“A Land Full of Issuance…”: Fundamentals of Bond … presentations/Bond Proceeds... ·...

41

© PFM 0 “A Land Full of Issuance…”: Fundamentals of Bond Proceeds Investment PFM Asset Management LLC 1200 Fifth Ave. Suite 1220 Seattle, WA 98101 206.264.8900 pfm.com Luke Schneider, CFA, Director Duncan Brown, Senior Managing Consultant

Transcript of “A Land Full of Issuance…”: Fundamentals of Bond … presentations/Bond Proceeds... ·...

© PFM 0

“A Land Full of Issuance…”:Fundamentals of Bond Proceeds Investment

PFM Asset

Management LLC

1200 Fifth Ave.

Suite 1220

Seattle, WA 98101

206.264.8900

pfm.com

Luke Schneider, CFA, Director

Duncan Brown, Senior Managing Consultant

© PFM 1

So…You Have a Big (or Small!) Capital Project to Fund

© PFM 2

Sources of Project Funding

• Develop a conservative yet reliable project construction time table

• Potential sources of funding:

– Accumulated revenues/reserves

– Ongoing revenues during construction period

– Grants and fundraising

– Debt financing:

• Low-interest State loans (PWTF, SRF, CERB, etc.)

• State LOCAL program

• Federal loans (e.g., USDA-RD)

• Bank loans

• Municipal bonds (publicly offered)

© PFM 3

When to Think About Investments?

• Developing “net” costs in Funding Plan

– Critical when determining how much to raise/borrow

• Investment environment may influence number and timing of debt issues

– May also influence debt structure (e.g., relative benefit of “draw-down” feature)

• When bond documents are being drafted

– Definition of “permitted investments”

– Allows time to implement the investment “game plan” at bond closing

© PFM 4

Why Is Having a Strategy Important?

Increases the potential for higher project fund earnings:

• Reduce “net” project costs and/or mitigate unplanned costs

– Potential to unburden cash reserves if the project is not 100% financed

• Act as a set aside for future/potential arbitrage rebate liability

– More likely in other interest rate environments

• Important to consider the upside of higher earnings

– Where/how can we apply excess funds?

© PFM 5

Factors Influencing Plan of Finance & Investment Decisions

• Project draw schedule

• Type of bonds and related funds

– Voted GO bonds vs. all other types

– Debt Service Reserve Fund

– Refunding escrow

• Permitted investments

– State law

– Bond documents

– Investment policies

• Prevailing and expected investment/rate environment

• Anticipated arbitrage rebate requirements

© PFM 6

Investment of Various Accounts in Normal Yield Curve Environment

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Debt Service Reserve Account

Advance Refunding Escrow

Current Refunding Escrow +

Debt Service Fund

Construction Fund + CAPI

Subject to

Arb Rebate

Subject To Yield Restriction

No Rebate Restrictions

Potentially No Rebate Restrictions

Equity Funds

Source: Bloomberg. As of March 31, 2017. See important disclosures at the end of this presentation.

© PFM 7

Factor: Permitted Investments

Investments determined by:

• Federal Tax Code & Arbitrage Rebate Regulations

• State Statutes

• Investment Policies (sometimes)

• Bond Covenants (bond ordinance or resolution)

• Bond Insurer Requirements (sometimes even if new bonds are not insured—right of prior

insurer to consent to document changes)

© PFM 8

Sample Permitted Investments

• Short-term Investments

– Local Government Investment Pools

– Overnight Repurchase Agreements

• Open-market Securities

– U.S. Treasuries & Direct Obligations (e.g., Treasury Notes, Bills)

– Federal Agency Securities (e.g., Fannie Mae & Freddie Mac)

– Commercial Paper (e.g., General Electric Capital Corp., Toyota)

– Corporate Notes

• Structured Investments

– Guaranteed Investment Contracts (GICs)

– Flexible Repurchase Agreements (Flex Repos)

– Forward Delivery Agreements (FDAs)

