Accenture Mobility - Trends for the Next Decade

44

Accenture Mobility Services Mobility – Trends for the Next Decade San Francisco, November 2011 Lars Kamp

-

Upload

lars-kamp -

Category

Technology

-

view

4.765 -

download

2

description

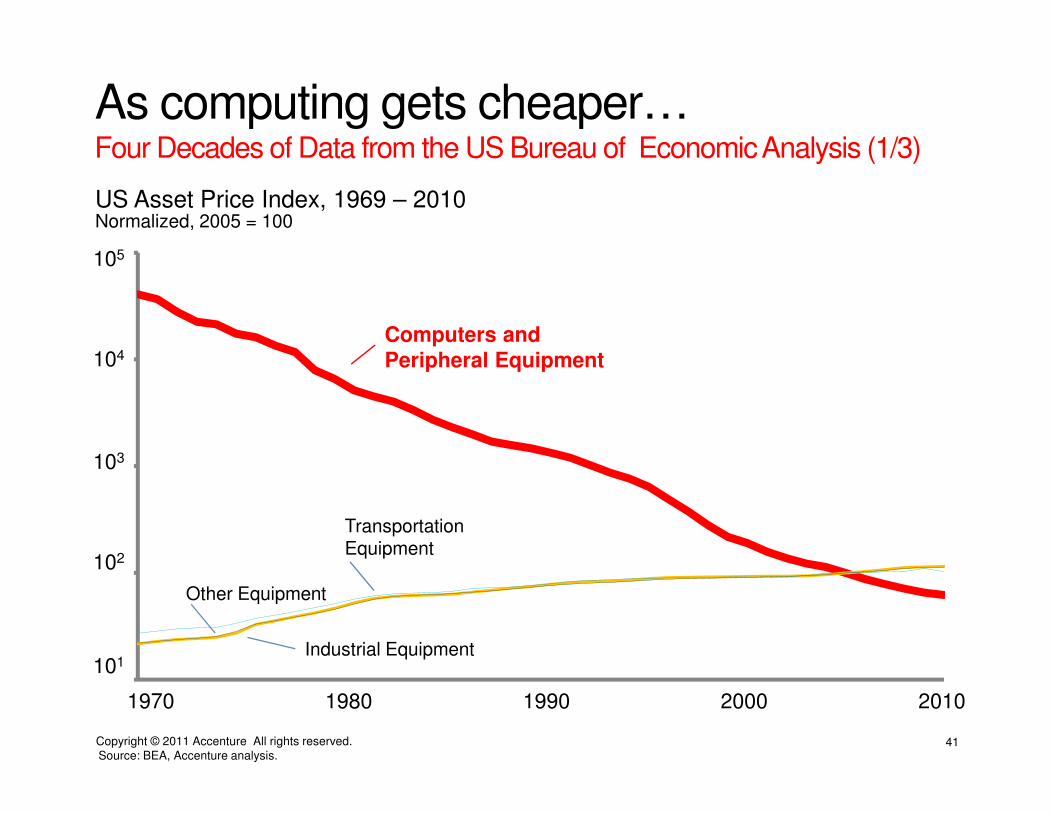

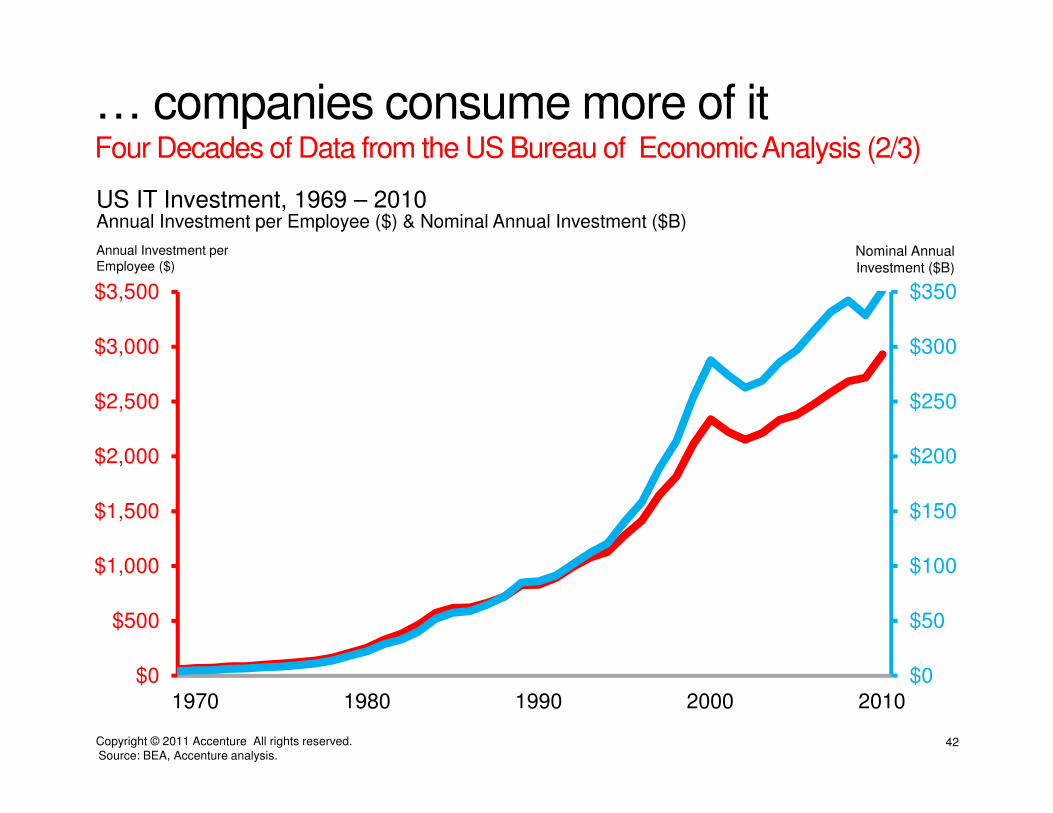

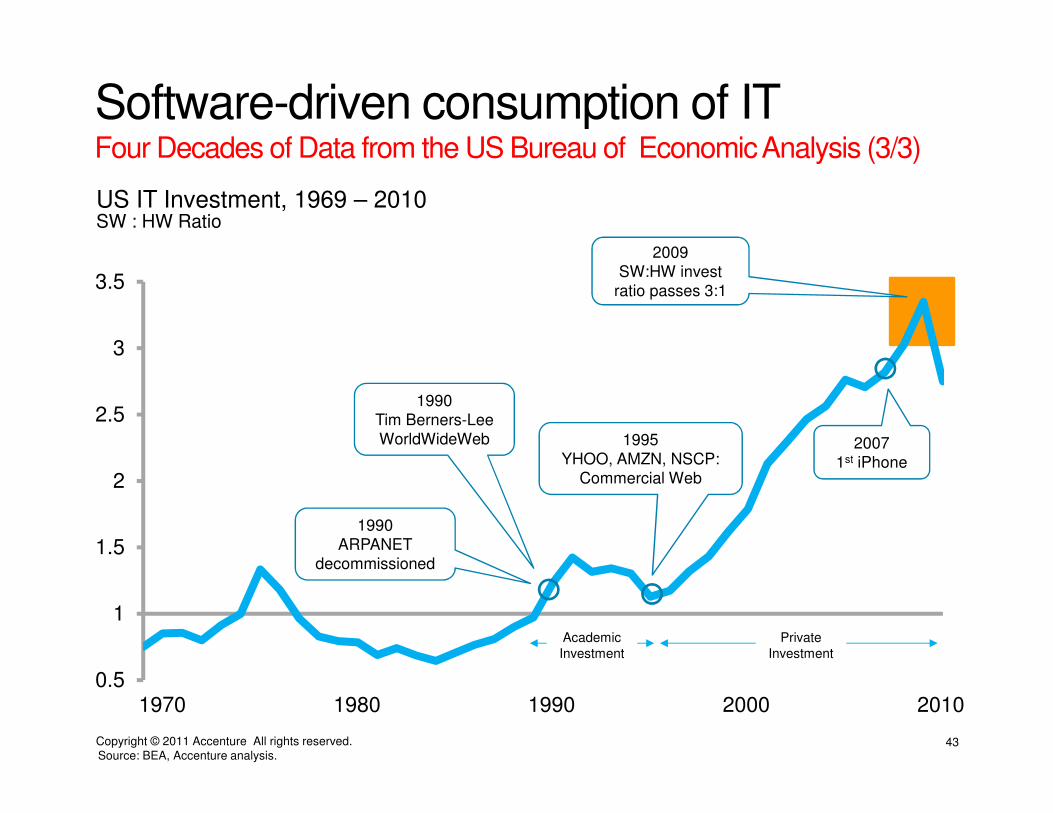

From a deck that I presented at the SIIA “All About Mobile” conference in November 2011 in San Francisco. It starts with the usual set of slides on the recent history of mobility (and I will keep presenting them until I see no more “I had no clue” faces in an audience), and then goes deeper into Moore’s Law and how we see it continuing for cell phones. An additional journey back in history to the early days of the industrialization and electricity. Companies had to generate their own power (by using wind, water, animals, etc.) and Burden’s Wheel is a good example of one big, giant monolithic effort to do so. Along came Tesla and Westinghouse, and the first power plant “Adam’s Plant” was able to provide about 3x the power, but over a much further distance, and to multiple customers. The concept of an electric utility was born, and what we saw happening was the fall of “enterprise power generation”. Fast forward to 1969, and Douglas Parkhill and John McCarthy came up with the concept of the “Computer Utility”. Today we see multi-$B investments into public cloud infrastructures. In very simple terms, if history in the utility industry is any indicator, we will see enterprise clouds disappear. And as cloud infrastructures scale and get more efficient, and the price of computing goes down (Moore’s Law), developers will find a way to use and instrument that computing power, and make it consumable to enterprises and consumers, which gets us to Jevons’ Paradox. Jevons observed how consumption of energy in England went up as coal power plants got more efficient. All the way to today where we keep the lights on in our homes 24/7, and darkness has actually become a scarce good in some metropolitan areas. Switching to enterprise computing and looking at BEA data on IT assets for the past four decades, we see that prices for IT assets are falling, whereas other assets follow an inflationary path. And as computing gets cheaper, enterprises consume more and more of it (and you can argue so do consumers, aka “Consumerization of IT”). What is striking that with the arrival of the public Internet in ‘90-95 and web companies like Yahoo and Amazon, the mix in consumption is shifting: it’s increasingly going towards software, up from a SW:HW ratio of roughly 1:1 over three decades, to now 3:1. So today, for every $1 spent on hardware, enterprises spend $3 on software. Hence, it seems like enterprises are making use of the public cloud, which would explain the rise of SaaS companies, such Salesforce, SuccessFactors and also Amazon’s AWS. And as the rise of smartphones is only beginning, enterprise mobility will likely drive the trend of an increasing SW:HW ratio further up. I wouldn’t be surprised to see the mix go to 10:1 in the next five years as smartphones proliferate and the amount of on-deck and off-deck computing power available to a single device is growing exponentially, the concept of “accelerated acceleratio

Transcript of Accenture Mobility - Trends for the Next Decade

Accenture Mobility Services

Mobility – Trends for the Next DecadeSan Francisco, November 2011

Lars Kamp

Copyright © 2011 Accenture All rights reserved. 2

Contact

Lars Kamp

Suite 1200560 Mission StreetSan Francisco, CA [email protected]

