Details of Unclaimed/Unpaid Dividend (1st Interim Dividend ...

Upload

alexina-wellsCategory

view

215download

0

Academy 03Basic Turbo’s and short selling

2

Part of company Dividend

Stocks

3

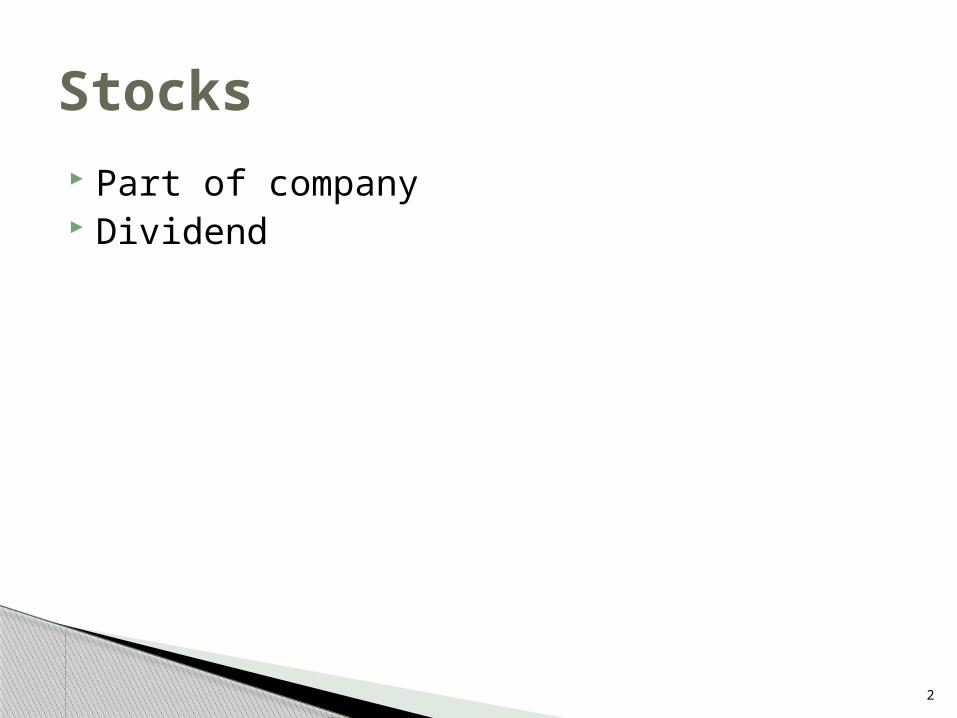

Loan Coupons

Bonds

C = coupon payment n = number of payments i = interest rate, or required yield M = value at maturity, or par value

