Access and Usage of Financial Services by MSMEs in Regions of Armenia

74

Access and Usage of Financial Services by MSMEs in Regions of Armenia Baseline Assessment Results 14 November, 2014 Economic Development and Research Center (EDRC)

-

Upload

armeniafed -

Category

Economy & Finance

-

view

133 -

download

1

Transcript of Access and Usage of Financial Services by MSMEs in Regions of Armenia

Access and Usage of Financial Services by

MSMEs in Regions of Armenia

Baseline Assessment Results

14 November, 2014

Economic Development and Research Center (EDRC)

2

AGENDA

11

22

33 Main Results

The Methodology

General overview of financial sector and Micro-Small and Medium Entrepreneurship in Armenia

• Usage of Financial Services and Business Financing

• Needs and Preferences

• Perceptions (Satisfaction, Confidence, Awareness, Literacy)

• Main Sources of Financial Information

• Financial Access

3

THE METHODOLOGY

4

OBJECTIVE AND SCOPE OF THE STUDY

The scope: Assessment of the awareness, literacy, confidence, needs, usage and access of

financial services

The target group: MSMEs operating in Marzes of Armenia with total personnel less than

100 employees.

The objective: to identify the pre-project (baseline) situation, periodically monitor the

progress and provide final evaluation.

Involves 3 stages:

Baseline Assessment (2013);

Mid-term Assessment and Evaluation (2015);

Final Evaluation (2016).

5

METHODOLOGY

Obtain comparable data - time series for 2013-2016,

Include both registered and non-registered enterprises,

Include all Marzes and sectors,

Reveal gender versus owner/director, and other relevant issues / features,

Country level representativeness (at 95% CL with maximum error margin of 5.5%).

Major Requirements

6

METHODOLOGY

Desk reviews;

Participatory rapid appraisals (PRAs), in particular, Key informant interviews (KII);

Enterprises sample survey:

Sample survey of MSMEs (registered enterprises)

Sample survey of Farms (non-registered enterprises)

Research methods

7

METHODOLOGY

Two-stage stratified random sampling;

Separate study of MSMEs and Farms;

Regional coverage: all Marzes, 105 settlements (55 and 50 villages);

Actual sample size: 724 enterprises;

Non-response rate of 50%.

Sample design

8

METHODOLOGY

Structure of the Questionnaire:

Section 1. Business description/general information

Section 2. Bank accounts and transactions

Section 3. Business financing

Section 4. Sources of financial information

200 primary variables for each enterprise

Mainly quantitative, as well as qualitative data

Research instruments

9

Financial sector and MSMEs in Armenia: general overview

10

GENERAL OVERVIEW OF FINANCIAL SECTOR

The financial sector is one of the fast growing sectors with high-income yields.

Value added in the financial sector is equivalent to 4.5% of the GDP.

Labor productivity and salary levels are the highest in this sector.

The banking system is the largest player in the Armenian financial sector. As of the beginning 2013, 89.7% of financial sector assets belonged to the banking.

Concentration indicator of the Armenian banking sector is relatively high.

The level of financial intermediation and depth is behind Eastern European countries.

During 2008-2012, volumes of both loans extended and deposits attracted by commercial banks increased by about 2.5 times.

The number of plastic cards also grows along with number and volumes of non-cash payments.

The non-bank financial sector continues to remain underdeveloped. The securities market is very small.

