A path to recovery - UniCredit

69

1Q Error! Unknown document property 2021 CEE Quarterly Macro Research Strategy Research Credit Research A path to recovery

Transcript of A path to recovery - UniCredit

1Q

Error! Unknown document property name.

2021

CEE

Quarterly

Macro Research

Strategy Research

Credit Research

A path to recovery

January 2021

UniCredit Research page 2 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

“Your Leading Banking Partner in

Central and Eastern Europe

”

January 2021

UniCredit Research page 3 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

Contents

4 A path to recovery

14 CEE strategy: Solid risk appetite and yield in demand

65 Acronyms and abbreviations used in the CEE Quarterly

COUNTRIES

21 Bulgaria: Difficult start to recovery but strong medium-term outlook

25 Croatia: Rough journey to the light at the end of the tunnel

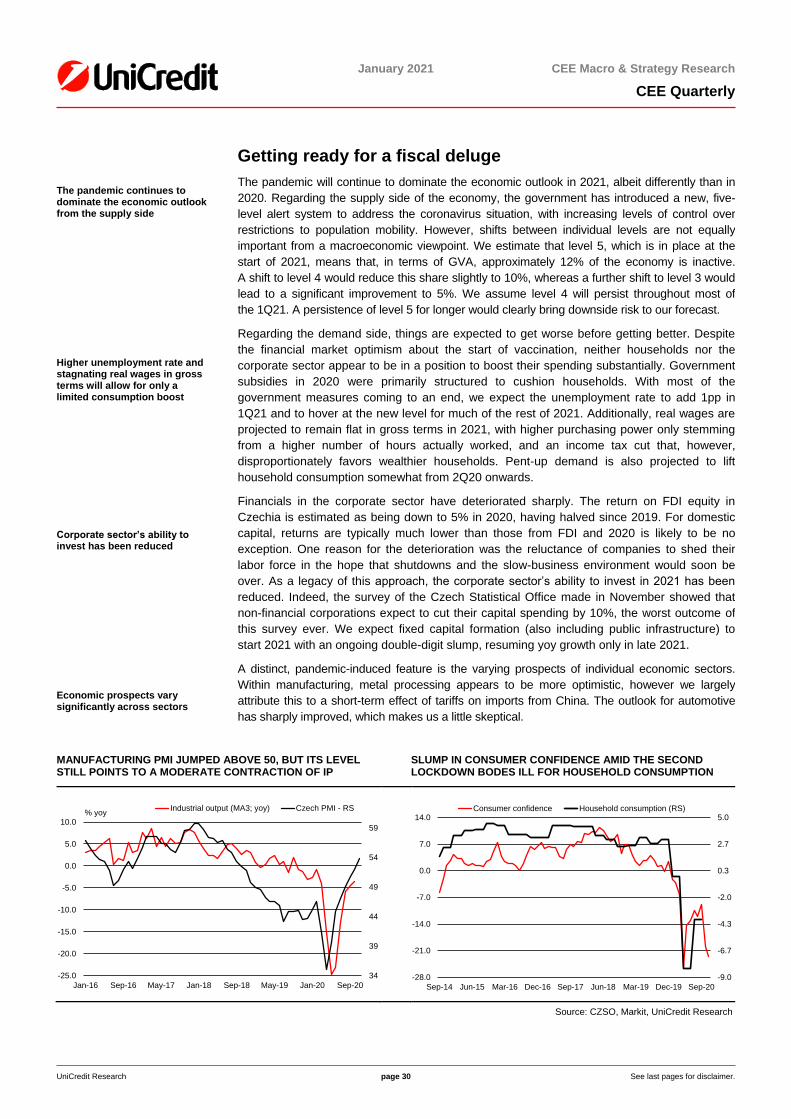

29 Czechia: Getting ready for a fiscal deluge

33 Hungary: Reassessing growth drivers

37 Poland: A swift recovery after the crisis

41 Romania: Looking for normality

45 Slovakia: More-resilient manufacturing to mitigate COVID-19 recession

47 Slovenia: Recovery amid COVID-19 uncertainty

EU CANDITATES AND OTHER COUNTRIES

49 Bosnia and Herzegovina: Smaller contraction in 2020 but slower recovery in 2021

51 North Macedonia: Slow recovery amid pandemic risk

53 Russia: Gradual recovery from shallow recession

57 Serbia: Recovery amid high uncertainty and risks

61 Turkey: A better policy mix

Published on 13 January 2021

Erik F. Nielsen Group Chief Economist (UniCredit Bank, London) 120 London Wall UK-London EC2Y 5ET

Imprint: UniCredit Bank AG UniCredit Research Am Eisbach 4 D-80538 Munich

Supplier identification: www.unicreditresearch.eu

Erik F. Nielsen, Group Chief Economist (UniCredit Bank, London) +44 207 826-1765, [email protected]

Dan Bucşa, Chief CEE Economist (UniCredit Bank, London) +44 207 826-7954, [email protected]

Artem Arkhipov, Head of Macroeconomic Analysis and Research Russia (UniCredit Russia) +7 495 258-7258 ext. -7558, [email protected]

Gökçe Çelik, Senior CEE Economist (UniCredit Bank, London) + 44 207 826-6077, [email protected]

Ariel Chernyy, Economist, Macroeconomic Analysis and Research Russia (UniCredit Russia) +7 495 258-7258 ext. 7562; [email protected]

Hrvoje Dolenec, Chief Economist (Zagrebačka banka) +385 1 6006-678, [email protected]

Dr. Ágnes Halász, Chief Economist, Head of Economics and Strategic Analysis Hungary (UniCredit Hungary) +36 1 301-1907, [email protected]

Ľubomír Koršňák, Chief Economist (UniCredit Bank Czech Republic and Slovakia) +42 12 4950-2427, [email protected]

Elia Lattuga, Co-Head of Strategy Research, Cross Asset Strategist (UniCredit Bank, London) +44 207 826-1642, [email protected]

Mauro Giorgio Marrano, Senior CEE Economist (UniCredit Bank, Vienna) +43 50505-82712, [email protected]

Anca Maria Negrescu, Senior Economist Romania (UniCredit Bank Romania) +40 21 200-1377, [email protected]

Kristofor Pavlov, Chief Economist (UniCredit Bulbank) +359 2 923-2192, [email protected]

Pavel Sobíšek, Chief Economist (UniCredit Bank Czech Republic and Slovakia) +420 955 960-716, [email protected]

January 2021

UniCredit Research page 4 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

A path to recovery

Dan Bucsa Chief CEE Economist (UniCredit Bank, London) +44 207 826-7954 [email protected]

■ We expect economies in EU-CEE1 and in the western Balkans, to grow by around 3.3% in 2021

after slumping by close to 5% in 2020. A weak start to 2021, lower fiscal support, looser labor-

market conditions, delayed investment and external risks could result in an incomplete recovery.

■ GDP in EU-CEE and the western Balkans could return to pre-COVID-19 levels in 2022,

when growth could accelerate to more than 4%. Interest rates could be increased in

Czechia at the end of 2021 and in Poland and Romania in 2022.

■ EU support in the form of the European instrument for temporary Support to mitigate

Unemployment Risks in an Emergency (SURE), Next Generation EU (NGEU) and the

2021-27 EU budget could support the recovery in EU-CEE in 2022 and beyond.

■ IN EU-CEE, only the NBR is expected to cut rates in 2021. The CNB could be the first

central bank to increase rates in 2H21, followed by the NBP and the NBR in 2H22. Central

banks could purchase more bonds if state funding needs rise above current plans.

■ In Turkey, economic growth could accelerate from around 1.2% in 2020, to 2.9% in 2021 and

4% in 2022. Without structural reforms, most of the monetary tightening implemented in 2020

could be reversed in 2021 to spur lending and growth. This strategy is not sustainable, and

may only serve to put pressure back on the current account, the currency and rates.

■ After declining by almost 4% in 2020, the Russian economy could grow by 2.2-2.3% in

2021 and 2022. The central bank could keep the policy rate at 4.25% in 2021-22 if inflation

remains below the 4% target.

■ The COVID-19 pandemic will continue to affect CEE countries in 2021, with herd immunity

reached this year only if vaccination accelerates significantly. However, restrictions and

their negative economic impact could be much milder next winter than they are currently.

■ In 2021, government anti-pandemic support will decline compared to 2020 in all CEE

countries but Bulgaria. Indirect support could be less efficient than last year, unless

governments focus on grants, rather than loans to SMEs. Labor-market support may be

needed to avoid a large second wave of layoffs. Support could be withdrawn starting in 2H21.

■ Political noise will be a risk in Bulgaria and Czechia, where parliamentary elections will be

held in 2021.

■ Democracy in CEE would benefit if the US administration returns to multilateralism.

■ In the next two years, EU fund disbursements are unlikely to be tied to observing the rule of law.

2020 recession…

In 2020, GDP fell in all CEE countries but Turkey, where the economy grew by around 1.2%,

around 3pp below potential. In the rest of the region, the contraction probably ranged between

1.1% in Serbia to almost 4% in Russia and around 5% in EU-CEE and the western Balkans

(Chart 1). The health crisis caused by the COVID-19 pandemic led to a deeper slump in 2Q20

than that which occurred during the global financial crisis. Economies that are more reliant on

domestic demand and that benefitted from timely government support were more resilient than

the small, open economies in central Europe. The recovery in 3Q20 was proportional to the

2Q20 slump but incomplete. In 4Q20, GDP probably fell again in most CEE countries due to

lockdowns imposed in response to the second wave of the COVID-19 pandemic, both

domestically and by the CEE’s largest European economic partners. Yet, the tightness of

restrictions and compliance with rules varied widely across countries. Thus, Croatia, Czechia,

Slovenia, Slovakia, Hungary and Poland probably suffered more than Romania, Russia and

Serbia. Turkey’s sharp credit adjustment, made as the country attempts to tackle yet another

balance-of-payments crisis, might have led to a GDP slump in 4Q20, despite anti-pandemic

restrictions having not been tightened as much as in central Europe.

1EU-CEE refers to CEE countries that are members of the EU: Bulgaria, Croatia, Czechia, Hungary, Poland, Romania, Slovakia and Slovenia.

January 2021

UniCredit Research page 5 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

…followed by an incomplete recovery in 2021

The 2021 recovery is likely to be incomplete in all CEE countries but Poland, Serbia and

Turkey. In Poland, quick and targeted support prevented a deeper slump in 2020. Serbia will

continue to benefit from large public spending and Turkey from its region-topping potential

growth. That said, all three countries could end 2021 with negative or zero output gaps. At the

other extreme, the Croatian economy is unlikely to return to its pre-pandemic level of activity

before 2023, as the tourism sector could take longer to recover. In 2021, EU-CEE could grow

by around 3.3%, in line with the western Balkans, with both the Russian and the Turkish

economies recovering by close to 2.5% (Chart 2). We see five main reasons why a full

recovery from the 2020 slump will be postponed to 2022 or later in most CEE countries:

1. A weak start to 2021: After small or negative carryover into 2021, economic activity could

remain subdued in 1Q21 if restrictions are maintained throughout the winter. Countries

whose governments reacted indecisively in 4Q20 (Bulgaria, Romania, Russia and Serbia)

could eventually tighten restrictions in 1Q21, leading to a GDP drop during the winter.

