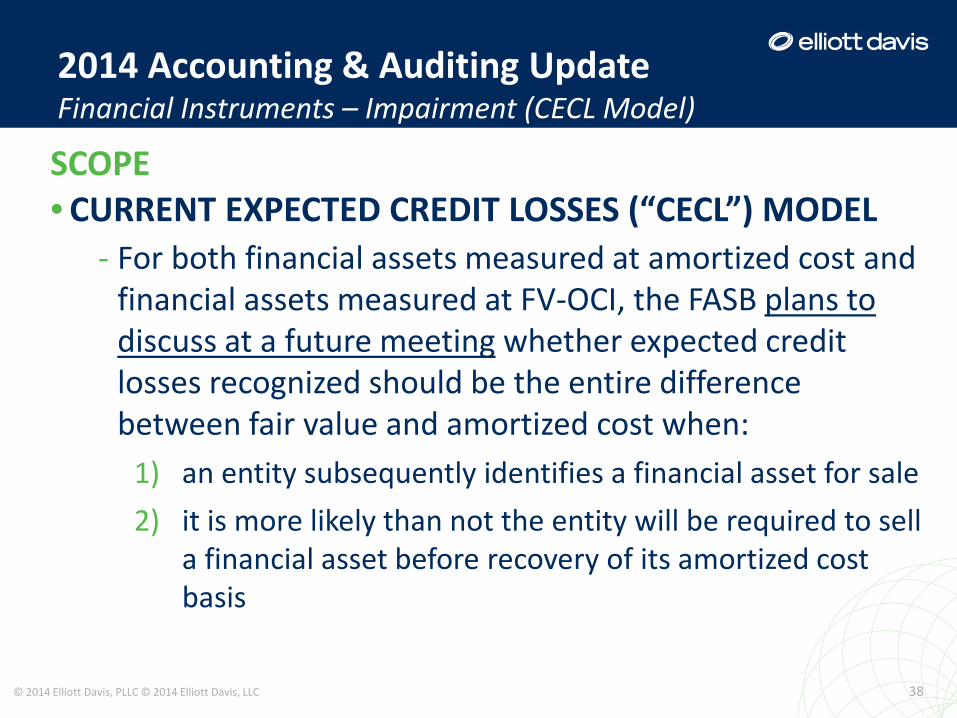

SCOPE • CURRENT EXPECTED CREDIT LOSSES (“CECL”) MODEL

- For both financial assets measured at amortized cost and financial assets measured at FV-OCI, the FASB plans to discuss at a future meeting whether expected credit losses recognized should be the entire difference between fair value and amortized cost when:

1) an entity subsequently identifies a financial asset for sale 2) it is more likely than not the entity will be required to sell