Accenture Mobility

Copyright © 2011 Accenture All rights reserved. 3

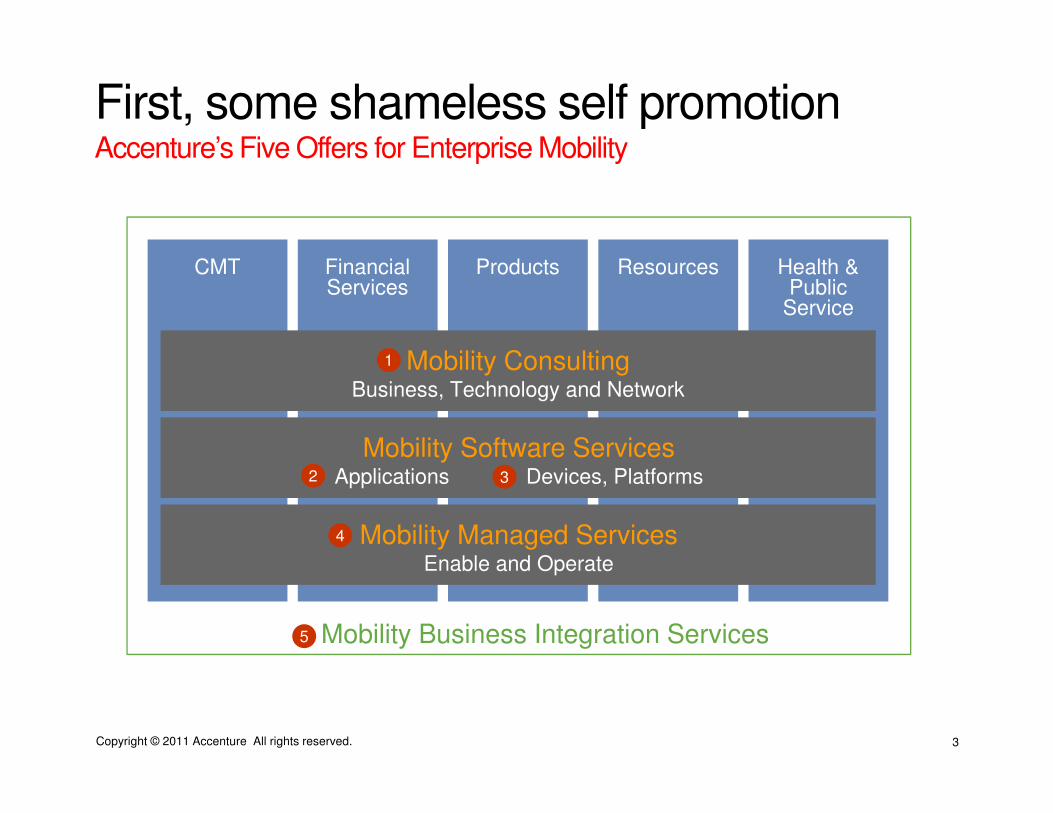

First, some shameless self promotionAccenture’s Five Offers for Enterprise Mobility

CMT FinancialServices

Products Resources Health & Public

Service

Mobility ConsultingBusiness, Technology and Network

Mobility Managed ServicesEnable and Operate

Mobility Business Integration Services

Mobility Software ServicesApplications Devices, Platforms

1

2 3

4

5

Copyright © 2011 Accenture All rights reserved. 4

Today’s topics.

History

Silicon

Cloud

What’s Next?

Copyright © 2011 Accenture All rights reserved. 5

Before we start

J. C. R. Licklider, 1965

“People tend to overestimatewhat can be done in one year and to underestimate what can be done in five to ten years.”

Copyright © 2011 Accenture All rights reserved. 6

Back in 2006

Copyright © 2011 Accenture All rights reserved. 7

History

Copyright © 2011 Accenture All rights reserved. 8

The start of mobile computing.General Magic Mission Statement, May 1990 – Mountain View, CA

“We have a dream of improving the lives of many millions of people by means of small, intimate life support systems that people carry with them everywhere.

These systems will help people to organize their lives, to communicate with other people, and to access information of all kinds.

They will be simple to use, and come in a wide range of models to fit every budget, need, and taste. They will change the way people live and communicate.”

Source: SEC.

Copyright © 2011 Accenture All rights reserved. 9

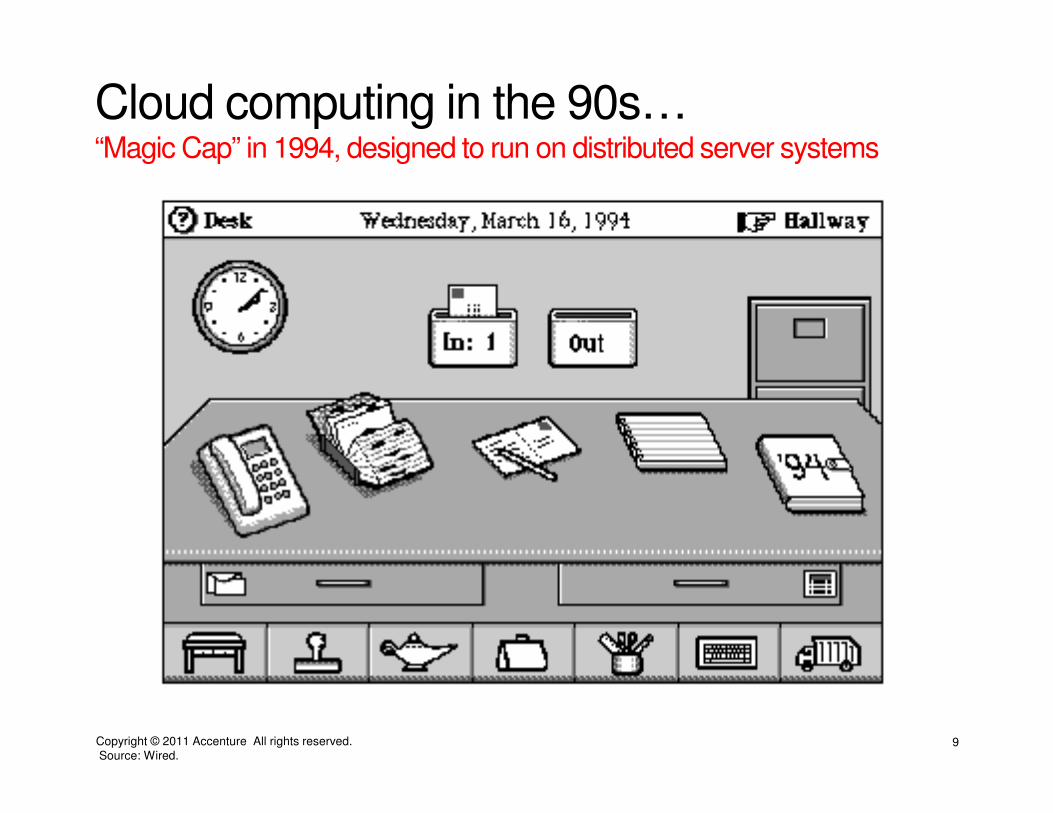

Cloud computing in the 90s…“Magic Cap” in 1994, designed to run on distributed server systems

Source: Wired.

Copyright © 2011 Accenture All rights reserved. 10

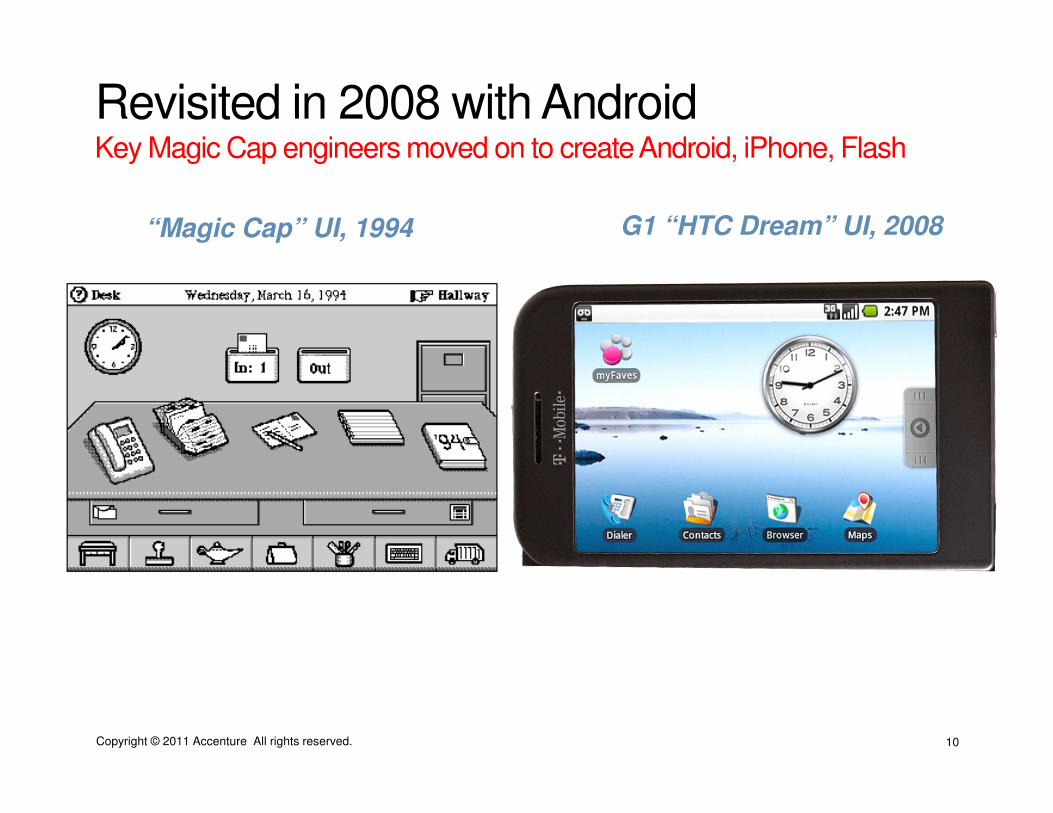

Revisited in 2008 with AndroidKey Magic Cap engineers moved on to create Android, iPhone, Flash

“Magic Cap” UI, 1994 G1 “HTC Dream” UI, 2008

Copyright © 2011 Accenture All rights reserved. 11

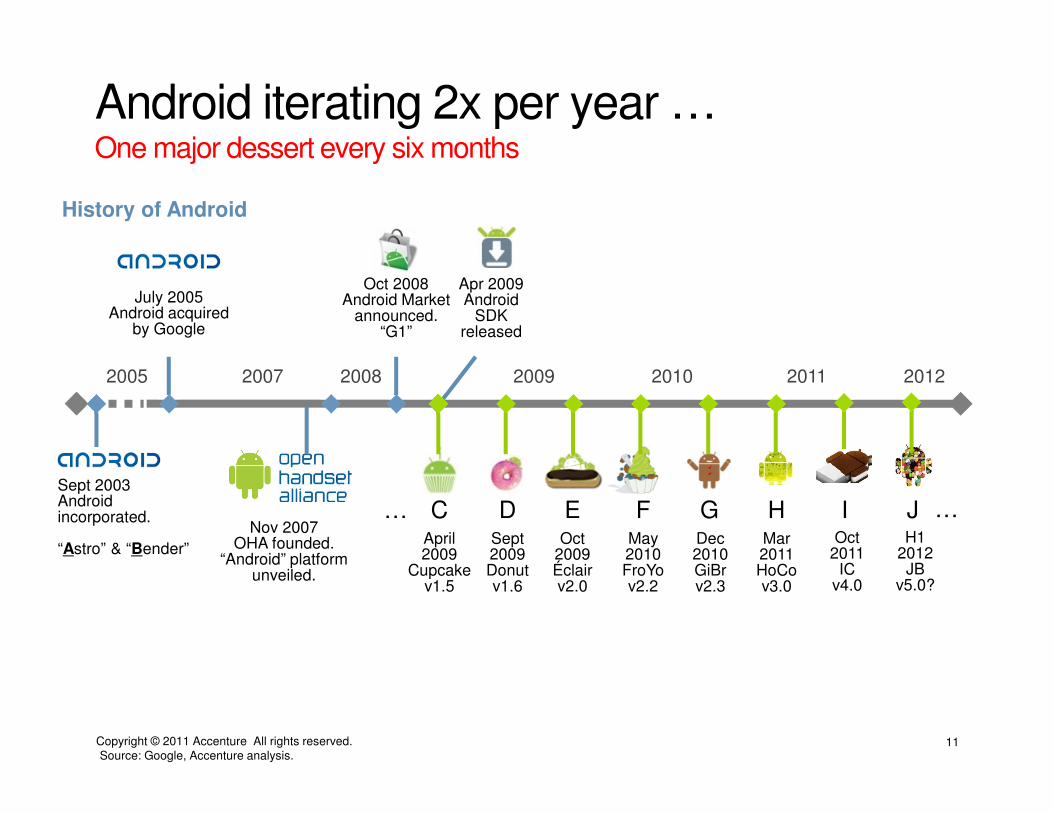

Android iterating 2x per year …One major dessert every six months

Oct 2008Android Market

announced.“G1”

July 2005Android acquired

by Google

2005 2007 2008 2009 20112010

Sept 2003Android incorporated.

“Astro” & “Bender”Nov 2007

OHA founded.“Android” platform

unveiled.