4

Bull and Bear market Lending and selling a share Stocks and bonds

Short and Long

5

Negative aspects Naked short selling Credit Crisis

Criticism

6

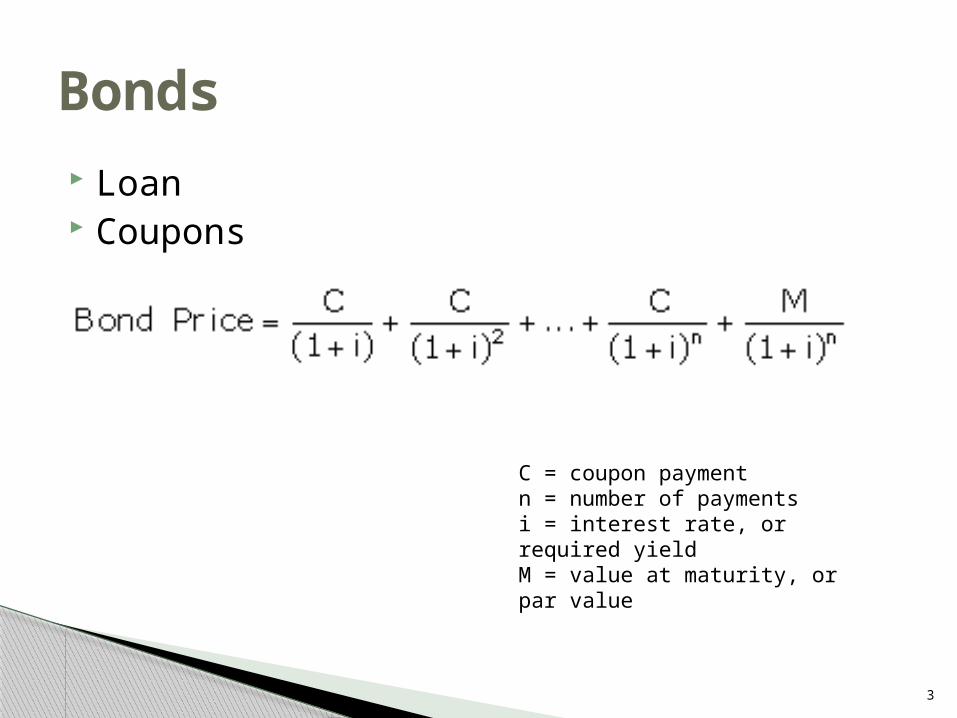

Short Squeeze

7

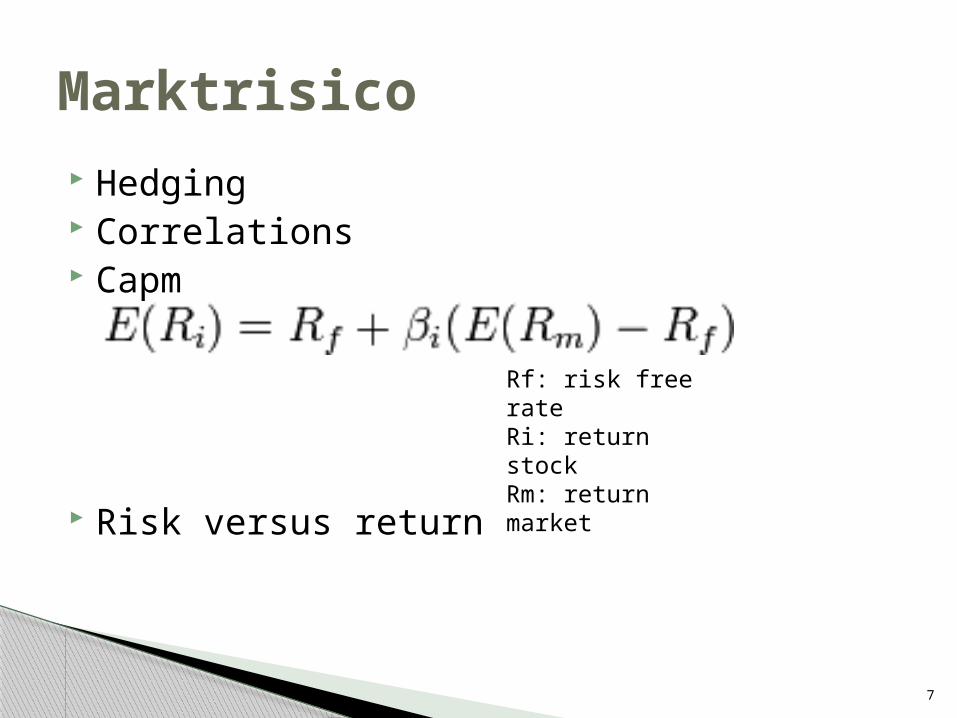

Hedging Correlations Capm

Risk versus return

Marktrisico

Rf: risk free rateRi: return stockRm: return market

8

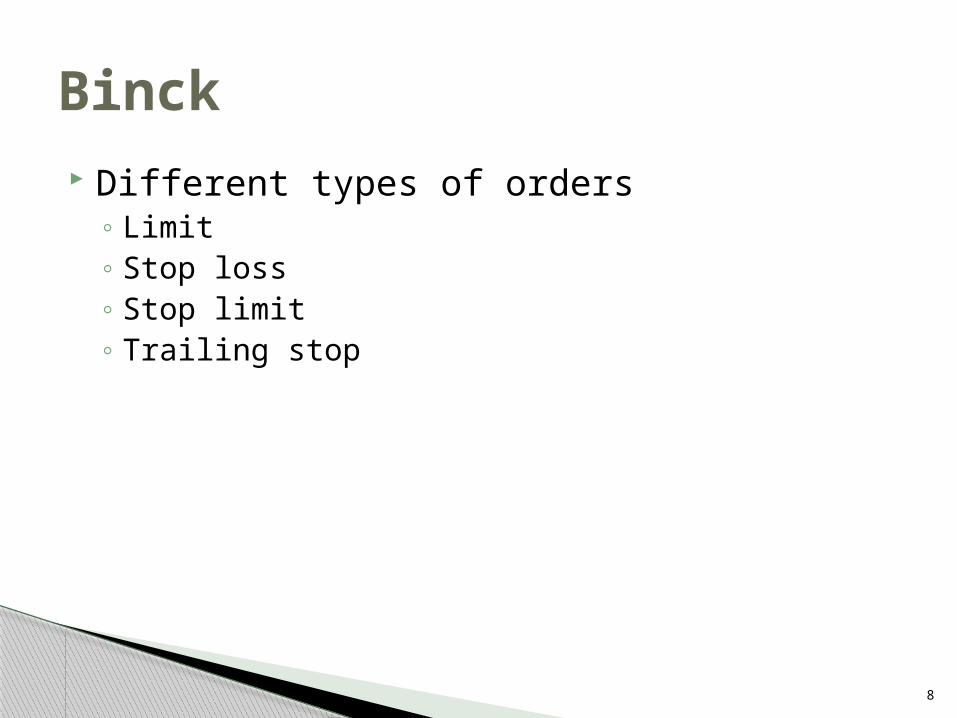

Different types of orders◦ Limit◦ Stop loss◦ Stop limit◦ Trailing stop

Binck

9

Unit4

Proposal

10

Break