2. Lower fiscal and monetary support than in 2020: We expect budget deficits to decline

in all CEE countries but Bulgaria, where anti-crisis support might increase in 2021

compared to last year. Budget shortfalls could narrow less than in official forecasts, even

after governments revised them at the end of 2020. In our opinion, most CEE authorities

are underestimating economic risks from the current pandemic wave. Some of the most

successful support schemes introduced in 2020 might be extended, such as those

backing furlough and part-time work, as well as loan repayment moratoriums. Deferred

taxes could be collected only partially and with a delay. Government guarantees will

remain available for corporate borrowers.

3. Weaker labor-market conditions and their negative impact on consumer spending:

Lengthy restrictions are likely to continue to affect employment, especially in leisure

services and manufacturing. In addition, wage bargaining will mostly occur in 1Q21, when

restrictions and weak foreign demand could lead to much lower wage growth than in

previous years. The first official announcements from car companies in EU-CEE suggest

that wages and bonuses will rise in single digits in 2021 and 2022, compared to 15-25%

annual growth rates in past years. Car manufacturing is a bellwether for at least half of

manufacturing wages in EU-CEE. There has already been a marked reduction in

household plans to make large purchases. We expect a recovery in household investment

in 2H21, at the earliest.

4. Postponed corporate investment: Companies may postpone investment as well, despite

sizeable credit and tax support from governments. While large companies could explore

opportunities to expand their market share or increase productivity, SMEs are less capable

of spending. They started the COVID-19 crisis in a significantly weaker position than their

eurozone counterparts, and preferential loans granted in 2020 increased their leverage to a

point where additional borrowing would be difficult to sustain. Several CEE governments

will hand out grants to SMEs, partly co-financed with EU money, to help them weather a

protracted reduction in demand. However, many SMEs may use grants to repay some of

their debt before venturing into new investment. Besides productive investment,

construction is also likely to suffer from a lack of orders at least until mid-2021. The most

affected will be housing and offices.

5. External demand outlook unclear: The outlook for external demand remains uncertain,

especially when it comes to car exports, tourism and Brexit. The high import content of

exports and muted domestic demand could offset a weak contribution from exports to

GDP in 1H21. Starting in 2H21, exports could rise throughout CEE if growth rebounds in

the eurozone and globally.

January 2021

UniCredit Research page 6 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

CHART 1: RECESSION IN ALL CEE COUNTRIES BUT TURKEY IN 2020…

CHART 2: …FOLLOWED BY INCOMPLETE RECOVERY IN 2021

Source: Eurostat, national statistical offices, UniCredit Research

Financial support from the EU is expected to fuel recovery in EU-CEE… …and accelerate growth to above 4% in 2022

The bright spot in the EU-CEE economic outlook for 2021 is EU support in the form of several

programs disbursing loans and grants (Chart 3). The first of these loan disbursements has

already arrived from SURE2, with funding already approved for all EU-CEE countries.

Together with NGEU loans, they are expected to replace at least 25% of external issuance in

2021, with grants starting to arrive towards the end of 2021. Together with late disbursements

from the EU’s 2014-20 multiannual financial framework (MFF), these transfers and loans

should smooth the transition to disbursements from the 2021-27 EU budget by ensuring that

public investment does not plummet in 2021-22. We expect EU funding to add 0.1-0.7pp to

GDP growth in 2021, with its smallest contribution in Czechia and its largest in the Balkans3.

Disbursements from NGEU and the MFF will rise gradually in the coming years. This should

set the stage for a further recovery in 2022, when GDP growth could exceed 4% (Chart 4). If

the negative effects of the pandemic are contained, the private sector could increase

spending, while exports may recover as the eurozone and global economies rebound as well.

This would allow labor-market conditions to tighten again, eliminating most scarring effects by

the end of 2022.

CHART 3: LARGE TRANSFERS FROM THE EU… CHART 4: …WILL BOOST THE RECOVERY IN 2022 AND BEYOND

Source: national statistical offices, European Commission, UniCredit Research

2The European instrument for temporary Support to mitigate Unemployment Risks in an Emergency

3We are less optimistic than the European Commission in our assessment of the potential impact of EU funding on growth in 2021.

-15.0 -10.0 -5.0 0.0 5.0 10.0

Czechia

Russia

Turkey

Slovakia

Bulgaria

Slovenia

Poland

Romania

Hungary

Serbia

Croatia

Private consumption Public consumption Fixed investment

Net exports Inventories, error GDP

yoy (%),pp

-4.0 -2.0 0.0 2.0 4.0 6.0

Czechia

Russia

Turkey

Slovakia

Bulgaria

Slovenia

Poland

Romania

Hungary

Serbia

Croatia

Private consumption Public consumption Fixed investment

Net exports Inventories, error GDP

yoy (%),pp

0.0 10.0 20.0 30.0 40.0 50.0

Czechia

Poland

Slovenia

Romania

Slovakia

Hungary

Bulgaria

Croatia

SURE NGEU loans

NGEU grants EU budget 2021-27

% of avg. GDP for 2021-27

-4.0 -2.0 0.0 2.0 4.0 6.0 8.0

Czechia

Russia

Turkey

Slovakia

Bulgaria

Slovenia

Poland

Romania

Hungary

Serbia

Croatia

Private consumption Public consumption Fixed investment

Net exports Inventories, error GDP

yoy (%),pp

January 2021

UniCredit Research page 7 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

The negative impact of COVID-19 could last throughout 2021

The second wave of the pandemic could require tighter restrictions in 1Q21

We expect the COVID-19 pandemic to further affect CEE economies in 2021. While

vaccination has started in EU-CEE and Russia (Chart 5) and is picking up, countries need to

accelerate immunization. At the current pace, no CEE country will come close to vaccinating

70% of its population in 2021. Significantly more efforts would be needed in Poland and

Romania, and especially in Bulgaria, Czechia and Russia to make sure that a large-enough

percent of the population receives the vaccine before the end of 2022.

Even if herd immunity is reached earlier due to rising infections, it is likely that the epidemic

will continue to affect lives and economic activity throughout 2021. The best hope for CEE

countries is that restrictions are significantly milder next winter compared to the current one.

Until then, CEE countries face several problems in the second wave of the pandemic4, such

as poor official communication, the lack of test-trace-isolate frameworks, low compliance with

restrictions, high usage of intensive care units and a shortage of health care workers5. In

addition, most CEE countries continue to test insufficiently and, as a result, the official

assessment of the viral spread is inadequate. Daily case estimates from Imperial College

London (ICL) are 2-8 times higher than officially communicated daily cases. The ICL

estimates correlate strongly with the number of deaths (Chart 6) and are a better predictor of

fatalities than officially published infection numbers.

While most CEE governments plan to remove restrictions in February, new viral strains could

delay the exit from lockdowns and even require tighter restrictions before the spring. These, in

turn, would further weigh on economic growth, employment and wage growth.

CHART 5: UNEVEN START FOR ANTI-COVID VACCINATION CHART 6: ICL ESTIMATES CORRELATE WITH COVID DEATHS

Source: CEE governments, Oxford University, Imperial College London, UniCredit Research

Governments are expected to maintain some anti-crisis support in 2021 Timeliness of disbursements could improve further

The risk of further restrictions and economic disruption require CEE governments to maintain

some support measures in 2021. While the size will not match what was spent in 2020

(Tables 1 and 2), the implementation of last year’s fiscal and financial packages carry

valuable lessons for authorities.

The most important lesson is that timeliness may be more important than size. Poland is the

most relevant example. The government’s decision to dole out most financial support through

the state-owned sovereign investment fund (PFR) and development bank (BGK) helped the

Polish economy weather the downturn better than its central European peers. At the other

extreme, Czechia pledged the largest indirect support package in the region, but managed to

implement only 7% of it. The good news is that most CEE countries have improved the

channeling of funding to the private sector, be it directly or via the banking sector, and

disbursements could become more efficient still in 2021.

4 While some prefer to call it the third wave, we believe that the second wave never ended in CEE and the decline in the number of cases was mostly due to fewer

tests conducted before Christmas and during the winter holidays. The exception is Czechia, where a tight lockdown reduced the number of infections in 4Q20. However, the number of cases rose rapidly once restrictions were eased. 5 For details, please see the EEMEA Country Note – Long COVID risk in CEE from policy inaction, 10 December.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

BG HR CZ HU PL RO RU RS SK SI TR

Latest

World average

SARS-CoV-2 vaccination rates (vaccines per 100 inhabitants)

BG

HRCZ

HU

PL

RO

RU

RS

SK

SI

TR0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

0.0 0.5 1.0 1.5 2.0 2.5 3.0

De

ath

s p

er

mill

ion

in

ha

bita

nts

Baseline ICL estimate for daily infections per thousand inhabitants

data as of 25 December 2020 (ICL) and 5 January 2021 (deaths)

January 2021

UniCredit Research page 8 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

Labor-market support is needed throughout the second pandemic wave SMEs better targeted with grants than loans 2021 support packages are too heavy on new lending Direct support could increase if the second wave has significant economic costs

The second lesson is that labor-market support may have the farthest reaching effects of all

support measures. Prompt support for furlough and part time work blunted the rise in

unemployment, but could not prevent employment from falling in 3Q20 even in sectors such

as industry that rebounded strongly. Yet both employment and consumer expectations fell

much less than during the global financial crisis, probably helped by public safety nets.

Maintaining labor-market support in 2021 could be paramount for the recovery, especially if a

protracted second wave of the pandemic leads to another round of layoffs this winter.

The third lesson is that SMEs have limited room to further increase leverage. The take-up of

subsidized and/or guaranteed loans slowed towards the end of 2020 in most CEE countries.

For small companies saddled with debt and facing an uncertain future, grants may be a better

option than more loans. EU funding from NGEU and SURE could supplement national

resources in supporting hard-hit sectors (especially services) but also companies in sectors

prioritized by the European Commission, such as IT, environment and energy transition.

Taking these lessons into account, 2021 pandemic support packages seem too heavy on

lending incentives and guarantees. This is especially true in Hungary, where SMEs were

more leveraged than their regional peers even before the pandemic started. More subsidized

lending may achieve little in reducing corporate borrowing costs or spurring growth. The other

EU-CEE countries could use a mix of loans and grants, with Poland and Romania probably

favoring the latter. Russia and Turkey pledged the least indirect support in CEE. The CBR is

already subsidizing funding for banks and appetite for borrowing is very healthy in an

economy that missed out on the CEE credit boom of the mid-2010s. On the other hand, the

CBR is looking to slow credit growth, fearing that current growth rates could threaten financial

stability. The CBRT has also moved to cool down the credit boom it fueled in 2020. The

adjustment will continue at least in 1H21, leading to a negative credit impulse.