Apr 2009Android

SDK released

History of Android

D E FC GSept 2009Donutv1.6

Oct 2009Éclair v2.0

May 2010 FroYo v2.2

April 2009

Cupcakev1.5

Dec2010GiBrv2.3

… HMar2011HoCov3.0

…IOct

2011IC

v4.0

2012

JH1

2012JB

v5.0?

Source: Google, Accenture analysis.

Copyright © 2011 Accenture All rights reserved. 12

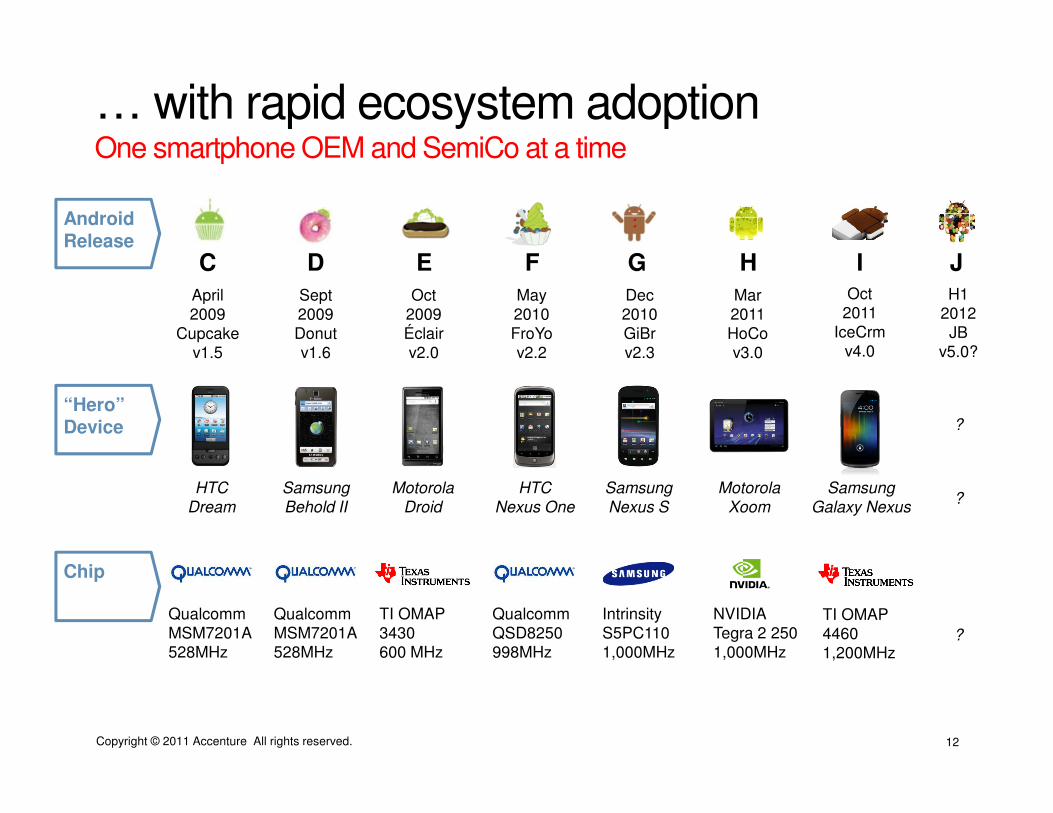

… with rapid ecosystem adoptionOne smartphone OEM and SemiCo at a time

D

Sept 2009Donutv1.6

E

Oct 2009Éclair v2.0

F

May 2010 FroYo v2.2

C

April 2009

Cupcakev1.5

G

Dec2010GiBrv2.3

H

Mar2011HoCov3.0

HTC

Dream

Samsung

Behold II

Motorola

Droid

HTC

Nexus One

Samsung

Nexus S

Motorola

Xoom

Android Release

“Hero” Device

Chip

Qualcomm MSM7201A 528MHz

QualcommQSD8250998MHz

IntrinsityS5PC1101,000MHz

NVIDIATegra 2 2501,000MHz

TI OMAP3430600 MHz

Qualcomm MSM7201A 528MHz

Oct2011

IceCrmv4.0

I

Samsung

Galaxy Nexus

H12012JB

v5.0?

?

?

?

TI OMAP44601,200MHz

J

Copyright © 2011 Accenture All rights reserved. 13

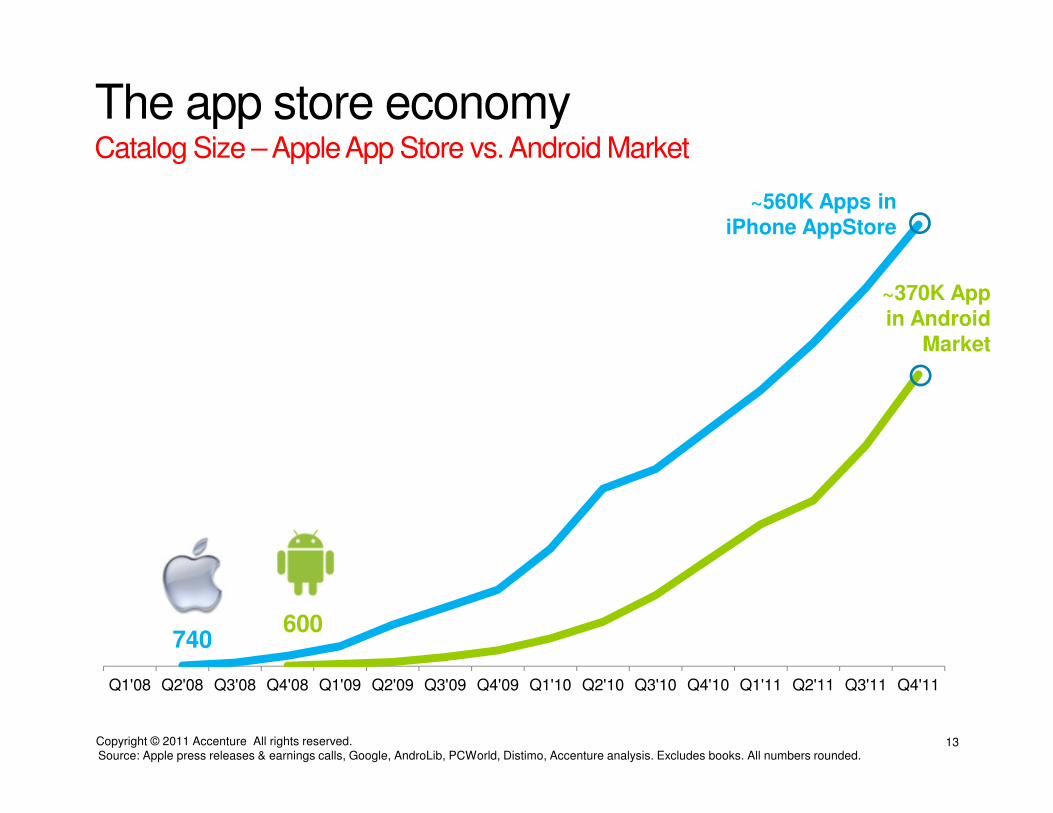

The app store economyCatalog Size –Apple App Store vs. Android Market

740600

Q1'08 Q2'08 Q3'08 Q4'08 Q1'09 Q2'09 Q3'09 Q4'09 Q1'10 Q2'10 Q3'10 Q4'10 Q1'11 Q2'11 Q3'11 Q4'11

Source: Apple press releases & earnings calls, Google, AndroLib, PCWorld, Distimo, Accenture analysis. Excludes books. All numbers rounded.

~560K Apps in iPhone AppStore

~370K App in Android

Market

Copyright © 2011 Accenture All rights reserved. 14

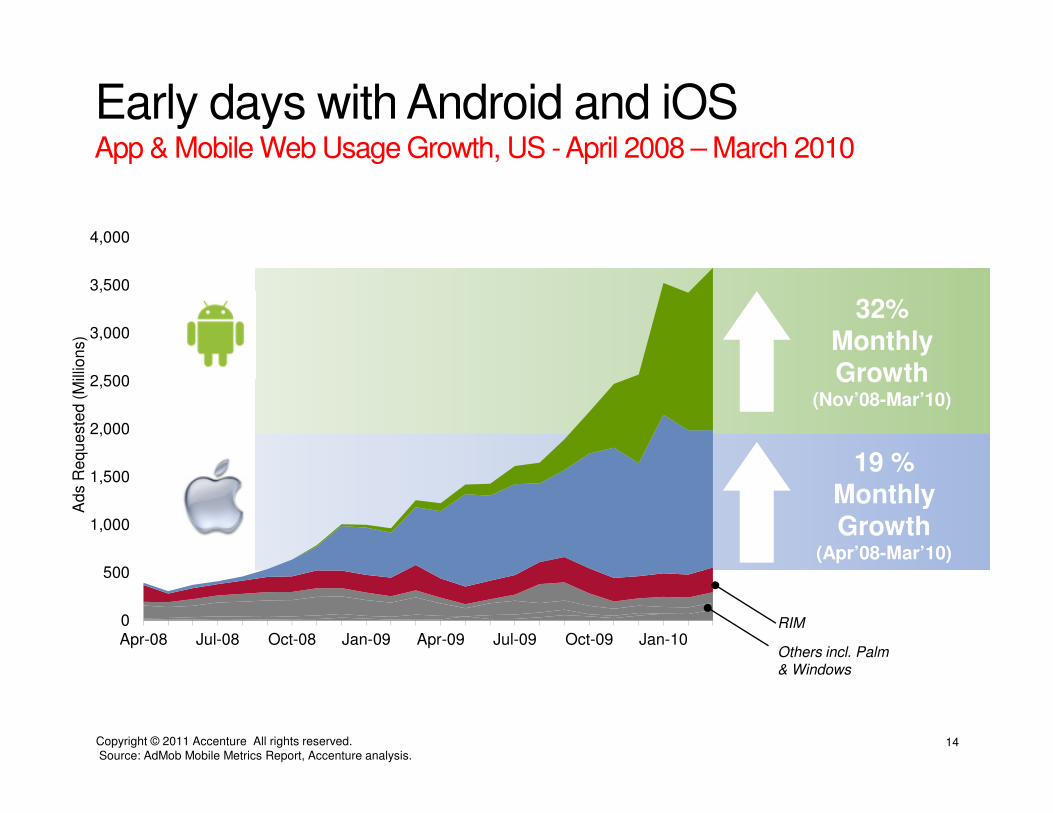

Early days with Android and iOSApp & Mobile Web Usage Growth, US -April 2008 – March 2010

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Apr-08 Jul-08 Oct-08 Jan-09 Apr-09 Jul-09 Oct-09 Jan-10

Ads

Req

uest

ed (

Mill

ions

)

32% Monthly Growth

(Nov’08-Mar’10)

19 % Monthly Growth

(Apr’08-Mar’10)

RIM

Others incl. Palm & Windows

Source: AdMob Mobile Metrics Report, Accenture analysis.

