A Tailored Approach - Casey Quirk Tailored Approach.pdf · A Tailored Approach: Positioning to...

19

More than 200 asset consultants, institutional investors and intermediaries worldwide responded to this year’s survey. Respondents highlighted five key themes in asset allocation and buying behavior: 1. Further implementation of outcome-oriented investing, as investors continue to accelerate their divergence in asset allocations and buying behaviors. This reflects the long-term desire of asset owners worldwide to design policy allocations around specific objectives, which differ from investor to investor. 2. A broad concern with a rising interest rate environment across buyer channels, especially pensions, as a primary theme guiding portfolio changes. 3. A continued realignment of fixed income, with 48% of all participants expecting to restructure their fixed income portfolios in 2014. Corporate plans, in particular, continue to adopt LDI and rate-concerned investors delink their portfolios from interest rate sensitive strategies. 4. Surging appetite for real assets as investors continue to diversify alternatives portfolios. Real assets represent the largest category of new search activity consultants expect in 2014, representing 14% of forecasted new search activity, versus 6% in 2013. 5. Increased competition amongst managers, in particular for traditional mandates, as net flows subside and replacement search activity becomes the norm. Domestic equity, EAFE equity, and domestic fixed income will see the collective proportion of expected search activity from manager replacement increase to 58%, from 45% in 2013. Successful asset managers will adapt to changing demand drivers by: • Segmenting clients in order to properly position products against desired outcomes • Developing compelling thought leadership that addresses concerns of target buyers • Implementing data-driven, forward-looking product development processes • Designing new strategic engagement models for consultative sales and service EVESTMENT EVESTMENT EVESTMENT EVESTMENT EVESTMENT A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014

Transcript of A Tailored Approach - Casey Quirk Tailored Approach.pdf · A Tailored Approach: Positioning to...

More than 200 asset consultants, institutional investors and intermediaries worldwide responded to this year’s survey.

Respondents highlighted five key themes in asset allocation and buying behavior:

1. Further implementation of outcome-oriented investing, as investors continue to accelerate their divergence in asset allocations and buying behaviors. This reflectsthe long-term desire of asset owners worldwide to design policy allocations around specific objectives, which differ from investor to investor.

2. A broad concern with a rising interest rate environment across buyer channels, especially pensions, as a primary theme guiding portfolio changes.

3. A continued realignment of fixed income, with 48% of all participants expecting to restructure their fixed income portfolios in 2014. Corporate plans, in particular, continue to adopt LDI and rate-concerned investors delink their portfolios frominterest rate sensitive strategies.

4. Surging appetite for real assets as investors continue to diversify alternatives portfolios. Real assets represent the largest category of new search activity consultants expect in 2014, representing 14% of forecasted new search activity, versus 6% in 2013.

5. Increased competition amongst managers, in particular for traditional mandates, as net flows subside and replacement search activity becomes the norm. Domestic equity, EAFE equity, and domestic fixed income will see the collective proportion of expected search activity from manager replacement increase to 58%, from 45%in 2013.

Successful asset managers will adapt to changing demand drivers by:

• Segmenting clients in order to properly position products against desired outcomes• Developing compelling thought leadership that addresses concerns of target buyers • Implementing data-driven, forward-looking product development processes• Designing new strategic engagement models for consultative sales and service

EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

A Tailored Approach:Positioning to Outcome-Oriented Global InvestorsFebruary 2014

Authorship

Primary authors:Benjamin F. Phillips, PartnerJeffrey A. Levi, Director J. Tyler Cloherty, ManagerJason D. Roche, Manager

Casey Quirk contributor:Vasudha Bhalla, Manager

Casey, Quirk & Associates is a management consulting firm focused solely on advising investment managementfirms worldwide. Our partners and associates help ourclients develop broad business growth strategies, improveinvestment/product appeal and growth prospects, evaluatenew market and product opportunities, and enhanceincentive alignment structures. Our unparalleled industryknowledge and experience, detailed proprietary data, andglobal network of relationships make Casey Quirk theleading advisor to the owners and senior executives ofinvestment management firms in the world.

Table of Contents

1. Demographics ............................................2

2. Drivers of Asset Owner Behavior ..................3

3. Investor Concerns........................................5

4. Consultants’ Viewpoint ................................7

5. Long-Term Trends: Asset Allocation

in 2016 ..................................................11

6. Implications for Asset Managers..................15

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 1EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

eVestment provides a flexible suite of easy-to-use, cloud-based solutions to help global investors and theirconsultants select investment managers, enable assetmanagers to successfully market their funds worldwide and assist clients to identify and capitalize on globalinvestment trends. With the largest, most comprehensiveglobal database of traditional and alternative strategies,delivered through leading-edge technology and backed by fantastic client service, eVestment helps its clients bemore strategic, efficient and informed. The company wasfounded in 2000 and is headquartered in Atlanta, Georgia with global offices in New York, Toronto, London, Sydneyand Hong Kong.

EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 2EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

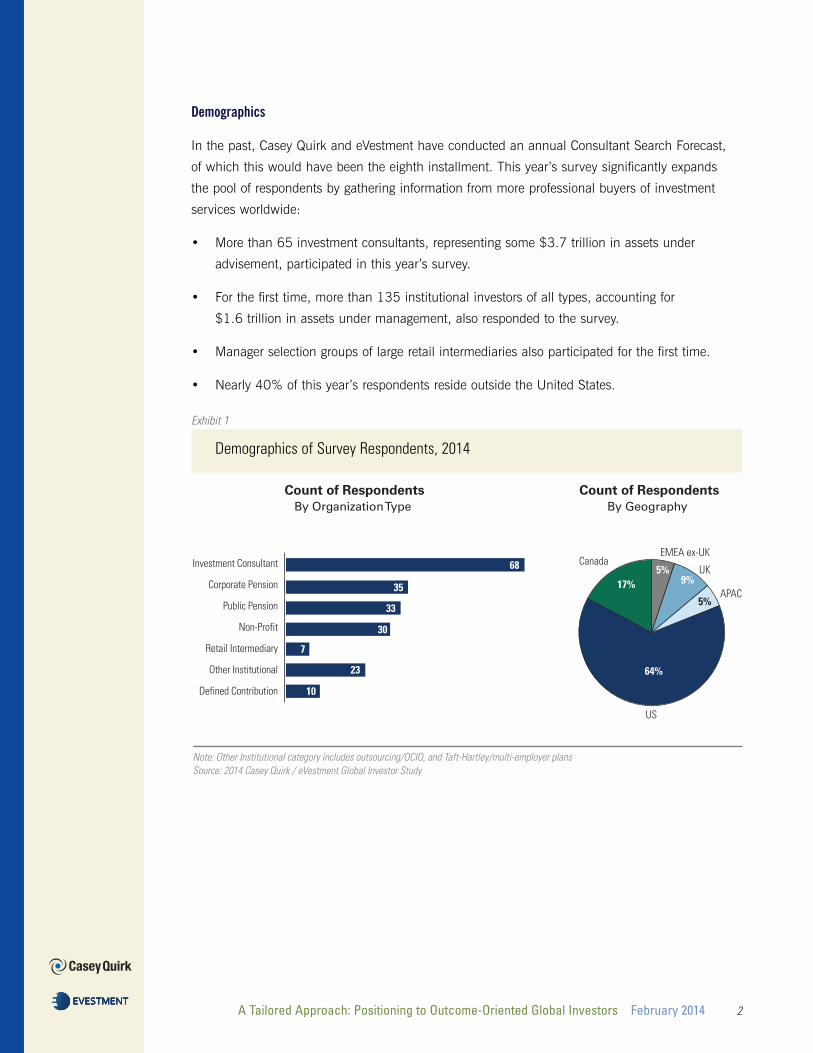

Demographics

In the past, Casey Quirk and eVestment have conducted an annual Consultant Search Forecast,

of which this would have been the eighth installment. This year’s survey significantly expands

the pool of respondents by gathering information from more professional buyers of investment

services worldwide:

• More than 65 investment consultants, representing some $3.7 trillion in assets under

advisement, participated in this year’s survey.

