A regulatory sandbox for robo advice

46

A regulatory sandbox for robo advice 3 December 2018 Georg Ringe and Christopher Ruof AGCOM & EJLE workshop, Rome

Transcript of A regulatory sandbox for robo advice

A regulatory sandboxfor robo advice

3 December 2018

Georg Ringe and Christopher Ruof

AGCOM & EJLE workshop, Rome

The topic

Main arguments

• Robo advice = automated financial advice, based on algorithms

• Regulatory uncertainty

• Proposal for sandbox, implementation within the EU framework

I. Robo Advice

Nutmeg

Robo Advice

Robo Advice

Robo Advice

How does it work?

• Input from consumer (online questionnaire): personal information, investment goals

• Algorithm: constructs portfolio proposal –typically ETFs, based on the stock, pension, or commodity markets and some mutual funds

• weighting of components depends on consumer input, in particular risk appetite

Robo Advice

• Investment decision by consumer

• Subsequent processing– depends on characteristics of the respective

robo advisor

– some provide continuous monitoring and evaluation of investment strategies

– some offer automatic reallocating or rebalancing of the portfolio according to stated preferences

Robo Advice

Robo Advice

Key advantages

• costs– Robo advice average fees between 0.4% and 0.8%

– fee for human financial advice usually 1-2%

– economies of scale – “advice” provided by one computer algorithm to many customers; human advice has fix cost for each individual advice process

• simplicity and accessibility of advice– independent from bank opening times, available

around the clock, each day of the year

– from any location in the world online

– advice typically after about 15 minutes, without traditional client onboarding process, extensive paperwork

Key advantages

• Quality of advice– Neutral, unbiased advice, free from human

error

– Cf history of fraud etc with humans

– Transparent, consistent, no conflicts of interest

– mitigate agency conflicts between financial advisors and customers?

– -> “trust advantage” for consumers

Performance (US robos)

Performance (German robos)

Key advantages

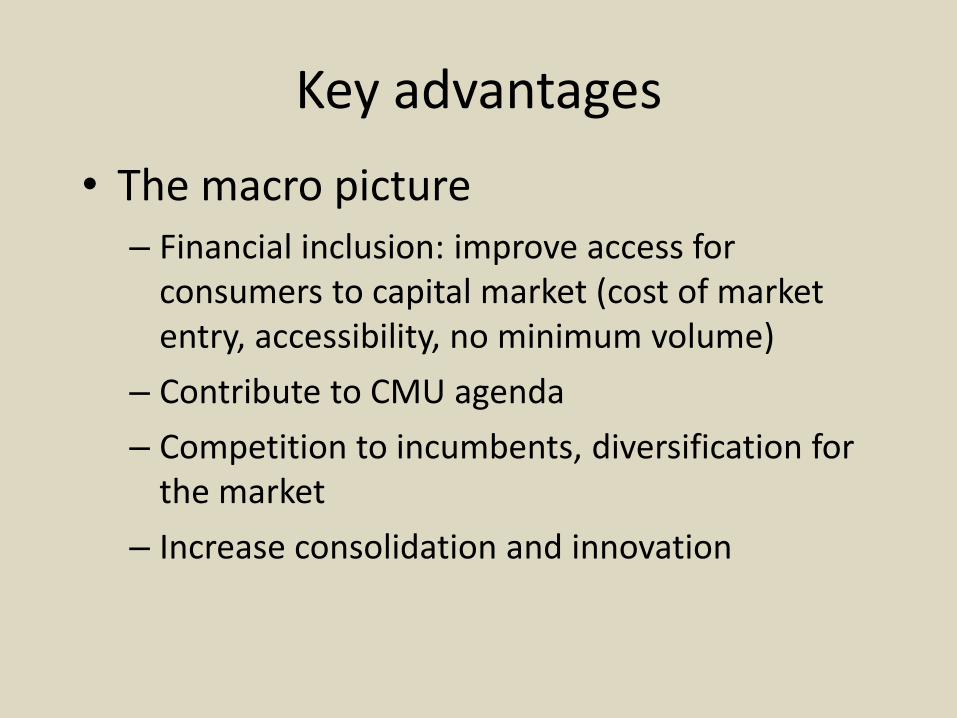

• The macro picture– Financial inclusion: improve access for

consumers to capital market (cost of market entry, accessibility, no minimum volume)