12

13

Turbo’s Why important? Possibility to enhance your return in relation

to a direct investment

More advantageous in short-term investing◦ B&R Competition

14

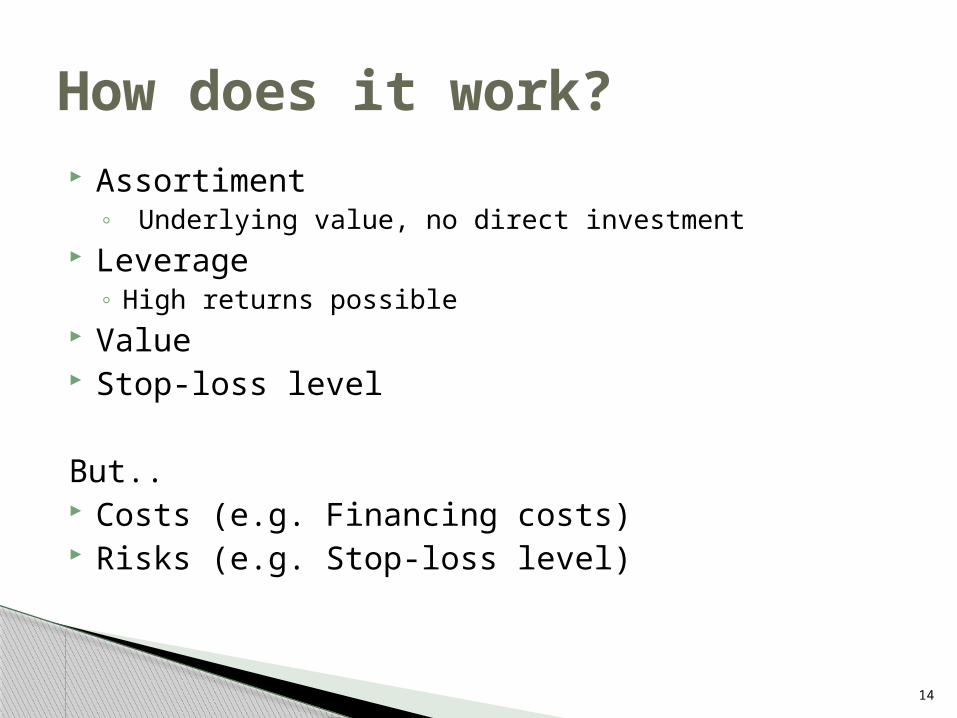

How does it work? Assortiment

◦ Underlying value, no direct investment Leverage

◦ High returns possible Value Stop-loss level

But.. Costs (e.g. Financing costs) Risks (e.g. Stop-loss level)

15

Assortiment What products can be trade with turbo’s?

◦ Regular stocks◦ Bonds◦ Indices◦ Valuata’s◦ Commodities◦ ...

