A GUIDE TO ESTABLISHING AND RUNNING A CLUB … · A GUIDE TO ESTABLISHING AND RUNNING A CLUB FOR...

28

investment clubs A GUIDE TO ESTABLISHING AND RUNNING A CLUB FOR EQUITY INVESTORS IN IRELAND Produced by the Irish Stock Exchange

Transcript of A GUIDE TO ESTABLISHING AND RUNNING A CLUB … · A GUIDE TO ESTABLISHING AND RUNNING A CLUB FOR...

investment clubsA G U I D E T O E S T A B L I S H I N G A N D R U N N I N G

A C L U B F O R E Q U I T Y I N V E S T O R S I N I R E L A N D

Produced by the

I r i s h S t o c k E x c h a n g e

Investment Club for PDF 4/7/00 4:30 pm Page 2

investment clubs

Investment Club for PDF 4/7/00 4:30 pm Page 3

an informative guide to investment clubs

1

contentsIntroduction .................................................................... page 3The Irish Stock Exchange and Investment Clubs;What are the benefits of membership in an Investment Club?;What exactly is an Investment Club?; How does an Investment Club operate?;Agreeing to a subscription level;Registering investments; Managing the finances fairly for members (The Unit Valuation System);What are thesteps to establishing an Investment Club?

Running a Club .............................................................. page 7Investment Clubs and the Law

Tax and accounting issues forInvestment Clubs in Ireland .............................................. page 12Record keeping; Bank records; Stamp duty;Taxation; Capital Gains Tax;Tax return filing;Tax payment dates

Appendix ...................................................................... page 16Rules of the Club; Sample agenda; Sample constitution; Sample declaration of trust

Investment Club for PDF 4/7/00 4:31 pm Page 4

The Irish Stock Exchange acknowledgesthe support and assistance of ProShare in the preparation of this brochure

ProShare is an independent non-profitmaking organisation based in the UnitedKingdom. ProShare’s mission is to promoteresponsible share-based investmentthrough education and research. Theorganisation provides independentinformation and a variety of servicesdesigned to help and encourage bothprivate investors and investment clubs.

ProShareLibrary Chambers13 & 14 Basinghall StreetLondon EC2V 5HU

© The Irish Stock Exchange Ltd. 2000

This brochure is a general guide to the operation of Investment Clubs. The Irish Stock Exchange has ensuredto the best of its ability that theinformation within the brochure iscorrect and applicable to Irish Law.However the Irish Stock Exchange isnot responsible for the performance ofclubs established on the basis of theadvice contained within this brochure.

The Irish Stock Exchange wishes toacknowledge the contribution ofMatheson Ormsby Prentice Solicitorsand Ernst & Young Accountants in thepreparation of this brochure.

The value of investments mayfall as well as rise and pastperformance is not necessarily a guide to future returns.

Investment Club for PDF 4/7/00 4:31 pm Page 5

The Irish Stock Exchange hasproduced this guide to InvestmentClubs to assist people who maybe interested in establishing such a club amongst a group of friends, relations, colleagues or acquaintances.Since the first Investment Club was established (inTexas in 1898), the popularity of the idea has spreadwidely.Within the United States alone there are nowover 40,000 clubs representing a total membership ofover 750,000 people.

There are over 3,000 such clubs in the UnitedKingdom and according to ProShare – an independentorganisation responsible for promoting share basedinvestment in the UK – new clubs are being set up inthe UK at the rate of 100 a month.

Already in Ireland a number of clubs have beenestablished and are operating successfully.The purposeof this guide is to encourage others who may beinterested in the concept and to assist anyone whodecides to organise such a club in their own area.

introductionchapter one

an informative guide to investment clubs

3

Investment Club for PDF 4/7/00 4:32 pm Page 6

The Irish Stock Exchangeand Investment Clubs

The Irish Stock Exchange is responsible for theoperation of the Irish Stock Market and is a strongadvocate of increased share ownership.

In recent years the number of Irish people directlyinvesting in shares has increased dramatically.Theflotation of major companies such as Telecom Eireann(now Eircom plc) and The Irish Permanent (now Irish Life& Permanent plc) has introduced share ownership tohundreds of thousands of Irish people. Others havebeen attracted by the strong performance of equities vis à vis other investment options.

But others have shied away from direct equityinvestment. Perhaps they have been motivated by areluctance to become involved in a process with whichthey are unfamiliar and one which many peopleassume involves considerable complexity.

International experience has shown that InvestmentClubs offer such people an ideal vehicle throughwhich to take their first steps towards share ownership.

What are the benefits of membership in an Investment Club?

It goes without saying that membership of anInvestment Club is not necessary for people to investdirectly in the Irish stock market. But many peoplemay find that they would prefer to become involved inshare investment in association with a group of like-minded people.

There are a number of practical benefits to Club membership.

■ The Club provides a forum in which members candebate the respective merits of different companiesand the wisdom of individual investment choices.

■ It allows members to pool their time and energy in researching different companies or identifyingdifferent opportunities.

■ It establishes a forum to which speakers with a particular knowledge of an industry or a company can be invited in order to broaden the relevant knowledge of members and informparticular decisions.

■ Membership of a club reduces the relativetransaction costs that would normally be associated with share investment.

■ Pooling of investments in a Club allows membersenjoy the advantages of having a stake in a largerportfolio of shares than might be possible for many individual investors.

How does an Investment Club operate?

Obviously the key difference between the operation ofordinary clubs and that of Investment Clubs is thatInvestment Clubs operate to facilitate the investmentof members’ money.

More so than in the case of other clubs therefore, thelifeblood of Investment Clubs is members’ subscriptions.

4

What exactly is an Investment Club?As the name suggests, an Investment Club is a club established by a group of people specificallyfor the purpose of sharing the experience of directly investing in the Stock Market.