• For the first time, more than 135 institutional investors of all types, accounting for

$1.6 trillion in assets under management, also responded to the survey.

• Manager selection groups of large retail intermediaries also participated for the first time.

• Nearly 40% of this year’s respondents reside outside the United States.

Exhibit 1

Demographics of Survey Respondents, 2014

Count of RespondentsBy Geography

Investment Consultant

Corporate Pension

Public Pension

Non-Profit

Retail Intermediary

Other Institutional

Defined Contribution

US

64%

17%5%

9%

5%

CanadaUK

APAC

Count of RespondentsBy Organization Type

68

35

33

30

7

23

10

EMEA ex-UK

Note: Other Institutional category includes outsourcing/OCIO, and Taft-Hartley/multi-employer plansSource: 2014 Casey Quirk / eVestment Global Investor Study

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 3EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Drivers of Asset Owner Behavior

Increasingly, asset allocations of asset owners are diverging, reflecting different policy objectives

among the various categories of professional buyers. While most investors plan to decrease

equity commitments in favor of fixed income exposure during the next three years, the degree of

change varies. More importantly, asset owners have starkly different views about continuing to

raise their exposure to alternative investments.

Exhibit 2

Asset Allocation by Investor Type 2014 vs. 2016

4%

15%

37%

44%

2014

4%

16%

40%

39%

2016

5%

15%

30%

51%

2014

4%

18%

30%

48%

2016

5%

25%

20%

50%

2014

4%

27%

20%

49%

2016

13%

9%

41%

37%

2014

12%

11%

41%

36%

2016

8%

17%

23%

52%

2014

8%

18%

23%

51%

2016

19%

27%

14%

41%

2014

8%

18%

23%

51%

2016

Corporate Pension Public Pension Non-Profit Other Institutional Retail Intermediary Defined Contribution*

gg Other gg Alternatives gg Fixed Income gg Equity

Note: Other includes cash and ETF* Defined Contribution plans consist primarily of Australian Superannuation funds.Source: 2014 Casey Quirk / eVestment Global Investor Study

Different goals appear to motivate each category of institutional investor:

• Corporate pension schemes, realizing improved funding ratios after a heady bull market in

2013, expect to accelerate de-risking as they aim to immunize liabilities once and for all.

• Public pension plans, still more poorly funded than many of their corporate counterparts,

continue to focus on appreciation, raising alternatives exposures.

• Non-profit schemes such as endowments and foundations worry about meeting target returns

while producing the necessary cash flow for operations. As a result, they exhibit the highest

exposures to alternatives across all surveyed investor types, although their allocation profiles

are expected to remain relatively constant through 2016.

• Gatekeepers at retail intermediaries also report that they expect more static portfolio

allocations over the next three years, although they anticipate further reductions in cash

positions built by cautious investors. Additionally, they expect the rising age of their

investor base to favor more fixed income strategies.

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 4EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Source: 2014 Casey Quirk / eVestment Global Investor Study

2014 37% 25% 29% 10%

gg Equity gg Fixed Income gg Alternatives gg Other

APAC

2016 41% 24% 26% 8%

2014 47% 26% 22% 5%

2016 49% 23% 23% 6%

2014 47% 28% 17% 9%

2016 44% 29% 18% 9%

2014 43% 41% 10% 6%

2016 40% 41% 13% 6%

2014 49% 36% 13% 2%

2016 46% 36% 15% 2%

EMEAEx-UK

US

UK

Canada

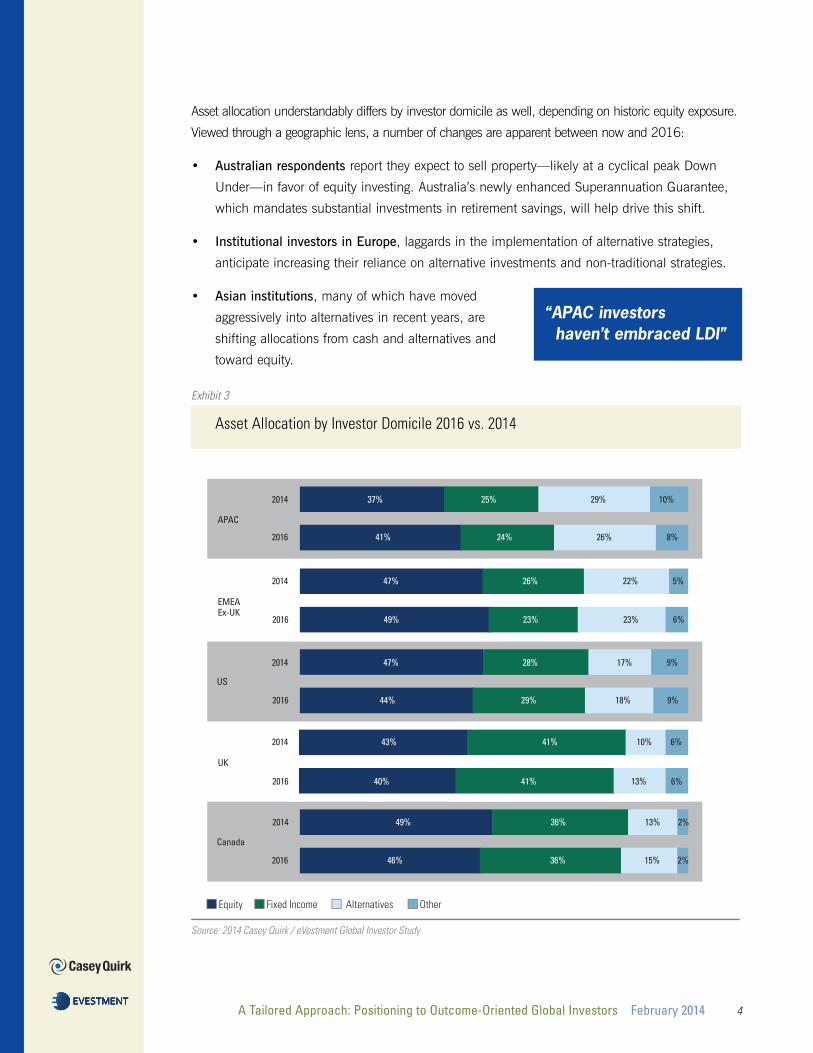

Asset allocation understandably differs by investor domicile as well, depending on historic equity exposure.

Viewed through a geographic lens, a number of changes are apparent between now and 2016:

• Australian respondents report they expect to sell property—likely at a cyclical peak Down

Under—in favor of equity investing. Australia’s newly enhanced Superannuation Guarantee,

which mandates substantial investments in retirement savings, will help drive this shift.

• Institutional investors in Europe, laggards in the implementation of alternative strategies,

anticipate increasing their reliance on alternative investments and non-traditional strategies.

• Asian institutions, many of which have moved

aggressively into alternatives in recent years, are

shifting allocations from cash and alternatives and

toward equity.

Exhibit 3

Asset Allocation by Investor Domicile 2016 vs. 2014

“APAC investorshaven’t embraced LDI”

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 5EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Source: 2014 Casey Quirk / eVestment Global Investor Study

