A Majjggor Emerging Oil Company in East Africa

30

A Major Emerging Oil Company in East Africa Corporate Presentation November, 2013 A Lundin Group Company

Transcript of A Majjggor Emerging Oil Company in East Africa

A Major Emerging Oil j g gCompany in East Africa

Corporate PresentationNovember, 2013

A Lundin Group Company

2013 – The Proof in the Pudding

• Moving to development– Exceeds threshold volumes for development

– Working with host governments and partners to put development plans in place

– Appraisal programs initiated (drilling and 3D seismic)

• Still major exploration upside– Over 100 undrilled prospects and leads identified

– 4 for 4 in South Lokichar Basin – 9 more prospects yet to drill4 for 4 in South Lokichar Basin 9 more prospects yet to drill

– Recent wells prove petroleum system in Turkana and Anza Basins

– Five new basin opening wells to be drilled in next 6 months

• Very Strong Balance Sheet – Recent $450MM funding means no additional financing required until mid-2015

Will likely do an industry deal at that point as reserve growth and development plan comes– Will likely do an industry deal at that point as reserve growth and development plan comes into focus

• High impact drilling intensive program – 6 rigs from 4th quarter 2013

2

Location, Location, Location

• First mover advantage in securing unequalled acreage position in what isunequalled acreage position in what is now the world’s top exploration spot

– Over 250,000 sq km or 62 million acres gross

• Four separate petroleum systems Rift Basin Area

proven to contain multi-billion barrels in surrounding countries

• At the crossroads for infrastructure buildup in East Africa (Kenya, Uganda, Sudan, Ethiopia), p )

• Major oil companies now scrambling to gain a foothold position

3

gain a foothold position

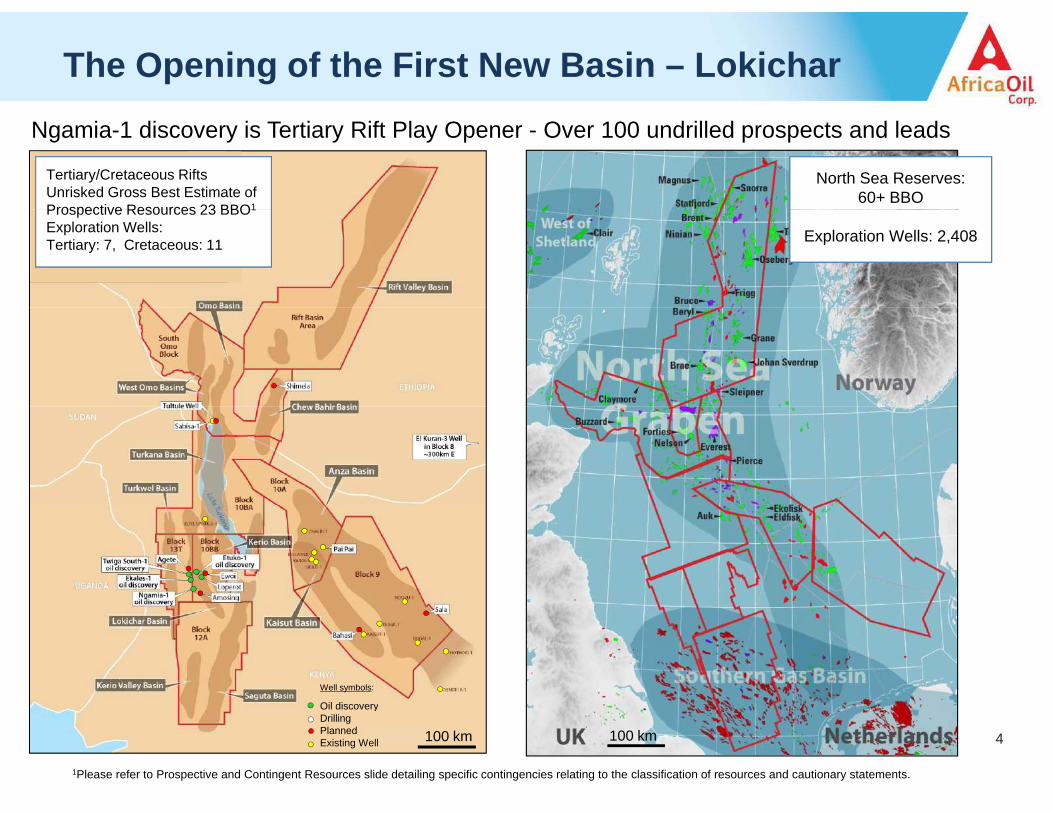

The Opening of the First New Basin – LokicharNgamia-1 discovery is Tertiary Rift Play Opener - Over 100 undrilled prospects and leads

North Sea Reserves:60+ BBO

Tertiary/Cretaceous Rifts Unrisked Gross Best Estimate of Prospective Resources 23 BBO1

Exploration Wells: 2,408Prospective Resources 23 BBO1

Exploration Wells: Tertiary: 7, Cretaceous: 11

Well symbols:

Oil di

4100 km

1Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

100 km

Oil discoveryDrillingPlannedExisting Well

Lokichar Basin – Low Risk Proven Hydrocarbon System

• 100% success rate to date – 4 for 4 on exploration wellsLokichar Sub-basin

Time Structure Map

• Etuko oil discovery confirms extension of productive fairway eastward into the ‘Rift Flank Play’.