Investment Clubs will normally be established by a group of people who are friends, relations,colleagues, or people who already share membership of a sporting or social club. But whateverother interests may bind its members; the purpose of coming together to form an InvestmentClub is to facilitate share investment.

an informative guide to investment clubs

Investment Club for PDF 4/7/00 4:32 pm Page 7

Managing Club Finances

For illustrative purposes, we reproduce herethe Unit Valuation System (UVS) that isrecommended by ProShare to Clubs in the UKas a way of managing finances.

The system operates on a simple formula:

A is the value of the club's net assets.To get thisfigure you add the current value of the sharesowned by the club and the cash in the bank, thentake away the liabilities, i.e. what the club owes.

B is the total number of units bought by all themembers.

C is the current value of each unit.

So, you divide the value of the club's net assetsby the number of units issued to members andthat gives you the current value of a unit.

Let's take an example, your Club has 10members and you decide each memberwill pay an initial lump sum subscriptionof £50 then £20 a month. All themoney will be used to buy shares.

Month 1: Everyone pays £70 so the Clubhas got £700.The UVS is based on £1 soeveryone has 70 units.At its first meeting,the Club decides there's not enough moneyin the kitty to buy a share yet.

Month 2: All members pay in their £20(total £200) and a new member, Sean, joins.He pays his £50 joining sub and his £20 sonow he has 70 units and the originalmembers have 90 units.The Club has £970

in the bank but again, erring on the side ofcaution because they can't decide whichshare to buy, the Club puts off the firstpurchase decision for another month.

Month 3: Now 11 members pay their £20and there is £1,190 in the Club’s kitty.Thefounders have got 110 units each and Seanhas got 90.

The Club buys 500 shares in Somefirm plcat £2 each.This leaves £190 in the bank.(Note:This example does not include brokerscharges which may vary from broker to broker orstamp duty which is imposed by the Government).

Success! Within a week Somefirm plc sharesgo up by 50p from £2 to £2.50.The 500shares are now worth £1,250.There's £190in the bank so the total asset value of theclub is now £1,440. Remember 1,190 unitshave been issued. So divide 1,190 into£1,440 and you come out with £1.21.

Each £1 of a member's subscription is nowworth £1.21.That's a 21% profit! Eachfounder members' share of the portfolio isworth £133.10 (i.e. 110 units) and Sean (whopaid £20 less than the others into the kitty)has a holding totalling £108.90 (i.e. 90 units).

There is one other accountancy issue thatneeds to be explained now.After themonthly revaluation, the new unit value willbe used to calculate the number of units tobe purchased with subscriptions.

Month 4: Each member pays in £20 but itdoes not buy 20 new units. Remember, theunit is more valuable than £1 now. £20 buysunits valued at £1.21 each, so each memberis allocated approximately 16.5 units.

The beauty of the UVS is that it enablesnew members to join the club at any timewithout benefiting (or suffering) from thepast profits (or losses) of the club.

5

an informative guide to investment clubs

Investment Club for PDF 4/7/00 4:32 pm Page 8

an informative guide to investment clubs

6

Agreeing a subscription level

One of the earliest decisions to be taken by membersof a Club is the level of subscription that they arewilling to invest.

In practice most Clubs agree a standard monthlysubscription paid by Direct Debit into a speciallycreated Bank Account. However it is not essential thatall members agree to the same subscription and Clubsshould be able to accommodate different memberssubscribing different amounts.

However it is imperative that in cases where votes aretaken, all members have an equal say – irrespective ofthe value of their individual subscriptions.

The size of subscriptions plays a key role indetermining the size and frequency of investmentsundertaken by the Club.We would suggest, as a rule of thumb, that investment decisions only be takenwhenever the amount involved is in excess of £1,000.

Registering investments

Because the Club will be making investments onbehalf of its members, each Club must decide on ameans of registering its investments.The two mostcommon methods are via club trustees or a nomineecompany operated by the Club's stockbroker.

Managing thefinances fairly for members

Because the business ofthe Club revolvesaround the investment ofits members subscriptions,it is vital that the Clubagrees a system ofaccounting to manage thesubscriptions being paid intothe Club, the investmentsmade through thosesubscriptions and the valuewhich individual members havein the Club.