48%

69%

58%

40%

48%

57%

33%

24%

52%

37%

43%

39%

21%

28%

44%

37%

30%

48%

30%

41%

27%

23%

35%

35%

18%

31%

31%

27%

17%

26%

Corporate Pension

Public Pension

Investment Consultant

Non-Profit

Other Institutional

Defined Contribution

Rising Interest R

ates

Government/Politic

al Risk/Regulation

Meeting Target Returns

Market Correctio

n/Recession

Risk Management/V

olatility

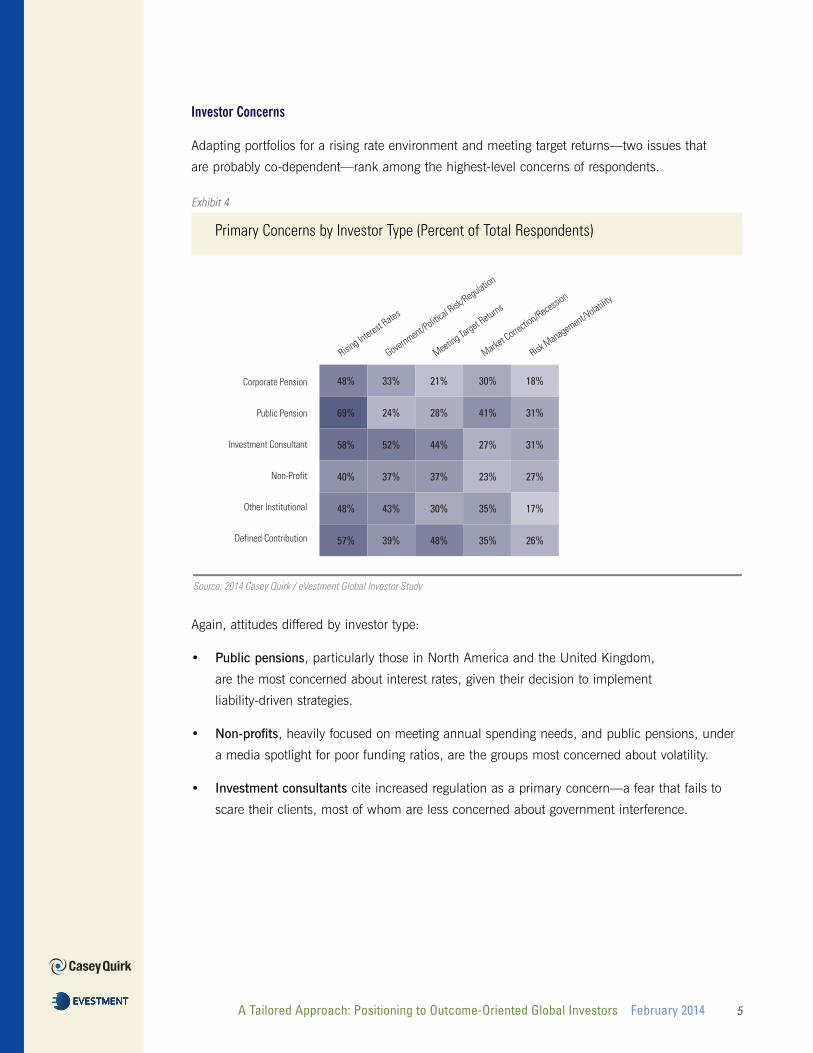

Investor Concerns

Adapting portfolios for a rising rate environment and meeting target returns—two issues that

are probably co-dependent—rank among the highest-level concerns of respondents.

Exhibit 4

Primary Concerns by Investor Type (Percent of Total Respondents)

Again, attitudes differed by investor type:

• Public pensions, particularly those in North America and the United Kingdom,

are the most concerned about interest rates, given their decision to implement

liability-driven strategies.

• Non-profits, heavily focused on meeting annual spending needs, and public pensions, under

a media spotlight for poor funding ratios, are the groups most concerned about volatility.

• Investment consultants cite increased regulation as a primary concern—a fear that fails to

scare their clients, most of whom are less concerned about government interference.

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 6EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Source: 2014 Casey Quirk / eVestment Global Investor Study

gg Higher allocation to Alternatives gg Offshoring and EM gg Invest in non traditional asset classes gg De-risking gg Passive Management gg Restructuring Fixed Income

Expected Changesby Organization Type

13%

25%

13%

50%

RetailIntermediary

13%

25%

13%

50%

DefinedContribution

15%

21%

8%

15%

3%

38%

CorporatePension

15%

15%

21%

12%3%

35%

PublicPension

21%

13%

22%

9%

3%

30%

InvestmentConsultant

19%

11%

15%

22%

7%

26%

Non-Profit

20%

20%

25%

10%

5%

20%

OtherInstitutional

Expected Changesby Organization Location

0% 0% 0% 0%

Europe 23% 23% 16% 19% 16% 3%

North America 32% 18% 16% 18% 12% 5%

Asset owners’ anticipated changes in investment policy reflect these worries:

• Pensions and retail intermediary gatekeepers—with

the most to lose from rising rates—are particularly

focused on restructuring their fixed income portfolios

during the next three years.

• U.S. investors are attracted to next-generation debt

strategies, positioned to generate income, agnostic of

interest rate movements.

• European investors, conversely, are more focused on raising their exposure to alternative

and non-traditional asset classes.

• While non-profits, overall, expect little change in their asset allocation, they cite de-risking as

a primary portfolio strategy for the next three years. This highlights the lack of homogeneity

even within a buyer segment: many non-profits indicate they feel over-allocated to risk asset

and illiquid stakes, while others are raising their allocation to drive total returns.

Exhibit 5

Expected Portfolio Strategy Changes by Investor Type and Domicile, 2014

“Domestic fixed income has a mix of strategic and tactical factors at play.”

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 7EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Low

201

4 E

xpec

ted

Sea

rch

Allo

cati

on

%

Hig

h

Source: 2014 Casey Quirk / eVestment Global Investor Study

Domestic Equity ◆

◆ EME

Low 2013 Expected Search Allocation % High

◆ Int’l Equity◆ Global Equity

RE ◆

◆ Commodities

◆ PE

FOHFs ◆

◆HY FI

IncreasingInterest

DecreasingInterest

ETF ◆

◆ HFs◆Other

EMD

•

◆ FI

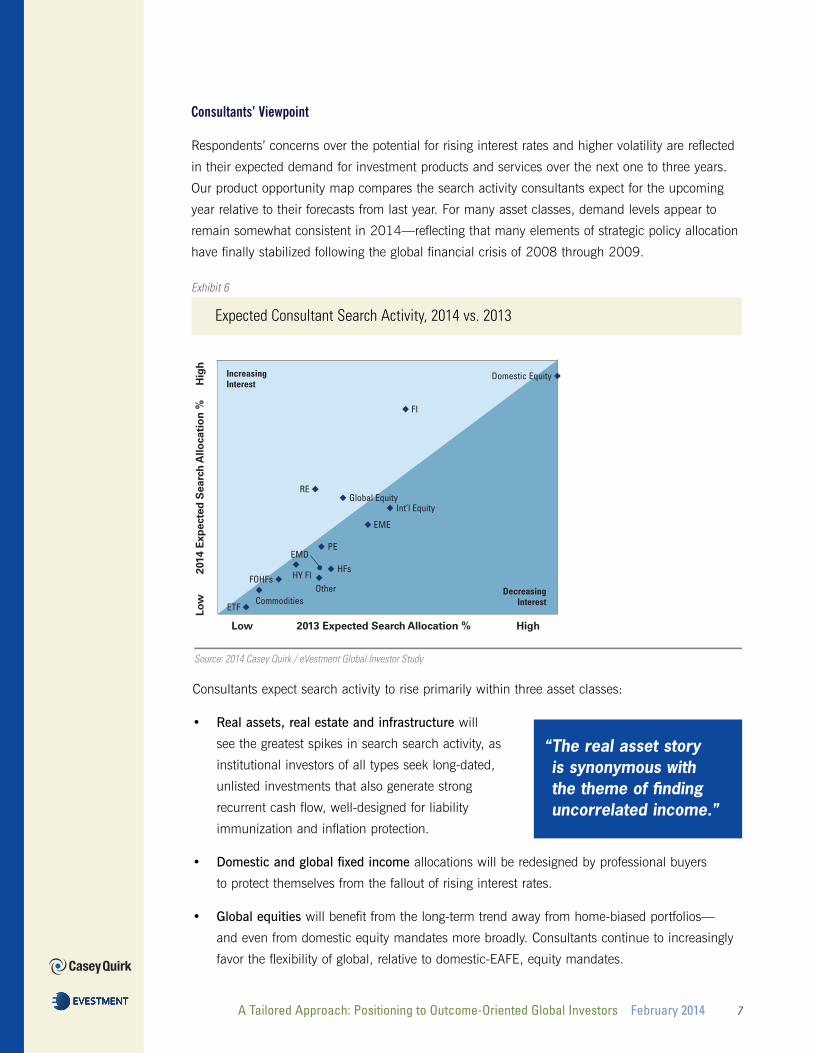

Consultants’ Viewpoint

Respondents’ concerns over the potential for rising interest rates and higher volatility are reflected

in their expected demand for investment products and services over the next one to three years.

