National Bank of Abu Dhabi PJSC ‒ General Terms and Conditions ...

Abu Dhabi National EnergyCompany (TAQA) PJSC

Annual Report 2007

ABU DHABI24O 28’ 00” N54O 22’ 00” E

(1,1) -1- 4/2/08 TAQA_RA_COVER ENG TP.indd 8/4/08 17:11:51(1,1) -1- 4/2/08 TAQA_RA_COVER ENG TP.indd 8/4/08 17:11:51

THE HAGUE52O 04’ 60” N04O 17’ 60” E

Peter Barker-Homek, CEO

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 01

CONTENTS

Operating and Financial Review

02 Key Figures03 2007 in Brief04 Business Overview06 Chairman’s Statement10 Our Operational Footprint12 Letter from CEO16 The Board & Executive Management18 Management Discussion & Analysis18 Operational Review 28 Financial Review34 Corporate Governance36 Health, Safety, Security and Environment (HSSE) Program38 TAQA in the Community40 Shareholder & Bondholder Information

Financial Statements

42 Board Report

43 Auditors’ Report44 Consolidated Income Statement45 Consolidated Balance Sheet46 Consolidated Statement of Changes in Equity48 Consolidated Cash Flow Statement49 Notes to the Consolidated Financial Statements95 Glossary of Terms

02

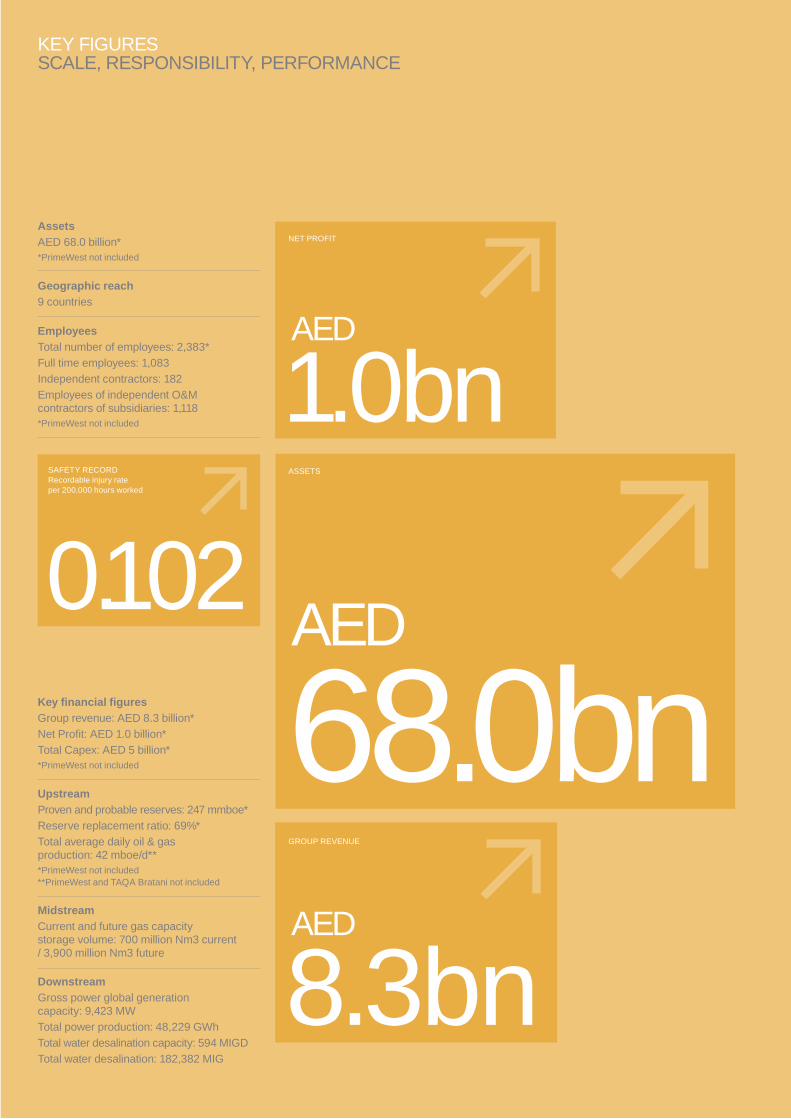

Assets

AED 68.0 billion**PrimeWest not included

Geographic reach

9 countries

Employees

Total number of employees: 2,383*

Full time employees: 1,083

Independent contractors: 182

Employees of independent O&Mcontractors of subsidiaries: 1,118*PrimeWest not included

Key fi nancial fi gures

Group revenue: AED 8.3 billion*

Net Profi t: AED 1.0 billion*

Total Capex: AED 5 billion**PrimeWest not included

Upstream

Proven and probable reserves: 247 mmboe*

Reserve replacement ratio: 69%*

Total average daily oil & gasproduction: 42 mboe/d** *PrimeWest not included**PrimeWest and TAQA Bratani not included

Midstream

Current and future gas capacity storage volume: 700 million Nm3 current/ 3,900 million Nm3 future

Downstream

Gross power global generationcapacity: 9,423 MW

Total power production: 48,229 GWh

Total water desalination capacity: 594 MIGD

Total water desalination: 182,382 MIG

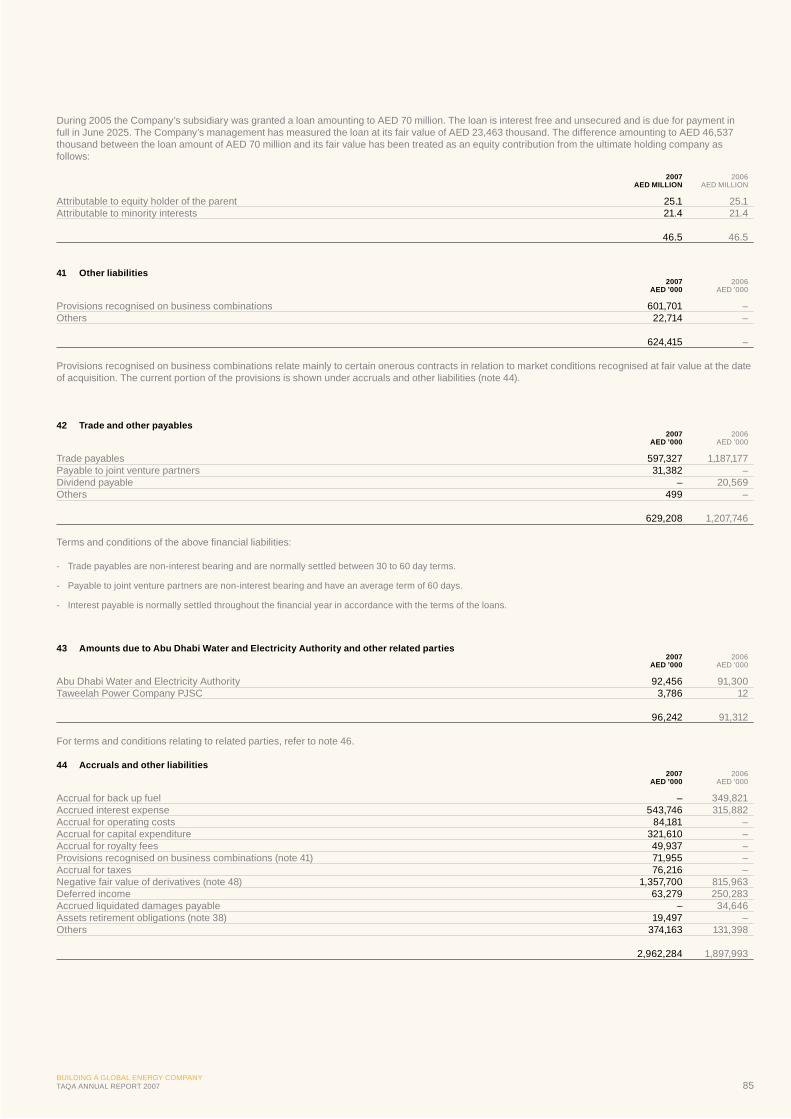

1.0bn

NET PROFIT

68.0bnAED

AED

ASSETS

8.3bn

GROUP REVENUE

0.102SAFETY RECORDRecordable injury rateper 200,000 hours worked

KEY FIGURES SCALE, RESPONSIBILITY, PERFORMANCE

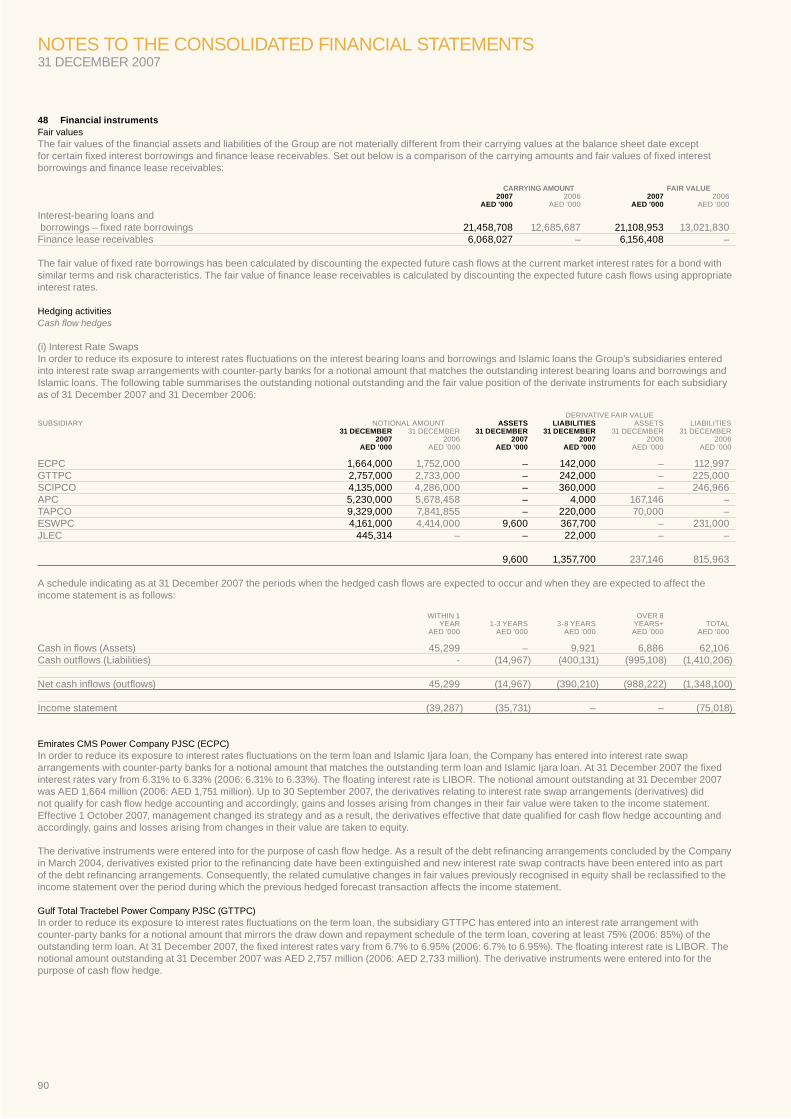

AED

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 03

2007 was a transformational year for TAQA, marking our entry into new geographies together with the considerable expansion of our energy operations within our chosen key markets. Through a series of signifi cant strategic acquisitions, we have created a global energy company that now operates in nine countries.