• Numerous low-risk undrilled prospects defined on t d ith i ti i i

Etom North

Time Structure MapTop Lokhone Shale

trend with existing seismic

Agete

Etom

Seismic Section along String of Pearls

Etuko-1Discovery

-Projected-Twiga S.‐1 Ekales

Swala

Agete

Etom

Ngamia‐1 AmosingTwiga SouthDiscovery

g

Loperot-1

Seismic Section along String of Pearls

Oil in shallow b h l

Ewoi

Southern Stringof Pearls

boreholesEkalesDiscovery

NgamiaDiscovery

Amosing

Ekunyuk

5

20 km13T 10BB

Ekosowan

* Some prospects renamed to reflect local designations

5 KMProspects& Leads

Ngamia & Twiga South DiscoveriesNgamia 1: Twiga South 1:

• Core and test data confirm excellent reservoirs:– 23-29% porosity– 100 md - 3 darcy permeability

• 2 812 b d f 3 t t

• Test data confirms excellent reservoir quality in Upper Auwerwer sands:

– 23-29% porosity– 50 – 400 md permeability

Ngamia-1: Twiga South-1:

• 2,812 bopd from 3 tests• Estimated 5,200 bopd potential with optimized artificial lift equipment • No formation water or pressure depletion during test

• Produced 3,200 bopd from six tests• With optimized artificial lift equipment this rate would

increase to a cumulative rate of around 5,400 bopd• No formation water or pressure depletion during test

MiocenePliocene

Auwerwer Sandstones

MiocenePliocene

Auwerwer Sandstones

Sandstones

Lokhone Shale

Lokhone Shale

6

ShaleSource

L.Lokhone Ss

Note: Transient pressure analysis has been conducted on the Ngamia-1 and Twiga South-1 well tests. No pressure depletion was recorded over the duration of the tests. Flow periods ranged from 0.5 to 2.5 days and build up ranged between 3 to 12 days.

L.Lokhone Ss

Lokichar Basin Exploration through 2014

Upcoming Wells:

•Agete (drilling)

Gross Best Estimate Contingent (2C) Resources to date:368 MMBO (gross)1

1 2013 Competent Persons Report (CPR)

Etom NorthBest-Estimate Gross Resources:Prospective : 234 MMBO

Etom Complex – Spud 1H, 2014B E i G R

g ( g)

•Amosing

•EwoiEtuko-1 (2013), TD: 3051m~40m net pay in Auwerwer & U. LokhonePossible 50m net in Lower LokhoneEtom

p p ( )Etom North

Best-Estimate Gross Resources:Prospective : 467 MMBO

Agete–1 (2013): Currently Drilling

Best-Estimate Gross Resources:Prospective : 276 MMBO •Ngamia West

•Ekunyuk

•Et

Best-Estimate Gross Resources:Contingent (2C) : 100 MMBO

EwoiEtuko

Twiga South-1 (2012), TD: 3227m>70m net pay: 2,812 bopd constrained

Best-Estimate Gross Resources:C ti t (2C) 87 MMBO

Agete

Twiga South Ewoi– Spud Q1, 2014

Best-Estimate Gross Resources:

Prospective : 276 MMBO

•Etom

•Ekosowan

•EtukoTest and appraisal

Ewoi

Loperot-1 (Shell, 1992), TD: 2950m18-50m net pay (estimated)Oil recovered to surface via wireline-Prospective Resources:I l d d i h E i P

Ekales-1 (2013) TD:2,554mPre-Drill Best-Estimate Gross Resources:

O

Contingent (2C) : 87 MMBOProspective : 132 MMBO

Ekales

Prospective : 317 MMBO

Loperot

pp

•Twiga appraisal

•Ngamia Appraisal

EkunyukIncluded with Ewoi ProspectProspective : 234 MMBO

3D Outline:550 sqkm

Ngamia & West Ngamia

Ngamia-1 (2012), TD: 2340m>200m net pay: 3,200 BOPD constrained

Best-Estimate Gross Resources:Contingent (2C) : 180 MMBO

Ekunyuk– Spud Q2, 2014 Best Estimate Gross Resources:Prospective : 203 MMBO

Seismic:

•Ngamia Twiga 3DEkosowan

Block 10BB13T

AmosingProspective : 281 MMBO

Amosing- Spud Q4, 2013Best-Estimate Gross Resources:Prospective : 172 MMBO 10BB

7

•Ngamia-Twiga 3D

(550 sqkm)Block 12A10km

Resource estimates are gross best estimates of “Prospective” resources from a Third Party Independent Resource Assessment, except when noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Ekosowan- Spud mid 2014Best-Estimate Gross Resources:Prospective : 153 MMBO