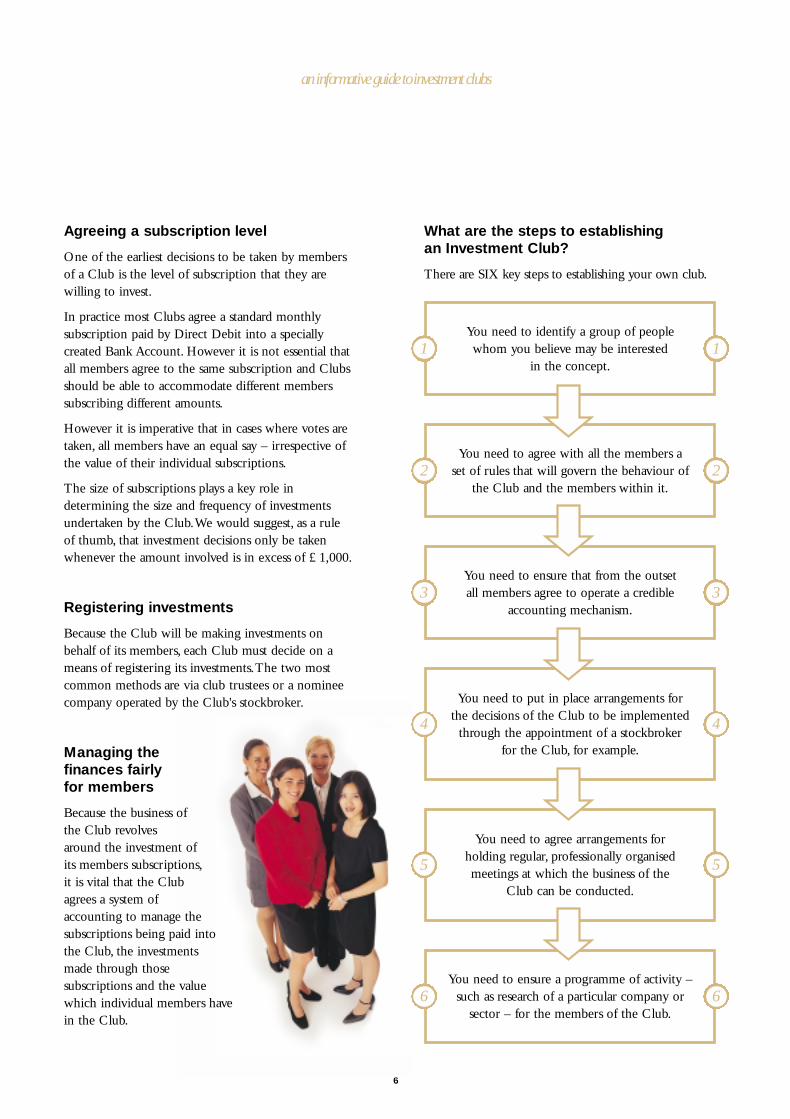

What are the steps to establishingan Investment Club?

There are SIX key steps to establishing your own club.

You need to identify a group of peoplewhom you believe may be interested

in the concept.1 1

You need to agree with all the members aset of rules that will govern the behaviour of

the Club and the members within it.2 2

You need to ensure that from the outsetall members agree to operate a credible

accounting mechanism.3 3

You need to put in place arrangements forthe decisions of the Club to be implemented

through the appointment of a stockbrokerfor the Club, for example.

4 4

You need to ensure a programme of activity –such as research of a particular company or

sector – for the members of the Club.6 6

You need to agree arrangements forholding regular, professionally organisedmeetings at which the business of the

Club can be conducted.

5 5

Investment Club for PDF 4/7/00 4:32 pm Page 9

7

running a clubchapter two

an informative guide to investment clubs

Investment Clubs and the Law

How many members?Legally most investment clubs are organised as generalpartnerships. Simply by adopting the rules andconstitution of the club, the members are effectivelyforming a partnership between themselves.This avoidsthe expense of forming a limited company andeliminates the potential problems of Corporation Taxthat would otherwise be applicable.

The law applicable to general partnerships is mostlycontained in the Partnership Act 1890 and the CompaniesActs 1963 – 1999. Generally, partnerships cannot havemore than 20 members.Whilst the law grants someexceptions these are not available to investment clubs.

A legal partnership does of course carry with it certainresponsibilities based on the principle that everypartner (club member) is jointly responsible for thepartnership’s (club’s) commitments whilst he or she is a

Investment Club for PDF 4/7/00 4:33 pm Page 10

8

an informative guide to investment clubs

LIKE MINDED FRIENDS,POOLING IDEAS, MAKINGDECISIONS... TOGETHER.

Investment Club for PDF 4/7/00 4:34 pm Page 11

9

partner. However in practice this should not be anissue for those clubs which do not borrow funds, tradeon margin or engage in leverage and where prudentsafeguards are included in the rules of the club.

Investment Intermediaries Act 1995 (as amended)The Investment Intermediaries Act 1995 (as amended)(the “IIA”) is wide ranging and covers many areas ofinvestment business.There are severe penalties forbreaching the provisions of the IIA and these applyequally to individuals and bodies such as investmentclubs.The following highlights only a few of theprovisions of the IIA, of which investment clubsshould be aware. If members are in any doubtindependent legal advice should be sought on allaspects of the IIA’s application to the club.

Investment activities regulated by the IIA includegiving investment advice, receiving and transmittingorders in relation to stocks and shares, dealing in stocksand shares for own account, executing orders for stocksand shares, managing portfolios of investments inaccordance with discretionary mandates, administeringcollective investment schemes and acting as manager orcustodian of collective investment schemes.

The setting up and running of an investment clubshould not ordinarily give rise to any requirement forauthorisation under the IIA or the Unit Trusts Act orother collective investment scheme legislation. It isessential if such legislation is not to be applicable, that aclub would be set up and conducted in such a way thatthe members do not constitute a section of the public– so that, as described in this guide, they are a circle offriends, relations, business or social acquaintances, anddo not in any event number more than 20 people –that the members have day to day control over theirinvestments, and that they are not remunerated apartfrom agreed out-of-pocket expenses.

Furthermore clubs must ensure that they do not giveadvice or provide investment business services for a feeto any other person, as this would require authorisation.

If clubs are unsure about this matter, they should referto their legal advisor.

Like all other investors, members of investment clubsare prohibited by law from engaging in insider dealing.

Insider dealing is an offence under Irish law.Anymember who is connected with a company or whowas connected in the past six months and who is inpossession of information that is not generally availableabout that company should disclose this prior to anyinvestment by the club in shares of that company.The club should take legal advice before investing inany company in respect of which a disclosure of thisnature has been made.

Stock broking services

Stockbrokers’ services can be divided into three main categories when referring to the type of service they provide:

EXECUTION-ONLYThe stockbroker can buy and sell shares on behalf ofthe Club and will not give advice on specific shares.The stockbroker takes the order and completes thetransaction, issuing the Club with a contract note.

The main advantage of using an execution-onlystockbroker is that costs are usually lower.This isbecause the stockbroker does not have to research theshare in order to give advice.

ADVISORY The advisory stockbroker can offer advice onparticular shares and sectors to the Club and thisinformation is usually supported by detailed researchand analysis.The charges for an advisory service areusually higher than for an execution-only service.

DISCRETIONARY This is often referred to as portfolio management.Thestockbroker manages the client’s portfolio, buying andselling shares within agreed parameters given by theclient. It is unlikely that this service will be relevant toinvestment clubs.

