A presentation by Sphamandla Ngema 07 May 2015 – Msunduzi Municipality Presentation 1.

41

A presentation by Sphamandla Ngema 07 May 2015 – Msunduzi Municipality Presentation 1

-

Upload

warren-rice -

Category

Documents

-

view

215 -

download

0

Transcript of A presentation by Sphamandla Ngema 07 May 2015 – Msunduzi Municipality Presentation 1.

1

A presentation by Sphamandla Ngema07 May 2015 – Msunduzi Municipality Presentation

2

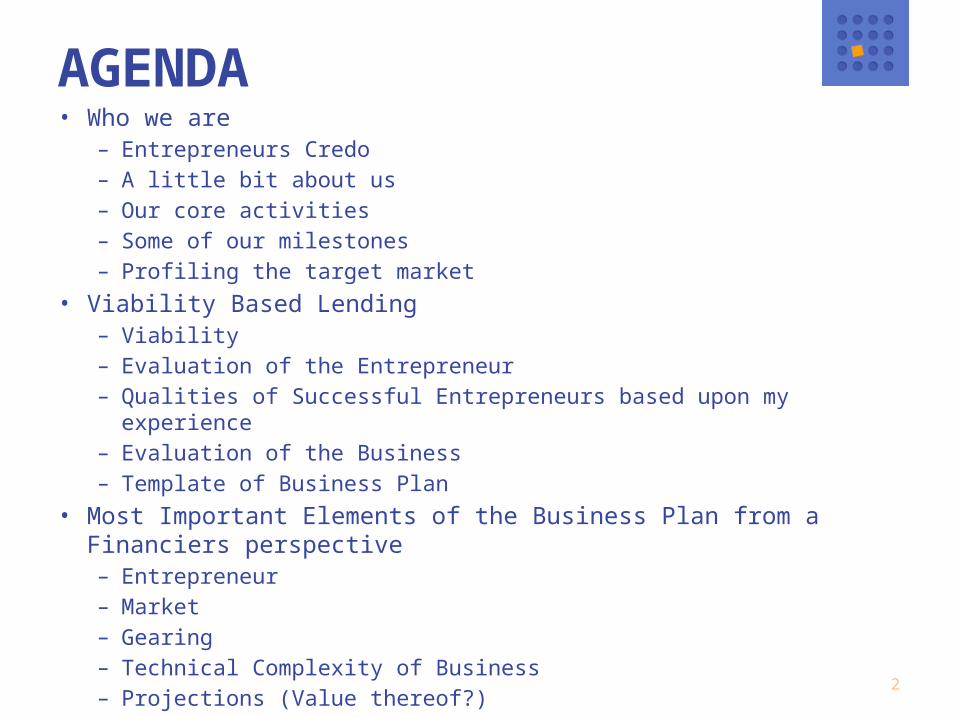

AGENDA • Who we are

– Entrepreneurs Credo– A little bit about us– Our core activities – Some of our milestones– Profiling the target market

• Viability Based Lending– Viability– Evaluation of the Entrepreneur– Qualities of Successful Entrepreneurs based upon my experience– Evaluation of the Business– Template of Business Plan

• Most Important Elements of the Business Plan from a Financiers perspective– Entrepreneur– Market– Gearing– Technical Complexity of Business– Projections (Value thereof?)

3

AGENDA

• Why is it difficult to get funding?– Limited funding available by financiers– Need clear track record– Difficult to prove serviceability of debt– Reluctance to fund SME’s– Security not available or acceptable to financiers

• If you are offered finance, what should you consider?– Flexibility– Risk Spread– Costs– Security Required– Hidden Costs– Economic Climate• Tips

4

01

WHO ARE WE?

ENTREPRENEURS CREDO

I do not choose to be a common man.It is my right to be uncommon … if I can.I seek opportunity … not security.I want to take the calculated risk;To dream and to build.To fail and to succeed.I will never cower before any master,Nor bend to any threat. It is my heritage to standProud and unafraid;To think and act for myself,To enjoy the benefit of my creationsAnd to face the world boldly and say:This, I have done.

