Acca f6 uk short note

22

ACCA Paper F6 Taxation (UK) Initial booster This is not an exhaustive note for ACCA paper F6. And this note does not cover full syllabus of the paper F6. However it may be handy as a startup in taxation. Some major calculations and confusing items are jotted down here considering exam kit and study text. A note of own working is the best note of all and advisable. Wishing your success through Hard Work and self- developed Techniques. MD. Inzamum - UL – Haque [email protected]

-

Upload

inzamum-ul-haque -

Category

Documents

-

view

248 -

download

6

description

ACCA Paper F6 Formats/ Short Notes

Transcript of Acca f6 uk short note

ACCA Paper F6 Taxation (UK)

Initial booster

This is not an exhaustive note for ACCA paper F6. And this note

does not cover full syllabus of the paper F6. However it may be

handy as a startup in taxation. Some major calculations and

confusing items are jotted down here considering exam kit and

study text. A note of own working is the best note of all and

advisable. Wishing your success through Hard Work and self-

developed Techniques.

MD. Inzamum - UL – Haque

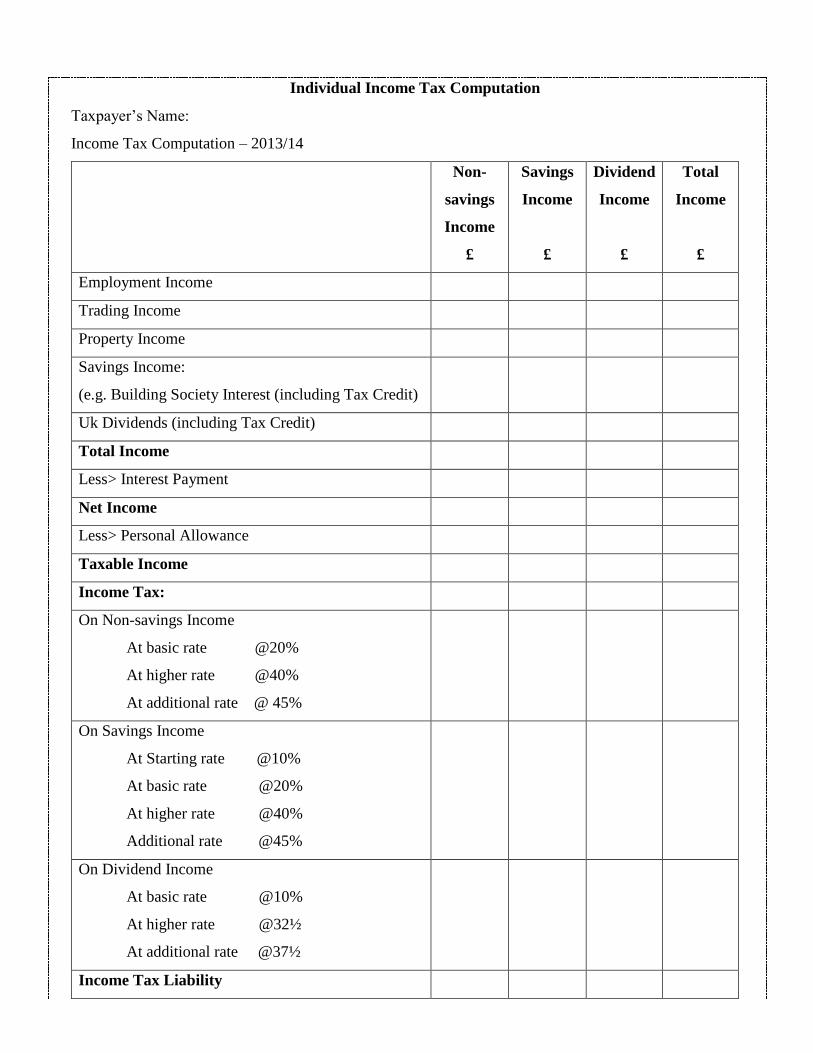

Individual Income Tax Computation

Taxpayer’s Name:

Income Tax Computation – 2013/14

Non-

savings

Income

£

Savings

Income

£

Dividend

Income

£

Total

Income

£

Employment Income

Trading Income

Property Income

Savings Income:

(e.g. Building Society Interest (including Tax Credit)

Uk Dividends (including Tax Credit)

Total Income

Less> Interest Payment

Net Income

Less> Personal Allowance

Taxable Income

Income Tax:

On Non-savings Income

At basic rate @20%

At higher rate @40%

At additional rate @ 45%

On Savings Income

At Starting rate @10%

At basic rate @20%

At higher rate @40%

Additional rate @45%

On Dividend Income

At basic rate @10%

At higher rate @32½

At additional rate @37½

Income Tax Liability

Md. Inzamum-Ul-Haque [[email protected]]

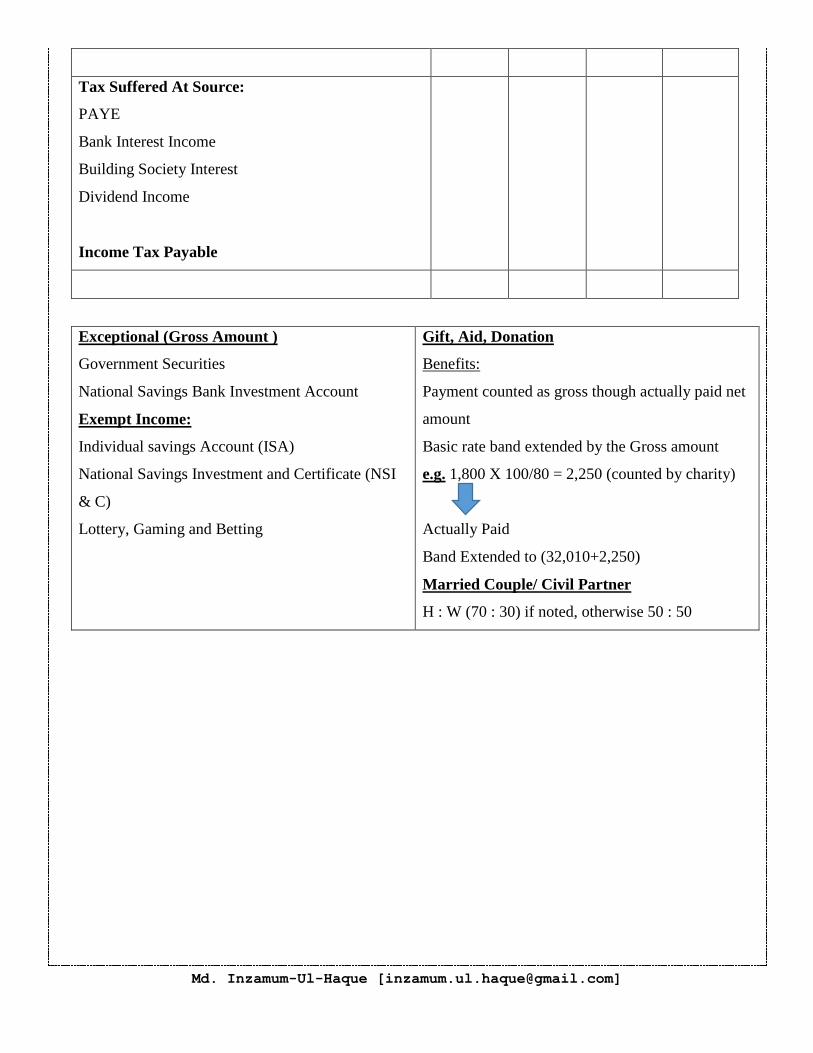

Tax Suffered At Source:

PAYE

Bank Interest Income

Building Society Interest

Dividend Income

Income Tax Payable

Exceptional (Gross Amount )

Government Securities

National Savings Bank Investment Account

Exempt Income:

Individual savings Account (ISA)

National Savings Investment and Certificate (NSI

& C)

Lottery, Gaming and Betting

Gift, Aid, Donation

Benefits:

Payment counted as gross though actually paid net

amount

Basic rate band extended by the Gross amount

e.g. 1,800 X 100/80 = 2,250 (counted by charity)

Actually Paid

Band Extended to (32,010+2,250)

Married Couple/ Civil Partner

H : W (70 : 30) if noted, otherwise 50 : 50

Md. Inzamum-Ul-Haque [[email protected]]

