ACC 424 Financial Reporting II Lecture 5 Introduction to consolidations.

15

ACC 424 Financial Reporting II Lecture 5 Introduction to consolidations

-

Upload

jeffery-mccormick -

Category

Documents

-

view

219 -

download

1

Transcript of ACC 424 Financial Reporting II Lecture 5 Introduction to consolidations.

ACC 424Financial Reporting II

Lecture 5

Introduction to consolidations

2

Agenda

• Nature of consolidated financial statements

• Why consolidate?

• Who has to consolidate?

• Consolidation at acquisition

• Consolidation after acquisition

3

Nature of consolidation• Consolidated financial statements report the financial affairs of affiliated

corporations as though they are a single firm

– A parent corporation & its subsidiaries are often referred to as affiliated corporations

• No separate books for the consolidated entity. Each affiliated corporation has

its own set of books & financial statements – The statements are prepared using working papers (spreadsheets)

• Intercompany transactions are eliminated:

– e.g., revenues are the revenues from sales of the group to outside customers

• Intercompany receivables & payables are also eliminated

4

Nature of consolidation• Consolidation’s effect on financial statements can be

significant• Prior to FAS 94 (1987) corporations did not have to consolidate

financial subsidiaries. If the big 3 US automakers had consolidated their financial subsidiaries in 1986, the effects would have been substantial:

Return on Assets Debt/Equity

Unconsolidated Consolidated Unconsolidated Consolidated

Ford 9% 4% 1.6 5.4

GM 4% 2% 1.4 3.9

Chrysler 10% 5% 1.7 5.2

Average Impact -52% +207%

Source: Seidler (1987)

5

Why consolidate?• Rationale for required consolidation

– Information motivation• Consolidations required to avoid “fooling” investors & creditors (e.g., financial

subsidiaries used to keep debt off balance sheets) • Current concern that joint ventures and other devices used for the same purpose• Among informed users (banks & securities firms) who lobbied on FAS 94 there was

little support for the standard (Mian & Smith, 1990)

• Evidence from voluntary consolidations– Australia in 1930s & 1950s (Whittred)– Of financial, insurance & real estate subsidiaries in the US prior to FAS 94

(Mian & Smith)

• Evidence from insurance company debt contracts– Contracts undo the equity method of accounting for unconsolidated subsidiaries

6

Who has to consolidate?Current standards

A parent owning >50% of the voting stock (legal control) except:

i) if control is temporary; or

ii) control does not rest with the majority owner (legal reorganization, bankruptcy, severe foreign exchange restrictions, controls or government imposed uncertainties)

7

Who has to consolidate?Exposure Draft, February, 1999

as modified to 12/31/99

• A parent must consolidate each subsidiary that it controls.

• Once a subsidiary is consolidated must be consolidated until parent ceases to control it

• Control involves 2 essential characteristics– A parent’s non-shared decision-making ability

– A parent’s ability to use that power to increase to increase the benefits it derives & limit the losses it suffers from the subsidiary’s activities

8

Who has to consolidate?Exposure Draft, February, 1999

as modified to 12/31/99

Control is presumed if an entity (including its subsidiaries):– Has majority voting interest in the election of a corporation’s governing body or a

right to appoint a majority of the members of that body– Has a large minority voting interest in the election of the governing body and no

other party or organized group of parties has a significant voting interest– Has a unilateral ability to

• Obtain a majority voting interest in the election of the governing body or• Obtain a right to appoint a majority of the governing body via currently

exercisable rights and expected benefits of exercising rights exceeds expected cost

– Is the only general partner in a limited partnership

A minority interest is large if it exceeds 50% of votes typically cast in a corporation’s election of directorsFor example, if only 60% of eligible votes are typically cast, 35% would be deemed large

9

Consolidation at acquisitionE3.4

1. Give the journal entry to record the business combination as a purchase & elimination entries necessary to prepare a consolidated balance sheet at the business combination date assuming the purchase method is used.2. Give the journal entry to record the business combination as a pooling of interests & elimination entries necessary to prepare a consolidated balance sheet at the business combination date assuming the pooling of interests method is used.