The year started with our purchase of Talisman’s Brae assets and this transaction completed on 31 December 2007. During January, we also tied up our acquisition of BP Netherlands’ gas exploration and production (E&P) assets. Both deals position us at the heart of the North Sea oil basin.

During the second quarter we acquired CMS Generation, a subsidiary of the US integrated energy fi rm CMS Energy, as well as ownership interests in generation assets held by ABB in Morocco and India, providing additional breadth to our portfolio of power assets. We now have downstream activities in UAE, Morocco, Saudi Arabia, Ghana and India.

The third quarter was signifi cant for TAQA as it marked our entry into North America. This began in August with the acquisition of 100 per cent of Northrock Resources Ltd (NRL), a Canadian oil and gas E&P company with operations in the Western Canadian Sedimentary Basin. Acquired from Pogo Producing Company for a total purchase price of US$2 billion, we have renamed the company TAQA North Limited.

During the same month, we announced the US$540 million acquisition of Pioneer Canada, an oil and gas E&P company with operations in the Western Canadian Sedimentary Basin.

We further cemented our North American presence when we announced in September that we had agreed to buy Calgary-based PrimeWest Energy Trust. The total consideration paid for the business, a conventional oil and gas royalty trust, was approximately Cdn$5 billion. The transaction completed on 16 January 2008 and, when combined with TAQA North’s other assets, has established TAQA as a top twelve Canadian oil and gas E&P company in its newest market.

We continue to look at opportunities across the Middle East and into other emerging markets. October saw us sign an agreement to co-operate on joint developments with National Power Company (NPC), an affi liate of the Al Zamil and Al Seif Groups, regional investment groups based in Saudi Arabia. We also signed a Letter of Intent with Kuwait Energy Company (KEC), a Kuwait-based oil E&P company, in respect of opportunities in the oil and gas sector.

During November, we completed the sale to Marubeni Corporation of 40 per cent of Emirates CMS Power Company and 100 per cent of Taweelah A2 Operating Company – the company responsible for the management, operations and maintenance of the Taweelah A2 Plant - demonstrating our commitment to retaining majority positions in performing assets, while fostering and benefi ting from partnerships with world-class international organizations.

2007 IN BRIEFA TRANSFORMATIONAL YEAR

04

BUSINESS OVERVIEWCAPTURING THE BENEFITS OF INVESTING ACROSS THE VALUE CHAIN

TAQA plans to build a diversifi ed international portfolio of operations and investments, balanced across stable developed economies and growing emerging markets.Peter Barker-Homek, CEO

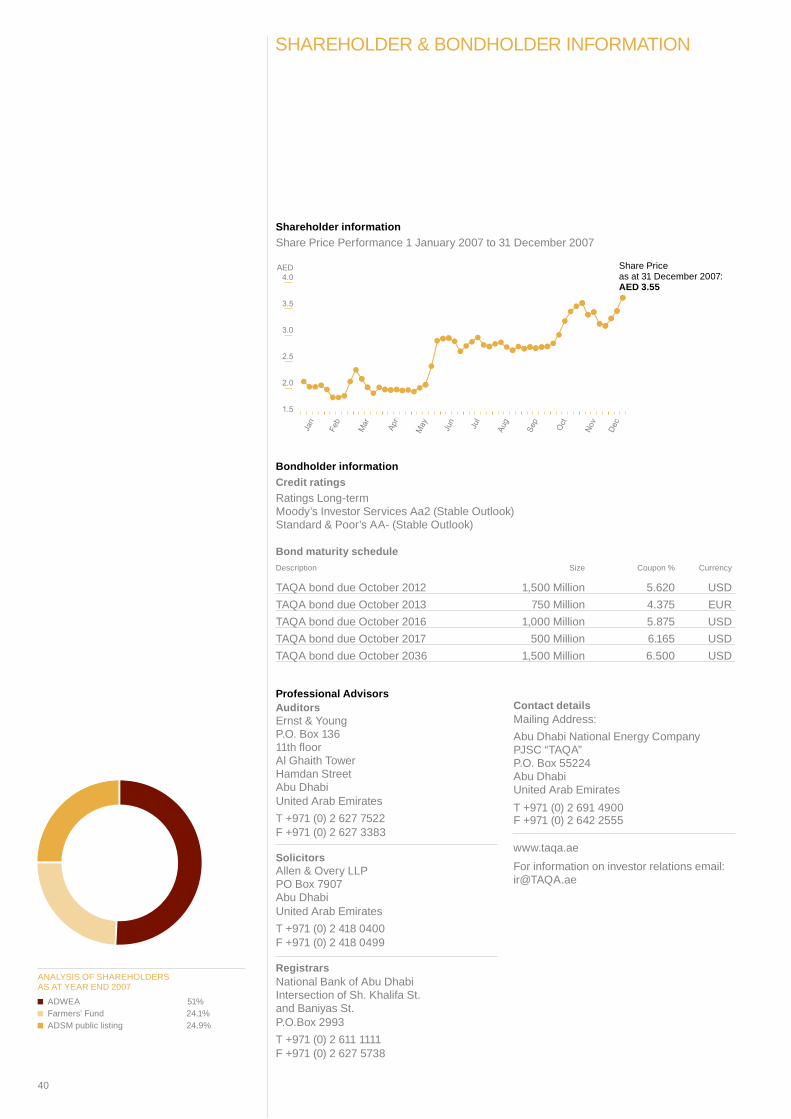

Founded in 2005, the Abu Dhabi National Energy Company (TAQA) PJSC is a global energy company with a growing asset base that now exceeds AED 68 billion. One of the largest companies listed on the Abu Dhabi Securities Market (ADSM), TAQA is a fl agship corporation for the Government of Abu Dhabi. TAQA carries an AA- credit rating from Standard & Poor’s and was recently upgraded to Aa2 by Moody’s.

TAQA employs 2,383 people from 38 different nations and operates from its offi ces inAbu Dhabi, Michigan, Aberdeen, Calgary, Amsterdam and The Hague. Our footprint is further extended through partnerships and investments across Africa, the Middle East, Europe, North America and India.

By capitalizing on our position as the leading electricity generation and water desalination company in the UAE, we have quickly emerged as a signifi cant global energy company. Since inception, our business portfolio has expanded to capture benefi ts from across the energy value chain and we now have operations in exploration, production, storage, transmission and generation.

Our operations are now organized into three businesses: downstream, midstreamand upstream.

Downstream (power generation and water desalinisation)

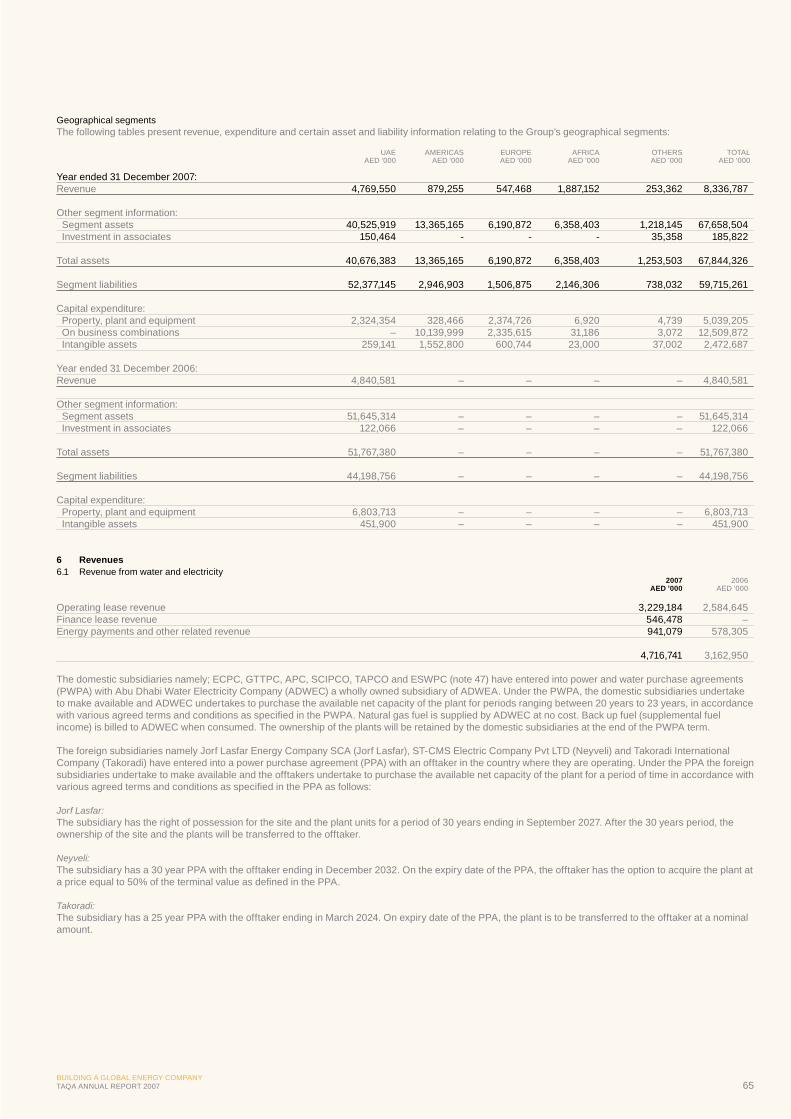

TAQA provides 90 per cent of the water and electricity requirements of the Emirate of Abu Dhabi through domestic generation subsidiaries situated in various locations in the Emirate of Abu Dhabi and the Emirate of Fujairah. Each domestic subsidiary is partially owned by us and operated with one or more leading international utilities, oil and gas companies and project developers.

Our domestic market position has provided a springboard for regional and international expansion within the power and water sectors. Our international power generation activities now span four countries: Ghana, India, Morocco and Saudi Arabia.

As at 31 December 2007, we had combined installed power capacity of 9,423 MW, of which 7,347 MW were from our domestic subsidiaries and 2,076 MW were from our international subsidiaries. For the same period we had 594 MIG/d of desalinated water capacity.

Midstream (storage, transportation and processing infrastructure)

Our existing midstream operations include two important gas storage assets in The Netherlands acquired from BP Netherlands Energie B.V. in January 2007, as well as our interests in the East Cantaur Gas Storage facility in Canada. Additionally, TAQA holds a long-term pipeline position on the Alliance pipeline system, transporting gas from Western Canada to the Chicago cantaur.

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 05

The midstream portfolio consists of three natural gas storage assets. PGI Alkmaar wasthe fi rst peak gas shaver storage installation in The Netherlands. Commissioned in 1997, it has a working gas volume of 500 million Nm3 and a production capacity of 36 million Nm3/d as well as signifi cant expansion potential of its processing capacity. The other storage asset in TAQA’s Dutch portfolio is the Bergermeer Gas Storage Project, which consists of the development of the Bergermeer reservoir into an underground gas storage facility with a future working gas capacity of approximately 3.2 billion Nm3. As of November 2007, Bergermeer is the largest gas storage development project in Europe based on working gas capacity and allows us to play a crucial and strategic role in solving Europe’s “Security of Supply” issue by investing in local storage and helping new long-distance gas suppliers service the Northwest European market securely all year round.