© PFM 9

Developing an Appropriate Investment Strategy

Active

Management

Passive

Strategies

Regulations

Consider rebate rules

and possible

exceptions

State Law

Compliance with

investment statutes

and policies

Bond Covenants

Compliance with bond

indenture and tax

code elections

Market Conditions

Consider absolute

and relative level of

interest rates

Bond Yield

Evaluate bond yield

relative to current

market rates

Cash Flow

Consider draw

schedule and timing

of cash flows

Liquidity Needs

Provide liquidity to

meet expected and

unforeseeable draws

Yield Restriction

Consider any current

or pending

requirements

Investment

Analysis

© PFM 10

Active Management vs. Passive Strategies

• Ideal for funds with expansive permitted investments or uncertain liquidity needs

• Strive to enhance investment earnings and manage risk via ongoing active portfolio management

– Capitalize on changes in sector yield spreads

– Competitively shop the market for cheap securities while ensuring adequate liquidity

– Manage duration of portfolio based upon relative value of different portions of the yield curve and

changing market conditions

– Adhere to both client and internal credit standards

• Ideal for funds with conservative, straight-forward permitted investments and predictable liquidity

needs

• Options include:

– One-time purchase of fixed-income portfolio

– Structured investments

Passive Strategies

Active Management

© PFM 11

Active Management Process

Relative value analysis

Quantitative security

analysis

Individual issue selection

Issuer credit research

Horizon analysis

Yield/return comparison

Strategies

To Add Value

Sector

allocation

Duration

management

Maturity

distribution

Yield curve

placement

Industry

selection

Issue selection

Portfolio Construction and Management

Employ both strategies to add value to portfolios

Entity

Objectives and

Policies

Macro-economic

conditions

Interest rates and trends

Inflation expectations

Credit outlook

Asset class expectations

Yield curve structure

Economic forecasts

Political factors

Top-down Analysis

Bottom-up Analysis

© PFM 12

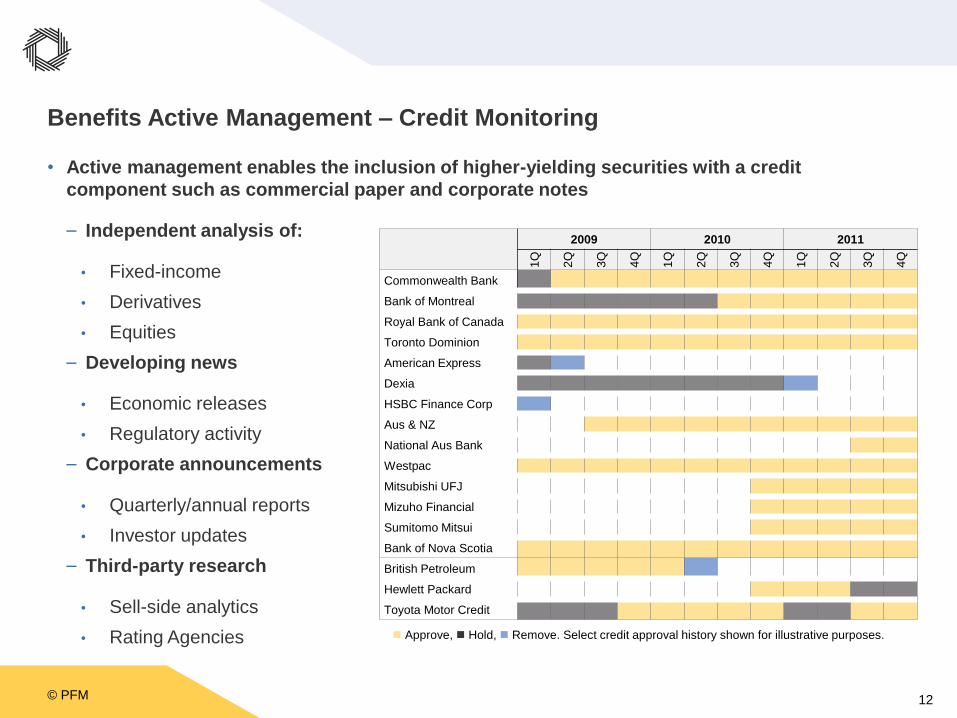

Benefits Active Management – Credit Monitoring

• Active management enables the inclusion of higher-yielding securities with a credit

component such as commercial paper and corporate notes

– Independent analysis of:

• Fixed-income

• Derivatives

• Equities

– Developing news

• Economic releases

• Regulatory activity

– Corporate announcements

• Quarterly/annual reports

• Investor updates

– Third-party research

• Sell-side analytics

• Rating Agencies

2009 2010 2011

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

1Q

2Q

3Q

4Q

Commonwealth Bank

Bank of Montreal

Royal Bank of Canada

Toronto Dominion

American Express

Dexia

HSBC Finance Corp

Aus & NZ

National Aus Bank

Westpac

Mitsubishi UFJ

Mizuho Financial

Sumitomo Mitsui

Bank of Nova Scotia

British Petroleum

Hewlett Packard

Toyota Motor Credit

Approve, Hold, Remove. Select credit approval history shown for illustrative purposes.

© PFM 13

Project Funds

© PFM 14

Project Fund Draw Schedule

• Project proceeds typically spend within 3 years

• Average life is approximately 1–1½ years

Average “life”

Time

“Typical” Project Fund Expenditure

Pattern

© PFM 15

If Draw Schedule Is Uncertain…

• Analyze historical capital spending patterns

• Structure investments around conservative estimates

• Build in additional liquidity

• Invest in securities that can be easily liquidated

• Rebalance based on changes in cash flows and/or market conditions

© PFM 16

If Draw Schedule Is Fairly Certain…

• Ladder investments, targeted to specific cash flow needs

• Monitor periodically to determine if actual expenditures are in line with expected project fund draws

• Rebalance based on changes in cash flows and/or market conditions

© PFM 17

Typical Investments for Project Funds

• Liquidity Vehicle:

– Local Government Investment Pool

• Structured fixed-income portfolio

• Structured investment product/contract

• Combination strategy

© PFM 18

Typical Investments for Project Funds

• Convenient

• Typically overnight liquidity

• Rate dependent

• Inherently taking view that rates will rise during construction period

Time1 yr 2 yr

Projected expenditures

© PFM 19

Portfolio Strategy

• Laddered to match project fund schedule

• Fixed rate of interest for life of the security

• Reinvestment risk if draw schedule is delayed

• Interest rate risk if security must be sold prior to maturity

• Inherently taking view that rates will not rise quickly during construction period

Time1 yr 2 yr

Projected expenditures

Projected maturities

© PFM 20

Yield Environment as of March 31st, 2017

Source: Bloomberg BVAL yield curves for Treasury, Corporate and Commercial Paper, TradeWeb for Federal Agency yields. 3 and 6 month corporate yields

from commercial paper; A-1+ for AA and A-1 for A. As of 03/31/17.

Source: WA LGIP daily yield as of 3/31/17 .http://www.tre.wa.gov..

Maturity WA LGIP TreasuryFederal

AgencyAA Corporate A Corporate

A1/P1

Commercial

Paper

Liquidity 0.82%

3-Month 0.75% 0.87% 0.96% 1.12% 1.08%

6-Month 0.90% 0.95% 1.12% 1.34% 1.30%

1-Year 1.02% 1.09% 1.35% 1.53%

2-Year 1.26% 1.37% 1.65% 1.85%

3-Year 1.49% 1.61% 1.94% 2.14%

5-Year 1.92% 2.02% 2.41% 2.61%

© PFM 21

Summary

• Understand the project expenditure

needs

• Strategize about investment options

during bond issuance process

• Assess current market environment

• Implement strategy

• Monitor proceeds throughout the life

of the project and restructure, if

needed

© PFM 22

Refunding Escrows

© PFM 23

Refunding Escrow Securities – “SLGS”

• SLGS = “State and Local Government Series” securities issued by the U.S. Treasury, commonly used in refunding escrows

• SLGS are subscribed for, not competitively procured; can be custom-tailored for particular refunding bond issues

• Availability of SLGS Program is based on the government’s borrowing capability—debt ceiling debate

• SLGS Program was suspended on March 15, 2017

P R E V I O U S S L G S S U S P E N S I O N S

May 15, 2002 – July 8, 2002 54 days

February 19, 2003 – May 27, 2003 97 days

October 19, 2004 – November 22, 2004 34 days

February 16, 2006 – March 17, 2006 29 days

September 27, 2007 – September 28, 2007 24 hours

May 6, 2011 – August 2, 2011 88 days

December 28, 2012 – February 5, 2013 40 days

May 17, 2013 – October 17, 2013 152 days

February 7, 2014 – February 14, 2014 7 days

March 13, 2015 – November 3, 2015 235 days

March 15, 2017 – ?????????????? ??????

