A Presentation on Schroder ISF EURO Equity Alpha* … · 4 SISF EURO Equity Alpha 0307 Italian...

21

SISF EURO Equity Alpha 0307 Representing Schroders: Angelo Manca Schroder Investment Management Ltd 31 Gresham Street, London, EC2V 7QA Authorised and Regulated by the Financial Services Authority April 2007 A Presentation on Schroder ISF EURO Equity Alpha* Capabilities *Schroder International Selection Fund will be referred to as Schroder ISF throughout this presentation For Professional Investors Only

Transcript of A Presentation on Schroder ISF EURO Equity Alpha* … · 4 SISF EURO Equity Alpha 0307 Italian...

SISF EURO Equity Alpha 0307

Representing Schroders:

Angelo Manca

Schroder Investment Management Ltd31 Gresham Street, London, EC2V 7QAAuthorised and Regulated by the Financial Services Authority

April 2007

A Presentation on Schroder ISF EURO Equity Alpha* Capabilities

*Schroder International Selection Fund will be referred to as Schroder ISF throughout this presentation

For Professional Investors Only

1

SISF EURO Equity Alpha 0307

Schroder ISF EURO Equity Alpha: Characteristics

Performance Aim: first decile on a rolling 3 year basis

Index: MSCI EMU (TR)

Geographies: Eurozone, Switzerland, Scandinavia, Eastern Europe

Non-Euro < 20% of portfolio

Approx 100% currency hedged (into Euro)

Max stock over(under) weight: 10%

Max sector over(under) weight: 15%

Usual UCITS III rules apply

Fund Manager: Angelo Manca

Tracking error range: < 10%

Number of stocks: 30 - 50

Launched: 23 March 2007

Product

2

SISF EURO Equity Alpha 0307

Why should I invest in Schroder ISF EURO Equity Alpha?

Schroder ISF Italian Equity strong performance, even more so when risk adjusted

Same investment approach as in Schroder ISF Italian Equity

Performance is driven by business understanding and logic, not local expertise

Downside protection/ amplified exposure to equities long term upside

“Value with a catalyst” investment philosophy

Stock universe enlarged to about 1,500 stocks, versus about 200 in ItalyEuro + selected areas offer far wider investment opportunities

Better leverage of Schroders resources and brainpower

Schroder ISF EURO Equity Alpha

“Value with a catalyst” + geographies + concentration, hypothesis driven screening

Differentiated product within Schroders range

3

SISF EURO Equity Alpha 0307

95

100

105

110

115

120

125

130

135

140

145

150

Dec-05 Mar-06 Jun-06 Sep-06 Dec-06 Mar-07

Schroder ISF Italian Eq Italian MIBTEL

Performance (Euro’s%)

Schroder ISF Italian Equity

Fund Performance since Takeover

Performance based on ‘C’ Class shares

Source: S&P Micropal, bid to bid, performance for 01/12/05 to 29/03/07

December 2005 through to 29th March 2007 vs. Italian Mibtel

Key performance contributors:

Coin

Jolly Hotels

Gemina

Banca Italease

Aeroporto di Firenze

Sirti

Underweight in Telecom Italia

4

SISF EURO Equity Alpha 0307

Italian Equity Risk Adjusted Performance

Fund manager track record

Schroder ISF Italian Equity *

Return**

*Class A**Total return Dec 30 2005- Dec 29 2006. All returns adjusted for dividends*** Calculated on daily data**** Calculated on weekly data***** Calculated on monthly dataSource: Schroders, Bloomberg

33.0%

0.59Beta***

0.35Sharpe ratio****

33.5%

1.12

0.31

23.6%

1

Fidelity Italy Fund

MIBTEL (benchmark)

Schroder ISF Italian Equity was number 2 in 2006…

…for 50bps!