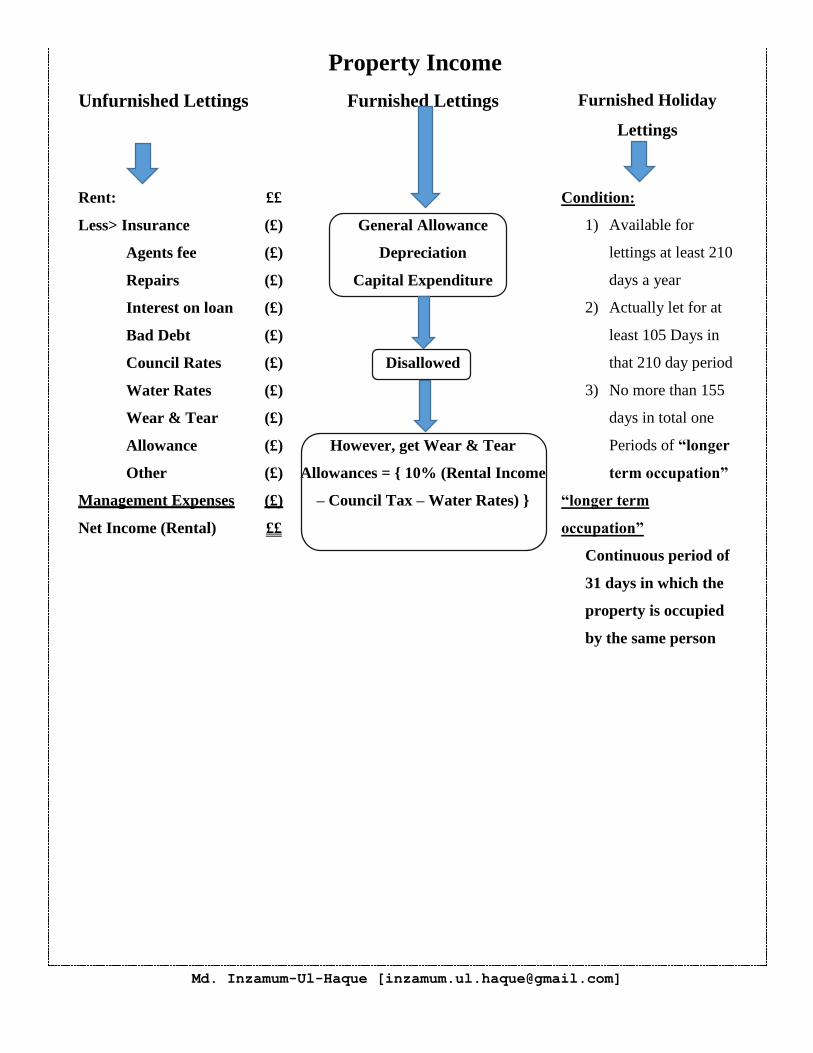

Property Income

Unfurnished Lettings Furnished Lettings Furnished Holiday

Lettings

Rent:

Less> Insurance

Agents fee

Repairs

Interest on loan

Bad Debt

Council Rates

Water Rates

Wear & Tear

Allowance

Other

Management Expenses

Net Income (Rental)

££

(£)

(£)

(£)

(£)

(£)

(£)

(£)

(£)

(£)

(£)

(£)

££

General Allowance

Depreciation

Capital Expenditure

Disallowed

However, get Wear & Tear

Allowances = { 10% (Rental Income

– Council Tax – Water Rates) }

Condition:

1) Available for

lettings at least 210

days a year

2) Actually let for at

least 105 Days in

that 210 day period

3) No more than 155

days in total one

Periods of “longer

term occupation”

“longer term

occupation”

Continuous period of

31 days in which the

property is occupied

by the same person

Md. Inzamum-Ul-Haque [[email protected]]

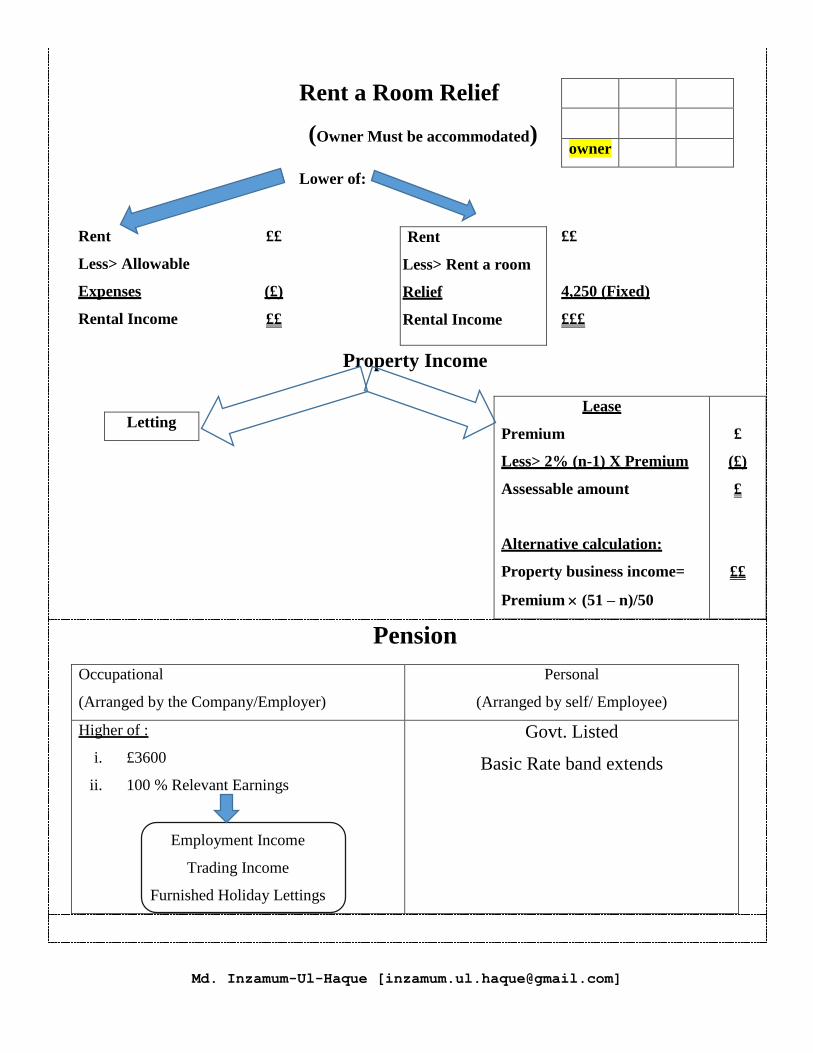

Rent a Room Relief

(Owner Must be accommodated)

owner

Lower of:

Rent

Less> Allowable

Expenses

Rental Income

££

(£)

££

Rent

Less> Rent a room

Relief

Rental Income

££

4,250 (Fixed)

£££

Property Income

Lease

Premium

Less> 2% (n-1) X Premium

Assessable amount

Alternative calculation:

Property business income=

Premium (51 – n)/50

£

(£)

£

££

Letting

Pension

Occupational

(Arranged by the Company/Employer)

Personal

(Arranged by self/ Employee)

Higher of :

i. £3600

ii. 100 % Relevant Earnings

Employment Income

Trading Income

Furnished Holiday Lettings

Govt. Listed

Basic Rate band extends

Md. Inzamum-Ul-Haque [[email protected]]

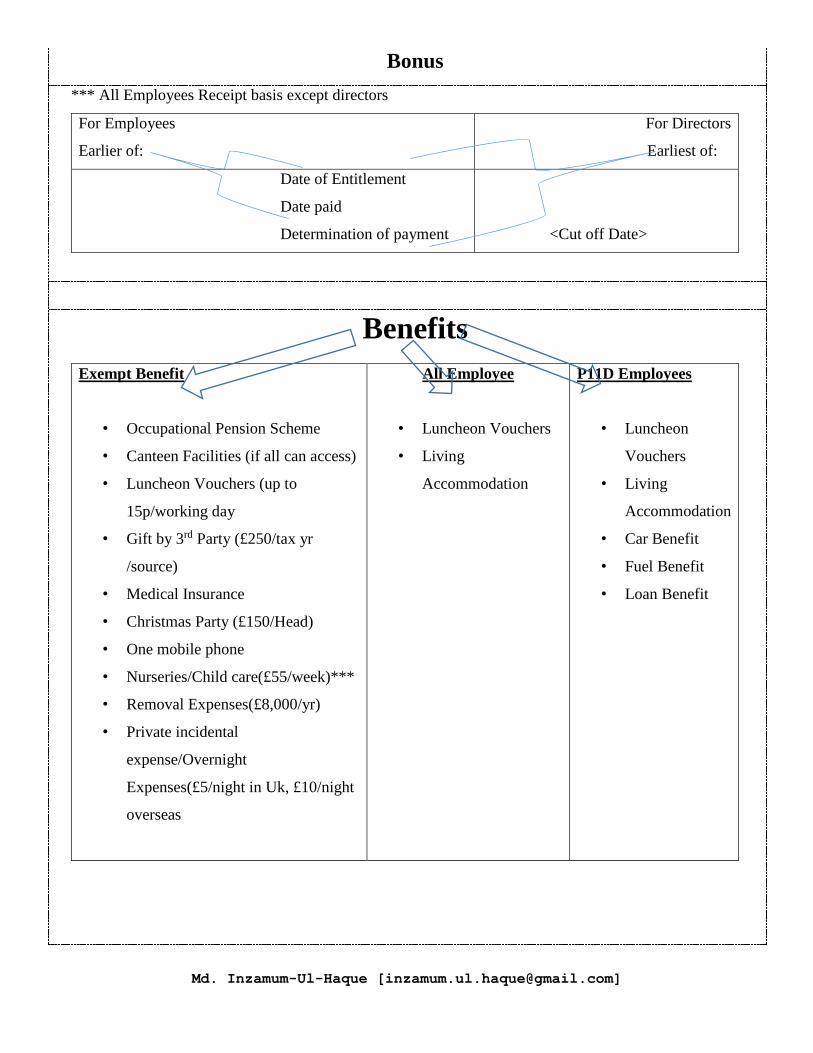

Bonus

*** All Employees Receipt basis except directors

For Employees

Earlier of:

For Directors

Earliest of:

Date of Entitlement

Date paid

Determination of payment

<Cut off Date>

Benefits

Exempt Benefit

• Occupational Pension Scheme

• Canteen Facilities (if all can access)

• Luncheon Vouchers (up to

15p/working day

• Gift by 3rd Party (£250/tax yr

/source)

• Medical Insurance

• Christmas Party (£150/Head)

• One mobile phone

• Nurseries/Child care(£55/week)***

• Removal Expenses(£8,000/yr)

• Private incidental

expense/Overnight

Expenses(£5/night in Uk, £10/night

overseas

All Employee

• Luncheon Vouchers

• Living

Accommodation

P11D Employees

• Luncheon

Vouchers

• Living

Accommodation

• Car Benefit

• Fuel Benefit

• Loan Benefit

Md. Inzamum-Ul-Haque [[email protected]]

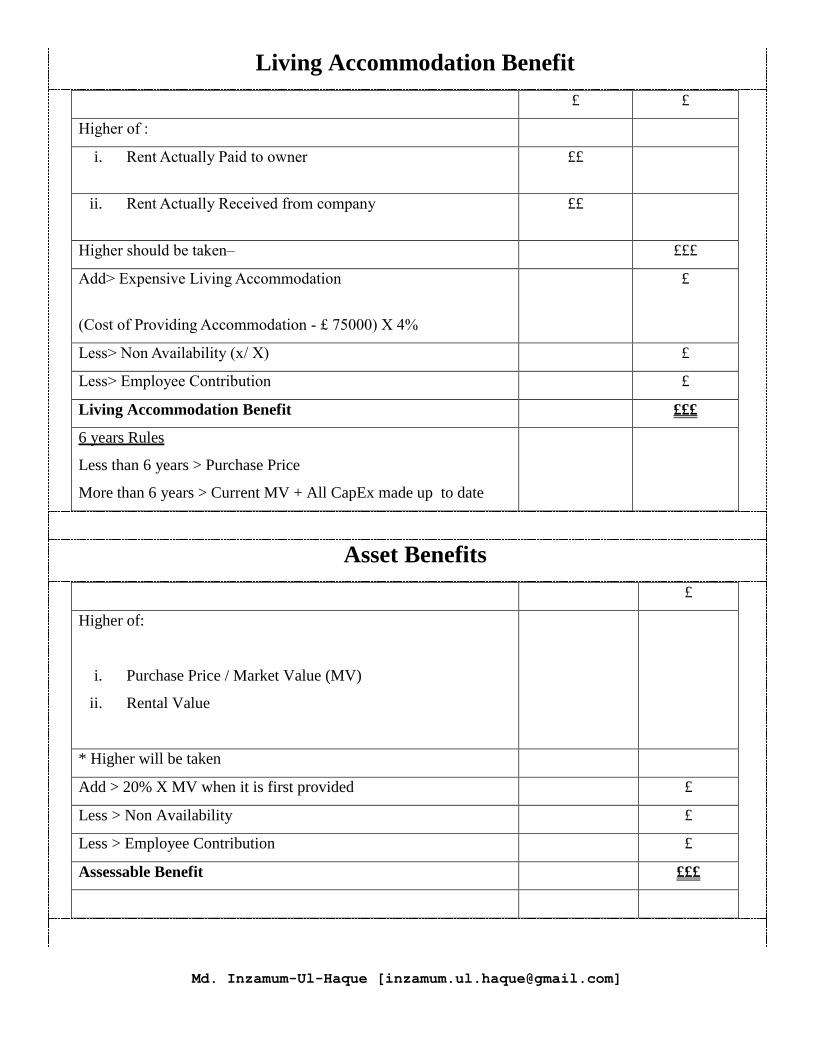

Living Accommodation Benefit

£ £

Higher of :

i. Rent Actually Paid to owner ££

ii. Rent Actually Received from company ££

Higher should be taken– £££

Add> Expensive Living Accommodation

(Cost of Providing Accommodation - £ 75000) X 4%

£

Less> Non Availability (x/ X) £

Less> Employee Contribution £

Living Accommodation Benefit £££

6 years Rules

Less than 6 years > Purchase Price

More than 6 years > Current MV + All CapEx made up to date

Asset Benefits

£

Higher of:

i. Purchase Price / Market Value (MV)

ii. Rental Value

* Higher will be taken

Add > 20% X MV when it is first provided £

Less > Non Availability £

Less > Employee Contribution £

Assessable Benefit £££

Md. Inzamum-Ul-Haque [[email protected]]

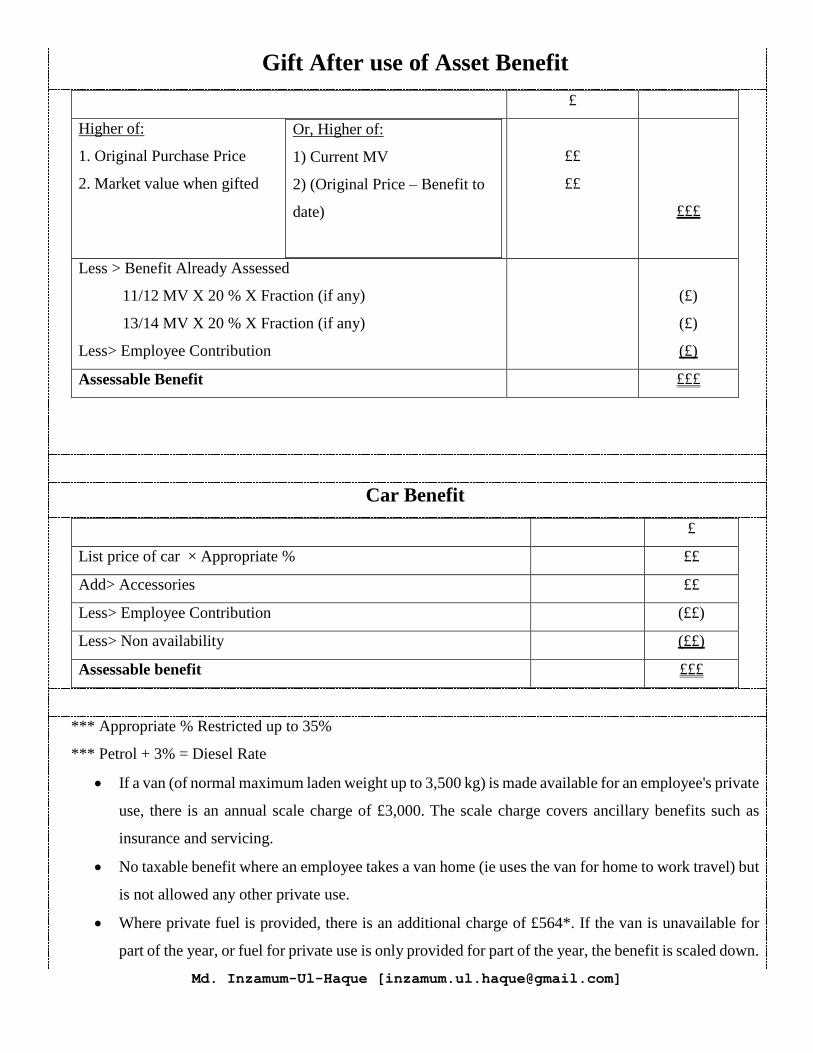

Gift After use of Asset Benefit

£

Higher of:

1. Original Purchase Price

2. Market value when gifted

Or, Higher of:

1) Current MV

2) (Original Price – Benefit to

date)

££

££

£££

Less > Benefit Already Assessed

11/12 MV X 20 % X Fraction (if any)

13/14 MV X 20 % X Fraction (if any)

Less> Employee Contribution

(£)

(£)

(£)

Assessable Benefit £££

Car Benefit

£

List price of car × Appropriate % ££

Add> Accessories ££

Less> Employee Contribution (££)

Less> Non availability (££)

Assessable benefit £££

*** Appropriate % Restricted up to 35%

*** Petrol + 3% = Diesel Rate

If a van (of normal maximum laden weight up to 3,500 kg) is made available for an employee's private

use, there is an annual scale charge of £3,000. The scale charge covers ancillary benefits such as

insurance and servicing.

No taxable benefit where an employee takes a van home (ie uses the van for home to work travel) but

is not allowed any other private use.

Where private fuel is provided, there is an additional charge of £564*. If the van is unavailable for

part of the year, or fuel for private use is only provided for part of the year, the benefit is scaled down.