© PFM 24

Considerations for Refunding Bonds

• So long as the SLGS window is closed, issuers contemplating refunding bonds will need to

consider alternative approaches to funding the escrow

• Permissible escrow securities are typically governed by prior bond documents, potentially

including bond insurance agreements

• Cash

– No interest rate benefit to issuer—high “negative arbitrage”

– Tax concerns for advance refunding transactions

• Open-market securities (“OMS”), typically Treasuries

– Generally higher-yielding than SLGS

– Must be obtained through specific bidding process; availability may be a concern for smaller

issuers / transactions

• Another approach: economic defeasance, with proceeds invested in the LGIP

– LGIP generally not a permitted escrow security, so both refunding and refunded bonds would

be legally outstanding at the same time

© PFM 25

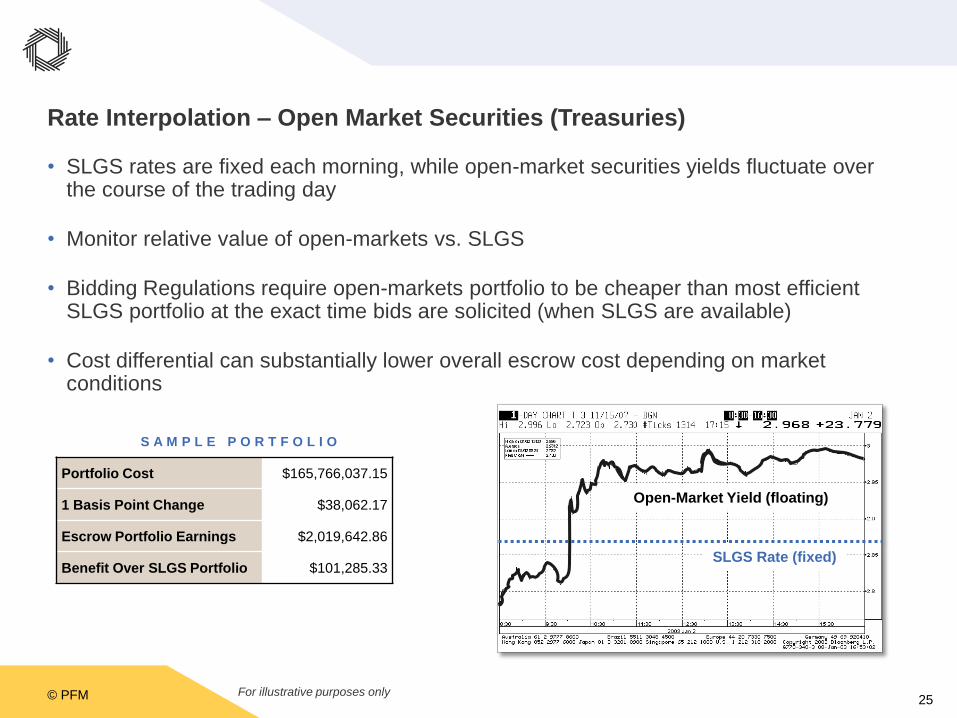

Rate Interpolation – Open Market Securities (Treasuries)

• SLGS rates are fixed each morning, while open-market securities yields fluctuate over the course of the trading day

• Monitor relative value of open-markets vs. SLGS

• Bidding Regulations require open-markets portfolio to be cheaper than most efficient SLGS portfolio at the exact time bids are solicited (when SLGS are available)

• Cost differential can substantially lower overall escrow cost depending on market conditions

For illustrative purposes only

Portfolio Cost $165,766,037.15

1 Basis Point Change $38,062.17

Escrow Portfolio Earnings $2,019,642.86

Benefit Over SLGS Portfolio $101,285.33

S A M P L E P O R T F O L I O

SLGS Rate (fixed)