With the exception of Bulgaria, direct support will be smaller than in 2020, in some cases

significantly so. In a repeat of 2020, many governments probably underestimate the negative

impact the pandemic will have on their economies. Others plan to reduce their budget deficits

and cap public debt before sovereign ratings are threatened. Either way, we expect all EU

countries to ramp up direct support in case of need, with the funding coming partly from the

EU (in EU-CEE and the western Balkans), government reserves (in Russia) and central bank

purchases (in Turkey). If economies start to recover in 2Q21, we expect government support

to be withdrawn in the second half of the year.

TABLE 1: OFFICIAL PANDEMIC SUPPORT IN 2020 TABLE 2: PANDEMIC SUPPORT PLEDGED FOR 2021

(% of GDP) Direct s upport

Indirect support

Total support

Bulgaria 3.2 0.2 3.4

Croatia 5.1 2.4 7.5

Czechia 3.9 1.2 5.1

Hungary 4.4 1.0 5.4

Poland 2.4 4.8 7.2

Romania 1.8 3.7 5.5

Russia 2.0 1.0 3.0

Slovakia 1.8 0.7 2.5

Slovenia 4.6 0.4 5.1

Serbia 7.5 3.2 10.7

N. Macedonia

Turkey 4.9 5.5 10.4

(% of GDP) Direct

support Indirect support

Total support

Bulgaria 4.0 2.0 6.0

Croatia 1.1 2.3 3.4

Czechia 2.0 0.0 2.0

Hungary 0.1 3.7 3.7

Poland 1.0 1.4 2.4

Romania 1.5 1.6 3.1

Russia 0.7 0.2 0.9

Slovakia 1.1 1.0 2.1

Slovenia 3.0 1.8 4.8

Serbia 0.0 0.5 0.5

N. Macedonia 0.1 0.9 1.0

Turkey 0.4 0.1 0.5

Source: CEE governments, UniCredit Research

January 2021

UniCredit Research page 9 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

Inflation is expected to be inside target ranges in 2021-22

Rate hikes are possible in Czechia in 2H21 and in Poland, Romania and Russia in 2H22 Turkey is likely to reverse monetary tightening in 2021

In 2021, low imported inflation, little scope for currency depreciation and weak domestic demand

could keep inflation safely inside target ranges in EU-CEE, Russia and Serbia

(Chart 7). Inflation is expected to rebound in 2022, without leaving target ranges in any of the

aforementioned countries. In EU-CEE, only the National Bank of Romania is expected to deliver

limited rate cuts from here on, while the Czech National Bank is contemplating rate hikes in

2021 if fiscal spending fuels inflationary pressure. By 2H22, the Polish, Romanian and Russian

central banks might consider increasing interest rates without giving up on negative real interest

rates. However, the CBR could leave the policy rate at 4.25% for longer if inflation remains

below the 4% target and economic growth does not accelerate above potential.

Turkey’s permanent target miss could extend to the coming years. We expect the CBRT to

reverse most of its rate hikes from 2020 in the second half of 2021, once disinflation resumes. In

the absence of structural reforms, the authorities may revert to the credit-driven growth model

that has led to several balance-of-payments crises – combined with TRY depreciation and sharp

swings in GDP dynamics – in the past decade. Such growth spurts are shorter, and the effect of

credit booms increasingly smaller, due to high leverage in the private sector. As a result, the

Turkish economy could grow below potential in 2021-22, which would revive the specter of

higher unemployment and populist spending ahead of 2023 parliamentary elections.

CHART 7: INFLATION INSIDE TARGET RANGES IN ALL COUNTRIES BUT TURKEY

CHART 8: 2020 BOND PURCHASES GIVE AN INDICATION OF THE SCOPE FOR CENTRAL BANK PURCHASES IN 2021

*CNB stands for the Croatian National Bank. Source: statistical offices, central banks, ministries of finance, UniCredit Research

CEE central banks could purchase more bonds in 2021

Some CEE central banks could continue bond purchases in 2021 due to high budget deficits.

We believe that purchases in 2020 (Chart 8) are a good indicator of how active central banks

may be in 2021. Besides the NBH, which still has around HUF 1.1tn in bonds to buy before

reaching its self-imposed limit, the Croatian and Serbian central banks are the likeliest to buy

bonds, followed by the NBP. However, actual purchases could be smaller than they were in

2020 as budget deficits decline. They could also target the longer end of the yield curve more

than they did in 2020, which is what the NBH is doing.

Elections could trigger fiscal populism in Bulgaria and Czechia The return of multilateralism is good news for democracy in CEE

Elections will add to noise in other CEE countries, with Bulgaria and Czechia holding

parliamentary elections in 2021. While populist fiscal spending may rise ahead of these polls,

both countries start from a very strong fiscal position. Strong institutions in Czechia and the

process of euro adoption in Bulgaria could deter legislation that would affect the rule of law.

The election of Democratic candidate and former Vice President Joe Biden as the next US

president could lead to more-targeted US involvement in the region if Mr. Biden follows in

Barack Obama’s footsteps. That said, we do not expect crippling sanctions to be placed on

Russia, while Turkish authorities could try to appease concerns in Washington to avoid conflict

with the incoming US administration.

-2

0

2

4

6

8

10

12

14

SI SK PL HR RS CZ BG BH RO RU HU TR

2020E 2021F 2022F Inflation targetannual inflation (eop, %)

0

1

2

3

4

5

6

CNB* NBP NBH NBS CBRT NBR

Other bonds

Government bonds

bond purchases since the start of the crisis, % of GDP

January 2021

UniCredit Research page 10 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

For EU-CEE, a return to multilateralism may strengthen democratic values while dampening the

prospects of those politicians who have tried to escape the process of further European

integration. None of the small, open economies in EU-CEE can afford to leave the EU, a reality

that could be made all the more clear by the effects of Brexit.

EU fund disbursements may not be tied to the rule of law in the next couple of years

The deal struck by EU governments to adopt the NGEU and the 2021-27 EU budget gave some

respite to Hungarian and Polish governments in their attempt to avoid linking EU fund

disbursements to observing the rule of law. However, this respite might be temporary and will

depend on how quickly European authorities define the rule of law and the European Court of

Justice (ECJ) rules whether the link between financial transfers and rule-of-law conditionality is

in agreement with European treaties. It might be much easier to back such conditionality for

NGEU than for the EU budget. Thus, the ruling could depend on whether the ECJ decides to

treat the two financing frameworks together. Thus, Hungary and Poland may have bought

themselves up to two years and a resolution could be issued close to the Hungarian

parliamentary elections expected in spring 2022.

In the medium term, additional reforms to take decisions in the European Council by a qualified

majority, rather than unanimously, and for European authorities to have a bigger say in national

legislative processes may be unavoidable if the EU does not choose the path of multi-speed

European integration.

January 2021

UniCredit Research page 11 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

OUR GLOBAL FORECAST

GDP growth, % CPI (Avg), % Policy interest rate** 10Y bond yield (EoP),% Exchange rate (LC vs. US)

2020E 2021F 2022F 2020E 2021F 2022F 2020 2021F 2022F 2020 2021F 2022F 2020 2021F 2022F

Eurozone -7.4 3.0 4.5 0.3 0.7 1.6 -0.50 -0.50 -0.50 -0.26 0.00 0.20 1.22 1.28 1.32

Germany -4.8* 3.3* 4.2* 0.4 0.9 1.7 -0.57 -0.30 -0.10

France -9.5 3.2 5.1 0.5 0.5 1.5

Italy -9.2 2.8 4.4 -0.1 0.1 0.8 0.55 0.85 1.40

UK -11.2 4.3 6.3 0.9 1.4 1.9 0.10 0.10 0.10 1.37 1.36 1.40

USA -3.8 1.8 3.5 1.2 1.9 2.1 0.25 0.25 0.25 0.91 1.30 1.75

Oil price, USD/bbl 43 41 50

*Non-wda figures. Adjusted for working days: -5.2% (2020), 3.3% (2021) and 4.2% (2022); **Deposit rate for ECB Source: UniCredit Research