I am an entrepreneur.

6

WHO ARE WE?

• We’re a specialist risk finance company that provides customised financial solutions, sector knowledge, mentorship, business premises and other added-value services for formal small and medium enterprises (SMEs) in sub-Saharan Africa.

• We’re passionate about funding, supporting and mentoring entrepreneurs, or as we like to call them, the square pegs in round holes.

7

WHAT IS A SQUARE PEG?

• We affectionately refer to entrepreneurs as square pegs

• They are the exceptional few who see the world not for what it is, but for what it could be.

• Entrepreneurs often challenge conformity • In the world of entrepreneurial finance and support we

too are the square pegs

8

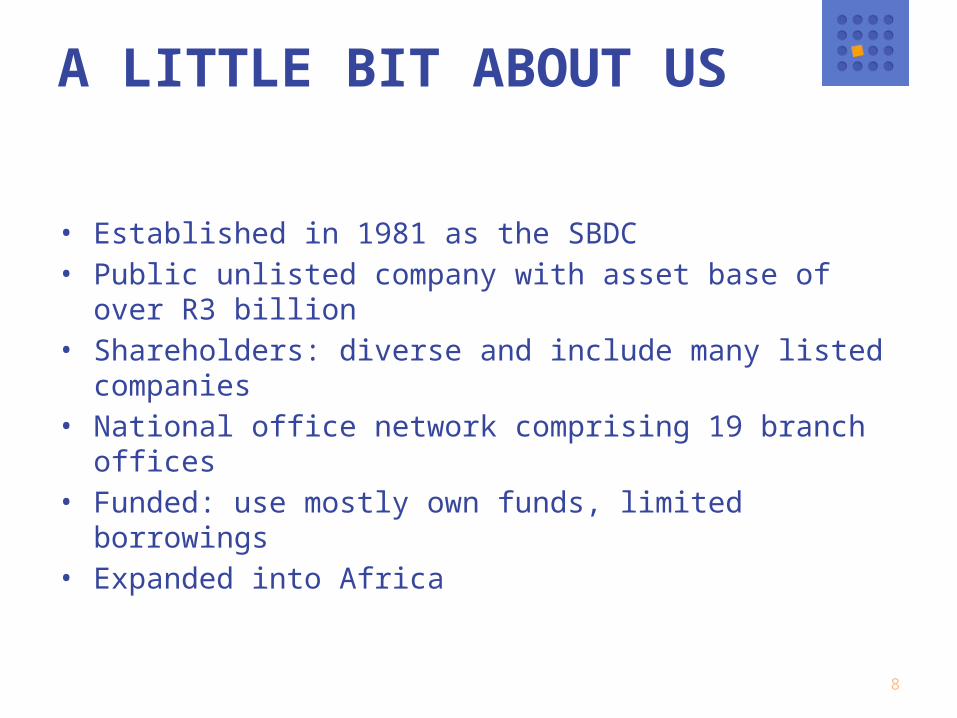

A LITTLE BIT ABOUT US

• Established in 1981 as the SBDC• Public unlisted company with asset base of over R3

billion • Shareholders: diverse and include many listed

companies• National office network comprising 19 branch offices • Funded: use mostly own funds, limited borrowings • Expanded into Africa