Ekales-Twiga-Agete-Etom ProspectsEtom North

Etom NorthwestBest-Estimate Gross

Resources81 MMBOCOS: 29%

Best-Estimate Gross Resources234 MMBO

COS: 21-25%

Etom EastEtom

Enlarged Map

Kenya

Etom ComplexBest-Estimate

Gross Resources

Etom EastBest-Estimate

Gross Resources42 MMBO

COS: 21-25%

Ewoi

Agete

Twiga South

Ekales

Etuko

Loperot Gross Resources467 MMBO

COS: 25-38%Ekunyuk

Ngamia

Amosing

Lokichar Basin

AgeteBest-Estimate

Gross Resources276 MMBOCOS: 54%

Ekosowan

Block 10BBBlock 12ABlock 13T

10km

Twiga South-1 DiscoveryBest-Estimate Gross Resources:Contingent (2C): 87 MMBOProspective: 132 MMBO, (COS: 64%)

Ekales-1 DiscoveryPRE-DRILL Best-Estimate

Gross Resources: 234 MMBO, 56% COS 5 km

8

Depth Structure Top Auwerwer Reservoirs

COS: Geologic Chance of Success (%)

Resource estimates are gross best estimates of prospective resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Ngamia-Amosing Area

Etom

Enlarged Map

Kenya

Ewoi

Agete

Twiga South

Ekales

Etuko

Loperot

Ngamia-1Ngami WestEkunyuk

Amosing

Lokichar Basin

Ngamia

Ekosowan

Block 10BBBlock 12ABlock 13T

10km

Amosing

Ngamia Discovery & Ngamia West ProspectBest-Estimate Gross Resources:Contingent(2C):180 MMBO

Depth Structure Map: Base Auwerwer

5 kmProspective : 281 MMBO, (COS: 64%)

AmosingCOS: Geologic Chance of Success (%)

9

AmosingBest-Estimate Gross Prospective Resources1 : 172 MMBO, (COS: 34%)

g ( )Resource estimates are gross best estimates of prospective resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Ewoi-Ekunyuk Prospects- The ‘Rift Flank Play’

Depth Structure: Top Lokhone Source Rock

Large Structural Traps Etom

Enlarged Map

Kenyao o e Sou ce oc

5kmPossible Stratigraphic Component

Ewoi

Agete

Twiga South

Ekales

Etuko

Loperot

EwoiBest-Estimate

Gross Resources317 MMBO(COS: 34%)

Etuko-1 Discovery (2013)Best-Estimate Gross Resources:Contingent (2C) : 100 MMBO

Ekunyuk

Amosing

Lokichar Basin

Ngamia

(COS: 34%)

Ekosowan

Block 10BBBlock 12ABlock 13T

10km

EkunyukBest-Estimate

Gross Resources

Loperot-1 Discovery (1992)Best-Estimate Gross Prospective Resources:(Included with Ewoi estimate)

G oss esou ces203 MMBO(COS: 34%)

Resource estimates are gross best estimates of prospective resources from Third Party Independent Resource Assessment except

10COS: Geologic Chance of Success (%)

Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

South Lokichar Basin Building World Class Resource Base

851800

1,000mmbo

Lokichar Basin Upside (3C)

Best Estimate (2C) and Upside (3C) Gross Contingent ResourcesUnrisked prospect average

size increased from 81 mmbo (2012) to 204 mmbo (2013)

400

600Lokichar Basin Best Estimate (2C)

Best Estimate Gross Contingent Resources

36856

0

200

20132012 (6)

Best Estimate Gross Contingent Resources,Gross Risked and Unrisked Prospective Resources

Drilling program to end 2014 accesses 60% to 70%

of South Lokichar Basin prospective resourcesprospective resources

2C resource increase of 557%

since 2012

1 This summary table was prepared by Company management for the convenience of readers.2 Please refer to the Company’s press release dated September 3, 2013 for details of the prospective and contingent resources byprospect and lead, including the geologic chance of success.

3 Ri k d h b l l t d d d b th ft i ki t d l d i di id ll G l i l Ch f3 Risked resources have been calculated and summed by the company after risking prospects and leads individually. Geological Chance of Success (GCOS) varies with each prospect or lead.

4 Net Prospective and Contingent Resources are stated herein in terms of the Company’s net working interest in the properties. Due to the very immature nature of these Resources, net estimates have not been computed as net entitlement volumes under the PSAs/PSCs. In this regard the volumes stated herein will exceed the volumes which will arise to AOC under the terms of the PSAs/PSCs.

5 There is no certainty that any portion of the Prospective Resources will be discovered. If discovered, there is not certainty that the discovery will be commercially viable to produce any portion of the resources.