THE OUTLOOK AT A GLANCE

Real GDP (% change) 2019 2020E 2021F 2022F

CPI (EoP) (% change) 2019 2020E 2021F 2022F

C/A balance (% GDP) 2019 2020E 2021F 2022F

EU-CEE 3.8 -4.9 3.3 4.1

EU-CEE 3.4 2.1 2.3 2.9

EU-CEE -0.4 1.1 0.6 0.4

Bulgaria 3.7 -5.5 2.7 4.5

Bulgaria 3.8 0.7 2.5 2.6

Bulgaria 3.0 2.7 3.2 3.4

Czechia 2.2 -6.4 2.0 4.9

Czechia 3.2 2.3 2.3 2.7

Czechia -0.3 3.6 2.7 1.2

Hungary 4.6 -5.6 4.1 4.3

Hungary 4.0 2.6 3.6 3.7

Hungary -0.2 0.0 -0.1 1.1

Poland 4.6 -3.0 3.5 3.1

Poland 3.4 2.3 1.9 3.2

Poland 0.5 3.0 1.5 1.4

Romania 4.2 -5.5 3.7 5.0

Romania 4.0 2.2 2.9 2.6

Romania -4.7 -4.9 -4.7 -4.8

Croatia 2.9 -9.1 4.6 4.8

Croatia 1.4 0.3 2.0 2.0

Croatia 2.7 -2.9 0.7 0.5

Russia 2.0 -3.9 2.3 2.2

Russia 3.0 4.9 3.5 3.5

Russia 3.9 2.5 1.0 1.8

Serbia 4.2 -1.1 4.2 4.2

Serbia 1.8 1.3 2.1 2.4

Serbia -6.9 -5.7 -5.5 -5.5

Turkey 0.9 1.2 2.9 4.0

Turkey 11.8 14.6 10.8 11.5

Turkey 0.9 -5.3 -3.0 -2.8

Extended basic balance (% GDP) 2019 2020E 2021F 2022F

External debt (% GDP) 2019 2020E 2021F 2022F

General gov’t balance (% GDP) 2019 2020E 2021F 2022F

EU-CEE 2.5 4.1 3.7 3.7

EU-CEE 66.6 72.5 69.4 66.4

EU-CEE -1.1 -7.4 -5.9 -3.9

Bulgaria 5.5 6.3 7.3 8.7

Bulgaria 58.0 66.1 65.2 63.2

Bulgaria 2.1 -3.7 -5.6 -2.8

Czechia 1.3 4.5 4.2 2.8

Czechia 76.2 82.4 80.7 81.4

Czechia 0.3 -7.0 -7.8 -6.0

Hungary 1.3 3.8 4.4 3.6

Hungary 91.0 111.5 104.5 97.6

Hungary -2.0 -9.2 -6.0 -2.7

Poland 4.1 6.9 4.8 5.1

Poland 59.7 58.0 52.0 47.1

Poland -0.7 -6.0 -4.6 -3.2

Romania -1.5 -2.4 -1.2 -1.0

Romania 33.3 42.9 46.5 46.9

Romania -4.3 -9.8 -7.0 -4.0

Croatia 6.7 2.5 5.8 5.7

Croatia 75.3 88.1 82.8 79.2

Croatia 0.4 -8.0 -3.5 -2.6

Russia 4.5 1.5 0.4 1.1

Russia 28.5 31.1 28.7 28.4

Russia 1.8 -5.0 -3.4 -1.8

Serbia 0.8 -0.8 0.3 0.3

Serbia 61.5 64.4 66.7 63.2

Serbia -0.2 -8.0 -3.5 -2.0

Turkey 1.7 -5.1 -2.3 -1.9

Turkey 57.1 62.0 59.4 58.3

Turkey -5.3 -5.6 -5.4 -5.1

Gov’t debt (% GDP) 2019 2020E 2021F 2022F

Policy rate (%) 2019 2020 2021F 2022F

FX vs. EUR (EoP) 2019 2020 2021F 2022F

EU-CEE 44.1 56.8 58.7 58.9

EU-CEE

EU-CEE

Bulgaria 19.9 25.0 28.3 29.1

Bulgaria - - - -

Bulgaria 1.96 1.96 1.96 1.96

Czechia 30.2 38.1 44.4 47.3

Czechia 2.00 0.25 0.50 0.75

Czechia 25.4 26.2 25.6 25.0

Hungary 63.7 84.6 85.4 83.4

Hungary 0.90 0.60 0.60 0.60

Hungary 331 365.1 353 360

Poland 45.4 58.7 58.5 58.2

Poland 1.50 0.10 0.10 1.00

Poland 4.26 4.61 4.45 4.45

Romania 35.3 46.8 49.4 49.9

Romania 2.50 1.50 1.00 1.00

Romania 4.78 4.87 4.95 5.05

Croatia 72.8 89.6 87.9 84.9

Croatia - - - -

Croatia 7.44 7.53 7.53 7.53

Russia 12.5 18.3 19.4 20.8

Russia 6.25 4.25 4.25 4.50

Russia 69.3 90.7 90.2 95.0

Serbia 52.9 59.0 59.4 58.2

Serbia 2.25 1.00 1.00 1.00

Serbia 117.6 117.6 117.9 118.3

Turkey 32.6 40.0 40.7 41.4

Turkey 12.00 17.00 12.00 12.00

Turkey 6.67 9.08 10.11 11.67

Source: National statistical agencies, central banks, UniCredit Research

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 12 See last pages for disclaimer.

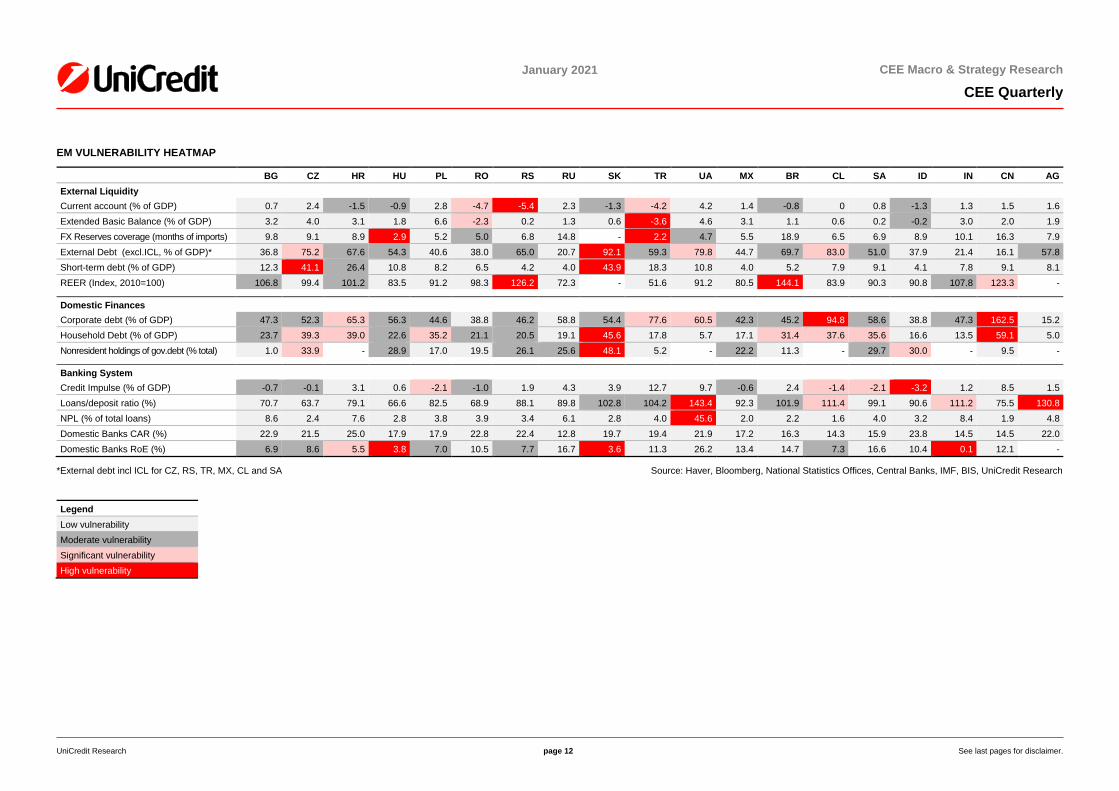

EM VULNERABILITY HEATMAP

BG CZ HR HU PL RO RS RU SK TR UA MX BR CL SA ID IN CN AG

External Liquidity

Current account (% of GDP) 0.7 2.4 -1.5 -0.9 2.8 -4.7 -5.4 2.3 -1.3 -4.2 4.2 1.4 -0.8 0 0.8 -1.3 1.3 1.5 1.6

Extended Basic Balance (% of GDP) 3.2 4.0 3.1 1.8 6.6 -2.3 0.2 1.3 0.6 -3.6 4.6 3.1 1.1 0.6 0.2 -0.2 3.0 2.0 1.9

FX Reserves coverage (months of imports) 9.8 9.1 8.9 2.9 5.2 5.0 6.8 14.8 - 2.2 4.7 5.5 18.9 6.5 6.9 8.9 10.1 16.3 7.9

External Debt (excl.ICL, % of GDP)* 36.8 75.2 67.6 54.3 40.6 38.0 65.0 20.7 92.1 59.3 79.8 44.7 69.7 83.0 51.0 37.9 21.4 16.1 57.8

Short-term debt (% of GDP) 12.3 41.1 26.4 10.8 8.2 6.5 4.2 4.0 43.9 18.3 10.8 4.0 5.2 7.9 9.1 4.1 7.8 9.1 8.1

REER (Index, 2010=100) 106.8 99.4 101.2 83.5 91.2 98.3 126.2 72.3 - 51.6 91.2 80.5 144.1 83.9 90.3 90.8 107.8 123.3 -

Domestic Finances

Corporate debt (% of GDP) 47.3 52.3 65.3 56.3 44.6 38.8 46.2 58.8 54.4 77.6 60.5 42.3 45.2 94.8 58.6 38.8 47.3 162.5 15.2

Household Debt (% of GDP) 23.7 39.3 39.0 22.6 35.2 21.1 20.5 19.1 45.6 17.8 5.7 17.1 31.4 37.6 35.6 16.6 13.5 59.1 5.0

Nonresident holdings of gov.debt (% total) 1.0 33.9 - 28.9 17.0 19.5 26.1 25.6 48.1 5.2 - 22.2 11.3 - 29.7 30.0 - 9.5 -

Banking System

Credit Impulse (% of GDP) -0.7 -0.1 3.1 0.6 -2.1 -1.0 1.9 4.3 3.9 12.7 9.7 -0.6 2.4 -1.4 -2.1 -3.2 1.2 8.5 1.5

Loans/deposit ratio (%) 70.7 63.7 79.1 66.6 82.5 68.9 88.1 89.8 102.8 104.2 143.4 92.3 101.9 111.4 99.1 90.6 111.2 75.5 130.8

NPL (% of total loans) 8.6 2.4 7.6 2.8 3.8 3.9 3.4 6.1 2.8 4.0 45.6 2.0 2.2 1.6 4.0 3.2 8.4 1.9 4.8

Domestic Banks CAR (%) 22.9 21.5 25.0 17.9 17.9 22.8 22.4 12.8 19.7 19.4 21.9 17.2 16.3 14.3 15.9 23.8 14.5 14.5 22.0

Domestic Banks RoE (%) 6.9 8.6 5.5 3.8 7.0 10.5 7.7 16.7 3.6 11.3 26.2 13.4 14.7 7.3 16.6 10.4 0.1 12.1 -

*External debt incl ICL for CZ, RS, TR, MX, CL and SA Source: Haver, Bloomberg, National Statistics Offices, Central Banks, IMF, BIS, UniCredit Research

Legend

Low vulnerability

Moderate vulnerability

Significant vulnerability

High vulnerability

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 13 See last pages for disclaimer.

EM VULNERABILITY HEATMAP (CONTINUED)

BG CZ HR HU PL RO RS RU SK TR UA MX BR CL SA ID IN CN AG

Policy

Policy Rate, nominal (%) - 0.25 - 0.60 0.10 1.50 1.00 4.25 0 17.00 6.00 4.25 2.00 0.50 3.50 3.75 4.00 4.35 38.00

Real policy rate (%) - -2.3 - -2.0 -2.8 -0.7 -0.5 -0.7 -1.5 2.1 2.1 0.9 -2.2 -2.2 0.3 2.1 -2.8 0.6 1.6

Real Money market rate (%) - -2.2 -1.8 -1.9 -2.8 -0.3 -0.7 0 -2.0 2.9 1.7 1.0 -3.7 -3.3 0.1 2.4 -3.1 4.5 -3.8

Headline inflation (% yoy) 0.4 2.7 -0.2 2.7 3.0 2.1 1.7 4.9 1.5 14.6 3.8 3.3 4.3 2.7 3.2 1.6 7.0 -0.6 35.8

Core Inflation (% yoy) 0.6 2.4 0.8 3.9 4.3 3.4 1.9 3.9 1.4 14.3 3.9 3.7 2.0 2.3 3.3 1.8 5.7 0.4 37.8

GG Fiscal balance (% of GDP) -2.3 -4.0 -3.1 -4.6 -5.5 -8.5 -7.5 -5.1 -4.7 -3.9 -8.5 -2.5 -13.7 -7.5 -10.7 -5.0 -6.3 -5.5 -8.9

