Access to Services and the Value Chain in Food Production ... · in Food Production and...

30

Access to Services and the Value Chain in Food Production and Distribution FOOD SECURITY WORKSHOP MEDAN, INDONESIA 27 JUNE 2013 SHERRY STEPHENSON – PECC AND SENIOR FELLOW, ICTSD

Transcript of Access to Services and the Value Chain in Food Production ... · in Food Production and...

Access to Services

and the Value Chain

in Food Production

and Distribution

FOOD SECURITY WORKSHOP MEDAN, INDONESIA 27 JUNE 2013

SHERRY STEPHENSON – PECC AND

SENIOR FELLOW, ICTSD

Food Security

“Food security exists when all people, at all times, have

physical and economic access to sufficient, safe and nutritious

food that meets their dietary needs and food preferences for

an active and healthy life”.

(World Food Summit, 1996)

4 dimensions of food security:

Food Availability

Food Access

Utilization

Stability

Farming-related services; food

engineering to ensure the proper quality

Logistics and Distributional Services

Adequate diet, clean water, sanitation

and health care

Referring to both access and utilization

S

E

R

V

I

C

E

S

New context for Trade: Intermediate

Goods and GVCs lead International Trade Flows

► “Made in the World” (WTO-JETRO 2011 Report ): Not one country but many countries involved in producing a single good

► New pattern of Trade Global Value Chain (GVC), also affecting food production and distribution

► As a consequence, transport services have increased…

Logistics Costs are more and more

important and constitute a key

factor in competitiveness

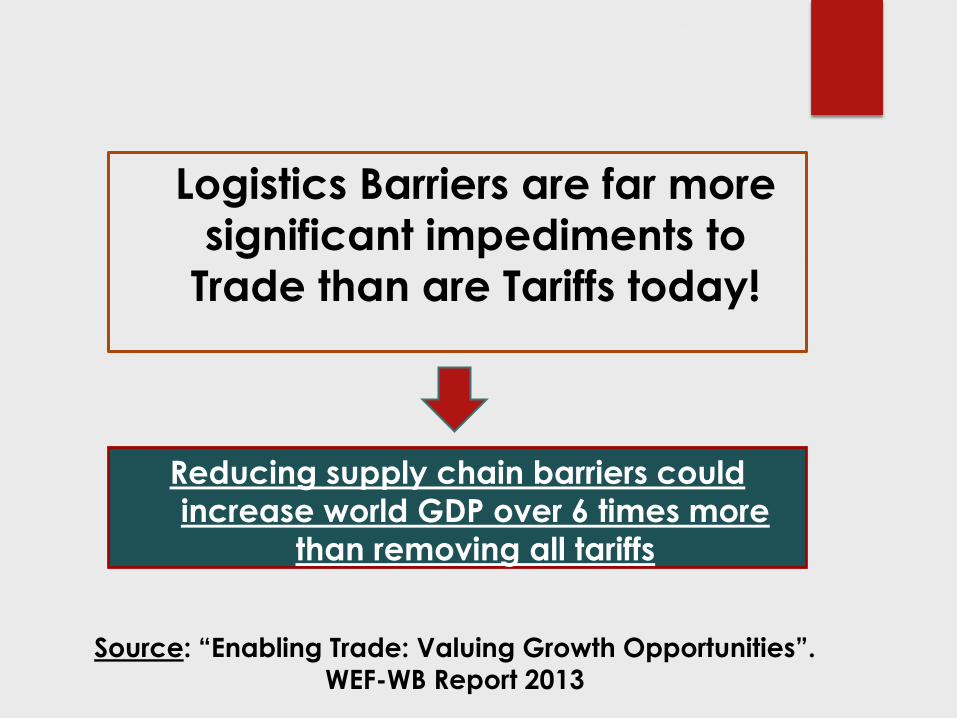

Logistics Barriers are far more

significant impediments to

Trade than are Tariffs today!