Open-Market Yield (floating)

© PFM 26

U.S. Government Sponsored Enterprises (“Federal Agencies”)

• Various spreads to Treasuries depending on location on the yield curve

• Are not full faith and credit obligations of the U.S. Government

• Supply continues to decrease as balance sheets are downsized

• Finding large blocks of Federal Agencies at favorable yields can be difficult, if not impossible

G S E s

Government Sponsored Enterprises (“GSEs”), often referred to as “Federal

Agencies,” include debt securities of:

• Fannie Mae (FNMA)

• Freddie Mac (FHLMC)

• Federal Home Loan Bank System (FHLB)

• Federal Farm Credit System (FFCB)

© PFM 27

U.S. Government Guaranteed Securities

• Supply decreasing, in large part, because of purchases for defeasance escrows

• Can be 5 to 20 basis points cheaper than comparable T-STRIPS or T-Notes

• Good match for fixed-liability portfolios (i.e., non-trading accounts such as escrows)

• Liquidity and bid/ask spread not a prominent concern

R E F C O R P s

Resolution Funding Corporation Interest STRIPS

A I D B o n d s

Agency for International Development Bonds

© PFM 28

Capturing Value with Open-Market Securities

• Seldom, if ever, does one broker win all securities

• Security-by-security trades often beat “all-or-none” bidding

– Captures highest yield and establish fair market value on each security

– Ability to reject individual securities if they do not produce savings v. SLGS (if available)

S E C U R I T Y M A T U R I T Y

T O T A L C O S T

B R O K E R # 1 B R O K E R # 2 B R O K E R # 3 B R O K E R # 4 B R O K E R # 5

TSTRIPS-I 11/15/2013 $5,919,228.04 PASS $5,914,781.40 $5,914,788.22 $5,910,143.80

RSTRIPS-I 10/15/2018 $5,376,921.60 PASS $5,364,998.40 $5,375,420.16 $5,351,485.44

RSTRIPS-I 4/15/2019 PASS PASS $429,125.76 $431,313.08 $427,334.80

RSTRIPS-I 10/15/2019 $5,198,955.00 PASS $5,116,736.85 $5,133,125.85 $5,135,311.05

RSTRIPS-I 4/15/2020 PASS PASS $274,886.65 $284,001.90 $282,668.70

RSTRIPS-I 10/15/2020 $5,056,662.00 PASS $4,970,567.16 $4,941,712.23 $5,018,220.09

RSTRIPS-I 4/15/2021 PASS PASS $133,237.00 $138,426.60 $136,840.60

RSTRIPS-I 10/15/2021 $4,906,075.00 PASS $4,840,498.75 $5,056,851.80 $5,020,906.30

DEALER LOT TOTAL $26,457,841.64 - $27,044,831.97 $27,275,639.84 $27,282,910.78

Difference between Best Dealer Lot: N/A N/A $(48,796.45) $(279,604.32) $(286,875.26)

T O T A L C O S TH I G H / L O W

C O S T D I F F E R E N T I A L

A V G . / L O W

C O S T D I F F E R E N T I A L

B E S T D E A L E R / A C T .

C O S T D I F F E R E N T I A L

$26,996,035.52 $466,324 $230,757 $48,796

S A M P L E S E C U R I T Y - B Y - S E C U R I T Y P R O C U R E M E N T R E S U L T S

© PFM 29

Reserve Funds

© PFM 30

Comparison of Operating and Reserve Funds

OPERATING FUNDS RESERVE FUNDS

Market, Credit, and

Tracking Error

Market, Credit, and

Replenishment

Relative

(Beat the benchmark)

Absolute

(Avoid negative returns)

Relatively Static

(Percentage of benchmark)

Dynamic

(Unconstrained)

RETURN TARGET

MEASURES OF RISK

DURATION TARGET

Investment Policy

Liquidity Needs

Investment Policy

Liquidity Needs

Valuation Methodology

CONSTRAINTS

© PFM 31

Reserve Fund Investment Considerations

Investment Decision Factor Considerations

Market Outlook Does the strategy account for the interest rate outlook?