◦ Turbo’s short vs. longwww.abnamromarkets.nl/turbo

16

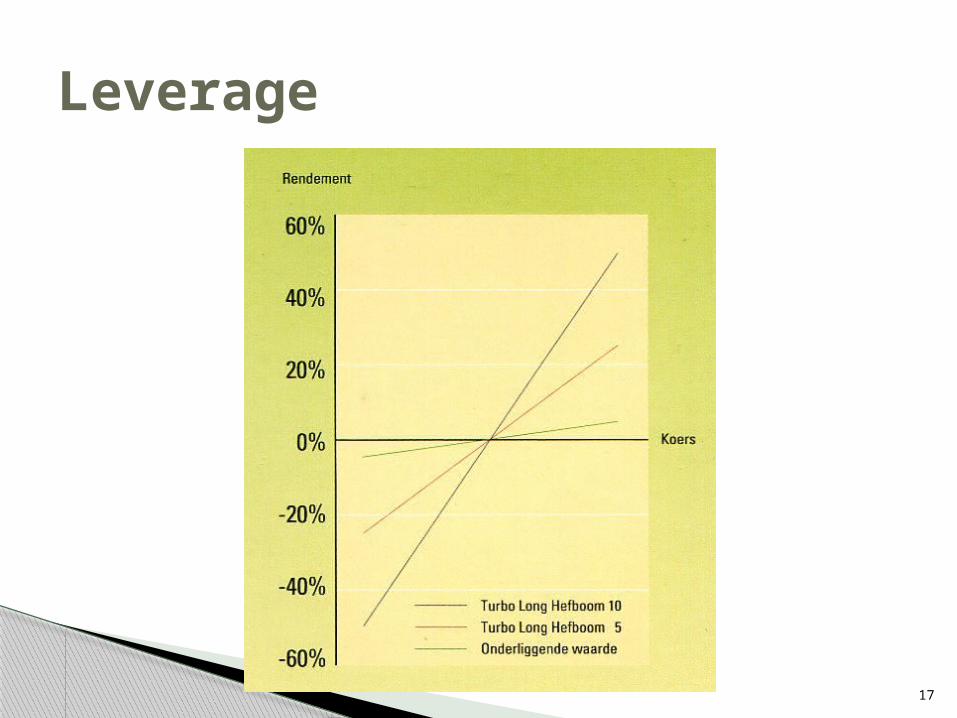

Leverage

17

Leverage

18

Leverage

19

Value Value equal to the difference between price

of underlying value and financing level turbo

Value turbo long = Price underlying value – financing levelValue turbo short = Financing level – Price underlying value

Note: Currency exchange rate

20

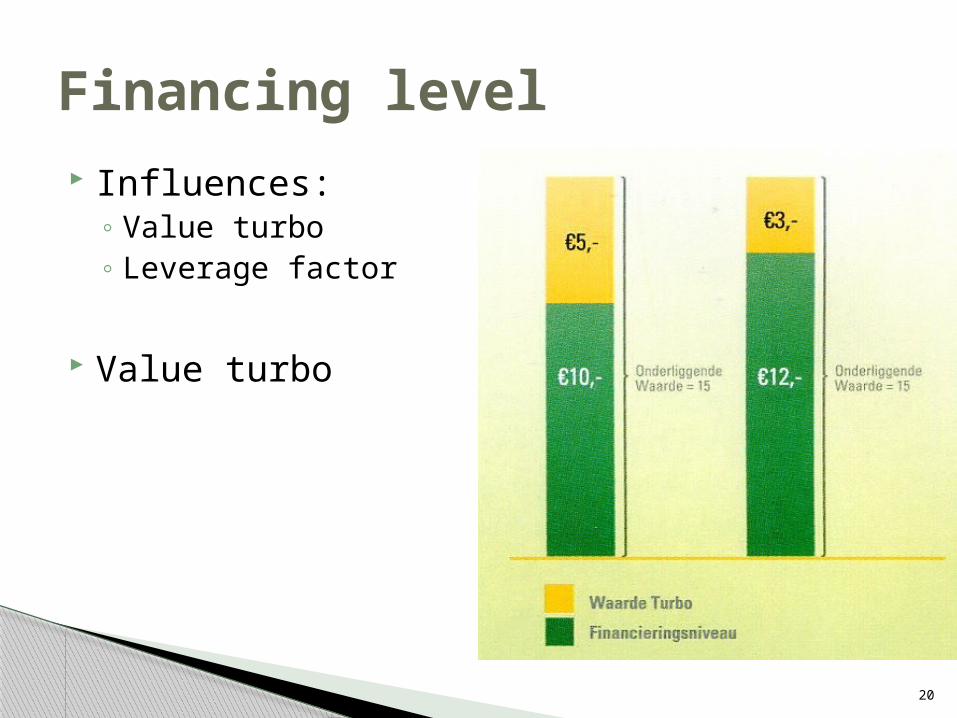

Financing level Influences:

◦ Value turbo◦ Leverage factor

Value turbo

21

Stop-loss level No expiration date Value turbo never negative

So, existence of stop-loss level◦ Losses at max total investment◦ Removed from exchange◦ Residual value

22

Tradability Euronext Amsterdam 9:05 till 17:30 Normal bid (bied) – offer (laat)

23

24

Costs Financing costs/benefits

◦ Daily completion◦ Libor rate (Londen Interbank offered rate)◦ Turbo short(costs) vs. Turbo long(benefits)

Buy and sell costs (depends on broker) Taxes

◦ We advice to go to tax adviser if necessary

25

Risks Price Leverage Stop-Loss

26

Risks Exchange rate risks

◦ Abroad investment Interest rate risk (changing) Credit risk

◦ Bankruptcy ABN Amro

27

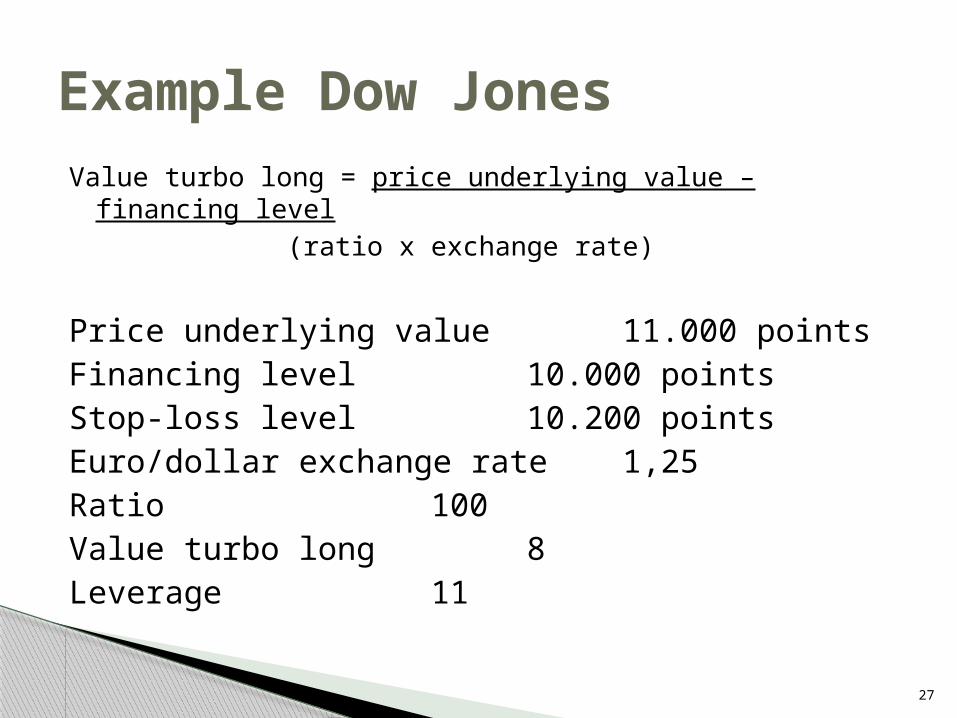

Example Dow JonesValue turbo long = price underlying value – financing level

(ratio x exchange rate)

Price underlying value 11.000 pointsFinancing level 10.000 pointsStop-loss level 10.200 pointsEuro/dollar exchange rate 1,25 Ratio 100Value turbo long 8Leverage 11