It is important to ensure that the stockbroker chosenby your investment club has all necessary authorisationsto provide the relevant services to the Club. If you arein any doubt about this you should contact the IrishStock Exchange.

an informative guide to investment clubs

Investment Club for PDF 4/7/00 4:34 pm Page 12

an informative guide to investment clubs

10

Registration of SecuritiesGenerally before a share certificate can be issued, thecompany’s Registrar must enter the holder’s name onthe Share Register.A holding may be entered in thename of an individual or individuals or in the name ofa body corporate i.e. a company. It cannot legally beregistered in the name of a partnership – and in thiscontext an investment club is a partnership.Threepossible solutions are available:

1.The formation of a limited companyThis option is rejected on the grounds of complexityand expense – except where the funds to be investedare very substantial.

2.The use of a nominee companyA second method, and one which is probably thesimplest, is to use a nominee company which is alimited company operated by a reputable organisation(usually a stockbroker) that allows its name to be usedfor the registration of shares.This method is becomingincreasingly popular with Clubs because the broker hasa direct agreement with the Club which specifiesexactly what services are offered and which officials ofthe Club have been appointed to transact Clubbusiness.The broker will also contract with the Clubto provide regular portfolio information and may alsooffer a share information service.This nomineecompany should be authorised with the IIA.

Should brokers wish to operate on behalf ofinvestment clubs, the following should be considered:

■ A formal agreement should be drawn up betweenbroker and Club (signed by all members of the club)

■ The broker should receive and keep a copy of theClub’s constitution

■ The broker should be provided with the names,addresses and telephone numbers of all officers inthe Club.

■ The Club should appoint two representatives(members) to act on its behalf. Only thoserepresentatives are authorised to act on behalf of the Club and both their signatures are required for all documentation.

There are several advantages to this system; paperwork,and thus administration for the Club, is reduced;

dealing charges are usually less; the whole process ofbuying or selling a share is easier and quicker; theproblems of having a trustee who goes on prolongedholidays, leaves the Club or dies are avoided.

Nominees normally charge a fee for their services and,because the shares are all registered in the name of thenominee company, all reports and correspondencefrom the company in which shares are held are sent to the nominee. Clubs must therefore make sure that they are not only informed when dividends are paidbut that they also receive the annual reports and other important correspondence.You should discuss all these points with your chosen stockbroker and spell out exactly what you want at the heart of your relationship.

3. Club members as trusteesSome Clubs choose to appoint two or three membersas trustees and register the Club’s involvements in theirnames.The suggested wording of the recommendedconstitution covers this option and this guide includesan example Declaration of Trust, which the trusteesshould sign.

If a Club wishes to be completely democratic it maywork out a rota of members so that each in turnbecomes the trustee for certain investments. Howeverthis system is complicated and costly particularly as theClub’s portfolio grows and if members leave. It isprobably more simple to appoint two or three "settled"members of long standing and let them act aspermanent trustees for all investments.

As long as the trustees remain members of the Club all is well. But when any of them leaves each of theinvestments registered in that name will have to be re-registered by lodging a stock transfer form with the relevant company registrar. Stamp duty will bepayable and there may be a company registration fee.

If one of the trustees dies, the company registrar willusually accept the death certificate as authority toremove the deceased’s name from the register leavingthe holding in the name(s) of the surviving trustee(s).However, if the Club’s rules call for a successor to be appointed (which they should if the number hasbeen reduced to one), then the holding will have to be re-registered.

Investment Club for PDF 4/7/00 4:34 pm Page 13

an informative guide to investment clubs

Trading units within the ClubThis involves the buying and selling of units within aClub and is an acceptable practice, providing it iscarried out strictly in accordance with the Club’s rules.It can be interesting as well as modestly profitable forthe shrewd member who estimates correctly when thevalue of the Club’s unit value is likely to rise or fall.

11

Investment Club for PDF 4/7/00 4:34 pm Page 14

12

an informative guide to share investment clubs

tax and accounting issues forinvestment clubs in ireland

chapter three

There are no legislative or taxation statutory provisionsgoverning the formation or administration ofInvestment Clubs in Ireland. However, it isrecommended for good house keeping purposes tomaintain adequate records and formalise responsibilitiesto ensure that members’ interests are protected. It isadvisable to reflect these in a written Agreement.

Record KeepingTwo separate records should be maintained, one inrespect of monetary issues and the second in respect ofadministration matters.

Monetary records:A record should be maintained of all;

■ contributions received from Club members

■ bank deposits and balances

■ investments made

■ interest earned

■ dividends received in respect of any share holding

■ administration expenses

■ distributions to members

Investment Club for PDF 4/7/00 4:34 pm Page 15

■ an income and expenditure account

■ costs of buying (including stamp duty) and selling

Administration records:These need not be too detailed but they should at leastrecord the following;

■ name and addresses of members

■ members saving contributions

■ distributions to members

■ dates of investments

■ minutes of meetings

■ details of investment decisions made

■ authorised signatories

■ nominated stockbrokers

Bank AccountsA bank account should be opened to hold andaccumulate the members’ contributions to theInvestment Club.The account may be a current ordeposit account. It is suggested that there are twoauthorised signatories on the account, with bothsignatures being required before funds can be accessed.

In circumstances where the account is interest bearingthe interest is taxable in the hands of the members.This matter will be addressed in more detail underTAXATION.

Stamp DutyA liability to stamp duty will arise on the acquisitionof shares in Irish-registered companies.The positionwith foreign shares should be checked before dealingin them.The current rate of stamp duty is 1% forIrish-registered shares (Year 2000).This liability is inaddition to the cost of the shares and the commissioncharged by stockbrokers who transact the business.

TaxationAlthough an investment club may be a partnership forlegal purposes, the Revenue Commissioners do not

regard the activities of a club as being a partnershipfor tax purposes – on the condition that suchactivities are on a modest scale.This brochure canonly offer general advice on the issue of taxation. It isrecommended that members of investment clubsshould seek professional advice before making anydecisions in relation to this issue.