9

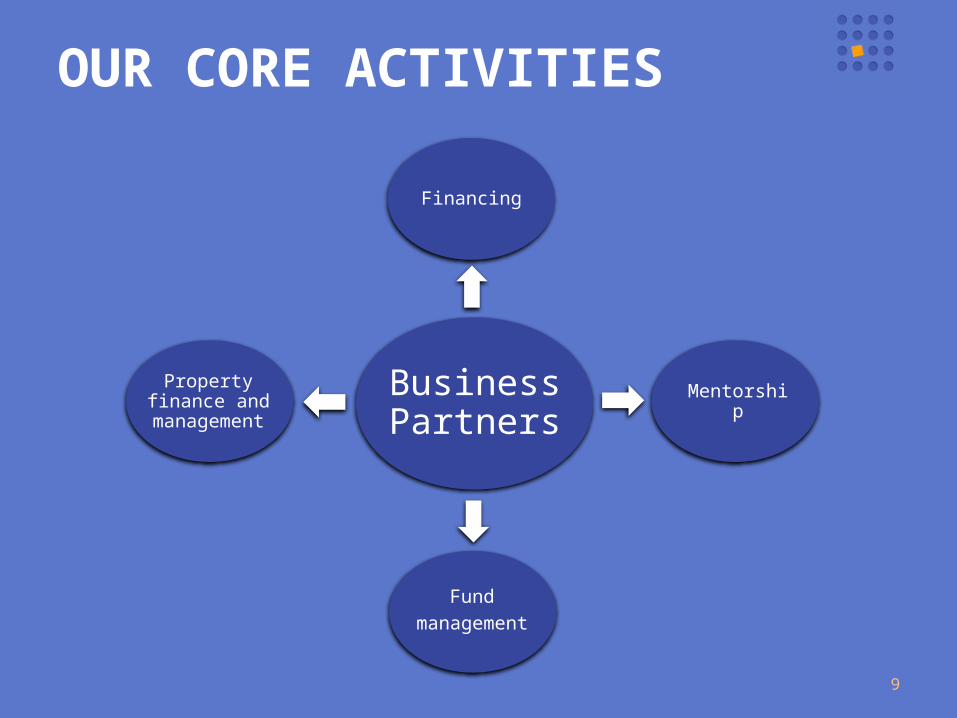

OUR CORE ACTIVITIES

Business Partners

Property finance and

management

Financing

Mentorship

Fundmanagement

10

SOME OF OUR MILESTONES

R14,608 billionFinance invested

578 801Job opportunities

70 028Businesses financed

11

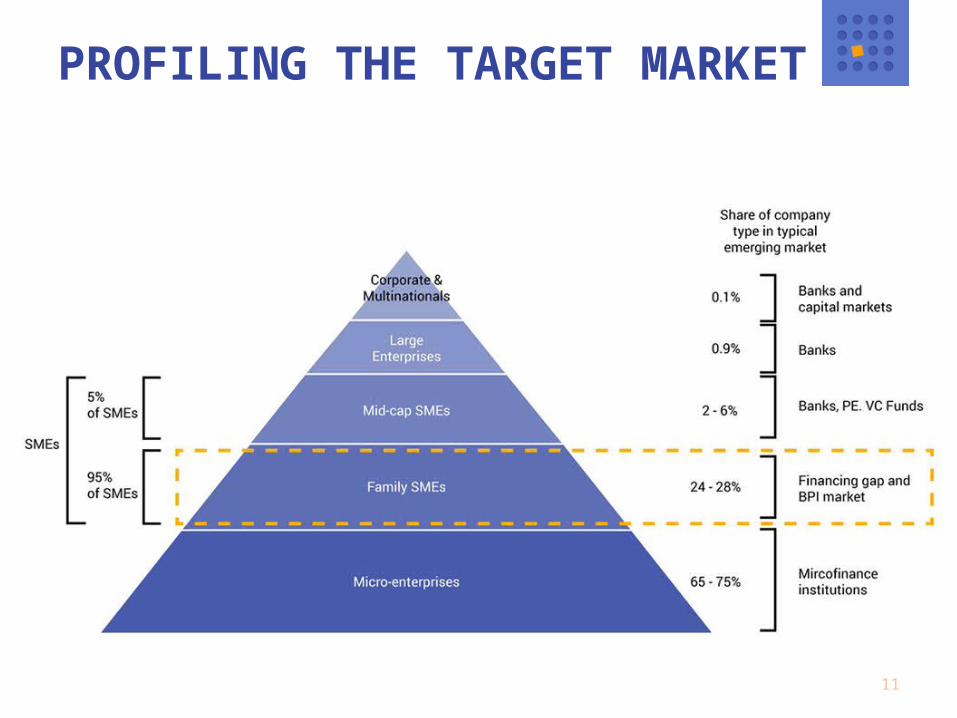

PROFILING THE TARGET MARKET

12

VIABILITY BASED LENDING

02

ENTREPRENEUR

BUSINESS

VIABILITY

IT’S A TWO HORSE RACE

01

14

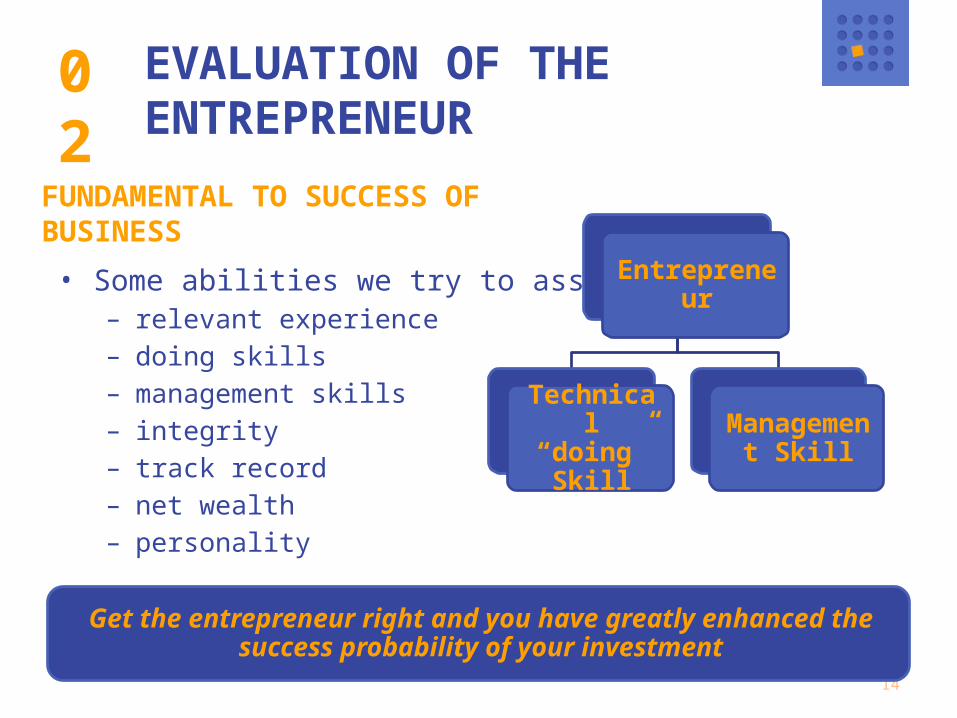

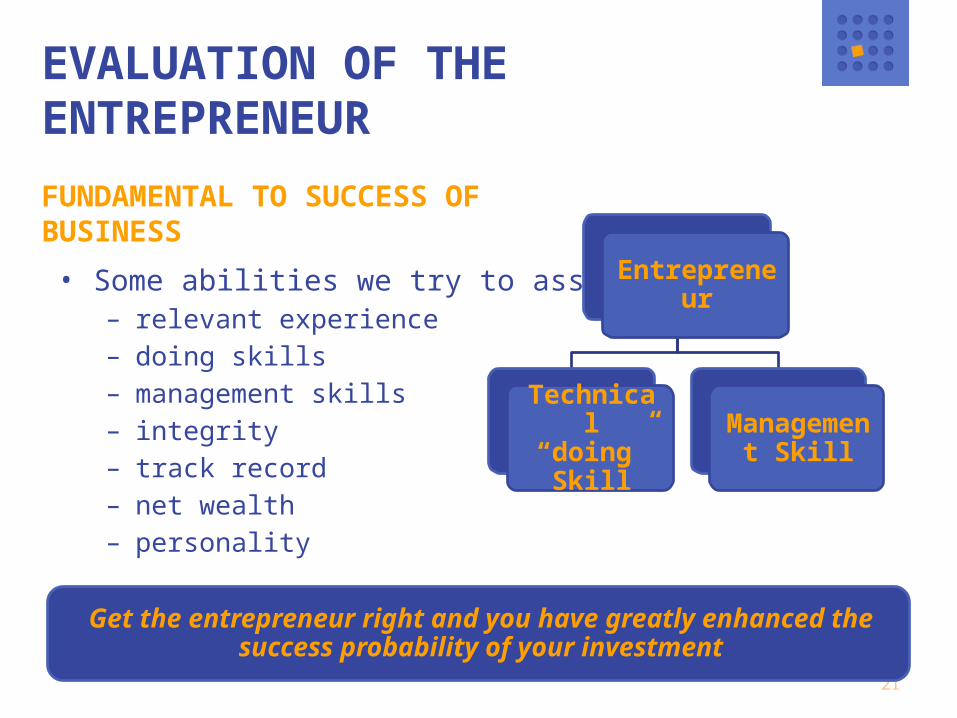

EVALUATION OF THE ENTREPRENEUR

• Some abilities we try to assess:– relevant experience– doing skills – management skills– integrity– track record– net wealth– personality

02

Entrepreneur

Technical “doing” Skill

Management Skill

FUNDAMENTAL TO SUCCESS OF BUSINESS

Get the entrepreneur right and you have greatly enhanced the success probability of your investment

15

QUALITIES OF A SUCCESSFUL ENTREPRENEUR BASED UPON MY EXPERIENCE

• Hard working• Goal orientated• Ambitious• Passionate• Negotiation skills• Get along with people• Prepared to take a risk

03

16

EVALUATION OF THE BUSINESS

• The financier considers the following:– Ability of the business to grow and offer the returns as