Md. Inzamum-Ul-Haque [[email protected]]

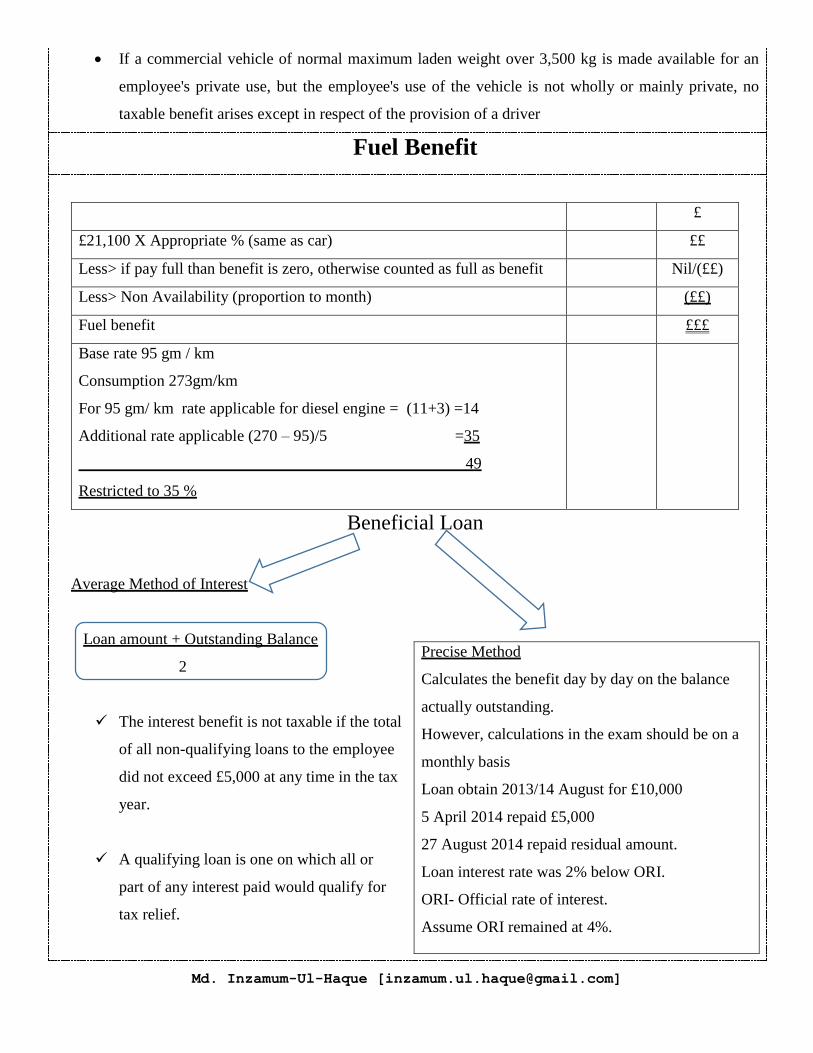

If a commercial vehicle of normal maximum laden weight over 3,500 kg is made available for an

employee's private use, but the employee's use of the vehicle is not wholly or mainly private, no

taxable benefit arises except in respect of the provision of a driver

Fuel Benefit

£

£21,100 X Appropriate % (same as car) ££

Less> if pay full than benefit is zero, otherwise counted as full as benefit Nil/(££)

Less> Non Availability (proportion to month) (££)

Fuel benefit £££

Base rate 95 gm / km

Consumption 273gm/km

For 95 gm/ km rate applicable for diesel engine = (11+3) =14

Additional rate applicable (270 – 95)/5 =35

49

Restricted to 35 %

Beneficial Loan

Average Method of Interest

Loan amount + Outstanding Balance

2

The interest benefit is not taxable if the total

of all non-qualifying loans to the employee

did not exceed £5,000 at any time in the tax

year.

A qualifying loan is one on which all or

part of any interest paid would qualify for

tax relief.

Precise Method

Calculates the benefit day by day on the balance

actually outstanding.

However, calculations in the exam should be on a

monthly basis

Loan obtain 2013/14 August for £10,000

5 April 2014 repaid £5,000

27 August 2014 repaid residual amount.

Loan interest rate was 2% below ORI.

ORI- Official rate of interest.

Assume ORI remained at 4%.

Md. Inzamum-Ul-Haque [[email protected]]

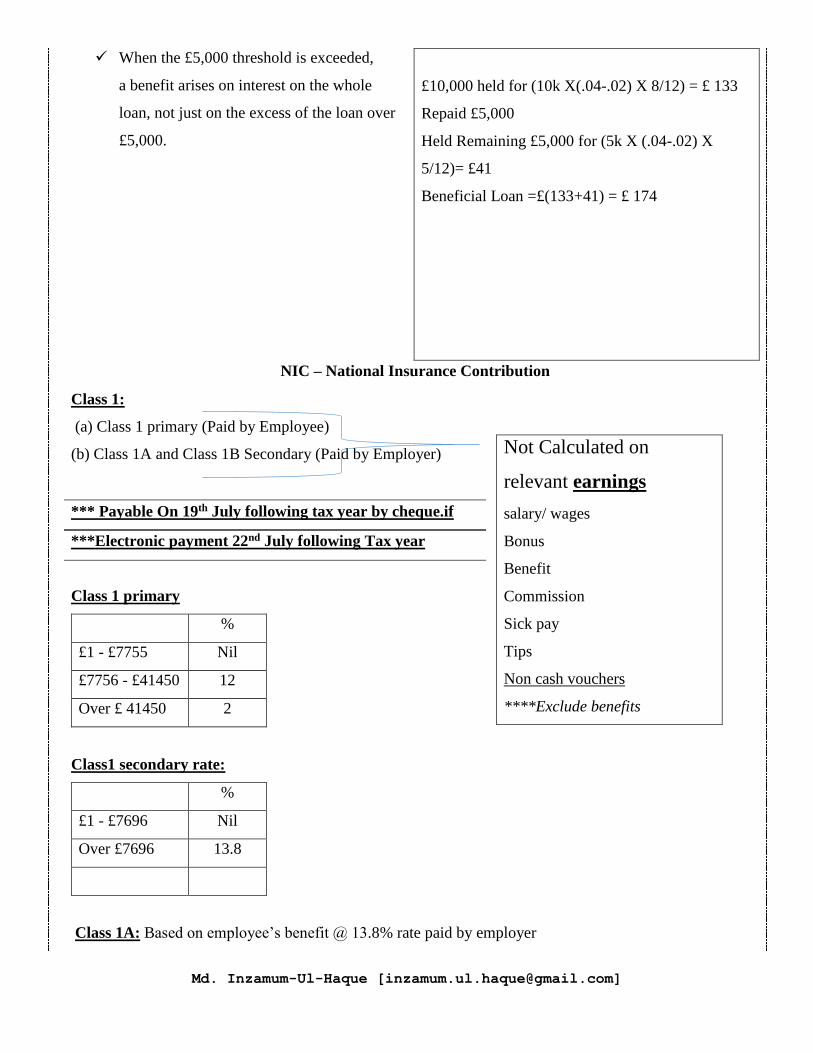

When the £5,000 threshold is exceeded,

a benefit arises on interest on the whole

loan, not just on the excess of the loan over

£5,000.

£10,000 held for (10k X(.04-.02) X 8/12) = £ 133

Repaid £5,000

Held Remaining £5,000 for (5k X (.04-.02) X

5/12)= £41

Beneficial Loan =£(133+41) = £ 174

NIC – National Insurance Contribution

Class 1:

(a) Class 1 primary (Paid by Employee)

(b) Class 1A and Class 1B Secondary (Paid by Employer)

*** Payable On 19th July following tax year by cheque.if

***Electronic payment 22nd July following Tax year

Class 1 primary

%

£1 - £7755 Nil

£7756 - £41450 12

Over £ 41450 2

Class1 secondary rate:

%

£1 - £7696 Nil

Over £7696 13.8

Class 1A: Based on employee’s benefit @ 13.8% rate paid by employer

Not Calculated on

relevant earnings

salary/ wages

Bonus

Benefit

Commission

Sick pay

Tips

Non cash vouchers

****Exclude benefits

Md. Inzamum-Ul-Haque [[email protected]]