Income or capital gains earned or realised by the Club is taxable in the hands of the individualmembers.The income and capital gains have to beallocated each tax year to each member on a pro ratabasis in line with their aggregate contribution to theClub after deducting any previous distributions.Brokers commission and stamp duty may be deductedfrom the amount chargeable to capital gains tax -other administration fees cannot.The Club has no tax reporting or payment responsibilities.

Income TaxGenerally the income of the club will consist ofdeposit interest, interest on stock or dividends. Each of these sources are taxable.The method of calculatingthe income tax liability varies with the source.

Deposit InterestAny income earned on an Irish deposit account will be paid after the bank or building society withholdsstandard rate income tax, i.e. D.I.R.T.. Each Clubmember must disclose their share of the deposit intereston their personal tax return.There is no further liabilityto income tax as D.I.R.T. satisfies the income taxliability even for Club members who pay income tax ata rate in excess of the standard rate. However, a liabilityto the Health Contribution at a rate of 2% will arise.

DividendsThe aggregate of any dividend received plus the incometax withheld at source is liable to income tax at themembers top income tax rate.The member is entitledto deduct from any income tax liability their share ofthe tax withheld at source from the gross dividend.

an informative guide to share investment clubs

13

Investment Club for PDF 4/7/00 4:34 pm Page 16

14

an informative guide to share investment clubs

Capital Gains TaxAs with income any gain realised on the disposal ofshares or stock must be apportioned on a pro ratabasis among the Club members. Similarly any lossesrealised must also be apportioned to the members.Any gains or losses must be disclosed on theindividual’s personal tax return. In addition, any sharesor stock acquired by the Club or disposed of by theClub must be disclosed on a pro rata basis on theindividual members personal tax return.

Capital gains:Capital gains are liable to capital gains tax at acurrent rate of 20%. In calculating any chargeablegain, members are entitled to subtract the cost of theshares or stock and broker’s commission and stampduty from the proceeds received. In addition amember is entitled to increase the cost of the sharesor stock investment by inflation (indexation) if theinvestment was held for a period of at least 12months.The Revenue Commissioners publish anannual table of index inflation factors. Finally each

member is entitled to an annual capital gainsexemption of IR£1,000.

Capital losses:Any losses realised by the Club on the disposal ofshares or stock may be set against any chargeablegains.The chargeable gain is after inflation(indexation) relief has been applied, but before theannual exemption is utilised.

Losses have to be used in the first available tax yearin preference to the annual IR£1,000 exemption.Any unused excess losses can be carried forward andused at the first available opportunity against theindividual member’s personal gains or gainapportioned by the Club.

Tax Return FilingEach member must file a personal tax return withtheir Inspector of Taxes no later then 31st January afterthe end of the relevant tax year. In circumstanceswhere a tax return is not filed by the due date asurcharge liability of up to 10% of the tax liability canbe imposed.

Tax Payment DatesIncome tax is due on the 1st November of therelevant tax year.Therefore if the Club earns incomein the tax year ended 5th April 2001 tax on thisincome is due for payment on the 1st November2001.The amount of income tax due on 1stNovember is the lower of

■ 90% of the actual liability for that tax year, or

■ 100% of the liability for the preceding tax year

after deducting any tax credits available such asP.A.Y.E.. Any income tax liability outstanding afterthe tax return has been submitted must be paid nolater than 30th April after the tax return filing date.If tax payments are incorrect or not paid on time, theRevenue Commissioners will charge interest at a rateof 1% per month.

Capital gains tax is due on the 1st November afterthe tax year in which the gains is realised.

Example

IR£

Gross Irish dividend 100

Less withholding tax @ 22% 22 (tax credit)

Actual amount received 78

Taxable 100

Assume 44% taxpayer 44

Less tax credit 22

Income tax due 22

Health contribution due 2 (IR£100 @ 2%)

Net income IR£100 less(22 + 22 + 2 ) = IR£54

Investment Club for PDF 4/7/00 4:34 pm Page 17

an informative guide to share investment clubs

15

SHARING THE RISK, RISINGTO THE CHALLENGE...

ENJOYING THE REWARDS.

Investment Club for PDF 4/7/00 4:35 pm Page 18

16

an informative guide to share investment clubs

appendix

These sample documents are reproduced

with kind permission from ProShare

■ Rules of the Club

■ Sample Agenda

■ Sample Constitution

■ Sample Declaration of Trust

Investment Club for PDF 4/7/00 4:36 pm Page 19

Rules of the ClubThe following set of rules is based on those whichhave proved satisfactory to most investment clubs.

1.THE AFFAIRS OF THE CLUBThe affairs of the Club shall be conducted inaccordance with the letter and spirit of theconstitution laid down by the members.Theconstitution may only be changed by agreement of notless than 75% of current members of the Club.

2. OFFICERSThe affairs of the Club shall be managed by threeofficers - chairperson, honorary secretary andhonorary treasurer - who shall be elected by a simplemajority of members attending the annual generalmeeting of the Club.These officers shall resign at thefollowing annual general meeting but shall be eligiblefor re-election. If an officer should leave the Club, dieor otherwise be unable to continue to carry outhis/her duties, a replacement may be elected at asubsequent ordinary meeting of members. Otherofficers may be elected from time to time to assist thethree main officers.

3. MEETINGSa) In each year there shall be held 11 monthly

meetings and one annual general meeting, at whichall members shall be entitled to be present and tovote on all matters.

b) Dates and venues of meetings may be varied inaccordance with a resolution supported by a simplemajority of those attending a properly constitutedmeeting of the Club. Such resolutions and all othersmust be carried at a meeting where there is aquorum comprising of more than half of thecurrent membership.

c) All members shall be given at least 5 days notice ofdates and venues of meetings.

d) A special general meeting may be convened by notless than three members for the purposes ofresolving special items of Club business subject to awritten request being submitted to the secretarywho will without undue delay then give at least 21days notice to all members.