In Canada, we are optimizing our East Cantuar storage facility in Saskatchewan which is jointly-owned with Husky Oil and provides a small working gas capacity of 7 BCF. Additionally, we are successfully managing our long-term position of 75 MMcf/d on the Alliance pipeline system until 2015 which we optimize daily by primarily fl owing our own produced gas from Western Canada to the more profi table Chicago market in the United States. Both Canadian midstream positions have been acquired through our Pioneer and Northrock acquisitions in 2007.

Our focus is on developing these existing midstream operations and their synergies with our upstream and downstream assets, while selectively targeting midstream acquisitions which will add value to our global asset portfolio.

Upstream (exploration and production)

Our oil and gas operations grew signifi cantly during 2007 and now comprise upstream interests in Europe and North America.

In Europe, we have an operating interest in the Bergen Licence, an area off the western coast of The Netherlands, which comprises four fi elds that are currently producing, together with six shut-in fi elds. Following our acquisition of Talisman Energy Inc.’s interests in the Brae Area oil and gas fi elds and associated pipeline1, we now have a presence in the UK North Sea.

As at 31 December 2007, our combined European upstream operations comprised approximately 40 mmboe of proven plus probable reserves. The acquisition of the Brae assets was completed on 31 December 2007.

As at 31 December 2007, TAQA North’s properties2 consisted of 2,506,732 gross acres, of which 1,834,177 are as yet undeveloped. For the 12 months to 31 December 2007, TAQA North had average production of 36,656 boe/d, consisting of 18,091 boe/d of oil, condensate, and natural gas liquids and 111.4 mmcf/d sales gas. As at 31 December 2007, TAQA North had proven plus probable reserves of approximately 207.5 mmboe, consisting of 99.98 mmbbls of oil, condensate and natural gas liquids and 645,518 mmcf of sales gas.

PrimeWest’s property, as at 31 December 2007, represented 1,140,329 gross acres, of which 737,566 are as yet undeveloped. For the comparable 12 months to 31 December 2007, PrimeWest had average production of 50,274 boe/d, consisting of 15,000 boe/d of oil, condensate, and natural gas liquids and 211.643 mmcf/d sales gas. As at 31 December 2007, PrimeWest had proven plus probable reserves of approximately 253.629 mmboe, consisting of 79.970 mmbbls of oil, condensate and natural gas liquids and 1,041,954 mmcf of sales gas.

1 The producing Brae assets and infrastructure are operated by Marathon Oil UK Limited. The SAGE terminal and associated pipeline is operated by Mobil North Sea Limited

2 The acquisition of PrimeWest closed subsequent to the year end in January 2008.

GLOBAL ASSETS BY REGION

UAE 60% Americas 20% Africa 9% Europe 9% Others 2%

06 06

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 07

CHAIRMAN’S STATEMENTA SHARED VISION FOR GLOBAL REACH

I am pleased to present our fi rst annual report on TAQA’s activities, together with the audited fi nancial statements for the year ended 31 December 2007.

Looking back, 2007 was a transformational year for TAQA and one in which we succeeded in delivering against our strategic objectives.

With entry into new markets, 2007 was the year we took TAQA, an Abu Dhabi champion, onto the world stage. From a performing base of domestic assets, our aim has been to develop TAQA into a global energy company with a diversifi ed and geographically varied portfolio. I am proud of our achievements to date.

Through a series of strategic acquisitions we have strengthened our traditional focus on downstream power and water activities, while also entering into the exploration and production market in North America and Europe and establishing an important base from which to grow our midstream operations.

TAQA has become one of the few enterprises which has managed to transform itself into a major oil and gas company outside its country of origin and we are unwavering in our commitment to become a standard bearer for other such enterprises. We set ourselves the highest standards throughout our operations and aspire to lead the way in demonstrating exceptional conduct in overseas markets.

TAQA’s vision is underpinned by a strategy that focuses on acquiring quality assets that are vertically diversifi ed, where we can enhance them or add further value. This has led to rapid expansion of our organization. Our priority is now to ensure that we create a cohesive business that is sustainable into the future and we have implemented a comprehensive program to bring about the swift integration of these acquisitions in order to create a best-in-class operator.

All of our assets have world-class track records for health and safety, and by drawing on the expertise we bring into the TAQA group and sharing knowledge across our entire organization, we are developing a robust framework to ensure these standards are rigorously upheld.

08

ABERDEEN57O 07’ 60” N02O 06’ 00” W

08

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 09

Furthermore, we are acutely aware of the potential environmental impact of TAQA as a global energy business and strive to make reductions in the company’s impact on the environment. We have become the fi rst GCC company to join the global 3C (Combat Climate Change) Initiative and are taking steps to monitor and minimise emissions from our portfolio of assets.

I view health & safety and the environment as business critical undertakings; a view that is shared across our organization and by those with whom we choose to work.

As our organization grows, we will continue our steadfast commitment to corporate governance and transparency and have sought to bring a consistency of approach across TAQA by establishing an enterprise-wide code of ethics built on the values of innovation, excellence, teamwork, integrity and performance. Such practices shape the character of our company and provide it with the supporting framework necessary to ensure full legal and regulatory compliance. They also provide our management team with the optimum architecture for innovation and productive decision-making as TAQA continues to grow.

Today, TAQA is a global business and diversity forms the backbone of our success and I take great pride in the breadth of skills and experience that our employee base brings to TAQA. We are now able to draw on this vast pool of talent and expertise, sharing knowledge and learnings across borders in order to continually enrich our organization. Our success is very much down to the drive and commitment of our people who are highly-skilled and passionate about their work. In particular, I would like to mention Peter Barker-Homek, our Chief Executive Offi cer, who has guided TAQA expertly during this transformational year.

Moving forward, the focus of our organization is on integrating our asset base into the TAQA family, creating further value and identifying new opportunities to contribute to the ongoing development of our business. I am fully confi dent of our abilities and that we will continue to grow and excel as a profi table, safe and environmentally responsible company.

Finally, on behalf of the Board and myself, I would like to express our gratitude and appreciation to His Highness Sheikh Khalifa bin Zayed Al Nahyan, President of the United Arab Emirates, Supreme Commander of the UAE Armed Forces and Ruler of Abu Dhabi,His Highness Sheikh Mohammed Bin Zayed Al Nahyan, the Crown Prince of Abu Dhabi, Deputy Supreme Commander of the UAE Armed Forces and Chairman of Abu Dhabi executive council and His Highness Sheikh Diab Bin Zayed Al Nahyan, Chairman of Abu Dhabi Water and Electricity Authority, for their continuing and outstanding support.

Hamad Mohamed Al-Hurr Al-SuwaidiChairmanAbu Dhabi National Energy Company (TAQA)

CHAIRMAN’S STATEMENT

I view health & safety and the environment as business critical undertakings; a view that is shared across our organization and by those with whom we choose to work

10 BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 11

OUR OPERATIONAL FOOTPRINT

Saudi ArabiaDownstream- Cogeneration Project- Power generation capacity: 250 MW- Gross power generation for 2007: 1,765,199 MWh

GhanaDownstream - Power Plant- Power generation capacity: 220 MW- Gross power generation for 2007: 1,417,330 MWh

The NetherlandsUpstream- Oil & Gas exploration and production- Proven and probable reserves: 11 mmboe

Midstream- Gas storage and transmission

IndiaDownstream - Power Plant- Power generation capacity: 250 MW - Gross power generation for 2007: 1,693,068 MWh

UAEDownstream - 6 Power generation and water desalination facilities- Power generation capacity: 7,347 MW- Gross power generation for 2007: 33,540 GWh- Total desalination capacity: 594 MIGD- Total water desalination output for 2007: 182,382 MIG

CONTRIBUTION TO REVENUES

Downstream

Power generation and water desalinisation assets 83%

Midstream

Storage and transmission assets 4%

Upstream

Exploration and production assets 13%

CanadaUpstream- Oil & Gas exploration and production- Proven and probable reserves: 207.5 mmboe* *includes Northrock Resources Ltd and Pioneer Natural Resources Canada Inc. Does not include PrimeWest which was acquired in January 2008

Midstream- Gas storage and transmission

MoroccoDownstream- Power Plant- Power generation capacity: 1,356 MW- Gross power generation for 2007: 9,812,330 MWh

United KingdomUpstream- Oil & Gas exploration and production- Proven and probable reserves: 29 mmboe

Midstream- Gas storage and transmission

12 12

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 13

LETTER FROM CEOGLOBAL REACH & DIVERSIFICATION

TAQA’s strategic goal is to build and operate a geographically diversifi ed global portfolio of energy businesses across the value chain. We strive to behave with the greatest integrity in all our markets and to ensure our business is responsible and sustainable into the future.

We seek to complement our strong domestic water and electricity production businessby identifying, purchasing and enhancing high-quality energy assets in upstream, midstream and downstream sectors across the Middle East, North Africa, India, Europe and North America.

Dear Stakeholders,

2007 was the year that TAQA put a solid stake in the ground. Early last year, we announced that we expected TAQA to be a AED 220 billion company in assets by 2012. I am pleased to report that the results of the past 12 months confi rm that we are executing on our plan. In one year we have gone from being a domestic power generation and desalination utility to a truly global energy company, that operates in nine countries and is comprised of qualityenergy assets. The dramatic reshaping of our business to encompass all aspects of the energy value chain has created new opportunities for TAQA around the world.

A year of diversifi cation

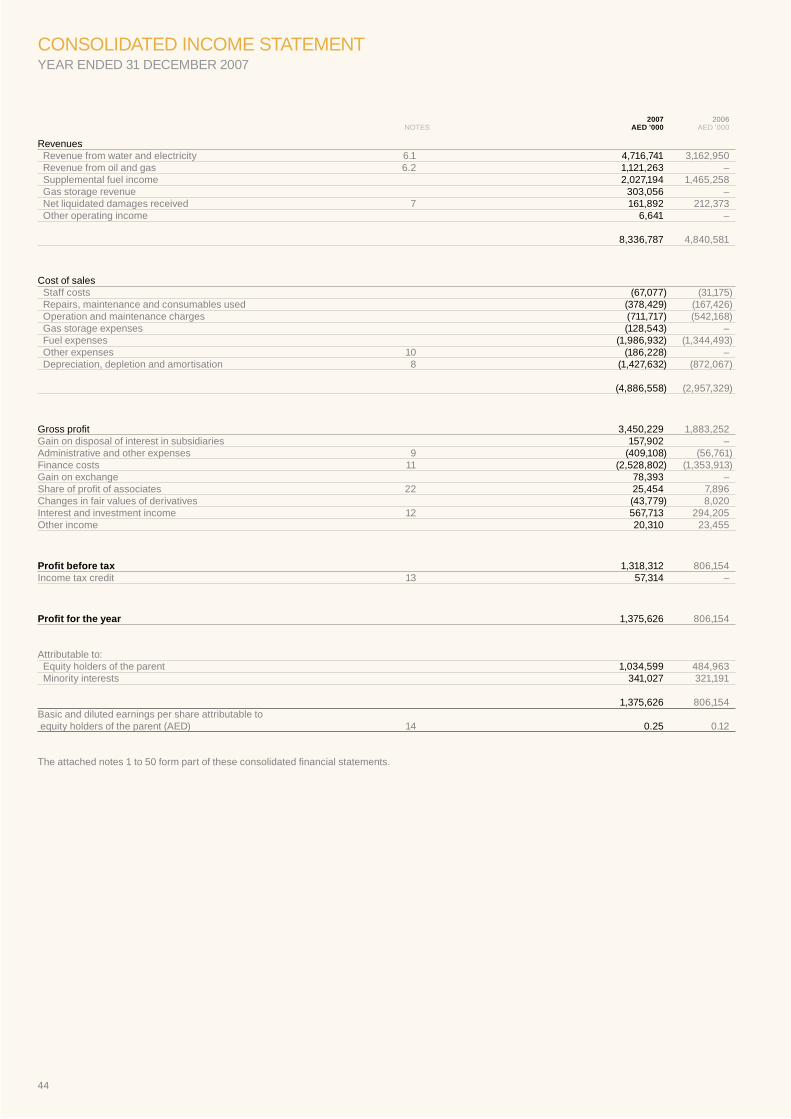

During the course of the year, we have grown our asset base by over 30 per cent to AED 68 billion and we are poised to build on the success of 2007 to create an enduring reputation for delivery and strength. Total revenues of AED 8.3 billion and net profi t of AED 1.0 billion for the year are clear demonstrations of our progress to-date.