Our product opportunity map compares the search activity consultants expect for the upcoming

year relative to their forecasts from last year. For many asset classes, demand levels appear to

remain somewhat consistent in 2014—reflecting that many elements of strategic policy allocation

have finally stabilized following the global financial crisis of 2008 through 2009.

Exhibit 6

Expected Consultant Search Activity, 2014 vs. 2013

Consultants expect search activity to rise primarily within three asset classes:

• Real assets, real estate and infrastructure will

see the greatest spikes in search search activity, as

institutional investors of all types seek long-dated,

unlisted investments that also generate strong

recurrent cash flow, well-designed for liability

immunization and inflation protection.

• Domestic and global fixed income allocations will be redesigned by professional buyers

to protect themselves from the fallout of rising interest rates.

• Global equities will benefit from the long-term trend away from home-biased portfolios—

and even from domestic equity mandates more broadly. Consultants continue to increasingly

favor the flexibility of global, relative to domestic-EAFE, equity mandates.

“The real asset story is synonymous with the theme of finding uncorrelated income.”

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 8EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Domestic Equity

Global Equity

International Equity

Emerging Markets Equity

Domestic/Global Fixed Income

High Yield Fixed Income

Emerging Market Debt

Hedge Funds

FQHF

Private Equity

Real Assets/RE/Infrastructure

Commodities

ETF

Other

Source: 2014 Casey Quirk / eVestment Global Investor Study

-10% -5% 0% 5% 10% 15%

-4.6%

-2.4%

-0.3%

-1.3%

-3.4%

-2.9%

-0.7%

-2.0%

-2.0%

8.8%

7.6%

1.8%

1.0%

Equi

ty

-1%

Othe

r

-7%

Fixe

d In

com

e

4%

Alte

rnat

ives

4%

0.2%

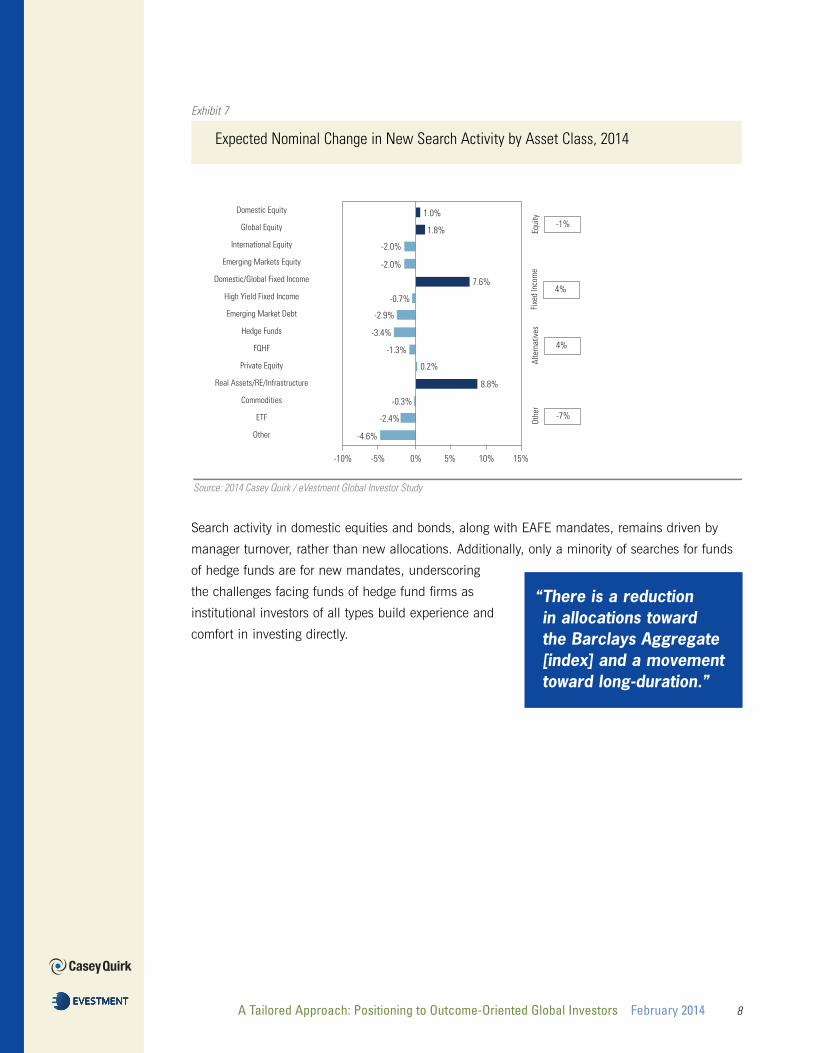

Exhibit 7

Expected Nominal Change in New Search Activity by Asset Class, 2014

Search activity in domestic equities and bonds, along with EAFE mandates, remains driven by

manager turnover, rather than new allocations. Additionally, only a minority of searches for funds

of hedge funds are for new mandates, underscoring

the challenges facing funds of hedge fund firms as

institutional investors of all types build experience and

comfort in investing directly.

“There is a reduction in allocations toward the Barclays Aggregate [index] and a movement toward long-duration.”

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 9EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Total Search Activity

Source: 2014 Casey Quirk / eVestment Global Investor Study

3%

11%

3%3%2%4%2%4%

6%

4%

9%

5%

7%

9%

10%

15%

2%0%0%

3%

14%

4%4%2%4%3%4%

8%

4%

7%

6%

8%

7%

10%

8%

2%0%0%

Other 3%

Alternatives24%

FixedIncome 25%

Equity 47%

4% Other

31% Alts

27% FI

38% Equity

New Search Activity

Other

Cash / MM

ETF

Commodities

Real Assets / RE/ Infra

PE FoFs

PE

FoHFs

HFs

Passive Fixed Income

EMD

Global Fixedf Income

HY Fixed Income

Domestic Fixed Income

Passive Equity

EME

International Equity

Global Equity

Domestic Equity

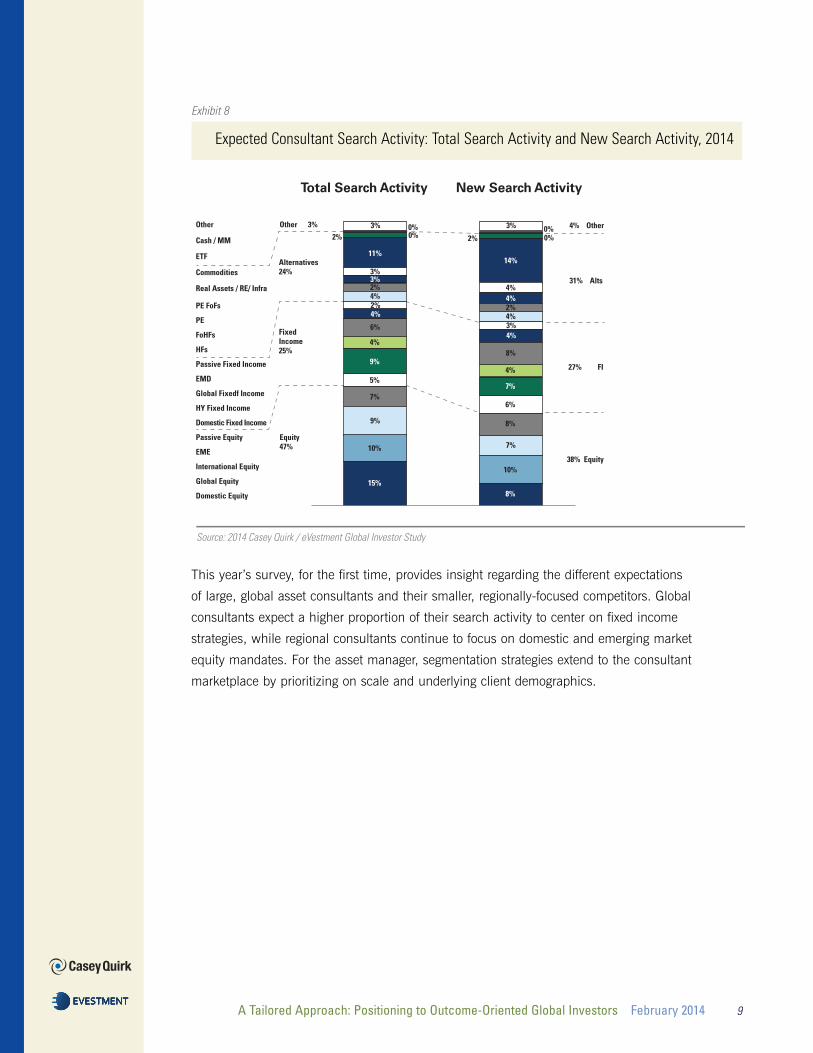

Exhibit 8

Expected Consultant Search Activity: Total Search Activity and New Search Activity, 2014