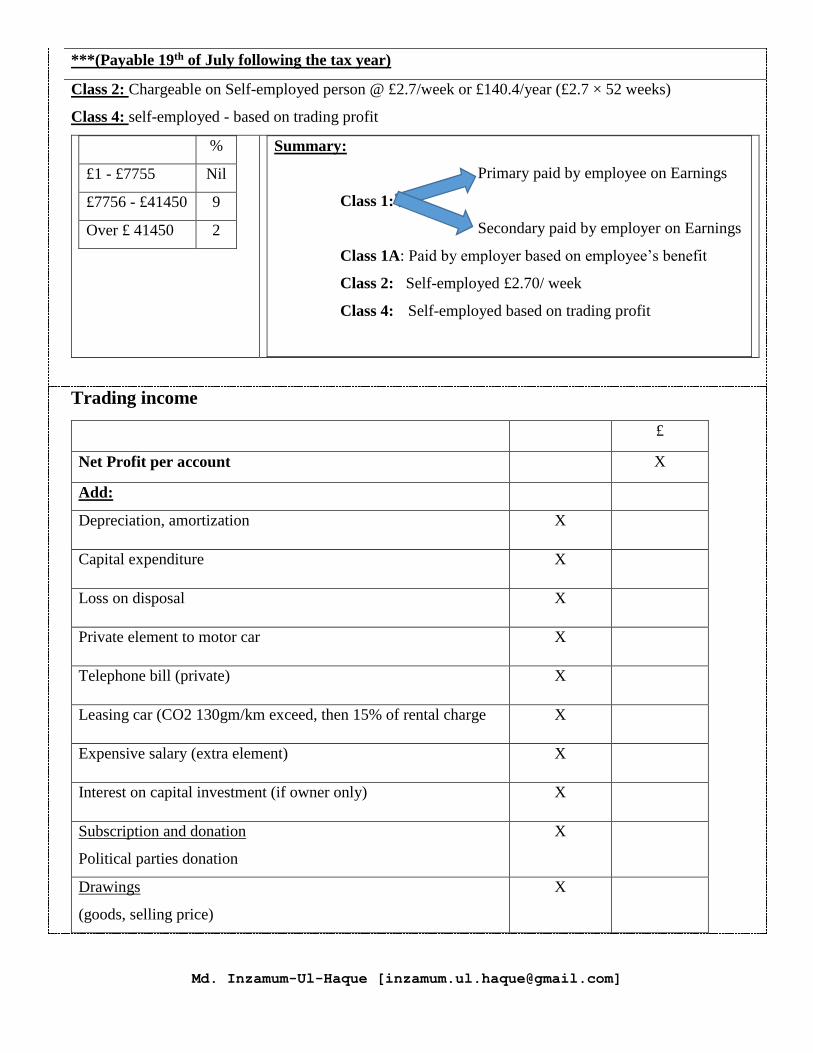

***(Payable 19th of July following the tax year)

Class 2: Chargeable on Self-employed person @ £2.7/week or £140.4/year (£2.7 × 52 weeks)

Class 4: self-employed - based on trading profit

%

£1 - £7755 Nil

£7756 - £41450 9

Over £ 41450 2

Summary:

Primary paid by employee on Earnings

Class 1:

Secondary paid by employer on Earnings

Class 1A: Paid by employer based on employee’s benefit

Class 2: Self-employed £2.70/ week

Class 4: Self-employed based on trading profit

Trading income

£

Net Profit per account X

Add:

Depreciation, amortization X

Capital expenditure X

Loss on disposal X

Private element to motor car X

Telephone bill (private) X

Leasing car (CO2 130gm/km exceed, then 15% of rental charge X

Expensive salary (extra element) X

Interest on capital investment (if owner only) X

Subscription and donation

Political parties donation

X

Drawings

(goods, selling price)

X

Md. Inzamum-Ul-Haque [[email protected]]

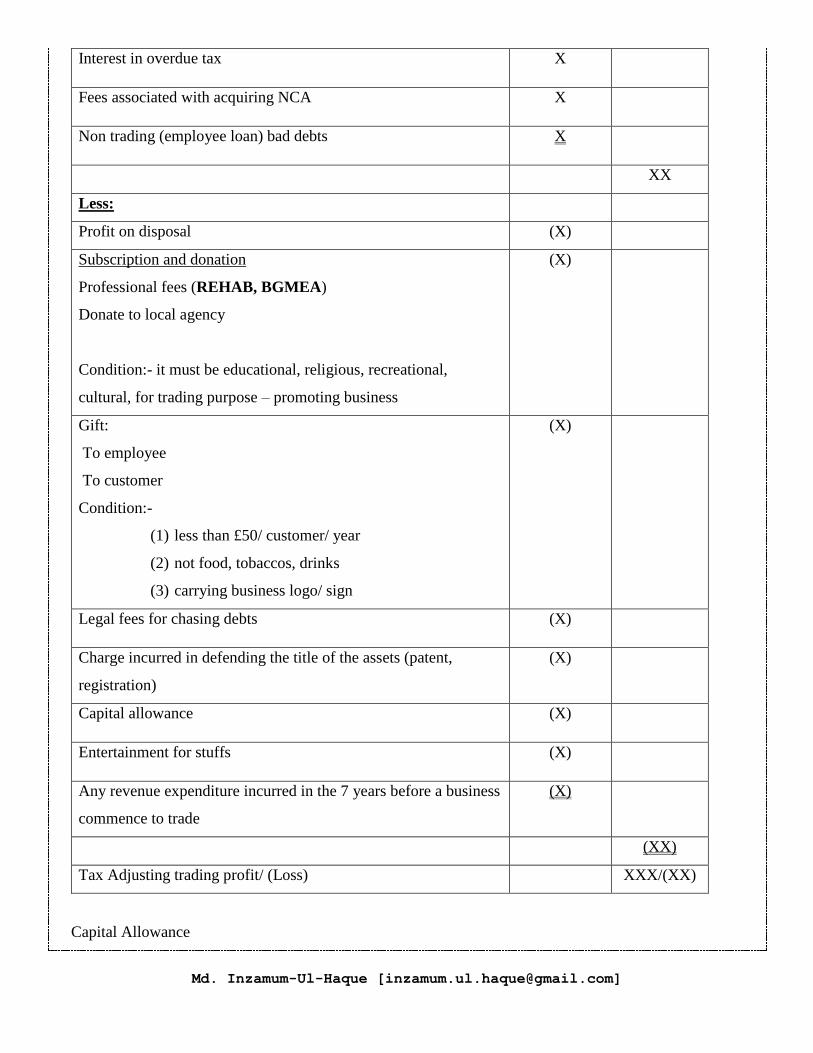

Interest in overdue tax X

Fees associated with acquiring NCA X

Non trading (employee loan) bad debts X

XX

Less:

Profit on disposal (X)

Subscription and donation

Professional fees (REHAB, BGMEA)

Donate to local agency

Condition:- it must be educational, religious, recreational,

cultural, for trading purpose – promoting business

(X)

Gift:

To employee

To customer

Condition:-

(1) less than £50/ customer/ year

(2) not food, tobaccos, drinks

(3) carrying business logo/ sign

(X)

Legal fees for chasing debts (X)

Charge incurred in defending the title of the assets (patent,

registration)

(X)

Capital allowance (X)

Entertainment for stuffs (X)

Any revenue expenditure incurred in the 7 years before a business

commence to trade

(X)

(XX)

Tax Adjusting trading profit/ (Loss) XXX/(XX)

Capital Allowance

Md. Inzamum-Ul-Haque [[email protected]]

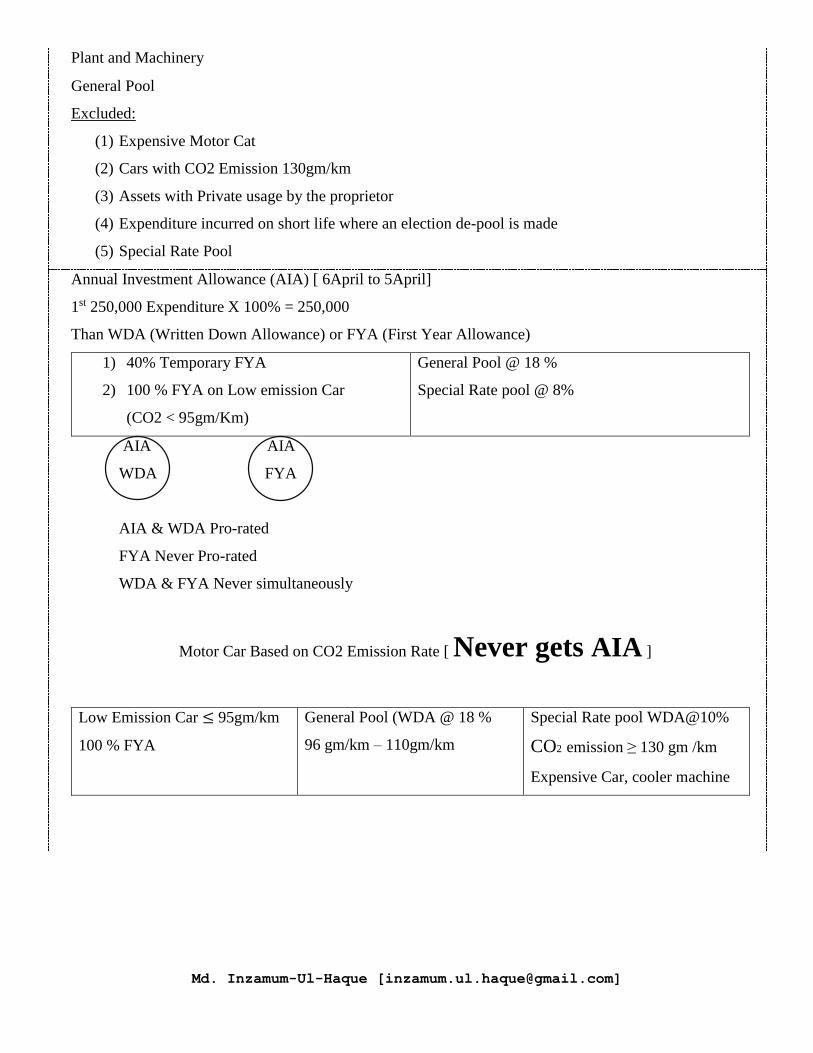

Plant and Machinery

General Pool

Excluded:

(1) Expensive Motor Cat

(2) Cars with CO2 Emission 130gm/km

(3) Assets with Private usage by the proprietor

(4) Expenditure incurred on short life where an election de-pool is made

(5) Special Rate Pool

Annual Investment Allowance (AIA) [ 6April to 5April]

1st 250,000 Expenditure X 100% = 250,000

Than WDA (Written Down Allowance) or FYA (First Year Allowance)

1) 40% Temporary FYA

2) 100 % FYA on Low emission Car

(CO2 < 95gm/Km)

General Pool @ 18 %

Special Rate pool @ 8%

AIA AIA

WDA FYA

AIA & WDA Pro-rated

FYA Never Pro-rated

WDA & FYA Never simultaneously

Motor Car Based on CO2 Emission Rate [ Never gets AIA ]

Low Emission Car ≤ 95gm/km

100 % FYA

General Pool (WDA @ 18 %

96 gm/km – 110gm/km

Special Rate pool WDA@10%

CO2 emission ≥ 130 gm /km

Expensive Car, cooler machine

Md. Inzamum-Ul-Haque [[email protected]]

Md. Inzamum-Ul-Haque [[email protected]]

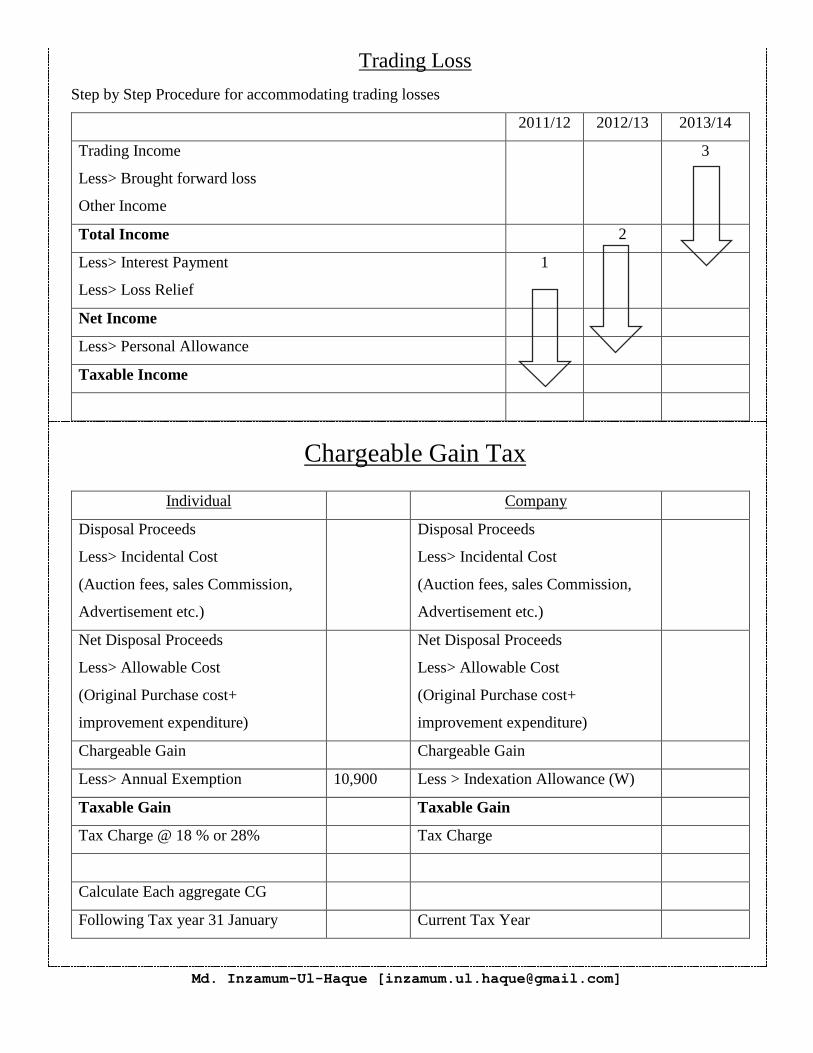

Trading Loss

Step by Step Procedure for accommodating trading losses

2011/12 2012/13 2013/14

Trading Income

Less> Brought forward loss

Other Income

3

Total Income 2

Less> Interest Payment

Less> Loss Relief

1

Net Income

Less> Personal Allowance

Taxable Income

Chargeable Gain Tax

Individual Company

Disposal Proceeds

Less> Incidental Cost

(Auction fees, sales Commission,

Advertisement etc.)

Disposal Proceeds

Less> Incidental Cost

(Auction fees, sales Commission,

Advertisement etc.)

Net Disposal Proceeds

Less> Allowable Cost

(Original Purchase cost+

improvement expenditure)

Net Disposal Proceeds

Less> Allowable Cost

(Original Purchase cost+

improvement expenditure)

Chargeable Gain Chargeable Gain

Less> Annual Exemption 10,900 Less > Indexation Allowance (W)

Taxable Gain Taxable Gain

Tax Charge @ 18 % or 28% Tax Charge

Calculate Each aggregate CG

Following Tax year 31 January Current Tax Year

Md. Inzamum-Ul-Haque [[email protected]]

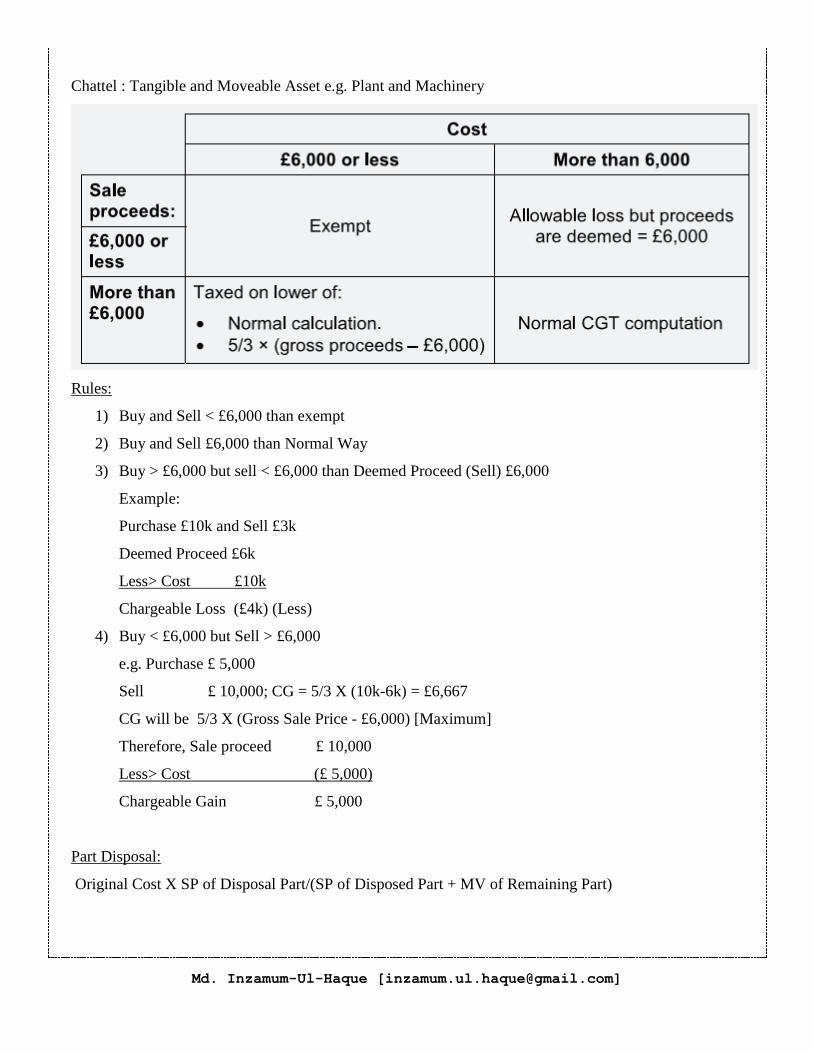

Chattel : Tangible and Moveable Asset e.g. Plant and Machinery

Rules:

1) Buy and Sell < £6,000 than exempt

2) Buy and Sell £6,000 than Normal Way

3) Buy > £6,000 but sell < £6,000 than Deemed Proceed (Sell) £6,000

Example:

Purchase £10k and Sell £3k

Deemed Proceed £6k

Less> Cost £10k

Chargeable Loss (£4k) (Less)