HOWEVER, it had much less exposure to market direction

Sharpe ratio only measure volatility…

… not reliance on market direction

0.86Beta**** 1.12 1

1.03Beta***** 1.48 1

(methodological note: in a steady bull market, outperforming funds’ realised Beta increases with time intervals)

Plain return ranking

2 1

Deep industry analysis and search for industrial catalysts have allowed us to deliver superior adjusted returns.

0.76Sharpe ratio*****

0.55

5

SISF EURO Equity Alpha 0307

Performance Attribution: Since Takeover

Source: Schroders, Wilshire Atlas

Currency: EURO

Where has performance come from?

Performance from 1st December 2005 to 29th March 2007The conviction over(under)weight positions we talked to you about in recent months have delivered strong outperformance

We expect continuing strong outperformance from them throughout 2007

Jolly Hotels

Banca Italease

Gruppo Coin

Gemina

Telecom Italia

Acea

ENI

Toro Assicurazioni

Bca Pop Di Verona

Telecom Italia

Return ContributionStock Position

Overweight

Overweight

Overweight

Overweight

Underweight

Overweight

Underweight

Overweight

Overweight

Underweight

+4.05

+3.35

+1.90

+1.75

+1.52

+1.05

+0.87

+0.70

+0.64

+0.60

210.0%

175.6%

70.8%

67.7%

-3.5%

68.1%

10.4%

56.1%

43.8%

-0.1%

Since Takeover: Top 10 positive stock contributors Since Takeover: Top 10 negative stock contributors

Management EC

Autostrade Merid

Dada

Intesa Sanpaolo

Immob Lombarda

Ifil

Capitalia

Guala Closures

Akzo Nobel

Finmeccanica

Overweight

Overweight

Overweight

Underweight

Overweight

Zero Weight

Underweight

Overweight

Overweight

Zero Weight

-1.17

-0.66

-0.59

-0.49

-0.45

-0.42

-0.37

-0.34

-0.27

-0.24

-12.0%

-6.4%

24.9%

47.5%

9.3%

111.8%

47.2%

26.8%

-1.5%

50.9%

Return ContributionStock Position

6

SISF EURO Equity Alpha 0307

Value with a catalyst investment style

No sector rotation/macro bets

Pure stock picking investing

Valuation and in-depth business research are key

European universe will allow to focus on catalysts

Early event situations

No “hedge fund crowded” investments

Looking for poorly researched companies

Looking for undervalued/unseen discontinuities in underlying businesses, regulation, industry, etc etc