Reducing supply chain barriers could

increase world GDP over 6 times more

than removing all tariffs

Source: “Enabling Trade: Valuing Growth Opportunities”. WEF-WB Report 2013

What are the main impediments to

Trade today? Policy makers should focus

on: SUPPLY CHAIN BARRIERS

► Today, the biggest deterrents to trade are the lack

of infrastructure, border policies, efficient services and institutions that create obstacles to the

movement of goods

► 4 main issue areas affecting supply chains before

and after the border (WEF Global Enabling Trade

Report 2012)

► Market Access

► Border Administration

► Telecommunications and Transportation

Infrastructure (SERVICES)

► Business Environment

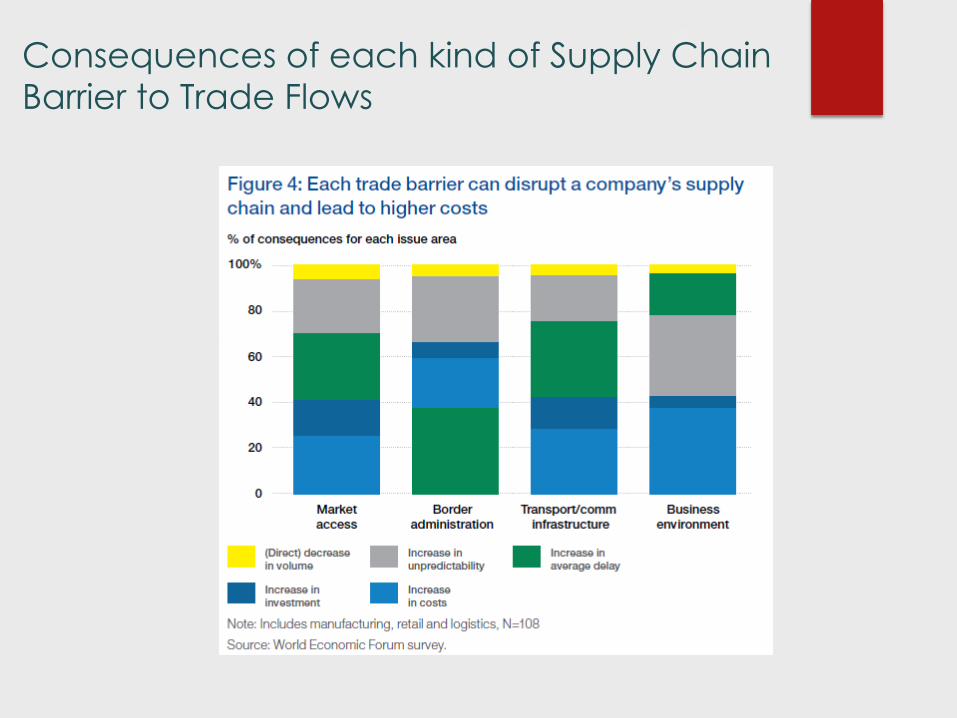

Supply Chain Barriers to Trade

Consequences of Supply Chain Barriers

Supply chain barriers weigh on a business or farmers engaging in trade in 4 direct ways:

► Add to costs - in terms of higher operating costs and increased capital expenditures

► Worsen the delays faced by business in making shipments less predictable or longer

► Reduce volume of trade activity

► Increase risk

► A BIG PART OF FOOD SECURITY IS GETTING BETTER, MORE SECURE AND TIMELY ACCESS FOR CONSUMERS TO FOOD THROUGH IMPROVING THE OPERATION OF SUPPLY CHAINS

Consequences of each kind of Supply Chain

Barrier to Trade Flows

How do firms deal with Supply Chain Barriers to their Trade?

► A company/ farmer’s experience will vary by

the specific barrier encountered and the actions taken in response

► Example: A company/farmer that must contend

with frequent truck breakdowns resulting from

badly maintained roads (poor transportation

infrastructure) might:

► accept a higher average delay in shipments; or

► purchase additional trucks, thereby increasing capital

expenditure;

► BOTH RESPONSES INCREASE COSTS

How do firms deal with Supply Chain Barriers to their Trade?

► For instance, transportation delays will be more

harmful to a company / farmer that sells fresh fish

than to one that sells canned tuna.

► Whatever response will necessarily increase costs and

be reflected in input higher prices to other producers

using the product and passed on to consumers, or

passed on directly in higher final prices.

Operational Priorities Industry Characteristics

What defines how an individual company responds to a

barrier to trade?

Growth of GDP and Trade to be derived

from reducing Supply Chain Barriers

Two key

components of

supply chain behind

these calculations:

1. BORDER

ADMINISTRATION

2. TRANSPORT AND

COMMUNICATIONS

INFRASTRUCTURE

(SERVICES)

Source: “Enabling Trade: Valuing Growth Opportunities”. WEF-WB Report, 2013

Why does lowering Supply Chain

Barriers produce such large gains?

► Because it eliminates resource waste, whereas

abolishing tariffs mainly reallocates resources.