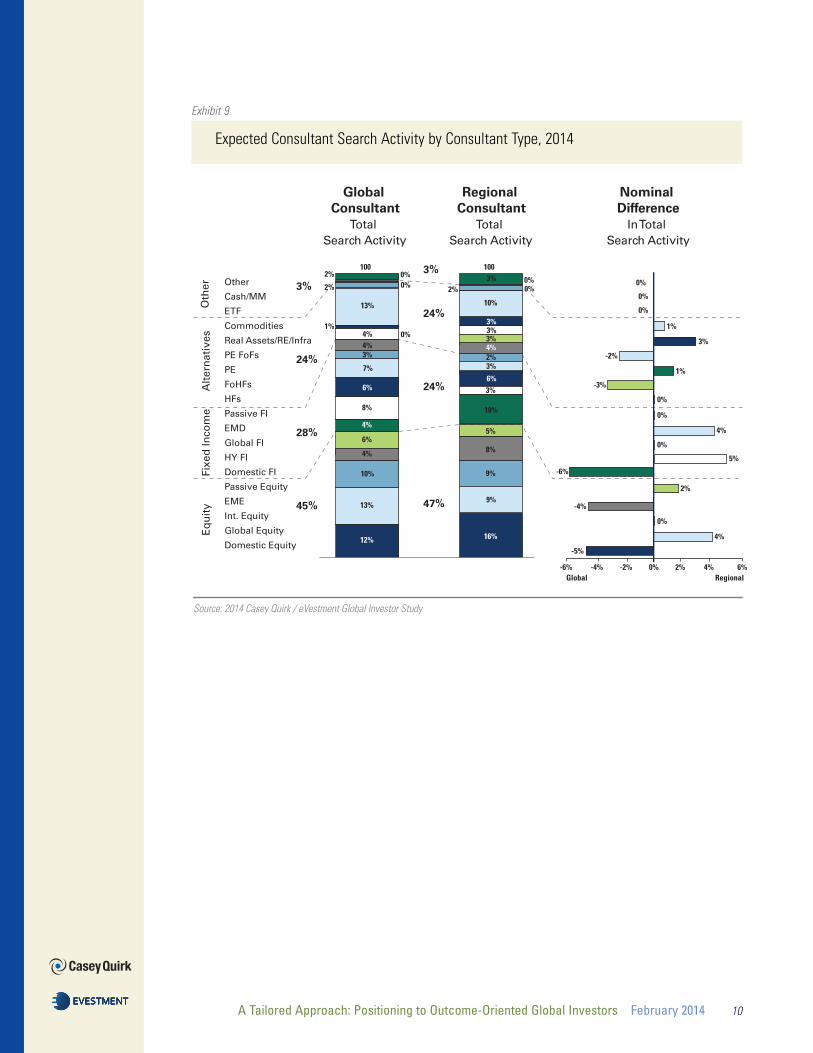

This year’s survey, for the first time, provides insight regarding the different expectations

of large, global asset consultants and their smaller, regionally-focused competitors. Global

consultants expect a higher proportion of their search activity to center on fixed income

strategies, while regional consultants continue to focus on domestic and emerging market

equity mandates. For the asset manager, segmentation strategies extend to the consultant

marketplace by prioritizing on scale and underlying client demographics.

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 10EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Global Consultant

Total Search Activity

Source: 2014 Casey Quirk / eVestment Global Investor Study

2%

13%

1%4%4%3%

7%

6%

8%

4%

6%

4%

10%

13%

12%

2%

0%0%

3%

14%

3%4%2%3%

6%

10%

3%

5%

8%

9%

9%

16%

2%0%0%

Other

Cash/MM

ETF

Commodities

Real Assets/RE/Infra

PE FoFs

PE

FoHFs

HFs

Passive FI

EMD

Global FI

HY FI

Domestic FI

Passive Equity

EME

Int. Equity

Global Equity

Domestic Equity

Regional Consultant

Total Search Activity

0% 3%3%

10%Oth

erA

lter

nat

ives

Fixe

d In

com

eE

qu

ity

3%

24%

28%

45%

3%

24%

24%

47%

0%

0%

0%

1%

3%

-2%

1%

-3%

0%

0%

0%

4%

5%

-6%

-4%

-5%

0%

2%

4%

-6% -4% -2% 0% 4% 6%2%

Nominal Difference

In Total Search Activity

Global Regional

100 100

Exhibit 9

Expected Consultant Search Activity by Consultant Type, 2014

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 11EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

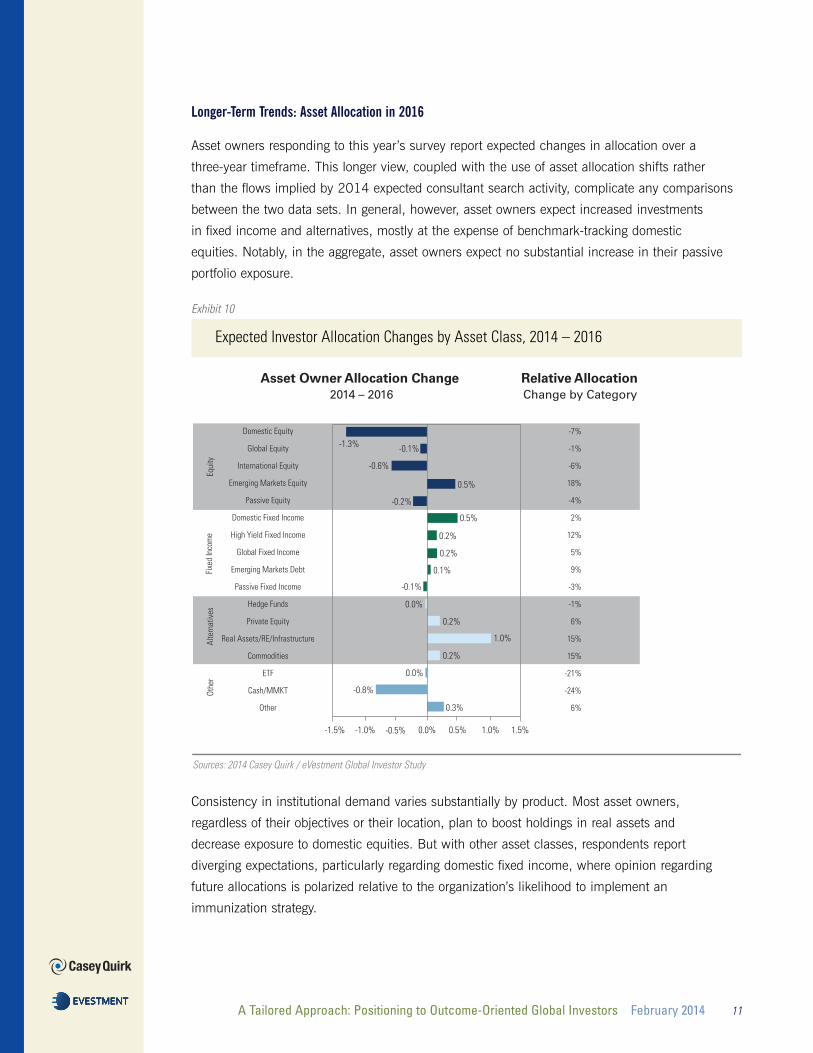

Longer-Term Trends: Asset Allocation in 2016

Asset owners responding to this year’s survey report expected changes in allocation over a

three-year timeframe. This longer view, coupled with the use of asset allocation shifts rather

than the flows implied by 2014 expected consultant search activity, complicate any comparisons

between the two data sets. In general, however, asset owners expect increased investments

in fixed income and alternatives, mostly at the expense of benchmark-tracking domestic

equities. Notably, in the aggregate, asset owners expect no substantial increase in their passive

portfolio exposure.