In upstream oil and gas, we have made good inroads into North America, with the creation of TAQA North, and have built a strong foothold in Europe, with our collection of assets in the UK North Sea and off the Dutch coast. This was brought about by the completion of our acquisition of BP Netherlands’ gas exploration and production (E&P) assets and Talisman’s Brae assets, but the move that truly put TAQA on the world map was our entry into Canada. During the course of 2007, we executed successfully on transactions totaling more than US$2.5 billion. This does not include our Cdn$5 billion acquisition of PrimeWest Energy Trust, which was announced last year, but completed in January 2008. This is TAQA’s largest acquisition to date and now affords us a position as one of Canada’s top ten companies in terms of net proven natural gas reserves and in the top 12 in terms of oil and gas production.

The formation of an upstream business, which by the end of 2007 already had total proven and probable reserves of over 247 mmboe and our total average daily oil and gas production of 42 mboe/d (excluding TAQA Bratani and PrimeWest) is a remarkable achievement. Moreover, this does not include PrimeWest’s proven and probable reserves (the acquisition closed in January 2008), which at year end stood at approximately 254 mmboe. This provides us with an excellent platform upon which to build.

We are continually investing in businesses we acquire. Our gas storage assets inThe Netherlands are currently undergoing a dramatic enhancement program, targeting total gas storage capacity equivalent to the annual gas consumption of 1.6 million households by 2012.

14

Within our domestic power generating business, we currently have 7,347 megawatts. The acquisitions of selected CMS Generation and ABB downstream assets in Morocco, Saudi Arabia, Ghana and India have added a further 2,076 megawatts of power capacity and we hope to substantially increase the capacity of our domestic and international downstream business in the next three to fi ve years. As I look back over the past year, I see we have an excellent team in place at TAQA who share a common mission to build a sustainable global energy business. Our record of identifying acquisition opportunities, negotiating and completing them is testament to the talent of our team and a measure of our determination and shared vision. By diversifying our operations into several new markets we now offer an attractive spread of market and operational risk. And while the pace of development has been dramatic, we are making rapid progress in swiftly integrating these assets to ensure they reach their full potential as part of TAQA.

With our business expanding dramatically into new segments and new geographies, that we are able to double the dividend that we have generated for our shareholders to AED415 million, is a clear endorsement of this strategy.

Developing the TAQA way

In building the TAQA business we have also developed the fi rm’s character, a commonality of approach that is central to the integration of our acquired assets, as well as championing ethics that are integral to TAQA.

The protection of our people, the communities our operations touch and the environment in which we operate are values which are central to everything we do. This starts with our workforce and at the core of this commitment is health and safety, to ensure both the welfare of our employees and the continuity of our operations.

Across the assets we have acquired in 2007, we had a recordable injury frequency rate of just 0.102 per 200,000 hours worked. Every member of our team shares the responsibility for ensuring our standards are upheld and our safety record is continually improved through regular evaluation and assessment.

It is important to me that the standards we set and share with our employees, across multiple geographies, are clearly defi ned and understood. As such, we developed a Code of Business Ethics that makes clear our stance on appropriate professional conduct in the offi ce, in the fi eld, and when representing the company. The code is rooted in an absolute compliance with local laws, an acceptance of transparent behavior at all times, and a respect for others’ cultures.

In 2007, we started the process of building a Corporate Social Responsibility (CSR) program. Our objective with CSR is to implement programs of ethical, environmental and social benefi t to all of the company’s stakeholders. As such, we have engaged with external auditors that will monitor our CSR efforts to ensure that our practices are effective and embedded throughout the organization.

Diversity and inclusion is an important part of our CSR policy since the company has over 2,383 employees from 38 different nationalities. In recognizing that our workforce consists of a diverse population of people, I believe that harnessing these differences helps to create a productive environment where people feel valued, where they feel that their talents are fully utilized, and in which the organizational goals are being met. TAQA prides itselfon being a meritocracy.

LETTER FROM CEOGLOBAL REACH & DIVERSIFICATION

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 15

Our place in the world

As a new company with a vision to become a global player in the energy sector, I believe we have a responsibility to lead the way in reducing our environmental impact and supporting the move towards a low emissions economy.

We were the fi rst GCC company to join the 3C (Combat Climate Change) Initiative, a global opinion group of prominent business leaders demanding the integration of climate issues into markets and trade. As the fi rst member from a non G8 + 5 country, TAQA joins forces with business leaders from nearly 50 large organizations committed to contributing to a common vision of a low emitting, sustainable society. The 3C Initiative’s goal is to set a global limit to the maximum temperature increase and defi ne emission reduction targetsfor 2030 and 2050 based on the best available research.

On a day to day basis, TAQA’s operations around the world are taking steps to monitor and reduce emissions of harmful greenhouse gases. Emission reduction initiatives include the introduction of solar powered equipment to eliminate the venting of greenhouse gases, upgrades to new technology to reduce fugitive, vented and fl ared methane, and the purchase of compression equipment with improved fuel performance. As a 3C Initiative signatory, we have committed to play a proactive role in combating climate change, andas the fi rst GCC member, we hope to set a precedent in the region.

I believe that changing individual behavior is an important step in combating environmental problems and will help to infl uence society’s collective response. To help our employees make a positive step, and to demonstrate our commitment to the environment, in 2007 we put in place a hybrid car buying program for our employees.

Looking ahead

I am convinced, not just by the success of 2007, but also by the energy and enthusiasm I see throughout the company, that the strategy we are implementing will allow TAQA to reach its potential of becoming a major blue chip company. If prudent opportunities continue to manifest themselves, TAQA will soon occupy the position of a market-leading energy company that we know it should.

To all of our people, I would like to say a sincere thank you for the commitment, professionalism, and for the determination they have shown in managing the many changes that were asked of them as part of the integration process. It is to their ability and dedication that we owe much of our success in 2007 and it is their skill that is TAQA’s greatest asset.

Finally, I would like to thank the Board and the Government of Abu Dhabi for their continued support in helping TAQA to fulfi l its potential.

Yours sincerely,

Peter Barker-HomekChief Executive Offi cerAbu Dhabi National Energy Company (TAQA)

As a new company with a vision to become a global player in the energy sector, I believe we have a responsibility to lead the way in reducing our environmental impact and supporting the move towards a low emissions economy

16

The Board has delegated the day-to-day management of TAQA to executive offi cers appointed by the Board. The current members of TAQA’s executive management are as follows:

Name Position Date of joining

Peter Barker-Homek Chief Executive Offi cer May 2006Doug Fraser Chief Financial Offi cer January 2008Carl Sheldon General Counsel and Deputy General Manager April 2008Frédéric Lesage GVP Integration and Optimization February 2007Daniel Dexter GVP Global Power May 2007Tim Granger Managing Director, TAQA North January 2008Gopal Gopalakrishnan GVP Accounting and Control May 2007Paul van Gelder Managing Director, TAQA Energy & TAQA Bratani July 2007Klaus Reinisch Head of Midstream December 2007Abdulla Khunji Chief of Staff, GVP Corporate Communications June 2007Yasser El-Zein GVP Technology September 2006Jos Schiffelers Head of HSSE July 2007

THE BOARD AND EXECUTIVE MANAGEMENT

DirectorsThe current members of the Board of Directorsof TAQA (the “Board’’) are as follows:

Name Position

H.E. Hamad MohamedAl-Hurr Al-Suwaidi ChairmanH.E. Ahmed Saif Al-Darmaki Deputy Chairman H.E. Abdulla Saif Al-Nuaimi DirectorH.E. Salem Al-Sayaari DirectorH.E. Mohammed Foulad Director

01 His Excellency Hamad Mohamed Al-Hurr Al-Suwaidi serves as Chairman of the Board and was appointed in 2005. His Excellency’s principal responsibilities outside TAQA are Under-Secretary of the Department of Finance of the Government of Abu Dhabi, Director of Mubadala Development Company, Chairman of the Financial Support Fund for Farm Owners in the Emirate of Abu Dhabi, Executive Director of the Abu Dhabi Investment Authority (“ADIA’’) and Chairman of the Board of Emirates Power Company.

02 His Excellency Ahmed Saif Al-Darmaki serves as Vice-Chairman of the Board and was appointed in 2005. His Excellency’s principal responsibilities outside TAQA include Chairman of ADWEC, Director of Planning and Development of ADWEA, and Offi ce Manager of the Chairman of ADWEA.

03 His Excellency Abdulla Saif Al-Nuaimi serves as a Director of the Board and was appointed in 2005. In addition, His Excellency is Director of the Privatization Directorate of ADWEA, Deputy Managing Director of ADWEC and Chairman of Gulf Power Company.

04 His Excellency Salem Al-Sayaari serves as a Director of the Board and was appointed in 2005. His Excellency is currently Deputy General Manager of Abu Dhabi Distribution Company and is a Director of Arabian Power Company.

05 His Excellency Mohammed Fouladserves as a Director of the Board and was appointed in 2005. His Excellency was previously Chairman and Managing Director of Taweelah Power Company.

03 02

01

04

05

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 17

02 0601

08

03

09

04 05

10 11 1207

01 Peter Barker-Homek is Chief Executive Offi cer. His professional background includes Senior Adviser in M&A at BP plc, Director of Worldwide Downstream Gas Distribution Development at BG International and Vice-President of Development for Eastern Europe and Latin America at Pacifi c Enterprises. He has worked at the US State Department and was an institutional sales consultant within the Capital Markets Group at Merrill Lynch. Peter Barker-Homek is a US national and holds an MBA from the University of Southern California.

02 Doug Fraser is Chief Financial Offi cer. He has previously held senior fi nancial positions as Assistant Controller with Imperial Oil Ltd, Treasurer at Petro-Canada, Vice President and Chief Financial Offi cer at Husky Energy and most recently as Vice President Finance and Chief Financial Offi cer at PrimeWest Energy. Doug Fraser is a Canadian national and is a Chartered Accountant.