– Contribute to CMU agenda

– Competition to incumbents, diversification for the market

– Increase consolidation and innovation

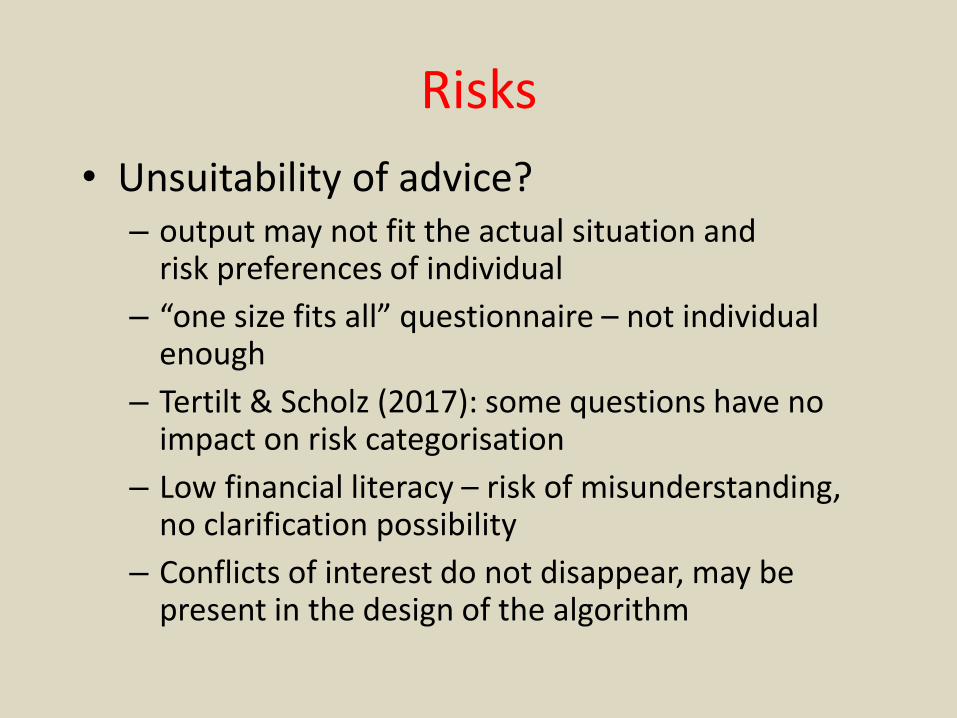

Risks

• Unsuitability of advice?– output may not fit the actual situation and

risk preferences of individual

– “one size fits all” questionnaire – not individual enough

– Tertilt & Scholz (2017): some questions have no impact on risk categorisation

– Low financial literacy – risk of misunderstanding, no clarification possibility

– Conflicts of interest do not disappear, may be present in the design of the algorithm

Risks

• Malfunctioning– Error in programming or functioning of algorithm

– Cyber threats, hacking likely in start up scenario

– Potentially greater impact on customers than for human error

• Behavioural problems– Fisch et al (2014): “warm body effect”