Exhibit 10

Expected Investor Allocation Changes by Asset Class, 2014 – 2016

Asset Owner Allocation Change 2014 – 2016

Domestic Equity

Global Equity

International Equity

Emerging Markets Equity

Passive Equity

Domestic Fixed Income

High Yield Fixed Income

Global Fixed Income

Emerging Markets Debt

Passive Fixed Income

Hedge Funds

Private Equity

Real Assets/RE/Infrastructure

Commodities

ETF

Cash/MMKT

Other

Sources: 2014 Casey Quirk / eVestment Global Investor Study

-1.5% -1.0% 0.0% 0.5% 1.0% 1.5%

0.3%

-0.8%

0.0%

0.2%

0.0%

-0.1%

0.1%

0.2%

0.5%

0.2%

0.2%

-0.2%

0.5%

Equi

tyOt

her

Fixe

d In

com

eAl

tern

ativ

es

-0.5%

-1.3%

-0.6%

-0.1%

1.0%

-7%

-1%

-6%

18%

-4%

2%

12%

5%

9%

-3%

-1%

6%

15%

15%

-21%

-24%

6%

Relative AllocationChange by Category

Consistency in institutional demand varies substantially by product. Most asset owners,

regardless of their objectives or their location, plan to boost holdings in real assets and

decrease exposure to domestic equities. But with other asset classes, respondents report

diverging expectations, particularly regarding domestic fixed income, where opinion regarding

future allocations is polarized relative to the organization’s likelihood to implement an

immunization strategy.

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 12EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Sources: 2014 Casey Quirk / eVestment Global Investor Study

+3.1%

3.0%

Corporate Pension

0.4%

-0.2%

0.1%

-0.3%

-1.1%

0.2%

0.6%

0.2% 0.2%

-0.8%

0.2%0.4%

0.0% 0.0%

0.7%

-0.3% -0.2%

0.1%

-0.1%

-0.7%

0.3%0.4%

0.0% 0.0%

1.3%

0.1%0.0% 0.0% 0.0%

Public Pension Non-Profit Other Institutional Retail Intermediary Defined Contribution

+0.1% -0.2% 0.2% 0.0% 0.5%

Total Change in Fixed Income Exposure

gg Domestic Fixed Income gg High Yield Fixed Income gg Global Fixed Inxcome gg EMD gg Passive Fixed Income

Exhibit 11

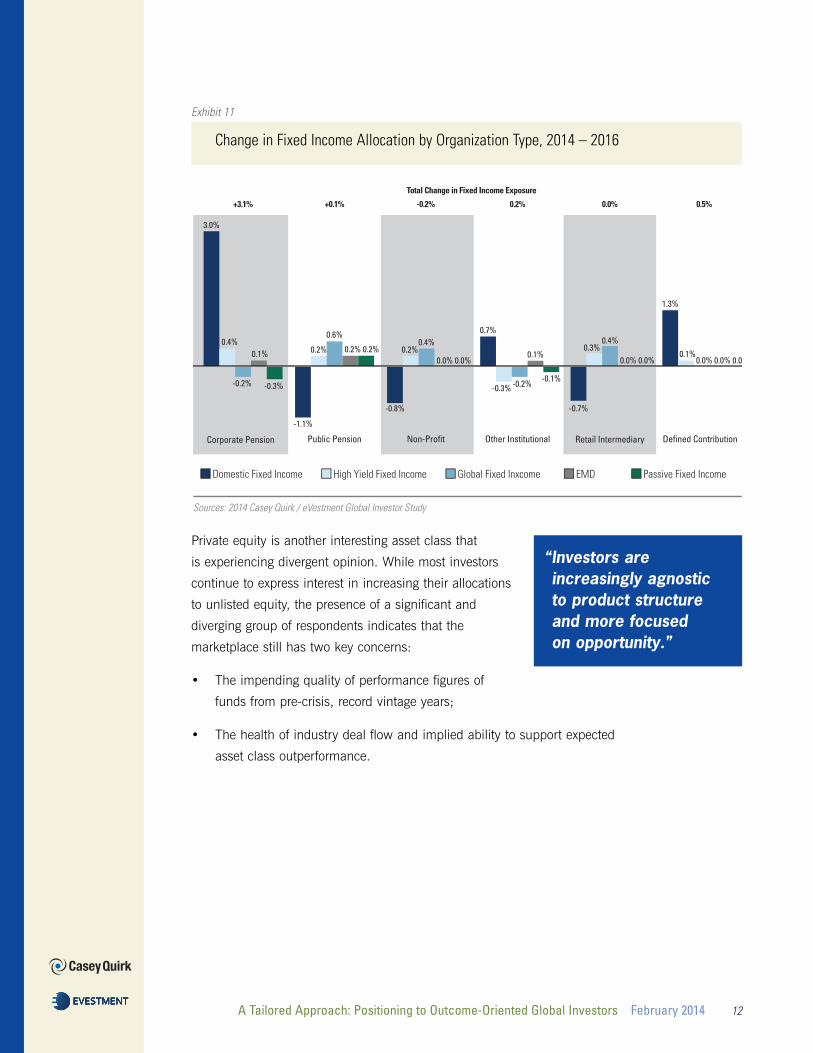

Change in Fixed Income Allocation by Organization Type, 2014 – 2016

Private equity is another interesting asset class that

is experiencing divergent opinion. While most investors

continue to express interest in increasing their allocations

to unlisted equity, the presence of a significant and

diverging group of respondents indicates that the

marketplace still has two key concerns:

• The impending quality of performance figures of

funds from pre-crisis, record vintage years;

• The health of industry deal flow and implied ability to support expected

asset class outperformance.

“Investors are increasingly agnostic to product structure and more focused on opportunity.”

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 13EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Note: Excludes institutions that expect no allocation change in the asset class.Source: 2014 Casey Quirk / eVestment Global Investor Study