4) Buy < £6,000 but Sell > £6,000

e.g. Purchase £ 5,000

Sell £ 10,000; CG = 5/3 X (10k-6k) = £6,667

CG will be 5/3 X (Gross Sale Price - £6,000) [Maximum]

Therefore, Sale proceed £ 10,000

Less> Cost (£ 5,000)

Chargeable Gain £ 5,000

Part Disposal:

Original Cost X SP of Disposal Part/(SP of Disposed Part + MV of Remaining Part)

Md. Inzamum-Ul-Haque [[email protected]]

Shares and Securities

Determining Share price :

Lower of:

(1) LP+ ¼ (HP – LP) [ Quarter Method]

(2) (LP+HP)/2 [Average Method]

For Individual For Company

Rules:

(1) Take the Share same Day Purchase

(2) From following 30 Days

(3) Share Pool

Calculation :

(1) Share Acquisition the Same Day

Disposal Proceed

(Total Sales Price X Taken Same Day / No of share would sold)

Less> Cost (No of Share X Purchase Price)

Capital Gain

(2) Following 30 Days

Disposal Proceeds (Total Sales Price X Taken from 30 Days/ No of

share would sold)

Less> Cost (No of Share X Purchase Price)

Capital Gain

(3) Share Pool :

Disposal Proceed

(Total Sales Price X Taken Same Day / No of share would sold)

Less> Cost (W1)

Capital Gain

Workings:

Year No Of Share Cost

2011 XX ££

Rules:

(1) Same Day Purchase

(2) During the 9 Days

before the sale

(taking earlier

acquisitions first)

(3) Shares in the FA 1985

Share Pool

Md. Inzamum-Ul-Haque [[email protected]]

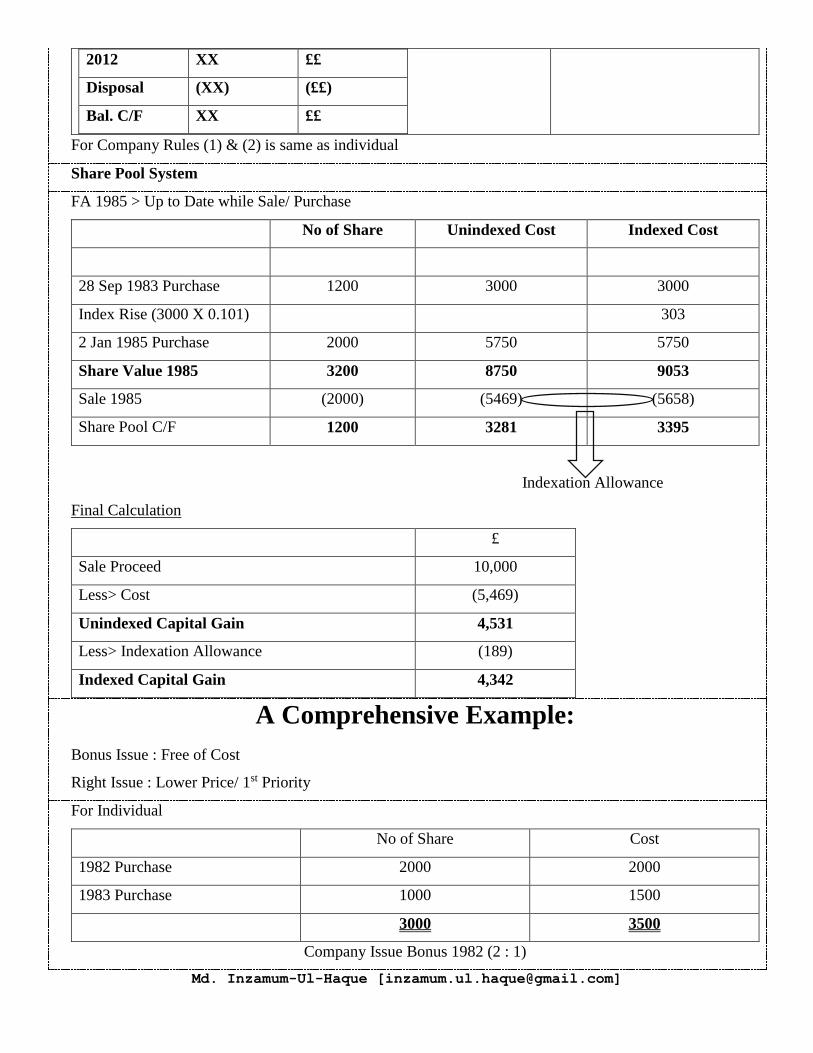

2012 XX ££

Disposal (XX) (££)

Bal. C/F XX ££

For Company Rules (1) & (2) is same as individual

Share Pool System

FA 1985 > Up to Date while Sale/ Purchase

No of Share Unindexed Cost Indexed Cost

28 Sep 1983 Purchase 1200 3000 3000

Index Rise (3000 X 0.101) 303

2 Jan 1985 Purchase 2000 5750 5750

Share Value 1985 3200 8750 9053

Sale 1985 (2000) (5469) (5658)

Share Pool C/F 1200 3281 3395

Indexation Allowance

Final Calculation

£

Sale Proceed 10,000

Less> Cost (5,469)

Unindexed Capital Gain 4,531

Less> Indexation Allowance (189)

Indexed Capital Gain 4,342

A Comprehensive Example:

Bonus Issue : Free of Cost

Right Issue : Lower Price/ 1st Priority

For Individual

No of Share Cost

1982 Purchase 2000 2000

1983 Purchase 1000 1500

3000 3500

Company Issue Bonus 1982 (2 : 1)

Md. Inzamum-Ul-Haque [[email protected]]

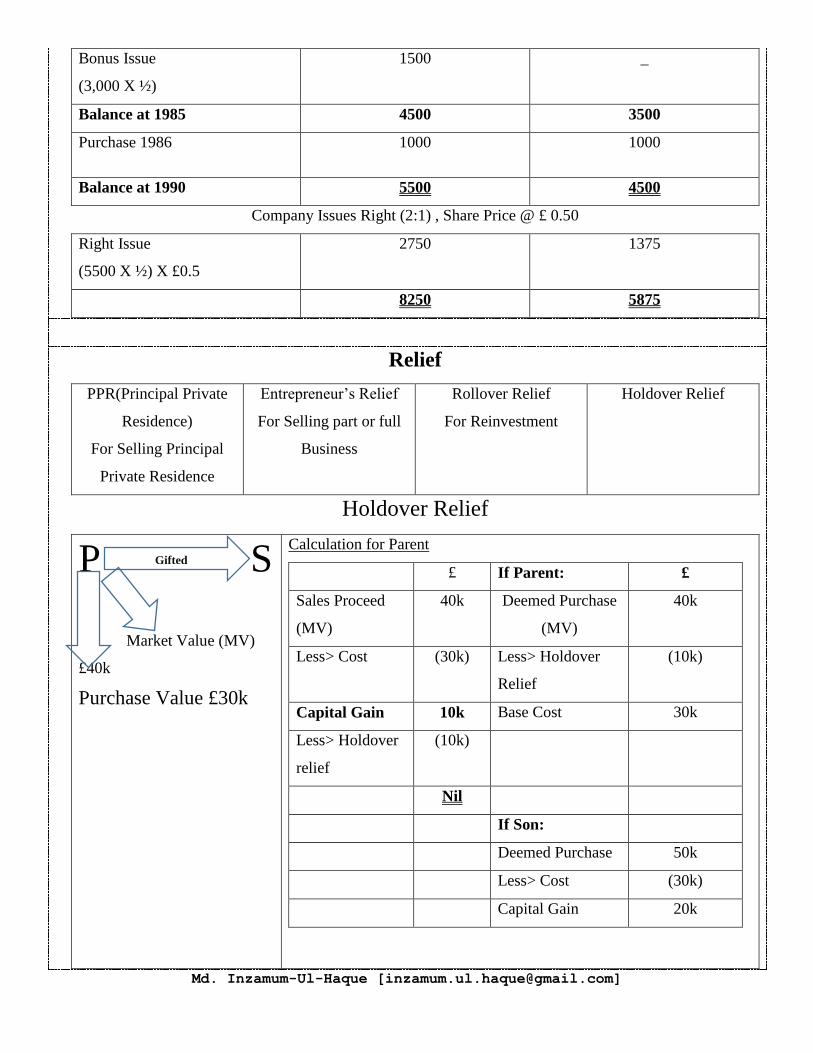

Bonus Issue

(3,000 X ½)

1500 _

Balance at 1985 4500 3500

Purchase 1986 1000 1000

Balance at 1990 5500 4500

Company Issues Right (2:1) , Share Price @ £ 0.50

Right Issue

(5500 X ½) X £0.5

2750 1375

8250 5875

Relief

PPR(Principal Private

Residence)

For Selling Principal

Private Residence

Entrepreneur’s Relief

For Selling part or full

Business

Rollover Relief

For Reinvestment

Holdover Relief

Holdover Relief

P S

Market Value (MV)

£40k

Purchase Value £30k

Calculation for Parent

£ If Parent: £

Sales Proceed

(MV)

40k Deemed Purchase

(MV)

40k

Less> Cost (30k) Less> Holdover

Relief

(10k)

Capital Gain 10k Base Cost 30k

Less> Holdover

relief

(10k)

Nil

If Son:

Deemed Purchase 50k

Less> Cost (30k)

Capital Gain 20k

Gifted

Md. Inzamum-Ul-Haque [[email protected]]

P S

Son Paid £20k

Or £35k

Calculation for Parent

£ Workings: £

Deemed Sales

Proceed

40k Actually Sales

Proceed

20k/35k

Less> Cost (30k) Less> Cost (30k)

Capital Gain 10k Chargeable

Gain

Nil/5k

Holdover Relief (10k)/(5k)(bal

fig.)