4. MEMBERSHIPIn accordance with the constitution the membershipof the Club shall not exceed 20 persons at any time.

5. ELECTION OF NEW MEMBERSa) The election of a new member is conditional upon

there being no objection from a member at themeeting at which the application is considered.

b) A prospective member must be proposed andseconded by two existing members at a monthlymeeting of the Club. Subject to acceptance by allmembers attending that meeting, the name andaddress of the prospective member will be includedin the minutes, which will be circulated to allmembers prior to the next monthly meeting.

c) The Club reserves the right to refuse admission toany person without giving a reason.

d) On admission to the Club, a new member will signan agreement (form enclosed with this guide).The new member shall pay the initial lump-sumsubscription (if applicable) and the first month'ssubscription.These sums will purchase for the newmember a number of units calculated according toClub rules and the unit value prevailing at the timeof joining.

6.WITHDRAWAL OF MEMBERSHIPa) A member shall cease to be a member of the Club

if he/she is in contravention of Clause 15 of theconstitution.

b) If a member should die or cease to be a memberfor any reason, the Club shall pay to the member orto the persons entitled by law an amount equal tothe former member's share in the assets of the Clubas defined in Rule 11.

7. INITIAL LUMP-SUM SUBSCRIPTION (Optional)a) All members will pay a joining fee of

£___________________ which will rank on parwith monthly subscriptions in that it will purchasefor that member an appropriate number of unitsaccording to the unit value at the time of joining.

b) This fee may be varied at the Club's annual generalmeeting or at a special general meeting.

an informative guide to share investment clubs

17

Investment Club for PDF 4/7/00 4:36 pm Page 20

8. SUBSCRIPTIONSa) A subscription of £___________________ per

calendar month shall be paid into the club's bank/building society account by all members on orbefore the 1st day of each month by means of astanding order from a bank, building society orsimilar source.

b) Each member's subscription will purchase for thatmember an appropriate number of units accordingto the unit value declared at the monthly meetingpreceding the date when the subscription was paid,subject to club brokerage if such should be in forceat that time.

c) The treasurer shall notify members at their monthlymeeting if any member is in arrears.

d) The monthly subscription and the level of the clubbrokerage may be varied at the club’s annual generalmeeting or at a general special meeting.

9. CAPITAL ACCOUNTa) The club's assets shall be valued monthly by the

treasurer and a report shall be presented at the nextmeeting.The value of investments shall be based on'middle' closing prices recorded in the national mediaor other reliable source of share price information.

b) The treasurer's monthly report shall include as aminimum: the current value of each of the Club'sinvestments; a statement of unpaid accounts and cashin hand on the aforesaid day; the total value of theClub's assets and the current unit value which shallbe determined by dividing the total net asset valueby the total number of units issued to members.

10. MEMBERS' ACCOUNTSAn account shall be kept for each member of the Clubshowing: the total investment made by each memberby means of subscription, initial lump-sum and/oradditional purchases of units; the total of withdrawalsmade by each member who has sold back units to theClub; the total number of units currently held by themember and the current value of his/her holding.

11. MEMBER LEAVING THE CLUBa) Resignations of membership must be submitted in

writing to the chairperson, treasurer or secretarynot less than seven days before the monthlymeeting at which the resignation is to take effect.

b) Members leaving the Club, whether by resignationor as the result of termination of membership underRule 6, shall sell back to the club their entireholding of units.

c) The amount to be paid to a member leaving theClub shall be calculated by multiplying the totalnumber of units held by the member by the unitvalue declared by the treasurer at the Club meetingat which the resignation became effective, subject todeduction of club brokerage if such should be inforce at that time and any legal or other fees incurredby the club in connection with the withdrawal of themember, whether in connection with the liquidationof positions or otherwise.Any surplus cash held tothe member's credit will be added.

d) Payment to the member who has left the Club shallbe made as soon as possible and in any case within90 days of the resignation becoming effective.

12.ADDITIONAL UNITSThe Club may, at its discretion, allow individualmembers to purchase additional units but it isimplicitly understood that every member shall haveequal voting powers on all matters.

13. RUNNING COSTSNo member shall be compensated for providingservices to the Club. Expenses incurred in managingthe Club shall be recorded in the club's cash accountwhich shall be funded from the Club's subscriptionand other income.The treasurer shall maintain a fulland accurate record of all expenditure to submit to theauditors annually.

14. BANKINGa) The Club's bank/building society shall be

determined annually at the annual general meetingbut may be changed by agreement of a majority ofmembers at a special general meeting called inaccordance with Rule 3.

b) All cheques drawn on the Club's account(s) shallrequire any two of three authorised signatures.Where possible one of the signatories of chequesshould be the chairperson. In the event of oneauthorised signatory being unavailable for anextended period, the officers of the Club mayauthorise a further signatory for the period

18

an informative guide to share investment clubs

Investment Club for PDF 4/7/00 4:36 pm Page 21

involved.All income shall be paid direct into theClub's bank/building society account(s) exceptwhere members have approved an arrangementwhereby their stockbroker retains funds from thesale of one or more investments pending thepurchase of other investments.

c) The Club's bank/building society shall be instructednot to grant any overdraft facilities to the Club.

15. BROKERSThe Club's brokers shall be instructed that:

a) Only one or two named officers are authorised tobuy or sell investments on behalf of the Club.

b) No member is authorised to commit the clubbeyond the cash held by the Club.

c) All cheques due to the Club's account are to be made out to the Club's name on non-transferable cheques.

16. COMMITMENTSNo Club member shall make any commitment onbehalf of the Club or commit Club funds withoutwritten authorisation to do so.

17.AMENDMENTS OF RULESThe rules of the Club may be amended or rescindedat a general meeting of the Club subject to agreementby at least 75% of members present.

18. MINUTESMinutes of the Club meetings shall be kept and shallbe available for inspection by any member of the Clubat any reasonable time.