Looking for changes in corporate structure

Looking for anomalies in companies valuation/market obsessions

Fairly valuing companies prospects

Follow conviction investment themes

Key advantages

Transformation in company P&L, hence value creation

Downside protection, as whatever markets do, P&L is transformed

No value traps

Concentration, effort intensity and efficiency

Investment Philosophy

Hypothesis driven screeningPrinciples

Activism

7

SISF EURO Equity Alpha 0307

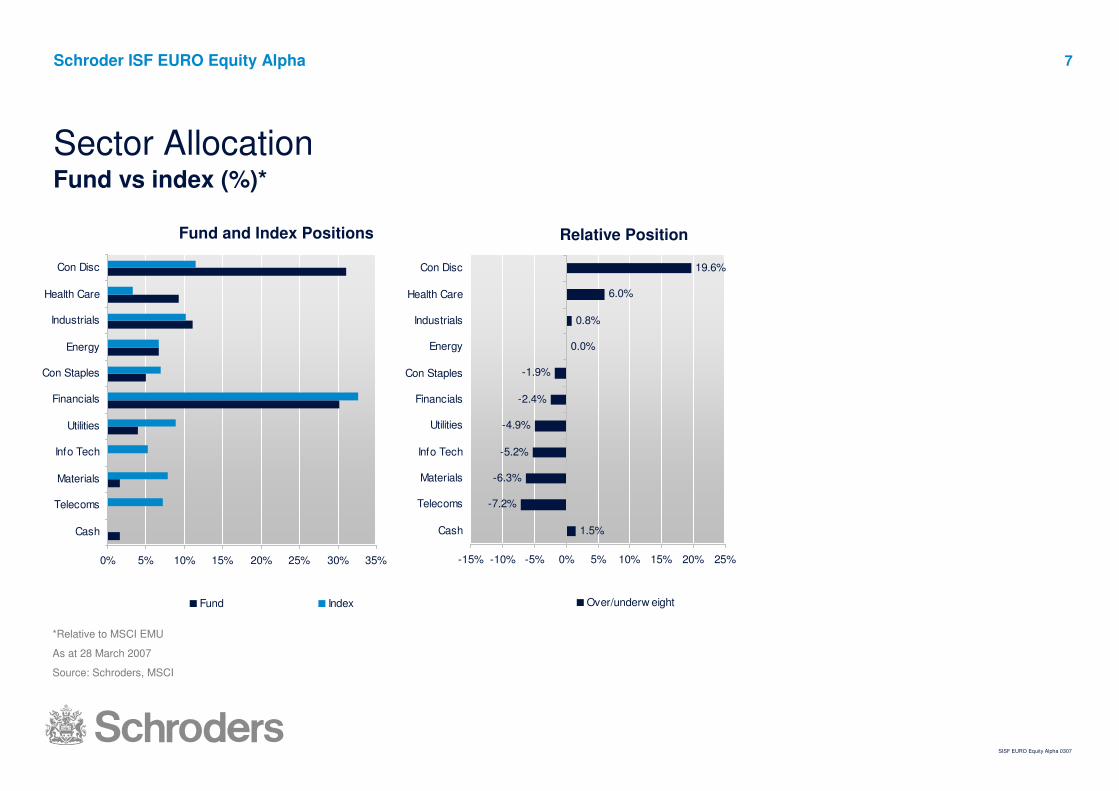

*Relative to MSCI EMU

As at 28 March 2007

Source: Schroders, MSCI

Sector Allocation

0% 5% 10% 15% 20% 25% 30% 35%

Cash

Telecoms

Materials

Info Tech

Utilities

Financials

Con Staples

Energy

Industrials

Health Care

Con Disc

Fund Index

Fund vs index (%)*

1.5%

-7.2%

-6.3%

-5.2%

-4.9%

-2.4%

-1.9%

0.0%

0.8%

6.0%

19.6%

-15% -10% -5% 0% 5% 10% 15% 20% 25%

Cash

Telecoms

Materials

Info Tech

Utilities

Financials

Con Staples

Energy

Industrials

Health Care

Con Disc

Over/underw eight

Fund and Index Positions Relative Position

Schroder ISF EURO Equity Alpha

8

SISF EURO Equity Alpha 0307

Current Active Loads on Individual Stocks

Telefonica

Nokia

Siemens

Sanofi-Aventis

BBVA

BNP Parabis

E.On

Daimler Chrysler

Axa

Societe Generale

-2.2

-2.0

-2.0

-1.9

-1.9

-1.9

-1.9

-1.7

-1.6

-1.4

Load difference

Jolly Hotels

ANF

Flo

Fielmann

Gemina

Anglo Irish Bank

Carrefour

Amplifon

Inditex

Allianz

9.6

4.3

4.0

3.9

3.1

3.0

3.0

3.0

2.3

2.1

Top 10 Positive Load Differences at 28.03.07

Source: Schroders

Load difference Top 10 Negative Load Differences at 28.03.07

Schroder ISF EURO Equity Alpha

9

SISF EURO Equity Alpha 0307

2

3

4

5

6

Dec-05 Feb-06 Apr-06 Jun-06 Aug-06 Oct-06 Jan-07 Mar-07

Gruppo Coin

Source: Thomson Financial Datastream

Gruppo Coin– Totally forgotten company

–Underperforming dept stores business

–New shareholders / management

–Rock solid asset base

–Bought at EUR 2.9 average (with in mind fair value EUR 5.5)