GG Primary balance (% of GDP) -1.8 -3.2 -1.0 -2.3 -2.6 -7.1 -5.6 -4.1 -3.4 -1.2 - 0.7 -8.9 -6.6 -6.2 -3.0 -2.9 n.a. -

Government Debt (% of GDP) 24.6 38.4 85.3 74.3 51.6 44.0 57.6 18.3 60.2 42.6 79.8 48.2 80.8 49.6 75.2 60.2 56.2 63.0 70.4

Markets

External Debt Spread (10Y, bp)** 57.7 20.0 105.4 92.2 47.7 181.5 153.9 126.3 43.2 454.0 504.2 110.0 210.5 53.5 298.6 150.3 105.0 -6.9 -

Local Currency Curve (5Y, %)*** 0.2 0.8 0.4 1.5 0.4 2.6 2.6 5.4 -0.6 13.4 4.9 4.8 5.1 1.6 8.0 5.2 5.4 2.9 52.0

Local currency bond spread (2s10s)**** 62.6 115.2 44.9 117.3 117.0 68.5 139.7 150.0 13.9 -142.0 285.7 141.0 261.5 397.0 283.0 192.7 151.9 56.6 -270.2

CDS (10Y, bp) 61 44 122 87 89 117 149 140 71 328 384 140 225 85 300 116 128 30 1400

FX 3m implied volatility (%) - 5.6 4.0 7.2 6.4 2.3 - 15.4 - 16.9 - 15.0 20.3 13.8 17.2 10.2 5.9 5.8 15.0

Structural*****

IBRD Doing Business 61 41 51 52 40 55 44 28 45 33 64 60 124 59 84 73 63 31 126

WEF Competitiveness Ranking 49 32 63 47 37 51 72 43 42 61 85 48 71 33 60 50 68 28 83

Unemployment (%) 4.9 2.9 6.7 4.4 3.4 5.1 9.5 6.3 7.2 12.7 9.3 4.4 14.3 10.8 30.8 7.1 6.5 5.2 11.9

** Spread between 10Y EUR government bond yields and the corresponding German government bond yields for BG, HR, HU, PL, RO. For CZ, the spread refers to the 5Y yield. For the other countries, the spread is computed with respect to US government bond yields

*** Data for UA refer to the generic USD bond. Data for HR refer to the 4Y bond

**** Data for UA refer to the generic USD bond. Data for CL refer SA to the spread between 8Y and 2Y bond and 9Y and 2Y bond respectively. Data for HU refer to spread between 10Y and 3Y bond. *****IBRD and WEF indicators for 2018

Source: Haver, Bloomberg, National Statistics Offices, Central Banks, IMF, BIS, UniCredit Research

Legend

Low vulnerability

Moderate vulnerability

Significant vulnerability

High vulnerability

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 14 See last pages for disclaimer.

CEE strategy: Solid risk appetite and yield in demand

Elia Lattuga Co- Head of Strategy Research, Cross Asset Strategist (UniCredit Bank, London) +44 207 826-1642 [email protected]

■ As markets shift focus towards economic recovery, and while monetary policy at key central

banks remains accommodative, financing conditions on global markets should help fuel the

performance of risky assets and keep yield hunting alive. Developments pertaining to the

pandemic and to long-term US yields are key sources of risk that should be monitored.

■ CEE assets are set to benefit from negative net supply in the eurozone, the yield hunting

environment and positive developments in bond supply. Higher-yielding exposure might be

preferred, but portfolio flows might also sustain higher-rated issuers.

Asset performance in 2020 With large swings in asset performance and unprecedented stimulus by fiscal and monetary

authorities, 2020 has been an extremely volatile year for global markets. At the end of the year,

the MSCI World Index was 14% higher than it was a year earlier after posting a staggering 68%

rally from March lows. In spite of some upward pressure at the long end of the curve, 10Y UST

yields are still 80bp below their YE 2019 levels. Credit spreads across both US and European

markets have been tightening steadily in recent months, and broad indices have returned to

levels that prevailed a year ago. A return of implied volatility on US equities in the 20 points area

and the weakening of the USD, which lost over 10% (DXY) from March peaks, also supported a

general easing of financial conditions. EM bonds benefited from such improvement and posted

a sharp tightening in credit spreads. However, this was not enough to fully recover from earlier

widening, leaving spreads in broad indices a tad wider than they were a year ago. In total-return

terms, however, EM bonds managed to close 2020 with a positive performance. Across several

segments of the market, total returns exceeded 5%, a very good performance when one

considers the extent of 1Q20 losses. LatAm and lower-rated buckets across EM bond indices

underperformed, displaying, in some cases, sharp losses that were heavily affected by the large

drop recorded in 1Q. A selective approach paid off during volatile times. EMEA did well,

especially across hard-currency indices.

Investors focus on economic recovery over the medium term

2021 started on a positive note for risky assets, after a very strong performance in the latter part

of 2020. Uncertainty surrounding short-term development in contagion curves is still high, and a

number of countries have stepped up restrictions in recent weeks and this bodes ill for GDP

growth over 1Q, but risk appetite has remained solid. Markets are taking a constructive stance

with respect to the effectiveness and rapid distribution of COVID-19 vaccines and treatments,

which should limit the need for additional lockdowns down the road and pave the way for a

sustainable recovery in 2021.

CHART 1: TOTAL RETURNS (USD) CHART 2: FINANCING CONDITIONS

Source: Bloomberg, UniCredit Research

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

LatAm Asia EMEA LatAm Asia EMEA A Baa Ba B Caa 1-3Year

7-10Year

LC HC-USD HC-USD HC-USD

4Q20 3Q20 2Q20 1Q20

2019 2018 2020

-3

-2

-1

0

1

2

3

4

5

6

7

8

Jan 17 Oct 17 Jul 18 Apr 19 Jan 20 Oct 20

Sta

nd

ard

ize

d le

ve

ls

10Y USD RY DXY VIX US HY

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 15 See last pages for disclaimer.

Moreover, lingering support by central banks and the hunt for yield should contribute to limiting

the impact of negative growth news in the short term while keeping investors focused on

economic recovery over the medium term. Indeed, central banks ended 2020 by conveying a

clear message of support for financial markets and will act to avoid that a tightening in financial

conditions might derail progress before an economic recovery gains pace and inflation outlooks

improve (which might still be several quarters off). Both the Fed and the ECB are expected to

leave their official rates at their currently low levels for several years, while net asset purchases

(and thus balance-sheet expansion) continues into 2021. This will help markets digest lower, but

still high, borrowing needs as fiscal policy remains accommodative.

Strategy view for 2021 In this scenario, we think that risky assets are well-positioned to outperform. We expect to see

equity indices delivering returns in the 10% area in 2021. We believe that credit-spread

tightening has more room to run as yield hunting pushes investors to move into riskier

segments of the market, while interest-rate levels remain subdued. Indeed, we forecast a

gradual adjustment towards higher yield levels and steeper USD-denominated and

EUR-denominated government-bond curves. More specifically, we expect that the 10Y UST

yield will increase to 1.30% by the end of next year and to 1.75% by the end of 2022, while we

project that 10Y Bund yields will close 2021 at -0.30% and 2022 at -0.10%, representing a

moderate drag on total returns in the IG space. In spite of some widening in the transatlantic

spread at the long end, we believe that EUR-USD will continue to move north and close 2021

at 1.28, as the correlation between equity prices and the US dollar remains negative. In a

nutshell, moderately higher risk-free rates, tighter credit spreads and a weaker dollar should

keep financing conditions for EM paper attractive, while investors struggle to find yield.

The main risks to our call for 2021

Our positive call with regard to risky assets is very much dependent on an assumption that

vaccine distribution will allow a broader and more-solid recovery in global growth in 2021.

Hence, that recovery expectations could be jeopardized by negative news regarding vaccine

distribution, or more in general, regarding health conditions might weigh on appetite for risk at a

time when equities reflect earnings growth in the 20-30% range for this year and the next.

Moreover, after Democratic Senate candidates won run-off elections in the US state of Georgia,

thereby avoiding a split Congress, 10Y UST yields rose above 1% for the first time since March,

and reflation expectations and bear steepening are regaining popularity. We think that inflation

breakevens have limited upside. However, as the US economy recovers and as GDP begins to

return to pre-crisis levels, markets might start to react in anticipation of some tapering and

possibly to a halting of net asset purchases by the Fed. In such a scenario, a sharp repricing of

US rates could spillover on credit markets, given narrow spreads and high leverage – and

possibly on equity valuations and on the US dollar. This is a key risk to monitor in our view.

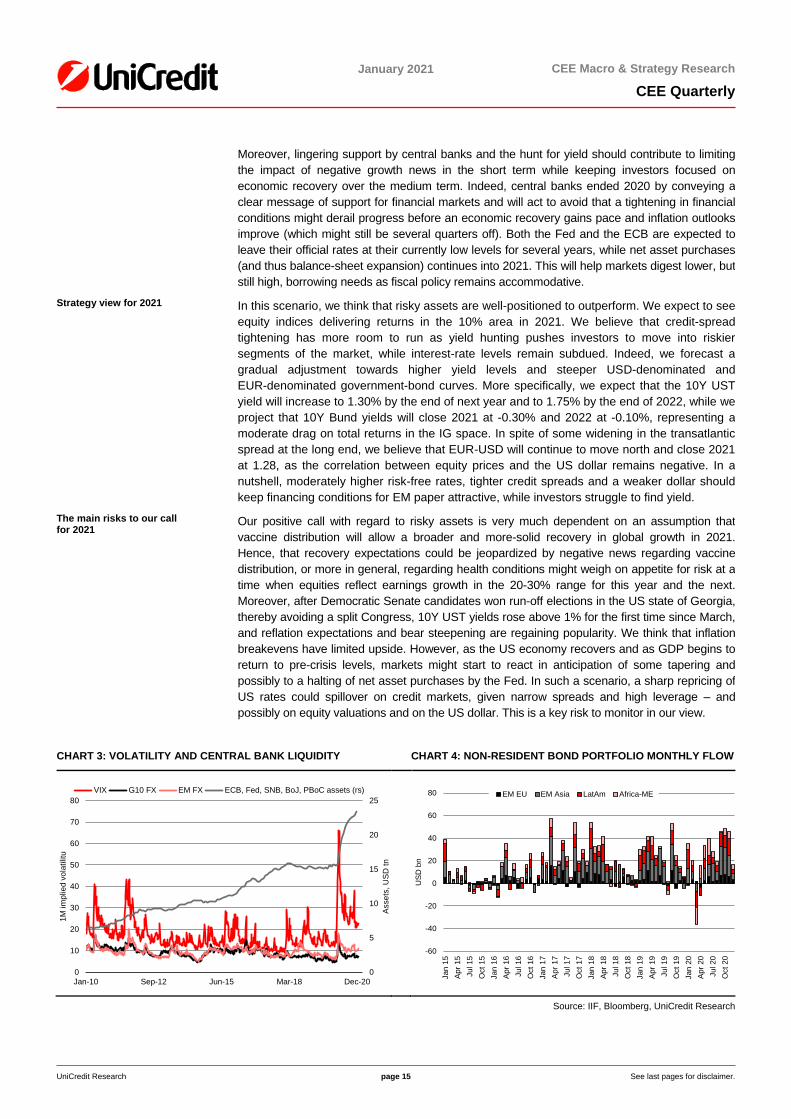

CHART 3: VOLATILITY AND CENTRAL BANK LIQUIDITY CHART 4: NON-RESIDENT BOND PORTFOLIO MONTHLY FLOW

Source: IIF, Bloomberg, UniCredit Research

0

5

10

15

20

25

0

10

20

30

40

50

60

70

80

Jan-10 Sep-12 Jun-15 Mar-18 Dec-20

Asse

ts, U

SD

tn

1M

im

plie

d v

ola

tilit

u

VIX G10 FX EM FX ECB, Fed, SNB, BoJ, PBoC assets (rs)

-60

-40

-20

0

20

40

60

80

Jan

15

Ap

r 15

Jul 15

Oct

15

Jan

16

Ap

r 16

Jul 16

Oct

16

Jan

17

Ap

r 17

Jul 17

Oct

17

Jan

18

Ap

r 18

Jul 18

Oct

18

Jan

19

Ap

r 19

Jul 19

Oct

19

Jan

20

Ap

r 20

Jul 20

Oct

20

US

D b

n

EM EU EM Asia LatAm Africa-ME

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 16 See last pages for disclaimer.

