· ace acc X acc Z ace acc ; acc ; acc Z ace / sce / Created Date: 10/27/2014 3:57:20 PM

Upload

ed-clarkCategory

view

120download

0

INSURANCE/EMPLOYEE BENEFITS

SLIDES

Annuities

AnnuitizationAccumulation

Exclusion RatioLIFO

Exclusion Ratio- Fixed Annuities

Exclusion Ratio = Total Basis Total Expected Payments

Exclusion Ratio- Variable Annuities

$ Exclusion = Total Basis Total Expected # of Payments

(Also can be used for fixed annuities)

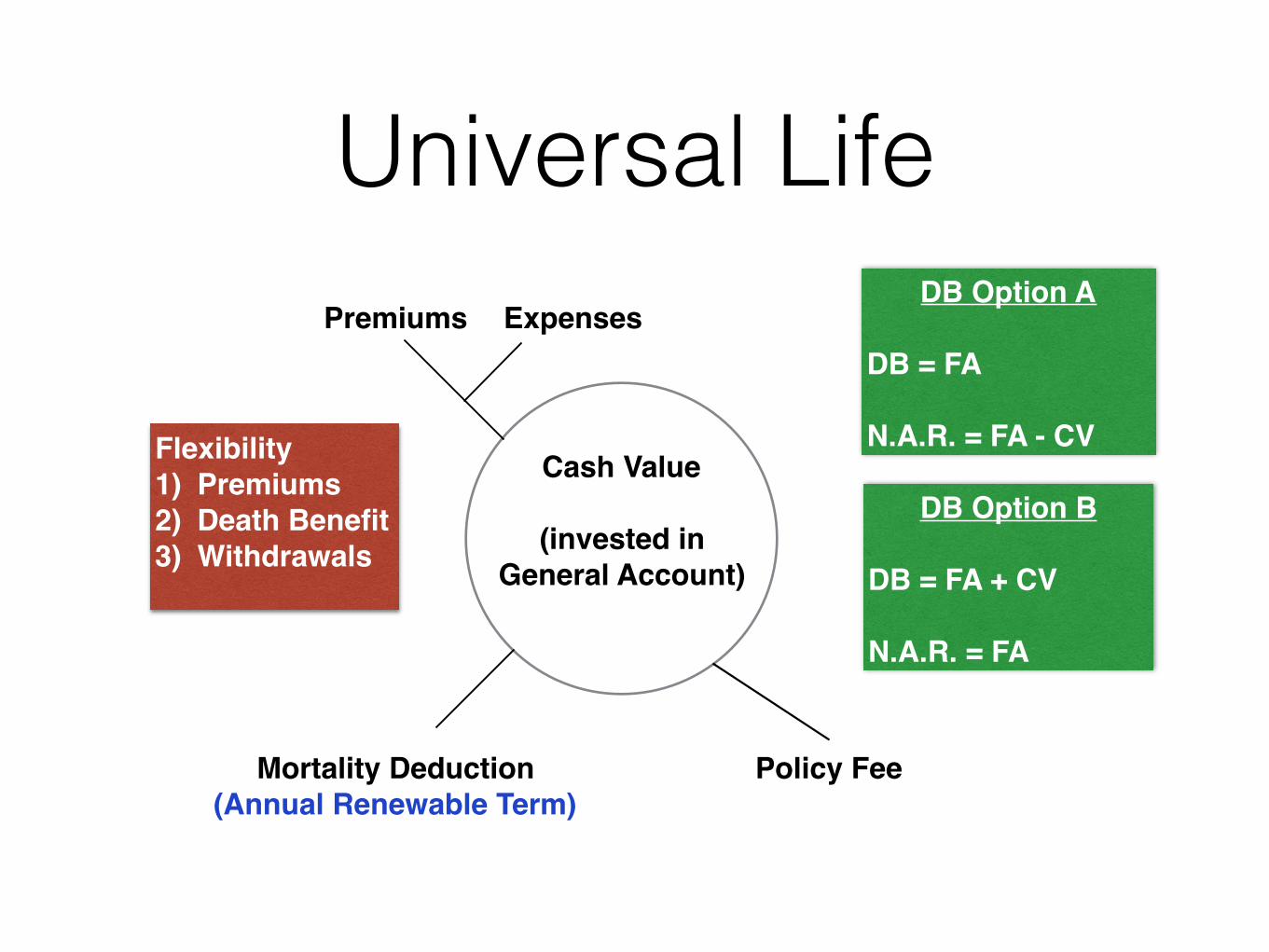

Universal LifeDB Option A

DB = FA

N.A.R. = FA - CV Cash Value

(invested in General Account)

Mortality Deduction(Annual Renewable Term)

Premiums

Policy Fee

ExpensesDB Option A

DB = FA

N.A.R. = FA - CV

DB Option B

DB = FA + CV

N.A.R. = FA

Flexibility1) Premiums2) Death Benefit3) Withdrawals

Variable Universal LifeDB Option A

DB = FA

N.A.R. = FA - CV Cash Value

Mortality Deduction(Annual Renewable Term)

Premiums

Policy Fee

ExpensesDB Option A

DB = FA

N.A.R. = FA - CV

DB Option B

DB = FA + CV

N.A.R. = FA

Flexibility1) Premiums2) Death Benefit3) Withdrawals

Revenue Ruling 2009-13"Investment in Contract" = Premiums Paid - Loans/Withdrawals - Dividends Rec'd in Cash

"Basis in Contract" = Premiums Paid - Loans/Withdrawals

- Dividends Rec'd in Cash - Cost of Insurance

Life Policy- Gain at Surrender"Investment in Contract" = Premiums Paid - Loans/Withdrawals - Dividends Rec'd in Cash

Gain at Surrender = CSV - "Investment in Contract" (Taxed as O.I.)

Life Policy- Gain at Sale"Basis in Contract" = Premiums Paid - Loans/Withdrawals

- Dividends Rec'd in Cash - Cost of Insurance

Gain at Sale = Amt. Realized - "Basis in Contract" (Taxed as O.I. & CG)

Major Medical ChartPolicy

Provisions$$$

AllocatedInsured

PaysInsurance Company

Pays