Chargeable Now Nil/ £5k

Calculation for

Son

Deemed Proceeds

(MV)

40k Payment from

when gifted

Less>Holdover

Relief

(5k) Less> Purchase

Price

Base Cost 35k Chargeable

Now

Rollover Relief

Asset cost £30k

Sales Proceed £60k

New Asset Cost £70k (PP) / if £50k

Full Reinvestment

£

Sales Proceed 60k

Less> Cost (30k)

Capital Gain 30k

Less> Rollover Relief (30k)

Chargeable Gain Nil

Partial Reinvestment

Lower Of:

Chargeable Gain (W1)

Not invested (60k – 50k) = 10k (Chargeable Now)

Workings 1:

Sales Proceed 60k

Less> Cost (30k)

Capital Gain 30k

A2 Reinvestment Cost 50k

Transfer Price $40k

PP

$3

0k

Md. Inzamum-Ul-Haque [[email protected]]

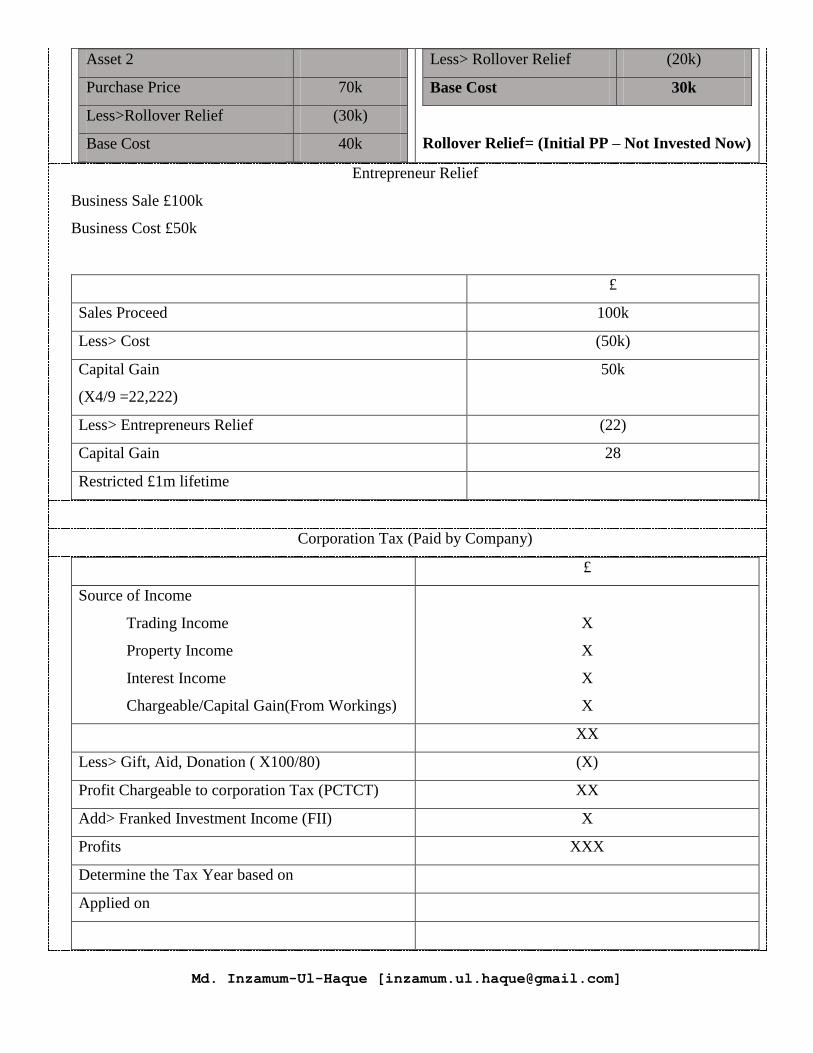

Asset 2

Purchase Price 70k

Less>Rollover Relief (30k)

Base Cost 40k

Less> Rollover Relief (20k)

Base Cost 30k

Rollover Relief= (Initial PP – Not Invested Now)

Entrepreneur Relief

Business Sale £100k

Business Cost £50k

£

Sales Proceed 100k

Less> Cost (50k)

Capital Gain

(X4/9 =22,222)

50k

Less> Entrepreneurs Relief (22)

Capital Gain 28

Restricted £1m lifetime

Corporation Tax (Paid by Company)

£

Source of Income

Trading Income

Property Income

Interest Income

Chargeable/Capital Gain(From Workings)

X

X

X

X

XX

Less> Gift, Aid, Donation ( X100/80) (X)

Profit Chargeable to corporation Tax (PCTCT) XX

Add> Franked Investment Income (FII) X

Profits XXX

Determine the Tax Year based on

Applied on

Md. Inzamum-Ul-Haque [[email protected]]

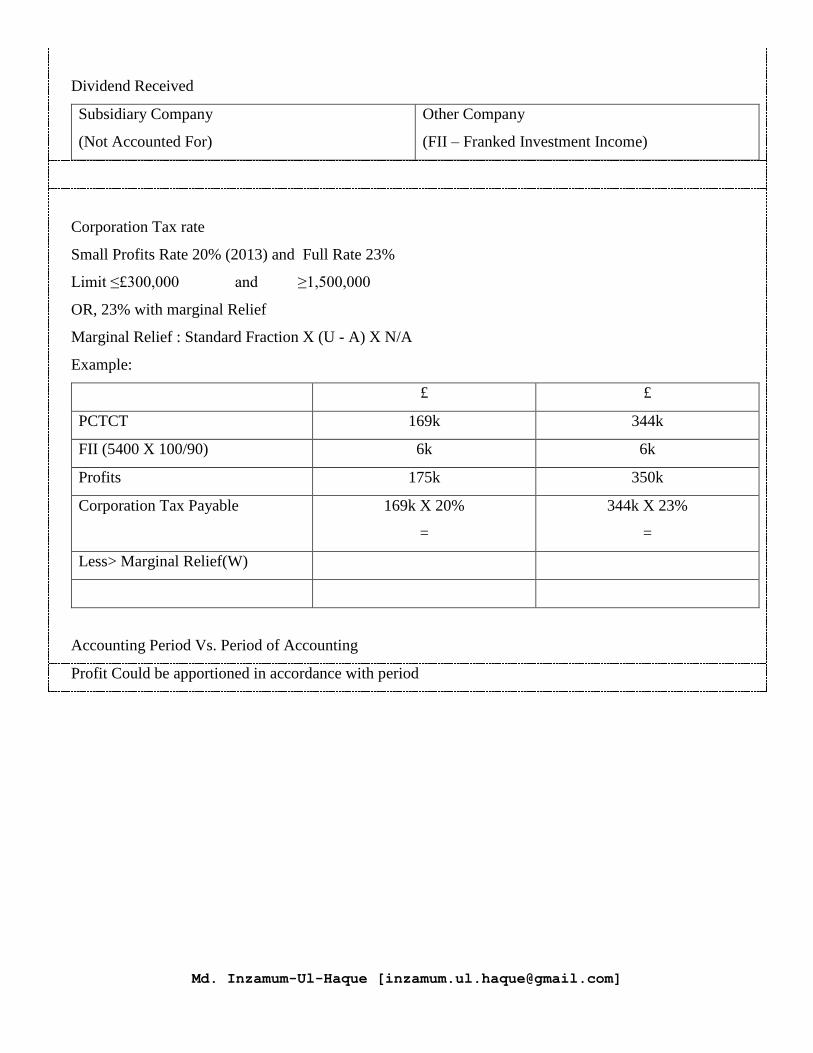

Dividend Received

Subsidiary Company

(Not Accounted For)

Other Company

(FII – Franked Investment Income)

Corporation Tax rate

Small Profits Rate 20% (2013) and Full Rate 23%

Limit ≤£300,000 and ≥1,500,000

OR, 23% with marginal Relief

Marginal Relief : Standard Fraction X (U - A) X N/A

Example:

£ £

PCTCT 169k 344k

FII (5400 X 100/90) 6k 6k

Profits 175k 350k

Corporation Tax Payable 169k X 20%

=

344k X 23%

=

Less> Marginal Relief(W)

Accounting Period Vs. Period of Accounting

Profit Could be apportioned in accordance with period