10

Consolidation at acquisitionE3.4 - Purchase

First determine the differential between price & book value (premium or discount)

Market value of shares issued $2,000,000

Accountants’ & attorneys’ fees 100,000

Total acquisition cost $2,100,000

Net book value acquired .9 $2,000,000 $1,800,000

Differential (premium) $ 300,000

Allocation to fair market values of assets & liabilities and goodwill

Increase in the value of inventory .9 $100,000 $ 90,000

Increase in net plant assets .9 $200,000 180,000

Increase in LT marketable securities .9 $20,000 18,000

$288,000

Less Increase in LT debt .9 $100,000 90,000

Share of value increase of identifiable net assets $198,000

Goodwill 102,000

Differential (premium) $300,000

11

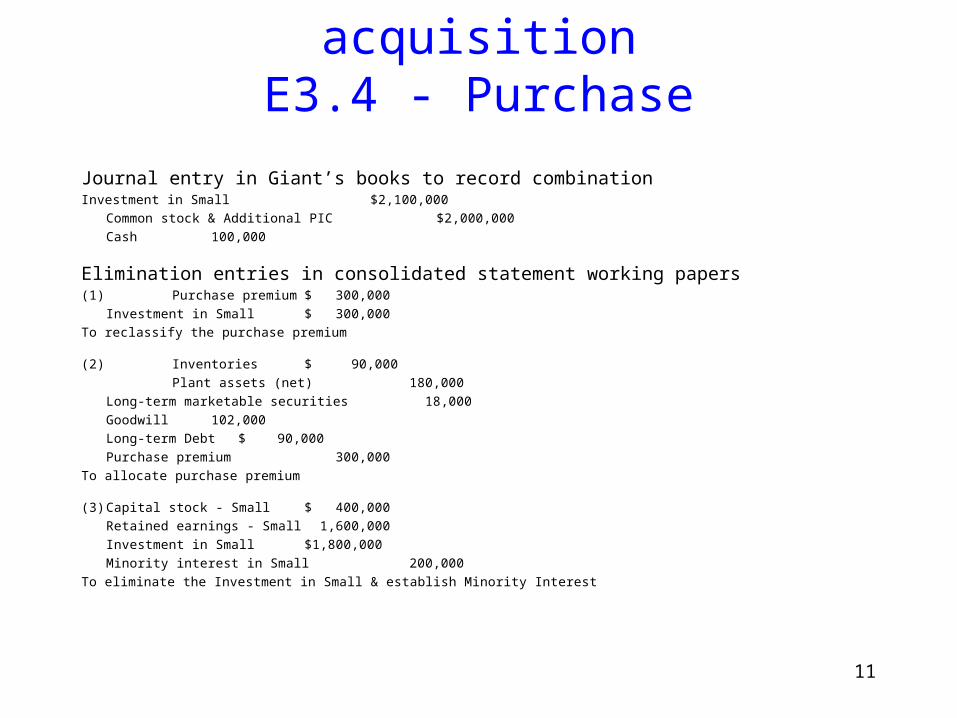

Consolidation at acquisitionE3.4 - Purchase

Journal entry in Giant’s books to record combinationInvestment in Small $2,100,000

Common stock & Additional PIC $2,000,000

Cash 100,000

Elimination entries in consolidated statement working papers(1) Purchase premium $ 300,000

Investment in Small $ 300,000

To reclassify the purchase premium

(2) Inventories $ 90,000

Plant assets (net) 180,000

Long-term marketable securities 18,000

Goodwill 102,000

Long-term Debt $ 90,000

Purchase premium 300,000

To allocate purchase premium

(3) Capital stock - Small $ 400,000

Retained earnings - Small 1,600,000

Investment in Small $1,800,000

Minority interest in Small 200,000

To eliminate the Investment in Small & establish Minority Interest

12

Consolidation at acquisitionE3.4 - purchase

13

Consolidation at acquisitionE3.4 - points on purchase

– The individual assets & liabilities of Small replace the Giant’s Investment in Small in the consolidated financial statements

– To that end Investment in Small is eliminated against Small’s stockholders’ equity and the purchase premium leaving minority interest

– Small’s individual assets & liabilities are increased by 90% of valuation difference and goodwill is included at 90% of its value

– The exposure draft would increase individual assets & liabilities by 100% of the valuation difference by increasing minority interest for its share of the write-up

– As of January, 1997, the board has also decided to increase goodwill to 100% of its value by including the minority share

– Note minority interest in subsidiary would be called noncontrolling interest in subsidiary under the exposure draft

14

Consolidation at acquisition E3.4 - pooling

Journal entry in Giant’s books to record combination

Investment in Small $1,800,000

Expenses of business combination 100,000

Stockholders’ equity $1,800,000

Cash 100,000

Elimination in consolidated statement working papers

Capital stock - Small $ 400,000

Retained earnings - Small 1,600,000

Investment in Small $1,800,000

Minority interest in Small 200,000

15

Consolidation at acquisitionE3.4 - pooling