Currency volatility Central-bank action has also eased implied volatility across a number of assets. The Chicago

Board Options Exchange Volatility Index (VIX) has begun approaching the 20-point level

again. This is at the low end of the VIX range that has prevailed since March. FX volatility has

been following a similar path, but EM currency volatility remains high compared to G7

currency volatility. As the growth outlook improves and the recovery broadens, and with major

central banks remaining committed to providing liquidity, we expect markets to become

calmer over the coming months, albeit with risks of short-lived spikes. Lower FX volatility

would contribute to channeling more funds towards EM markets from crossover investors.

Portfolio reallocation benefiting CEE

CEE bond markets are well-positioned in this respect to attract inflows as EUR-denominated

bond markets will be bid and increasingly owned by the Eurosystem. With governments

funding their fiscal expansions and corporates transforming their short-term liquidity sources

into capital-market borrowing, 2020 has been characterized by very intense supply pressure

on global markets. The very large gross and net supply has been digested smoothly, thanks

to the support of central banks’ asset-purchasing programs and strong demand from private

investors. In the euro area, PEPP and APP flows have led to a massive increase in demand

for bonds. This has taken gross supply net of redemptions and central-bank purchases to

negative levels in spite of large funding needs. In the past, sharply negative net supply

(including quantitative easing) in the euro area has fueled portfolio reallocations, also

benefiting CEE countries. In 2016-17, however, euro-area bond markets offered much better

entry levels for those willing to add duration or credit risk. Yield curves were steeper, and

spreads were wider and more dispersed. The share of eurozone bonds trading at negative

yield levels has increased steadily over the past few months, and scarcity has become a more

material issue across several segments of the market. The ECB’s asset purchases will

continue over the coming quarters and, according to our calculations, will more than offset net

borrowing for both government and non-financial corporate debt over the course of 2021.

CEE bonds appear well-positioned to benefit from portfolio reallocation in such an

environment. Higher-yielding exposures, such as to Romania or Hungary might be favored,

but given their scarcity of yield and higher-rated paper, exposure to Poland and Czech bonds

might also be of interest – if volatility on the currency market subsides.

CHART 5: PORTFOLIO INFLOWS INTO CEE DEBT (12M SUM) CHART 6: YIELD CURVES EUR-DENOMINATED BONDS

*Euro-area net issuance refers to net government and non-financial corporations’ gross issuance net of redemptions and of ECB APP and PEPP flows, which are calculated as a three-month rolling sum.

Source: Haver, Bloomberg, UniCredit Research

-300

-200

-100

0

100

200

300-25

-20

-15

-10

-5

0

5

10

15

20

25

Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

EA

issu

an

ce

Po

rtfo

lio in

flo

ws U

SD

bn

EA net issuance* (rs, inv.) CZK RON PLN HUF

-1

-0.5

0

0.5

1

1.5

2

2.5

3

2019 2024 2030 2035 2041 2046 2052 2057

Romania Hungary Poland Euro Swap

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 17 See last pages for disclaimer.

Reduced supply pressure in CEE

In 2021, three additional factors will reduce net borrowing needs in CEE, supporting bond

prices: 1. budget deficits will fall compared to 2020; 2. up to 25% of funding needs could be

covered out of the market by borrowing from EU facilities such as SURE and NGEU. This is

especially true for higher yielders such as Croatia and Romania, which have a larger incentive

to tap funds at a cost below market levels. However, even Bulgaria, Hungary and Poland

could decide to tap EU loans to extend debt duration at below-market costs. The availability of

such funds will also allow greater flexibility for issuers, reducing further supply risk;

3. remaining gross external borrowing needs will either be below redemptions or fall short of

the purchases needed to maintain the current allotment by index-trackers (in percent of

assets under management).

In EU-CEE, we continue to prefer Romanian bonds to their regional peers, both outright and

in spreads. We believe that the downgrade premium should be completely priced out in 2021,

besides investors having to anchor yield expectations lower due to cheap EU funding. In

Russia, a more stable currency could persuade foreign investors to take exposure back to

early 2020 levels as the OFZ curve could bull flatten further after 2020’s rate cuts. In Turkey,

investors could prefer an outright carry trade in 1Q21 as the CBRT remains hawkish and

inflation continues to rise. However, likely rate cuts in 2H21 could see investors pile into

TURKGBs for a while. Lower real rates may end the attractiveness of this trade before year-

end due to potential currency depreciation.

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 18 See last pages for disclaimer.

Updating our REER models

PLN

■ The last few weeks have seen some volatility on EUR-PLN

but the pair has recently approached the 4.50 handle,

nearly 2% higher compared to the December lows.

■ In REER terms, the zloty trades close to the average over

the past six months; according to our model, it is broadly

in line with its fair value.

■ The short-term outlook for the currency is positive and we

see EUR-PLN dropping below 4.45. This level should

prove as a good anchor for developments during the year.

We do not envisage departures from the 4.40-4.50 range

over the forecast horizon, as the NBP could intervene to

keep the pair from falling below 4.40. Levels above 4.50

offer good selling opportunities, in our view.

CZK

■ The CZK closed 2020 on a solid footing, having recovered

most of the losses recorded in September and October

against the EUR. Breaking below 26.0 would take the pair

to its lowest level since March.

■ Our REER model for the CZK displays the currency as

slightly overvalued, after the last few months’ recovery.

However, this should not prevent the CZK from gaining

against the EUR in the medium term.

■ We think that EUR-CZK might break below 26.0 and

approach 25.5 by the end of 2021. The CNB is more hawkish

than its peers, supporting CZK appreciation. In the short

term, the PLN might outperform the CZK.

HUF

■ EUR-HUF has displayed large swings in the 355-365 area

over the past four months, with only short-lived deviations

outside of the range. The pair remains at the upper end of

the 2020 range, and also in REER terms the recovery has

been limited.

■ According to our REER model, the HUF remains

moderately undervalued, having recovered only part of its

undervaluation compared to the crisis period.

■ We forecast EUR-HUF within the 355-360 area over the next

few quarters. While the NBH tried to decouple monetary

policy decisions from HUF fluctuations, the currency remains

the favorite short for investors in central Europe.

Source: Haver, Bloomberg, UniCredit Research

-15%

-10%

-5%

0%

5%

10%

15%

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Mar-07 Dec-09 Sep-12 Jun-15 Mar-18 Dec-20

RE

ER

under/

over

valu

ation

Spot F

X

Model (rs) EUR USD

-15%

-10%

-5%

0%

5%

10%

15%

10

15

20

25

30

35

40

45

50

Jan-00 Sep-02 Jun-05 Mar-08 Dec-10 Sep-13 Jun-16 Mar-19

RE

ER

und

er/

over

va

luatio

n

Spo

t F

X

Model (rs) EUR USD

-15%

-10%

-5%

0%

5%

10%

15%

125

175

225

275

325

375

425

Jan-00 Feb-04 Mar-08 Apr-12 Jun-16 Jul-20

RE

ER

und

er/

over

va

luatio

n

Spo

t F

X

Model (rs) EUR USD

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 19 See last pages for disclaimer.

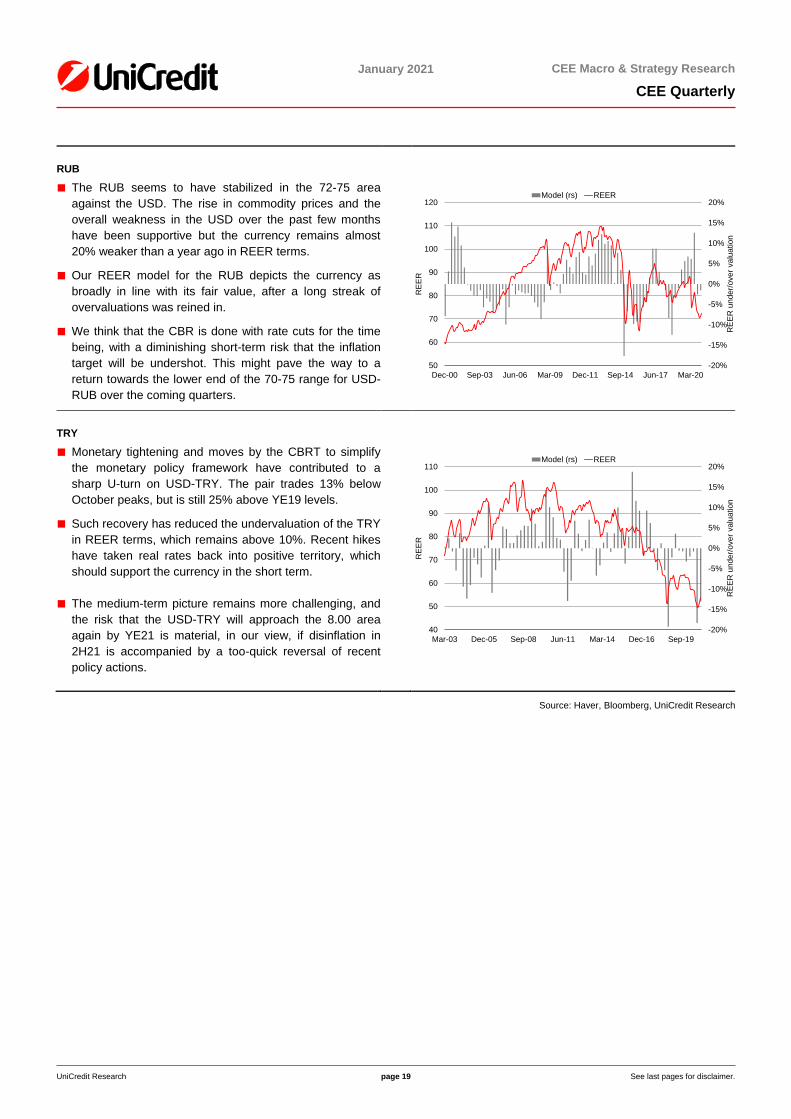

RUB

■ The RUB seems to have stabilized in the 72-75 area

against the USD. The rise in commodity prices and the

overall weakness in the USD over the past few months

have been supportive but the currency remains almost

20% weaker than a year ago in REER terms.