11

GENERAL OVERVIEW OF FINANCIAL SECTOR

Indicators describing the Armenian financial system

Beginning 2004

Beginning 2008

Beginning 2013

Number of commercial banks 20 22 21 Sub-branches of commercial banks 232 347 474Credit organizations 6 21 32 Sub-branches credit organizations 1 40 102Investment companies - 15 9Insurance companies - 9 9Pawn shops - 63 103Accountable issuers - 16 14Foreign exchange trade offices 284 250 226Money transfer operators 0 7 6

Source: CBA and EDRC calculations

12

GENERAL OVERVIEW OF FINANCIAL SECTOR

Indicators describing the payment system

2008 2012 2012/2008Number of ATMs 538 1170 2.17Number of POS-terminals 2,280 6,674 2.93Number of cards in circulation 454,357 1,322,949 2.91Number of card transactions in the territory of Armenia 6,586,134 18,867,715 2.86Volumes of card transactions in the territory of Armenia, AMD mln

326,371 999,771 3.06

Number of bank transfers through non-cash payment systems

5,043,571 14,350,895 2.85

Volumes of bank transfers through non-cash payment systems, AMD mln

15,135,666 29,836,587 1.97

Source: CBA and EDRC calculations

13

Source: State Revenue Committee of RA and EDRC calculations

THE ENTREPRENEURSHIP IN ARMENIANumber of enterprises operating in Armenia

14

ENTREPRENEURSHIP IN ARMENIASize of enterprises based on number of employees

Up to 10 11-100More than

100Total

Total 92.3 6.9 0.8 100

Yerevan 91.1 7.8 1.1 100

Marz 93.7 5.9 0.4 100

Source: State Revenue Committee of RA and EDRC calculations

15

MICRO-SMALL AND MEDIUM ENTREPRENEURSHIP IN ARMENIAMSMEs in Marzes per legal status

Source: State Revenue Committee of RA and EDRC calculations

16

MICRO-SMALL AND MEDIUM ENTREPRENEURSHIP IN ARMENIA

Source: State Revenue Committee of RA and EDRC calculations

Distribution of MSMEs per Marzes

17

MICRO-SMALL AND MEDIUM ENTREPRENEURSHIP IN ARMENIA

Source: State Revenue Committee of RA and EDRC calculations

Distribution of MSMEs per sectors

18

OVERVIEW OF MSMEs and AGRICULTURAL FARMS

SP LP Total

Manufacturing 13.5 32.9 17.9

Food industry 8.4 20.5 11.1

Other productions 5.2 12.3 6.8

Trade 73.7 46.6 67.6

Other Services 12.7 20.5 14.5

Total 100.0 100.0 100.0

Female Male Total

Manufacturing 25.9 74.1 100.0

Food industry 36.1 63.9 100.0

Other productions 9.1 90.9 100.0

Trade 36.2 63.8 100.0

Other Services 42.9 57.1 100.0

Total 38.9 61.1 100.0

Source: MSMEs Baseline Survey 2013, EDRC

Sectors of MSME activities ,%

19

OVERVIEW OF MSMEs and AGRICULTURAL FARMS

Source: Agricultural Farms Baseline Survey 2013, EDRC

Breakdown of Farms per sectors of activities and agricultural production, %

20

USAGE OF FINANCIAL SERVICES

21

USAGE OF FINANCIAL SERVICESNumber of bank accounts. MSMEs

SP LP Total

Availability of bank accounts in AMD 100.0 100.0 100.0

Have one account 71.7 61.6 69.4

Have two or more accounts 4.8 38.4 12.3

Do not have accounts 23.5 0.0 18.2

Availability of bank accounts in foreign currencies 100.0 100.0 100.0

Have one accounts 10.0 24.7 13.3

Do not have accounts 90.0 75.3 86.7

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

22

USAGE OF FINANCIAL SERVICESNumber of bank accounts. Agricultural farms

As % in total agricultural farmsAs share in agricultural farms

with bank accounts

Have accounts 38.5 100.0

Have 1 account 26.3 68.2

Have 2 accounts 8.7 22.7

Have 3 and more accounts 3.5 9.1

No accounts 61.5 -

Total 100.0 -

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

23

USAGE OF FINANCIAL SERVICESNumbers of transactions. MSMEs

SP LP Total

Do not use 4.7 0.0 3.4

1 service 17.1 6.8 14.8

2 services 28.7 28.8 28.7

3 services 19.1 11.0 17.3

4 services 8.0 20.5 10.8

5 and more services 0.0 32.9 7.4

Total 100 100 100

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

24

USAGE OF FINANCIAL SERVICESNumbers of transactions. Agricultural farms

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

79 percent of Agricultural farms used some type of bank services:

25

USAGE OF FINANCIAL SERVICESBank transactions. MSMEs

Source: MSMEs Baseline Survey 2013, EDRC

SP LP Total

Tax payments 39.4 82.2 49.1

Loan service 43.4 50.7 45.1

Encashment 31.9 60.3 38.3

Purchase of goods and services 19.1 58.9 28.1

Utility and communication services 21.5 45.2 26.9

Sale of goods and services 8.4 49.3 17.6

Salary payments 0.0 13.7 3.1

26

USAGE OF FINANCIAL SERVICESBank transactions. Agricultural farms

Agricultural farms that use bank

transactionsAgricultural farms that have bank

accounts

Share in total agricultural farms

Share in the respective group

Share in total agricultural farms

Share in the respective group

Loan service 45.8 57.5 23.0 59.7

Money transfers from abroad 30.5 38.4 10.5 27.3

Salaries, pensions, benefits 20.5 25.8 18.5 48.1

Utility/communication service payments 18.8 23.6 9.5 24.7

Taxes, stamp duties, mandatory payments 8.3 10.4 4.8 12.3

Other payments related with agricultural activity

4.5 5.72.0 5.2

Receipt for sales of their harvest 4.0 5.0 2.5 6.5

Total (using at least one service) 79.5 100 38.5 100Source: MSMEs Baseline Survey 2013, EDRC

27

USAGE OF FINANCIAL SERVICES

MSMEsAgricultural

farms

No necessity, no need 66.0 73.3

Did not have occasion, not used to 46.0 40.3

Our partners do not agree 10.3 0.3

Processes are to complex 9.8 2.3

Tariffs and commission fees are high 8.9 5.0

Do not trust banks, not safe 6.2 6.8

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Main reasons for not using bank transfers, %