19. DISPUTES.a) Any disputes as to the interpretation of these rulesshall be decided by the chairperson unless notice isproperly served requesting that the matter should beresolved by a special general meeting of Clubmembers.

b) Any disputes relating to the valuation of a member'sshare in the assets of the Club or his/her entitlementto that share shall be decided by a charteredaccountant (to be appointed by the chairperson of theClub) of at least seven years' standing whose writtendecision shall be final. Fees incurred in obtaining thisdecision shall be paid by the party to the disputeagainst whom the decision is made or, in the case of

this not being clear, the fees shall be shared betweenthe Club and the member or ex-member concerned.

20.WINDING UPThe Club shall be would up and all assets dividedamong members (after payment of Club expenses) inaccordance with the number of units held by eachmember if a resolution to that effect is passed by atleast 75% of the members at a special general meetingof the Club.

21.TAX LIABILITYMembership of the Club implies acceptance ofproportional tax liability on income or gains made bythe club in any tax year.

an informative guide to share investment clubs

19

Investment Club for PDF 4/7/00 4:36 pm Page 22

20

an informative guide to share investment clubs

New Members Agreement

Full name of joining member

Address

The above named was nominated for membership of The _____________________________________________

Investment Club at a meeting held on ____________________________________________ 20

and there having been no objection is warmly invited to become a member of the Club by accepting theconstitution, consenting to the rules and paying the specified joining fee and monthly subscriptions inaccordance with the rules.

Signed (Secretary) Date

Declaration by Joining Member

I have received and read the constitution of The _____________________________________________

Investment Club dated ____________________________________________ 20 __________

I agree that the affairs of the Club shall be conducted in accordance with the letter and spirit of the constitutionand I agree to abide by the rules and any amendment thereto made in accordance with Clause _____________of the Rules.

I agree to pay a joining fee of £_________________ which entitles me to a number of units in the Club ascalculated by the honorary treasurer using the same unit price as applied to valuations for existing members forthe relevant month. Thereafter individual valuations will be provided in accordance with the rules.

I agree to pay monthly subscription of £_________________ by standing order into the Club's account.

I will endeavour to attend and participate in the Club meetings and respond to other written reasonablerequests concerning Club business.

Signed Date

Investment Club for PDF 4/7/00 4:36 pm Page 23

an informative guide to share investment clubs

21

The ConstitutionThis is an important document, compiled and signedby the founder members, which spells out the basicprinciples of the Club. It shows the reason why theClub was formed and the broad basis of its operations.All members should read this document and agree withthe principles laid down. On joining, new memberswill agree in writing to abide by the constitution.

Rules about the level of subscription and similar issuesmay be amended from time to time according to thewishes of the members, but serious consideration shouldbe given before altering the terms of the constitution.For this reason most clubs agree that changes to theconstitution may only be made with agreement from avery high proportion of the members, possibly 100%.

Clubs may vary in deciding what matters are includedin the constitution as opposed to being in the rules,but the draft below is suggested as being appropriate.

CONSTITUTION of the

___________________________________________

Investment Club

This agreement is made this _______________ day of

______________________________________ in the

year of 20_____ between the undersigned people asfounder members for the purpose of joint investment instocks, shares, bonds, options, securities and investmentsof a like nature for their mutual benefit and interest.TheClub shall not have the power to borrow money or topurchase or agree to purchase investments involvingleverage.The Club shall not engage in short sales.

1. The first principle of the Club shall be that nomember shall be deprived of his/her equitableshare in the assets of the Club.

2. Members of the Club shall make regularcontributions in such amounts and on such basis as is from time to time agreed or requiredby the rules.

3. Members shall be bound by the rules to bedetermined by members. Such rules may be variedby majority resolution at a properly convened

general meeting but the rules shall not at any timecontravene the principles of this constitution.The constitution cannot be altered without theagreement of 75% of the Club for the time being.

4. The Club shall deal solely with investments onbehalf of its own members and shall neither dealnor advise any persons other than its members in relation to investments of any kind.All itsactivities will be confined to the mutual benefitand interest of its members.

5. Club membership shall be restricted to amaximum of 20 people. New members shall onlybe admitted after being proposed and secondedby two existing members and there being noobjection from any other member of the Club.

6. No member shall assign, pledge, transfer, mortgageor sell any part of his/her interest in the Club toanother member or to anyone else except aspermitted by the authorised procedure for sellingback all or part of his/her interest to the Club itself.

7. No member shall be compensated for servicesrendered to the Club and no member shall bindor obligate the Club or any member of the Club,and in respect of the Club's affairs they shall onlyenter into agreements on the authority of aresolution properly passed by members.

8. The rules shall determine the procedure whereby a member may resign from the Cluband withdraw his/her equitable share of theClub's assets but the maximum period to elapsebetween the date of resignation and the date of full repayment shall not exceed 90 days.

9. The Club shall hold a general meeting once inevery calendar year as its annual generalmeeting provided that every annual generalmeeting shall not be more than 15 months afterthe preceding annual general meeting.TheClub’s first annual general meeting shall bewithin 15 months of its inauguration.

10. At each annual general meeting, the membersshall elect a chairman, honorary treasurer andhonorary secretary who will resign at thefollowing annual general meeting but be subjectto re-election. Members will also elect the Club's

Investment Club for PDF 4/7/00 4:36 pm Page 24

22

an informative guide to share investment clubs

auditors. If the auditors are members of the Clubthey shall be at least two in number and shall notbe executive officers of the Club.

11. At each annual general meeting, a statement ofaccount shall be given by the treasurer, togetherwith the report of the auditors.The treasurer'sreport shall include a full record of the Club'sincome and expenditure; a list of the Club's assetstogether with its end-of-year valuation; also acapital account for each member showing his/hertotal contributions and withdrawals together withthe current value of his/her holding.

12. Upon the death of any member the value ofhis/her equitable share in the Club shall be paidto the executor of the estate in accordance withthe Club's rules for dealing with a memberleaving the Club.

13. The Club's investment shall be registered througha nominee company provided by a reputablesource such as a bank or stockbroker OR suchinvestments shall be held in the names of trustees,of whom there shall be at least two, who will signa Declaration of Trust and who shall be appointedby a resolution of a majority of Club members.