28

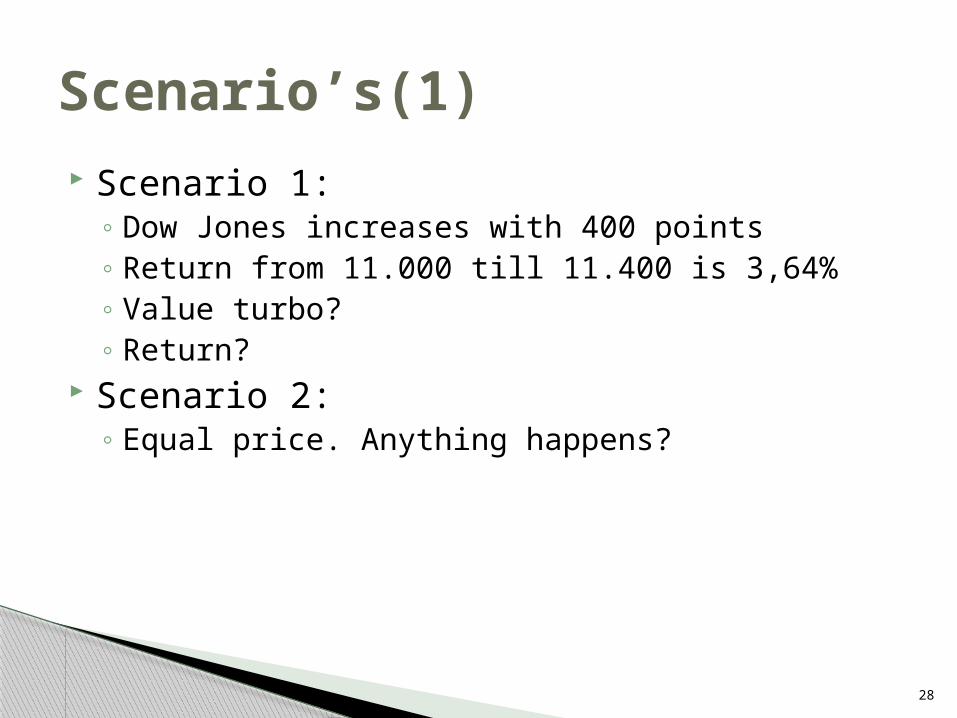

Scenario’s(1) Scenario 1:

◦ Dow Jones increases with 400 points◦ Return from 11.000 till 11.400 is 3,64%◦ Value turbo?◦ Return?

Scenario 2:◦ Equal price. Anything happens?

29

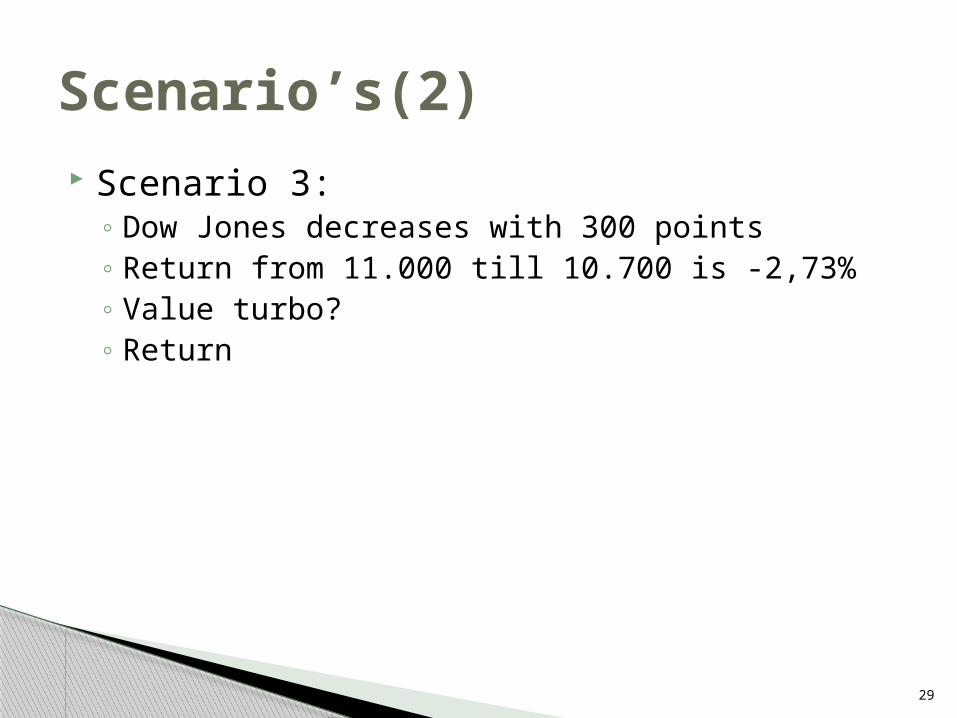

Scenario’s(2) Scenario 3:

◦ Dow Jones decreases with 300 points◦ Return from 11.000 till 10.700 is -2,73%◦ Value turbo?◦ Return

30

Scenario(3) Scenario 4:

◦ Dow Jones decreases with 800 points◦ Stop-loss is 10.200 and bank sells product for

10.150 (-7,73%)◦ Value turbo?◦ Return?

Scenario 5:◦ Scenario 4, but bank sells at 9.995?

31

Conclusion Turbo’s Opportunity to leverage Huge profit- and loss potential Don’t lose more then investment

◦stop-loss Easily tradable Broad asortiment Euronext Amsterdam

But.. Risk and costs involved!

32

Deutsche Bund

Proposal

33

Leverage turns good deals into great deals!*

*©CFQ