28

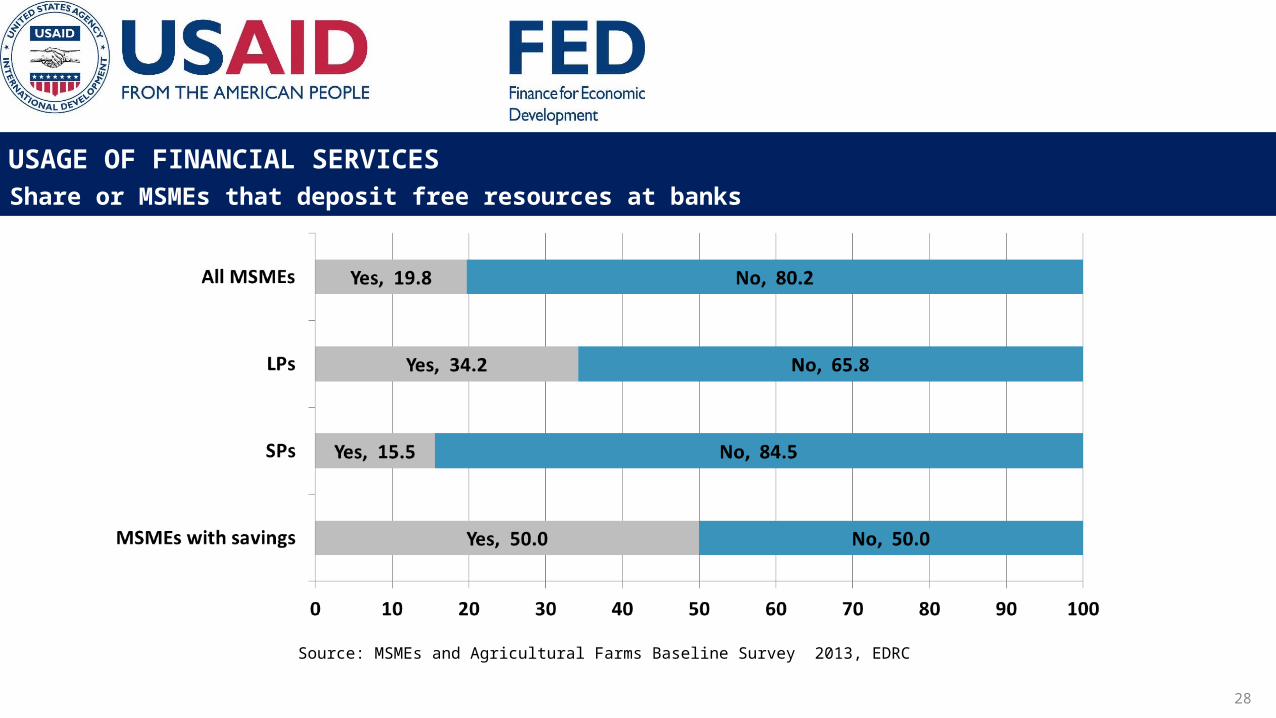

USAGE OF FINANCIAL SERVICESShare or MSMEs that deposit free resources at banks

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

29

USAGE OF FINANCIAL SERVICESShare or MSMEs that deposit free resources at banks

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

MSMEsAgricultural

farms

Do not trust banks, not safe 26.9 26.0

No necessity, no need 58.1 14.8

Did not have occasion, not used to 27.7 3.8

Proposed interest rates (income) is low 21.5 1.3

Never had free resources 75.4 65.5

% in total for each group

30

USAGE OF FINANCIAL SERVICESMain sources for business financing and investment

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

MSMEs

31

USAGE OF FINANCIAL SERVICESMSMEs with debt liabilities

Source: MSMEs Baseline Survey 2013, EDRC

32

USAGE OF FINANCIAL SERVICES

Source: Agricultural Farms Baseline Survey 2013, EDRC

Agricultural farms with debt liabilities

38 percent of all agricultural farms have some type of debt liability:

33

USAGE OF FINANCIAL SERVICES

MSMEs Agricultural Farms

Interest rate For bank loansFor credit

organizations

Interest rate

For bank loans

For credit organization

s Less than 10% 5 -

10-12% 31.5 11.1 10-12% 21.8 5.113-14% 13.3 11.1 13-14% 23.8 7.715-17% 21.0 11.1 15-17% 13.9 2.618-20% 21.0 22.2 18-20% 21.8 20.521-24% 13.3 40.7 21-25% 13.9 64.1

Above 25% - 3.7 Average annual

interest rate 15.3% 19.0%

15.6% 21.3%

Average size of loans 4,4 mln 1.05 mlnSource: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Distribution of loans per interest rates

34

USAGE OF FINANCIAL SERVICESBreakdown of loans per type of collateral. MSMEs

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

29 percent of MSMEs borrowed from banks and credit organizations without collateral.

35

USAGE OF FINANCIAL SERVICESBreakdown of loans per type of collateral. Agricultural farms

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

16.5 percent of Agricultural farms borrowed from banks and credit organizations without collateral.

36

USAGE OF FINANCIAL SERVICESInvestment directions broken down per MSMEs that borrowed from banks or did not

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Yes No Total

Real estate acquisition 9.6 9.5 9.6

Capital construction and renovation 44.1 26.5 36.1

Investments in mobile property 25.4 21.8 23.8Purchase, renovation and modernization of devices and equipment

40.1 35.4 38.0

Expansion of current activities 84.7 86.4 85.5Testing and introduction of new products, activities or technologies