-7%

RealAssets/RE/Infra

-42%

-29%-22%

-9% -8%-14% -13%

-18%-1% -5% -9%

-25%

-7% -4%-2%

38%

12% 6% 9%20% 17%

7%20%

12% 8% 11% 13%22%

4% 6% 1%

High Agreement

Low Agreement

DivergingOpinion

DomesticEquity

Cash/MM

IntEquity

EME HFs PassiveEquity

PE GlobalEquity

Commodities HY Fixed

Income

GlobalFixed

Income

DomesticFixed

Income

PassiveFixed

Income

EMD ETF

Decr

ease

Incr

ease

Exhibit 12

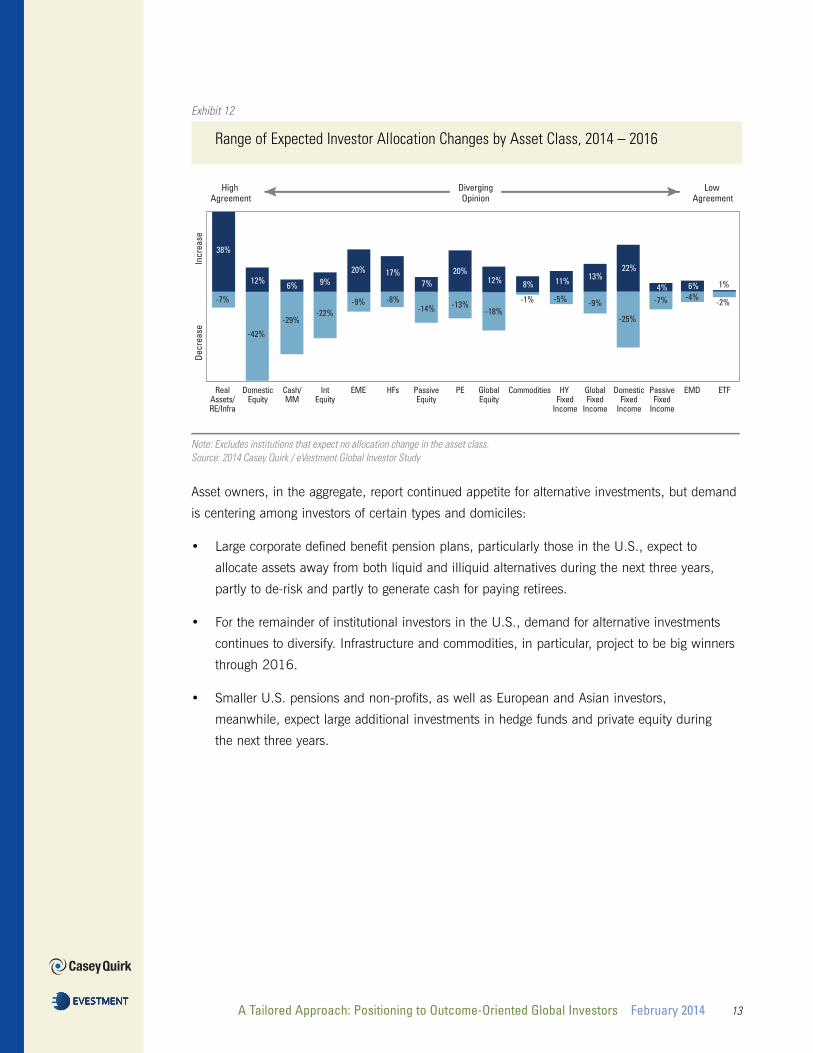

Range of Expected Investor Allocation Changes by Asset Class, 2014 – 2016

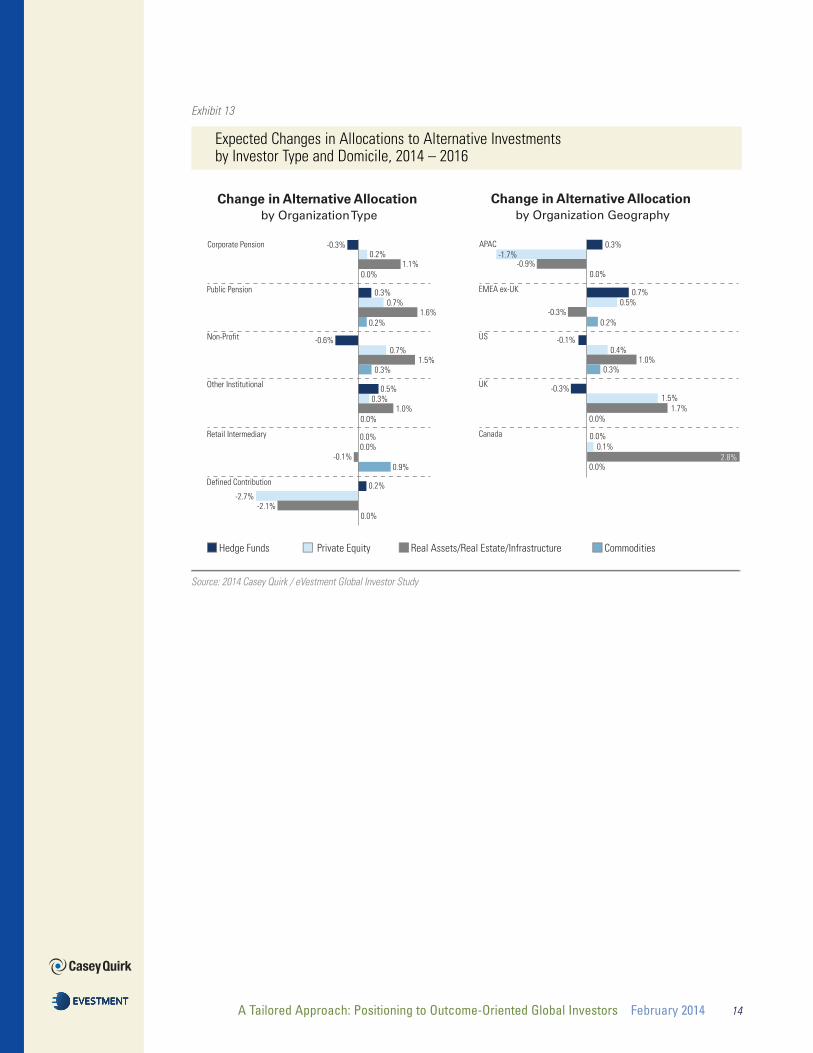

Asset owners, in the aggregate, report continued appetite for alternative investments, but demand

is centering among investors of certain types and domiciles:

• Large corporate defined benefit pension plans, particularly those in the U.S., expect to

allocate assets away from both liquid and illiquid alternatives during the next three years,

partly to de-risk and partly to generate cash for paying retirees.

• For the remainder of institutional investors in the U.S., demand for alternative investments

continues to diversify. Infrastructure and commodities, in particular, project to be big winners

through 2016.

• Smaller U.S. pensions and non-profits, as well as European and Asian investors,

meanwhile, expect large additional investments in hedge funds and private equity during

the next three years.

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 14EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Exhibit 13

Expected Changes in Allocations to Alternative Investments by Investor Type and Domicile, 2014 – 2016

Change in Alternative Allocation by Organization Type

Source: 2014 Casey Quirk / eVestment Global Investor Study

Corporate Pension

Public Pension

Non-Profit

Other Institutional

Retail Intermediary

Defined Contribution

-0.3%0.2%

1.1%0.0%

0.3%0.7%

1.6%0.2%

-0.6%0.7%

1.5%0.3%

0.5%0.3%

1.0%0.0%

0.0%0.0%

-0.1%0.9%

0.2%-2.7%

-2.1%0.0%

Change in Alternative Allocation by Organization Geography

APAC

EMEA ex-UK

US

UK

Canada

0.3%-1.7%

-0.9%0.0%

0.7%0.5%

-0.3%0.2%

-0.1%0.4%

1.0%0.3%

-0.3%1.5%

1.7%0.0%

0.0%0.1%

2.8%0.0%

gg Hedge Funds gg Private Equity gg Real Assets/Real Estate/Infrastructure gg Commodities

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 15EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

Implications for Asset Managers

Shifting demand characteristics among asset owners worldwide are creating tactical product-

related opportunities for asset managers. But this year’s survey findings also underscore five broad

themes reshaping strategic asset allocation among investors globally, with repercussions for asset

managers and the way they position their capabilities to clients:

1. Outcome-oriented investing: Continually diverging approaches to asset allocation among

different types of investors underscores the fact that asset owners and intermediaries

increasingly allocate their portfolios among outcomes, not benchmarks. This means an asset

manager’s products and services will increasingly play different roles in the portfolios of

different investors. Recognizing the investor-specific positioning will improve the chances

of winning a specific mandate and deepening a client relationship.

2. Fixed income: The end of tapering and the prospect of rising rates will be the most

powerful short-term trend reshaping retail and institutional investor portfolios. Asset

managers who can position their offers within the context of a shift from compartmentalized,

benchmark-oriented fixed income assignments to a more dynamic, multi-sector approach

to bond investing will benefit dramatically. Winning next-generation products will include

multi-asset income portfolios, unconstrained bond mandates, global and emerging market

strategies and volatility-managed products.

3. Liability-driven strategies: The survey findings clearly indicate that the conversations asset

managers have with corporate pensions will differ dramatically than those they have with

any other investor. As defined benefit plans move into their twilight phase, they will seek

products that help them achieve specific objectives linked to de-risking, liquidity, and cash

flow to retirees. Additionally, the competitive environment for these assignments will change,

as insurers offer pension risk transfer arrangements. Asset managers will need to separately

evaluate and service the opportunities they see in the defined benefit segment.