Copyright © 2011 Accenture All rights reserved. 15

Silicon

Copyright © 2011 Accenture All rights reserved. 16

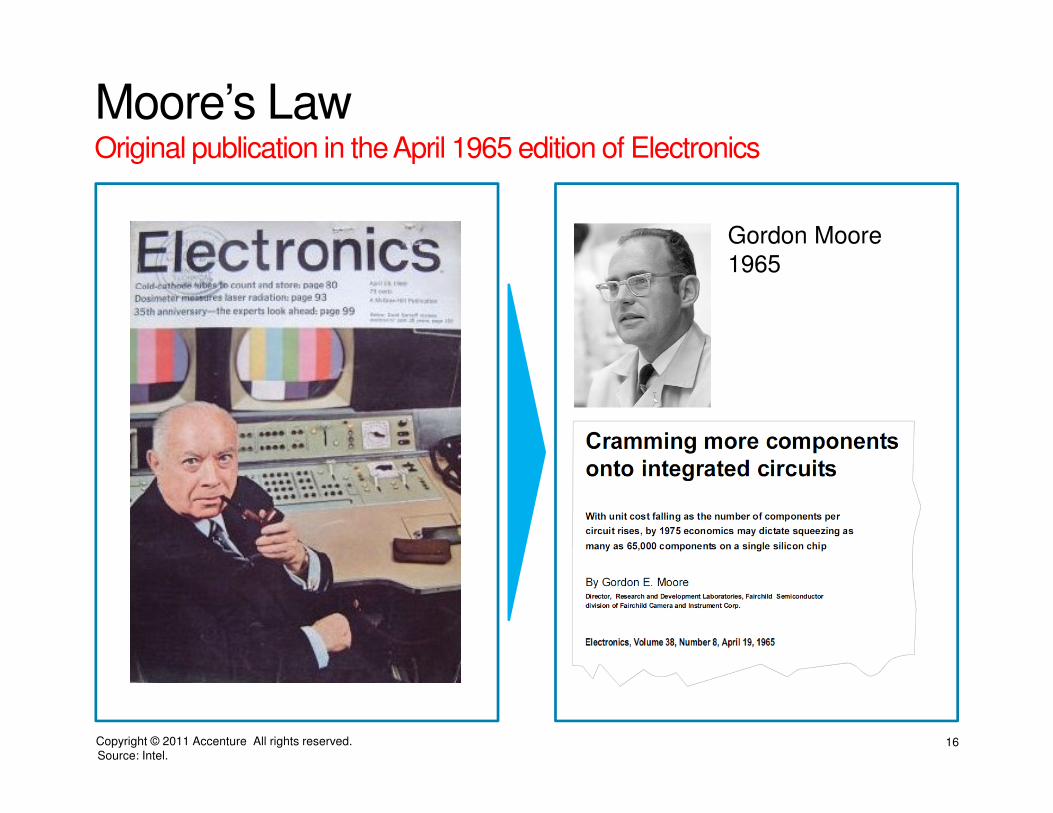

Moore’s LawOriginal publication in the April 1965 edition of Electronics

Gordon Moore1965

Source: Intel.

Copyright © 2011 Accenture All rights reserved. 17

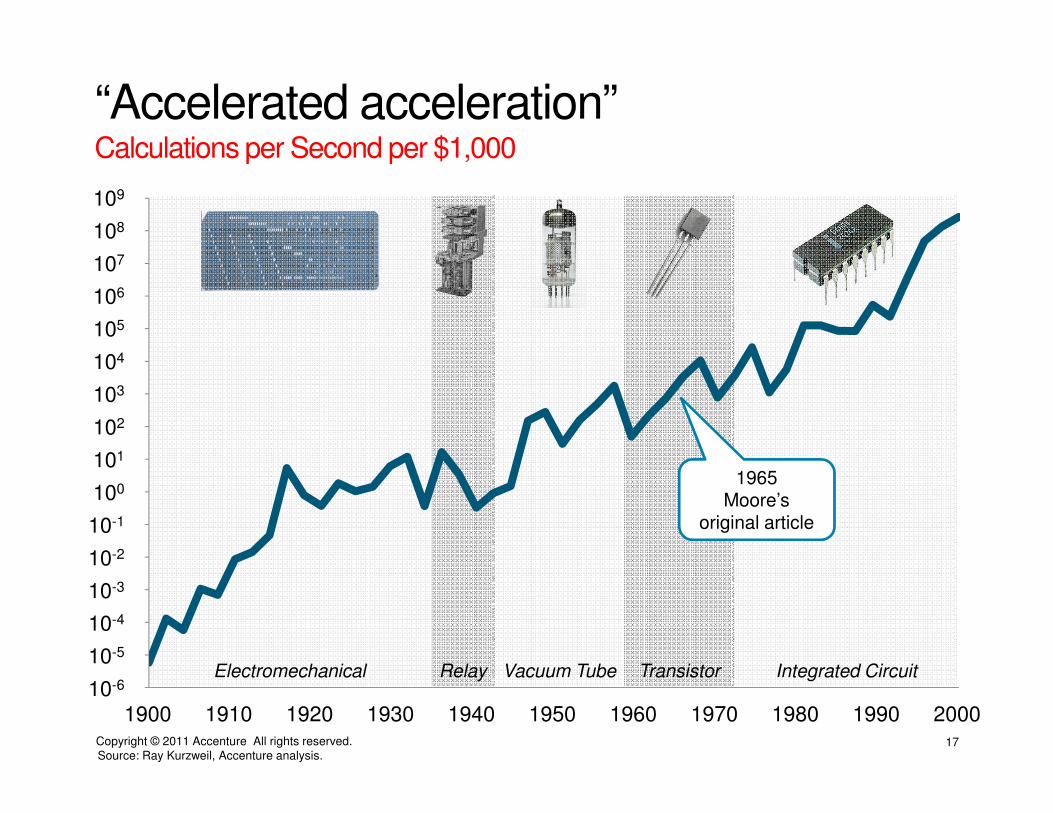

“Accelerated acceleration”Calculations per Second per $1,000

10-6

10-2

103

104

105

10-5

10-4

10-3

10-1

100

102

101

106

107

108

109

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

Electromechanical Relay Vacuum Tube Transistor Integrated Circuit

Source: Ray Kurzweil, Accenture analysis.

1965Moore’s

original article

Copyright © 2011 Accenture All rights reserved. 18

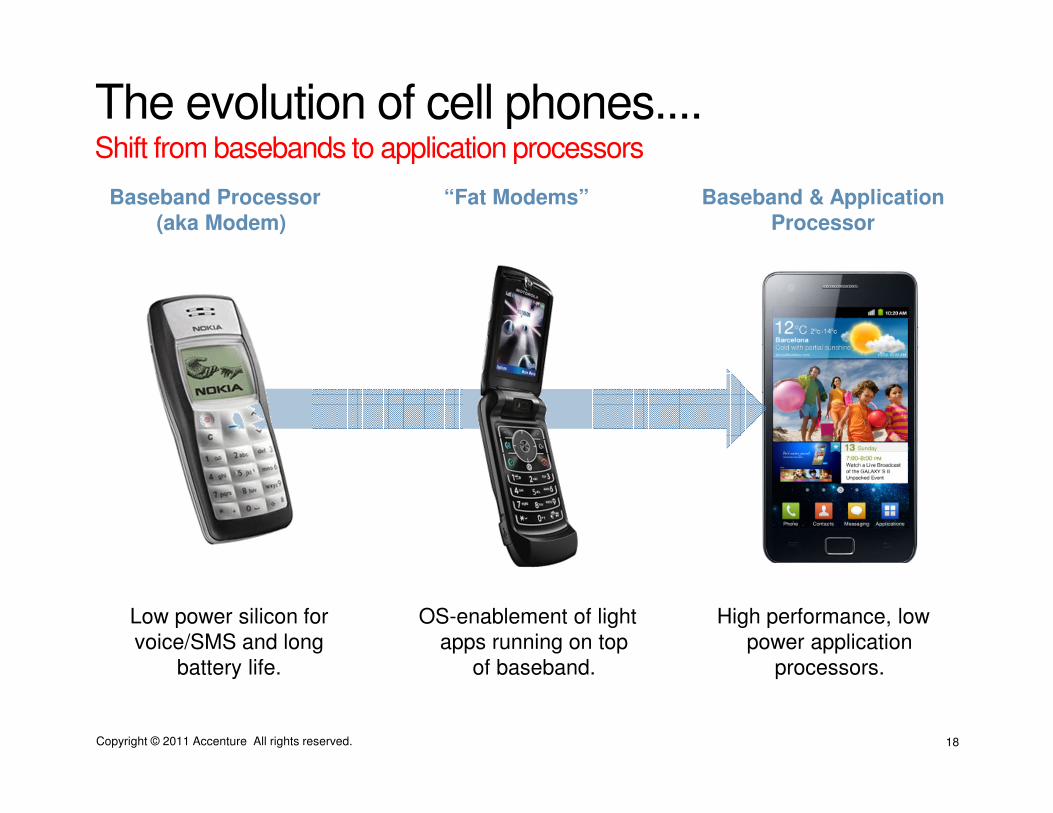

The evolution of cell phones....Shift from basebands to application processors

Baseband Processor (aka Modem)

“Fat Modems” Baseband & Application Processor

Low power silicon for voice/SMS and long

battery life.

OS-enablement of light apps running on top

of baseband.

High performance, low power application

processors.

Copyright © 2011 Accenture All rights reserved. 19

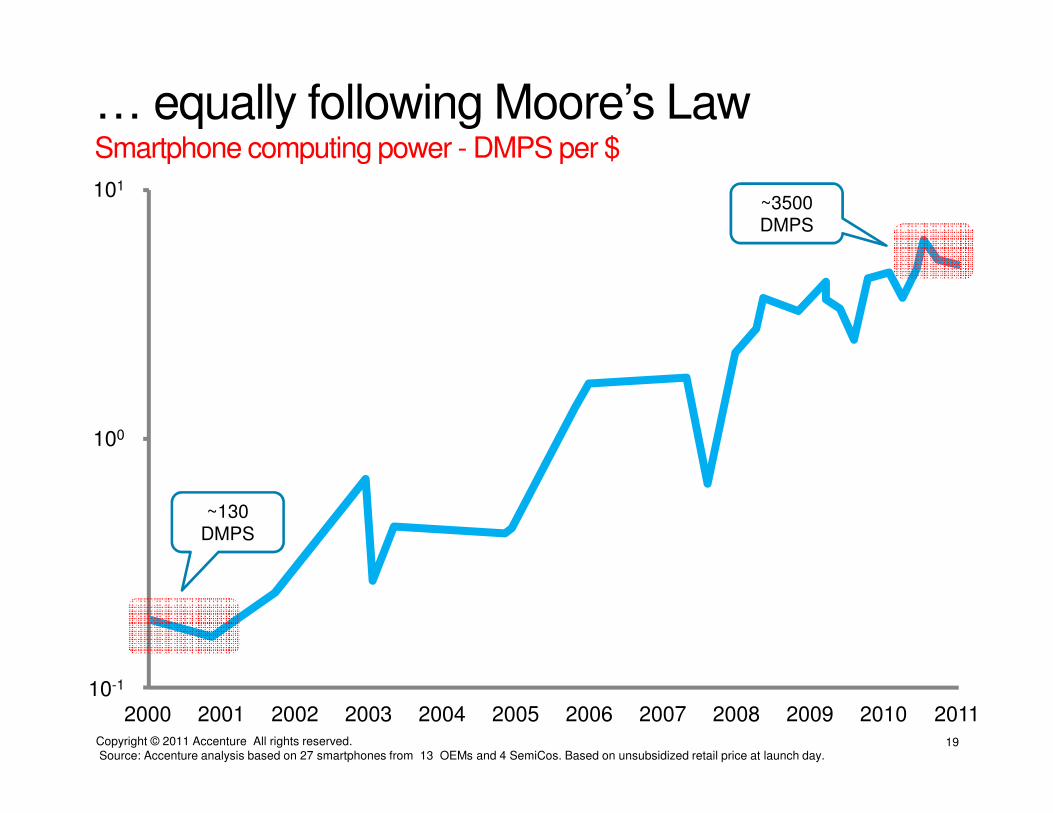

… equally following Moore’s LawSmartphone computing power - DMPS per $

10-1

101

100

2000 2001 2002 20112003 2004 2005 2006 2007 2008 2009 2010

Source: Accenture analysis based on 27 smartphones from 13 OEMs and 4 SemiCos. Based on unsubsidized retail price at launch day.