■ Our REER model for the RUB depicts the currency as

broadly in line with its fair value, after a long streak of

overvaluations was reined in.

■ We think that the CBR is done with rate cuts for the time

being, with a diminishing short-term risk that the inflation

target will be undershot. This might pave the way to a

return towards the lower end of the 70-75 range for USD-

RUB over the coming quarters.

TRY

■ Monetary tightening and moves by the CBRT to simplify

the monetary policy framework have contributed to a

sharp U-turn on USD-TRY. The pair trades 13% below

October peaks, but is still 25% above YE19 levels.

■ Such recovery has reduced the undervaluation of the TRY

in REER terms, which remains above 10%. Recent hikes

have taken real rates back into positive territory, which

should support the currency in the short term.

■ The medium-term picture remains more challenging, and

the risk that the USD-TRY will approach the 8.00 area

again by YE21 is material, in our view, if disinflation in

2H21 is accompanied by a too-quick reversal of recent

policy actions.

Source: Haver, Bloomberg, UniCredit Research

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

50

60

70

80

90

100

110

120

Dec-00 Sep-03 Jun-06 Mar-09 Dec-11 Sep-14 Jun-17 Mar-20

RE

ER

und

er/

over

va

luatio

n

RE

ER

Model (rs) REER

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

40

50

60

70

80

90

100

110

Mar-03 Dec-05 Sep-08 Jun-11 Mar-14 Dec-16 Sep-19

RE

ER

und

er/

over

va

luatio

n

RE

ER

Model (rs) REER

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 20 See last pages for disclaimer.

Countries

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 21 See last pages for disclaimer.

Bulgaria Baa1 stable/BBB stable/BBB stable*

Outlook

Additional fiscal measures were announced at the end of 2020 to mitigate the damages caused by the second wave of the

COVID-19 pandemic. We expect the early phase of the recovery in Bulgaria to be somewhat weaker than in most CEE

economies for two reasons. First, Bulgaria was among the countries worst hit by the second wave of COVID-19 infections.

Second, Parliamentary elections will lead to a slow start for the NGEU program and to delays in some infrastructure projects

initiated under the previous government. However, economic recovery is likely to gain stronger momentum in 2022 and 2023

once the health crisis ends and Bulgaria’s absorption of NGEU funds shifts to a higher gear.

Strategy

Sovereign’s funding needs are set to rise this year, as Bulgaria is the only CEE country where budget deficit is expected to

increase. To meet these needs, a combination of new Eurobond issue, domestic bond issuance, and low-cost borrowing

provided under SURE financial assistance instrument will be used. The first tranche of low-cost borrowing from NGEU is

expected in 2022.

Author: Kristofor Pavlov, Chief Economist (UniCredit Bulbank)

KEY DATES/EVENTS

■ Mid-Feb: Labor force 4Q20 data

■ Mid-Feb, Early-Mar: GDP data (4Q20 flash estimate and

structure, preliminary data for 2020)

■ End March or early April: General elections

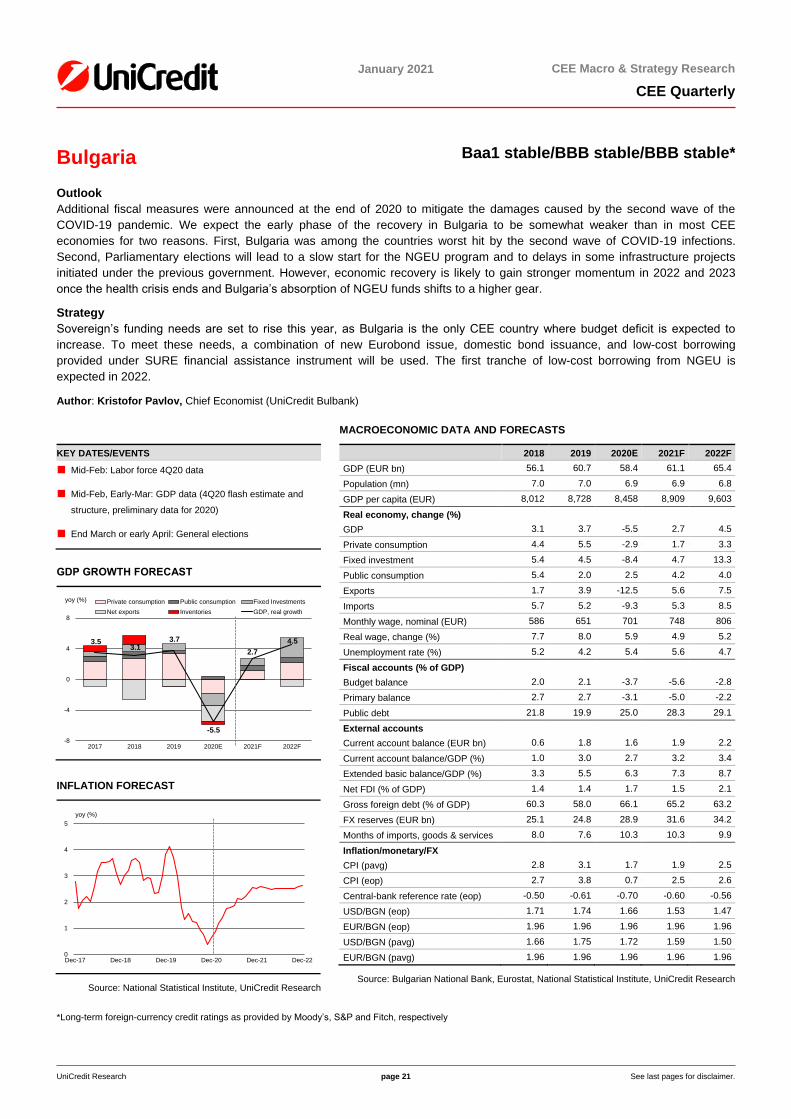

GDP GROWTH FORECAST

INFLATION FORECAST

Source: National Statistical Institute, UniCredit Research

MACROECONOMIC DATA AND FORECASTS

2018 2019 2020Е 2021F 2022F

GDP (EUR bn) 56.1 60.7 58.4 61.1 65.4

Population (mn) 7.0 7.0 6.9 6.9 6.8

GDP per capita (EUR) 8,012 8,728 8,458 8,909 9,603

Real economy, change (%)

GDP 3.1 3.7 -5.5 2.7 4.5

Private consumption 4.4 5.5 -2.9 1.7 3.3

Fixed investment 5.4 4.5 -8.4 4.7 13.3

Public consumption 5.4 2.0 2.5 4.2 4.0

Exports 1.7 3.9 -12.5 5.6 7.5

Imports 5.7 5.2 -9.3 5.3 8.5

Monthly wage, nominal (EUR) 586 651 701 748 806

Real wage, change (%) 7.7 8.0 5.9 4.9 5.2

Unemployment rate (%) 5.2 4.2 5.4 5.6 4.7

Fiscal accounts (% of GDP)

Budget balance 2.0 2.1 -3.7 -5.6 -2.8

Primary balance 2.7 2.7 -3.1 -5.0 -2.2

Public debt 21.8 19.9 25.0 28.3 29.1

External accounts

Current account balance (EUR bn) 0.6 1.8 1.6 1.9 2.2

Current account balance/GDP (%) 1.0 3.0 2.7 3.2 3.4

Extended basic balance/GDP (%) 3.3 5.5 6.3 7.3 8.7

Net FDI (% of GDP) 1.4 1.4 1.7 1.5 2.1

Gross foreign debt (% of GDP) 60.3 58.0 66.1 65.2 63.2

FX reserves (EUR bn) 25.1 24.8 28.9 31.6 34.2

Months of imports, goods & services 8.0 7.6 10.3 10.3 9.9

Inflation/monetary/FX

CPI (pavg) 2.8 3.1 1.7 1.9 2.5

CPI (eop) 2.7 3.8 0.7 2.5 2.6

Central-bank reference rate (eop) -0.50 -0.61 -0.70 -0.60 -0.56

USD/BGN (eop) 1.71 1.74 1.66 1.53 1.47

EUR/BGN (eop) 1.96 1.96 1.96 1.96 1.96

USD/BGN (pavg) 1.66 1.75 1.72 1.59 1.50

EUR/BGN (pavg) 1.96 1.96 1.96 1.96 1.96

Source: Bulgarian National Bank, Eurostat, National Statistical Institute, UniCredit Research

*Long-term foreign-currency credit ratings as provided by Moody’s, S&P and Fitch, respectively

yoy (%)

3.53.1

3.7

-5.5

2.7

4.5

-8

-4

0

4

8

2017 2018 2019 2020E 2021F 2022F

Private consumption Public consumption Fixed Investments

Net exports Inventories GDP, real growth

0

1

2

3

4

5

Dec-17 Dec-18 Dec-19 Dec-20 Dec-21 Dec-22

yoy (%)

<date>

UniCredit Research page 22 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

Difficult start to recovery but strong medium-term outlook

The outlook is for a subdued economic recovery in 2021 Bulgaria was hit hard by the second wave In 2021, economic growth will depend on path of virus Another difficult season for summer tourism is expected Share of vaccinated people to become the most closely watched indicator No need for new restrictions in winter 2021-22 Fiscal support likely to increase in 2021

After GDP contracted by around 5.5% in 2020, our baseline scenario envisages only a partial

recovery of 2.7% this year. Recovery will take a stronger hold in 2022 and 2023, when we

anticipate GDP growth to accelerate to something between 4% and 5% annually. We expect

GDP to return to its pre-crisis level in mid-2022. Getting back to full employment is likely in the

end of 2023. Uncertainty over the near-term outlook remains elevated. Risks to our baseline

macro scenario are dominated by pandemic dynamics and local politics related factors.

The economy faces a difficult winter. The main reason is the surge in COVID-19 infections (see

lhs chart) that have led to the adoption of new restrictions in November. The new restrictions are

milder than those implemented during the first wave of the pandemic, but are likely to remain in

place for longer. We expect the economy to contract in both 4Q20 and 1Q21. The fall in GDP is

likely to be more modest compared to the first wave of the pandemic, because some sectors are

excluded from the restrictions, including most importantly the manufacturing sector.