4. Real assets: Increasing allocations and search activity

indicate that asset owners have growing demand for

non-correlated investments, but seem dissatisfied

with the current products—and, by extension, the

real asset managers—on offer. This partly reflects

that asset managers still sell real assets as illiquid

yield generators, rather than developing and

positioning real asset products that meet specific

outcomes. This is particularly critical given that different asset owners use such products

as a means to different ends; for example, corporate pensions use real assets for long-term

yield, while non-profits seek alpha. Asset management firms must carefully think through

the product and positioning strategies attached to their real asset strategies.

“Size is a factor for real assets. Not every institution can take advantage of opportunities.”

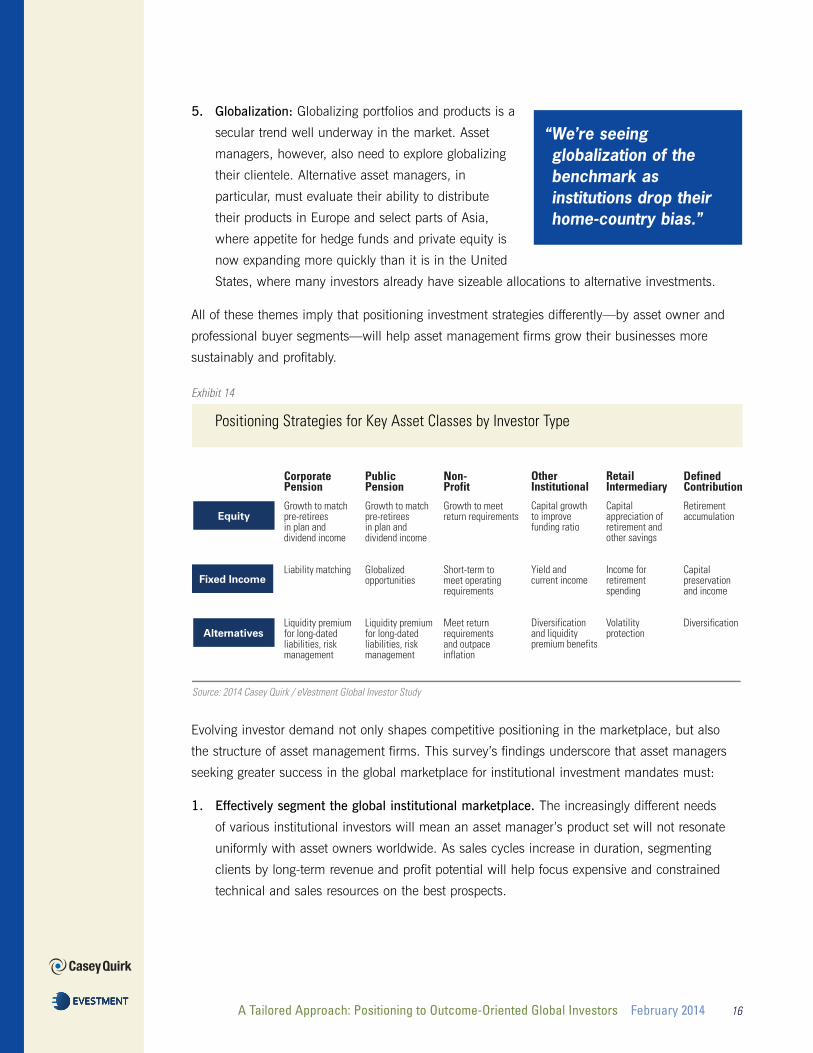

Equity

CorporatePension

Growth to match pre-retirees in plan and dividend income

Liability matching

Liquidity premiumfor long-dated liabilities, risk management

PublicPension

Growth to match pre-retirees in plan and dividend income

Globalized opportunities

Liquidity premiumfor long-dated liabilities, risk management

Non-Profit

Growth to meet return requirements

Short-term to meet operating requirements

Meet return requirements and outpace inflation

OtherInstitutional

Capital growth to improve funding ratio

Yield and current income

Diversification and liquidity premium benefits

RetailIntermediary

Capital appreciation of retirement and other savings

Income for retirement spending

Volatilityprotection

DefinedContribution

Retirement accumulation

Capital preservation and income

Diversification

Fixed Income

Alternatives

Source: 2014 Casey Quirk / eVestment Global Investor Study

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 16EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

5. Globalization: Globalizing portfolios and products is a

secular trend well underway in the market. Asset

managers, however, also need to explore globalizing

their clientele. Alternative asset managers, in

particular, must evaluate their ability to distribute

their products in Europe and select parts of Asia,

where appetite for hedge funds and private equity is

now expanding more quickly than it is in the United

States, where many investors already have sizeable allocations to alternative investments.

All of these themes imply that positioning investment strategies differently—by asset owner and

professional buyer segments—will help asset management firms grow their businesses more

sustainably and profitably.

Exhibit 14

Positioning Strategies for Key Asset Classes by Investor Type

Evolving investor demand not only shapes competitive positioning in the marketplace, but also

the structure of asset management firms. This survey’s findings underscore that asset managers

seeking greater success in the global marketplace for institutional investment mandates must:

1. Effectively segment the global institutional marketplace. The increasingly different needs

of various institutional investors will mean an asset manager’s product set will not resonate

uniformly with asset owners worldwide. As sales cycles increase in duration, segmenting

clients by long-term revenue and profit potential will help focus expensive and constrained

technical and sales resources on the best prospects.

“We’re seeing globalization of the benchmark as institutions drop their home-country bias.”

A Tailored Approach: Positioning to Outcome-Oriented Global Investors February 2014 17EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

2. Develop thought leadership that credibly positions their products within an outcome-

oriented context. Asset managers able to lead broad discussions about investments,

markets and portfolios—and translate those opinions into a conversation about how their

investment products and strategies will help meet client needs in a rising rate environment—

will stand out.

3. Support data-driven product development processes that meet the increasing complexity

of investor needs, as asset owners measure managers by their ability to meet outcomes

rather than beat benchmarks.

4. Use a strategic engagement model with clients. As relationships with professional buyers

become more complex in an outcome-oriented environment, correctly staffing and structuring

both sales and client service to support a consultative approach to institutional clients will

become a critical competitive differentiator.

EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT

John F. Casey, ChairmanKevin P. Quirk, PartnerDavid J. Bauer, PartnerDaniel Celeghin, PartnerGrace L. Cicero, PartnerJeb B. Doggett, PartnerYariv Itah, Managing PartnerBenjamin F. Phillips, Partner

Casey, Quirk & Associates is a management consulting firm focused solely on advisinginvestment management firms worldwide. Our partners and associates help our clientsdevelop broad business growth strategies, improve investment/product appeal and growth prospects, evaluate new market and product opportunities, and enhanceincentive alignment structures. Our unparalleled industry knowledge and experience,detailed proprietary data, and global network of relationships make Casey Quirk theleading advisor to the owners and senior executives of investment management firms in the world. To discuss this white paper, please contact:

Benjamin F. Phillips Jeffrey A. Levi J. Tyler ClohertyPartner Director ManagerNew York Darien [email protected] [email protected] [email protected] +1 917 476 2140 US +1 203 899 3035 US +1 203 899 3023

Casey, Quirk & AssociatesDarien • New York • Hong Kongwww.caseyquirk.com

A Tailored Approach:Positioning to Outcome-Oriented Global InvestorsFebruary 2014

About eVestment (www.evestment.com)eVestment provides a flexible suite of easy-to-use, cloud-based solutions to help global investors and their consultants select investment managers, enable asset managers to successfully market their funds worldwide and assist clients to identify and capitalize on global investment trends. With the largest,most comprehensive global database of traditional and alternative strategies, delivered through leading-edge technology and backed by fantastic client service, eVestment helps its clients be more strategic,efficient and informed. The company was founded in 2000 and is headquartered in Atlanta, Georgia with global offices in New York, Toronto, London, Sydney and Hong Kong.

Kwittken & Company+ 1 [email protected]

eVestment5000 Olde Towne Parkway, Suite 100Marietta, Georgia 30068 +1 877-769-2388 www.evestment.com

EVESTMENTEVESTMENTEVESTMENTEVESTMENTEVESTMENT