a financial asset before recovery of its amortized cost basis

38 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

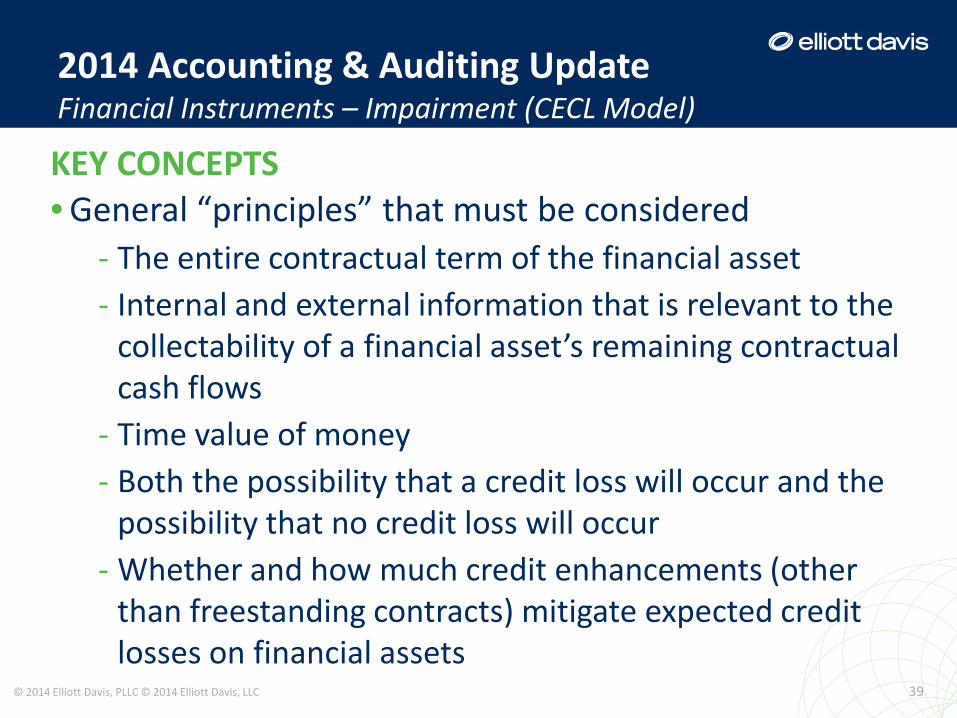

KEY CONCEPTS • General “principles” that must be considered

- The entire contractual term of the financial asset - Internal and external information that is relevant to the

collectability of a financial asset’s remaining contractual cash flows

- Time value of money - Both the possibility that a credit loss will occur and the

possibility that no credit loss will occur - Whether and how much credit enhancements (other

than freestanding contracts) mitigate expected credit losses on financial assets

39 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

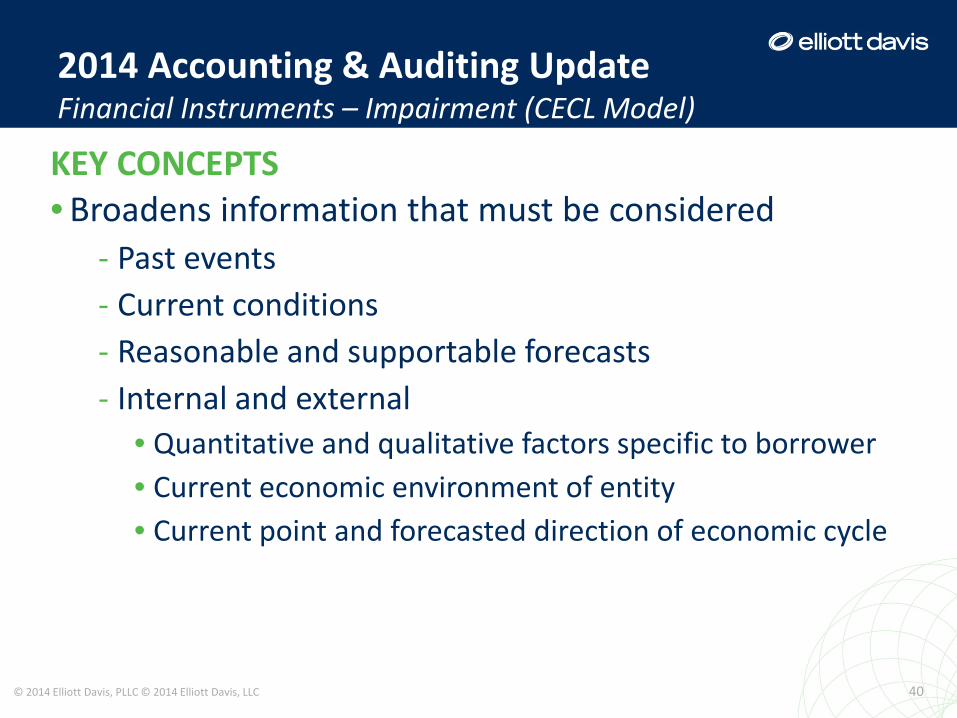

KEY CONCEPTS • Broadens information that must be considered

- Past events - Current conditions - Reasonable and supportable forecasts - Internal and external

• Quantitative and qualitative factors specific to borrower • Current economic environment of entity • Current point and forecasted direction of economic cycle

40 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • Intended to leverage existing internal credit risk

management tools and systems; however, inputs to the measurement will change

• No specific guidance as to whether credit losses should be measured on an individual or collective (pool) basis

41 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • Estimate shall reflect time value of money

- Example: discounted cash flow - Other methods implicitly consider time value of money such as

loss-rate, roll-rate, probability-of-default, and provision matrix - FV of collateral permitted for collateral dependent financial

assets

• Neither a best case or worst case scenario - Must reflect both the possibility that a credit loss will occur and

the possibility that no credit loss will occur - Cannot be based solely on the most likely outcome - Probability-weighted approach not required

42 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • Permitted to measure impairment based on the fair

value of collateral less cost to sell when repayment is expected to be provided “primarily or substantially through the operation of the collateral by the lender or sale of the collateral.”