03 Carl Sheldon is General Counsel and Deputy General Manager. He was previously a partner at Allen & Overy LLP where over his career he practiced in the energy sector, as well as running the fi rm’s German and U.S. operations. He is a dual qualifi ed lawyer admitted to practice in New York and in England. He holds an MA from Cambridge University.

04 Frédéric Lesage is Group Vice-President, Integration & Optimization. Prior to joining TAQA, he worked as a senior consultant for McKinsey & Co. and practiced law for eight years at a leading Canadian law fi rm, specializing in Labour & Employment litigation. He holds a law degree from Université de Montréal and a Master of Business Administration (with distinction) from the Ivey School of Business at the University of Western Ontario. Frederic Lesage is a Canadian national.

05 Daniel Dexter is Group Vice President of the Global Power Group. His professional background includes the positions of Executive Managing Director of International Operations with CMS Enterprises, various CEO/President level positions for a number of independent power businesses and General Manager of the Johnson City, Tennessee, Power Board. He has an MBA from New Mexico State University, which includes a specialised study emphasis on regulatory economics. Daniel Dexter is a US national.

06 Tim Granger is Managing Director of TAQA North. He previously held overall responsibility for Development and Production Operations at PrimeWest and, prior to this, undertook a variety of management roles at Pogo Canada Ltd, Petro-Canada and Amerada Hess Canada Ltd, in addition to engineering positions at Dynex Petroleum Ltd, Canterra Energy Ltd and Dome Petroleum Ltd. Tim Granger holds a P.Eng. (Mechanical) from Carlton University and is a Canadian national.

07 Gopal Gopalakrishnan is Group Vice President Accounting and Control. He is a Chartered Accountant and has held senior management positions in accounting and fi nance for 20 years. He has been a director of Utilicorp New Zealand Ltd and Utilicorp Finance Company, both subsidiaries of Aquila Inc in New Zealand. Prior to joining TAQA, Gopal Gopalakrishnan was Director of Accounting for CMS Enterprises. He is a New Zealand national.

08 Paul van Gelder is Managing Director of TAQA Energy and TAQA Bratani. His previous positions included Project Director Bergermeer Gas Storage, Maintenance Manager for BP and Director of Logistics for Driessen Aerospace Systems. This followed a career in the Royal Netherlands Navy where he rose to Commanding Offi cer of a Navy General Purpose Ship and Commanding Offi cer Maintenance and Logistics for 323 Squadron. Paul van Gelder is a graduate from the Royal Netherlands Naval College and has a Masters degree in Operations Management and Logistics from the Technische Universiteit Eindhoven. He is a Dutch national.

09 Klaus Reinisch is Head of Midstream. He previously headed up the business development function at Gazprom Marketing & Trading and has been instrumental in setting up various projects and businesses in gas storage, LNG, pipeline asset management, power generation, and carbon credit sourcing. Klaus Reinisch has an MBA in International Management from Thunderbird School of Global Management in Arizona. He is an Austrian national.

10 Abdulla Khunji is Chief of Staff, GVP Corporate Communications. He previously worked at the Environment Agency of Abu Dhabi, where his most recent position was Head of Public Relations, Marketing & Communication. Prior to this role he was a senior member of the System Support team at the Environment Agency. Abdulla Khunji holds a Masters in Innovation & Entrepreneurship HCT/CERT (Harvard, Stanford, MIT), UAE and a Bachelor of Business & Public Administration, Management Information Systems from Eastern Washington University, USA. He is a UAE national.

11 Yasser El-Zein is Group Vice President Technology. He has worked in various technical and managerial capacities for IBM, PaineWebber, The New York Mercantile Exchange (NYMEX) and, more recently, as Director of Engineering and Advanced Development for Major League Baseball AM. Yasser El-Zein holds an MSE in Electrical and Computer Engineering from the University of Iowa and has authored scientifi c publications in periodicals such as the Physics of Plasmas Journal, Planetary Space Science Journal, Journal of Applied Physics and Journal of Plasma Physics. He is a US national.

12 Jos Schiffelers is Head of HSSE. He has worked in various technical and managerial positions at Refi nery, Chemical and Oil & Gas assets. He has experience of European and North American industry with Exxon and BP, most recently as the HSE Manager for BP Netherlands. He has a diploma of Business administration of the Netherlands Open University. In Q2 2008 he will achieve his Master degree of Safety, Health & Environment from the Delft University of Technology. He is a Dutch national.

18

AMSTERDAM52O 22’ 23” N04O 53’ 32” E

18

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 19

2007 marked TAQA’s emergence onto the world stage as a global energy company. During the fi nancial year under review, we took signifi cant steps in both announcing and completing six acquisitions. Our priority has then been to begin the integration work to bring these companies together under the TAQA umbrella, while taking care to contain business disruption.

The year was therefore characterized by two key objectives: to ensure sound and rapid deal execution and to strive for operational excellence within companies we acquire. Both of these objectives are designed to bring us nearer to our strategic goal of building and operating a geographically diversifi ed global portfolio of energy businesses across the value chain. We maintain an unwavering commitment to ongoing investment and asset optimization, the highest standards of health and safety, environmental stewardship and diversity and inclusion.

By building and rationalizing our diversifi ed portfolio, we went from an asset base of AED 52.0 billion to AED 68.0 billion. The growth in our footprint is already generating total revenues for the year of AED 8.3 billion. This does not yet include a full-year contribution of those assets acquired during the course of the year, nor does it include the PrimeWest transaction, which only closed in January 2008, but gives an indication of our potential scale.

During 2007, we established our fi rst operating presence in seven additional jurisdictions; Morocco, India, Ghana, Saudi Arabia, The Netherlands, The UK and Canada. Many of these acquisitions were foundational, in that we entered the market with each acquisition. In these instances, we acquired a quality, going-concern and retained a leadership team; both of which have combined to provide TAQA with a springboard for future expansion.

Our integration mandate is designed to bring acquisitions into the TAQA way of doing things and ensure that all functional areas are completely integrated into the group where they need to be. We have been working with an international management consultancy fi rm since June 2007 to build a world-class, best practice integration process specifi c to TAQA which defi nes how we approach integration projects. The integration of our assets will enable TAQA to bring harmony to our diverse in multiple geographies; a process which has already allowed us to build signifi cant integration knowledge and skills internally.

As the asset base has grown during the year, so too has the relative fi nancial strength of the company. Today our diversifi ed portfolio of assets generates robust cash fl ows, with cash and cash equivalents at year end 2007 of AED 7.0 billion. When combined with the benefi t of our low-risk domestic utility business and strong support from our majority shareholder, this allows us to sustain current levels of debt and maintain a low cost of capital. Profi t for the period reached AED 1.0 billion, a rise of 113 per cent when compared to 31 December 2006.

Downstream (power generation and water desalinsation)

During 2007, we built on our solid downstream foundation, leveraging our team’s experience of developing, commissioning and operating power generation facilities to grow our downstream assets both in the familiar territory of the UAE as well as internationally.

TAQA’s downstream capability now represents total global generation capacity (gross) of approximately 9,423 MW. During 2007, total power production ran to 48,229 GWh. Our total water desalination capacity is approximately 594 MIGD, with total water desalination of 182,382 MIG in 2007.

Downstream activities comprised 83 per cent of total revenues during 2007 and 72 per cent of profi t for the period.

MANAGEMENT DISCUSSION & ANALYSISOPERATIONAL REVIEW

20

MANAGEMENT DISCUSSION & ANALYSISOPERATIONAL REVIEW

Our objective in the global power business is to provide the group with a base of stable earnings and cash fl ows. The development of TAQA’s downstream business is critical to cementing our position as a leading global energy company. Downstream provides a vital component of our integrated offering and helps to ensure our enlarged business remains sustainable into the future.

During 2007, the acquisition of CMS Generation substantially developed our downstream footprint beyond the domestic market, expanding into Saudi Arabia, Morocco, Ghanaand India.

The integration of CMS Generation was greatly assisted by a commonality of standards. The objectives we had at TAQA were largely aligned with the operational success CMS achieved over its years of operation.

Domestic assets

TAQA’s six domestic subsidiaries, or Independent Water and Power Producers (IWPPs), are characterized by low-risk utility operations, underpinned by quasi-Government off-take agreements.

Combined, our domestic subsidiaries provide over 90 per cent of Abu Dhabi’s power and water needs, thus performing a vital domestic role. These assets consist of modern, gas-fi red plants. The Abu Dhabi Water and Electricity Company (ADWEC) has undertaken to purchase the entire net capacity of the plants owned by TAQA’s subsidiaries under long-term off-take agreements.

The domestic downstream portfolio is the heart of the TAQA group as it has provided us with a stability of cash fl ow upon which to build our global diversifi ed strategy. It is our intention to retain majority positions in these performing assets, while fostering and benefi ting from partnerships with world-class organizations.

In May 2007, as part of the acquisition of CMS Generation, we acquired a further 40 percent interest in Emirates CMS Power Company (ECPC) which operates the Taweelah A2 facility. In line with our stated strategy, we sold 40 per cent of ECPC and 100 per cent of the plant’s associated O&M company to Marubeni Corporation in October 2007. TAQA and its affi liates have retained a 60 per cent interest in ECPC. This transaction, worth US$140million in cash, represented excellent value for TAQA. It is also another example of Abu Dhabi attracting the highest quality of international investor, keen to share in the country’s growth potential.

As part of the CMS Generation acquisition, we also acquired a further 20 per cent interest in Shuweihat S1 and a 50 per cent interest in Shuweihat O&M Ltd Partnership, which is responsible for the management, operation and maintenance of the plant.

Abu Dhabi is the second largest economy in the Gulf Cooperation Council (GCC) region, after Saudi Arabia. Real GDP growth in Abu Dhabi reached 6 per cent in 2007. It is forecast to remain at these levels in 2008 and remain signifi cantly above that of the MENA region. GDP per capita in Abu Dhabi is one of the highest in the world at US$49,700

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 21

Domestic factfi le

Emirates CMS Power Company (Plant Taweelah A2)TAQA ownership interest: 54%

A combined cycle gas-fi red facility located on the coastal Taweelah site approximately 50 kilometers north-east of Abu Dhabi City. Taweelah A2 is owned and operated pursuant to a joint venture agreement with Marubeni Corporation.

Gross power generation capacity 777 MW

2007 gross power generation 4,123,060 MWh

Total desalination capacity 50 MIGD

2007 water desalination output 16,863 MIG

Gulf Total Tractebel Power Company (Plant Taweelah A1)TAQA ownership interest: 54%

A gas-fi red power generation and water desalination plant on the coastal Taweelah site approximately 50 kilometers north-east of Abu Dhabi City. Taweelah A1 is owned and operated pursuant to a Joint Venture agreement with Suez Energy and Total.

Gross power generation capacity 1,350 MW

2007 gross power generation 6,183,608 MWh

Total desalination capacity 84 MIGD

2007 water desalination output 25,976 MIG

Taweelah Asia Power Company (Plant Taweelah B)TAQA ownership interest: 54%

A gas-fi red power generation and water desalination plant on the coastal Taweelah site. Owned and operated in a Joint Venture agreement with Marubeni Corporation, BTU Power Company, Pendekar Power and JGC Corporation, the Taweelah B power plant is a brownfi eld development, commissioned in 2002.