6 3C resources not reported for 2012 Gaffney Cline & Associates review11

Focus on Opening New Basins

• North Turkana (South Omo Block)S bi W ll d l d iSabisa Well proved source, seal and reservoir

Tutule well should prove up trap and concept

• Chew Bahir Basin (South Omo Block)New seismic identified large inventory of prospects

Prospects supported by direct hydrocarbon indicators

• W t Sh L k T k (10BA)North Turkana Chew Bahir • Western Shore, Lake Turkana (10BA)Latest seismic confirms large prospect inventory

Several interesting prospects drillable onshore

Western Shore • South Kerio Basin (Block 10BB)New seismic identifies Ngamia-style play

AnzaS. Kerio Several prospects & leads

• Anza Basin (Block 9)Drilling campaign to start Q3 2013

12100 km

Drilling campaign to start Q3, 2013

Potential to extend the Sudan play into Kenya

North Turkana Basin (South Omo Block)

• Sabisa-1 TD’d with oil and gas shows

• Possible trap failure

• T lt l t t t th f lt t

Sabisa -1

W Dip LineE

Tultule Prospect

A• Tultule to test upthrown fault-trap

Tertiary Marker 5Depth Structure Map

Tertiary Marker 5

Sabisa NorthBest-Estimate Gross Resources28 MMBO

Limited seismic control

Sabsa-1

Strike Line`

West SabisaBest-Estimate Gross Resources124 MMBO

Strike Line

A

Tertiary MarkerTertiary Marker 5TultuleBest-Estimate Gross Resources18 MMBO

Sabisa-1P&A with shows

BLimited seismic control

13

B3km control

Resource estimates are gross best estimates of prospective resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Chew Bahir Basin (South Omo Block)

Chew Bahir BasinZorit

Wemay NESIR

Jigra

Jigra S.Sila

Best-Estimate Gross Resources

ShimelaBest-Estimate Gross

Resources48 MMBO

Shimela S.

241 MMBO

East BM

100 km

GardimBest-Estimate

Gross Resources89 MMBO

Sorene

• Possible basin-opener S d fi t ll d 2013

CherebaBest-Estimate Gross

Resources166 MMBO

• Spud first well end 2013• Large prospect inventory• DHI’s AVO anomalies

KesamiBest-Estimate

Gross Resources 20 MMBO

Tertiary

Chereba S.

Kesami SEBest-Estimate

G

14

DHI s, AVO anomalies visible over some prospects

Marker 3

Shala 10km

Gross Resources120 MMBOResource estimates are gross best estimates of

prospective resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Chew Bahir Basin Prospects (South Omo Block)Shi l 48 MMBO

CB Marker 3

SW NEShimela: 48 MMBOBest-Estimate Gross Resources Sila: 241 MMBO

Best-Estimate Gross ResourcesNW SEJigra: 5 MMBO Best-Estimate Gross Resources

CB Marker 5

CB Marker 7

CB Marker 3

CB Marker 5

Line CB 09 Line CB 40

CB Marker 7

Line CB-09 Line CB-40

W

Chereba: 166 MMBOBest-Estimate Gross Resources

Kesami: 20MMBO, Kesami SE: 120 MMBOBest-Estimate Gross Resources

JigraE

CB Marker 3ShimelaSila

CB Marker 5

CB Marker 7

Chereba

CB 20 Resource estimates are gross best

15Line CB-20

Kesami

10km

CB-20

Kesami SE

Resource estimates are gross best estimates of prospective resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Newly-Awarded Rift Basin Area PPSA• PPSA award follows 3-year Joint Study

• Extends AOC position in Tertiary Rift BasinsRif B i ARif B i A • Frontier area, no existing seismic data or wells

• Initial exploration program includes 37,000 sqkm Full Tensor Gradiometry survey (70% complete) and 400km of

Rift Basin AreaRift Basin Area42,519 sq km

Tensor Gradiometry survey (70% complete) and 400km of 2D seismic

50km

Tar reported lalong

shoreline

Multiple oil slicks identified on landsat High Resolution

Free Air Gravity

16

y

• Acquired block-wide high resolution airborne gravity & magnetics in 2011

50km

Lake Turkana Western Shore Prospects (Block 10BA)

• 1,350 km of new onshore and marine seismic significantlmarine seismic significantly increased prospect inventory

S i i i iti t t d• Seismic acquisition concentrated along western shore

Kiboko• Large prospects, different play

types, drillable from land

Kiboko

Shaba

Kifaru

• Uncertain stratigraphy between sub-basins

Samaki Lake Turkana

• ‘Bright spots’ seen in new offshore seismic

17

• Spud first well, mid 201410 km

Lake Turkana Western Shore Prospects (10BA)Line 2012-08 Kifaru

Mrkr 5

Shaba

Western Shore

Mrkr 5

Plio. Volcanic

KibokoBest-Estimate

Gross Resources106 MMBO

Shore

3 kmShaba

Best-Estimate Gross Resources

19 MMBOLake

TurkanaLine 2012-32-TZ

Samaki (projected)

Marine OnshoreLine 2012-08Kifaru

KifaruBest-Estimate

Gross Resources333 MMBO

Flat Spots Line 2012-32TZ

Samaki(new, from recent

seismic)Plio. Mrkr

Resource estimates are gross best

5 kmPlio. Volc

18

estimates of prospective resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

South Kerio Prospects (Block 10BB)