14. The Club shall open an account with a bank orbuilding society and all club monies shall be paidinto this account except in so far as monies fromdisposal of investments may be retained by theClub's stockbroker pending reinvestment.At leasttwo of the Club's officers or other membersnominated by the Club for this purpose mustsign all cheques and the bank/building societyshall be instructed accordingly.

15. If any member should assign, charge orotherwise encumber his/her share in the Club asprohibited by clause 6 of this agreement, he/sheshall be expelled from the Club. If any membershall become bankrupt, insane or otherwiseincapable of taking part in the club's business,OR shall act in any manner inconsistent withthe good faith observable between members,OR shall be guilty of any conduct which couldinjure the good name of the Club, OR bringabout its dissolution or fail to attend at least 25%of properly constituted meetings in any one

financial year, it shall be lawful for othermembers to notify the offending member inwriting that members shall consider his/herexpulsion from the Club.A member beingissued with such a warning shall be given anopportunity to offer other members anyexplanation as he/she considers desirable.

16. A member shall be expelled if ALL other memberspresent at a properly constituted meeting of theClub support a resolution to that effect.A memberwho is expelled shall be notified in writing andshall have his/her equitable share of the Club assetsreturned in accordance with the rules of the Club.

IN WITNESS whereas the undersigned have set their

hands this _____________________________ day of

_________________________ in the year of 20____

Name Signature

Witnessed by

Investment Club for PDF 4/7/00 4:36 pm Page 25

an informative guide to share investment clubs

23

A Sample AgendaA sample agenda for a normal monthly meeting mightread as follows.

The ______________________________________

Investment Club Meeting to be held at

___________________________________________

at __________________________________ am/pm

____________________________ 20____________

1. Apologies for absence.

2. Minutes of the previous meeting. (The secretarymay read these or, if circulated previously, they may betaken as read and dealt with under item 3.)

3. Matters arising from the previous minutes.

4. Treasurer's report:The treasurer runs through the report alreadycirculated and may comment on changes whichhave taken place since the report was prepared.Details of the report are dealt with in Part Oneunder 'Rules of the Club; 9b'.

5. Investments:Proposals for buying and selling are difficult toseparate as one is often dependent on the other.A good format is for the chairperson to invitemembers' views on each of the currentinvestments in turn, perhaps noting some as apossible sell before going on to proposals forbuying.This item may also include reports whichmembers have been asked to prepare oninvestments discussed at a previous meeting aswell as requests to members to carry out similarinvestigations before the next meeting.

6. Any other Business.

7. Date, time and venue for the next meeting.

Sample Declaration of TrustIf a club decides that its investments, should beregistered in the names of trustees, rather than use anominee company, these trustees should sign aDeclaration of Trust.

A specimen declaration is given below:

THIS DECLARATION OF TRUST

this _______________ day of _________________

in the year of 20_______

By:

who are hereinafter together called the trustees of thetrust hereby constituted.

WHEREAS

A) The _____________________________________

Investment Club (hereinafter called the Club) was formedon the ______________________________________

day of 20________ for the purposes set forth in theconstitution and rules thereof.

B) In accordance with the constitution and rules (acopy of which has been given to each of the trustees)approved by the members on the ________________

day of _____________________________________

20___________ the trustees were appointed for thepurposes and with the powers hereinafter stated.

Investment Club for PDF 4/7/00 4:36 pm Page 26

an informative guide to share investment clubs

24

THIS DEED WITNESSES AS FOLLOWS:1. The trustees hereby declare that they will hold

all investments and property of whatsoever kindwhich are now or may hereinafter be transferredto or vested in them or placed under theircontrol as trustees upon trust for the members ofthe club and that they will obey lawfully writtendirections of the Club with regard to thecustody, control, handling and realising of thesaid investments and property (subject only totheir obligation under the trust hereby declared)and the provisions of the constitution of therules of the Club in so far as applicable to theirduties as trustees and to the trusts thereof.

2. The trustees shall be entitled to assume that anydocument purporting to be signed by suchofficers of the Club, as under the rules areauthorised in that behalf, is in fact a lawfulwritten direction of the Club.

3. In the exercise of the trusts and powers hereof,no trustee shall be liable for any loss arising fromthe negligence or fraud or any agent employedby the trustees or any other trustee hereofalthough the employment of such agents was notstrictly necessary or expedient or by reason ofany mistake or omission made in good faith byany trustee hereof or by reason of any matter orthing except willful fraud or wrongdoing on thepart of the trustee who it is sought to makeliable and the trustees shall be entitled to look atthe members of the Club for an indemnityagainst all costs, damages and expenses incurredby the trustees as a result of any of the causesmentioned in this clause and for all loans andinterest costs and expenses properly incurred bythem in the execution of these trusts.

4. The trustees may when directed by the club inthe manner aforesaid whether by charge on theaforesaid investments or property or by depositthereof raise monies and pay or apply the same asif investments or property of the Club.

5. The trustees hereby declare that they will not bebound by any alteration in the aforesaid rulesunless they and each of them shall have hadnotice in writing from the secretary of the Club.

IN WITNESS whereof the parties hereto havehereunder set their hands and seals the day and theyear of the first before written.

Signed by Trustee

Witnessed by

1.

2.

3.

Investment Club for PDF 4/7/00 4:36 pm Page 27

investment clubs

DES

IGNED

AND P

RODUCE

D B

YTH

E DES

IGN H

OUSE

– T

ELEP

HONE:

(+3

53-1

) 66

0470

0

Investment Club for PDF 4/7/00 4:36 pm Page 28

The Irish Stock Exchange Limited28 Anglesea Street, Dublin 2.

Tel: +353 (1) 617 4200Fax: +353 (1) 677 6045e-mail: [email protected]: www.ise.ie

Investment Club for PDF 4/7/00 4:36 pm Page 29