Dedt $500 $500 $500 -------

Coinsurance80/20 with

$5,000 coinsurance

limit

$5,000 $1,000 $4,000

100% Insurer pays 100% Remainder ------- 100%

Major Medical ExamplePolicy

Provisions$$$

AllocatedInsured

PaysInsurance Company

Pays

Dedt$250 per person

(limit of 3)$750 $750 -------

Coinsurance80/20 ($5,000 coinsurance)-

everyone $20,000 $4,000 $16,000

100% Insurer pays 100% Remainder ------- $9,250

Form 1040All Income (from whatever source derived)- ExclusionsGross Income

- Deductions ("Above the Line")AGI

- Greater of:Standard DeductionItemized Deductions

- Personal/Dependency ExemptionsRegular Taxable Income*

* Regular Taxable Income is the starting point for calculating AMTI

Medicare Part A- Hospital• Insured pays (2017):

• Days 0-60: $1,316 deductible/benefit period • New benefit period begins after patient is

out of hospital for 60 days • Days 61-90: $329/day • Days 91-150: $658/day if lifetime reserve

day used- otherwise, all cost • 60 lifetime reserve days provided

Medicare Part A- Skilled Nursing Facility Care

• Insured pays (2017): • Days 0-20: $0 • Days 21-100: $164.50/day • Days 101+: All cost

Medicare Part D- Prescription Drug• Insured pays (2017):

• $400 deductible • 25% coinsurance until insured/insurer have

paid $3,700 OOP including deductible • Until $1,250 OOP reached:

• 40% of brand-name drugs • 51% of generic drugs

• Coinsurance or copayment for all remaining costs

MedigapA B C D F G K L M N

Basic Benefits X X X X X X X X X X

Part A Deductible

X X X X X 50% 75% 50% X

Skilled Nursing X X X X 50% 75% X X

Part B Deductible

X X X

Part B Excess X X

Foreign Travel X X X X X X

SIS Rider Example$4,000 Base Benefit $1,000 Social Insurance Substitute Rider 90-Day Elimination Period Social Security pays $800 after 5 months