S Kerio D

Tertiary Marker 2

New prospects from ongoing seismic program

Estimated prospective

S. Kerio C

S. Kerio DEstimated prospective resources in the 50-100 MMBO class, pending CPR audit

South Kerio

S. Kerio B100 km

• Possible basin-opener • Ngamia-type trapsg yp p• Try to confirm extension of Lokhone source rocks• Spud first well, mid 2014

S. Kerio A

Resource estimates are gross best estimates of prospective resources from Third Party Independent Resource Assessment

19

5km

resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Anza Graben, Block 9: Extension of the Sudan Play

• Cretaceous Basin on trend with South Sudan with over 6 billion barrels of oil discovered along trend

• Play concept confirmed at Paipai wellNEBahasi-1SW

• Drill Bahasi and Sala back-to-back, both with large resource potential

• D illi i 3 d 2013

Tertiary Mrkr1

Tertiary Play

• Drilling to commence in 3rd quarter 2013

• AOC Operates (50% WI), Marathon (50%)Tertiary-

Cretaceous Unconformity

Tertiary Mrkr2

Paipai-1

Sala:Best Estimate

Unconformity

SW NESala-1

BasementAwaiting Test:

185 BCF (or possible light oil)Best-Estimate Gross Resources

Extension of Sirius oil-prone sub-basin into Kaisut sub-basin

Surface volcanics

Ndovu

Best-Estimate Gross Resources

402 MMBOBlock 9Block 9

Tert. Marker

Bogal 1 Discovery:Best-Estimate Gross

Resources

Bahasi:Best-Estimate

Gross Resources320 MMBO

L C t

L. Tertiary

20

1.88 TCFG

* Some prospects renamed to reflect local designations

L. Cretaceous

BasementResource estimates are gross best estimates of prospective resources from Third Party Independent Resource Assessment except where noted as “Contingent”. Please refer to Prospective and Contingent Resources slide detailing specific contingencies relating to the classification of resources and cautionary statements.

Basin Opening Strategy 2013/2014

New Basin De-Risking ScheduleGross Best Estimate Unrisked Prospective Resources

mmbo

New Basin De-RiskingBest Estimate Net Unrisked & Risked Prospective Resources

Q4 1H 2H 2015+

8,012

7 000

8,000

9,000mmbo

Net Unrisked Best Estimate Prospective ResourcesNet Risked Best Estimate Prospective Resources

2013 2014 2014 2015+

5,696

5,000

6,000

7,000 p

2,000

3,000

4,000

522 690

0

1,000

2013/14 Program Total Prospective Resources

1 This summary table was prepared by Company management for the convenience of readers.2 Please refer to the Company’s press release dated September 3, 2013 for details of the prospective and contingent resources byprospect and lead, including the geologic chance of success.

3 Risked resources have been calculated and summed by the company after risking prospects and leads individually. Geological Chance of

21

y p y g p p y gSuccess (GCOS) varies with each prospect or lead.

4 Net Prospective and Contingent Resources are stated herein in terms of the Company’s net working interest in the properties. Due to the very immature nature of these Resources, net estimates have not been computed as net entitlement volumes under the PSAs/PSCs. In this regard the volumes stated herein will exceed the volumes which will arise to AOC under the terms of the PSAs/PSCs.

5 There is no certainty that any portion of the Prospective Resources will be discovered. If discovered, there is not certainty that the discovery will be commercially viable to produce any portion of the resources.

World Class Development Project

• Ngamia, Twiga South and Etuko discoveries prove prolific light oil South Lokichar basin prove prolific light oil South Lokichar basin with significant running room

• South Lokichar Basin exceeds threshold volumes for developmentvolumes for development

• Kenyan & Ugandan Presidents agree joint export pipeline*

• Concept work on pipeline and offshore loading complete

• Expect to agree pipeline cooperation• Expect to agree pipeline cooperation agreement between Kenyan & Ugandan Joint Ventures imminently

P FEED i i i i li d• Pre-FEED activities on pipeline expected to start imminently

22

22

*Tullow public disclosure

What you will see by end 2014

2013 1H 2014 2H 2014

Basin OpenersTultule Bahasi Sala Shimela S. Kerio W. Turkana

EtomNgamia W

Gardim

Lokichar Drill OutAgete EkunyukEwoiAmosing Ekosowan

Lokichar Appraisal Etuko-2 Twiga-2 Twiga-3 Ngamia-2 Ngamia-3 Ngamia-4 Ekales-2

EWT

LokicharDevelopment

Gov’t Kenya Pipeline tender & Pre-FEED

Long-term Development Plan Definition

• Drill 5 Basin Openers• Drill all key Lokichar Prospects

23

Drill all key Lokichar Prospects• Fully appraise Ngamia and Twiga• Define development way forward

AOI Corporate Summary

• Funding

$450MM equity issuance completed Oct 2013• $450MM equity issuance completed Oct-2013