– Prevalence of biases when answering questionnaire

– Investors reluctant to read / digest online information

Risks

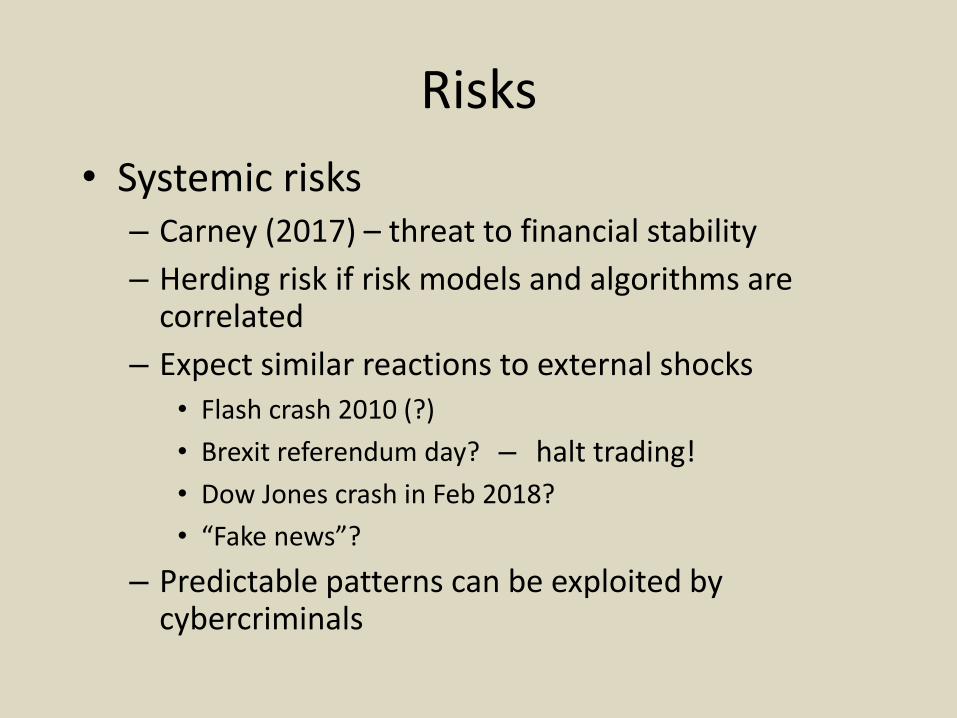

• Systemic risks– Carney (2017) – threat to financial stability

– Herding risk if risk models and algorithms are correlated

– Expect similar reactions to external shocks

• Flash crash 2010 (?)

• Brexit referendum day?

• Dow Jones crash in Feb 2018?

• “Fake news”?

– Predictable patterns can be exploited by cybercriminals

– halt trading!

Artificial Intelligence

• Key determinant in future development of robo advice

• Exploit machine learning & big data

– Individual level: “actions speak louder than words”

– Market level?

• Entails promises (more tailored advice etc.) & risks (black box decisions etc.)

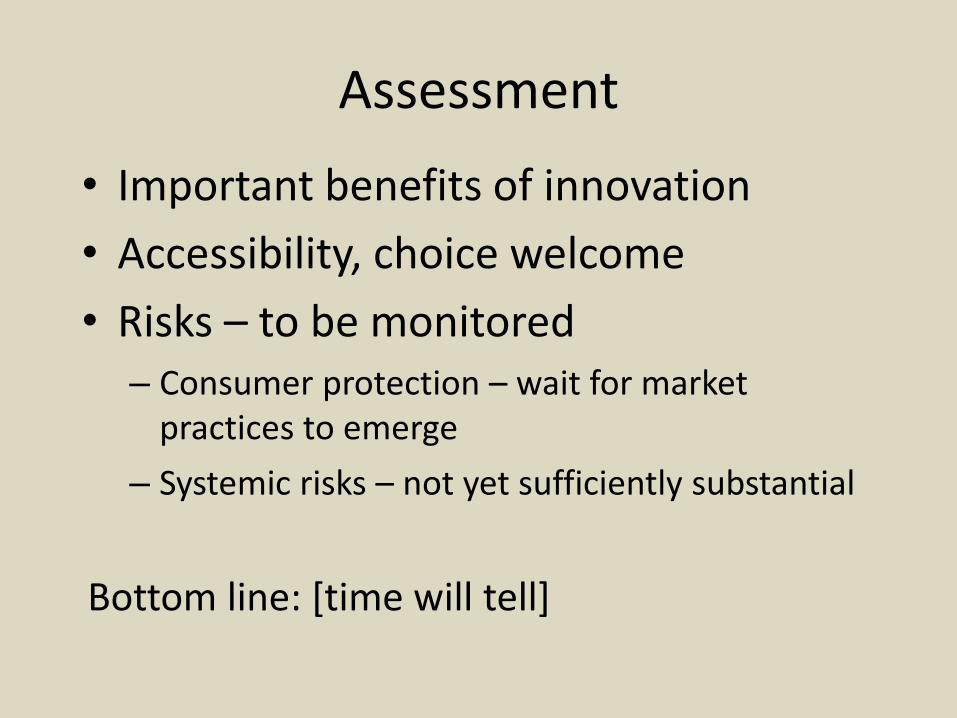

Assessment

• Important benefits of innovation

• Accessibility, choice welcome

• Risks – to be monitored– Consumer protection – wait for market

practices to emerge

– Systemic risks – not yet sufficiently substantial

Bottom line: [time will tell]

II. How does regulation respond?

“Uncertainty”

• EU consultation (2016): regulatory uncertainty– Mifid etc: “written for a different age”

• EBA 2017: very different regimes across EU, 35% of robo advisors under no regulatory regime at all

• Zetsche et al (2017); EU Commission (2017): MS interpret pieces of EU law very differently

Consequences

• barrier to entry • barrier for potential investors & consumers • may increase “time to market” by a third,

at a cost of 8% of product lifetime revenue (Stern et al 2014)

• Problem for regulators, arbitragepossibilities.