per projections– This ability is influence by the Product and Market– Financial Aspects (cash flow, margins, gearing)– Stage (start-up failure rate of 75%)– Industry– Economic Climate

04

17

TEMPLATE OF BUSINESS PLAN

A Summary of the Key Components are:

• A cover or title page• Executive Summary• Business Overview

– Business Profile– The product or service

• Management– the entrepreneurs – The management structure– Franchise information (where applicable)

05

For template, please see: http://www.businesspartners.co.za/

18

TEMPLATE OF BUSINESS PLAN

• The Market• Sales and marketing strategy• Financial statements and projections• Legal and regulatory environment• Swot analysis and risk/reward assessment• Appendices and supporting documentation

05

19

MOST IMPORTANT ELEMENTS OF THE BUSINESS PLAN FROM A FINANCIERS PERSPECTIVE

03

20

ENTREPRENEURS

• Is he capable of delivering on his promises made in an environment where 73% will fail in 3 years?

• No separation of management and ownership.• Normally highly geared, often no reliable financials• Essential Question – Will he deliver on the plan?

01

If the entrepreneur is having a good day, the business is having a good day

21

EVALUATION OF THE ENTREPRENEUR

• Some abilities we try to assess:– relevant experience– doing skills – management skills– integrity– track record– net wealth– personality

Entrepreneur

Technical “doing” Skill

Management Skill

FUNDAMENTAL TO SUCCESS OF BUSINESS

Get the entrepreneur right and you have greatly enhanced the success probability of your investment

22

MARKET

• If there is no market, it does not matter that you have:– Skilled staff– No government red tape– No problems accessing money– Competitive advantage

02

23

GEARING/COMMITMENT

• Optimum amount that the owner should commit, varies from business to business per industry type.– If you are managing your cash flow and you are not

really managing your business

• The central issues in Risk Financing are:– How much do I stand to lose?– What do I stand to make?

03

Who is risking what, for what return?

24

TECHNICAL COMPLEXITY OF BUSINESS

• Does the existing plant and equipment meet capacity requirements?– Packaging plant funded in Western Cape

• Are special skills needed in the production process?– Galvanizing plant

• Technological changes– Print Industry

• New Technology– Photo processing plants– Back up by supplier (China)

• Distribution Channels– Moving bulky low value items (i.e. Charcoal/water/fizzy

drinks)