• Funding in place through mid-2015

• Expect to enter 2014 with cash in excess of $500MM

63.0 2013 Forecast O&G Expenditures (gross): $567MM

$500MM

• $43.5MM Marathon farmout carry – dedicated to Block 9, Block 12 and Rift Basin Area

• Drilling focused 2013 exploration budget:403.8

99.9 Drilling

Seismic

Other• Drilling: 74%

• Seismic/FTG: 14%

• Other: 12%

Other

2013 Forecast O&G Expenditures (net): $209MM• Other: 12%

• Indicative 2014 net budget: $300MM - $330MM

• Drilling focused with 6 rigs operational 29.1 25.0

Drilling

p ( ) $

• Capital Structure

• 309.5MM Shares

• 13.4MM options

155.7 Seismic

Other

24

• Nil warrants

• Nil debt24

A History of Value Creation

Company 2002 Recent NotesCompany 2002 Recent Notes

Tanganyika $0.55/share$13.5 million MC

$31.50/share$1.9 billion MC

Sold to Sinopec 2008

Valkyries $0.45/share $16.00/share Sold to Lundin Petroleum 2006y $ /$4 million MC

$ /$750 million MC

Red Back $1.35/share (2000)$45.4 million MC

$30.50/share$8.98 billion MC

Sold to Kinross in 2010

di l $ / h $ / hLundin Petroleum U $0.41/shareU $101 million MC

$23/share$6.9 billion MC+ Enquest spin off US $1.5 billion MC

Active

BlackPearl $0.25/share$2.1 million MC

$2.18/share$645 million MC

Active

ShaMaran $0.175 (2003)$6.7 million MC

$0.46/share$377 million MC

Active

9 Year value increase: $173MM => $21 BillionAverage share price increase: 32x

25

Average share price increase: 32x

Corporate Social Responsibility Commitment

Africa Oil is committed to addressing the challenge of

Risk Management and Value Creation

sustainability - delivering value to our shareholders, while providing economic and social benefits to impacted communities and minimizing our environmental footprint.

•To create a working environment such that we cause no harm to people, and where we minimize our impact on the environment.

•To create a secure and safe working environment for our peopleTo create a secure and safe working environment for our people and assets

•To conduct our business in an honest and ethical manner.

•To enter into dialogue and engagement with key stakeholders, conducted in the spirit of transparency and good faith.

•To deliver tangible and sustainable benefits that contribute to theTo deliver tangible and sustainable benefits that contribute to the social and economic well being of citizens in our host countries.

•To support the development of financial transparency and good governance mechanisms

26

governance mechanisms.

•To support and protect internationally recognized human rights.

Opportunity Summary

• Africa Oil has the best onshore acreage position in East Africa and• Africa Oil has the best onshore acreage position in East Africa, and perhaps the largest upside portfolio in the world

• The Ngamia, Twiga, Etuko and Ekales discoveries have significantly g g g yde-risked the South Lokichar Basin – expect very high future success rate

Th C tl h 5 ti i d i f• The Company currently has 5 active rigs and are in process of mobilizing 2 additional lightweight rigs to Lokichar Basin with at least 20 wells planned in 2014

• New basin opening wells have chance for high impact growth and step change in share valuation

• Research coverage from 25 analysts with an average target price of $12.55/share

27

AOI has a Strong Management Team

Keith Hill, President and CEOMr. Hill has over 25 years experience in the oil industry including international new venture management and senior exploration positions at Occidental Petroleum and Shell Oil Company. His education includes a Master of Science degree in Geology and Bachelor of Science degree in Geophysics from Michigan State University as well as an MBA from the University of St. Thomas in Houston. Prior to his involvement with Africa Oil, Mr. Hill was President and CEO of Valkyries where he led the company through rapid growth and ultimately a highly successful $700 million takeover by Lundin Petroleum. In addition, Mr. Hill was one of the founding directors of Tanganyika Oil which was recently the subjectultimately a highly successful $700 million takeover by Lundin Petroleum. In addition, Mr. Hill was one of the founding directors of Tanganyika Oil which was recently the subject of a $2 billion takeover by Sinopec International Petroleum.

Ian Gibbs, CFOIan Gibbs is a Canadian Chartered Accountant and a graduate of the University of Calgary where he obtained a bachelor of commerce degree. Ian Gibbs has held a variety of prominent positions within the Lundin Group of Companies; most recently as CFO of Tanganyika Oil Company Ltd. where he played a pivotal role in the recent $2 billion acquisition by Sinopec International Petroleum Prior to Tanganyika Mr Gibbs was CFO of Valkyries Petroleum Corp which was the subject of a $700million takeoveracquisition by Sinopec International Petroleum . Prior to Tanganyika, Mr. Gibbs was CFO of Valkyries Petroleum Corp which was the subject of a $700 million takeover.

Nick Walker, COOMr. Walker has 27 years of industry experience including 17 years with Talisman Energy Inc. where he served as Executive Vice‐President of International Operations West as well as country manager positions in the UK and Malaysia/Vietnam. He started his career as a petroleum engineer with BP plc. and also worked in senior management positions at Bow Valley Energy Inc. He previously served on the Board of Oil & Gas UK, the trade association representing the UK oil and gas business. His education includes a Bachelor of Science Degree in Mining Engineering from Imperial College in London a Master of Science Degree in Computing Science from University College in London and an MBA fromScience Degree in Mining Engineering from Imperial College in London, a Master of Science Degree in Computing Science from University College in London and an MBA from City University Business School, also in London.