7.9 9.5 8.6

Employee Trainings 0.0 2.7 1.2

Repayment of debt 24.9 15.0 20.4

Real estate acquisition 100 100 100

37

USAGE OF FINANCIAL SERVICESUses of loans of Agricultural farms

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

38

NEEDS AND PREFERENCES

39

NEEDS AND PREFERENCESEstimates in case of additional financing

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

40

NEEDS AND PREFERENCESBehavior in case of need for finance or investments

MSMEs Agricultural farms

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

41

NEEDS AND PREFERENCESNeed of additional investments

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Agricultural farms

42

NEEDS AND PREFERENCESDirections of planned investments

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

MSMEs Agricultural farms

43

NEEDS AND PREFERENCESWillingness to borrow on market terms

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Agricultural farmsMSMEs

44

NEEDS AND PREFERENCESWillingness to borrow on market terms for MSMEs and Agricultural farms that plan or need investments

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

45

NEEDS AND PREFERENCES

Reasons for refusing the loans at current market terms. MSMEs

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

46

NEEDS AND PREFERENCES

Reasons for refusing the loans at current market terms. Agricultural farms

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

47

PERCEPTION OF FINANCIAL INSTITUTIONS AND SERVICES

SATISFACTION, CONFIDENCE, AWARENESS, LITERACY

48

SATISFACTIONSatisfaction of MSMEs from banks servicing their accounts

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

49

SATISFACTIONReasons for dissatisfaction from bank account servicing or current transactions

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

50

SATISFACTIONSatisfaction from loans or other debt liabilities

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

51

SATISFACTIONReasons for dissatisfaction or complaints from loans or other debt liabilities among MSMEs and agricultural farms