Gross power generation capacity 1,370 MW

2007 gross power generation 3,425,945 MWh

Total desalination capacity 100 MIGD

2007 water desalination output 30,076 MIG

Emirates SembCorp Water and Power Company (Plant Fujairah 1)TAQA ownership interest: 54%

Located in the Emirate of Fujairah, Fujairah 1 is owned and operated in a Joint Venture agreement with SembCorp Utilities. It is the latest of the partially privatized Independent Water and Power Producers (IWPPs)

Gross power generation capacity 650 MW

2007 gross power generation 4,450,025 MWh

Total desalination capacity 100 MIGD

2007 water desalination output 32,829 MIG

GROSS POWER GENERATION CAPACITYBY DOMESTIC SUBSIDIARY

Emirates CMS Power Company (Plant Taweelah A2) 11%

Gulf Total Tractebel Power Company (Plant Taweelah A1) 18%

Taweelah Asia Power Company (Plant Taweelah B) 19%

Emirates SembCorp Water and Power Company (Plant Fujairah 1) 9%

Arabian United Power Company (Plant Umm Al Nar) 23%

Shuweihat CMS International Power Company (Plant Shuweihat S1) 20%

TOTAL DESALINATION CAPACITYBY DOMESTIC SUBSIDIARY

Emirates CMS Power Company (Plant Taweelah A2) 8%

Gulf Total Tractebel Power Company (Plant Taweelah A1) 14%

Taweelah Asia Power Company (Plant Taweelah B) 17%

Emirates SembCorp Water and Power Company (Plant Fujairah 1) 17%

Arabian United Power Company (Plant Umm Al Nar) 27%

Shuweihat CMS International Power Company (Plant Shuweihat S1) 17%

22

Arabian United Power Company (Plant Umm Al Nar)TAQA ownership interest: 54%

Located in Sas Al-Nakeel (previously Umm Al Nar) at the entrance of Abu Dhabi island. Umm Al Nar is owned and operated in a Joint Venture agreement with International Power plc, Mitsui Corporation and Tokyo Electric Power Company.

Gross power generation capacity 1,700 MW

2007 gross power generation 8,378,505 MWh

Total desalination capacity 160 MIGD

2007 water desalination output 44,878 MIG

Shuweihat CMS International Power Company (Plant Shuweihat S1)TAQA ownership interest: 74%

Located on the coast of the Arabian Gulf, Shuweihat S1 is owned and operated in a Joint Venture agreement with International Power plc. Shuweihat S1 is one of the largest plants in the UAE representing close to 15 per cent of the UAE’s desalination capacity and 19% of its power capacity.

Gross power generation capacity 1,500 MW

2007 gross power generation 6,979,009 MWh

Total desalination capacity 100 MIGD

2007 water desalination output 31,760 MIG

International assets

In May 2007, TAQA acquired CMS Generation for a total purchase price of US$900 million. As a result, our interests in power production and water desalination assets now extend beyond the UAE, across Morocco (Jorf Lasfar), India (Neyveli), Ghana (Takoradi) and Saudi Arabia (Jubail).

The CMS Generation acquisition has been benefi cial to TAQA in three main ways: the company’s long-term contracts and established customer relationships in the jurisdictions in which it operated together with an experienced management team with a proven track record, and technical expertise and specialized skills in the fi eld of independent power and water project development.

In May 2007, TAQA also purchased the 50 per cent indirect interests of ABB Ltd in the Jorf Lasfar (Morocco) and Neyveli (India) power plants for a total purchase price of US$490 million. This acquisition gave TAQA 100 per cent ownership of both assets.

Our focus for the international downstream business, since acquiring this portfolio has been to make substantial progress in asset optimization. In most instances, this has been a question of business structure, rather than operational enhancement.

MANAGEMENT DISCUSSION & ANALYSISOPERATIONAL REVIEW

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 23

International factfi le

Jorf Lasfar Energy Company, MoroccoTAQA ownership interest: 100%

The largest privatization on the African continent to date, Jorf Lasfar supplies on average 50 per cent of the electricity demand for Morocco and represents approximately one third of the country’s total installed capacity. Electricity from Jorf Lasfar is sold to Morocco’s Offi ce National d’Electricite under a 30-year power purchase agreement.

Gross power generation capacity 1,356 MW

2007 gross power generation 9,812,330 MWh

ST CMS Electric PvT Limited, Neyveli, IndiaTAQA ownership interest: 100%

A lignite-fi red power plant at Neyveli in Tamil Nadu. One of eight fast-track projects counter-guaranteed by the Indian government, it has a 30-year agreement to sell power generated by the plant to the Tamil Nadu Electricity Board.

Gross power generation capacity 250 MW

2007 gross power generation 1,693,068 MWh

Saudi ArabiaTAQA ownership interest: 25%

Steam plant located at Jubail in Saudi Arabia.

Gross power generation capacity 250 MW

2007 gross power generation 1,765,199 MWh

GhanaTAQA ownership interest: 90%

A three-stage Power Plant project, the third stage of which is yet to be implemented. The entire existing power generation capacity is purchased by the Volta River Authority.

Gross power generation capacity 220 MW

2007 gross power generation 1,417,330 MWh

GROSS POWER GENERATION CAPACITYBY INTERNATIONAL SUBSIDIARY/ASSOCIATE

Jorf Lasfar Energy Company, Morocco 65% ST CMS Electric PvT Limited, Neyveli, India 12% Saudi Arabia 12% Ghana 11%

24

Midstream (storage, transportation and processing infrastructure)

We extended our reach in 2007 by expanding into the midstream market, acquiring assets with signifi cant existing gas storage capacity and even higher storage development potential in The Netherlands and have taken our fi rst steps towards establishing a midstream presence in North America, with the combined storage and pipeline assets now held as part of TAQA North in Canada.

The rationale behind TAQA’s acquisitions and our focus on developing best-in class midstream operations is that we believe these operations are central to extracting optimal value from our comprehensive portfolio of upstream and downstream assets and therefore vital to the long-term sustainability of our fully integrated global energy business.Our midstream revenues also provide an ideal source of income diversifi cation, bolstering TAQA’s growing fi nancial position and further strengthening our creditworthiness by delivering a new source of high-quality cash fl ows.

By having acquired a key peak shaving gas storage facility in The Netherlands and developing a new even much larger storage facility, TAQA is investing in assets to ease the security of supply issue Europe is facing. As local European gas reserves decline sharply in the coming years, the continent will become increasingly dependent on long-distance imports primarily from Russia, as well as other continents, via LNG. Russia accounts for one-fi fth of the EU’s total energy consumption today, but is expected by some analysts to provide up to 66 per cent of Europe’s gas supplies by 2025. By investing in storage in the highly strategic Northwest European gas market, we are making sure that a suffi cient supply of gas is available to European consumers during times of supply problems or unexpected high demand.

Furthermore, we now own our fi rst North American midstream assets through the acquisitions of Northrock and Pioneer. The East Cantuar storage facility is a gas cap on top of an oil fi eld in Saskatchewan, Canada which can deliver up to 7 bcf of working gas capacity. East Cantuar is jointly owned in equal parts with our partner Husky Oil who also operates the facility on our behalf. The long-term position and booking on the Alliance gas pipeline system connecting the Western Canada producing regions with the Chicago market in the USA is our fi rst global gas pipeline position. This is managed through our TAQA North subsidiary.

European assets

Through our acquisition in January 2007, TAQA acquired two natural gas storage projects from BP Netherlands Energie BV. The fi rst is a mature and operating peak shaving gas storage facility at PGI Alkmaar and the second is Northwest Europe’s largest seasonal gas storage project at Bergermeer which is now being developed by TAQA to become operational in 2012 or earlier.

PGI Alkmaar

PGI Alkmaar was the fi rst peak gas shaver in The Netherlands designed and built specifi cally to provide a back-up gas storage service, including meeting peak requirements in the west of the Netherlands during winter and to meet emergency gas supply requirements in the event of network interruptions. Commissioned in 1997, the facility has a working gas volume of 500 million Nm3 and a production capacity of 36 million Nm3/d.

We intend to further enhance PGI Alkmaar’s service offering beyond the current capacity contract to fulfi ll short-term as well as seasonal demand for gas storage capacity, while maintaining a strict asset/return profi le. We are also currently evaluating a further expansion of the storage project which would increase capacity signifi cantly as early as 2010.

MANAGEMENT DISCUSSION & ANALYSISOPERATIONAL REVIEW

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 25

Bergermeer Gas Storage

Bergermeer is a high-permeability, well-defi ned onshore reservoir in the Bergen Licence, 35 kilometers from the Dutch landfall of the Balgzand Bacton Line (“BBL”) pipeline to the UK and is connected to the H-Gas (high calorifi c gas) grid. The development and conversion of the gas reservoir into Northwest Europe’s largest seasonal gas storage asset is already well under way with the fi rst commercial storage capacity becoming operational by 2012.

As early as 1994, Bergermeer was recognized by a government commission as one of the most suitable fi elds for gas storage in the Netherlands. Tests conducted in summer 2007 reconfi rmed that the depleted Bergermeer gas fi eld is ideal for gas storage and our intentions have been met with keen interest from the market. As Europe’s own local gas production is declining rapidly, new storage capacity is now high on the strategic agenda of all European energy players as well as local governments and regulators.

TAQA has therefore started to develop the Bergermeer reservoir into an underground gas storage facility with a working gas capacity of approximately 3.2 billion Nm3 which is equivalent to the annual gas consumption of 1.6 million households.

Full development and construction of the Bergermeer gas storage project is scheduled for 2012. Once the entire facility is operational, Bergermeer Gas Storage is expected to remain in service for 40 to 50 years, providing the European consumer market with much-needed fl exibility for generations to come. Bergermeer is the largest gas storage development project in Europe, based on planned working gas capacity, and we are proud to be the driving force in ensuring this strategic asset is developed to its full potential as quickly as possible.

North American Assets

Through our Canadian acquisitions, we now own two distinct midstream assets in North America, allowing us to gain insights into the commercialization of storage in the regional market as well as the optimization possibilities of gas pipeline capacity bookings.

The East Cantuar project is owned in equal parts with Husky Oil and is operated by Husky Marketing. TAQA provides input on operational decisions and seeks to optimize its capacity commercially. East Cantuar is a gas cap on top of an oil fi eld which can be blown down and emptied to regulate and control oil production while providing a valuable alternative source of revenues as a regional gas storage facility.

Furthermore, the Alliance Pipeline booking allows us to fl ow gas from Western Canada to the Chicago market to take advantage of the higher prices in the Metropolitan Chicago area. By making use of our own upstream production gas in Western Canada, we are able to enhance returns on the sale of gas to a higher priced market, while optimizing the physical fl ow on the pipeline on a daily basis. This allows us to take advantage of additional transportation capacities being made available to us by the operator for low additional costs. We continue to monitor the differences between the Western Canadian and Chicago gas prices to ensure we receive maximum returns from the long-term pipeline booking, which expires in 2015.

While we apply best-in-class principles in the way we operate and optimize our current midstream assets, we are also always on the look out for new and profi table midstream projects that best utilize our existing infrastructure. TAQA has designed and proposed to construct a LNG regasifi cation terminal drawing upon our existing Dutch pipeline assets offshore, and have received very positive indications of interest from many market participants. We will continue to explore this and other LNG terminal opportunities in all our global markets.