~130 DMPS

~3500 DMPS

Copyright © 2011 Accenture All rights reserved. 20

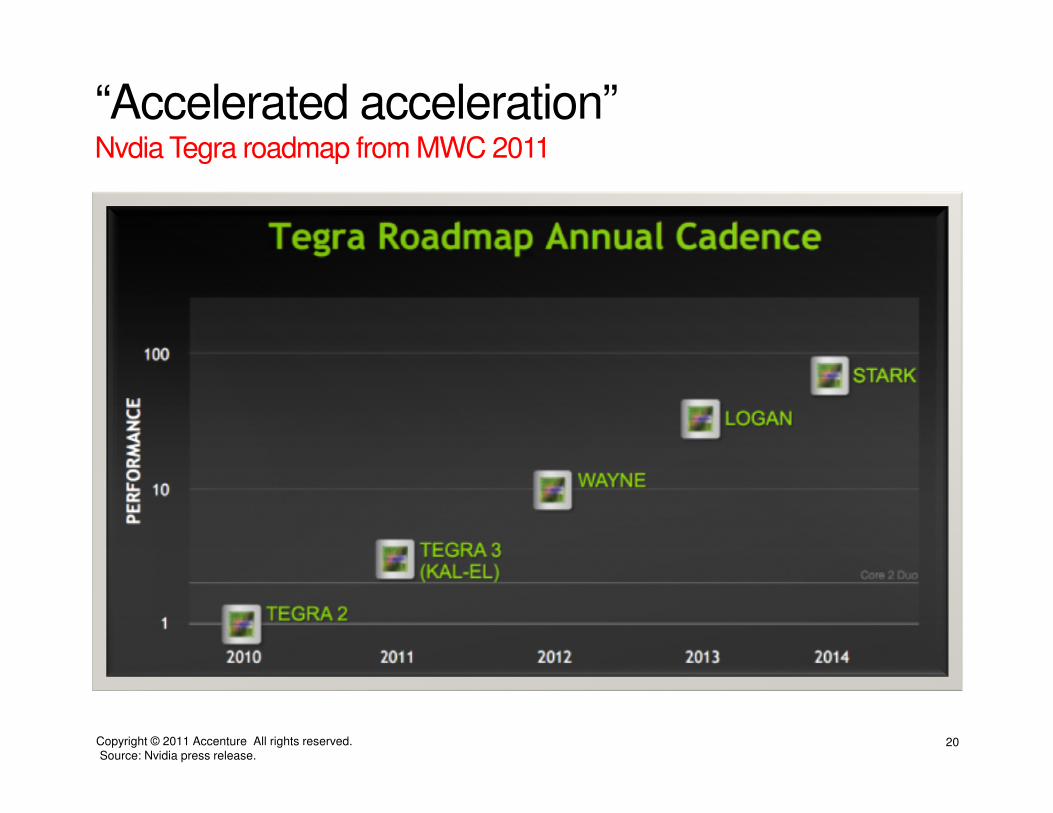

“Accelerated acceleration”Nvdia Tegra roadmap from MWC 2011

Source: Nvidia press release.

Copyright © 2011 Accenture All rights reserved. 21

Delayering of the silicon industrySystem porting emerging as the new layer – “connected devices”.

Fully Vertically Integrated: Design & Foundry

1970sVertical

Suppliers

ASIC Vendor

System Manufacturer

(Foundry)

1980sASIC

Vendors

Design & Distribution (“Fabless”)

Electronic Design

Automation

Foundry

1990sFablessSemis

IP

Design & Distribution

EDA

Foundry

2000sIP-drivenDesign

IP

Design & Distribution

EDA

Foundry

2010sSW-driven

Design

System Porting

“Texas Instruments” “VLSI Technology” “Qualcomm” “ARM” Various

1 : 0 1 : 0.5 1 : 1 1 : 2 1 : 2+RatioHW : SWEngineers

Source: ARM, Cadence, Accenture analysis..

Copyright © 2011 Accenture All rights reserved. 22

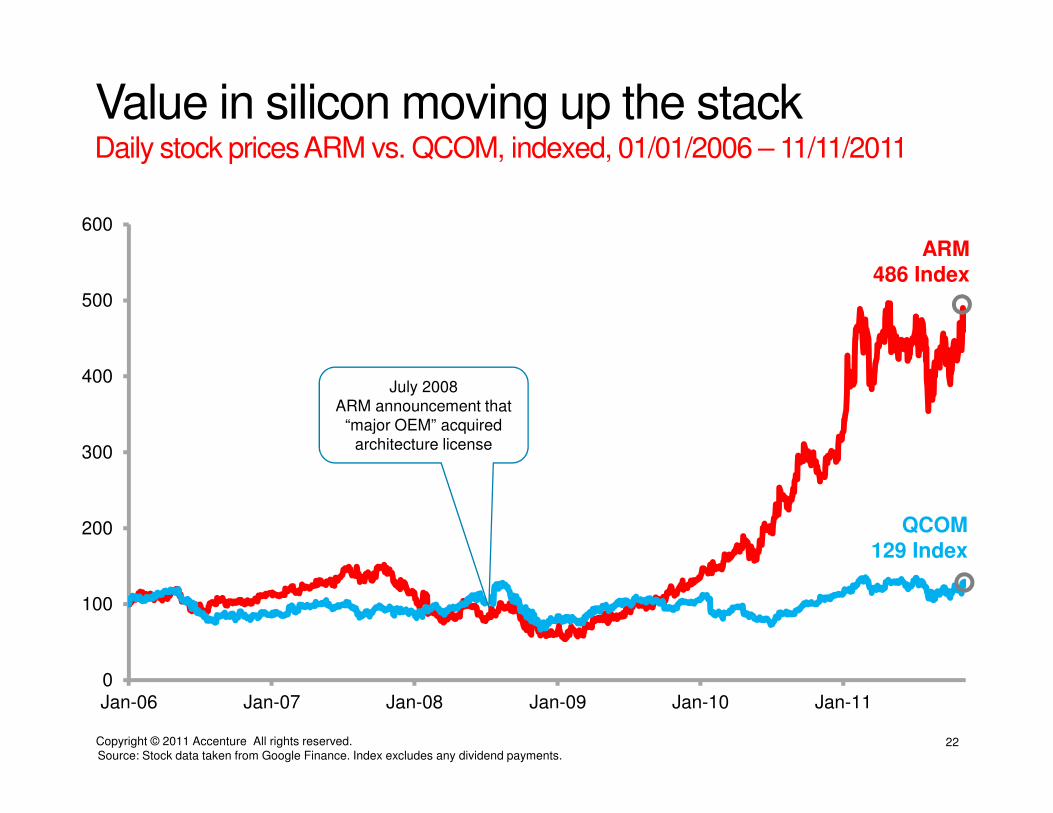

Value in silicon moving up the stackDaily stock prices ARM vs. QCOM, indexed, 01/01/2006 – 11/11/2011

0

100

200

300

400

500

600

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11

QCOM129 Index

ARM486 Index

July 2008ARM announcement that

“major OEM” acquired architecture license

Source: Stock data taken from Google Finance. Index excludes any dividend payments.

Copyright © 2011 Accenture All rights reserved. 23

Cloud

Copyright © 2011 Accenture All rights reserved. 24

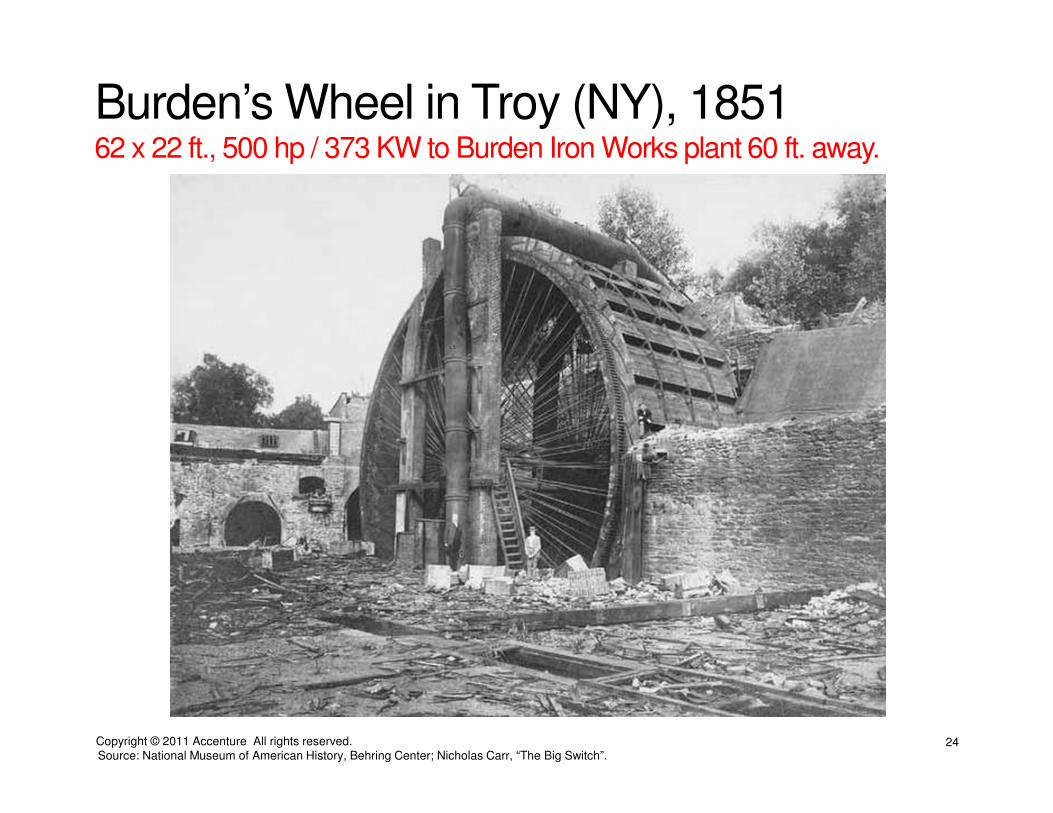

Burden’s Wheel in Troy (NY), 185162 x 22 ft., 500 hp / 373 KW to Burden Iron Works plant 60 ft. away.

Source: National Museum of American History, Behring Center; Nicholas Carr, “The Big Switch”.

Copyright © 2011 Accenture All rights reserved. 25

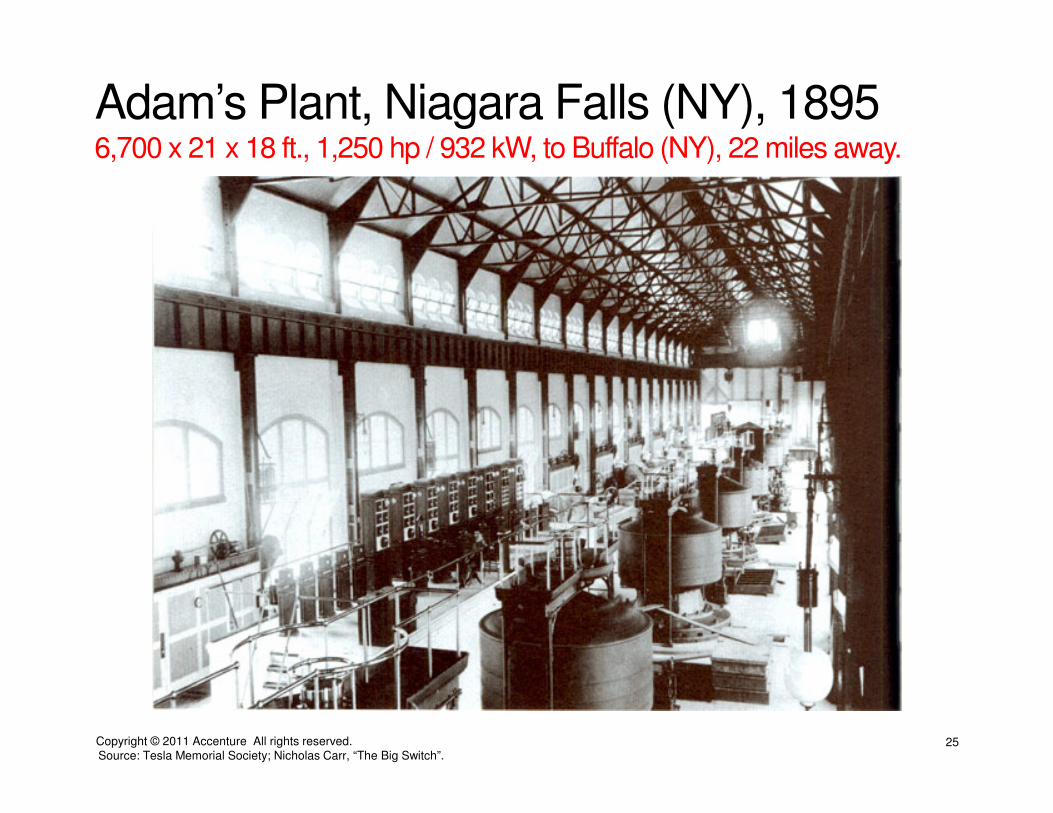

Adam’s Plant, Niagara Falls (NY), 18956,700 x 21 x 18 ft., 1,250 hp / 932 kW, to Buffalo (NY), 22 miles away.

Source: Tesla Memorial Society; Nicholas Carr, “The Big Switch”.