► Moreover, the gains from reducing barriers are

more evenly distributed among nations than the

gains from eliminating tariffs, reducing inequality

worldwide.

Source: “Enabling Trade: Valuing Growth Opportunities”. WEF Report, 2013

Distribution of the Gains to Trade and GDP

from REDUCTION OF LOGISTICS BARRIERS

► Gains in GDP associated with trade facilitation would

take place in all regions, though they would be

concentrated in those with the greatest improvements.

► These regions would include sub-Saharan Africa, South

Asia, parts of Central and West Asia, as well as other

developing regions.

Economic gains from barrier reductions are

more evenly distributed across countries than

the gains associated with tariff elimination

Implications by Region

(under the ambitious scenario)

Source: “Enabling Trade: Valuing Growth Opportunities”. WEF Report, 2013

Increase in GDP (%) by Region from reduction

of Logistics Barriers to Trade: SE Asia benefits

more than any region but Africa

Who are the main beneficiaries from reduction

in LOGISTICS COSTS TO TRADE?

► Reducing supply chain barriers lowers costs and hence lowers prices,

both for consumers and for firms that use these inputs.

► Consumers gain access to a wider variety of goods

► Workers benefit also – should stimulate employment growth.

► In the long run, this promotes a shift in resources to more productive

industries and firms, thereby increasing productivity and wages.

Reducing supply chain barriers also makes

locations more attractive for off-shoring

investment.

Source: “Enabling Trade: Valuing Growth Opportunities”. WEF Report, 2013

Case Studies FOOD OPERATIONS USING SUPPLY CHAINS

o Poor infrastructure and logistics hobble operations

► Ports operate beyond capacity result in delays

► Lagging telecommunications infrastructure makes it difficult to track containers, rendering operations and planning

cumbersome and time consuming. Sometimes ships depart

half-empty since the containers are “lost” within the system.

► Weak road and rail infrastructure make it difficult to reach

many inland markets. In order to reach some markets CPG

Co. must set up additional regional plants to cover the

geography must carry excess inventories at each point of

the supply chain.

► Risk and uncertainty from poor logistics impact on ability of

CPG Co. to arrange financing which sometimes leads to

interrupted selling operations

Case Study I: CPG - Consumer

Packaged-Goods Producer

operating in Africa

Case Study II: Hugo Restrepo y Cía –

chili pepper paste provider for Tabasco

► Hugo Restrepo y Cía – Colombian enterprise and the main provider of chili pepper paste for Tabasco Leading worldwide hot sauce brand

► Hugo Restrepo y Cía organizes farmers located in the Colombian southwest to grow the chili pepper required by Tabasco, which it then processes, packages and sends abroad, through a supply chain

► Hugo Restrepo y Cia frequently outsources the production of chili pepper paste. This outsourcing often takes place across borders, because crop locations respond to climate and soil conditions.

Source: IDB (2012) International Product Fragmentation and the Insertion of Latin America and the Caribbean in Global

Production Networks. Colombian Case Studies

Chili Paste Value Chain

Chili pepper

production

Chili paste

production

Packing &

storage Hot sauce

production

Distribution &

marketing Inputs

Seeds

Fertilizers

Agrochemical

s (Herbicides,

fungicides & pesticides)

Farm

equipment

Irrigation

equipment

Chili

peppers:

Tabasco

Cayenne

Habanero

Chipotle

Jalapeño

Others

Chili pepper

paste

Brine

Barrel Bottles of

different hot

sauce recipes Containers

ACTIVITIES

ACTORS

PRODUCTS

Producers Processors Traders Producer

firms

Inputs

suppliers

Supermarkets

Food services

Wholesalers

Retailers

Bottles of

different hot

sauce recipes

Source: IDB (2012) International Product Fragmentation and the Insertion of Latin America and the

Caribbean in Global Production Networks. Colombian Case Studies

Case Study II: Hugo Restrepo y Cía –

chili pepper paste provider for Tabasco

Hugo Restrepo

involved in…

Hugo Restrepo

does not own

lands of crops -

link to small

farmers bound

by contractual

agreements

43%

5%

22%

30%

Breakdown of the costs of chili pepper

paste sold in the international market

Agricultural input

Stock-up and

Processing Costs

Packaging and

Storage

International

Logistics

Case Study II: Hugo Restrepo y Cía –

chili pepper paste provider for Tabasco

57% correspond to the stages in

which the firm is directly involved: - stock-up and

processing costs (5%);

- packaging and storage (22%);

- international logistics

(30%).