James Phillips, VP Business DevelopmentBefore joining Africa Oil, Mr. Phillips was Vice President Exploration‐Africa and Middle East for Lundin Petroleum AB where he played a pivotal role in securing the majority of Africa Oil’s current portfolio. Mr. Phillips is a graduate of the University of California, Berkeley and San Diego State University where he obtained BS and MS degrees, both in Geology He has over 25 years of experience in the oil industry including senior positions with Shell Oil company and Occidental including heading up Oxy’s Africanboth in Geology. He has over 25 years of experience in the oil industry including senior positions with Shell Oil company and Occidental including heading up Oxy s African exploration ventures.

Paul Martinez, VP ExplorationDr. Martinez, most recently Director of International Business Development with Occidental Petroleum Corporation, has over 21 years of domestic US and international senior management experience in oil and gas exploration and development, including projects in the Texas Gulf Coast, Permian Basin, Rockies, Latin America, Africa, Middle East, and Russia He has held overseas management positions for Oxy in Libya Oman and Peru Dr Martinez holds a doctorate in petroleum geology from Stanford University and aRussia. He has held overseas management positions for Oxy in Libya, Oman and Peru. Dr. Martinez holds a doctorate in petroleum geology from Stanford University and a Bachelor of Science degree in geology from the University of Texas at Austin. Dr. Martinez is based in the Africa Oil Calgary technical office and is responsible for all geological and geophysical activities of the Company.

Alex Budden, VP External RelationsBefore joining Africa Oil Alex Budden served as a Diplomat for the British Foreign & Commonwealth Office for 21 years. His international experience has seen him serve in Africa,

28

Asia, the Middle East, Russia, the Balkans and North America. Throughout his career he has focused on international security, conflict, governance, human rights, energy and environment issues and specializes in government and security relations, complex stakeholder management and strategic communications work.

Cautionary Statements

This document has been prepared and issued by and is the sole responsibility of Africa Oil Corp. (the “Company”) and its subsidiaries. It comprises the written materials for a t ti t i t d/ i d t f i l i th C ’ b i ti iti B tt di thi t ti d/ ti f thi d tpresentation to investors and/or industry professionals concerning the Company’s business activities. By attending this presentation and/or accepting a copy of this document,

you agree to be bound by the following conditions and will be taken to have represented, warranted and undertaken that you have agreed to the following conditions.

This presentation may not be copied, published, distributed or transmitted. The document is being supplied to you solely for your information and for use at the Company’s presentation to investors and/or industry professionals concerning the Company’s business activities. It is not an offer or invitation to subscribe for or purchase any securities and nothing contained herein shall form the basis of any contract or commitment whatsoever This presentation does not constitute or form part of any offer or invitation to whatsoever. sell or issue, or any solicitation of any offer to purchase or subscribe for, any shares in the Company in any jurisdiction nor shall it or any part of it nor the fact of it di t ib ti f th b i f b li d i ti ith t t it t i t t d i i i l ti th t d it tit t d tiits distribution form the basis of, or be relied on in connection with, any contract commitment or investment decision in relation thereto nor does it constitute a recommendation regarding the securities of the Company. The information contained in this presentation may not be used for any other purposes.

This update contains certain forward looking information that reflect the current views and/ or expectations of management of the Company with respect to its performance, business and future events including statements with respect to financings and the Company’s plans for growth and expansion. Such information is subject to a number of risks, uncertainties and assumptions, which may cause actual results to be materially different from those expressed or implied including the risk that the Company is unable to obtain required financing and risks and uncertainties inherent in oil exploration and development activities. Readers are cautioned that the assumptions used in the

ti f h i f ti h k t i f il d d h i l d t th C ’ bilit t l d l d d t t d il dpreparation of such information, such as market prices for oil and gas and chemical products, the Company’s ability to explore, develop, produce and transport crude oil and natural gas to markets and the results of exploration and development drilling and related activities, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, undue reliance should not be placed on forward-looking information. The Company assumes no future obligation to update these forward looking information except as required by applicable securities laws.

Certain data in this presentation was obtained from various external data sources, and the Company has not verified such data with independent sources. Accordingly, no representation or warranty, express or implied, is made and no reliance should be placed, on the fairness, accuracy, correctness, completeness or reliability of that data, and

h d t i l i k d t i ti d i bj t t h b d i f tsuch data involves risks and uncertainties and is subject to change based on various factors.