Copyright © 2011 Accenture All rights reserved. 26

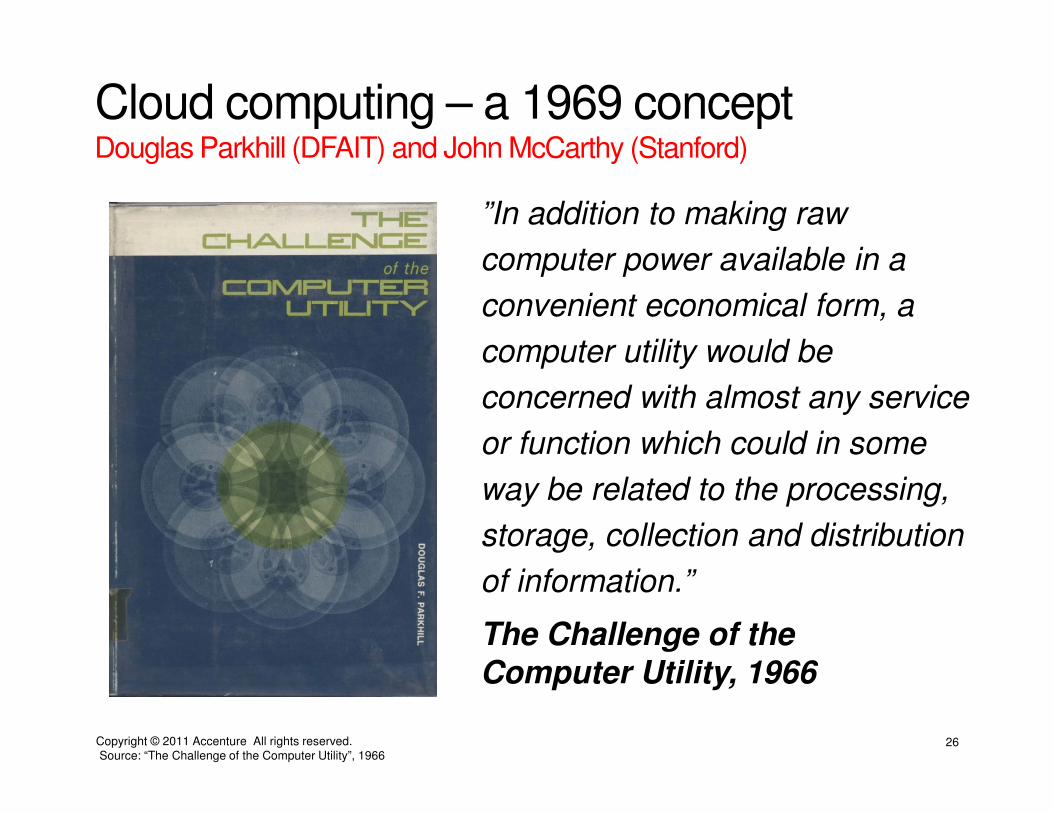

Cloud computing – a 1969 conceptDouglas Parkhill (DFAIT) and John McCarthy (Stanford)

”In addition to making raw

computer power available in a

convenient economical form, a

computer utility would be

concerned with almost any service

or function which could in some

way be related to the processing,

storage, collection and distribution

of information.”

The Challenge of the Computer Utility, 1966

Source: “The Challenge of the Computer Utility”, 1966

Copyright © 2011 Accenture All rights reserved. 27

$B investments into data centersMassive, “off-deck” geo-distributed computing power

Prineville, OR USA The Dalles, OR USA

Maiden, NC USA Dublin, Ireland

Lockport , NY USA

Morrow, OR USA

Copyright © 2011 Accenture All rights reserved. 28

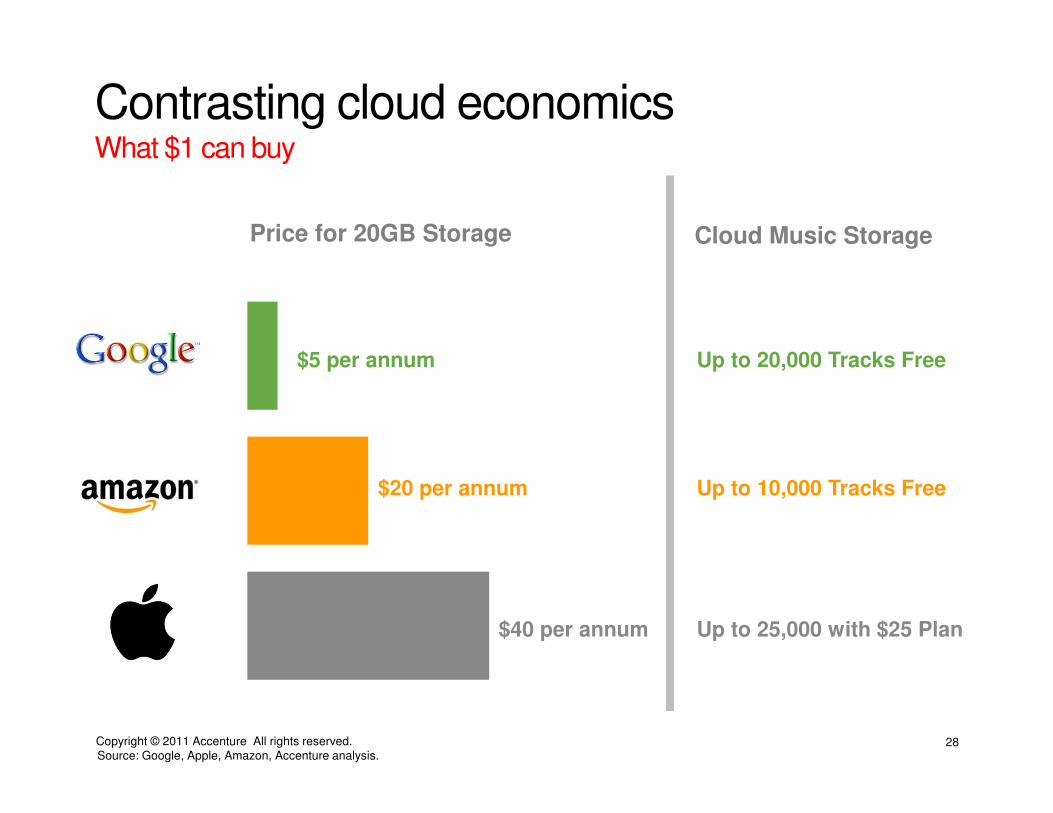

Contrasting cloud economicsWhat $1 can buy

$5 per annum

Price for 20GB Storage Cloud Music Storage

$20 per annum

$40 per annum

Up to 20,000 Tracks Free

Up to 10,000 Tracks Free

Up to 25,000 with $25 Plan

Source: Google, Apple, Amazon, Accenture analysis.

Copyright © 2011 Accenture All rights reserved. 29

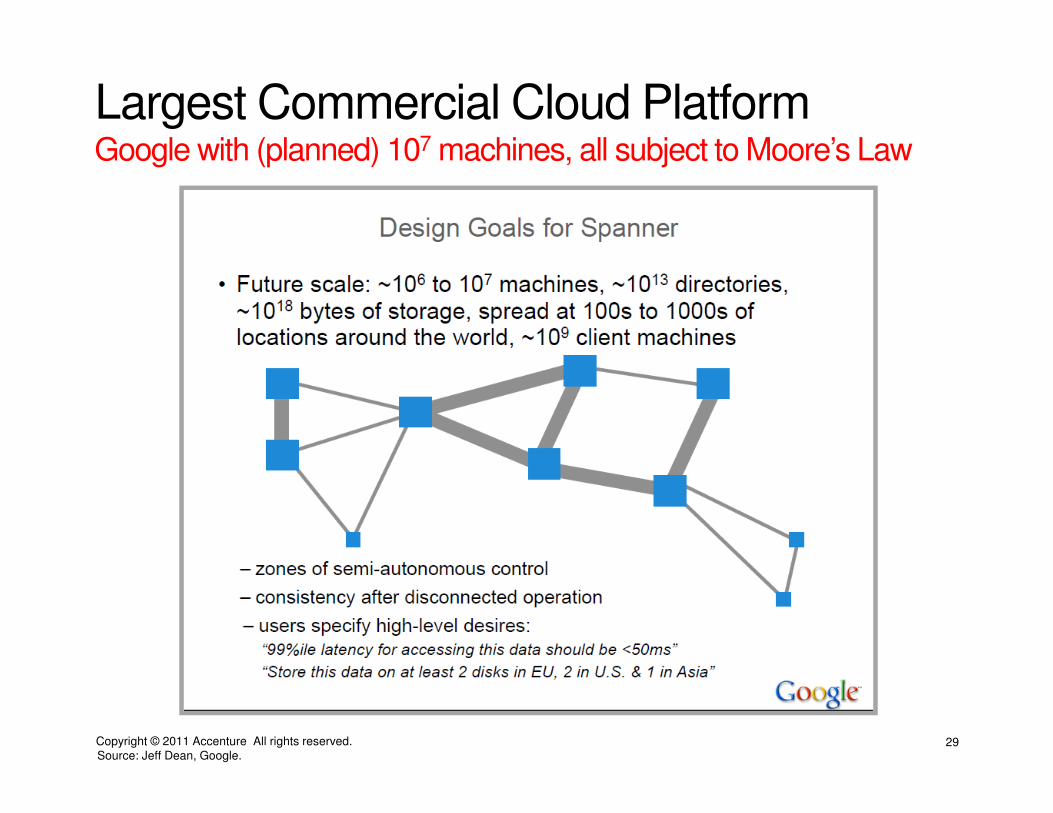

Largest Commercial Cloud PlatformGoogle with (planned) 107 machines, all subject to Moore’s Law

Source: Jeff Dean, Google.

Copyright © 2011 Accenture All rights reserved. 30

What’s next?

Copyright © 2011 Accenture All rights reserved. 31

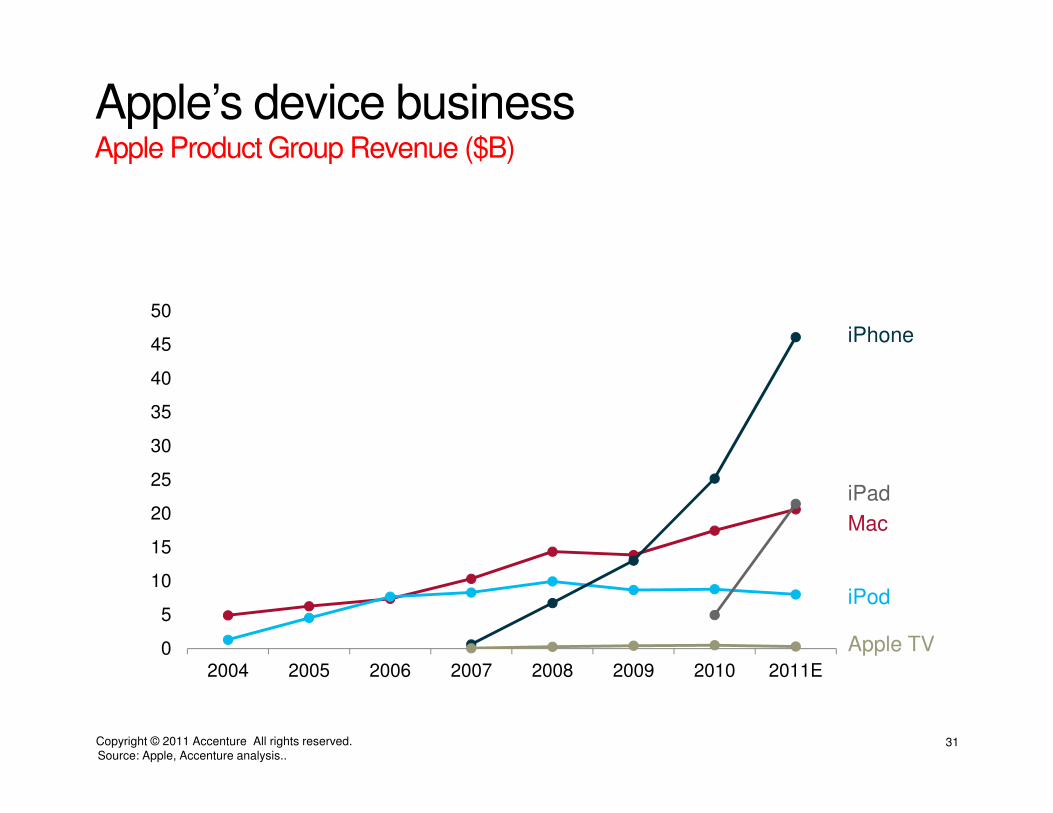

Apple’s device businessApple Product Group Revenue ($B)

0

5

10

15

20

25

30

35

40

45

50

2004 2005 2006 2007 2008 2009 2010 2011E

iPad

Apple TV

iPod

Mac

iPhone

Source: Apple, Accenture analysis..