–Selling discipline: sold a fourth at EUR 4.8, another fourth at EUR5.27

Stock Examples

Gruppo CoinDec 2005-March 2007 stock price charts

€

10

SISF EURO Equity Alpha 0307

0

5

10

15

20

25

30

Sep-05 Dec-05 Apr-06 Jul-06 Nov-06 Mar-07

Jolly Hotels

Source: Thomson Financial Datastream

Jolly Hotels

Jolly Hotels: the time has come (overweight)

Undermanaged for years

Real estate: make it work or sell

EUR580m owned real estate

All disposals made at higher prices

New top management

Fair value in the EUR25 area (indeed bid at EUR25)

Stock Examples

11

SISF EURO Equity Alpha 0307

1.4

1.8

2.2

2.6

3.0

3.4

3.8

Sep-05 Nov-05 Jan-06 Mar-06 May-06 Jul-06 Sep-06 Nov-06 Jan-07 Mar-07

GEMINA

Source: Thomson Financial Datastream

Gemina

Gemina: precious assets (overweight)

Impressive asset base

Unique airport with no constraint, passenger to grow by 50% in 6 years

Secular traffic growth as final destination

Global demographics to support traffic

Unexploited real estate development

Current sector reorganisation is an opportunity to increase efficiency/asset utilisation

Stock Examples

12

SISF EURO Equity Alpha 0307

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

Dec-05 Mar-06 Jul-06 Nov-06 Mar-07

FIELMANN

Source: Thomson Financial Datastream

Fielmann

Stock Examples

Dec 2005-March 2007 stock price charts

Fielmann

–Optical retailer: attractive sector

–Dominant position in Germany

–Unexploited pricing power

–Expanding abroad

–Favourable demographics

–Favourable industry trends

–Bought during September sell-off

€

13

SISF EURO Equity Alpha 0307

19.0

20.0

21.0

22.0

23.0

24.0

25.0

Dec-05 Mar-06 Jul-06 Nov-06 Mar-07

AUTOSTRADESource: Thomson Financial Datastream

Autostrade

Stock Examples: Intellectual Discipline- How We Manage Mistakes

Dec 2005-March 2007 stock price charts

Autostrade

- For once lured in a ‘popular, crowded trade’

- Bought 7000,000 shares on Apr 24-25 2006 around EUR 24

- Why we bought? We thought it was a wise diversification, in Abertis valuable assets (especially Airports), forming a global infrastructure giant able to compete on every tender in the world.

- Deeper analysis revealed that maybe a catalyst was there, but not value:

- Sell side analysts using unreasonably low WACC, assuming unreasonable traffic growth on Italian motorways

- No real advantage in being a “global bidder”: competition is on cost of debt, there is no edge vs Macquarie and the likes

- Sold it on May 23-26 2006 around EUR 22.8 (-5%)

- Since then Autostrade underperformed the market by 19%

€

14

SISF EURO Equity Alpha 0307

Key European investment themes

Optical retailers consolidation

Elevators manufacturers expansion

Global wealth’s flight to performance

“Media disintermediation”

Gaming opportunity

European markets structure, available assets

Global market trends, building business for the future

Huge assets available throughout Europe

Buy content and online content aggregator, sell physical distribution platforms

Italian + emerging countries

Portfolio implications

Fielmann, Luxottica

Schindler

Non traditional asset managers

No telecom stocks, no media, but Endemol!

Looking at European Equities

Current evidence Analysis

Lottomatica, Intralot

15

SISF EURO Equity Alpha 0307

Key European investment themes (continued)

Global mobility

Society polarization

Population ageing

Restructuring, change in management

Capacity constraint asset vs airlines

Fragmented luxury markets

Nursing homes, hearing aid industry structure and dynamics

Often spectacular at retailers

Portfolio implications

Orpea, Fresenius, CIR, Phonak, Amplifon, William Demant

Coin, Etam Developpement, Wolford

Current evidence Analysis

Looking at European Equities

Yachting

Rome, Vienna

16

SISF EURO Equity Alpha 0307

Key differences versus current Schroder ISF range

Eurozone only

Schroder ISF EURO Equity

Differentiated product within Schroders range

Schroder ISF European Special Situations

Schroder ISF EURO Equity Alpha

Geographies

Eurozone + Scandinavia, Switzerland, Eastern Europe (up to 20%)