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

52

CONFIDENCEDistrust in bank deposits and credits

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

53

CONFIDENCEDistrust in borrowing from financial institutions

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

54

AWARENESSAwareness on bank deposit terms and conditions

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

55

AWARENESSAwareness on presented financing options

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

56

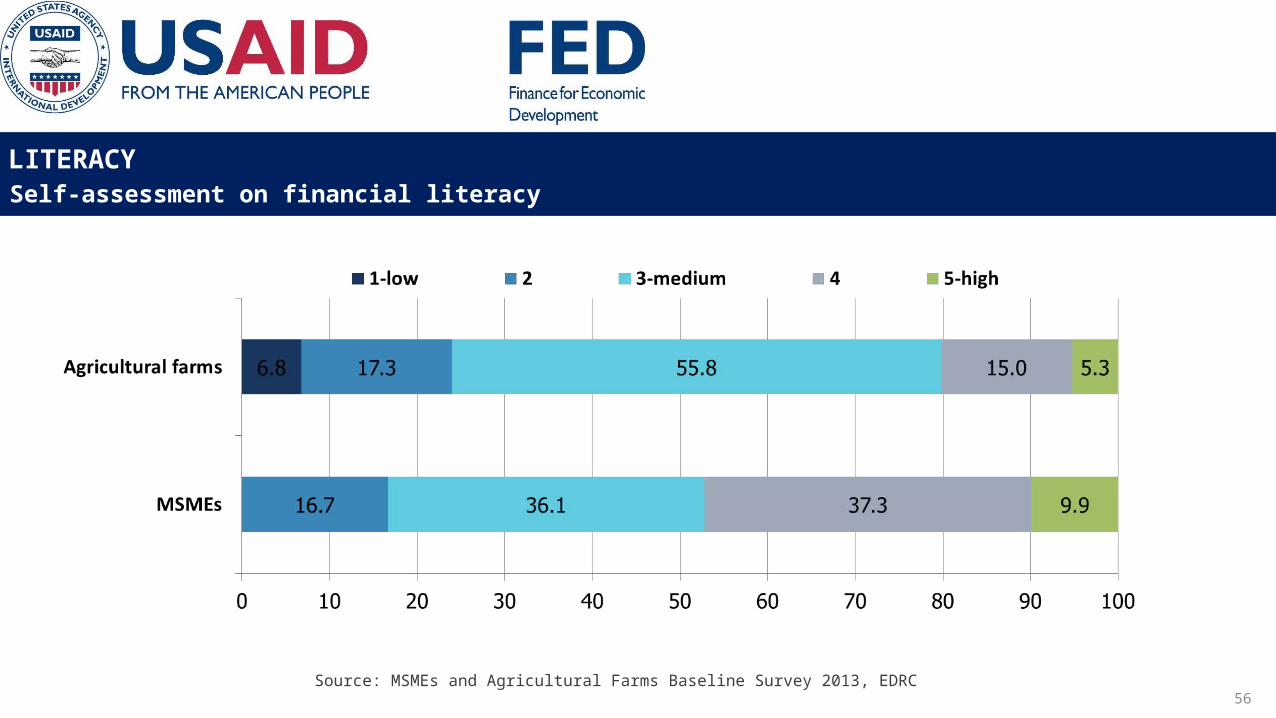

LITERACYSelf-assessment on financial literacy

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

57

LITERACYWillingness to improve financial literacy

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

58

MAIN SOURCES OF FINANCIAL INFORMATION

59

MAIN SOURCES OF FINANCIAL INFORMATION Satisfaction with available information

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

60

MAIN SOURCES OF FINANCIAL INFORMATION Willingness to receive financial information regularly

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

61

MAIN SOURCES OF FINANCIAL INFORMATION Preferred sources to receive financial information