43 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

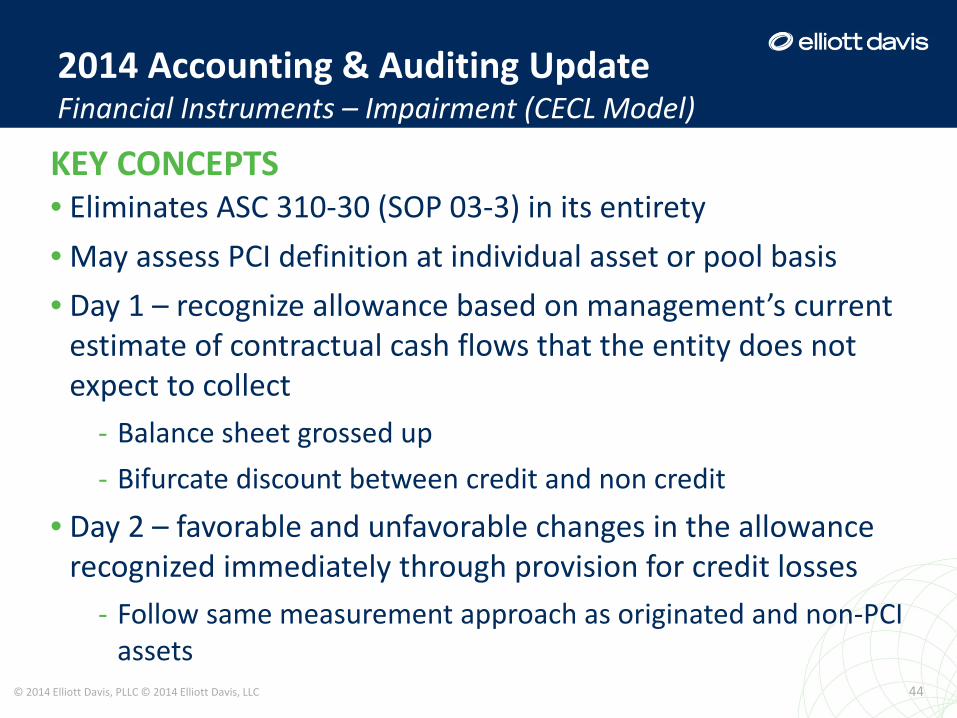

KEY CONCEPTS • Eliminates ASC 310-30 (SOP 03-3) in its entirety • May assess PCI definition at individual asset or pool basis • Day 1 – recognize allowance based on management’s current

estimate of contractual cash flows that the entity does not expect to collect

- Balance sheet grossed up - Bifurcate discount between credit and non credit

• Day 2 – favorable and unfavorable changes in the allowance recognized immediately through provision for credit losses

- Follow same measurement approach as originated and non-PCI assets

44 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • The FASB has decided not to expand the PCI approach,

as proposed in the proposed ASU, to other financial assets.

• The FASB has also decided to include in the CECL Model a requirement that the non-credit-related discount or premium resulting from acquiring a pool of PCI financial assets should be allocated to each individual financial asset.

45 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • Debt Securities

- Would record an allowance for credit losses (vs. current US GAAP which requires an adjustment to the amortized cost when there is OTTI)

• An entity may elect, as a practical expedient, not to recognize expected credit losses for FV-OCI financial assets if both:

- Fair value exceeds amortized cost - Expected credit losses are insignificant

46 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • In measuring the expected credit losses:

1)An entity should revert to a historical average loss experience for the future periods beyond which the entity is able to make or obtain reasonable and supportable forecasts.

2)An entity should consider all contractual cash flows over the life of the related financial assets.

3)When determining the contractual cash flows and the life of the related financial assets:

a) An entity should consider expected prepayments b) An entity should not consider expected extensions, renewals, and

modifications unless the entity reasonably expects that it will execute a troubled debt restructuring with a borrower.

47 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • In measuring the expected credit losses:

4)An entity’s estimate of expected credit losses should always reflect the risk of loss, even when that risk is remote. However, an entity would not be required to recognize a loss on a financial asset in which the risk of nonpayment is greater than zero yet the amount of loss would be zero.

5) In addition to using a discounted cash flow model to estimate expected credit losses, an entity would not be prohibited from developing an estimate of credit losses using loss-rate methods, probability-of-default methods, or a provision matrix using loss factors.

48 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • Charge-off—The proposed ASU carries forward the existing

requirements that a charge-off should be recorded when there is no reasonable expectation of future recovery

• Nonaccrual—The FASB decided to exclude the proposed nonaccrual guidance from the CECL Model.