Risk ManagementIs interest rate risk exposure based on the investment

valuation methodology and frequency?

Replenishment RequirementsIf investment values decline, must the Reserve Fund be

replenished?

Opportunity CostsAre there yield enhancement opportunities within your risk

management parameters?

Arbitrage Rebate ComplianceWere rebate complexities and liability expectations

considered?

Accounting Method Is the DSRF a commingled fund or in separate accounts?

© PFM 32

Strategy Development – Risk Tolerance

• Strategy is always viewed within the context of:

– Valuation requirements

– Likelihood that reserve will need to be accessed due to debt service fund deficiency

– Entity's willingness or ability to replenish any shortfalls

Valuation at cost

Valuation at market with

buffer

Annual valuation at market

Semi-annual valuation at market

Monthly/ quarterly valuation at market

just past valuation upcoming valuation

+ –Portfolio’s ability to take interest risk

© PFM 33

Breakeven Analysis

• Forward curves used to determine economic indifference between various investment

horizons

5-year Initial Investment vs. 2-year Interim with 3-Year Breakeven

5 years

2 years 3 years

1.85%

1.20% 2.36%

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

0 1 2 3 4 5

Net

Inte

rest

Earn

ings

Investment Horizon, Years

5-year Investment

2-year Interim

3-year Breakeven

Rates as of January 6, 2017.

© PFM 34

Sensitivity Analysis

• It is important to thoroughly evaluate the impact of interest rate changes and design

strategies to mitigate interest rate risk

– The target duration is developed to protect the portfolio against the impact of rising

rates while seeking higher yields available from longer maturities

• Short time to valuation date warrants conservative duration positioning with extension

trades once the valuation occurs

2-year TreasuryYield of 1.203% / Duration of 1.95 (as of January 6, 2017)

10-year TreasuryYield of 2.434% / Duration of 8.94 (as of January 6, 2017)

Change in Interest

RatesMarket Value

Change in Market

Value

Change in Interest

RatesMarket Value

Change in Market

Value

-1.0% $ 10,196,534.49 $ 196,534.49 -1.0% $ 10,928,451.85 $ 928,451.85

-0.5% $ 10,097,663.54 $ 97,663.54 -0.5% $ 10,452,701.63 $ 452,701.63

0.0% $ 10,000,000.00 $ - 0.0% $ 10,000,000.00 $ -

0.5% $ 9,903,526.14 $ (96,473.86) 0.5% $ 9,569,161.43 $ (430,838.57)

1.0% $ 9,808,224.56 $ (191,775.44) 1.0% $ 9,159,064.40 $ (840,935.60)