As we grow into a more integrated global energy company, we will continue to look to acquire midstream assets and companies in all of our markets. Our aim is to extract value-adding synergies from our integrated portfolio and to build a sustainable and highly diversifi ed midstream business wherever opportunities that fi t with our corporate strategy arise.

We believe our midstream operations are central to extracting optimal value from our comprehensive portfolio of upstream and downstream assets and therefore vital to the long-term sustainability of our fully integrated global energy business

26 26

Upstream (exploration and production)

2007 was the year TAQA moved into the upstream market in earnest, with a strong foothold at the heart of the European oil and gas industry and with our acquisition of Canadian assets (including PrimeWest which closed in January 2008) we have become one of Canada’stop ten companies in terms of net proven natural gas reserves and in the top 12 companies in terms of oil and gas production.

Our substantial upstream presence stems from the acquisition of a series of quality exploration and production (E&P) assets throughout the year, providing us with operations in Canada, The Netherlands and the UK.

From this foundation we are focused on qualifying other upstream opportunities, optimizing our acquired footprint and sharing knowledge and experience across TAQA in order to grow and develop our capabilities further.

Demonstrating our commitment to supporting local communities and managing the impact of our presence, wherever we operate, has been key to TAQA in 2007 and will remain a company priority into the future. As a new upstream operator venturing into new geographical regions for the rst time, it is vital we underline TAQA’s commitment to corporate social responsibility.

European assets

In January 2007, TAQA furthered its upstream aims when it acquired BP’s Netherlands exploration and production business. Assets added to TAQA’s portfolio include upstream oil and gas facilities (both on- and offshore in the Netherlands), pipelines, gas processing operations and storage facilities. The attraction was not only the potential of BP’s operating assets, but also its management and workforce expertise; together they have provided a launch pad for TAQA’s push into the European oil and gas sector.

Though indigenous European oil and gas production is typically viewed to be on a long-term downward trajectory, the North Sea is proving an increasingly active market, helped by the high oil price climate. The area has become an increasingly active play for TAQA and other operators as the majors release mature assets to concentrate their E&P investment programs in other parts of the world. The result has seen the North Sea penetrated by a raft of new entrants buying prospective acreage thought to have substantial upside growth potential. The industry believes there could still be a further 22-39 billion barrels of oil and gas yet to be produced from the region, providing healthy upstream opportunities to niche players for years to come.

TAQA is planning to double or triple its European upstream asset base and workforce over the next two to four years. Annual production of our combined European upstream operations is currently approximately 2.1 mmboe and the current workforce comprises85 staff and 35 long-term contractors. Proven and probable reserves are approximately40 mmboe.

Shortly before the BP Netherlands’ purchase was completed, TAQA announced that it was adding to its European energy sector portfolio by purchasing Talisman Energy’s non-operated interest in the North Sea Brae eld. The acquisition closed on 31 December 2007, therefore the plants production gures have not been included for the year under review. The operation produces 14,600boe/d and has boosted TAQA’s proven reserves by 29 mmboe.

MANAGEMENT DISCUSSION & ANALYSISOPERATIONAL REVIEW

Our substantial upstream presence stems from the acquisition of a series of quality exploration and production (E&P) assets throughout the year, providing us with operations in Canada, The Netherlands and the UK

CONTRIBUTION TO 2P RESERVESBY REGION

European Assets 16% North American Assets 84%

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 27

North American Assets

Our entry into the Canadian upstream market began when we acquired Northrock Resources Ltd. from Pogo Producing Company in May 2007. A Calgary-based oil and gas exploration company, it has operations in the Western Canadian Sedimentary Basin (WCSB).

This upstream presence in the WCSB was bolstered following a second transaction in August 2007, which saw us acquire the wholly-owned Canadian subsidiaries of Pioneer Natural Resources Canada Inc.

In January 2008, we went on to complete the acquisition of PrimeWest Energy Trust, a conventional oil and gas royalty trust that actively acquires, develops, produces and sells natural gas, crude oil and natural gas liquids. Complementing its top-quartile asset base, Reserve Life Index and signifi cant development portfolio, PrimeWest has achieved recognition for its commitment to health and safety in the workplace, receiving the Alberta Safe Work award three years in a row (2003-2006).

Combined, these three acquisitions have enabled TAQA to establish a solid platform of quality assets with signifi cant upside development potential and our objective is to continue improving the asset base, realizing opportunities from the undeveloped acreage and creating operational synergies to enhance capital effi ciency together with supply chain and operational cost effi ciencies. This coming year the largest portion of our capital expenditure budget will be directed towards these assets, now grouped under the name TAQA North, where we are investing up to US$500m.

2007 was another year of strong, but volatile, oil prices with Brent crude averaging 11 per cent higher than in 2006 at US$72.55/bbl – a new record in money-of-the-day terms. Having started the year at below US$60/bbl, it ended 2007 at US$96.02/bbl. Continued strong consumption growth in China (up 4.5 per cent on 2006), moderate supply growth and the weakness of the US dollar all contributed to this rise.

Crude prices initially fell sharply in January, reaching their lowest levels since May 2005, because of the combined effects of warm weather on demand, ample OPEC supply and rising US stocks. Brent Crude averaged US$53.68/bbl, 14 per cent lower than December 2006.

From the mid-January low, prices recovered as revived geopolitical tensions and rising demand powered a strong rise to over US$67/bbl on average in April. Prices stabilized at this level in May when it became clear that the US held healthy inventories. Between May and the end of July prices rose close to US$10/bbl on average (with July Brent averaging US$77.01/bbl) before easing in August (to US$70.73/bbl) when concerns that economic growth and equity market instability might adversely effect oil demand estimates emerged. The upward trend was resumed (to US$76.87/bbl) in September as storms hit in the Gulf of Mexico and US interest rates were cut.

In October, US dollar weakness, tensions in the Middle East and unrest in West Africa all contributed to a further rise of about US$6/bbl (averaging US$82.50/bbl). Brent crude was a further 12 per cent higher in November (at US$92.62/bbl on average) as a weak US dollar contributed to increased speculative activity in the energy futures market. This upward trend moderated in December as concerns over economic growth in 2008 began to impact estimates of oil demand. Nevertheless, the average Brent price in December 2007 was over 46 per cent higher than its level in the same month in 2006.

28

CALGARY51O 04’ 60” N

114O 04’ 60” W

28

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 29

Revenues

TAQA receives revenue from the generation, production and sale of electricity, water,oil and gas, and the storage of gas. In 2006, 100 per cent of the revenues related to our activities in the UAE.

Total revenues were AED 8.3 billion for 2007, an increase of 72 per cent compared to AED 4.8 billion for 2006. Of this, AED 4.8 billion, or 58 per cent, was attributable to our business interests in the UAE and AED 3.5 billion, or 42 per cent, was derived from our activities outside our domestic market. The acquisitions made in 2007, and those that subsequently closed in 2008, do not fully feature in this consolidated fi gure.

The UAE generation assets were forced to run on back-up fuel periodically during 2006and 2007, due to a shortage of gas. Supplemental back-up fuel revenue was AED 2.0 billion in 2007 versus AED 1.5 billion in 2006. For 2007, the fuel revenue also includes the fuel recovery from the offtaker in our subsidiaries in Morocco and India.

Revenue from the oil and gas and gas storage businesses accounted for AED 1.4 billion (there is no comparable like-for-like fi gure in 2006).

In the space of a year, upstream activities have gone from a zero revenue contribution in2006 to AED 1.4 billion for the period under review, equivalent to 13 per cent of total revenues.

Cost of Sales

Cost of sales was AED 4.8 billion for 2007, an increase of 65 per cent compared with costof sales of AED 2.9 billion for 2006. Cost of sales for the period decreased as a percentage of revenues from 61 per cent in 2006 to 59 per cent in 2007.

Depreciation, depletion and amortisation was AED 1.4 billion for 2007, an increase of 64 per cent compared with AED 0.87 billion for 2006, which was primarily due to the acquisitions made during 2007.

Gas storage expenses of AED 129 million was a new cost due to the acquisition of BP Netherlands Energie BV in January 2007 which provided two natural gas storage projects in The Netherlands.

The increase in cost of sales was also driven by a 48 per cent increase in fuel expenses, due to fuel costs at Emirates Sembcorp Water and Power Company (ESWPC) and at the newly acquired subsidiaries, partially offset by decreases in other domestic subsidiaries. Fuel expenses are linked to back up fuel income explained under our revenue breakdown, but these do not correspond exactly because on the revenue line this is taken at market price, while on the cost line fuel is taken as consumption from inventory. Costs related to repairs, maintenance and consumables due to acquisitions and due to full year operations at ESWPC.

MANAGEMENT DISCUSSION & ANALYSISFINANCIAL REVIEW

30 30

MICHIGAN42O 16’ 31” N83O 43’ 51” W

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 31

Gross Profi t

2007 gross profi t was AED 3.5 billion, a year-on-year increase of 83 per cent, compared with AED 1.9 billion in 2006. This represents an improvement in our gross margin from 39 per cent to 41 per cent.

Administrative and Other Expenses

Administrative and other expenses were AED 409 million in 2007, an increase of AED 352 million compared with 2006. The increase was driven by our acquisitions throughout the year and was primarily impacted by increases in salaries and related expenses, business development expenses and professional fees.

Finance Costs

Finance costs were AED 2.5 billion for 2007, an increase of AED 1.2 billion, or 87 percent, compared with fi nance costs of AED 1.4 billion for 2006. The increase in fi nance costs primarily results from full impact of three-part US$3.5 bond issue in October 2006, and US$2 billion two-part bond issues in October 2007 to fund acquisitions during 2007.

Interest and Investment Income

Interest and investment income for 2007 amounted to AED 568 million, compared with interest income of AED 294 million for 2006. The increase was attributable to interest generated on TAQA’s bank deposits which rose from AED 288 million to AED 521 million, primarily as a result of a signifi cant portion of the proceeds of TAQA’s October 2006 US$3.5 billion bond issue that were utilized for acquisitions only during the second half of 2007.

Foreign Exchange

TAQA conducts operations in nine countries around the world and reports its consolidated fi nancial statements in UAE Dirham. As a result, its results of operations are affected by exchange rate fl uctuations between the UAE Dirham and other currencies, in particular the Canadian Dollar, Euro and Sterling.

The main driver of the foreign exchange gain of AED 78 million recorded in 2007 is from our Moroccan subsidiary, relating to net investment in Euro.

Profi tability

Profi t from Ordinary Activities and Profi t for the YearProfi t for the year for 2007 was AED 1.4 billion compared to AED 0.8 billion in 2006. Net profi t after minority interests increased 131 percent from AED 0.5 billion to AED 1.0 billion. The profi t for the year included an income tax credit of AED 57 million relatingto deferred income tax less current income tax.

In 2007, basic and diluted earnings per share attributable to equity holders of TAQA more than doubled to AED 0.25 compared to AED 0.12 in 2006.

Dividend

TAQA’s proposed cash dividend for 2007 of AED 415 million increased by 100 per cent,up from AED 208 million in 2006.