04

25

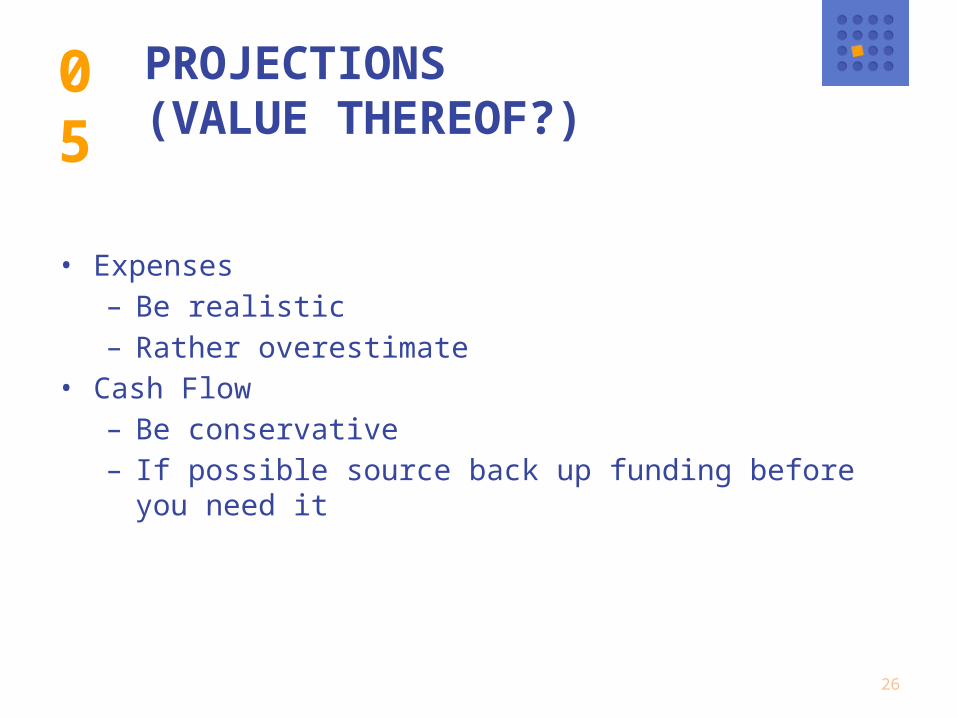

PROJECTIONS (VALUE THEREOF?)

• Motivate all projections in as simple terms as possible.• Do not be unrealistic• Sales motivation (most difficult in a start up)

– Back up with Documented proofLetters of intentMarket research

05

26

PROJECTIONS (VALUE THEREOF?)

• Expenses– Be realistic– Rather overestimate

• Cash Flow– Be conservative– If possible source back up funding before you need

it

05

27

04

WHY IS IT DIFFICULT TO GET FUNDING

28

LIMITED FUNDING AVAILABLE BY FINANCIERS

• Funding is subject to policies of financiers• Policies are not known by entrepreneurs• Financial statements required for existing business• Limited own contribution available which may not

qualify in terms of financiers policies

01

29

NEED CLEAR TRACK RECORD

• If you have judgments, deal with them, take steps to resolve them

• Disclose them and disclose steps to resolve them• Understand that it does weaken your application• Risk funding – more emphasis on integrity

02

30

DIFFICULT TO PROVE SERVICEABILITY OF DEBT

• What do financiers base decision on?- Perceived ability of entrepreneur to achieve the

projections contained in the Business Plan.- Exisiting businesses are evidence of past

performance and are used to predict future success.

- The new Business Plan and entrepreneurs achievements are key to deciding when faced with new ventures.

• Cash Flow and Profitability- Will you and the financier make money?- At worst, will you service the debt?