No reliance may be placed for any purposes whatsoever on the information contained in this presentation or on its completeness. The Company and its members, directors, officers and employees are under no obligation to update or keep current information contained in this presentation, to correct any inaccuracies which may become apparent, or to publicly announce the result of any revision to the statements made herein except where they would be required to do so under applicable law, and any opinions expressed in them are subject to change without notice, whether as a result of new information or future events. No representation or warranty, express or implied, is given by the Company or any of its subsidiaries undertakings or affiliates or directors, officers or any other person as to the fairness, accuracy, correctness, completeness or reliability

f th i f ti i i t i d i thi t ti h th i d d tl ifi d h i f ti d li l th ill b t l i kof the information or opinions contained in this presentation, nor have they independently verified such information, and any reliance you place thereon will be at your sole risk. Without prejudice to the foregoing, no liability whatsoever (in negligence or otherwise) for any loss howsoever arising, directly or indirectly, from any use of this presentation or its contents or otherwise arising in connection therewith is accepted by any such person in relation to such information.

For additional details on the Company, please see the Company’s profile at www.sedar.com.

29

Prospective and Contingent ResourcesThere is no certainty that any discovered resources referred to in this presentation will be commercially viable to produce. There is no certainty that any portion of the undiscovered resources will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of the resources.

Risks associated with discovering oil:The estimation of prospective resource volumes for high-risk and poorly calibrated basins can be subject to large variation from the introduction of new information. The estimates presented herein are based on all of the information available at the effective date of the resource estimate. New data or information is likely to have a material effect on the resource assessment values. Since the effective date of the resource estimates provided, the Company has continued to actively explore, with multiple 2D seismic crews operational and several exploration wells drilled. p p y y p p p pWhile discoveries have been made at Ngamia-1, Twiga South-1, and Etuko-1 in the Lokichar basin of the Tertiary rift in Kenya, there is no certainty that any additional resources will be discovered. Once discovered, there is no certainty that the discovery will be commercially viable to produce any portion of the resources. Given that most of the resources in the portfolio are in leads that require additional data to fully define their potential it is likely that significant changes to the resource estimates will occur with the incorporation of additional data and information.

Risk Associated with the Estimates:In the event of a discovery, basic reservoir parameters, such as porosity, net hydrocarbon pay thickness, fluid composition and water saturation, may vary from those assumed by the Company’s independent third party resource evaluator affecting the volume of hydrocarbon estimated to be present. Other factors such as the reservoir pressure, density and viscosity of the p y p p y g y p p y yoil and solution gas/oil ratio will affect the volume of oil that can be recovered. Additional reservoir parameters such as permeability, the presence or absence of water drive and the specific mineralogy of the reservoir rock may affect the efficiency of the recovery process. Recovery of the resources may also be affected by well performance, reliability of production and process facilities, the availability and quality of source water for enhanced recovery processes and availability of fuel gas. There is no certainty that certain mineral interests are not affected by ownership considerations that have not yet come to light.

Substantial Capital Requirements:Africa Oil expects to make substantial capital expenditures for exploration, development and production of oil and gas reserves in the future. The Company's ability to access the equity or debt markets may be affected by any prolonged market instability. The inability to access the equity or debt markets for sufficient capital, at acceptable terms and within required time frames, could have a material adverse effect on the Company's financial condition, results of operations and prospects.

Ability to Execute Exploration and Development Program:It may not always be possible for Africa Oil to execute its exploration and development strategies in the manner in which the Company considers optimal. Execution of exploration and development strategies is dependent upon the political and security climate in the host countries where the Company operates and agreement amongst the Company joint venture partners. The Company's exploration and development programs in East Africa may involve the need to obtain approvals from relevant authorities who may require conditions to be satisfied or the exercise of discretion by the relevant authorities. It may not be possible for such conditions to be satisfied.

Absence of a Formal Development Plan including Required Funding:There is no certainty the Company will prepare and have approved a development plan for any portion of the contingent resources or that the Company will be successful in funding any development should such a plan be prepared. General market conditions, the sufficiency of such a development plan and the outlook regarding oil and gas prices are some factors that will influence the availability of funding or the Company’s ability to attract oil and gas industry partners to participate in the project.

Access to Infrastructure:Currently there is limited local infrastructure for the production and distribution of oil and gas in the countries in which Africa Oil operates. Export infrastructure to enable other markets to be accessed has not yet been developed and is contingent on numerous factors including, but not limited to, sufficient reserves being discovered to reach a commercial threshold to justify the construction of export pipelines and agreement amongst various government agencies regulating the transportation and sale of oil and gas. Africa Oil is working with its joint venture partners and government authorities to evaluate the commercial potential and technical feasibility of discoveries made to date and potential future discoveries.

Additional Risks:

30

Additional risks associated with the estimate of the prospective and contingent resources include risks associated with the oil and gas industry generally (i.e. financing; operational risks in exploration, development and production; delays or changes in plans with respect to exploration or development projects or capital expenditures; the uncertainty of estimates and projections related to production; costs and expenses; health, safety, security and environmental risks; and the uncertainty of resource estimates), drilling equipment availability and efficiency, the ability to attract and retain key personnel, the risk of commodity price and foreign exchange rate fluctuations, the uncertainty associated with dealing with governments and obtaining regulatory approvals, and the risk associated with international activities.