MANAGEMENT DISCUSSION & ANALYSISFINANCIAL REVIEW

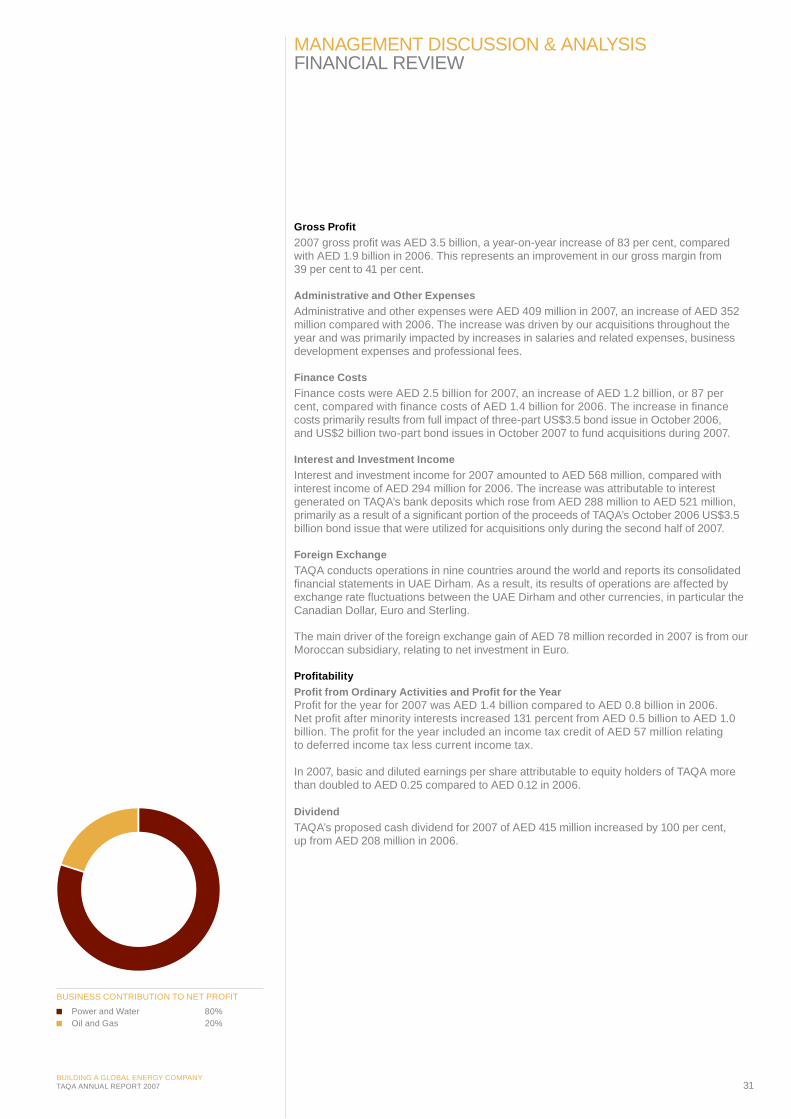

BUSINESS CONTRIBUTION TO NET PROFIT

Power and Water 80% Oil and Gas 20%

32

Cash Flow Statement

Changes in cash fl ow from operating activities have been affected by changes in amounts due to/from other parties and principal payments to related parties. Net cash earned in operating activities was AED 1.3 billion in the year ended 31 December 2007 comparedwith AED 2.3 billion for the year ended 31 December 2006. The decrease was primarily due to interest paid.

Changes in cash fl ow from investing activities were driven mainly by purchases of subsidiaries and investments in property, plant and equipment. Net cash used in investing activities was AED 17.1 billion in the year ended 31 December 2007 compared with almost AED 8.0 billion in the year ended 31 December 2006. The increase was primarily due to the cost of acquisitions of subsidiaries completed during 2007.

TAQA’s cash requirements arise primarily from the capital intensive nature of its power generation and water desalination operations, its oil and gas exploration and production and the operation of its gas storage and peak gas facilities, debt servicing costs and dividends as well as the expansion of its business portfolio.

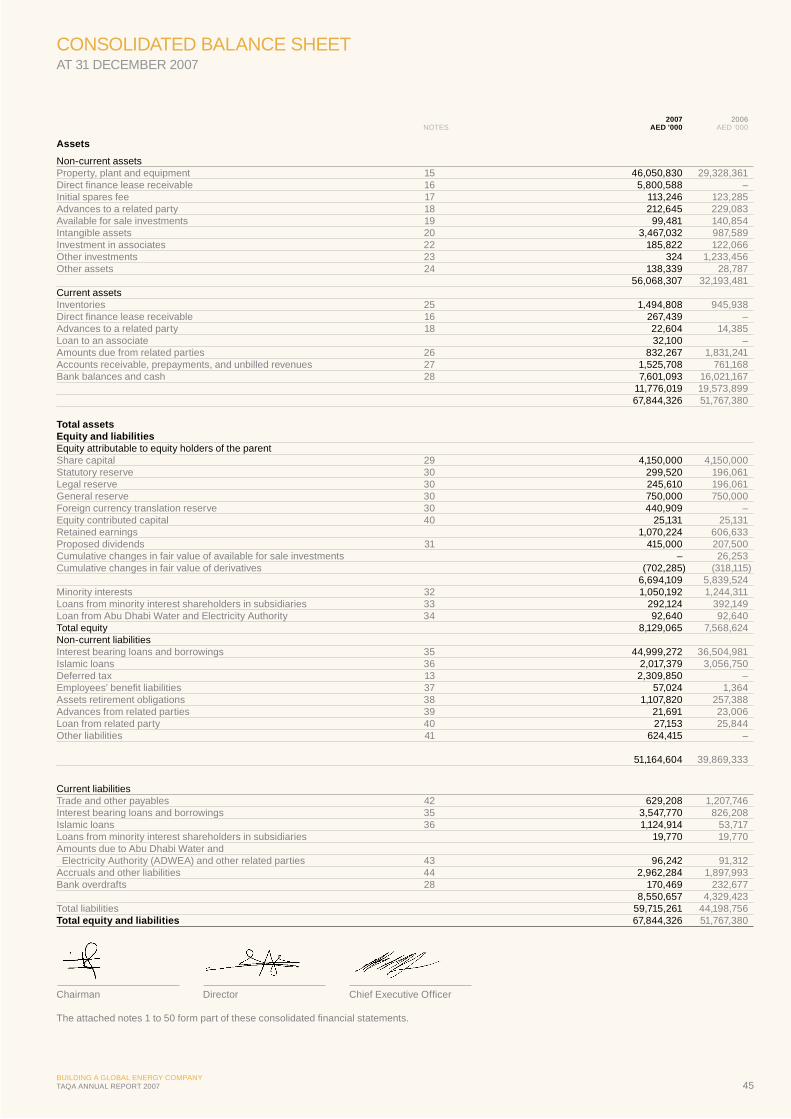

The commitments to TAQA’s ongoing operations are expected to be fi nanced with cash provided by the operations themselves. The authorized capital expenditures contracted at 31 December 2007, but not provided for, amounted to AED 19.6 billion, which primarily includes the commitment for the PrimeWest acquisition.

Balance Sheet

In 2007, total assets grew 31 per cent to AED 68 billion compared to AED 52 billion for 2006. The main drivers behind this increase were oil and gas assets, which accounted for AED 14.7 billion (there is no comparable like-for-like fi gure in 2006), direct fi nance lease receivable at AED 5.8 billion and intangible assets which increased to 3.5 billion from AED 1.0 billion

The book value of equity increased by 7.4 per cent to AED 8.1 billion from AED 7.6 billion, mainly as a result of a 76 per cent increase in retained earnings at AED 1.0 billion from AED 0.6 billion in 2006. In 2007, foreign currency translation reserves which are used to record exchange differences arising from the translation of the fi nancial statements of foreign subsidiaries and to record the effect of hedging net investments in foreign operations, were AED 440 million. There was no like-for-like fi gure in 2006.

Non-current liabilities rose 28 per cent to AED 51.2 billion for the year, mainly due to the increase of interest bearing loans and borrowings by 23 per cent to AED 44.9 billion and deferred tax at AED 2.3 billion (there was no like-for-like fi gure in 2006). Current liabilities rose 98 per cent to AED 8.5 billion, driven by interest bearing loans and Islamic loans.

The 2007 increase in interest bearing loans and borrowings was driven by the issue of Abu Dhabi National Energy Notes at a value of AED 7.3 billion and two term loans for subsidiaries, Jorf Lasfar Energy Company (AED 1.5 billion) and ST-CMS Electric Company India Private Limited (AED 640 million).

MANAGEMENT DISCUSSION & ANALYSISFINANCIAL REVIEW

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 33

Funding Strategy

Our stated strategy of investing in strategic growth opportunities to grow to an asset base of AED 220 billion by 2012 requires signifi cant fi nancial support.

In 2007, we were recognized by Euromoney as ‘Best Borrower – Middle East and Northern Africa’ for our initial bond offering of US$3.5 billion. The award recognizes our long-term approach and our ability to expand our global operations rapidly while protecting our credit rating.

In 2007, we established a global Medium Term Note Program which debuted in 2007with a US$2 billion offering in a two-part bond sale. The Program is rated Aa2 by Moody’s Investors Service and AA- by Standard & Poor’s, both with a stable outlook.

In July 2007, TAQA established a working capital facility of US$1 billion with National Bank of Abu Dhabi, of which no amount was drawn and the entire US$1 billion was available at 31 December 2007.

Subsequent to the period under review, we put in place a US$3.1 billion 1-year Multi-Currency Revolving Credit Facility. This was signed on 10 January 2008 and represents a debut for TAQA in the syndicated loan market.

We continue to target strategic expansion across the energy sector, including upstream oil and gas, midstream distribution systems such as pipelines, LNG regasifi cation, and gas storage and power generation and water activities. While competition for acquisitions can be intense, especially with high energy prices boosting the purchasing power of companies in this sector, TAQA’s management team has considerable mergers and acquisitions experience, allowing it to expediently screen targets, assess risks and structure deals.

We will consider raising additional debt to fi nance our growth strategy, but are continually reviewing our fi nancing to ensure the most balanced and effi cient capital structure for the business.

TAQA’s Medium Term Note Program is rated Aa2 by Moody’s Investors Service and AA- by Standard & Poor’s, both with a stable outlook

34 34

ABERDEEN57O 07’ 60” N02O 06’ 00” W

BUILDING A GLOBAL ENERGY COMPANYTAQA ANNUAL REPORT 2007 35

The Securities & Commodities Authority (“SCA”) is in the process of introducing a new corporate governance code to be adopted by all companies listed on the ADSM and DFM. TAQA is in the process of developing a corporate governance framework supported by a system of internal controls based on international best practices to ensure compliance with the SCA’s new corporate governance requirements.

TAQA’s Code of Ethics describes and reinforces conduct that is based on its guiding core values, consistent with its policies and practices and essential for its legal and regulatory compliance obligations. A summary of the Code of Ethics is publicly available on TAQA’s website.

Committees

Audit Committee

TAQA’s audit committee is comprised of the following members who are appointed for a term of two years:Name Position

H.E. Salem Al-Sayaari Chairman H.E. Abdulla Saif Al-Nuaimi Member H.E. Mohammed Foulad Member