A genuine relaxation of the restrictions will start in March, when we expect the pandemic

curve to become more promising. The spring will limit the spreading of the disease, similarly,

to what we witnessed in 2020. We expect GDP to rebound in 2Q21 and beyond, as the direct

impact of the pandemic on the economy eases, and fiscal stimulus provide further support.

However, consumption in tourism and other sectors most exposed to the pandemic’s impact

will remain subdued. This is because the positive impact from vaccination will take time to

materialize, thereby causing many people to continue behaving cautiously and maintaining

some sort of voluntary physical distancing throughout the summer months of 2021.

The strength and speed of the recovery will depend on the timing and effectiveness of the roll-out

of the vaccines. Opinion poll conducted by Alpha research in December suggests that the share of

the population who want to be vaccinated is similar to the rest of Europe (see right chart). We hope

that the share of people wishing to be vaccinated will increase, as information about the pros and

cons of doing so becomes more widely available and as leaders in politics, business and the arts

presumably lead a large-scale campaign to boost vaccination rates.

Rising vaccination levels (closer to the one required to reach collective immunity) will prevent

the need for new restrictions in winter 2021-22. We expect spending to rise and consumption

patterns to slowly start to normalize, boosting GDP growth in 4Q21 and further into 2022.

The strength of the recovery will depend on the size and efficiency of the fiscal policy

response. Initially, Bulgaria’s fiscal policy response was more delayed and timid than in the

other CEE countries. The scale of the fiscal support was gradually increased thereafter and

we expect it to have reached 3.2% of GDP in 2020.

BULGARIA BADLY HIT BY SECOND WAVE OF PANDEMIC WILLINGNESS TO GET COVID -19 VACCINE IS MORE THAN 50%

Source: Worldometer, Alpha Research, UniCredit Research

0

100

200

300

400

500

600

700

Slo

ven

ia

Bulg

aria

Cro

atia

Hu

ng

ary

Bosnia

and

H.

Ma

ce

do

nia

Lithu

ania

Italy

Austr

ia

Cze

chia

Nov-20 Dec-20

10 most badly hit European countries from the second wave:New COVID-19 deaths per 1 mn inhabitants

15%

40%

45%

Want to be vaccinated, but will wait to see if the vaccines had negative effects

Want to be vaccinated

Don't want to be vaccinated

Share of Bulgarians who say they want/don`t want to be vaccinate against COVID-19. (Dec'20)

<date>

UniCredit Research page 23 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

Government to start withdrawing fiscal support from 2022 Wage subsidies and short-time work schemes have helped prevent a massive increase in unemployment Absent policies to facilitate a rapid reallocation of workers, significant rise in unemployment rate is likely toward the end of 2022, when phasing out of job retention schemes should begin Bulgarian are likely to go to the polls on 28 March GERB likely to remain largest party… …but BSP more likely to form next government

As Bulgaria was among the countries hit hardest by the second wave of the pandemic, and

because it is one of the economies with the largest free fiscal room available, we expect fiscal

support to increase this year (see lhs chart).

If our estimates are broadly right, fiscal support will increase to around 4.0% of GDP in 2021.

On top of that, the government has raised public sector wages, pensions and some social

payments, which are likely to cost some 2.0% of GDP. All of these spending increases will

drive the fiscal deficit on an accrual basis to 5.6% of GDP in 2021, up from 3.7% in 2020,

making Bulgaria the only CEE country where budget deficit is expected to rise this year. We

think the government will start withdrawing fiscal support only very gradually and when

economic recovery is likely to have already taken a stronger hold. Other less fiscally strong

economies in CEE, however, will have to start withdrawing fiscal support earlier, perhaps

beginning from the 2H21, potentially hampering their economic recovery prospects.

The unemployment rate has increased only modestly thanks to the widespread use of job

retention schemes. Indeed, the sharp reduction in overall hours worked in the 2Q20 and 3Q20

(see rhs chart) was mostly driven by a reduction in hours per worker and not by excessive job

losses. In fact, the unemployment rate increased to only 5.9% in 2Q20 and 4.8% in 3Q20,

from 4.1% in 4Q19. The decline in the participation rate, which was mostly attributable to the

labor market stress and the related exit of discouraged workers from the labor force, also

helped moderating the rise in the unemployment rate. Following the rise in the unemployment

rate to an average of 5.4% in 2020, we expect a further increase to 5.6% in 2021 on average.

After values above 6% mark in 4Q20 and 1Q21, the situation is not expected to ease until

later in the current year. The acceleration of GDP growth, which is expected to begin in 2022,

is likely to help economy get back to full employment toward the end of 2023.

The president intends to schedule the next regular parliamentary elections on the earliest

possible date envisaged by the law. If such decision is eventually taken, it will shorten the

election campaign time and is likely to benefit large and well-established political parties.

Small parties will face even more difficulties in the preparation of the election, because the

vote will be organized and held amidst the worst health crisis in the country’s modern history.

The GERB is likely to remain the largest party in the new parliament. However, the BSP is

more likely to form the next government. If the past has any clues to offer, the transition to a

new government will slow down decision making in the public administration. This, in turn, is

likely to cause some delays in starting NGEU-funded projects and in the completion of some

key infrastructure projects initiated under the GERB, which will negatively affect the pace of

recovery in 2021. Importantly, the BSP is likely to remove the flat personal income tax, which

we expect to support growth, as those at the bottom of the income distribution will benefit.

ROLE OF FISCAL POLICY SUPPPORT TO RISE IN 2021 LABOR MARKET ADJUSTMENT WAS LESS PAINFULL THIS TIME

Source: Eurostat, National Statistical Institute, Ministry of Finance, UniCredit Research

1.6

2.6

0.6

1.2

1.0

0.2

0

1

2

3

4

5

6

2020 2021

Fiscal support without clear beneficiary

Fiscal support for companies

Fiscal support for households

as % of GDP

3.2

4.0

-12.0

-8.0

-4.0

0.0

4.0

8.0

1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20

Hours worked, yoy growth Unemployment rate%

<date>

UniCredit Research page 24 See last pages for disclaimer.

January 2021 CEE Macro & Strategy Research

CEE Quarterly

New Eurobond issue is likely in the second half of the year

Fiscal reserve remains at a very comfortable level Sovereign funding needs set to rise this year Next Eurobond likely in 2H21 Public debt to peak at 30% of GDP in 2021… …before slowly going down in both 2022 and 2023

As the pandemic took a turn for the worse toward the end of 2020, fiscal stimulus had to

increase too, pushing the budget deficit on a cash basis up to 3.1% of GDP in 2020 (from the

September estimate of 2.4%). The corresponding increase in funding needs last year was met

using fiscal reserves, which had reached a record high of 11.9% of GDP, after successful

Eurobond issuance of EUR 2.5bn in September.

Bulgaria’s funding needs are set to rise in 2021, as it is the only country in CEE expected to

register a larger budget deficit this year than in 2020. To meet these needs, we expect the

authorities to use a combination of new Eurobond issue, domestic bond issuance, and low-cost

borrowing provided under SURE financial assistance instrument. The first traches of low-cost

borrowing from NGEU program are not anticipated before the beginning of 2022, in our view.

We expect Bulgaria to issue its next Eurobond in the 2H21. The volume of the new Eurobond

issue is likely to be around EUR 1.5 billion, while domestic bond issuance is forecasted to

remain close to the level of bond issuance already posted in 2020 (BGN 1.2 billion).

The combination of ample fiscal reserves and low-cost borrowing available under SURE

financial assistance program and NGEU recovery plan is likely to keep yields on Bulgarian

sovereign bonds low in the years leading up to the euro adoption, which we expect in 2024.

If our projection is broadly right, public debt will rise to 28.3% of GDP in 2021. As growth

momentum gets stronger and the government starts to withdraw fiscal policy support,

sovereign funding needs will decrease and public debt will stabilize at levels slightly below

30% mark in the next two years. After peaking at 29.5% of GDP in 2023, our projection

envisages public debt slowly go down to 26.1% in the long end of our forecast in 2027.

GOVERNMENT GROSS FINANCING REQUIREMENTS

GROSS EXTERNAL FINANCING REQUIREMENTS

EUR bn 2020E 2021F 2022F

Gross financing requirement 2.6 3.4 3.4

Budget deficit 1.8 2.8 1.8

Amortization of public debt 0.7 0.6 1.6

Domestic 0.5 0.4 0.2

Bonds 0.5 0.4 0.2

Bills 0 0 0

Loans/other 0 0 0

External 0.2 0.2 1.4

Bonds and loans 0 0 1.3

IMF/EU/other IFIs 0.2 0.2 0.2

Financing 2.6 3.4 3.4

Domestic borrowing 0.6 0.6 0.6

Bonds 0.6 0.6 0.6

Bills 0 0 0

Loans/other 0 0 0

External borrowing 2.6 2.6 2.6

Bonds and loans 2.5 2.0 1.5

IMF/EU/other IFIs 0.1 0.6 1.1

Privatization/other 0 0 0

Fiscal reserves change (- =increase)

-0.6 0.2 0.2

EUR bn 2020E 2021F 2022F

Gross financing requirement 9.6 10.0 11.0

C/A deficit -1.6 -1.9 -2.2

Amortization of medium and long term debt 3.3 3.2 4.3

Government/central bank 0.2 0.2 1.4

Banks 0.5 0.5 0.6

Corporates/other 2.5 2.5 2.3

Amortization of short-term debt 7.9 8.7 9.0

Financing 9.6 10.0 11.0

FDI (net) 1.0 0.9 1.4

Portfolio equity, net -0.2 1.1 -0.6

Medium and long-term borrowing 5.8 3.9 5.5

Government/central bank 2.6 2.6 2.6

Banks 0.5 0.6 0.6

Corporates/other 2.8 0.7 2.3

Short-term borrowing 8.7 9.0 9.3

EU structural and cohesion funds 1.1 1.6 2.1

Other -2.7 -3.9 -4.0

Change in FX reserves (- = increase) -4.1 -2.7 -2.6

Memoranda:

Nonresident purchases of LC gov’t bonds 0 0 0

International bond issuance, net 2.5 2.0 0.3

Source: Bulgarian National Bank, Ministry of Finance, UniCredit Research

<date>

January 2021 CEE Macro & Strategy Research

CEE Quarterly

UniCredit Research page 25 See last pages for disclaimer.

Croatia Ba2 positive /BBB- stable /BBB- stable*

Outlook

We now expect 4.6% GDP growth in 2021 and 4.8% in 2022. The renewed spread of COVID-19 in the autumn was an important

factor influencing our view. Tougher restrictions in 4Q20 and 1Q21 will likely constrain private spending, pushing back growth to 2H21

and 2022, when we also expect more impact from the absorption of NGEU funds. An important factor for growth in 2021 will be the

performance of the tourism season, the segment that likely differentiates the development in Croatia from the rest of CEE. A rapid

implementation of vaccinations and a higher immunization rate would help. On the other hand, fiscal stimulus announced by the