Logistics account for 1/3 of final costs of

product sold in international market.

► Alimentos SAS A fruit-pulp producer with more

than 350 active customers; participation in the

global market as exporter of tropical fruit pulps

naturally concentrated, and frozen cut fruit.

► Products made by Alimentos SAS fruit pulp, whole

and cut frozen fruit, and fruit juices. Produced and

sold through a supply chain, with exports accounting

for 26%.

► Firm’s customers food chain stores and business or

institutional clients around the world (fast food chain

restaurants, hotels, restaurants, educational

institutions, and hospitals).

Case Study III: Alimentos SAS – fruit-pulp

producer taking part in international market

Fruit pulp value chain

Transport &

distribution

Extraction

of pulp

Freezing/

pasteurization

Product

preparation

Distribution &

marketing

Fruit crops and

harvesting

Fruits Fruits Fruit pulp

Cut fruit

Frozen fruit

pulp

Preserves

Beverages

ACTIVITIES

ACTORS

PRODUCTS

Transporters Processors Firms Farmers

Supermarkets

Food services

Wholesalers

Retailers

Fruit pulp (different

presentations)

Industrial

firms

Sugar

confectionery

Other fruit

products

Pasteurized

fruit pulp

Case Study III: Alimentos SAS – fruit-pulp

producer taking part in international market

The firm and its linkages

► Products delivered to final customers in Bogotá or elsewhere.

Transport is outsourced from independent transporters. ► Alimentos has had a long-term contract with an offshoring client

in the supply chain – Matosantos - the marketer providing fruit-

pulp for juices in Puerto Rico.

► Matosantos terminated its contract with Alimentos SAS and

replaced firm with a Costa Rican supplier able to offer the

product at a better price due to better logistics, distribution and refrigerating services. Why? stated need to maintain

competitive position in the supply chain; logistics components of

Alimentos production had become too expensive

Case Study III: Alimentos SAS – fruit-pulp

producer taking part in international market

Case IV: Transport Costs –

Chickens in Indonesia

Source: “Indonesia’s Poultry Value Chain. Costs, Margins, Prices, and Other Issues”. Nathan

Associates Inc and USAID. (2013)

4.7% of the retail price for broilers Transport Costs

The highest cost

is for transport of imported raw

materials to get

from the port to

the mill

Why is this transport cost elevated?

► The high import component of Indonesian poultry

feed

► Inefficient port handling facilities (insufficient berths in

Jakarta)

► Excess demurrage due to slow turnaround of vessels

► Slow time for transport from port to mill requiring 2-4

times as many trucks to execute the process (with

associated over capitalization of the trucking sector)

High costs reflect inefficiencies in port and road infrastructure

Case IV: Transport Costs –

Chickens in Indonesia

Increased Total Factor Productivity derived

from liberalization in Services in Indonesia:

Comparison with Korea and Brazil

If Indonesia were to

match policies of these

service sector reform

champions, the

productivity gains for

Indonesian

manufacturing firms

would be over 5%, instead of the 3.5%

realized as results of current reforms

Source: Duggan, Rahardja, Varela. “Service Sector Reform and Manufacturing Productivity. Evidence

from Indonesia” (WB, 2013)

BUT – THERE IS MUCH MORE TO BE DONE TO

IMPROVE PRODUCTIVITY AND LOGISTICS

► Logistics costs in Indonesia are estimated

to be nearly double those in South Korea,

and nearly three times those in Japan

► Total factor productivity gains accrue

disproportionately to those firms that are relatively

more productive; those gains are directly linked to

the relaxation of restrictions in the transport and

electricity, gas, and water sectors.

(WB Study for Indonesia, 2013)

Source: Duggan, Rahardja, Varela. “Service Sector Reform and Manufacturing Productivity. Evidence from Indonesia” (WB, 2013)

Importance of non-food inputs

for better FOOD SECURITY

► Food production and distribution dependent upon SERVICES all along the value chain

► Especially IMPORTANT logistics and distributional services, as well as trade facilitation (E.g. extra cost at customs ; inefficient port handling; poor road or telecom systems)

► Key role of technology along Food GVCs can improve food security as well (E.g. specialized seeds / development of new methods to maintain fruit-pulp fresh / development of new packages in order to optimize logistics)

► Agriculture negotiations need to take better account of the important role of Services

Trade facilitation agreement at the WTO will contribute to

food security since many of the barriers that affect food

GVCs have to do with logistics and supply chain barriers