Copyright © 2011 Accenture All rights reserved. 32

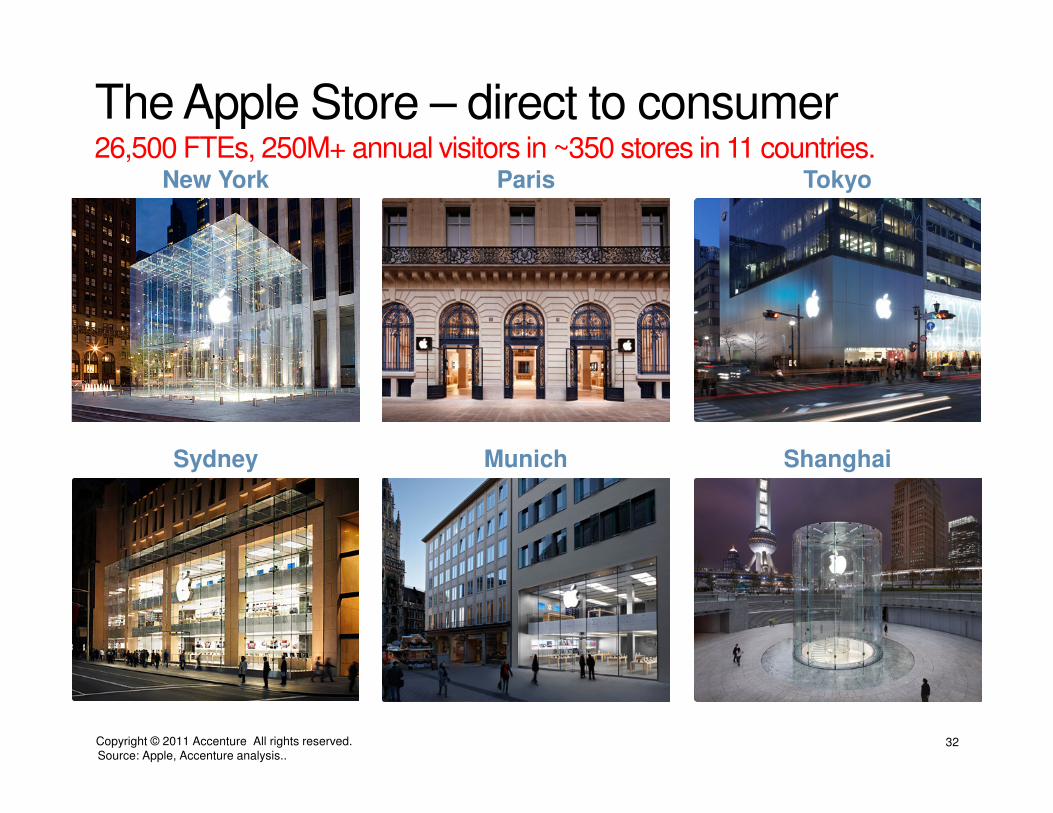

The Apple Store – direct to consumer26,500 FTEs, 250M+ annual visitors in ~350 stores in 11 countries.

New York Paris Tokyo

Sydney Munich Shanghai

Source: Apple, Accenture analysis..

Copyright © 2011 Accenture All rights reserved. 33

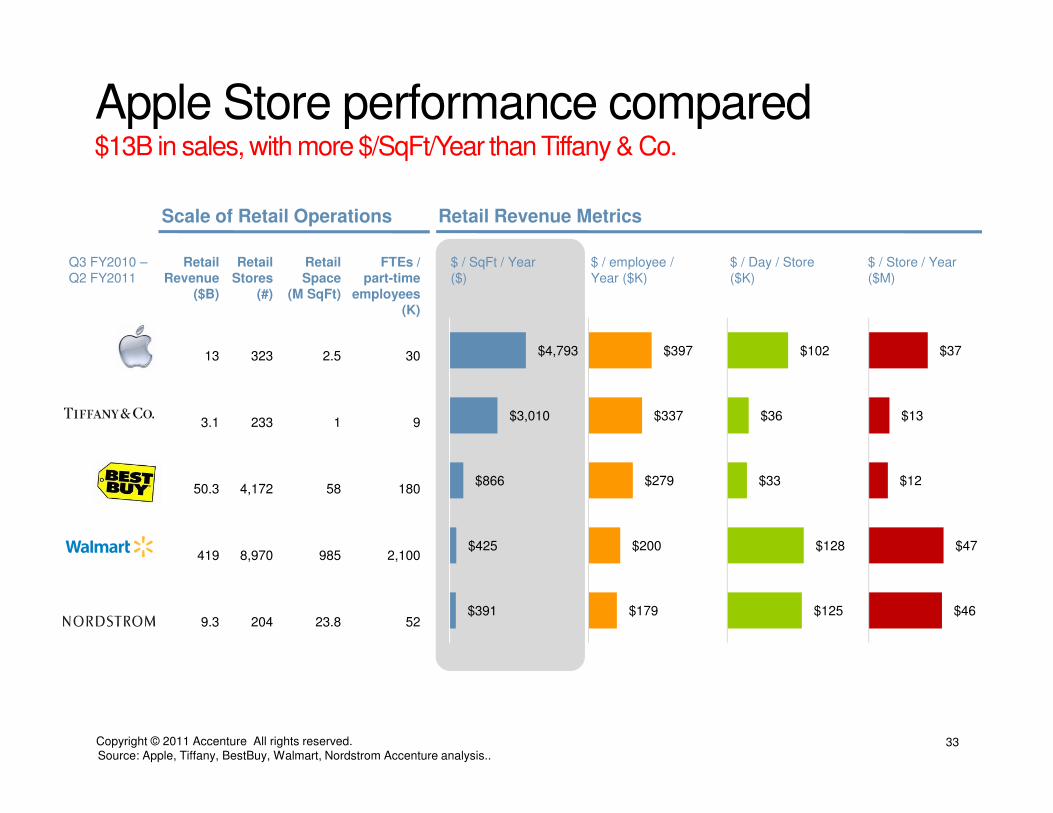

Apple Store performance compared$13B in sales, with more $/SqFt/Year than Tiffany & Co.

$4,793

$3,010

$866

$425

$391

Retail Revenue

($B)

Retail Stores

(#)

Retail Space

(M SqFt)

FTEs / part-time

employees(K)

13 323 2.5 30

3.1 233 1 9

50.3 4,172 58 180

419 8,970 985 2,100

9.3 204 23.8 52

$397

$337

$279

$200

$179

$102

$36

$33

$128

$125

$ / SqFt / Year ($)

$ / employee / Year ($K)

$ / Day / Store($K)

$ / Store / Year($M)

Scale of Retail Operations Retail Revenue Metrics

Q3 FY2010 –Q2 FY2011

$37

$13

$12

$47

$46

Source: Apple, Tiffany, BestBuy, Walmart, Nordstrom Accenture analysis..

Copyright © 2011 Accenture All rights reserved. 34

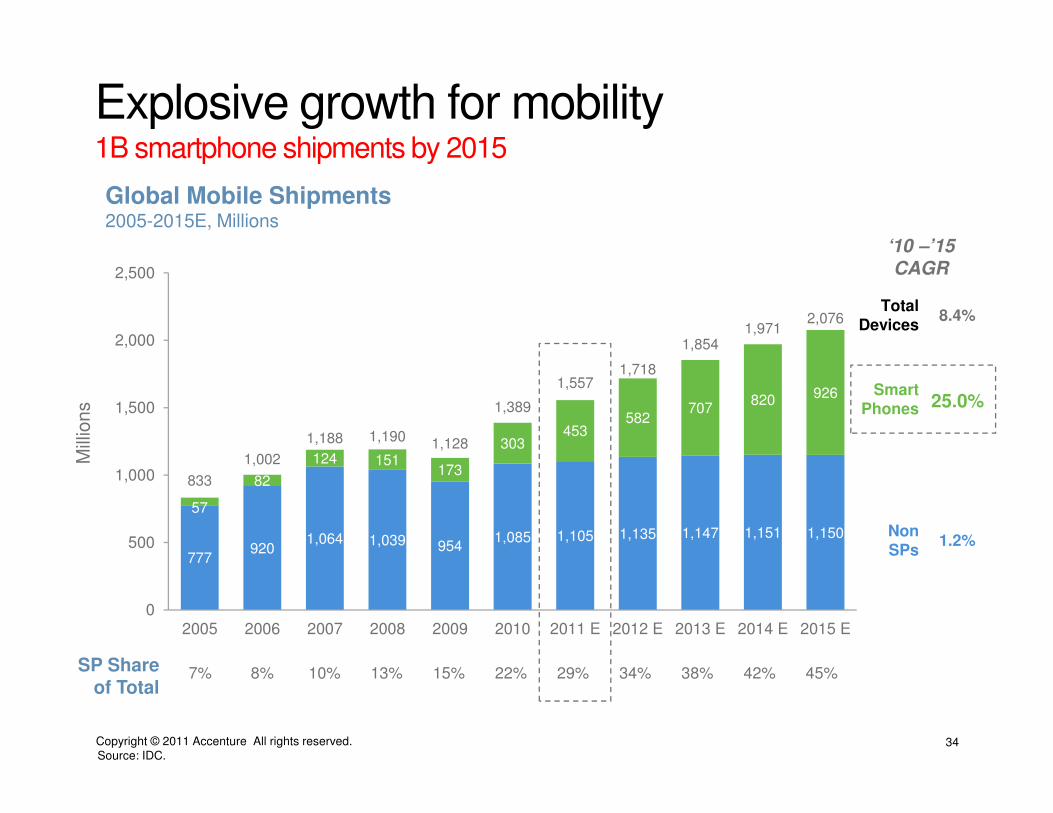

Explosive growth for mobility1B smartphone shipments by 2015

Global Mobile Shipments2005-2015E, Millions

Total Devices

Mill

ions

777920

1,064 1,039 9541,085 1,105 1,135 1,147 1,151 1,150

57

82

124 151173

303453

582707 820 926

833

1,0021,188 1,190 1,128

1,389

1,5571,718

1,8541,971

2,076

0

500

1,000

1,500

2,000

2,500

2005 2006 2007 2008 2009 2010 2011 E 2012 E 2013 E 2014 E 2015 E

SP Share of Total

7% 8% 10% 13% 15% 22% 29% 34% 38% 42% 45%

‘10 –’15 CAGR

8.4%

SmartPhones 25.0%

NonSPs

1.2%

Source: IDC.

Copyright © 2011 Accenture All rights reserved. 35

Ephemeralization“Progressively doing more with less”

Buckminster Fuller, 1938

“To do more and more with less

and less until eventually you can

do everything with nothing”

Copyright © 2011 Accenture All rights reserved. 36

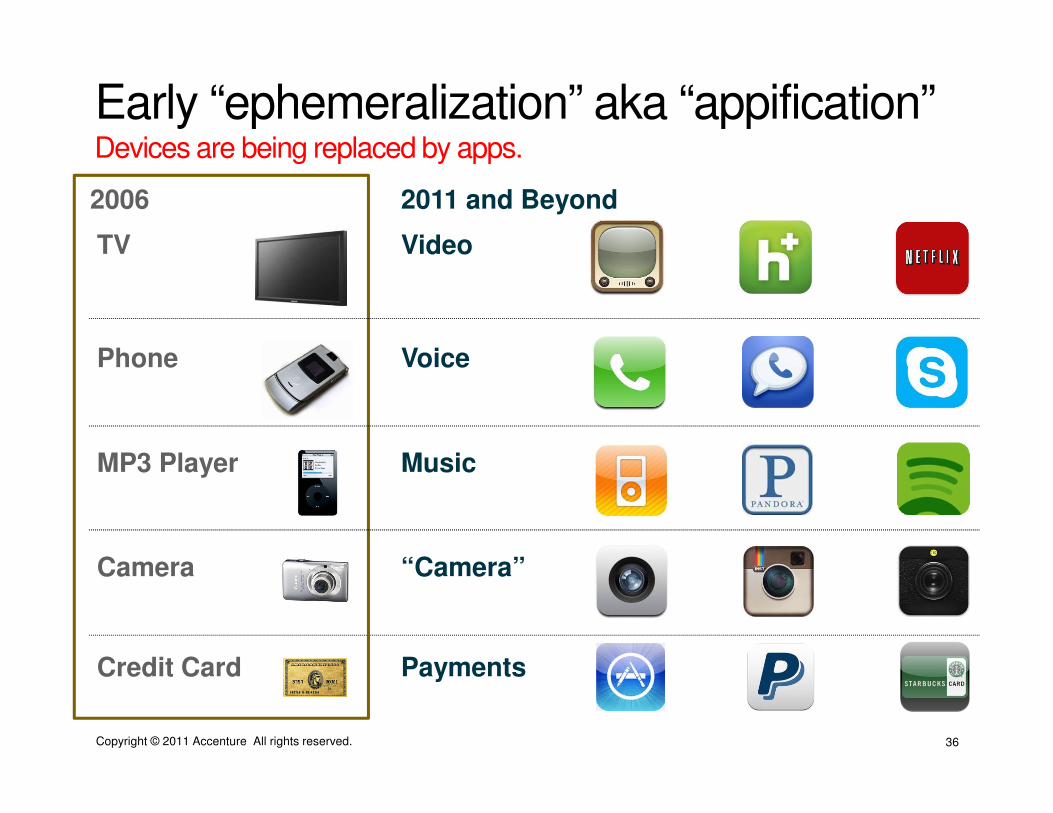

Early “ephemeralization” aka “appification”Devices are being replaced by apps.