03

Risk vs. Reward

31

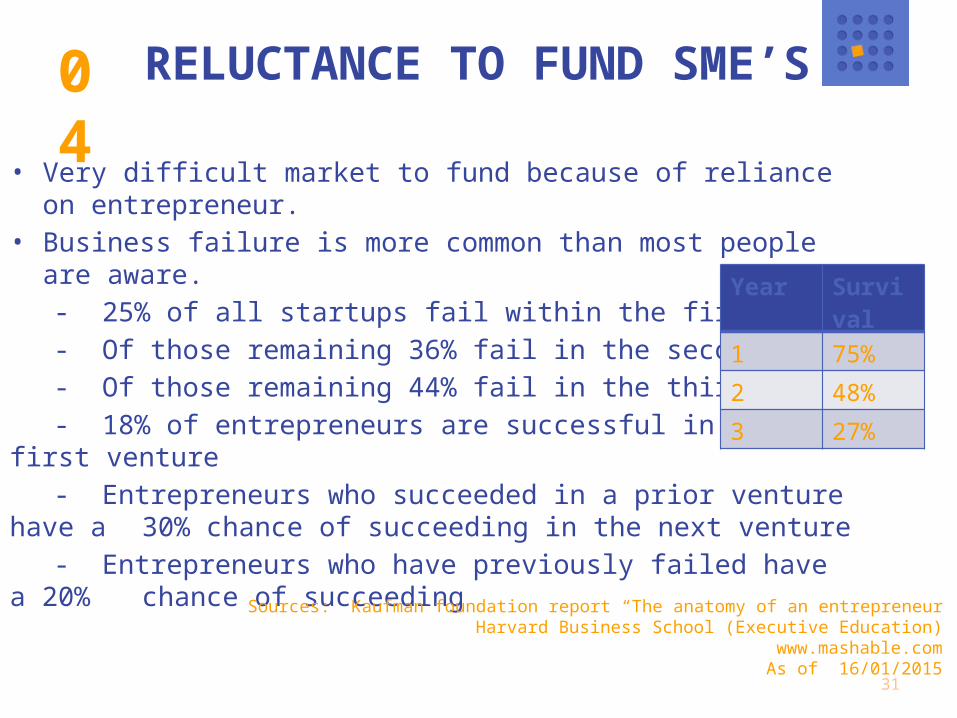

RELUCTANCE TO FUND SME’S

• Very difficult market to fund because of reliance on entrepreneur.

• Business failure is more common than most people are aware.

- 25% of all startups fail within the first year- Of those remaining 36% fail in the second year- Of those remaining 44% fail in the third year- 18% of entrepreneurs are successful in their first

venture- Entrepreneurs who succeeded in a prior venture

have a 30% chance of succeeding in the next venture

- Entrepreneurs who have previously failed have a 20% chance of succeeding

04

Sources: Kaufman foundation report “The anatomy of an entrepreneurHarvard Business School (Executive Education)

www.mashable.comAs of 16/01/2015

Year Survival

1 75%

2 48%

3 27%

32

SECURITY NOT AVAILABLE OR ACCEPTABLE TO FINANCIERS

• Funders mitigate risk by taking security of something that is of value.– Value is not an absolute concept but based upon

personal experience and changes dependent upon conduct)

• Buying – if true value = 1000, then you pay 900• Selling – then you want 1100• Financier is valuing security being sold in a difficult

market• Highly subjective

05

33

HOW THE BANK SEES YOUR PROPERTY

34

HOW THE SELLER SEES HIS PROPERTY

35

WHAT YOUR PROPERTY ACTUALLY LOOKS LIKE

36

IF YOU ARE OFFERED FINANCE, WHAT SHOULD YOU CONSIDER?

05

37

1. Flexibility • Does the finance fit? (Term, structure, rate etc)• What if there are problems downstream?

2. Risk Spread• Equity

- Networks, Advice, Expertise- Hands on or hands in?!

3. Costs which include: • interest rates, term, other costs and opportunity cost

4. Security Required• Inclusive of the costs of registering the security• Personal or business?

5. Hidden Costs• Account consolidation with one financier, add-on products

(eg. insurance), undisclosed admin costs6. Economic climate

38

TIPS

• Go prepared by preparing your own business plan• Believe in yourself and your business• It’s your business – do the negotiations• Be honest and open• Don’t ask for too little money• Put everything in writing even when dealing with

family and friends• Nothing comes easy, and nothing is for free. • EASY MONEY has a catch SOMEWHERE.• If not successful. Ask why. Listen and learn.

Don’t give up.

39

QUESTIONS?

40

NAME OF PERSON PRESENTING

• Sphamandla Ngema• Work number : (031) 240 7700• Email : [email protected]

41

THANK YOU