III. How should regulation respond?

Starting point

Assessment of robo advice ambiguous

• Promises and risks of new business model

• Regulatory uncertainty; shortcoming of the framework; some unaddressed risks; high barriers to entry

• Dynamic solution needed that responds to immediate need – yet safeguards against risks

• Case for “regulatory sandbox”

Sandbox

Regulatory sandbox

• “controlled space” where firms can test and validate innovative products, regulation relaxed

• special safeguards for consumers

• limited period of time

• support and monitoring by authority

• “mutual learning” idea

SandboxSandboxes in operation

• UK and NL

• Switzerland, Canada, East Asia and Australia etc.

Common features

• Entry requirements: innovation factor, stability concerns, individual need; sectoral limitations

• Consumer protection: redress, ombudsman, compensation scheme

• Time limitation

• Relaxation of regulatory burden: waivers, no enforcement, discretion, guidance

• Exit: remove privilege, consumer exit

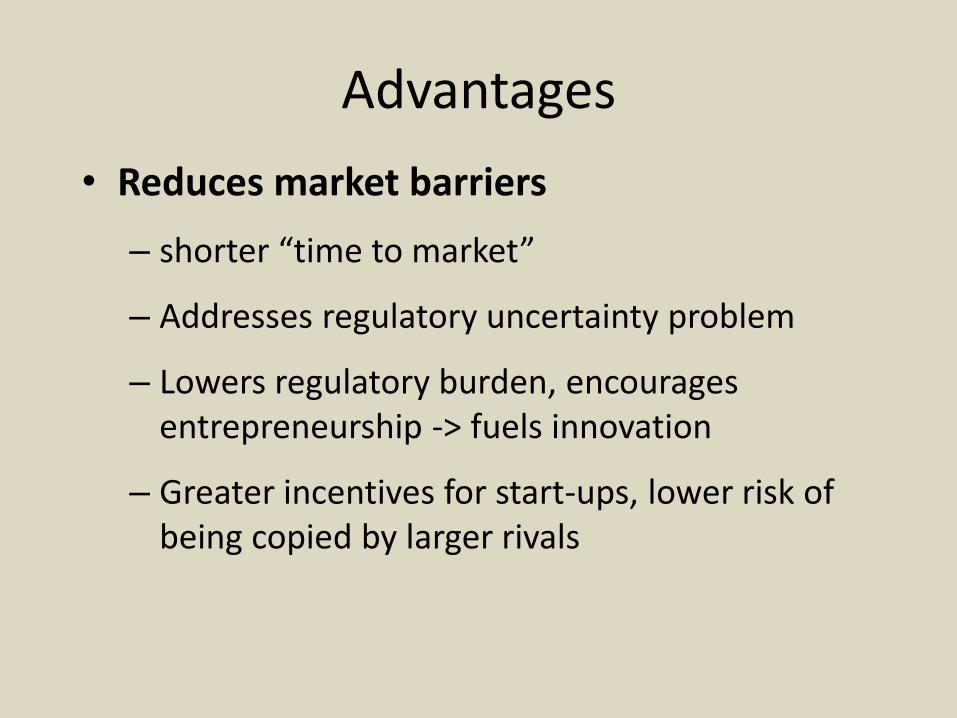

Advantages

• Reduces market barriers

– shorter “time to market”

– Addresses regulatory uncertainty problem

– Lowers regulatory burden, encourages entrepreneurship -> fuels innovation

– Greater incentives for start-ups, lower risk of being copied by larger rivals

Advantages

• Institutionalised dialogue between firm and regulator (mutual learning)

– Regulatory learning – risks and benefits

– Collection of data and experience

– Creates culture of dialogue and cooperation

• Signalling effect – communicates regulatory flexibility and open-mindedness towards new technologies and innovative firms