© PFM 35

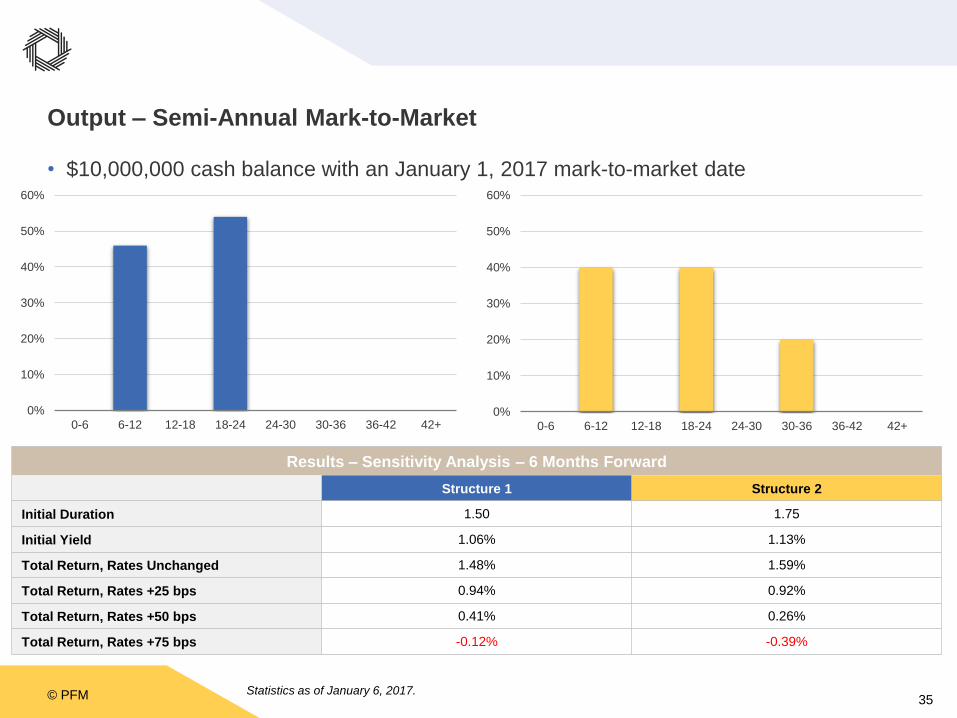

Output – Semi-Annual Mark-to-Market

• $10,000,000 cash balance with an January 1, 2017 mark-to-market date

Statistics as of January 6, 2017.

Results – Sensitivity Analysis – 6 Months Forward

Structure 1 Structure 2

Initial Duration 1.50 1.75

Initial Yield 1.06% 1.13%

Total Return, Rates Unchanged 1.48% 1.59%

Total Return, Rates +25 bps 0.94% 0.92%

Total Return, Rates +50 bps 0.41% 0.26%

Total Return, Rates +75 bps -0.12% -0.39%

0%

10%

20%

30%

40%

50%

60%

0-6 6-12 12-18 18-24 24-30 30-36 36-42 42+0%

10%

20%

30%

40%

50%

60%

0-6 6-12 12-18 18-24 24-30 30-36 36-42 42+

© PFM 36

Structured Investments

© PFM 37

Types of Structured Investments

• Uncollateralized Guaranteed Investment Contracts

– Generically referred to as GICs - unsecured pledge to pay principal and interest on investment;

historically provided by insurance companies or banks

• Collateralized Guaranteed Investment Contracts

– Referred to as Collateralized GICs - pledge to repay principal and interest is secured by collateral

posted to a third-party custodian

• Repurchase Agreements

– Referred to as Repo, Flex Repo, Term Repo - agreement to purchase securities and resell back to

counterparty in the future at a guaranteed yield; typically provided by broker-dealers and banks

• Forward Delivery Agreements

– Referred to as Forward Purchase (Purchase and Sale) Agreements, FPAs, FDAs - agreement

stipulating the outright purchase of securities from a counterparty* through time; typically provided by

broker-dealers and banks

*Counterparties (“providers”) vary depending on agreement type

© PFM 38

Comparison of Structured Investment Agreements

FDAGuaranteed Investment

ContractRepurchase Agreement

Security for

InvestmentPurchased securities

Promissory note from

counterparty

Collateral held at 3rd

party custodian

Mechanism for

Interest

Payments

Difference between

purchase price and par

amount of securities

Credited to account Credited to account

Credit Risk

Limited to underlying

deliverables; very low if

UST

Depends on agreement

counterparty

Depends on agreement

counterparty; collateral

reduces concerns subject

to “J”-Risk

Bankruptcy

Considerations

None – clean

bankruptcy opinion is

market standard

Subject to clawback and

bankruptcy stay

Intended to be exempt;

however, clean

bankruptcy opinion not

possible

Other Risks

Mark-to-market risk

(auditors) and

performance risk

Overnight bankruptcy risk

– no collateral

“J”-Risk – interpretation

of structure under

Bankruptcy Code

© PFM 39

Thank You

© PFM 40

Disclosures

This material is based on information obtained from sources generally believed to be

reliable and available to the public; however, PFM Asset Management LLC cannot

guarantee its accuracy, completeness, or suitability. This material is for general information

purposes only and is not intended to provide specific advice or a specific

recommendation. All statements as to what will or may happen under certain

circumstances are based on assumptions, some but not all of which are noted in the

presentation. Assumptions may or may not be proven correct as actual events occur, and

results may depend on events outside of your or our control. Changes in assumptions may

have a material effect on results. Past performance does not necessarily reflect and is not

a guaranty of future results. The information contained in this presentation is not an offer to

purchase or sell any securities.