MSMEs* Agricultural farms*

TV 59.6 62.1

Internet 56.3 28.0

Radio or press 15.8 3.1

SMS 49.2 27.3

Printed materials/booklets 17.5 26.1

*- of those who are willing to regularly receive information

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

62

MAIN SOURCES OF FINANCIAL INFORMATION Preferred information types

MSMEs Agricultural farms

On loans 97.3 94.4

On deposits 39.9 18.6

Account service and bank transfers 51.4 13.7

On securities 13.1 6.2

On other financial tools and transactions 6.0 0.6

*- of those who are willing to regularly receive information

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

63

ASSESSMENT OF FINANCIAL ACCESS

64

ASSESSMENT OF FINANCIAL ACCESSFinancial inclusion

“Overall” financial inclusion

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

65

ASSESSMENT OF FINANCIAL ACCESSFinancial inclusion

“Comparatively deep” financial inclusion

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

66

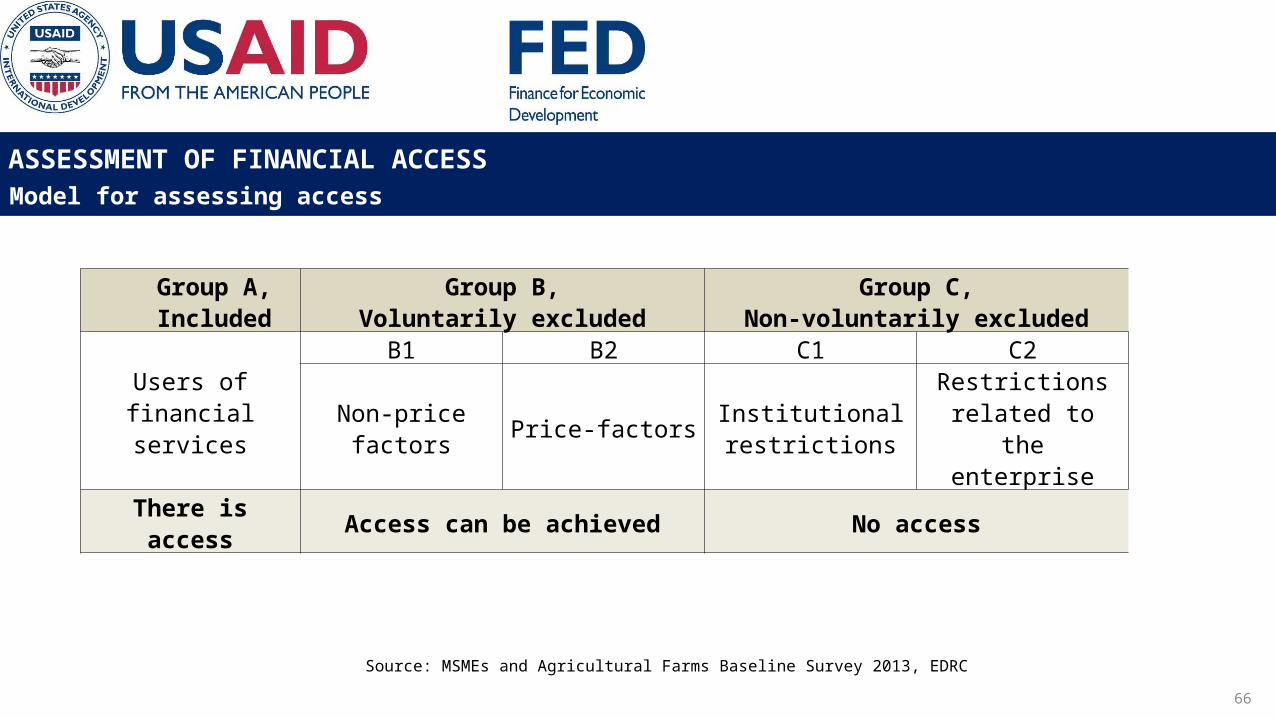

ASSESSMENT OF FINANCIAL ACCESSModel for assessing access

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Group A,Included

Group B,Voluntarily excluded

Group C,Non-voluntarily excluded

Users of financial services

B1 B2 C1 C2

Non-price factors Price-factorsInstitutional restrictions

Restrictions related to the enterprise

There is access Access can be achieved No access

67

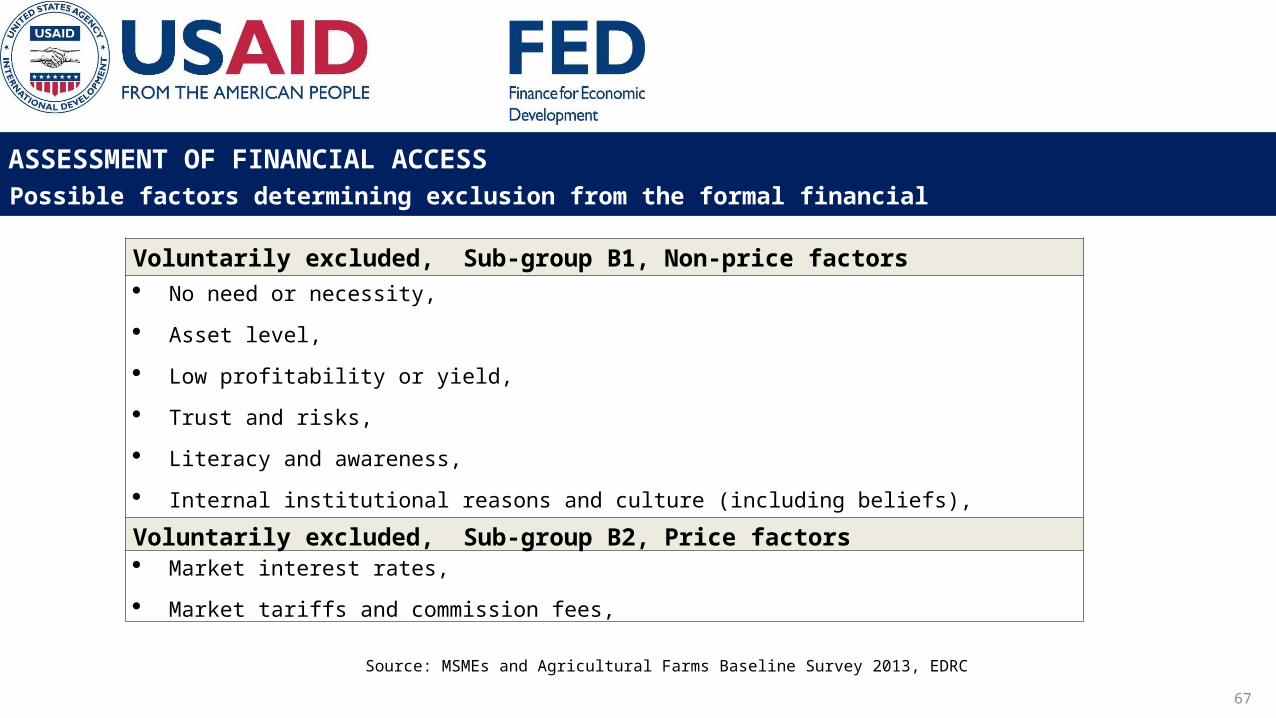

ASSESSMENT OF FINANCIAL ACCESSPossible factors determining exclusion from the formal financial system

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Voluntarily excluded, Sub-group B1, Non-price factors No need or necessity,

Asset level,

Low profitability or yield,

Trust and risks,

Literacy and awareness,

Internal institutional reasons and culture (including beliefs),

Voluntarily excluded, Sub-group B2, Price factors Market interest rates,

Market tariffs and commission fees,

68

ASSESSMENT OF FINANCIAL ACCESSPossible factors determining exclusion from the formal financial system

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