– UK sandbox contributes to London’s pre-eminence as a fintech hub

A Sandbox for Robos

Benefits for robo advice firms

• Addresses regulatory uncertainty problem

• Lowers market access problem

• Help, guidance throughout sandbox testing phase

• May lead to regulatory improvement and cutting of red tape generally

• Create more trust towards customers and investors

A Sandbox for Robos

Benefits for regulators

• Better monitoring of market and individual firms

• Data collection, learning process

• Experimentation with RegTech/SupTech

• will inform macroprudential issues

A Sandbox for Robos

Benefits for consumers

• More innovation and competition – lower prices

• Regulatory uncertainty improved and consumer protection in place

• Increase “trust” in innovative products

• Increased competition – higher diversification – fosters stability

A Sandbox for Robos

Advantages over changing traditional regulation

• Experimentation character, overcoming regulatory agnosticism and knowledge dilemma (difficulty of cost-benefit analysis in financial regulation, Gordon 2014)

• Speed – in particular in the EU context

• Flexibility / possibility of subsequent change

A Sandbox for Robos

Disadvantages

• Costly, resource-intensive

• No panacea, no ultimate solution

• May not be credible if no strong regulatory expertise (Zetsche et al 2017)

• Lack of transparency?

IV. Specific proposal

Implementing the Sandbox

Additional problem in EU

• Multiple layers of legislation / regulation

• Sandboxes operating on MS level cannot set aside EU legislation

• No true EU regulator who could undertake sandbox on EU level

Implementing the Sandbox

Olivier Guersent, DG for financial stability (September 2016):

“We think we should dedicate a bit of thought to how we can have a sound regulatory sandbox approach in Europe that allows markets to develop, that allows innovation to flourish, that allows those companies that innovate to go across borders in the single market while being consistent with our framework”.

Implementing the Sandbox

Two possibilities

(1) Introduce a genuine EU sandbox, either

– fully operated at EU level, or

– executed by MS

(2) “Guided sandbox”: sandbox at MS level, coordinated by EU

Implementing the Sandbox

(1) Genuine EU sandbox

• Apparently some support by EU Commission

• Respondents to fintech consultation

• But: politically unrealistic

• Legal barriers (Meroni)

• Treaty change required? Long period of implementation versus time constraints

Implementing the Sandbox

A more realistic option

• European Banking Federation (EBF) 2016; Banking Stakeholder Group (BSG) 2017

• recommend harmonised framework for experimentation (with harmonised tools)

• i.e. establishment of level playing field for MS and participants, but execution within the power of national authorities

• Easier to implement yet still time consuming

• One-size-fits-all?

Implementing the Sandbox

(2) “Guided sandbox”

• MS sandboxes, coordinated by EU

• “guided policy implementation”: experimentation with sandbox concept itself

• ESMA could serve as

– Monitor

– Forum of exchange with experiences

– Institution adopting guidelines and recommendations

• MS have incentive to experiment and compete

Implementing the Sandbox

Advantages

• Speed of adoption and flexibility

• ESMA’s role initially – highlight where room for flexibility exists already now

• Future legislation may deliberately leave more room for manoeuver

• Smaller MS would benefit disproportionately from ESMA guidance

• More sophisticated regulators may experiment themselves

Implementing the SandboxMultiple-level feedback process

• MS report back to ESMA

• ESMA’s feedback to MS

• Market and competition as a source of feedback

• More sophisticated regulators may experiment themselves

Race to the bottom?

• If executed properly, market failures will be addressed

• EU law setting minimum standards

• Expect market learning process, MS specialisation

Follow-up regulationRegulatory Trajectory

(1) Maintaining dialogue

• Build on positive relationship from Sandbox

• Maintain information and data exchange

• Increasingly monitor macro issues

(2) Addressing barriers within the market

• Identify inadequate obstacles and address them

• Accompanied + supervised scaling up

• Cooperation with other regulators (MoUs)

Conclusion

Robo advice• Greater consumer choice, efficient tool, facilitates market

access• Risks still underexploredThe case for a sandbox• Helpful regulatory tool for uncertain, new phenomena• Particular EU context – challenges• Pragmatic proposal to implement on the MS level with EU

guidanceFollow-up Trajectory• Maintaining dialogue & information exchange, while

addressing barriers to scaling up