MonthsDI Base Benefit

PmtSoc Sec

PmtSIS Rider

Pmt

1-3 $0 $0 $0

4-5 $4,000 $0 $1,000

6+ $4,000 $800 $200

HO Coinsurance Formula

Ins. Amount * Loss - Deductible 80% of RC

NQSOs

Grant No Tax

ExerciseBargain Element (FMV-EP)

is W-2 Income (subject to FICA)

Sale(Amt. Realized - Basis) is

Capital Gain

(Basis is FMV @ purchase)

ISOs

Grant No Tax

Exercise

Reg.: None

AMT: Bargain element is AMTI(Positive adjustment)

Sale

HPR met: All gain is LTCG

HPR not met: Bargain element is W-2 Income (no FICA); other gain is Capital Gain (L/T or S/T)

AMT

All Income Regular Taxable Income- ExclusionsGross Income

- Deductions ("Above the Line")AGI

- Greater of:Standard DeductionItemized Deductions

- Personal/Dependency Exemptions Regular Taxable Income AMT Income

+++

ISO Negative AdjustmentER grants EE an ISO with exercise price of $25. EE exercises 2 years later when the stock has FMV of $35. EE sells stock 2 years after exercise when stock has FMV of $50.

HPR are met.

Grant $0 Regular Income $0 AMTI

Exercise $0 Regular Income $10 AMTI (Pos. Adj.)

Sale $25 Regular Income(LTCG)

$25 ($10 AMTI Neg. Adj.)

$15 AMTI

Cashless Exercise

Bargain Element x Tax Rate x # Shares Exercise Price x # Shares +

FMV at Exercise

Income TaxCost of Exercising

ESPP TaxationGrant No Tax

Exercise No Tax

Sale

HPR Met:

W-2 income (LESSER of):FMV @ grant - option price

Sale price - option price

Capital gain for remainder

HPR NOT Met:

W-2 income:FMV @ purchase - option price

Capital gain for remainder

ESPP Example (Qualifying Disposition)Assume 6-mo. offering period Option price will be 85% of lesser of:

FMV on 1st or last day of offering period FMV of stock on 1st day of offering period: $100 FMV of stock on last day of offering Period: $110 Option price = .85 * 100 = $85 FMV of stock @ purchase (last day of offering period): $110 Stock is sold 2 years after purchase for $130 (HPR met)

Grant date → No tax Exercise date → No tax Sale date → Total gain = $130 - $85 = $45 W-2 income is LESSER of: FMV @ grant – option price OR Sale price – option price ($100 - $85) = $15 OR ($130 - $85) = $45

Tax consequence is:$15 W-2 income $30 LTCG

ESPP Example (Disqualifying Disposition)Assume 6-mo. offering period Option price will be 85% of lesser of:

FMV on 1st or last day of offering period FMV of stock on 1st day of offering period: $100 FMV of stock on last day of offering Period: $110 Option price = .85 * 100 = $85 FMV of stock @ purchase (last day of offering period): $110 Stock is sold 15 months after purchase for $130 (HPR not met)

Grant date → No tax Exercise date → No tax Sale date → Total gain = $130 - $85 = $45 W-2 income: FMV @ purchase – option price $110 - $85 = $25

Tax consequence is:$25 W-2 income $20 LTCG

Phantom Stock vs. Stock Appreciation Rights

Phantom Stock Stock Appreciation Rights

Value given to EE Full value of shares or Appreciation Appreciation

Payment made in ... Cash (OI)

Cash (OI) or Shares (OI @ distribution &

CG for further appreciation)

Timing of payments Determined by plan (EE has no control) EE determines

NQDC PLANS FUNDED UNFUNDED (No Substantial Risk (Substantial Risk of Forfeiture) of Forfeiture)

Secular Trust Promise to Pay

Surety Bond (ER buys) Rabbi Trust