• TDRs—The FASB decided that the TDR classification remains relevant under the CECL model. In addition, the FASB decided to revise the CECL Model to require that, in certain TDRs, an entity may be required to increase the cost basis of the restructured financial asset through a corresponding increase in the entity’s allowance for expected credit losses.

• Disclosures—Will require expanded disclosures 49 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

KEY CONCEPTS • Expected to be finalized during the 2nd half of 2014 • Effective date

- To be determined • Transition

- Cumulative-effect adjustment to the statement of financial position as of the beginning of the first reporting period in which the guidance is effective

- No early adoption

50 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

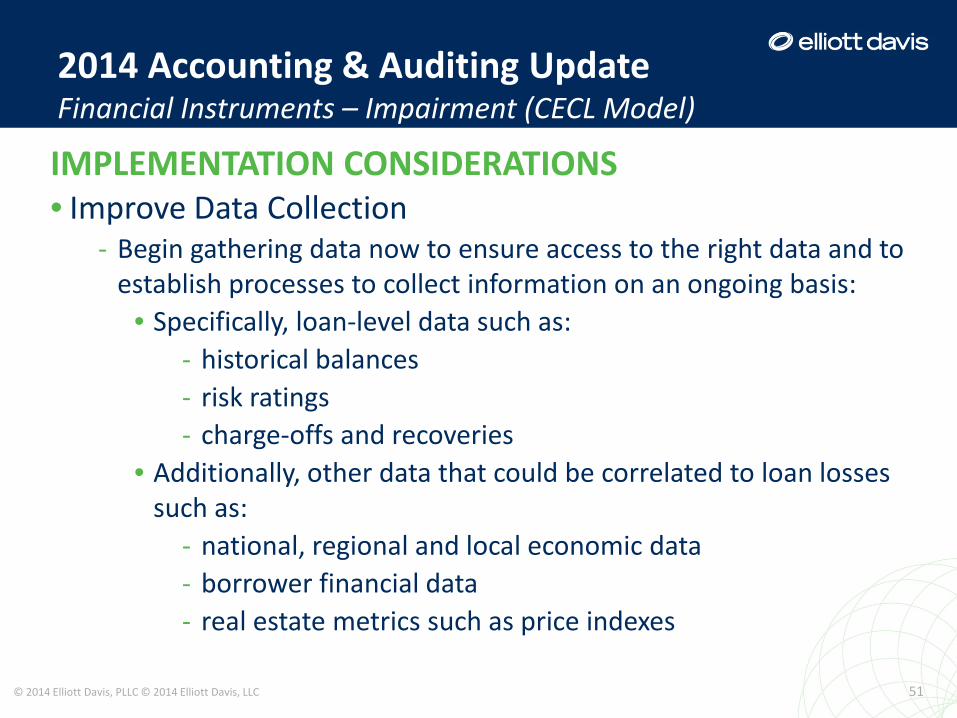

IMPLEMENTATION CONSIDERATIONS • Improve Data Collection

- Begin gathering data now to ensure access to the right data and to establish processes to collect information on an ongoing basis:

• Specifically, loan-level data such as: - historical balances - risk ratings - charge-offs and recoveries

• Additionally, other data that could be correlated to loan losses such as:

- national, regional and local economic data - borrower financial data - real estate metrics such as price indexes

51 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

2014 Accounting & Auditing Update Financial Instruments – Impairment (CECL Model)

IMPLEMENTATION CONSIDERATIONS • Begin Planning for Potential Impact on Capital Levels

- Most analysts and bankers believe that the CECL model will increase an institution’s allowance reserve.

- If this is correct, this will require a one-time capital adjustment.

- Institutions should take proactive steps to increase capital in advance of the changes

52 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Questions?

53 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Contact Information

54 © 2014 Elliott Davis, PLLC © 2014 Elliott Davis, LLC

Lee Haynes Email: [email protected] Phone: 704.808.5208 Website: www.elliottdavis.com

Elliott Davis, LLC/PLLC is one of the largest accounting, tax and consulting services firms in the Southeast and ranks among the top 50 CPA firms in the U.S. With offices in SC, NC, GA and VA, the firm provides clients across a wide range of industries with smart, customized solutions and its people with rewarding opportunities. Founded in 1925, Elliott Davis is a member of The Leading Edge Alliance, an international professional association of independently owned accounting firms based in the U.S. and is strategically aligned with LEA Europe and LEA Asia Pacific, a worldwide network of more than 450 offices in 100 countries around the globe. For more information about Elliott Davis and its services, visit http://www.elliottdavis.com.