Pan Europe

Style Value with a catalyst/pre-event situations

Flexible – no inherent style bias

Concentration 30-50 stocks

Flexible – no inherent style bias

50-100 stocks 50-70 stocks

Performance AimsTo outperform the MSCI EMU by 3% p.a (net of fees) over rolling 3 year periods

To outperform the MSCI Europe, and to be first decileamongst the peer group over a rolling 3 year period

To outperform the MSCI Europe, and to be first decileamongst the peer group over a rolling 3 year period

17

SISF EURO Equity Alpha 0307

Appendix

18

SISF EURO Equity Alpha 0307

Angelo Manca

— Masters in Financial Markets and Institutions-Bocconi University

— Career started at McKinsey in Italy in Mar 2000

— Investment career started in Mar 2001: Julius Baer Brokerage Italy, equity analysts, covering Italian Telecoms and diversified portfolios of medium/small cap companies

— In Aug 2004 joined Redbrick Capital Management in Boston, where he was responsible for company research and trading of positions in European equity markets

— Joined Schroders in September 2005

Angelo Manca

European Equity Fund Manager

European Equity Team

19

SISF EURO Equity Alpha 0307

Investment TeamsSignificant European investment resources

Denis Clough 23Olaf Siedler 22Gary Clarke 13Leon Howard-Spink 10James Squire 7Angelo Manca 6

Ken LambdenHead of Equities

Rosemary Banyard 25Andrew Brough 20Andrew Lynch 8Iain McNaught 7Gillian De Candole 6

17 European Analysts and Associates*

Large Cap Team Small Cap Team

Years’ Experience Years’ Experience

Chris Taylor 18 years’ experienceProduct Manager

European Team

Note: Team Heads are highlighted in bold. Numbers relate to years of investment experience *17 analysts includes 6 dedicated to Europe ex UK, 8 dedicated to the UK and 3 covering global sectors

20

SISF EURO Equity Alpha 0307

Important informationThis presentation does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder International Selection Fund (the “Company”). Nothing in this presentation should be construed as advice and is therefore not a recommendation to buy or sell shares.

Subscriptions for shares of the Company can only be made on the basis of its latest prospectus together with the latest audited annual report (and subsequent unaudited semi-annual report, if published), copies of which can be obtained, free of charge, from Schroder Investment Management (Luxembourg) S.A.

In accordance with the current prospectus, other than for the Schroder ISF Global Property Securities fund, the Company will seek UK distributor status for all distribution A and C shares.

An investment in the Company entails risks, which are fully described in the prospectus.

Past performance is not a guide to future performance and may not be repeated. Investors may not get back the full amount invested, as prices of shares and the income from them may fall as well as rise. Third party data is owned by the applicable third party identified above and is provided for your internal use only. Such data may not be reproduced or re-disseminated and may not be used to create any financial instruments or products or any indices. Such data is provided without any warranties of any kind. Neither the third party data owner nor any other party involved in the publication of this document can be held liable for any error. The terms of the third party's specific disclaimers are set forth in the Important Information section at www.schroders.lu

Exchange rate changes may cause the value of any overseas investments to rise or fall.

Schroders has expressed its own views and opinions in this presentation and these may change.

The fund referred to in this presentation may be in or out of scope of the European Union Directive 2003/48/EC (Taxation of Savings Income in the Form of Interest Payments), as implemented in Luxembourg Law.

This presentation is issued by Schroder Investment Management (Luxembourg) S.A., 5, rue Höhenhof, L-1736 Senningerberg, Luxembourg.For your security, all telephone calls are recorded. R.C.S. Luxembourg: B 37.799