Non-voluntarily excluded, Sub-group C1, Institutional obstacles or obstacles related to the product Physical, geographical restrictions,

Activity sector,

Restrictions related to the availability or adequacy of services,

Tariff restrictions (non-market conditions),

Non-voluntarily excluded, Sub-group C2, Restrictions related to enterprise characteristics Assets, income, turnover, number of employees, expertise etc.

69

ASSESSMENT OF FINANCIAL ACCESSFinancial inclusion - bank transactions

Source: MSMEs and Agricultural Farms Baseline Survey 2013, EDRC

70

ASSESSMENT OF FINANCIAL ACCESSCategorization of non-inclusion reasons in savings accounts and deposit transactions

MSMEs

Agricultural farms

Voluntary non-inclusion Price factors

Proposed interest rate (income) is low 21.5 1.3Tariffs and commission fees are high 2.7 0.5

Non-price factorsNo free resources/savings 75.4 69.7Non necessity or need 58.1 15.7There was no occasion or not used to 27.7 4Do not trust bank, not safe 26.9 27.7Not aware 1.9 9.6Terms and conditions are not acceptable 6.9 1.3Partners or other HH members do not agree 0.8 3.2

Non-voluntary exclusionBank is too far, physically inconvenient 1.9 0.5Processes are too complex 2.3 0.3

71

ASSESSMENT OF FINANCIAL ACCESSEstimates of ease of borrowing from banks and credit organizations

72

ASSESSMENT OF FINANCIAL ACCESSInclusion of MSMEs and agricultural farms per loans

73

ASSESSMENT OF FINANCIAL ACCESSCategorization of main factors determining non-inclusion

MSMEs

Agricultural farms

Voluntary non-inclusionPrice factorsInterest rates, service fees are high 49.6 13.6

Non-price factorsRisky, do not trust 38.4 53.7Income is unstable 11.2 50No necessity, no need 8.8 3.3Process is too complex, difficult to collect all documents 8 0.5Have negative prior experience 0.8 4.2Beliefs - 1.9

Non-voluntary exclusionRequired documents 50 9.1Collateral requirement 35 25Loan terms (duration) 45 18.2Absence of financing or small volumes 7.5 25No guarantor - 4.5Age limitations - 2.3

74

THANK YOU

WWW.EDRC.AM

WWW.FACEBOOK.COM/EDRC.ARMENIA

WWW.ARMENIAFED.COM