2006 2011 and Beyond

Camera “Camera”

Credit Card Payments

MP3 Player Music

TV Video

Phone Voice

Copyright © 2011 Accenture All rights reserved. 37

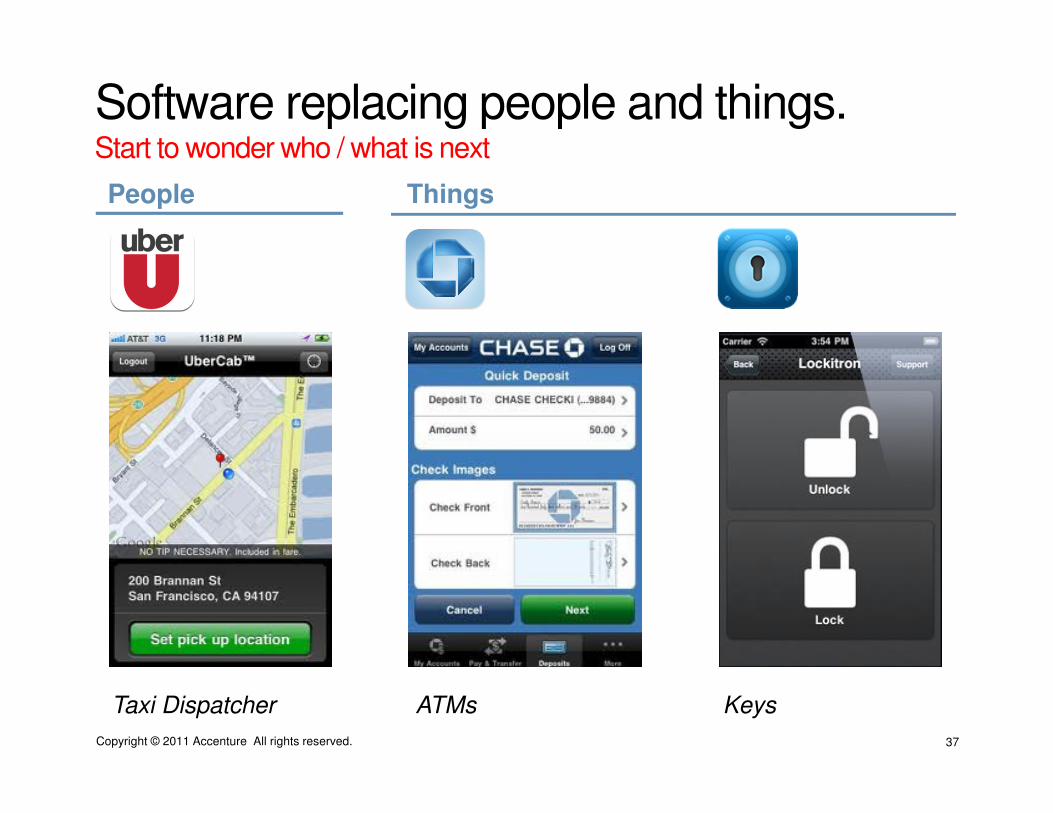

Software replacing people and things.Start to wonder who / what is next

People Things

Taxi Dispatcher ATMs Keys

Copyright © 2011 Accenture All rights reserved. 38

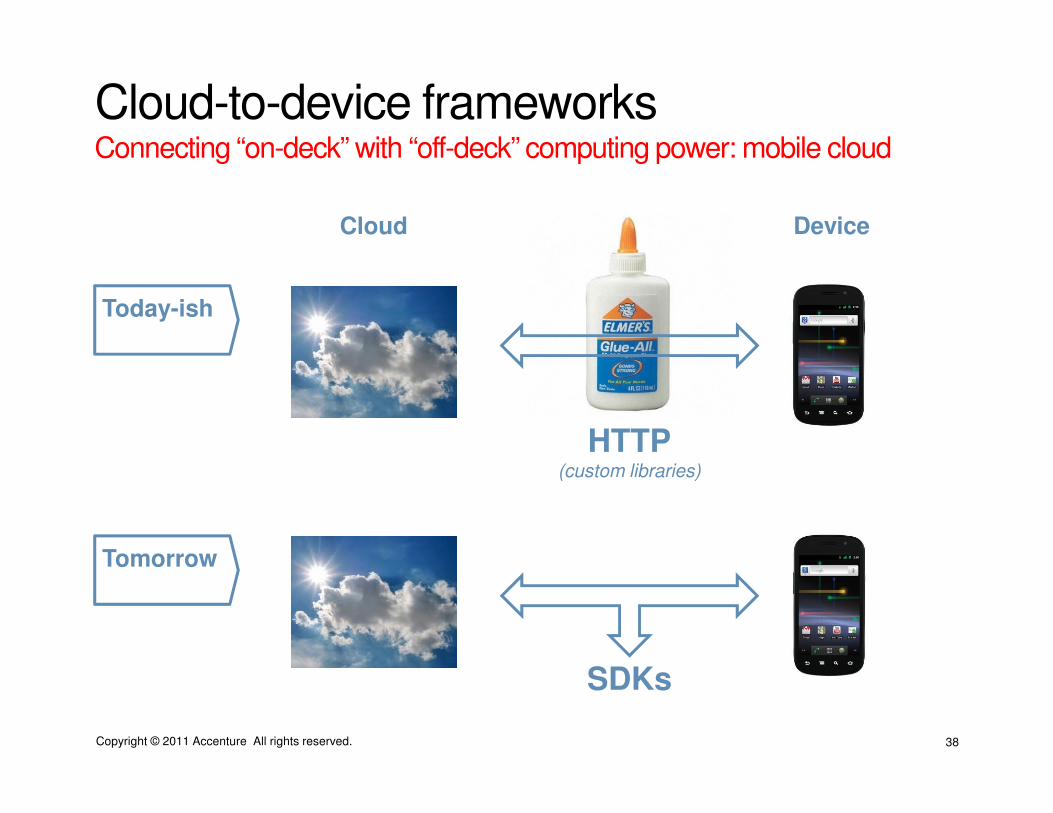

Cloud-to-device frameworksConnecting “on-deck” with “off-deck” computing power: mobile cloud

Today-ish

Tomorrow

HTTP(custom libraries)

SDKs

Cloud Device

Copyright © 2011 Accenture All rights reserved. 39

Industrialization of the back-endCloud-to-device tools and frameworks.

Copyright © 2011 Accenture All rights reserved. 40

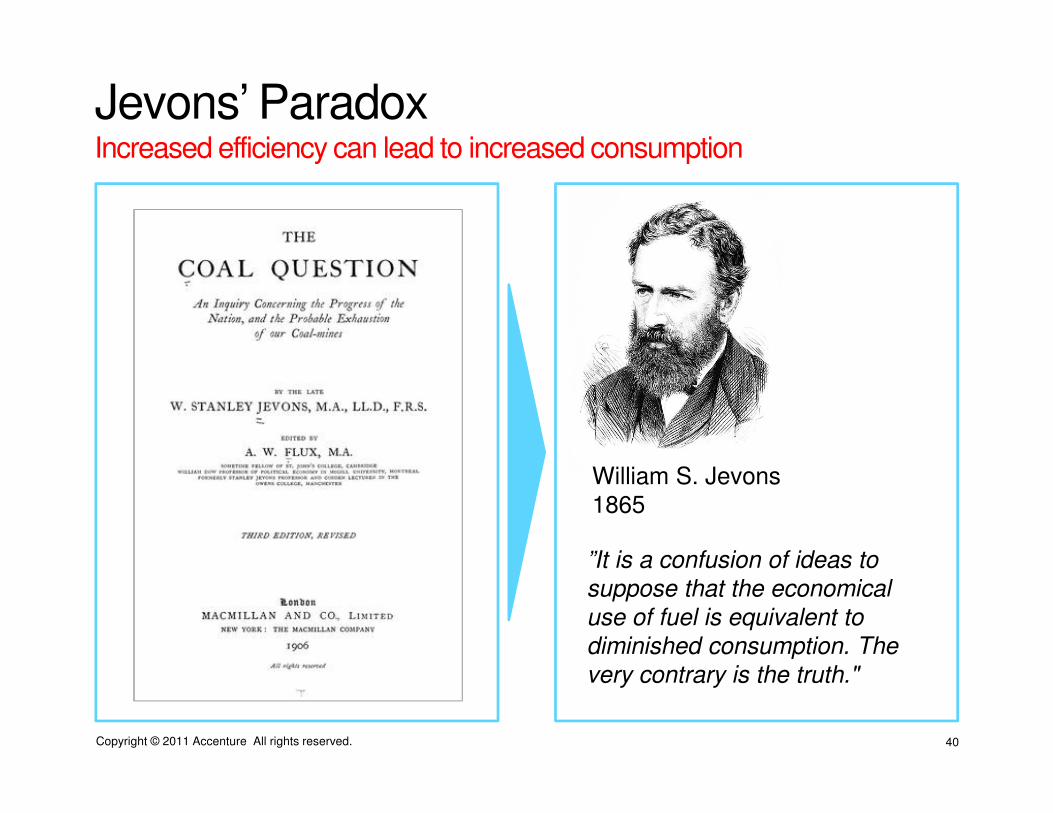

Jevons’ Paradox Increased efficiency can lead to increased consumption

”It is a confusion of ideas to

suppose that the economical

use of fuel is equivalent to

diminished consumption. The

very contrary is the truth."

William S. Jevons1865

Copyright © 2011 Accenture All rights reserved. 41

As computing gets cheaper…Four Decades of Data from the US Bureau of Economic Analysis (1/3)

101

102

103

104

105

Source: BEA, Accenture analysis.

1970 2010200019901980

US Asset Price Index, 1969 – 2010Normalized, 2005 = 100

Industrial Equipment

Other Equipment

Transportation Equipment

Computers and Peripheral Equipment

Copyright © 2011 Accenture All rights reserved. 42

… companies consume more of itFour Decades of Data from the US Bureau of Economic Analysis (2/3)

$0

$50

$100

$150

$200

$250

$300

$350

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

US IT Investment, 1969 – 2010Annual Investment per Employee ($) & Nominal Annual Investment ($B)

Annual Investment per Employee ($)

Nominal Annual Investment ($B)

Source: BEA, Accenture analysis.

1970 2010200019901980

Copyright © 2011 Accenture All rights reserved. 43

Software-driven consumption of ITFour Decades of Data from the US Bureau of Economic Analysis (3/3)

0.5

1

1.5

2

2.5

3

3.5

US IT Investment, 1969 – 2010SW : HW Ratio

1970 2010200019901980

1995YHOO, AMZN, NSCP:

Commercial Web

1990Tim Berners-LeeWorldWideWeb 2007

1st iPhone

Source: BEA, Accenture analysis.

1990ARPANET

decommissioned

Academic Investment

Private Investment

2009SW:HW invest

ratio passes 3:1

Copyright © 2011 Accenture All rights reserved. 44

Think again

J. C. R. Licklider, 1965

“People tend to overestimatewhat can be done in one year and to underestimate what can be done in five to ten years.”